The 2026 Bankruptcy of Eddie Bauer: A Structural Analysis of Retail Fragmentation, Macroeconomic Volatility, and the Demise of the Traditional Outfitter

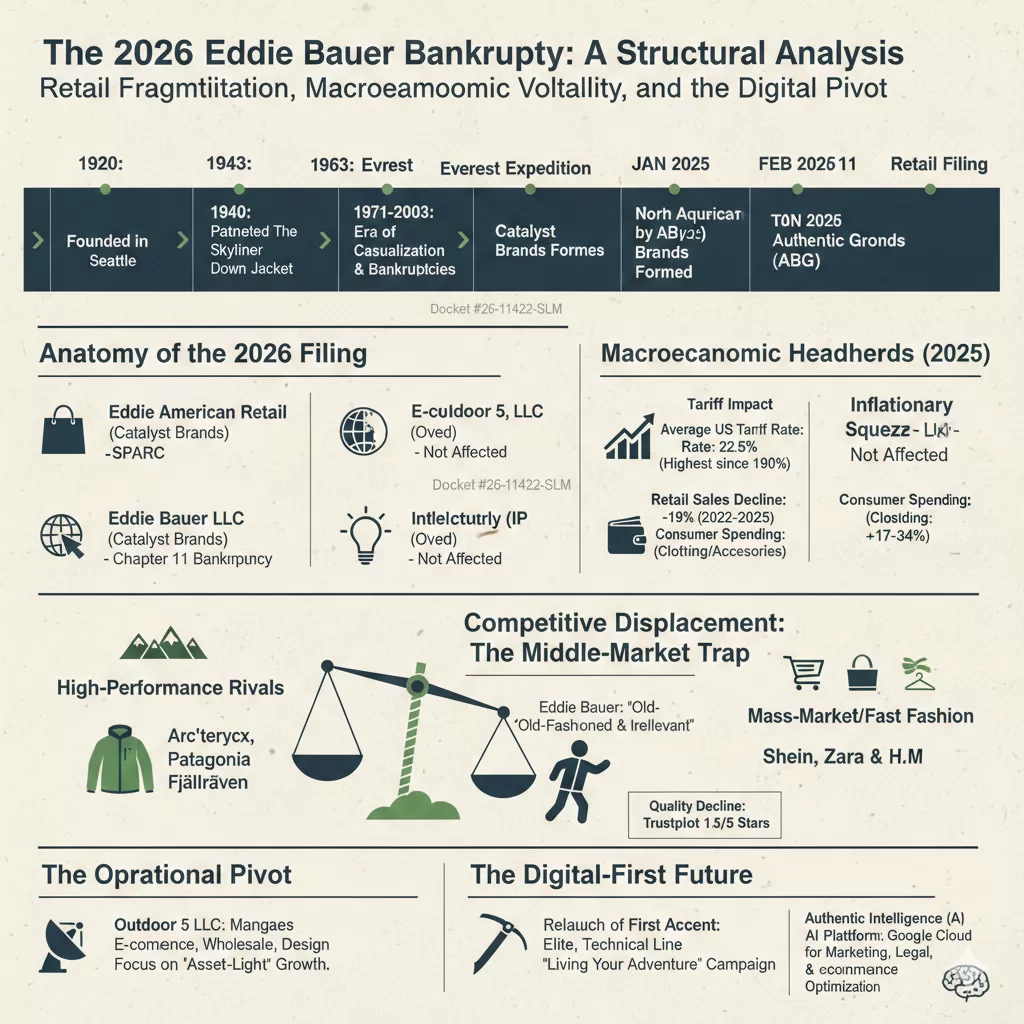

The voluntary filing for Chapter 11 bankruptcy protection by Eddie Bauer LLC on February 9, 2026, represents more than a singular corporate failure; it serves as a definitive case study in the structural fragmentation of legacy retail in the mid-2020s. This move, marking the third time the 106-year-old brand has sought creditor protection in a little over two decades, is the culmination of a sophisticated strategic carve-out executed within the complex ecosystem of modern brand management. While the physical store operations, housed under the Catalyst Brands umbrella, undergo a court-supervised wind-down or potential sale, the brand’s intellectual property, e-commerce, and wholesale divisions have been insulated from the filing. This analysis explores the causal mechanisms behind the 2026 filing, the macroeconomic headwinds of the preceding year, the competitive displacement of the brand, and the bifurcated future of the Eddie Bauer name in a digital-first economy.

The Anatomy of the 2026 Bankruptcy Filing

The filing in the United States Bankruptcy Court for the District of New Jersey under docket #26-11422-SLM specifically targets the retail operator of approximately 180 Eddie Bauer stores across the United States and Canada. The financial distress reported by the company is severe, with court documents indicating liabilities that could range from $1 billion to as high as $10 billion, set against assets valued at only $100 million to $500 million. At the time of the filing, the retail entity faced a critical liquidity crisis, reporting average weekly disbursements of approximately $1.6 million against a cash reserve of only $20 million.

A defining feature of this bankruptcy is its targeted scope. The Chapter 11 proceedings do not include Eddie Bauer’s e-commerce platforms, wholesale operations, manufacturing divisions, or international locations outside of North America. This structural insulation was achieved through a series of tactical transfers occurring just weeks before the filing. In January 2026, Authentic Brands Group (ABG), the owner of the Eddie Bauer intellectual property, transitioned the licenses for e-commerce and wholesale to a separate entity, Outdoor 5 LLC (Oved), effective February 2, 2026. This maneuver effectively separated the profitable digital and wholesale channels from the debt-burdened physical retail footprint, leaving the latter to navigate the bankruptcy process as a standalone entity.

| Operational Segment | Entity Responsible (Feb 2026) | Bankruptcy Status |

| North American Retail Stores | Eddie Bauer LLC (Catalyst Brands) | Chapter 11 Filing |

| E-commerce & Digital Sales | Outdoor 5, LLC (Oved) | Not Affected |

| Wholesale & Manufacturing | Outdoor 5, LLC (Oved) | Not Affected |

| Intellectual Property (IP) | Authentic Brands Group (ABG) | Not Affected |

| International Operations | Various International Licensees | Not Affected |

The retail operator entered into a Restructuring Support Agreement (RSA) with its secured lenders to facilitate what it calls a “dual-path” process. This strategy involves conducting immediate liquidation sales across its North American fleet while simultaneously seeking a “going concern” buyer for the physical store operations. If a suitable buyer is not secured by the court-mandated deadline of March 12, 2026, the company will proceed with an orderly total wind-down of its U.S. and Canadian brick-and-mortar presence by April 30, 2026.

Macroeconomic Catalysts: The 2025 Trade Regime and Inflationary Squeeze

While the internal structural issues of Eddie Bauer were longstanding, the “final blow” came from a series of macroeconomic shocks throughout 2025 that the company’s overleveraged business model could not absorb. CEO Marc Rosen of Catalyst Brands explicitly cited “ongoing tariff uncertainty” and persistent inflation as the primary accelerators of the retailer’s demise.

The 2025 Tariff Impact on the Apparel Sector

The trade environment of 2025 was characterized by aggressive new tariffs that fundamentally altered the cost structure of North American retail. Research from the Yale Budget Lab indicates that the overall average effective U.S. tariff rate reached 22.5 percent in 2025—the highest level recorded since 1909. These tariffs disproportionately targeted categories central to Eddie Bauer’s product mix, including apparel, footwear, and leather products.

| Commodity Category | Short-Run Price Increase (2025) | Long-Run Projected Increase |

| General Apparel | 17.0% – 34.0% | 11.0% – 13.0% |

| Leather Products & Footwear | 36.0% – 37.0% | 12.0% – 13.0% |

| Textiles | 21.0% | 7.0% |

These cost increases were rapidly passed on to consumers, pushing key price thresholds beyond what casual outdoor enthusiasts were willing to pay. For a brand like Eddie Bauer, which operated in the “middle-of-the-road” value segment, the inability to absorb these costs led to a significant collapse in discretionary spending. Data from Earnest Analytics revealed a 3.9 percent year-over-year drop in consumer spending at clothing and accessories establishments in early 2025, making it the worst-performing major retail segment of the year.

Inflationary Pressures and Consumer Sentiment

The residual effects of post-pandemic inflation further squeezed the profit margins of physical retail operations. Eddie Bauer’s retail sales saw a precipitous 19 percent decline between 2022 and 2025, driven by the increased cost of doing business and shifting consumer priorities. A survey conducted by Circana in October 2025 revealed that 38 percent of consumers intended to cut back on spending specifically due to tariff-induced price hikes, with clothing and footwear identified as the primary targets for reduced purchases. The combination of rising labor costs, increased rent in premium mall locations, and the higher cost of imported goods created a “sustained period of negative earnings” that ultimately made the retail entity unsustainable.

The Strategic Formation of Catalyst Brands

The formation of Catalyst Brands in January 2025 was an ambitious attempt to stabilize several struggling heritage labels through the economies of scale. This joint venture was created through the merger of SPARC Group—the operating partner for brands like Aéropostale, Brooks Brothers, Lucky Brand, and Nautica—and JCPenney. The venture brought together a portfolio of six iconic retail banners with combined annual revenue exceeding $9 billion.

The ownership structure of Catalyst Brands reflects a partnership between major mall landlords and brand management firms, including Simon Property Group, Brookfield Corporation, Authentic Brands Group, and Shein. This alliance was designed to leverage a robust distribution network of 1,800 store locations and 60,000 employees, with the hope that shared design, sourcing, and logistics capabilities would drive operational efficiencies.

| Brand | Year Acquired by Catalyst/Predecessor | Original Founding Year |

| Eddie Bauer | 2021 (by SPARC) | 1920 |

| Brooks Brothers | 2020 (by SPARC) | 1818 |

| JCPenney | 2020 (by Simon/Brookfield) | 1902 |

| Nautica | 2018 (by SPARC) | 1983 |

| Aéropostale | 2016 (by SPARC) | 1987 |

| Lucky Brand | 2020 (by SPARC) | 1990 |

Despite having $1 billion in liquidity at its launch, Catalyst Brands inherited a “challenged situation” at Eddie Bauer. Marc Rosen, the CEO of Catalyst Brands, noted that while the leadership team made significant strides in product development and marketing over the first year of the venture, these improvements could not be implemented fast enough to address the structural problems created over several decades. The bankruptcy of the Eddie Bauer retail operator suggests that the “zombie mall store” strategy—where landlords acquire their tenants to maintain occupancy—may have reached its financial limits in the face of the 2025-2026 economic headwinds.

Historical Context: The Erosion of a Technical Identity

The collapse of Eddie Bauer’s retail operations marks a stark departure from the brand’s origins as a premier technical outfitter. Founded by outdoorsman Eddie Bauer in Seattle in 1920, the company was responsible for some of the most significant innovations in outdoor gear of the 20th century.

The Legacy of Innovation (1920–1968)

Eddie Bauer’s early history was defined by a commitment to high-performance products, often developed out of personal necessity. After suffering hypothermia during a winter fishing trip, Bauer sought an alternative to heavy, water-logged wool garments. This led to the 1940 patent of “The Skyliner,” the first quilted goose-down-insulated jacket in the United States. This technical expertise earned the company massive government commissions during World War II, during which it manufactured over 50,000 B-9 Flight Parkas and 100,000 sleeping bags for the military. Notably, Eddie Bauer was the only government supplier granted permission to affix its logo to military-issue products.

This era of technical dominance culminated in the 1963 American Mount Everest Expedition, where Jim Whittaker wore Eddie Bauer gear to become the first American to summit the world’s highest peak. The brand’s creed—”To give you such outstanding quality, value, service and guarantee that we may be worthy of your high esteem”—was established during this period of innovation.

The Shift to Casual Apparel and Serial Ownership (1968–2021)

The retirement of Eddie Bauer in 1968 signaled the beginning of a decades-long transition from technical specialist to casual lifestyle brand. Successive ownership changes each prioritized different financial and market strategies, often at the expense of the brand’s performance-oriented heritage.

- General Mills Era (1971–1988): Under the ownership of the food conglomerate, Eddie Bauer expanded its retail footprint to 60 stores and increasingly focused on casual apparel and home furnishings.

- Spiegel Era (1988–2003): The brand underwent massive expansion but was dragged into bankruptcy along with its parent company in 2003.

- Golden Gate Capital Era (2009–2021): After a second bankruptcy in 2009, private equity firm Golden Gate Capital acquired the brand, often focusing on cost-cutting measures and the expansion of the outlet channel.

By the time Authentic Brands Group acquired the brand in 2021, the product line had become “middle-of-the-road,” struggling to differentiate itself in an increasingly specialized market.

Competitive Displacement: The “Middle-Market Trap”

By 2025, the outdoor apparel market had become highly polarized, with consumers gravitating toward either high-performance specialist brands or trendy, low-cost athleisure. Eddie Bauer found itself caught in a “middle-market trap,” lacking the elite technical credibility of its high-end rivals while being unable to compete on price with mass-market discount retailers.

Technical Rivals and Brand Identity

Competitors such as Arc’teryx, Patagonia, and Fjällräven successfully built distinct identities that resonated with younger, tech-savvy consumers. While Eddie Bauer’s brand name remained well-known, it was increasingly perceived by younger shoppers as “old-fashioned and a bit irrelevant”.

| Brand | Market Positioning | Key Strategy / Point of Difference |

| Arc’teryx | Elite Technical | Focus on alpine performance and “tech-wear” aesthetics |

| Patagonia | Activist / Heritage | Commitment to environmentalism and free lifelong repairs |

| Fjällräven | Trendy / Functional | Distinctive aesthetics and G-1000 material durability |

| Eddie Bauer | Traditional Casual | Reliance on outlets and perpetual 40% off discounting |

The Decline of Quality and Service

A critical factor in Eddie Bauer’s loss of market share was a perceived decline in product quality. For an outdoor brand, whose value is intrinsically tied to the performance of its gear, this deterioration was particularly damaging. Industry analyst Neil Saunders of GlobalData Retail noted that the brand had not kept pace with the innovation cycles of its rivals.

By 2025, consumer sentiment reflected a significant loss of trust. Trustpilot ratings for the brand languished at 1.3 out of 5 stars, with shoppers citing frequent order errors, poor customer service, and materials that were “not like they used to be”. Furthermore, the watering down of the brand’s once-famous lifetime guarantee to a limited return policy in the mid-2010s had eroded a primary pillar of its customer loyalty.

Operational Fragmentation: The Digital Pivot and “Outdoor 5”

The 2026 bankruptcy of the retail operator must be viewed in the context of a broader shift toward an asset-light, digital-first business model. By carving out the profitable e-commerce and wholesale segments, Authentic Brands Group and its partners have essentially insulated the future of the Eddie Bauer brand from the failure of its physical stores.

The Role of Outdoor 5 LLC (Oved)

In January 2026, Outdoor 5 LLC (Oved) assumed responsibility for Eddie Bauer’s e-commerce, wholesale, design, and product development operations across the United States and Canada. Oved, a longtime partner of the brand for over two decades, brings specific expertise in the outdoor and performance apparel space. The company also manages other prominent brands in the Authentic portfolio, including Billabong, Quiksilver, and Hurley.

The strategic goal of this partnership is to align the brand’s channel mix with modern shopping behaviors. Authentic Brands Executive Vice President David Brooks noted that this approach provides the brand with greater flexibility, broader consumer access, and a more capital-efficient path to growth. By focusing on digital and wholesale channels, the brand can maintain its market presence while avoiding the high fixed costs associated with a 180-store physical retail fleet.

The Return of First Ascent

To revitalize the brand’s technical credibility, the new strategy centers on the relaunch of First Ascent, Eddie Bauer’s elite, performance-tested line. Originally developed for elite outdoor pursuits, the First Ascent collection features advanced technical specifications, including:

- Waterproofing and taped seams.

- High breathability and wind resistance.

- 800-fill down insulation.

The Spring 2026 campaign, “Living Your Adventure,” aims to integrate these high-performance features into the core brand offering, appealing to both serious adventurers and everyday outdoor enthusiasts. This return to technical roots is a direct response to the brand dilution that occurred during years of mall-dependent, casual-focused ownership.

Technological Integration: Authentic Intelligence and AI

A key component of the brand’s survival strategy in 2026 is the adoption of cutting-edge technology to drive efficiency and consumer engagement. Authentic Brands Group has partnered with Google Cloud to implement “Authentic Intelligence,” a proprietary AI platform built on Google’s Gemini and Vertex AI infrastructure.

This AI integration is being deployed across the brand’s operational spectrum to “supercharge collaboration and creativity” :

- Marketing & Creative: AI-enhanced ad creative for brands in the portfolio has delivered up to 60 percent higher return on ad spend (ROAS) compared to traditional imagery.

- Business Development: AI agents are used to build comprehensive profiles of potential licensing partners and accelerate lead generation.

- Legal & Licensing: “Authentic Intelligence” assists with the rapid review and analysis of contracts, ensuring accuracy and faster turnaround times.

- Digital Experience: Through a partnership with Pattern Group, the brand is expanding its presence on emerging platforms like TikTok Shop, utilizing AI-powered platforms to optimize conversion at scale.

This digital-first, data-driven approach is intended to provide clearer visibility into supply and demand, improve coordination across licensing partners, and ensure that the brand remains relevant in an environment that moves faster than traditional retail cycles.

Implications for Stakeholders: Landlords, Vendors, and Employees

The bankruptcy and potential wind-down of 180 physical store locations have immediate and severe consequences for the various stakeholders tied to the retail entity.

Landlord Risk and the “Dark Store” Threat

For shopping center owners, the filing by Eddie Bauer LLC creates significant operational and financial disruption. The company’s presence in approximately 180 locations means that landlords must navigate the risk of permanent vacancies. Key concerns for landlords include:

- Lease Uncertainty: The uncertainty regarding whether the company will choose to assume or reject specific leases during the restructuring.

- Co-tenancy Clauses: The closure of a prominent tenant like Eddie Bauer can trigger co-tenancy clauses in the leases of other tenants, allowing them to pay reduced rent or terminate their own leases.

- Administrative Expenses: Landlords may face disruptions in rent payments and challenges regarding the recovery of administrative expenses during the bankruptcy process.

Vendor Exposure and Trade Credit

The fragmented corporate structure of Eddie Bauer creates a complex risk profile for vendors. Because the Chapter 11 filing only involves the store-operator entity, trade creditors must carefully identify which legal entity owes their outstanding invoices. Creditors of the retail operator may find their recoveries limited, as the most valuable assets—the intellectual property and the digital sales platforms—are held by entities not included in the bankruptcy proceedings.

Employee Impact

The potential closure of up to 180 retail locations puts thousands of jobs at risk across North America. While some employees involved in design and e-commerce may be absorbed by Outdoor 5 LLC as they scale their operations, the bulk of the retail staff faces the prospect of permanent displacement if a “going concern” buyer for the physical stores is not found by March 2026.

Conclusion: The Finality of the Mall-Based Era

The 2026 bankruptcy of Eddie Bauer’s retail operator represents the final chapter of the brand’s 106-year relationship with traditional American brick-and-mortar retail. The failure of the physical store model under Catalyst Brands is a clear signal that the combination of heavy debt, mall dependence, and macroeconomic volatility is no longer sustainable for heritage mid-market labels.

While the physical stores are being liquidated, the Eddie Bauer name itself is poised for a digital-first resurrection. The strategic bifurcation of the business—carving out the profitable digital and wholesale pieces while shedding the liabilities of the physical stores—is the new blueprint for legacy brand survival. By returning to its technical roots through the relaunch of First Ascent and leveraging AI-driven efficiencies, the brand owners hope to recapture the technical credibility that was lost during decades of casual-focused expansion. For the broader retail industry, the Eddie Bauer case serves as a cautionary tale: in the economy of the mid-2020s, a storied history and a well-known name are no longer enough to support the high fixed costs of a traditional retail fleet. The future of legacy retail is asset-light, digital-first, and increasingly separated from the physical malls that once defined it.