Business Interruption Insurance

For many small businesses, a temporary closure due to an unforeseen disaster can spell financial ruin. Whether it’s a fire, flood, cyberattack, or pandemic-related shutdown, the inability to operate—especially without a steady stream of revenue—can lead to permanent closure. One solution that is often considered is business interruption insurance.

This form of insurance helps replace lost income and covers operating expenses if your business is forced to shut down temporarily. But is it right for every small business? In this article, we’ll explore the pros and cons of purchasing business interruption insurance, and whether it’s a wise investment or an unnecessary expense.

Table of Contents

- What Is Business Interruption Insurance?

- How It Works

- Common Perils Covered

- What It Typically Doesn’t Cover

- Pros of Business Interruption Insurance

- Income Protection

- Employee Retention

- Business Continuity

- Helps with Loan Repayment

- Protection from Uncontrollable Events

- Cons of Business Interruption Insurance

- High Premium Costs

- Complex Claims Process

- Limited Coverage Scope

- Waiting Periods

- Exclusions in Pandemics and Civil Unrest

- Industry-Specific Considerations

- Case Studies: Success and Failure Stories

- Evaluating Whether Your Business Needs It

- How to Choose a Policy

- Alternatives to Business Interruption Insurance

- Final Thoughts

1. What Is Business Interruption Insurance?

Business interruption insurance, also known as business income insurance, is a type of policy that compensates a business for income lost during events that cause a suspension of operations. It is often part of a Business Owner’s Policy (BOP) or added as a rider to a commercial property policy.

Rather than covering physical damage to property, like traditional insurance, it addresses lost income and operational expenses during downtime.

2. How It Works

Let’s say a restaurant suffers a kitchen fire and must close for three months for repairs. While property insurance may cover the cost of rebuilding, business interruption insurance would cover the revenue the restaurant loses during the closure. It may also cover:

- Rent or lease payments

- Employee wages

- Taxes

- Loan payments

- Relocation expenses (if needed)

Payouts are typically based on historical revenue and expense figures.

3. Common Perils Covered

Policies may vary, but most standard business interruption policies cover income losses resulting from:

- Fire

- Storm damage

- Vandalism

- Equipment failure

- Power outages (under specific conditions)

- Natural disasters (when tied to physical damage)

- Cyberattacks (if specified)

Note that coverage is often triggered only if physical damage occurs that leads to a disruption of operations.

4. What It Typically Doesn’t Cover

Understanding what’s not covered is crucial. Standard exclusions often include:

- Earthquakes and floods (unless separately insured)

- Communicable diseases (e.g., COVID-19) without specific riders

- Power outages not caused by insured damage

- Utility failures off-premises

- Government shutdowns

- Losses due to poor business decisions

Always read the fine print, as each policy varies widely in scope.

5. Pros of Business Interruption Insurance

a. Income Protection

The most obvious advantage is the ability to maintain revenue. For many small businesses with limited cash reserves, one disaster could cause a long-term financial crisis. Business interruption insurance can cover:

- Lost net income

- Operating costs

- Ongoing fixed costs (e.g., rent)

b. Employee Retention

Maintaining payroll during downtime can be difficult. Coverage ensures you can retain skilled staff even when operations are paused. This reduces costly rehiring and retraining when business resumes.

c. Business Continuity

Insurance allows your business to maintain continuity even when faced with catastrophic events. Whether you need to set up a temporary location or invest in new technology post-disaster, the policy may help absorb those costs.

d. Helps with Loan Repayment

Loan obligations don’t disappear during a business interruption. Income coverage can help ensure you stay current with lenders, preserving your credit and business reputation.

e. Protection from Uncontrollable Events

No matter how well a business is managed, disasters can strike without warning. Business interruption insurance provides peace of mind and a financial safety net.

6. Cons of Business Interruption Insurance

a. High Premium Costs

Premiums for business interruption insurance can be significant, especially for businesses in high-risk industries or locations. The cost is typically based on:

- Industry type

- Business location

- Revenue

- Claim history

For cash-strapped small businesses, the cost may outweigh the perceived benefits.

b. Complex Claims Process

Filing a claim isn’t always straightforward. Business owners must:

- Provide extensive financial documentation

- Prove the extent of lost income

- Demonstrate that the event fits within the policy’s parameters

This often requires professional help from accountants or attorneys, adding more costs.

c. Limited Coverage Scope

Many business owners mistakenly believe all disruptions are covered. But many policies only pay out for losses directly tied to physical damage. If your business is closed due to a power grid failure or nearby event (but no property damage), the policy may not apply.

d. Waiting Periods

Policies often include a waiting period—the number of hours or days a business must be closed before coverage begins. If your closure is brief, you may not qualify for reimbursement at all.

e. Exclusions in Pandemics and Civil Unrest

The COVID-19 pandemic revealed a major gap: most insurers excluded communicable diseases. Likewise, business interruptions from protests, curfews, or political unrest may not be covered unless specifically stated in the policy.

7. Industry-Specific Considerations

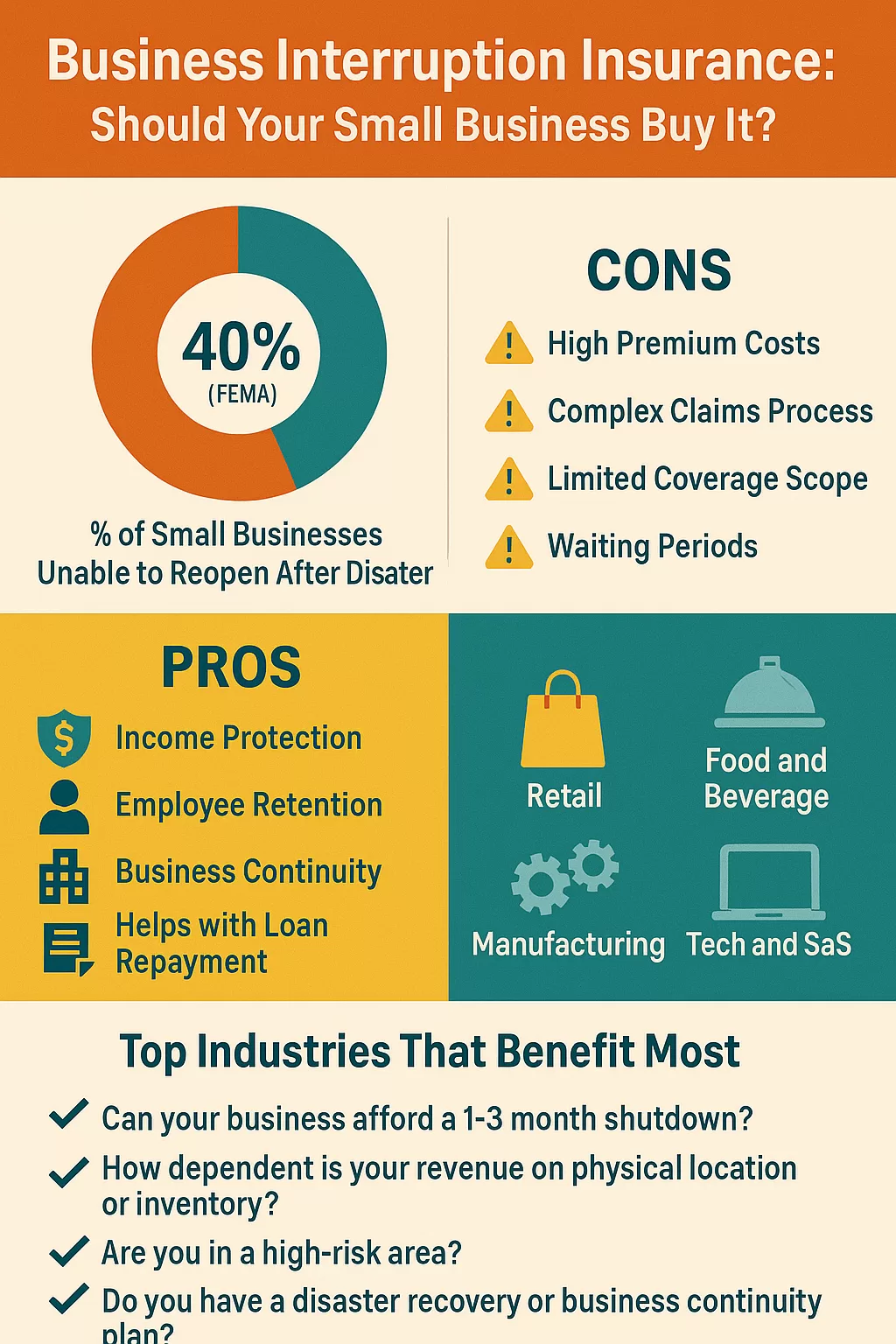

Retail

Retailers reliant on foot traffic and perishable goods benefit most. A temporary closure could mean complete inventory loss and customer defection.

Food and Beverage

Restaurants are particularly vulnerable to fires, health-code closures, and utility disruptions. Business interruption insurance can be vital.

Tech and SaaS

While these businesses may not suffer from physical damage, they may be impacted by cyberattacks or server failures. Many standard policies don’t cover these events.

Manufacturing

A broken supply chain or equipment failure can grind production to a halt. Business interruption insurance helps keep contracts and payroll on track.

8. Case Studies: Success and Failure Stories

Case 1: Bakery Fire Recovery

A family-owned bakery in New Jersey suffered a severe fire and had to close for five months. Thanks to business interruption insurance, they covered wages, relocated temporarily, and resumed operations without losing market share.

Case 2: COVID-19 Denials

Thousands of small businesses filed claims due to pandemic-related closures. Most were denied, as communicable disease exclusions applied. A well-known Chicago restaurant sued their insurer but lost in court, highlighting a significant gap in coverage.

Case 3: Flood Exclusion

A furniture retailer in Houston shut down for two months after a flood. Despite having business interruption insurance, they received no payout—flood damage was excluded unless separately insured.

9. Evaluating Whether Your Business Needs It

Here are some questions to guide your decision:

- Can your business afford to shut down for 1–3 months with no income?

- How dependent is your revenue on physical location or inventory?

- Do you have a disaster recovery or business continuity plan?

- Are you in a high-risk area (storms, floods, crime)?

- Do you have access to emergency funding or credit lines?

If your answer to several of these is “no,” you may want to consider coverage.

10. How to Choose a Policy

a. Assess Risk Exposure

Conduct a risk analysis based on your industry, location, and operations. Identify the most likely threats and their potential cost.

b. Understand Coverage Options

Look for:

- Named perils vs. all-risk coverage

- Inclusion of extra expenses

- Optional riders for cyber events, civil unrest, or pandemics

- Time limits and maximum benefit caps

c. Work with a Knowledgeable Agent

A specialized commercial insurance broker can help tailor the policy to your business’s needs and ensure you understand all exclusions and fine print.

d. Review Regularly

Your business will evolve. So should your insurance. Reassess annually to ensure your policy still fits your current situation.

11. Alternatives to Business Interruption Insurance

If coverage feels too expensive or limited, consider:

Emergency Savings Fund

Set aside 3–6 months of operating expenses in a liquid account.

SBA Disaster Loans

The U.S. Small Business Administration offers low-interest disaster loans for qualified businesses.

Line of Credit

Maintain an open line of credit for emergency cash flow.

Self-Insuring

Larger or more financially stable businesses may opt to absorb potential losses themselves.

12. Final Thoughts

Business interruption insurance is not a one-size-fits-all solution. For some small businesses, especially those in disaster-prone areas or industries reliant on physical assets, it may be a lifeline. For others, the cost, exclusions, and complexity may outweigh the benefits.

Ultimately, the decision comes down to your business’s risk tolerance, cash reserves, and reliance on uninterrupted operations. Whether or not you purchase a policy, having a robust business continuity plan is essential.

Infographic Suggestion (for Visual Use):

Title: Business Interruption Insurance: Should Your Small Business Buy It?

Sections:

- Pie chart: % of small businesses unable to reopen after disaster (FEMA stat: 40%)

- Pros list (with icons)

- Cons list (with warning signs)

- Top industries that benefit most

- Checklist: “Is It Right For You?”