The 2026 Bankruptcy of Eddie Bauer: A Structural Analysis of Retail Fragmentation, Macroeconomic Volatility, and the Demise of the Traditional Outfitter

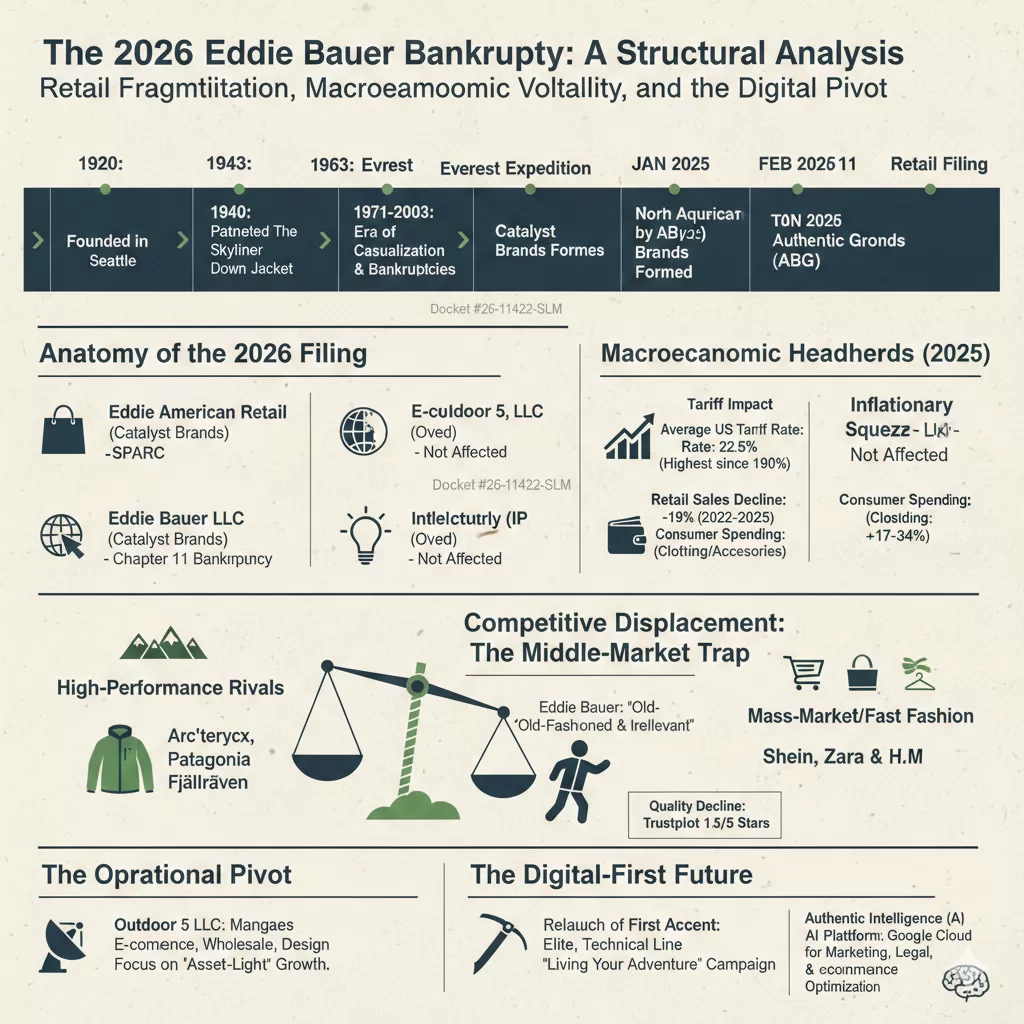

The voluntary filing for Chapter 11 bankruptcy protection by Eddie Bauer LLC on February 9, 2026, represents more than a singular corporate failure; it serves as a definitive case study in the structural fragmentation of legacy retail in the mid-2020s. This move, marking the third time the 106-year-old brand has sought creditor protection in a little over two decades, is the culmination of a sophisticated strategic carve-out executed within the complex ecosystem of modern brand management. While the physical store operations, housed under the Catalyst Brands umbrella, undergo a court-supervised wind-down or potential sale, the brand’s intellectual property, e-commerce, and wholesale divisions have been insulated from the filing. This analysis explores the causal mechanisms behind the 2026 filing, the macroeconomic headwinds of the preceding year, the competitive displacement of the brand, and the bifurcated future of the Eddie Bauer name in a digital-first economy.

The Anatomy of the 2026 Bankruptcy Filing

The filing in the United States Bankruptcy Court for the District of New Jersey under docket #26-11422-SLM specifically targets the retail operator of approximately 180 Eddie Bauer stores across the United States and Canada. The financial distress reported by the company is severe, with court documents indicating liabilities that could range from $1 billion to as high as $10 billion, set against assets valued at only $100 million to $500 million. At the time of the filing, the retail entity faced a critical liquidity crisis, reporting average weekly disbursements of approximately $1.6 million against a cash reserve of only $20 million.

A defining feature of this bankruptcy is its targeted scope. The Chapter 11 proceedings do not include Eddie Bauer’s e-commerce platforms, wholesale operations, manufacturing divisions, or international locations outside of North America. This structural insulation was achieved through a series of tactical transfers occurring just weeks before the filing. In January 2026, Authentic Brands Group (ABG), the owner of the Eddie Bauer intellectual property, transitioned the licenses for e-commerce and wholesale to a separate entity, Outdoor 5 LLC (Oved), effective February 2, 2026. This maneuver effectively separated the profitable digital and wholesale channels from the debt-burdened physical retail footprint, leaving the latter to navigate the bankruptcy process as a standalone entity.

Operational Segment

Entity Responsible (Feb 2026)

Bankruptcy Status

North American Retail Stores

Eddie Bauer LLC (Catalyst Brands)

Chapter 11 Filing

E-commerce & Digital Sales

Outdoor 5, LLC (Oved)

Not Affected

Wholesale & Manufacturing

Outdoor 5, LLC (Oved)

Not Affected

Intellectual Property (IP)

Authentic Brands Group (ABG)

Not Affected

International Operations

Various International Licensees

Not Affected

The retail operator entered into a Restructuring Support Agreement (RSA) with its secured lenders to facilitate what it calls a “dual-path” process. This strategy involves conducting immediate liquidation sales across its North American fleet while simultaneously seeking a “going concern” buyer for the physical store operations. If a suitable buyer is not secured by the court-mandated deadline of March 12, 2026, the company will proceed with an orderly total wind-down of its U.S. and Canadian brick-and-mortar presence by April 30, 2026.

Macroeconomic Catalysts: The 2025 Trade Regime and Inflationary Squeeze

While the internal structural issues of Eddie Bauer were longstanding, the “final blow” came from a series of macroeconomic shocks throughout 2025 that the company’s overleveraged business model could not absorb. CEO Marc Rosen of Catalyst Brands explicitly cited “ongoing tariff uncertainty” and persistent inflation as the primary accelerators of the retailer’s demise.

The 2025 Tariff Impact on the Apparel Sector

The trade environment of 2025 was characterized by aggressive new tariffs that fundamentally altered the cost structure of North American retail. Research from the Yale Budget Lab indicates that the overall average effective U.S. tariff rate reached 22.5 percent in 2025—the highest level recorded since 1909. These tariffs disproportionately targeted categories central to Eddie Bauer’s product mix, including apparel, footwear, and leather products.

Commodity Category

Short-Run Price Increase (2025)

Long-Run Projected Increase

General Apparel

17.0% – 34.0%

11.0% – 13.0%

Leather Products & Footwear

36.0% – 37.0%

12.0% – 13.0%

Textiles

21.0%

7.0%

These cost increases were rapidly passed on to consumers, pushing key price thresholds beyond what casual outdoor enthusiasts were willing to pay. For a brand like Eddie Bauer, which operated in the “middle-of-the-road” value segment, the inability to absorb these costs led to a significant collapse in discretionary spending. Data from Earnest Analytics revealed a 3.9 percent year-over-year drop in consumer spending at clothing and accessories establishments in early 2025, making it the worst-performing major retail segment of the year.

Inflationary Pressures and Consumer Sentiment

The residual effects of post-pandemic inflation further squeezed the profit margins of physical retail operations. Eddie Bauer’s retail sales saw a precipitous 19 percent decline between 2022 and 2025, driven by the increased cost of doing business and shifting consumer priorities. A survey conducted by Circana in October 2025 revealed that 38 percent of consumers intended to cut back on spending specifically due to tariff-induced price hikes, with clothing and footwear identified as the primary targets for reduced purchases. The combination of rising labor costs, increased rent in premium mall locations, and the higher cost of imported goods created a “sustained period of negative earnings” that ultimately made the retail entity unsustainable.

The Strategic Formation of Catalyst Brands

The formation of Catalyst Brands in January 2025 was an ambitious attempt to stabilize several struggling heritage labels through the economies of scale. This joint venture was created through the merger of SPARC Group—the operating partner for brands like Aéropostale, Brooks Brothers, Lucky Brand, and Nautica—and JCPenney. The venture brought together a portfolio of six iconic retail banners with combined annual revenue exceeding $9 billion.

The ownership structure of Catalyst Brands reflects a partnership between major mall landlords and brand management firms, including Simon Property Group, Brookfield Corporation, Authentic Brands Group, and Shein. This alliance was designed to leverage a robust distribution network of 1,800 store locations and 60,000 employees, with the hope that shared design, sourcing, and logistics capabilities would drive operational efficiencies.

Brand

Year Acquired by Catalyst/Predecessor

Original Founding Year

Eddie Bauer

2021 (by SPARC)

1920

Brooks Brothers

2020 (by SPARC)

1818

JCPenney

2020 (by Simon/Brookfield)

1902

Nautica

2018 (by SPARC)

1983

Aéropostale

2016 (by SPARC)

1987

Lucky Brand

2020 (by SPARC)

1990

Despite having $1 billion in liquidity at its launch, Catalyst Brands inherited a “challenged situation” at Eddie Bauer. Marc Rosen, the CEO of Catalyst Brands, noted that while the leadership team made significant strides in product development and marketing over the first year of the venture, these improvements could not be implemented fast enough to address the structural problems created over several decades. The bankruptcy of the Eddie Bauer retail operator suggests that the “zombie mall store” strategy—where landlords acquire their tenants to maintain occupancy—may have reached its financial limits in the face of the 2025-2026 economic headwinds.

Historical Context: The Erosion of a Technical Identity

The collapse of Eddie Bauer’s retail operations marks a stark departure from the brand’s origins as a premier technical outfitter. Founded by outdoorsman Eddie Bauer in Seattle in 1920, the company was responsible for some of the most significant innovations in outdoor gear of the 20th century.

The Legacy of Innovation (1920–1968)

Eddie Bauer’s early history was defined by a commitment to high-performance products, often developed out of personal necessity. After suffering hypothermia during a winter fishing trip, Bauer sought an alternative to heavy, water-logged wool garments. This led to the 1940 patent of “The Skyliner,” the first quilted goose-down-insulated jacket in the United States. This technical expertise earned the company massive government commissions during World War II, during which it manufactured over 50,000 B-9 Flight Parkas and 100,000 sleeping bags for the military. Notably, Eddie Bauer was the only government supplier granted permission to affix its logo to military-issue products.

This era of technical dominance culminated in the 1963 American Mount Everest Expedition, where Jim Whittaker wore Eddie Bauer gear to become the first American to summit the world’s highest peak. The brand’s creed—”To give you such outstanding quality, value, service and guarantee that we may be worthy of your high esteem”—was established during this period of innovation.

The Shift to Casual Apparel and Serial Ownership (1968–2021)

The retirement of Eddie Bauer in 1968 signaled the beginning of a decades-long transition from technical specialist to casual lifestyle brand. Successive ownership changes each prioritized different financial and market strategies, often at the expense of the brand’s performance-oriented heritage.

General Mills Era (1971–1988): Under the ownership of the food conglomerate, Eddie Bauer expanded its retail footprint to 60 stores and increasingly focused on casual apparel and home furnishings.

Spiegel Era (1988–2003): The brand underwent massive expansion but was dragged into bankruptcy along with its parent company in 2003.

Golden Gate Capital Era (2009–2021): After a second bankruptcy in 2009, private equity firm Golden Gate Capital acquired the brand, often focusing on cost-cutting measures and the expansion of the outlet channel.

By the time Authentic Brands Group acquired the brand in 2021, the product line had become “middle-of-the-road,” struggling to differentiate itself in an increasingly specialized market.

Competitive Displacement: The “Middle-Market Trap”

By 2025, the outdoor apparel market had become highly polarized, with consumers gravitating toward either high-performance specialist brands or trendy, low-cost athleisure. Eddie Bauer found itself caught in a “middle-market trap,” lacking the elite technical credibility of its high-end rivals while being unable to compete on price with mass-market discount retailers.

Technical Rivals and Brand Identity

Competitors such as Arc’teryx, Patagonia, and Fjällräven successfully built distinct identities that resonated with younger, tech-savvy consumers. While Eddie Bauer’s brand name remained well-known, it was increasingly perceived by younger shoppers as “old-fashioned and a bit irrelevant”.

Brand

Market Positioning

Key Strategy / Point of Difference

Arc’teryx

Elite Technical

Focus on alpine performance and “tech-wear” aesthetics

Patagonia

Activist / Heritage

Commitment to environmentalism and free lifelong repairs

Fjällräven

Trendy / Functional

Distinctive aesthetics and G-1000 material durability

Eddie Bauer

Traditional Casual

Reliance on outlets and perpetual 40% off discounting

The Decline of Quality and Service

A critical factor in Eddie Bauer’s loss of market share was a perceived decline in product quality. For an outdoor brand, whose value is intrinsically tied to the performance of its gear, this deterioration was particularly damaging. Industry analyst Neil Saunders of GlobalData Retail noted that the brand had not kept pace with the innovation cycles of its rivals.

By 2025, consumer sentiment reflected a significant loss of trust. Trustpilot ratings for the brand languished at 1.3 out of 5 stars, with shoppers citing frequent order errors, poor customer service, and materials that were “not like they used to be”. Furthermore, the watering down of the brand’s once-famous lifetime guarantee to a limited return policy in the mid-2010s had eroded a primary pillar of its customer loyalty.

Operational Fragmentation: The Digital Pivot and “Outdoor 5”

The 2026 bankruptcy of the retail operator must be viewed in the context of a broader shift toward an asset-light, digital-first business model. By carving out the profitable e-commerce and wholesale segments, Authentic Brands Group and its partners have essentially insulated the future of the Eddie Bauer brand from the failure of its physical stores.

The Role of Outdoor 5 LLC (Oved)

In January 2026, Outdoor 5 LLC (Oved) assumed responsibility for Eddie Bauer’s e-commerce, wholesale, design, and product development operations across the United States and Canada. Oved, a longtime partner of the brand for over two decades, brings specific expertise in the outdoor and performance apparel space. The company also manages other prominent brands in the Authentic portfolio, including Billabong, Quiksilver, and Hurley.

The strategic goal of this partnership is to align the brand’s channel mix with modern shopping behaviors. Authentic Brands Executive Vice President David Brooks noted that this approach provides the brand with greater flexibility, broader consumer access, and a more capital-efficient path to growth. By focusing on digital and wholesale channels, the brand can maintain its market presence while avoiding the high fixed costs associated with a 180-store physical retail fleet.

The Return of First Ascent

To revitalize the brand’s technical credibility, the new strategy centers on the relaunch of First Ascent, Eddie Bauer’s elite, performance-tested line. Originally developed for elite outdoor pursuits, the First Ascent collection features advanced technical specifications, including:

Waterproofing and taped seams.

High breathability and wind resistance.

800-fill down insulation.

The Spring 2026 campaign, “Living Your Adventure,” aims to integrate these high-performance features into the core brand offering, appealing to both serious adventurers and everyday outdoor enthusiasts. This return to technical roots is a direct response to the brand dilution that occurred during years of mall-dependent, casual-focused ownership.

Technological Integration: Authentic Intelligence and AI

A key component of the brand’s survival strategy in 2026 is the adoption of cutting-edge technology to drive efficiency and consumer engagement. Authentic Brands Group has partnered with Google Cloud to implement “Authentic Intelligence,” a proprietary AI platform built on Google’s Gemini and Vertex AI infrastructure.

This AI integration is being deployed across the brand’s operational spectrum to “supercharge collaboration and creativity” :

Marketing & Creative: AI-enhanced ad creative for brands in the portfolio has delivered up to 60 percent higher return on ad spend (ROAS) compared to traditional imagery.

Business Development: AI agents are used to build comprehensive profiles of potential licensing partners and accelerate lead generation.

Legal & Licensing: “Authentic Intelligence” assists with the rapid review and analysis of contracts, ensuring accuracy and faster turnaround times.

Digital Experience: Through a partnership with Pattern Group, the brand is expanding its presence on emerging platforms like TikTok Shop, utilizing AI-powered platforms to optimize conversion at scale.

This digital-first, data-driven approach is intended to provide clearer visibility into supply and demand, improve coordination across licensing partners, and ensure that the brand remains relevant in an environment that moves faster than traditional retail cycles.

Implications for Stakeholders: Landlords, Vendors, and Employees

The bankruptcy and potential wind-down of 180 physical store locations have immediate and severe consequences for the various stakeholders tied to the retail entity.

Landlord Risk and the “Dark Store” Threat

For shopping center owners, the filing by Eddie Bauer LLC creates significant operational and financial disruption. The company’s presence in approximately 180 locations means that landlords must navigate the risk of permanent vacancies. Key concerns for landlords include:

Lease Uncertainty: The uncertainty regarding whether the company will choose to assume or reject specific leases during the restructuring.

Co-tenancy Clauses: The closure of a prominent tenant like Eddie Bauer can trigger co-tenancy clauses in the leases of other tenants, allowing them to pay reduced rent or terminate their own leases.

Administrative Expenses: Landlords may face disruptions in rent payments and challenges regarding the recovery of administrative expenses during the bankruptcy process.

Vendor Exposure and Trade Credit

The fragmented corporate structure of Eddie Bauer creates a complex risk profile for vendors. Because the Chapter 11 filing only involves the store-operator entity, trade creditors must carefully identify which legal entity owes their outstanding invoices. Creditors of the retail operator may find their recoveries limited, as the most valuable assets—the intellectual property and the digital sales platforms—are held by entities not included in the bankruptcy proceedings.

Employee Impact

The potential closure of up to 180 retail locations puts thousands of jobs at risk across North America. While some employees involved in design and e-commerce may be absorbed by Outdoor 5 LLC as they scale their operations, the bulk of the retail staff faces the prospect of permanent displacement if a “going concern” buyer for the physical stores is not found by March 2026.

Conclusion: The Finality of the Mall-Based Era

The 2026 bankruptcy of Eddie Bauer’s retail operator represents the final chapter of the brand’s 106-year relationship with traditional American brick-and-mortar retail. The failure of the physical store model under Catalyst Brands is a clear signal that the combination of heavy debt, mall dependence, and macroeconomic volatility is no longer sustainable for heritage mid-market labels.

While the physical stores are being liquidated, the Eddie Bauer name itself is poised for a digital-first resurrection. The strategic bifurcation of the business—carving out the profitable digital and wholesale pieces while shedding the liabilities of the physical stores—is the new blueprint for legacy brand survival. By returning to its technical roots through the relaunch of First Ascent and leveraging AI-driven efficiencies, the brand owners hope to recapture the technical credibility that was lost during decades of casual-focused expansion. For the broader retail industry, the Eddie Bauer case serves as a cautionary tale: in the economy of the mid-2020s, a storied history and a well-known name are no longer enough to support the high fixed costs of a traditional retail fleet. The future of legacy retail is asset-light, digital-first, and increasingly separated from the physical malls that once defined it.

Del Monte Foods, a name synonymous with canned fruits and vegetables for generations, filed for Chapter 11 bankruptcy protection on July 1, 2025. This pivotal event marks a significant moment for one of America’s most recognizable packaged food brands, underscoring the profound challenges faced by legacy companies in a rapidly evolving consumer and economic landscape. The bankruptcy filing, characterized by the company as a strategic maneuver for restructuring and sale, was the culmination of a complex interplay of historical financial decisions, shifting market dynamics, and external macroeconomic pressures.

This report delves into the intricate factors that led to Del Monte Foods’ financial distress and eventual bankruptcy. It traces the company’s storied history, analyzes the impact of successive leveraged acquisitions, dissects the erosion of its financial performance, explores the fundamental shifts in consumer preferences away from its core products, and examines the external economic and geopolitical forces that exacerbated its vulnerabilities. By understanding these multifaceted elements, a clearer picture emerges of how a century-old titan of the food industry reached a critical turning point.

A Legacy Forged in Cans: Del Monte Historical Evolution (1880s – 2010s)

Del Monte’s journey from a nascent Californian canning operation to a global brand is a testament to its early innovation and market dominance. However, this long history also reveals a strategic trajectory that, over time, positioned the company precariously against emerging market forces.

Founding and Early Dominance in California Canning

The origins of Del Monte Foods are deeply rooted in the vibrant, albeit tumultuous, Californian canning industry of the late 19th century. Hundreds of small packers emerged across the state during this period, capitalizing on California’s burgeoning agricultural output. The broader American economy of the 1890s, marked by industrialization, also brought significant upheaval to sectors including food production.

The “Del Monte” name itself predates the formal company, originating in the 1880s. An Oakland, California, food distributor first used the moniker to market a premium coffee blend specifically prepared for the esteemed Hotel Del Monte on the Monterey Peninsula. The brand’s success quickly led to its expansion, and by 1892, “Del Monte” was chosen as the brand name for a new line of canned peaches. This early adoption of a premium brand identity laid the groundwork for its future market position.

A significant consolidation in the West Coast canning industry occurred in 1898 with the formation of the California Fruit Canners Association (CFCA), a merger of 18 canning companies. The Del Monte brand was one of several under the new company’s umbrella. The iconic Del Monte Shield, with its distinctive red and old English lettering, was introduced in 1909 and applied exclusively to their premier products. By 1915, the brand’s prominence was undeniable: despite Calpak offering 72 other “leading” brands, fifty products were sold under the Del Monte shield, signifying its growing recognition and trust among consumers.

The California Packing Corporation (Calpak) Era and Brand Building

Further industry consolidation marked a pivotal moment in 1916 with the formation of the California Packing Corporation, widely known as Calpak. This major merger, led by George Newell Armsby, brought together CFCA, Alaska Packers Association, Central California Canneries, and Griffin & Skelley, a food brokerage house. This strategic integration extended beyond canning, encompassing control over drying and packing houses, the brokers who sold these products, and even the farmers who grew them, creating a formidable vertically integrated enterprise.

Calpak began marketing its products under both the Del Monte and Sunkist brands. A groundbreaking marketing campaign commenced on April 21, 1917, with a full-page advertisement in the Saturday Evening Post simply stating, “California’s finest fruits and vegetables are packed under the Del Monte brand”. This initiative was instrumental in boosting brand recognition nationwide, establishing the Del Monte shield as a guarantee of “value” and “extra quality”.

The phenomenal success of new products, such as the Del Monte Pineapple-Grapefruit drink introduced in 1956, spurred further diversification into beverages and snack foods. Calpak established a research facility in Walnut Creek, California, which actively developed new product lines and brand names, including Granny Goose “fun foods” and “Pudding Cups”. By June 1967, the multinational scope of its operations rendered the name “California Packing Corporation” obsolete, leading to its official renaming as Del Monte Corporation, leveraging the strength of its leading brand.

Diversification, Acquisitions, and Divestitures (1970s-2000s) Del Monte

Del Monte Corporation continued to evolve, demonstrating an early commitment to consumer information by becoming the first major U.S. food processor to voluntarily adopt nutritional labeling on all its products in 1972. However, the late 20th and early 21st centuries saw the company undergo a series of complex ownership changes and strategic divestitures that significantly reshaped its portfolio.

In 1979, Del Monte became part of R.J. Reynolds Industries, Inc., which later became RJR Nabisco, Inc.. Following Kohlberg Kravis Roberts’ (KKR) acquisition of RJR Nabisco in 1988, several Del Monte divisions were sold off. Notably, the fresh fruit business was divested to Polly Peck, while RJR Nabisco retained Del Monte Canada and Venezuela. The core food processing divisions, now known as Del Monte Foods, were subsequently sold in 1989 to a consortium including Merrill Lynch, Citicorp Venture Capital, and Kikkoman, with Kikkoman separately acquiring the Del Monte brand rights in Asia (excluding specific regions). T

Despite these divestitures, Del Monte Foods re-engaged in acquisitions in the late 1990s and early 2000s, acquiring Contadina (1997), reacquiring Del Monte Venezuela (1998), and securing worldwide rights to the SunFresh (2000) and S&W (2001) brands. A major expansion occurred in 2002 with the purchase of several brands from Heinz, nearly tripling Del Monte Foods’ size. The company also diversified into pet food, acquiring Meow Mix (2006) and Milk-Bone (2006), becoming the second-largest pet food company.

Del Monte Foods briefly returned to being a publicly traded company in 1999, but its stock was delisted from the NYSE in March 2011 following a leveraged buyout.

The Distinction: Del Monte Foods vs. Fresh Del Monte Produce

A crucial element in understanding Del Monte’s recent financial struggles is the clear distinction between Del Monte Foods and Fresh Del Monte Produce. In 1989, the original Del Monte Corporation underwent a significant organizational split, dividing into two separate entities: Del Monte Tropical Fruit and Del Monte Foods.

Del Monte Tropical Fruit subsequently rebranded as Fresh Del Monte Produce N.V. in 1993. This entity operates as a leading vertically integrated producer, marketer, and distributor of high-quality fresh and fresh-cut fruits and vegetables globally. Its financial performance, as reflected in various reports, has generally been stable and often profitable, with notable growth in fresh and value-added products such such as pineapples and avocados. This entity is explicitly identified as a “separate company” that “remains stable”.

In contrast, Del Monte Foods, the entity that ultimately filed for bankruptcy, primarily focuses on canned fruits and vegetables, alongside other brands like Contadina (tomato products), College Inn and Kitchen Basics (broth), and Joyba (bubble tea). This distinction is paramount, as the financial woes and the recent bankruptcy filing pertain specifically to the U.S.-based Del Monte Foods, not the fresh produce arm. The separate financial health of Fresh Del Monte Produce should not be conflated with the challenges faced by the canned goods business.

The strategic divestiture of the fresh produce business in 1988 , and later the StarKist seafood division in 2008, was intended to allow Del Monte Foods to concentrate on pet food and “higher-margin produce”. The pet food division was also spun off in 2014. This series of divestitures, particularly the shedding of the fresh produce segment, meant that Del Monte Foods, the entity that filed for bankruptcy, progressively narrowed its focus to its “signature canned products”. This strategic narrowing left the company with a core business inherently more vulnerable to subsequent market shifts in consumer preferences.

Furthermore, the complex history of numerous ownership changes, mergers, acquisitions, and significant divestitures has led to a fragmentation of the singular “Del Monte” brand identity in the consumer’s mind. While the organizational separation into Del Monte Foods and Fresh Del Monte Produce might have been a logical business decision, it likely resulted in consumers primarily associating the “Del Monte” brand with its historical, less desirable canned goods. This perception overshadowed any innovations or healthier offerings from the separate fresh produce entity.

The Weight of Leverage: Debt Accumulation and Financial Engineering at Del Monte

A primary driver of Del Monte Foods’ bankruptcy was the substantial debt burden accumulated through a series of leveraged acquisitions and subsequent financial maneuvers. These decisions severely constrained the company’s financial flexibility and ability to invest in necessary adaptations.

The 2011 Leveraged Buyout (LBO) by KKR and Partners

A significant financial turning point for Del Monte Foods was its acquisition on March 8, 2011, by an investor group spearheaded by Kohlberg Kravis Roberts & Co. L.P. (KKR), Vestar Capital Partners, and Centerview Capital, L.P.. This leveraged buyout (LBO) valued the company at approximately $5.3 billion, with stockholders receiving $19.00 per share in cash.

A critical aspect of this transaction was the assumption of approximately $1.3 billion in existing net debt. In addition, the LBO was heavily financed with new debt, including a $2.7 billion term loan, $1.3 billion in new senior notes (which were intended to replace an up-to-$1.6 billion unsecured bridge loan), and a $500 million revolving credit facility. The Sponsors themselves contributed $1.7 billion in equity. Following the completion of the acquisition, Del Monte’s common stock ceased trading on the New York Stock Exchange on March 9, 2011, as the company transitioned to private ownership.

The 2011 LBO, while a common private equity strategy, burdened Del Monte Foods with a substantial debt load exceeding $4 billion. This massive leverage immediately made the company highly susceptible to any adverse market conditions, economic downturns, or shifts in consumer preferences. Such a heavy debt burden drastically limited the company’s financial flexibility, constraining the capital available for crucial investments in innovation, marketing, or adapting its product portfolio to future trends.

Furthermore, legal proceedings surrounding the 2011 LBO brought to light potential conflicts of interest. Barclays, an investment bank advising Del Monte’s board, also sought a role in providing buyer-side financing. The court deemed this “appearance of conflict” to be “unreasonable” and noted that Barclays’ “active concealment of Vestar’s role in the process” “materially reduced the prospect of price competition for Del Monte”. This suggests that the LBO, despite board approval, might not have secured the absolute best possible terms for Del Monte’s shareholders, potentially resulting in a lower sale price than could have been achieved in a truly competitive process.

Del Monte Pacific’s 2014 Acquisition: A “Catastrophic Gamble”

The financial burden on Del Monte Foods was further compounded in February 2014 when Philippines-based Del Monte Pacific Limited (DMPL) acquired Del Monte Foods’ consumer food business for US$1.675 billion. This acquisition, too, was heavily financed with debt, including a bridge loan of $350 million and a term loan of $165 million, totaling $515 million. DMPL also aimed to raise an additional $150 million through a share placement.

For DMPL, this acquisition, initially hailed as a “transformational move,” ultimately proved to be a “catastrophic gamble”. It was “financed heavily with debt and never integrated profitably into the broader group”. As of January 31, 2025, DMPL’s net investment in Del Monte Foods Holdings Ltd (DMFHL), the U.S. subsidiary, stood at US

579million,withanadditionalUS169 million in net receivables from DMFHL and its units, bringing DMPL’s total exposure to a staggering US$748 million. This exposure was nearly nine times DMPL’s market capitalization as of July 4, 2025.

The 2014 acquisition by DMPL layered additional, significant debt onto a company already struggling under the weight of the 2011 LBO. DMPL’s financing of this acquisition with over half a billion dollars in new loans demonstrates a continuation of the highly leveraged financial strategy. While DMPL may have acquired Del Monte Foods at a “reasonable price” , the underlying financial fragility of the target company, coupled with the “fading” consumer taste for canned goods , meant that even a seemingly good deal on valuation could not prevent a deepening of the “debt trap”.

Escalating Interest Expenses Del Monte

The cumulative effect of these debt-heavy transactions was a dramatic increase in Del Monte Foods’ financial obligations. By 2025, the company’s annual interest payments had ballooned to 125million,nearly double what they were in 2020.

The dramatic increase in annual interest payments represents a direct and substantial drain on Del Monte Foods’ operational cash flow. This financial constraint meant that capital that could have been reinvested in crucial areas like product innovation, aggressive marketing campaigns to counter changing consumer trends, or supply chain efficiencies was instead diverted to debt servicing. This created a vicious cycle: high debt limited the company’s ability to adapt and innovate, leading to declining sales and profitability, which in turn made the existing debt burden even harder to service and further restricted future strategic investments.

The following table summarizes the major debt events that contributed to Del Monte Foods’ financial fragility:

Year

Event

Key Debt Figures (USD)

2011

KKR Leveraged Buyout (LBO)

Total Enterprise Value: $5.3B; Assumed Net Debt: $1.3B; New Term Loan: $2.7B; New Senior Notes: $1.3B; Revolving Credit: $500M; Equity Contribution: $1.7B

2014

Del Monte Pacific (DMPL) Acquisition

Acquisition Price: $1.675B; Bridge Loan: $350M; Term Loan: $165M; Total DMPL Debt Exposure (as of Jan 2025): $748M

2024

Liability Management Exercise (LME)

Debt Raised: $240M; Impact on Annual Interest Expenses: +$4M

Financial Erosion: Performance Trends Leading to Crisis (2020-2024)

The years immediately preceding the bankruptcy filing reveal a sharp deterioration in Del Monte Foods’ financial performance, characterized by declining profitability and severe liquidity challenges.

Detailed Analysis of Revenue, Gross Profit, and Net Income/Loss

The financial health of Del Monte Foods (specifically Del Monte Foods Holdings Limited, the U.S. entity that filed for bankruptcy) experienced a significant decline. For fiscal year 2024 (ended April 28, 2024), the company reported net sales of $1,737.3 million, a marginal increase from $1,733.1 million in fiscal year 2023. However, this apparent stability in top-line revenue masked a severe erosion of profitability.

Gross profit for Del Monte Foods Holdings Limited plummeted to $245.0 million in FY2024, a sharp decrease from $400.3 million in FY2023 and $396.1 million in FY2022. This substantial decline in gross profit indicates a significant squeeze on margins, likely due to rising production costs and the company’s inability to pass these increases on to consumers. The company’s financial trajectory shifted dramatically from a net income of $57.2 million in FY2022 to a net loss of $2.9 million in FY2023, which then worsened considerably to a net loss of $118.6 million in FY2024. This steep descent into unprofitability highlights the severity of its financial distress.

Del Monte Pacific (DMPL), the parent company, also reported a decline in group sales (down 5% in Q3 FY2024, primarily due to lower sales in the U.S., Philippines, and packaged exports) and reduced gross profit, resulting in a net loss of US29millioninQ3FY2024.[34]ForthefirstninemonthsofFY2024,DMPLrecordedanetlossofUS51 million. Specifically, for its U.S. subsidiary (DMFI), sales decreased by 6% in Q3 FY2024, driven by a “strategic shift away from lower-margin co-pack products” and, more critically, “lower canned fruit and vegetable sales on declining category trends”. While Del Monte Foods did see some sales growth in its newer brands like Joyba bubble tea and broth in fiscal 2024, this growth was “not enough to offset weaker sales of Del Monte’s signature canned products”.

It is crucial to differentiate these figures from the financial results of Fresh Del Monte Produce Inc. (FDP), which is a separate entity. Reports pertaining to FDP (e.g.) indicate different and generally more positive financial performance (e.g., $4.28 billion net sales and $142.2 million net income for full fiscal year 2024). These figures are not representative of the financial health of the bankrupt Del Monte Foods. The relevant financial statements for the bankrupt entity are found in.

The financial reporting structure, particularly the distinction between Del Monte Pacific’s consolidated results and Fresh Del Monte Produce’s separate reports, initially obscured the specific and severe financial distress of the U.S. canned goods business (Del Monte Foods). While some consolidated reports might have shown stable group sales, the underlying reality for the U.S. subsidiary was a sharp decline in gross profit and a significant net loss. This demonstrates how corporate reporting can mask the specific vulnerabilities of individual business units, delaying recognition of critical problems until they reach a crisis point. The “US implosion” was, in essence, a hidden crisis within the broader Del Monte Pacific portfolio.

Cash Flow Dynamics and Liquidity Challenges

The escalating interest payments, which nearly doubled from 2020 to 125millionin2025[23],severelyconstrainedDelMonteFoods′cashflow.Thisfinancialpressureledto”erodedliquidity”andsignificantlyhamperedthecompany′sabilitytoadapttochangingmarketconditions.[23]Thedwindlingcashreserves,reportedatonlyUS16.2 million for Del Monte Pacific as of January 31, 2025 , indicated a broader liquidity crunch within the group, heavily influenced by the U.S. subsidiary’s performance.

The substantial increase in interest expenses, coupled with declining gross profits and mounting net losses, created a severe liquidity squeeze for Del Monte Foods. A company cannot sustain operations or invest in necessary strategic shifts without adequate cash flow. The diminishing cash reserves meant that Del Monte was operating on the brink, unable to absorb unexpected costs or market fluctuations. This lack of liquidity made the company highly vulnerable and ultimately forced it to seek Chapter 11 protection, not just to restructure debt, but crucially, to access debtor-in-possession (DIP) financing to maintain basic operations. The bankruptcy filing itself became a necessary mechanism to secure the cash needed to continue as a “going concern.”

The 2024 Liability Management Exercise

In August 2024, Del Monte Foods undertook a Liability Management Exchange (LME) transaction, which raised $240 million of debt. However, this amount was explicitly stated as “not enough to stave off a more fulsome restructuring”.

This LME proved highly controversial, immediately sparking a lawsuit from a group of lenders who claimed it violated a $725 million financing agreement. The restructuring strategy, known as a “drop-down transaction,” involved shifting substantially all of Del Monte’s assets to a new subsidiary to secure new super-priority loans, effectively prioritizing certain lenders over others. The litigation, filed under Section 225 of the Delaware General Corporation Law, challenged the validity of the LME’s board changes and the underlying default claims.

The case was settled in April/May 2025, just before closing arguments were to be heard. As part of this settlement, Del Monte incurred a loan that paradoxically increased its annual interest expenses by an additional $4 million. In June 2025, Del Monte’s parent company, Del Monte Pacific Ltd., chose to skip a payment to its lenders as part of this lawsuit settlement.

The 2024 LME was a desperate attempt to address Del Monte’s debt issues but proved insufficient and, more damagingly, triggered a costly and contentious lawsuit from “left-behind lenders”. This legal battle not only consumed significant financial and management resources but also highlighted a deep breakdown in trust and a fractured relationship with a substantial portion of its creditors. The settlement, which counter-intuitively increased Del Monte’s annual interest expenses by $4 million , demonstrates how attempts to resolve one problem (debt structure) can inadvertently exacerbate others (increased costs, legal entanglements, creditor distrust), ultimately accelerating the company’s trajectory towards bankruptcy.

Debt Covenant Breaches and Defaults

The culmination of these financial pressures and failed restructuring efforts led directly to Del Monte Foods defaulting on its obligations in June 2025. Creditors responded swiftly to this default by appointing a new majority of directors to the boards of Del Monte Foods Holdings Ltd (DMFHL) and its units, and taking control of 25% of Del Monte Pacific’s equity in DMFHL. This decisive action directly preceded and effectively triggered the Chapter 11 filing.

While the long-term trends of declining sales, eroding profitability, and mounting debt created the underlying conditions for Del Monte’s demise, the immediate trigger for the Chapter 11 filing was the company’s default on its debt obligations in June 2025. This default empowered creditors to take decisive action, including replacing the board and taking equity control. This indicates that the company had exhausted its ability to negotiate or operate outside of formal court protection.

The following table provides a concise overview of Del Monte Foods’ (U.S.) financial performance in the years leading up to its bankruptcy:

Note: The “Loans & Borrowings” figures in the table are derived by summing the “Loans and borrowings” from both Non-current Liabilities and Current Liabilities sections of the financial statements for the respective fiscal years.

Shifting Tides: Consumer Preferences and Market Disruption

Beyond internal financial decisions, Del Monte Foods was profoundly impacted by fundamental shifts in consumer behavior and the broader market landscape, which directly undermined its traditional business model.

The Decline of Traditional Canned Goods: A Generational Shift

A fundamental reason for Del Monte’s bankruptcy is the significant and sustained shift in U.S. consumer preferences, with individuals increasingly opting for healthier or cheaper alternatives over canned products. Industry experts widely concur that “consumer preferences have shifted away from preservative-laden canned food in favor of healthier alternatives”.

This trend is not isolated to Del Monte but reflects a broader industry challenge. The American canned fruit-and-vegetable processing industry has experienced an average annual revenue decline of 0.4% over the past five years, a trend that is projected to continue. Del Monte’s collapse is therefore described as a “symptom of a broader industry malaise” , indicating that its struggles are indicative of a systemic issue within the canned food sector.

Despite the inherent advantages of canned goods, such as generally lower prices and longer shelf life compared to fresh produce , consumer demand has consistently shifted away from them. This suggests that the demand for Del Monte’s core products is relatively

inelastic to traditional competitive factors like price or convenience, but highly elastic to evolving perceptions of health, freshness, and quality. This fundamental disconnect means that simply cutting costs or offering promotions, while potentially providing short-term relief, cannot fundamentally reverse the decline in demand for a product category that consumers increasingly view as outdated or less desirable. This makes recovery exceptionally challenging for a legacy brand deeply entrenched in this declining segment.

The Rise of Health-Conscious Consumers and Demand for Fresh/Minimally Processed Foods

The post-pandemic era has witnessed a significant pivot by consumers towards fresher, healthier, and minimally processed food options. This trend is an integral part of a broader “foodie revolution” that prioritizes taste and texture, areas where traditional canned produce often struggles to compete culinarily.

The market for organic produce serves as a strong indicator of this shift, experiencing robust growth with sales expanding at a 10.35% Compound Annual Growth Rate (CAGR) and projected to reach $159 billion by 2033. A substantial portion of consumers, 55% of Americans, explicitly prefer organic produce for health reasons. Del Monte’s failure to adequately innovate and adapt its product lines to align with this burgeoning market for organic, plant-based, and ethically sourced products is identified as a “critical flaw” in its strategy.

The rise of health-conscious consumers and the broader “foodie revolution” is not merely a transient trend but a fundamental, structural reshaping of the food industry. This shift positions traditional, “preservative-laden canned food” as increasingly obsolete, rendering companies like Del Monte, which adhered to these “outdated business models,” vulnerable to “existential threats”. Del Monte’s bankruptcy serves as a “wake-up call” and a “pivotal moment” for the entire canned food sector, demonstrating that failure to innovate in areas like organic certification, transparency, and fresh offerings can lead to corporate failure. Even if Del Monte resolves its debt issues, its long-term viability will depend on a radical transformation of its product portfolio and a significant repositioning of its brand image to align with the evolving consumer demand for food that is “fresh, green, and transparent”.

The following table illustrates the contrasting market trends between the declining canned goods sector and the growing fresh and organic food segments:

Category

Metric

Timeframe

Current Market Size / Projection

Canned Fruit and Vegetable Processing Industry

Average Annual Revenue Decline

Past five years

-0.4%

Organic Sales

CAGR

Projected to 2033

10.35%

Impact of Private Label Brands and Increased Competition

Grocery inflation played a significant role in driving consumers towards cheaper store brands. This trend contributed to a slowdown in demand for branded packaged food, as customers increasingly opted for private label products amidst higher prices. The competitive landscape intensified, with nearly 45% of shelf space being filled by private-label competitors.

Ironically, Del Monte’s strategic decision to “shutter plants and scale back private-label production only accelerated its decline” , as it failed to capture the growing demand for more affordable alternatives. Competitors such as Kroger, with its successful “Simple Truth” brand, and United Natural Foods (UNFI) have effectively dominated the organic and private-label space, leaving Del Monte lagging in these crucial market segments.

Del Monte faced a compounding challenge from both inflation and the rise of private label brands. Inflationary pressures directly eroded consumer purchasing power, making them more price-sensitive. Simultaneously, the proliferation and increasing quality of private label brands offered readily available, cheaper alternatives to Del Monte’s branded products. This created a “double bind”: Del Monte’s branded products faced declining sales volume due to higher prices, while its market share was simultaneously eroded by more affordable private labels.

External Pressures: Macroeconomic Headwinds and Geopolitical Factors at Del Mon

Beyond internal financial decisions and shifting consumer tastes, Del Monte Foods was significantly impacted by broader macroeconomic and geopolitical forces, which exacerbated its inherent vulnerabilities.

Grocery Inflation and its Effect on Consumer Purchasing Behavior

Grocery inflation directly contributed to Del Monte’s struggles by compelling consumers to seek out cheaper store brands. Food prices, generally, rose faster than overall inflation in May 2025, with food prices in May 2025 being 2.9% higher than in May 2024. The period also saw significant food-at-home price increases, notably a 3.5% rise in 2020 following the onset of the COVID-19 pandemic. While overall food prices were predicted to rise at about the historical average rate in 2025, the cumulative effect of prior inflation had already pushed consumers towards more economical choices.

Inflation presented a dual challenge for Del Monte Foods. Firstly, it increased the company’s operational costs, including raw materials, labor, and transportation. Secondly, and perhaps more critically, it directly impacted consumer purchasing power, forcing them to become more price-sensitive and “turn to cheaper store brands”. This meant Del Monte faced a squeeze on both its supply side (higher costs, eroding margins) and its demand side (reduced sales volume for its branded, higher-priced products). For a company already operating with thin margins in a commoditized market, this dual pressure significantly undermined its financial stability and ability to compete.

The Burden of Steel Tariffs on Production Costs and Margins at Del Monte

A significant and specific external shock to Del Monte Foods was the imposition of President Donald Trump’s 50% tariff on imported steel, which became effective in June. These Section 232 tariffs dramatically increased the cost of production for metal cans, a critical component for Del Monte’s core product line. The Producer Price Index (PPI) for metal cans showed a “dramatic spike” between April and May 2025.

Given the “heavily commoditized nature” of Del Monte’s canned goods, the company’s margins were already low. The sharply higher cost of metal cans therefore imposed “significant financial pressure”. Crucially, Del Monte was unable to pass these increased costs on to consumers, as the Consumer Price Index (CPI) for processed fruits and vegetables rose only moderately, “nowhere near the spike in metal can costs”. This inability to adjust pricing further compressed already thin profit margins.

Furthermore, the tariffs had international ripple effects: the European Union’s announced countermeasures led European importers to seek alternative suppliers, impacting U.S. exports of preserved fruits and vegetables. The capital-intensive nature of canned goods production meant that reducing output was not an effective way to cut costs, as the industry relies on high production volumes to achieve economies of scale.

The steel tariffs were not just another cost increase; they were a direct, acute, and unavoidable shock to Del Monte’s already fragile cost structure. Because canned goods are a “heavily commoditized” product and Del Monte lacked the pricing power to pass on these increased costs to consumers , the tariffs directly and severely squeezed its already thin profit margins. This external policy decision disproportionately impacted Del Monte due to its specific product type and operating model, transforming a challenging financial situation into an immediate crisis. The inability to reduce production efficiently further trapped the company, highlighting how geopolitical forces can expose and accelerate the vulnerabilities of legacy industries.

Broader Industry Challenges: Labor Shortages and Supply Chain Volatility

Beyond tariffs and consumer shifts, the food industry as a whole faced significant headwinds, including “elevated food costs, labor shortages, changing consumer habits, and tariffs”. Specific operating challenges in 2024 included “rising food costs, rising labor costs, inflation, staffing recruitment and retention, and ingredient shortages and unavailability (supply chain)”.

Data indicated an increase in foodservice unemployment (e.g., from 5.2% in June to 6.6% in July) , suggesting broader labor market difficulties impacting the food sector. Supply chain obstacles were also a recognized headwind.

While specific factors like debt and consumer shifts were primary drivers, Del Monte’s path to bankruptcy was exacerbated by a confluence of systemic industry challenges. Elevated food costs, labor shortages, and general supply chain volatility are not unique to Del Monte, but for a company already struggling with a heavy debt burden and declining demand for its core products, these additional pressures magnified its vulnerability. Each of these factors, individually manageable for healthier companies, cumulatively eroded Del Monte’s profitability and operational stability, demonstrating that corporate failure often results from a perfect storm of multiple, interconnected adverse conditions rather than a single isolated cause.

The Chapter 11 Filing: A Strategic Maneuver for Survival

The filing of Chapter 11 bankruptcy by Del Monte Foods represents a critical juncture, intended to provide a structured path for the company to address its overwhelming debt and reposition itself for future viability.

The July 1, 2025, Filing: Court, Debt Magnitude, and Immediate Actions

Del Monte Foods Corporation II Inc. and certain affiliates voluntarily filed for Chapter 11 bankruptcy protection in the U.S. Bankruptcy Court for the District of New Jersey on July 1, 2025. Court documents estimate the company’s liabilities and assets to be between $1 billion and $10 billion. The filing also listed between 10,000 and 25,000 creditors.

President and CEO Greg Longstreet characterized the filing as a “strategic step forward” and “the most effective way to accelerate our turnaround and create a stronger and enduring Del Monte Foods”.

Debtor-in-Possession (DIP) Financing for Del Monte

To ensure the continuity of business operations during the Chapter 11 process, Del Monte Foods secured a commitment for $912.5 million in debtor-in-possession (DIP) financing from existing lenders. This financing package includes $165 million in new funding and is subject to court approval.

The primary purpose of this liquidity is to support daily operations, particularly during the critical “pack season” , and to ensure the company can continue fulfilling its obligations to employees, growers, customers, and vendors without interruption.

The substantial $912.5 million Debtor-in-Possession (DIP) financing, including $165 million in new money, is indeed critical for maintaining operations and fulfilling obligations to employees, growers, and vendors during the bankruptcy process. However, it is a complex financial instrument. DIP financing is typically super-priority debt, meaning it gets paid back before other pre-petition debts, which can further disadvantage existing unsecured creditors. The objection raised by non-participating lenders at the first-day hearing highlights this point, as they argued the DIP’s “roll up” of existing debt gave participating lenders an unfair “leg up” in the subsequent sale process.

The Restructuring Support Agreement (RSA) and “Going-Concern” Sale Process

The Chapter 11 filing is part of a broader Restructuring Support Agreement (RSA) reached with a group of its existing lenders. The RSA formalizes a “going-concern” sale process, meaning the company’s assets will be sold as a whole rather than liquidated piecemeal. The aim is to identify the “highest or best offer” for “all or substantially all” of the company’s assets. The stated goal is to achieve an “improved capital structure, enhanced financial position and new ownership” to better position the company for long-term success.

While CEO Greg Longstreet frames the Chapter 11 filing as a “strategic step forward” , it is more accurately understood as a forced strategic pivot. The company’s deep financial distress, culminating in debt default , left it with limited options. Bankruptcy, in this context, serves as a legal mechanism to shed unsustainable debt, resolve contentious lender disputes , and facilitate a change in ownership and capital structure that would be exceedingly difficult or impossible outside of court protection.

Exclusion of Non-U.S. Subsidiaries and their Continued Operations

It is explicitly stated that the voluntary Chapter 11 filing applies only to Del Monte Foods Corporation II Inc. and specific U.S. subsidiaries. Crucially, “certain non-U.S. entities are not part of the proceedings and continue operating as usual”. Del Monte Pacific, the parent company, affirmed that its “Asian and other international businesses continue to perform well, with resilient consumer demand, supported by a strong and stable supply chain”.

The deliberate exclusion of non-U.S. subsidiaries from the Chapter 11 filing highlights a clear strategic decision to “ring-fence” the healthier, more viable parts of the global Del Monte enterprise from the distressed U.S. canned goods business. This indicates a significant geographic disparity in performance, with international operations, particularly in Asia, remaining profitable. This action protects these assets from the immediate claims of the U.S. bankruptcy court, allowing them to continue generating revenue and potentially providing a source of future value for the broader Del Monte Pacific group, albeit potentially subject to value extraction to cover the U.S. losses.

The following table provides a snapshot of Del Monte Foods’ bankruptcy filing details:

Detail

Description

Filing Date

July 1, 2025

Court

U.S. Bankruptcy Court for the District of New Jersey

Case Number

3:25-bk-16984

Estimated Liabilities

Between $1 billion and $10 billion

Estimated Assets

Between $1 billion and $10 billion

Number of Creditors

10,000 to 25,000

Debtor-in-Possession (DIP) Financing Secured

$912.5 million

New Funding within DIP

$165 million

Purpose of Filing

Strategic balance-sheet restructuring and court-supervised sale process for all or substantially all assets

Impact on Operations

Expected to continue normally during the sale process

Non-U.S. Subsidiaries

Excluded from filing, continue normal operations

Conclusions regarding Del Monte

The bankruptcy filing of Del Monte Foods on July 1, 2025, is a complex narrative rooted in a confluence of factors rather than a single cause. The analysis reveals that the company’s financial distress was primarily driven by an unsustainable debt burden, exacerbated by fundamental shifts in consumer preferences away from its core canned products, and compounded by challenging macroeconomic and geopolitical pressures.

The successive leveraged buyouts in 2011 and 2014, while intended to drive growth and value, ultimately saddled Del Monte Foods with an immense debt load. This high leverage severely constrained its financial flexibility, diverting crucial capital from innovation and market adaptation towards escalating interest payments. The controversial 2024 liability management exercise and subsequent lender lawsuits further fractured creditor relationships and paradoxically increased the company’s interest expenses, signaling a desperate attempt to manage an unmanageable debt structure. The eventual default on its obligations in June 2025 by the U.S. subsidiary was an inevitable consequence of this financial fragility, directly triggering the bankruptcy filing.

Simultaneously, Del Monte Foods faced a secular decline in demand for its signature canned products. The rise of health-conscious consumers, a preference for fresh and minimally processed foods, and the increasing market penetration of cheaper private-label brands created an existential threat to its traditional business model. The company’s strategic divestitures of its fresh produce and pet food businesses in earlier periods, while potentially logical at the time, meant it shed segments that proved more resilient or aligned with emerging consumer trends, leaving its core business highly vulnerable. This, coupled with brand fragmentation due to multiple ownership changes, hampered its ability to pivot effectively.

Finally, external forces such as grocery inflation, which eroded consumer purchasing power and pushed them towards more affordable alternatives, and especially the U.S. steel tariffs, which dramatically increased the cost of metal cans without allowing for price pass-through, delivered acute financial shocks. These factors, combined with broader industry challenges like labor shortages and supply chain volatility, created a perfect storm that overwhelmed an already weakened Del Monte Foods.

The Chapter 11 filing, characterized as a strategic sale process, is a forced pivot designed to shed unsustainable debt and attract new ownership with fresh capital. While the exclusion of non-U.S. subsidiaries protects some value within the broader Del Monte Pacific group, the future of the U.S. canned goods business hinges on a successful sale and a radical transformation to align with contemporary consumer demands. Del Monte Foods’ experience serves as a stark reminder that even a century-old brand with a strong legacy cannot withstand the combined pressures of excessive financial leverage, profound shifts in consumer preferences, and adverse macroeconomic conditions without significant and timely adaptation.

Spirit Airlines has initiated a Chapter 11 bankruptcy process as part of a comprehensive restructuring strategy. This step, taken under a pre-arranged Restructuring Support Agreement (RSA), aims to reduce the airline’s $3.3 billion debt burden and bolster its financial flexibility. The plan includes converting $795 million of funded debt into equity and securing $350 million in new investments from bondholders. An additional $300 million in debtor-in-possession financing will support operations during the restructuring.

Key factors contributing to Spirit’s financial difficulties include high operating costs, stiff competition, and disruptions caused by grounded planes due to engine issues. The airline was also affected by the collapse of its planned $3.8 billion merger with JetBlue, which faced regulatory roadblocks

Despite the bankruptcy, Spirit Airlines will continue to operate normally, with flights, loyalty programs, and employee wages unaffected. The restructuring is expected to be completed by mid-2025, positioning Spirit for improved operational stability and growth,

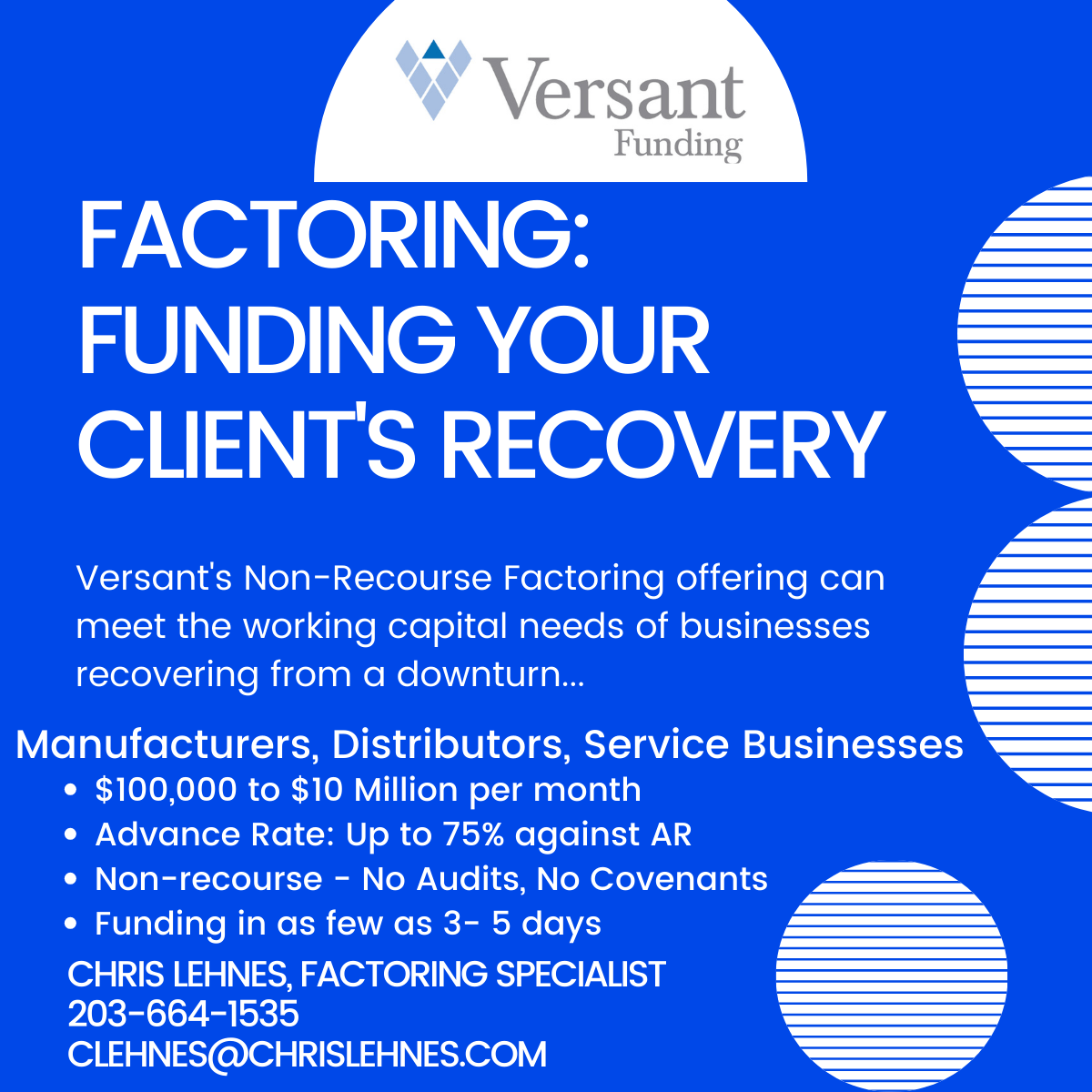

Factoring: Funding your client’s Recovery – Versant’s Non-Recourse Factoring offering can meet the working capital needs of businesses recovering from a downturn…

Contains information related to marketing campaigns of the user. These are shared with Google AdWords / Google Ads when the Google Ads and Google Analytics accounts are linked together.

90 days

__utma

ID used to identify users and sessions

2 years after last activity

__utmt

Used to monitor number of Google Analytics server requests

10 minutes

__utmb

Used to distinguish new sessions and visits. This cookie is set when the GA.js javascript library is loaded and there is no existing __utmb cookie. The cookie is updated every time data is sent to the Google Analytics server.

30 minutes after last activity

__utmc

Used only with old Urchin versions of Google Analytics and not with GA.js. Was used to distinguish between new sessions and visits at the end of a session.

End of session (browser)

__utmz

Contains information about the traffic source or campaign that directed user to the website. The cookie is set when the GA.js javascript is loaded and updated when data is sent to the Google Anaytics server

6 months after last activity

__utmv

Contains custom information set by the web developer via the _setCustomVar method in Google Analytics. This cookie is updated every time new data is sent to the Google Analytics server.

2 years after last activity

__utmx

Used to determine whether a user is included in an A / B or Multivariate test.

18 months

_ga

ID used to identify users

2 years

_gali

Used by Google Analytics to determine which links on a page are being clicked

30 seconds

_ga_

ID used to identify users

2 years

_gid

ID used to identify users for 24 hours after last activity

24 hours

_gat

Used to monitor number of Google Analytics server requests when using Google Tag Manager