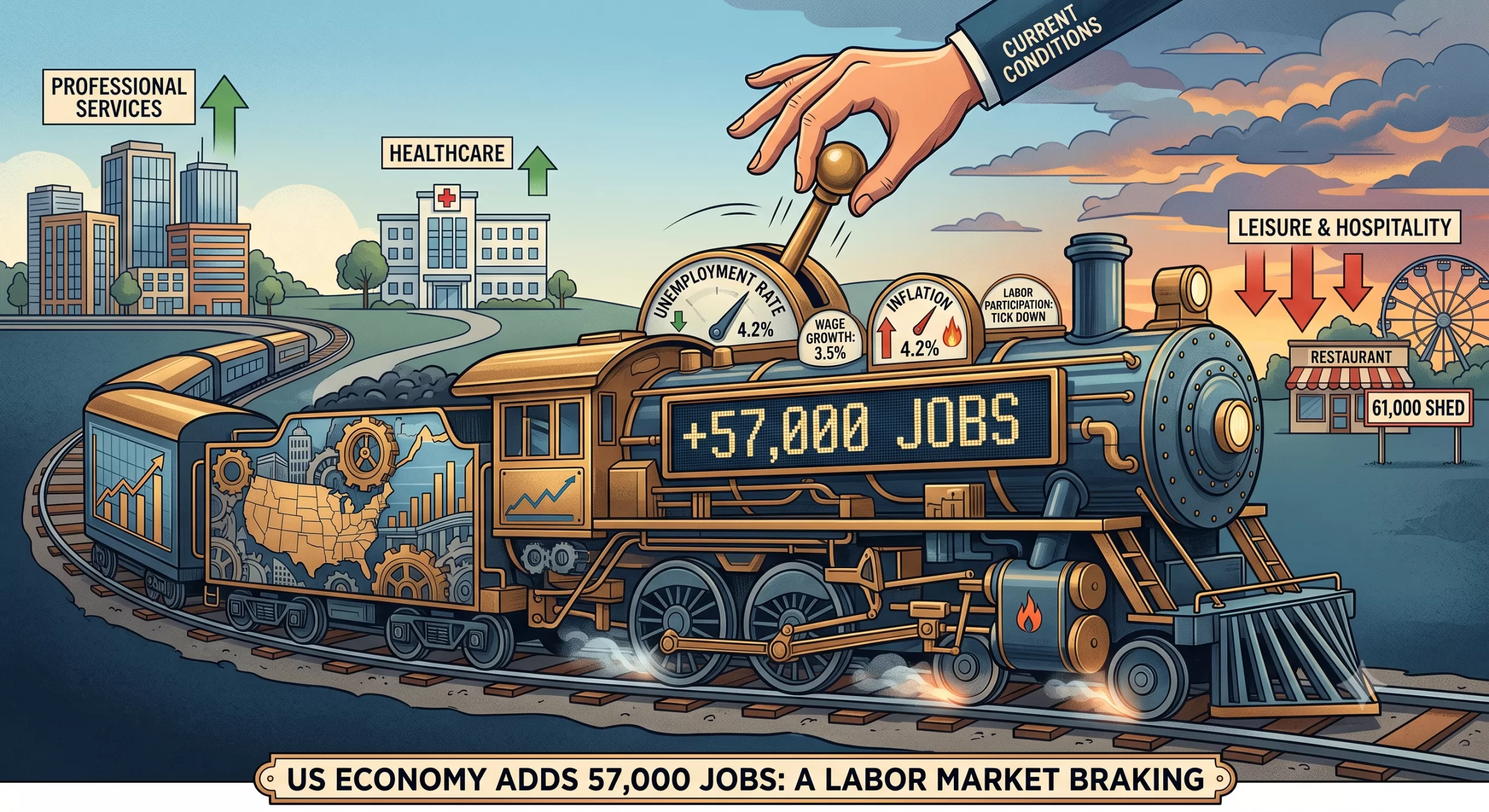

The June 2026 Jobs Report: A Labor Market Hitting the Brakes

The latest U.S. jobs numbers dropped this morning, and they’ve thrown a bit of cold water on the summer economic outlook. According to the Bureau of Labor Statistics, the U.S. economy added just 57,000 jobs in June 2026. This comes in far below Wall Street’s expectations of roughly 110,000 to 115,000 jobs, marking a significant cooldown after three months of stronger-than-expected hiring.

Here is a breakdown of what you need to know about the June report, where the jobs are going, and what it means for the broader economy.

The Headline Numbers

At first glance, the data presents a mixed bag. Job growth is slowing, yet the unemployment rate actually ticked downward.

| Metric | June 2026 Reality | What Was Expected |

|---|---|---|

| New Jobs Added | 57,000 | ~115,000 |

| Unemployment Rate | 4.2% | 4.3% |

| Wage Growth (YoY) | 3.5% | N/A |

Why did unemployment fall if hiring slowed? It comes down to labor force participation. The unemployment rate dropped from 4.3% in May to 4.2% in June primarily because roughly 720,000 people left the labor force entirely. When people stop actively looking for work, they are no longer counted as “unemployed.” This dynamic can artificially drag the headline rate down even in a sluggish hiring environment.

Where the Jobs Are (And Aren’t)

The June report highlighted a stark divergence between sectors. The stalwarts are still hiring, but consumer-facing industries are feeling the pinch.

- The Winners: Professional and business services led the pack, adding 36,000 new positions. Healthcare and social assistance also continued their long-term growth trend, adding 22,000 and 25,000 jobs respectively, though healthcare hiring has slowed slightly from its 12-month average.

- The Losers: The biggest surprise was in leisure and hospitality, which shed 61,000 jobs. Many economists anticipated a strong summer hiring surge fueled by traditional vacations and the World Cup being hosted in the U.S., but early optimistic hiring seems to have been scaled back.

- Downward Revisions: Adding to the softer picture, the Labor Department revised April and May’s job totals downward by a combined 74,000 jobs. May’s initially robust report of 172,000 new jobs was walked back to just 129,000.

What This Means for the Fed and Your Wallet

The central question on everyone’s mind is how this impacts inflation and interest rates. With inflation recently hitting a three-year high of 4.2% (partly driven by the geopolitical ripple effects of the ongoing conflict in Iran), the Federal Reserve under new Chair Kevin Warsh has been walking a tightrope.

Prior to this report, markets were bracing for the Fed to raise interest rates as soon as October to combat rising prices. However, a labor market that is clearly shifting down in momentum gives the Fed a bit of breathing room. Traders are now scaling back those expectations, betting that the central bank might hold off on rate hikes until December.

For the average worker, the job market has become a “low-hire, low-fire” environment. Layoffs remain relatively low, but companies aren’t bringing on new talent at the frantic pace seen in recent years. Meanwhile, average hourly earnings rose by 0.3% in June, bringing the annual increase to 3.5%. Unfortunately, with inflation outpacing that wage growth, many households are still feeling their purchasing power diminish.

The Bottom Line The labor market is still holding steady, but the engine is definitely decelerating. We are transitioning away from a job hopper’s market into a phase where both employers and employees are staying put, watching the inflation data, and waiting to see what the Fed does next.