We continue to assist companies nationwide in converting IEEPA tariff refund claims into immediate cash, even after the launch of U.S. Customs and Border Protection’s(“CBP”) CAPE refund portal and the latest April 28th update from the U.S. Court of International Trade (“CIT”).

CIT’s April 28th status review confirmed that the lead IEEPA refund litigation has largely moved from the legal entitlement phase into the implementation and payment phase. In simple terms, the question is no longer primarily whether many importers are entitled to refunds, the issue is when those refunds will actually be paid.

While CBP officially launched CAPE on April 20th to process refunds, there was no new court order requiring immediate payment of all claims. Instead, the CIT is supervising execution, while Customs works through claim submissions, liquidation status, eligibility reviews, and administrative processing. This distinction matters. CBP has indicated that certain accepted claims may be paid within approximately 45–60 days plus statutory interest.

However, “acceptance” is not the same as submission. Importers must first complete filing requirements, resolve broker authority issues, verify liquidation status, satisfy procedural review, and clear compliance review before the payment clock truly begins. For many importers, especially those with older entries, previously liquidated claims, multiple brokers, documentation issues, or claims that may fall outside CAPE Phase 1, the actual recovery timeline could extend for many months or significantly longer. As a result, our buyers remain highly active in purchasing IEEPA tariff refund claims, with transactions from $250,000 to $7 million purchased at a Buy Rate of 85%, while claims exceeding $7 million have a Buy Rate of 90%.

Why Importers are still Selling Tariff Refund Claims after CAPE Opened

Judge Eaton of CIT did not order immediate universal payment of all claims. CBP’s estimated payment window begins only after formal claim acceptance, not submission.

Many claims do not clearly qualify for CAPE Phase 1 and may require later phases. Finally liquidated entries remain one of the largest unresolved issues. Previously liquidated entries may still require protests, reliquidation, or additional litigation. The right to a refund is clearer—but the timing of payment remains uncertain.

CSV upload issues, ACE access problems, and broker mismatches can delay acceptance. Documentation gaps and reconciliation issues remain common. Customs audit and compliance review may delay payment even after filing.

Trump Administration appeal deadlines and future legal developments could delay the timing of refund payments. Processing millions of entries may create substantial administrative backlogs. Port-by-port inconsistencies may slow recovery for certain importers. Working capital needs often cannot wait for government processing timelines/.

Importers Are Choosing To Monetize Now

Immediate working capital for inventory, payroll, and vendor obligations. Reduced lender pressure and improved borrowing base flexibility. Elimination of refund timing risk and litigation uncertainty. Improved balance sheet certainty. Faster access to liquidity without waiting for government disbursement. Stronger buyer pricing now that CAPE implementation is underway as Buy Rates increased from 45% in February to 85% today

For many businesses, immediate liquidity today is worth more than waiting for a larger payment later. Many importers are no longer asking. “Will I get paid?”, They are asking, “Is waiting worth the delay, uncertainty, and operational risk?”. For many companies, the answer is no. We work with importers with claims starting at $250,000, with no maximum limit across industries including food, seasonal goods, apparel, and home products.

Most transactions can be completed in approximately 10 business days, assuming proper documentation and credit quality.

Convert IEEPA Tariff Claims to Cashon an Expedited Basis

I have been actively assisting companies nationwide in converting their IEEPA tariff refund claims into immediate cash.

U.S. Customs and Border Protection is rolling out a centralized system (CAPE) to process refunds, and some trade experts believe that certain importers could begin receiving refunds within the next six months. However, there remains significant uncertainty around timing, and many industry participants believe that a large portion of claims could still take years to fully resolve.

Convert IEEPA Tariff Claims to Cash on an Expedited Basis

This divergence is driven by several factors, including: The complexity and scale of processing millions of entries The possibility that certain categories of claims may be prioritized over others, delaying recovery for more complex or lower-volume importers The need for new administrative procedures, as IEEPA does not clearly define a refund mechanism The potential for case-by-case eligibility determinations

Ongoing legal and procedural developments, including possible appeals by the Trump Administration and implementation challenges

Liquidation Status – Whether entries have already been liquidated, which in many cases may require formal protests or litigation to reopen and recover duties The likelihood of inconsistent treatment across ports (port-by-port) or entry types as CBP implements new processes in phases Documentation gaps and data reconciliation issues, particularly for older entries or those filed across multiple brokers The absence of clear guidance on how interest on refunds will be calculated and paid, which could lead to further disputes

Capacity constraints within CBP and the potential for processing backlogs as refund volumes scale

Continued legal challenges around the scope of eligibility, including disputes over classifications, valuation, or origin that could delay specific claims

As a result, while some importers may receive refunds within six months, others, particularly those with more complex or previously liquidated entries, could face a multi-year recovery timeline. To address this uncertainty, financial institutions and hedge funds are actively purchasing IEEPA tariff refund claims at a discount.

Current buy rates are as high as 85% of the expected refund value, depending on claim size, credit quality of the importer and documentation quality as these claims are not directly assignable. AES works with importers with claims starting at $250,000, with no maximum limit. Since entering this market five months ago, AES has facilitated the monetization of approximately $20 million in claims across industries including food, seasonal goods, apparel, and home products.

Market pricing has evolved significantly: Prior to the February 20, 2026, Supreme Court ruling, claims traded at approximately 20–25% Following the ruling, pricing increased to 40–50% More recently, improving legal clarity and market participation have driven pricing to current levels of up to 85% of the IEEPA tariff refund amount

While some importers initially adopted a “wait and see” approach in anticipation of near-term refunds, the combination of timing uncertainty and significantly improved pricing has led many to explore monetization as a way to eliminate risk and accelerate liquidity. The Funds AES works with are able to complete transactions in approximately 2–3 weeks, depending on the completeness and quality of documentation.

Trade experts predict it could take at least 2 to 5 years for importers to receive their IEEPA tariff refunds due to both the long-standing rules that are in effect and the Administration’s adversarial stance to issuing tariff refunds.

The administration can make appeals, request Stays from the U.S. Court of International Trade, Customs could request a case-by-case eligibility review and there could be delays in the system upgrades that Customs and Border Protection are working on. Financial institutions are purchasing these tariff claims at a discount.

The current Buy Rates are now up to 85% of the refund amount. Rates are based on claim size and credit quality as tariff refund claims are not assignable. Importers with IEEPA tariff refund claims starting at $350,000 are eligible and there is no maximum limit. AES has monetized $20 million in refund claims since its involvement in brokering IEEPA tariff refund claims commenced 5 months ago.

Clients include those in the food, seasonal decoration, apparel and home goods industries. Prior to the Supreme Court’s ruling on February 20, 2026 IEEPA claims were trading at an average of only 22%. After the ruling against the Administration Buy Rates increased to 40%-50 % and subsequent to some positive rulings on March 4 and 6th by the Court of International Trade (“CIT”) and other encouraging news stories, Buy Rates have now increased to up to 85 %.

Importers were initially taking a wait and see approach after the recent rulings by CIT as there was initially hope they might see refunds in a manner of months. With the significant increase in Buy Rates and negativity regarding timing in the media, importers are now coming off the sidelines and exploring the potential sale of their IEEPA tariff refund claims. The Funds AES works with can purchase claims within approximately 3 to 5 weeks depending on the quality of documentation assembled by the importer. For a detailed discussion of how these two options work see below.

How the Process of Selling an IEEPA Tariff Claim Works

Model is: As an example, Company X has paid ($10 Million) in tariffs since April 7, 2025Company X wants to de-risk prior to determination and finalization of the IEEPA tariff Refund Process. Company X sells (50%, 100%, or some other percentage) of its tariff ‘claim’ to Buyer A in the form of a participation. The Trade is nonrecourse to Company X as to the outcome of the Refund Process; but recourse to Company X only if the amount / validity of the claim is proven to be false, or too high.

Process for Selling IEEPA Tariff Claims: As an example, Company X has paid $10 million in IEEPA Tariffs. Company X agrees to “sell” its tariff claim to Buyer for 85% of the claim amount, i.e. $8.5 million. Buyer sends Seller a Confirm, and then ultimately a Participation Agreement which will govern the transaction.

IMPORTANT – Company X retains its status as the “Plaintiff” / “Claimant” since these tariff claims are not transferable. Buyer might ask Company X to commence litigation for the return of the IEEPA tariffs paid. The rationale for this is that it is possible that only those parties who have commenced actual litigation are entitled to refunds.

Thus, Company X will need to commence litigation in order to receive their refund.Buyer will continue to monitor the situation and inform Company X of developments.If and when the refund is received on the claim, Company X will receive the refund and forward to the Buyer.

Using an IEEPA Tariff Claim as Collateral for a Loan In lieu of selling an IEEPA Tariff Claim at a discount, it is possible to use this claim as collateral for a term loan. This term loan would be on a “recourse: basis to the borrower. The potential loan amount could be up to approximately 50% to 60% of the total IEEPA claim amount. However, the claim must exceed $20 million to qualify for a loan. The interest rate would be in the low to mid-teens.

Important Points Regarding the Sale of a Tariff Claim: Company X (as seller of the Claim) must be a financially healthy enough counterparty for Buyer A to enter into what could be a 2-to-5-year process of obtaining the refund. Legal fees are split going forward based on risk percentage. If Company X sells 100% today, Buyer A will pay 100% of legal costs today. Buyers are currently paying up to 85% to companies seeking to sell their IEEPA tariff claims.

However, this is an evolving market and these percentages can either increase or decrease depending on the markets’ reaction to the Trump Administration’s expected obstructionism and the unresolved Court of International Trade’s procedural issues.

Prior to the Supreme Court decision, buyers were purchasing tariff claims at an average of 22% due to the high risks involved. We will be monitoring on a daily basis the rates at which Buyers are purchasing IEEPA claims and we will update our website accordingly. Feel free to email us to ascertain what the rate is on any particular day. There would likely be an administrative process instituted such that companies that have paid these IEEPA tariffs will need to file special claims and wait to get refunded by the government.

The process of receiving the refund payment from the government could take up to 2 to 5 years according to trade experts.

What is Factoring: In the world of distribution, the “growth paradox” is a real headache. You land a massive new retail contract—which is great news—but suddenly you’re shelling out for inventory and shipping costs while your customer sits on a 60- or 90-day payment term.

For many distributors, waiting for those invoices to clear creates a suffocating bottleneck. This is where Accounts Receivable (AR) Factoring comes in. It’s not a loan; it’s a financial tool that turns your unpaid invoices into immediate working capital.

How It Works: The Quick Breakdown

Instead of waiting months for a customer to pay, you sell your outstanding invoices to a “factor” (a specialized financial company).

The Advance: The factor typically advances you 80% to 90% of the invoice value within 24 hours.

The Collection: The factor handles the collection from your customer.

The Rebate: Once the customer pays, the factor sends you the remaining balance, minus a small fee (usually 1–3%).

4 Major Benefits for Distributors

1. Bridge the Inventory Gap

Distributors often have to pay suppliers long before they get paid by their own clients. Factoring provides the liquidity to pay your manufacturers upfront, often allowing you to take advantage of early-payment discounts that can actually offset the cost of the factoring fee itself.

2. Fuel Rapid Scalability

Traditional bank loans are limited by your credit history or collateral. Factoring, however, scales with your sales. The more you sell to reputable customers, the more funding becomes available. It allows you to say “yes” to large orders that you otherwise couldn’t afford to fulfill.

3. Professional Credit Management

Many factoring companies act as an extension of your back office. They perform credit checks on your potential customers, helping you avoid “bad seeds” before you ship a single pallet. This reduces your risk of bad debt and saves your team the awkwardness of making collection calls.

4. No New Debt

Since factoring is the purchase of an asset (your invoice) rather than a loan, it doesn’t show up as debt on your balance sheet. This keeps your debt-to-equity ratio clean, making your business look much healthier to future investors or traditional lenders.

Is It Right For You?

Factoring is particularly powerful if you are:

A startup with a thin credit history but blue-chip customers.

Experiencing seasonal spikes that drain your cash reserves.

Tired of the “waiting game” associated with 30, 60, or 90-day terms.

While there is a cost involved, the ability to reinvest that cash immediately into new inventory or operations often outweighs the fee. In the fast-moving world of distribution, speed is a competitive advantage.

Factoring vs. A Traditional Line of Credit: A Distributor’s Comparison

While both tools solve cash flow problems, they operate very differently. Here is how they stack up for a growing distributor:

Feature

AR Factoring

Traditional Bank Line of Credit (LOC)

Funding Limit Based On…

The creditworthiness of your customers and your accounts receivable balance.

Your business’s credit history, profitability, and your collateral.

Speed of Funding

Extremely fast. Setup takes a few days; once active, funding often occurs within 24–48 hours of invoice verification.

Slow. The approval process can take weeks or even months.

Debt Type

Not Debt. It is the “asset purchase” of your invoices.

Debt. This is a loan that appears as a liability on your balance sheet.

Impact on Credit

Boosts Credit Score. It provides cash to pay your suppliers and operational debts on time.

Lowers “Available” Credit. Utilizing the full LOC can temporarily lower your score until it’s paid down.

Administrative Support

The factor often provides credit management and collection services, freeing up your back office.

You retain full responsibility for all collections and monitoring customer credit.

Scalability

Unlimited. As your credit-worthy sales grow, your available funding automatically increases.

Capped. Your limit is fixed and requires a re-application process to increase.

Gemini said

Certainly. Here is a comparison table and a section you can drop directly into your blog post.

Factoring vs. A Traditional Line of Credit: A Distributor’s Comparison

While both tools solve cash flow problems, they operate very differently. Here is how they stack up for a growing distributor:

Feature

AR Factoring

Traditional Bank Line of Credit (LOC)

Funding Limit Based On…

The creditworthiness of your customers and your accounts receivable balance.

Your business’s credit history, profitability, and your collateral.

Speed of Funding

Extremely fast. Setup takes a few days; once active, funding often occurs within 24–48 hours of invoice verification.

Slow. The approval process can take weeks or even months.

Debt Type

Not Debt. It is the “asset purchase” of your invoices.

Debt. This is a loan that appears as a liability on your balance sheet.

Impact on Credit

Boosts Credit Score. It provides cash to pay your suppliers and operational debts on time.

Lowers “Available” Credit. Utilizing the full LOC can temporarily lower your score until it’s paid down.

Administrative Support

The factor often provides credit management and collection services, freeing up your back office.

You retain full responsibility for all collections and monitoring customer credit.

Scalability

Unlimited. As your credit-worthy sales grow, your available funding automatically increases.

Capped. Your limit is fixed and requires a re-application process to increase.

Which One Wins for Distributors?

A bank line of credit is almost always the cheapest form of capital if you can get approved for a large enough limit.

However, for distributors in a hyper-growth phase, or those whose balance sheets don’t match their ambition, AR factoring offers unmatched speed and scalability. It allows you to leverage your customers’ financial strength to fund your own growth.

The Final Verdict: When to Choose Factoring

For a distributor, the choice between factoring and other financing boils down to your growth trajectory and customer base.

A traditional bank line of credit is often the lowest-cost option, but it is also the most rigid. If you have years of steady profitability and a “boring” (predictable) growth curve, the bank is your best friend.

However, AR factoring is the superior choice if:

You are growing faster than your cash flow allows: If a sudden 50% increase in orders would actually break your business because you can’t afford the inventory, you need factoring.

You have “lumpy” revenue: If you deal with seasonal spikes where you need $500k in October but only $50k in January, the flexibility of factoring is unmatched.

Your customers are larger than you: If you are a small distributor selling to giants like Walmart or Amazon, a factor will look at their multi-billion-dollar credit rating to fund you, rather than your own limited history.

Ultimately, factoring isn’t just a way to get paid early—it’s a way to weaponize your accounts receivable to outmaneuver competitors who are still stuck waiting for a check in the mail.

(March 19, 2026) Versant Funding LLC is pleased to announce that it has funded a $5 Million non-recourse factoring facility to a 90+ year-old company that provides services to major consumer brands.

After acquisition by a Private Equity Group, our latest client’s new management team implemented a turnaround plan which required additional cash. While the company was in the process of applying for an asset-based line of credit, time was of the essence and a funding date for the ABL facility was uncertain.

“Versant can fund faster than most traditional financing sources because we focus solely on the credit quality of our clients’ customers and do not perform a full underwriting or audit of the business” according to Chris Lehnes, Business Development Officer for Versant Funding, and originator of this financing opportunity. “Since this company’s customers include some of the world’s strongest consumer brands, we quickly approved the transaction and were ready to fund in about a week.”

Versant Funding’s custom Non-Recourse Factoring Facilities have been designed to fill a void in the market by focusing exclusively on the credit quality of a company’s accounts receivable. Versant Funding offers non-recourse factoring solutions to companies with B2B or B2G sales from $100,000 to $30 Million per month. All we care about is the credit quality of the A/R. To learn more contact: Chris Lehnes |203-664-1535 | chris@chrislehnes.com

The first few warm days of spring mean flowers, baseball, and for many small business owners in March 2026, the annual financial checkup. If you’ve looked at your numbers and realized you need a cash injection for new equipment, that third location, or an aggressive inventory build, you know the drill: It’s time to find the capital. While large national banks are the obvious choice, they are often difficult, impersonal, and slow. By comparison, credit unions have become the unexpected superstars of commercial lending, especially for small and medium-sized enterprises (SMEs).

If you are hunting for a business loan this month, you need to understand why credit unions are dominating and how to find the one that will actually make that critical “yes” happen for your business.

The Not-So-Secret Advantage of the Member-Owner

To understand why credit unions often beat banks on business lending, you have to look at their structure.

Banks answer to shareholders who demand profits and high returns on equity. Every decision, including who gets a loan, is filtered through the lens of maximizing shareholder value.

Credit unions, however, are not-for-profit cooperatives. They do not have public stock. Their members (you, me, and other account holders) are the owners.

This single difference ripples through every interaction. For business lending in 2026, it means:

1. Rates and Fees That Just Make More Sense: Instead of returning profit to Wall Street, credit unions reinvest earnings back into the institution and their members. This often manifests as lower interest rates on commercial loans and significantly lower loan-origination and maintenance fees. In 2026, when inflation has been a recent headache, a difference of 0.5% on a large loan term can mean thousands of dollars saved.

2. Hyper-Local Expertise: When you sit down with a commercial lender at a bank, their rules, algorithms, and models might be set at headquarters 2,000 miles away. They may not understand the specific micro-market in Newtown, Connecticut, where you are operating. But your local credit union officer lives here. They understand why opening a second pizza parlor on the new development is a smart bet, not a risky venture. They lend based on local market knowledge.

3. Relationships Over Risk-Scores: A bank will look at your credit score and financial statements, enter them into a model, and receive a automated “Approve” or “Deny.” Credit unions, especially smaller, focused ones, prioritize relationships. They are more likely to have a real human look at your complete business plan, understand your unique vision, and listen to the story behind your application, not just the numbers on the page.

The “New Reality” of SBA Lending

One of the most important developments in 2026 is that the Small Business Administration (SBA) has made it significantly easier and faster for credit unions to facilitate SBA 7(a) and 504 loans.

For many small businesses, these government-backed loans are the Holy Grail: long terms, lower interest rates, and lower down-payment requirements. Previously, massive banks dominated this space because the paperwork was crushing.

However, the “Streamline and Connect Act” of 2024 (as we projected) drastically simplified the SBA application process and created digital interfaces specifically designed for smaller community financial institutions.

This means that in March 2026, the local credit union you never expected to handle an SBA application is now a Preferred Lender, capable of getting your government-backed loan approved in weeks, not months.

How to Evaluate a Credit Union in March 2026

You can’t just walk into the nearest credit union and expect a perfect loan offer. To find the “best” one for your business right now, you must be strategic:

Step 1: Membership Criteria (The Gateway)

Credit unions can’t just lend to anyone. They operate under a specific “field of membership” (FOM). While some have broadened their charters, many are still strictly limited. To find the “best,” you must find the one you can actually join.

Geographic FOM: Are you eligible because your business is located in Newtown, CT, or the surrounding county? This is the most common path.

Associational or Professional FOM: Are you a veteran? An educator? A first responder? A member of a specific local church or union? There are niche credit unions specialized for these groups, and they often offer highly beneficial industry-specific lending programs.

Step 2: Technology and Speed

While personal relationships are the hallmark of credit unions, it’s 2026. You should not have to wait 30 days for a response to your application. A strong, business-friendly credit union will have a fast, streamlined digital application portal.

They should have digital tools that connect directly to your accounting software (like QuickBooks or Xero), allowing their lenders to instantly verify your cash flow without forcing you to hunt down piles of paper bank statements. If a credit union’s website looks like it hasn’t been updated since 2018, that is a massive red flag.

Step 3: Ask About Specific Business Expertise

The credit union that is excellent for a car loan or a personal mortgage is not necessarily the best choice for a $500,000 commercial line of credit to finance inventory for a manufacturing business.

When you interview a prospective credit union, ask about their experience in your industry. A credit union that specializes in healthcare practice lending will have different perspectives and better loan structures than one that primarily works with general contractors.

The March 2026 Takeaway: Don’t Lead with a Bank

Your default shouldn’t be the massive financial conglomerate that you can only reach via an 800-number. Your first stop in 2026 should be your local, community-focused credit union. They are built to serve owners like you, and they have the tools and local knowledge to help your business take flight this spring.

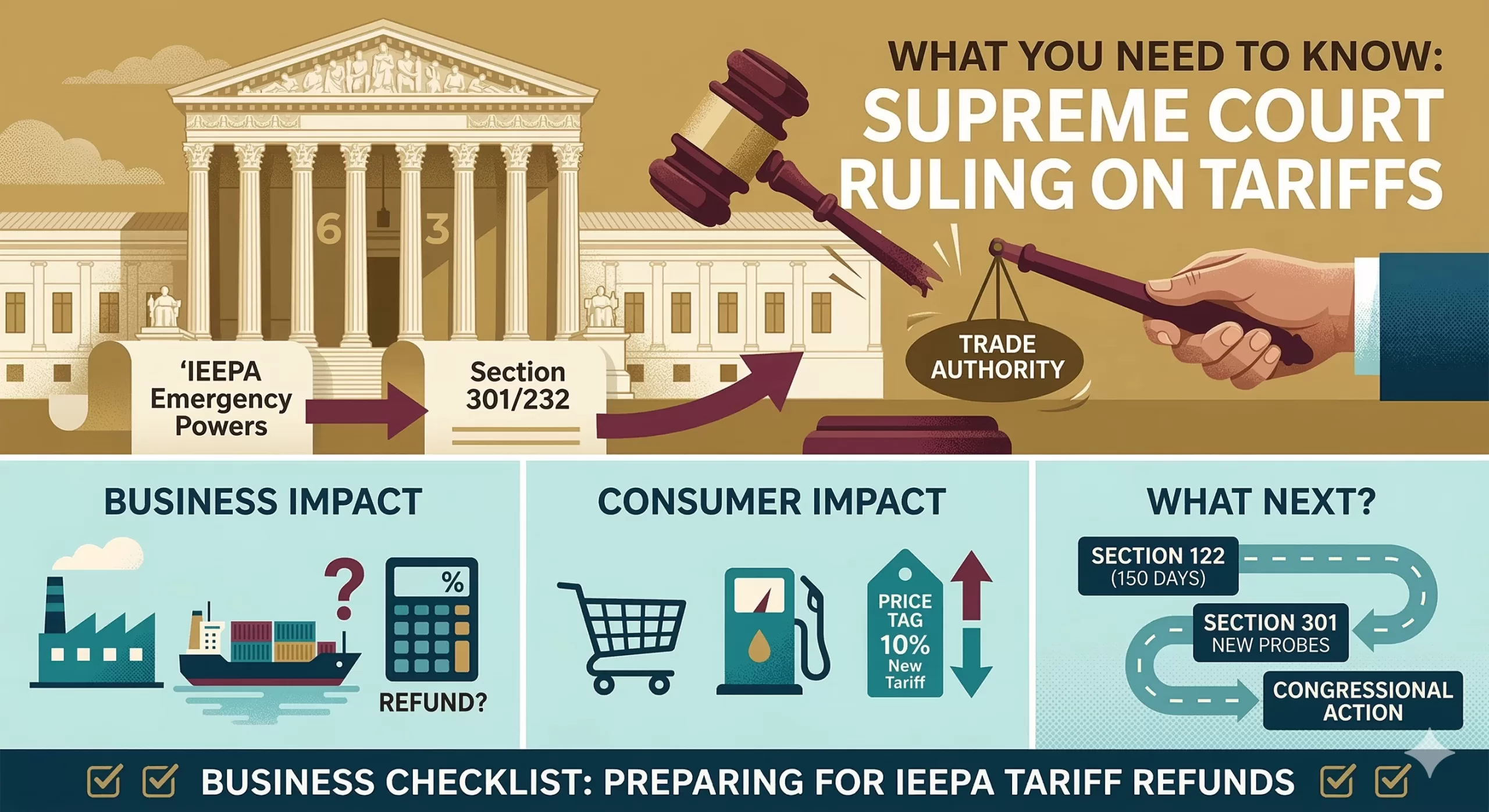

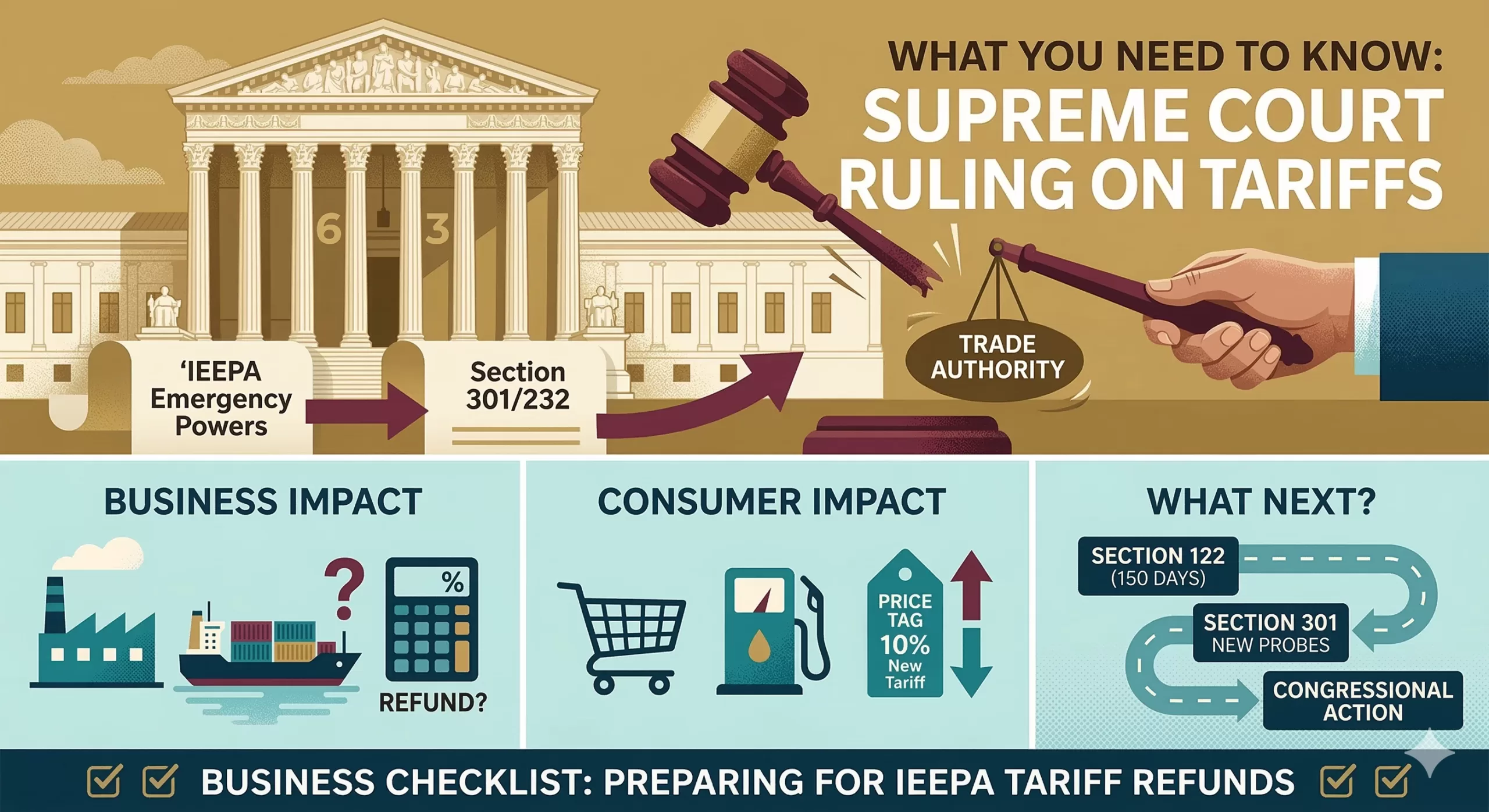

In a landmark decision that has reshaped the landscape of IEEPA Tariffs and American trade policy, the Supreme Court recently issued a ruling in Learning Resources, Inc. v. Trump. The 6-3 decision struck down a series of sweeping tariffs, delivering a significant blow to the administration’s use of emergency powers to regulate the economy.

If you’re a business owner, importer, or simply a consumer wondering why prices are shifting again, here is everything you need to know about this historic ruling about IEEPA Tariffs and what comes next.

The Heart of the Case: IEEPA Tariffs vs. The Taxing Power

The central question before the Court was whether the International Emergency Economic Powers Act (IEEPA) of 1977 gives the President the authority to impose tariffs.

The administration had used IEEPA to levy “reciprocal tariffs” and “trafficking tariffs” on products from China, Canada, and Mexico, arguing that trade imbalances and border security issues constituted a national emergency. However, the Supreme Court ruled that:

Tariffs are Taxes: Chief Justice John Roberts, writing for the majority, emphasized that the power to tax—which includes tariffs—belongs exclusively to Congress under Article I of the Constitution.

“Regulate” is not “Tax”: The Court held that IEEPA’s authority to “regulate importation” does not mean the President can unilaterally set tax rates

The Major Questions Doctrine: The Court applied this principle, stating that if Congress intended to delegate such massive economic power to the Executive Branch, it would have said so clearly and explicitly.

“The Framers did not vest any part of the taxing power in the Executive Branch,” wrote Chief Justice Roberts.

What Happens to the Money? The Refund “Mess”

One of the most pressing questions for businesses is the status of the billions of dollars already collected. Since 2025, the government has gathered an estimated $133 billion to $200 billion in IEEPA-based tariffs.

Court of International Trade (CIT) Action: Following the Supreme Court ruling, the CIT has ordered U.S. Customs and Border Protection (CBP) to begin preparing for a massive refund process.

The “Mess” Factor: Justice Brett Kavanaugh noted in his dissent that issuing these refunds will be a “mess.” It remains unclear exactly how and when businesses will see that money returned, as the Supreme Court did not provide a specific roadmap for the refund process

The Administration’s Pivot: Section 122 and 301

If you thought this ruling meant the end of tariffs, think again. Within hours of the decision, the administration began moving to alternative legal authorities:

Section 122 (Trade Act of 1974): The President implemented a temporary 10% global baseline tariff under this law. However, this power is limited to 150 days and a maximum rate of 15% unless Congress intervenes.

Section 301 Investigations: The U.S. Trade Representative (USTR) has launched new investigations into “structural excess capacity” and “forced labor” in countries like China and Mexico. These could lead to new, more legally “durable” tariffs in the coming months.

Section 232 Still Stands: Tariffs on steel and aluminum, which rely on a different national security statute, were not affected by this specific ruling and remain in place.

What This Means for You

For Businesses and Importers

The immediate relief from IEEPA tariffs is a win, but it is replaced by a new 10% surcharge under Section 122. You should:

Audit your entries: Identify which tariffs you paid were based on IEEPA to prepare for potential refund claims.

Stay Flexible: The trade environment remains volatile as the administration shifts its legal strategy to avoid future Court losses.

For Consumers

While the invalidation of billions in tariffs sounds like a price drop is coming, the introduction of the new 10% global tariff may offset those savings. Economists expect “trade-weighted” average tariff rates to remain higher than historical norms through 2026.

Summary of Key Impacts

Feature

IEEPA Tariffs (Struck Down)

Section 122 Tariffs (New)

Legal Status

Unconstitutional/Invalid

Currently Active

Current Rate

0% (Effective Feb 20, 2026)

10% (Effective Feb 24, 2026)

Duration

N/A

150 Days (Expires July 24, 2026)

Refunds

Likely, but process is TBD

No

The Supreme Court has drawn a firm line in the sand regarding the separation of powers. While the President still has significant tools to influence trade, the era of “unbounded” emergency tariffs appears to be over.

Starting or growing a business requires capital. While major banks are a common first thought, savvy entrepreneurs are increasingly looking toward credit unions. These member-owned cooperatives often provide a level of service and a focus on local community that large financial institutions can’t match. This guide will help you understand why a credit union might be the perfect partner for your small business loan and highlight some excellent examples.

Why Choose a Credit Union for Your Business Loan?

Unlike banks, which prioritize profit for shareholders, credit unions operate on a not-for-profit basis, existing solely to serve their members. This fundamental difference translates to several key advantages for business borrowers:

Competitive Rates and Fees: Credit unions often return their earnings to members through lower interest rates on loans and reduced fees. In a landscape where every dollar counts, these savings can be significant.

Personalized Service and Relationships: Loan officers at credit unions frequently live and work in the same community as you. They are more likely to take the time to understand your unique business plan, local market, and individual challenges, leading to a more collaborative and supportive lending process.

A Focus on the Local Economy: Credit unions thrive when their local communities thrive. By lending to small businesses, they are directly investing in local jobs, services, and growth. Your success is inherently linked to their mission.

A “Member-First” Mentality: You aren’t just a customer to a credit union; you are a member and a part-owner. This philosophy often results in a more empathetic and constructive approach, especially during tougher economic times. They may be more willing to work through setbacks and offer flexibility that larger banks wouldn’t consider.

Streamlined Decision-Making: Local credit unions often have a flatter organizational structure, meaning loan decisions can be made faster and by people who are directly accessible, rather than a centralized, distant corporate office.

Leading Examples (for inspiration, remember to research current 2026 options)

While specific rates and programs change rapidly, several credit unions consistently stand out for their robust and competitive small business lending offerings. As you conduct your research in March 2026, keep these institutions and their types in mind as a benchmark.

Navy Federal Credit Union: As the world’s largest credit union, Navy Federal (serving military members and their families) offers an extensive suite of business loans. They are well-known for their highly competitive interest rates, a diverse range of loan types (including SBA loans, term loans, and lines of credit), and a focus on assisting veterans and military families in their entrepreneurial journeys. If you meet the eligibility requirements, they are always a top contender to research.

America First Credit Union: Highly regarded in the Western United States, America First is a strong example of a regional powerhouse that delivers big-bank capabilities with credit union service. They offer a comprehensive range of commercial loans, including flexible terms, competitive rates, and specific expertise in industries common to their region. They often get high marks for technology integration and ease of doing business.

Digital Federal Credit Union (DCU): Though headquartered in the Northeast, DCU is another example of a credit union that serves members nationwide through its robust digital platform and community partnerships. They are often recognized for their competitive rates on both personal and business loan products and their simplified, tech-forward application processes, making them a good option for businesses looking for efficiency.

Local “Community-Hero” Credit Unions: This is often the best-kept secret. The strongest option for your business might be a credit union focused directly on your specific region or industry. These institutions possess unmatched understanding of your local market dynamics and may offer specialized loan programs designed to support niche local needs.

How to Find the Best Credit Union in March 2026

To find the ideal lending partner for your business right now, you need to conduct specific, up-to-the-minute research. The landscape shifts, and the “best” choice is always subjective to your unique needs. Follow these steps:

1. Gather Your Business Financials: The first step for any loan application is a solid business plan, detailed financial statements (P&L, balance sheet), and cash flow projections. This preparation shows you are serious and ready.

2. Define Your Loan Needs Precisely: How much capital do you need? What will the funds be used for (e.g., equipment, real estate, working capital)? Do you need a term loan or a flexible line of credit? Knowing this helps you narrow down which credit unions offer the most relevant programs.

3. Search for Eligibility First: Not everyone can join any credit union. Look for credit unions where you, your employees, or your business location make you eligible for membership. Some credit unions have broad eligibility (e.g., specific professions, community associations), making it easier than you might think.

4. Compare Rates, Terms, and Fees: Request specific quotes from at least 3-4 credit unions (and possibly one community bank for a point of comparison). Look beyond just the headline interest rate—examine the total cost of borrowing, including application fees, closing costs, and repayment terms.

5. Read Reviews and Testimonials: Talk to other local small business owners. Read online reviews. The experiences of your peers can provide invaluable insight into the speed of the loan process, the professionalism of the staff, and how supportive the institution is.

6. Schedule In-Person Meetings: If possible, meet with commercial loan officers from your top contenders. This allows you to ask detailed questions, present your business plan directly, and gauge whether they are truly interested in and enthusiastic about supporting your vision.

Choosing the right credit union for your business loan can make all the difference, not just in securing capital but in finding a long-term financial partner that understands your goals. By doing your homework and focusing on institutions that prioritize personalized service and community impact, you set your small business on the path to successful growth in March 2026 and beyond.

If you’re a business owner who has been dutifully paying the Trump administration’s “reciprocal” or “fentanyl” tariffs over the past year, February’s Supreme Court ruling in Learning Resources, Inc. v. Trump probably felt like a hard-won victory to get you a tariff refund. The Court’s 6-3 decision effectively dismantled the legal foundation for these tariffs, ruling that the President lacked the authority to impose them under the International Emergency Economic Powers Act (IEEPA).

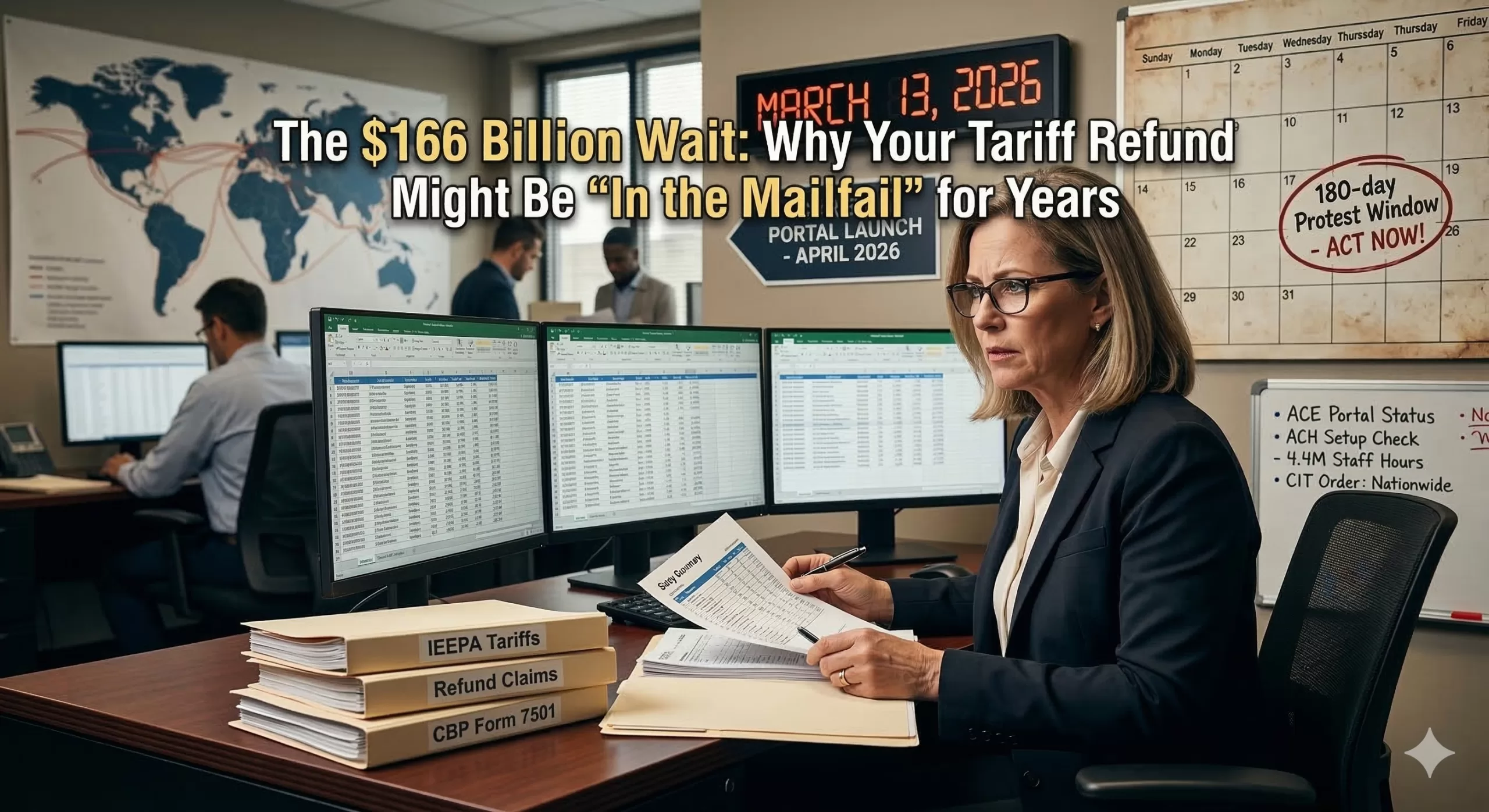

But don’t clear a spot in your budget for those refund checks just yet. While the Supreme Court was clear on the law, the White House and U.S. Customs and Border Protection (CBP) are signaling that returning that money—totaling an estimated $166 billion—will be anything but fast.

The “Logistical Nightmare” Defense

The administration’s current stance on refunds can be summarized in one word: Complexity. In recent court filings and public statements, officials have laid out a daunting timeline for processing the millions of entries subject to refunds. Here is the current state of play:

The 4.4 Million Hour Problem: CBP officials recently testified that manually processing the 53 million individual entries affected by the ruling would require roughly 4.4 million staff hours.

The “ACE” Upgrade: To avoid a decades-long wait, the government is rushing to build a new automated system within the Automated Commercial Environment (ACE) platform. While they hope to have a “self-service portal” ready by mid-April 2026, there are no guarantees it will work seamlessly on day one.

Validation Hurdles: Even with automation, the government insists on a “review period” for every refund to ensure importers haven’t violated other customs laws. Treasury Secretary Scott Bessent has warned that the process could take “years to litigate and get to a payout.”

A Tactical Delay?

Critics and trade lawyers aren’t buying the “it’s just too hard” excuse. Many see the administration’s warnings as a tactical move to hold onto revenue while they pivot to new trade strategies.

Just hours after the IEEPA tariffs were struck down, the administration invoked Section 122 of the Trade Act of 1974 to impose a new 10% “temporary import surcharge.” This 150-day “emergency” measure keeps the tariff pressure high while the administration searches for more permanent legal footing—and while the refund battle plays out in the Court of International Trade (CIT).

What This Means for Your Business

If you are among the thousands of importers owed money, the path forward is becoming a “choose your own adventure” of red tape:

The Wait-and-See Approach: You can wait for the CBP’s promised automated portal in April. However, this relies on the government’s ability to execute a massive tech project under extreme pressure.

The Litigation Path: Many law firms are advising clients to join the ongoing lawsuits at the CIT. While the court has ordered “nationwide” refunds, the government is expected to appeal, potentially dragging the case back to the Supreme Court.

The Interest Factor: One small silver lining? Under current law, these refunds should technically include interest. But as any business owner knows, interest is cold comfort when you need the cash flow now to pay suppliers or expand operations.

The Bottom Line

The Trump administration has made it clear: collecting tariffs is a “sprint,” but returning them is a “marathon.” With the government fighting the scope of refund orders and warning of massive administrative burdens, businesses should prepare for a long, litigious road to recovery.

As of March 2026, the path to recovering your share of the estimated $166 billion in invalidated IEEPA tariffs is finally taking shape. Following the Supreme Court’s ruling in Learning Resources, Inc. v. Trump, U.S. Customs and Border Protection (CBP) has committed to launching a streamlined refund functionality within the ACE (Automated Commercial Environment) platform by mid-April 2026.

However, this isn’t an automatic process. To ensure your business is at the front of the line—and to avoid the “4.4 million hour” manual processing delay the government warned about—you need to be “ACE-ready” today.

Phase 1: The “Digital Gateway” Requirements

The most significant change in 2026 is the mandatory transition to electronic refunds. As of February 6, 2026, the Treasury has ceased issuing paper checks for CBP refunds.

[ ] ACE Portal Account: Ensure your company has an active ACE Secure Data Portal account. If you haven’t logged in recently, check that it isn’t “inactive” or “voided,” as reactivation can take several days.

[ ] ACH Refund Enrollment: You must enroll in the Automated Clearing House (ACH) Refund program via the “ACH Refund Authorization” tab in the ACE Portal.

Note: If you have multiple Importer of Record (IOR) numbers, you must ensure each suffix is correctly enrolled.

[ ] U.S. Bank Account: Refunds must be deposited into a U.S. bank account. If you are a foreign importer, you must either establish a U.S. account or formally designate a third party (like a customs broker) via CBP Form 4811.

Phase 2: The Documentation Audit

When the “self-service” portal goes live in April, you will likely be required to file a declaration listing every entry for which you are claiming a refund. You should have the following data points organized and ready to upload:

[ ] Entry Summaries (CBP Form 7501): The “smoking gun” for every claim. You’ll need the entry number, entry date, and port code.

[ ] Specific Tariff Codes: Documentation must clearly separate IEEPA duties (the illegal ones) from “stacked” duties that remain legal, such as Section 301 (China) or Section 232 (Steel/Aluminum) duties.

[ ] Proof of Payment: Evidence that the duties were actually paid to CBP (e.g., ACH debit confirmations or canceled checks).

[ ] Liquidation Status: Identify which entries are unliquidated, newly liquidated (within the last 180 days), or finally liquidated (older than 180 days). This determines whether you file a “Post Summary Correction” or an “Administrative Protest.”

Phase 3: The “Gotcha” Protection

The administration has warned they will use a “review period” to check for other compliance issues before issuing refunds. Don’t give them a reason to deny your claim.

[ ] Audit Your Classifications: Ensure the HTS codes used on your IEEPA entries were accurate. If CBP finds you undervalued goods or used the wrong code, they may “offset” your refund with new penalties.

[ ] Check Protest Deadlines: For entries that liquidated recently, the 180-day protest window is your primary legal protection. Do not let these lapse while waiting for the April portal launch.

Pro-Tip: The “Interest” Calculation

Under 19 U.S.C. § 1505(c), these refunds should include interest. However, CBP has stated that if they attempt a refund and it fails because your ACH info is incorrect, interest stops accruing. Double-check your banking details today to keep the meter running in your favor.

This letter is designed to be sent to your customs broker immediately. It specifically addresses the March 2026 procedural landscape, including the mandatory transition to electronic ACH refunds and the expected April launch of the CBP’s automated refund portal.

[Company Letterhead]

Date: March 13, 2026

To: [Customs Brokerage Name] Attn: [Broker Name / Compliance Department] Re: Urgent Request for IEEPA Tariff Refund Documentation & ACE Setup Verification

Following the U.S. Supreme Court’s February 20, 2026, ruling in Learning Resources, Inc. v. Trump and the subsequent March 4, 2026, order from the Court of International Trade (CIT), we are preparing our claims for the recovery of all duties paid under the International Emergency Economic Powers Act (IEEPA).

To ensure we are prepared for the CBP’s automated “self-service” refund portal launch in mid-April 2026, please provide the following and confirm our account status by [Insert Date – Suggest 5 business days]:

1. Data Retrieval: Entry Summary (ES-003) Report

Please generate and transmit an ACE Entry Summary Detail Report (ES-003) in Excel format for all entries filed under our Importer of Record (IOR) number(s) from February 4, 2025, to February 24, 2026.

Specifically, please ensure the report captures all entries containing the following IEEPA-related HTSUS codes:

9903.01.XX (Reciprocal/Fentanyl-related measures)

9903.02.XX (Country-specific IEEPA measures)

2. Documentation Package for Validation

For each affected entry, please assemble a digital folder containing:

CBP Form 7501 (Entry Summary)

Commercial Invoices (specifically highlighting any IEEPA duty line items)

Proof of Payment (ACH debit confirmations or payment receipts)

3. Electronic Refund (ACH) Verification

Per the Electronic Refunds Interim Final Rule that went into effect on February 6, 2026, we understand that paper checks are no longer being issued.

Please confirm if our account currently designates you (the broker) as the “4811 Notify Party” for refunds.

If you are the designated recipient, please provide written confirmation that your firm is fully enrolled in the CBP ACH Refund Program to prevent our refunds from being placed in “Reject Status.”

4. Liquidation and Protest Monitoring

While we await the automated portal, please provide a list of any affected entries that have liquidated within the last 150 days. We wish to ensure that administrative protest deadlines (180 days from liquidation) are monitored so we do not lose our legal right to these refunds during the government’s 45-day portal development period.

Please confirm receipt of this request and let us know if you require any further authorization to proceed.

Here is a list of the specific IEEPA-related tariff codes that were invalidated by the Supreme Court’s February 20, 2026, ruling. You can include this list as an addendum to your letter to help your broker filter your entry summaries more effectively.

IEEPA Refund Reference Codes

The following Chapter 99 subheadings were used to implement the now-invalidated IEEPA duties between February 4, 2025, and February 24, 2026.

Region / Category

ACE / HTS Code

Details & Invalidated Rates

China

9903.01.25

Fentanyl-related supply chain (10% duty)

China

9903.01.63

Reciprocal trade measures (Rates varied: 84% to 125%)

Mexico

9903.02.XX

Southern Border measures (25% base; 10% on potash)

Canada

9903.02.XX

Northern Border measures (35% base; 10% on energy)

Global

9903.01.34

Reciprocal “Baseline” Tariff (10% global rate)

Brazil

9903.02.40

Non-exempted goods (40% “free speech” tariff)

India

9903.02.25

Russian Oil/secondary measures (25% on India-origin)

Important Filter Notes for your Broker:

The “USMCA” Distinction: Note that goods that qualified for USMCA (United States-Mexico-Canada Agreement) were generally exempt from these IEEPA codes. Your broker should focus on entries where the USMCA preference was not claimed or was denied.

The “Section 122” Switch: Remind your broker that entries made after 12:01 a.m. ET on February 24, 2026, are likely subject to the newSection 122 10% surcharge. These are not currently eligible for the IEEPA refund and should be kept on a separate ledger.

Interest Accrual: Under 19 U.S.C. § 1505(c), interest should be calculated from the date of deposit of the estimated duties to the date of the refund.

When we think of the massive oil tankers carving through the turquoise waters of the Persian Gulf, we usually focus on the millions of barrels of crude they carry or the geopolitical weight of the Strait of Hormuz. But behind every voyage is an invisible, multi-layered shield of paper and promise: Maritime Insurance.

In the high-stakes environment of 2026, where regional tensions have sent shockwaves through energy markets, understanding how these vessels are protected is more than just a lesson in finance—it’s a window into how global trade survives in a crisis.

1. The Trinity of Protection

Insuring a $150 million vessel carrying $100 million worth of oil isn’t a “one-and-done” policy. It is built in three primary layers:

Hull and Machinery (H&M)

Think of this as the “comprehensive” insurance for the ship itself. It covers physical damage to the vessel’s structure and engines caused by “perils of the sea”—collisions, groundings, fires, or heavy weather.

Who provides it? Commercial insurers (often via the Lloyd’s of London market).

Protection and Indemnity (P&I)

This is unique to the shipping world. Instead of a traditional company, shipowners join P&I Clubs—mutual associations where members pool their money to cover third-party liabilities.

What it covers: Oil spills (pollution), crew injuries, and damage to docks or other ships.

Why it matters: In the event of a catastrophic leak in the Gulf, the P&I club provides the billions of dollars needed for cleanup.

War Risk Insurance

This is the “hot” layer. Standard H&M policies specifically exclude damage from weapons of war, mines, or terrorism. To sail into the Persian Gulf, owners must purchase a separate War Risk policy.

The “Listed Areas”: The Joint War Committee (JWC) in London designates high-risk zones. Once a ship enters these waters, its standard coverage is suspended, and a special “voyage premium” kicks in.

2. The “Additional Premium” Spike

In stable times, war risk insurance is a negligible cost. However, in the current 2026 climate—marked by recent escalations—the math has changed drastically.

When the Strait of Hormuz is designated a high-risk zone, insurers charge an Additional War Risk Premium (AWRP).

Normal rates: Historically around 0.01% to 0.05% of the ship’s value.

Current 2026 rates: We have seen spikes reaching 1% to 5% (or even 10% for “missile magnet” vessels with specific national ties).

The Reality Check: For a tanker worth $130 million, a 1% premium means the owner must pay $1.3 million just for a single seven-day transit through the Gulf.

3. 2026: The Rise of Government Backstops

The most significant shift this year has been the intervention of national governments. When private insurers find the risk “unpriceable” or “opaque,” they may stop offering coverage entirely, which effectively halts oil flow.

To prevent a global energy collapse, we are seeing:

U.S. Reinsurance Plans: The U.S. International Development Finance Corp (DFC) recently announced a $20 billion reinsurance program to provide a “safety net” for commercial insurers.

Sovereign Guarantees: Countries like India or China may provide state-backed insurance for their own flagged vessels to ensure their energy security remains intact when the private market retreats.

4. Why This Matters to You

You might not own a tanker, but you feel the insurance market every time you visit the gas station. When insurance premiums jump from $200,000 to $2,000,000 per trip, that cost is passed down the supply chain. If the “invisible shield” of insurance disappears, the tankers stop moving, and the world’s energy supply enters a chokehold.

Maritime insurance isn’t just a legal requirement; it is the financial lubricant that allows the world’s most dangerous—and essential—trade route to stay open.

When a massive oil spill occurs in the Persian Gulf, the response isn’t just about booms and skimmers—it’s about a highly choreographed financial “waterfall” designed to handle billions of dollars in claims.

In the context of the current 2026 escalations, the International Group of P&I Clubs (IG) and global compensation regimes are facing their most significant test since the 1990s.

1. The P&I “Claims Waterfall” (2026/27 Structure)

If a member vessel spills oil, the money for cleanup and compensation flows through a specific hierarchy. For the 2026 policy year, the limits are structured to handle “mega-spills”:

Tier

Amount

Source of Funds

Individual Club Retention

First $10 million

The specific P&I Club the ship belongs to (e.g., Gard, Skuld).

The Pool

$10 million – $100 million

Shared among all 12 P&I Clubs in the International Group.

Market Reinsurance (GXL)

$100 million – $1.1 billion

Global reinsurers (lead by AXA XL in 2026).

Overspill Layer

Up to ~$9.8 billion

A “catch-all” where all member shipowners globally are taxed to pay the claim.

Crucial Note for 2026: While general P&I cover can reach nearly $10 billion, oil pollution claims are strictly capped at $1 billion per incident under standard P&I rules. If damages exceed $1 billion, the international “Fund” system takes over.

2. The Three-Tier Compensation Regime

When a spill exceeds what the shipowner’s insurance can pay, international conventions (which most Gulf nations are party to) kick in:

Tier 1: The Civil Liability Convention (CLC). This is the shipowner’s P&I insurance (up to the $1 billion cap). It is “strict liability,” meaning the owner pays even if the spill wasn’t their “fault,” provided it wasn’t an act of war.

Tier 2: The 1992 IOPC Fund. If the damage exceeds the shipowner’s limit, this fund (financed by oil importers, not shipowners) pays out additional compensation.

Tier 3: The Supplementary Fund. Provides a third layer of compensation for major disasters, bringing the total available to approximately $1.15 billion.

3. The 2026 “Act of War” Complication

There is a massive legal “elephant in the room” right now. Under the CLC and P&I rules, shipowners and their insurers are not liable for oil pollution if the spill was caused directly by an “act of war, hostilities, civil war, or insurrection.”

The Current Crisis Scenario:

As of March 2026, several tankers (like the one off the coast of Kuwait last week) have been damaged by explosions.

If it’s an accident: The P&I “Waterfall” works as described above.

If it’s a missile/mine (Act of War): The standard P&I Club may deny the claim. This is why the War Risk Insurance you asked about earlier is so critical. It “buys back” that pollution coverage specifically for war events.

The “Blue Card” System

Even in 2026’s volatility, ships must carry a “Blue Card” issued by their P&I Club. This is a certificate of financial responsibility that proves to Gulf coastal states (like Saudi Arabia or the UAE) that there is a billion-dollar guarantee behind that ship, regardless of the geopolitical climate.

4. 2026 Market Update: Coverage Suspensions

As of March 5, 2026, several major P&I clubs (including NorthStandard and the American Club) have issued 72-hour cancellation notices for certain “non-poolable” war risk covers in the Gulf.

What this means: While the “mutual” (core) insurance remains, the extra “war-time” pollution cover is being moved to a “buy-back” basis, often costing charterers up to $30,000 per week just to maintain the same level of protection they had for $25,000 per year in 2025.

In the wake of the escalations earlier this month, the maritime insurance market effectively seized up. Standard war risk premiums skyrocketed from 0.25% to over 1.5% of a vessel’s value, and many insurers issued 72-hour cancellation notices, essentially “grounding” the global tanker fleet.

To break this deadlock, the U.S. government launched a massive intervention on March 6, 2026. Here is how the new $20 Billion Reinsurance Backstop works and why it’s a radical shift in maritime finance.

1. The “Sovereign Backstop” Mechanics

Normally, the U.S. International Development Finance Corporation (DFC) focuses on infrastructure in developing nations. Under the new directive, it has pivoted to become the world’s largest “reinsurer of last resort” for the Persian Gulf.

The Waterfall: Private insurers (like Chubb, who was named lead partner yesterday, March 11) issue the primary policies to shipowners. If a tanker is hit, Chubb pays the claim, but the DFC “backstops” the loss, reimbursing the insurance company for the most extreme payouts.

The Rolling Fund: The DFC is providing $20 billion on a rolling basis. This means as voyages successfully complete and the risk expires, that capacity is “recycled” to cover the next wave of ships.

Targeted Coverage: The program focuses specifically on Hull & Machinery and Cargo. Notably, early reports suggest it may exclude certain pollution liabilities if a ship is sunk, leaving that risk to the P&I Clubs.

2. Why the Government Stepped In

Private markets like Lloyd’s of London are built on “priceable risk.” When the risk of a missile strike becomes a “near certainty” rather than a “possibility,” private premiums become so expensive they are effectively a “no.”

By offering insurance at what the administration calls a “very reasonable price,” the U.S. is effectively subsidizing the cost of the voyage. This prevents a “risk premium” from being tacked onto every barrel of oil, which was threatening to push prices toward $200 a barrel last week.

3. The 2026 “Military-Insurance” Nexus

This isn’t just a financial program; it’s a tactical one. The DFC is coordinating directly with CENTCOM (U.S. Central Command).

Qualified Vessels: Not every ship gets this coverage. To qualify for the $20 billion pool, vessels must meet strict criteria, likely including adherence to specific “safe corridors” monitored by the U.S. Navy.

Naval Escorts: President Trump has linked the insurance backstop with the possibility of Navy escorts. The message to shipowners is: “We will insure the ship financially, and we will protect the ship physically.”

4. Current Market Friction

Despite the $20 billion infusion, the “Ghost Fleet” problem remains. Even with a guaranteed payout, many shipowners are hesitant because:

Crew Safety: Insurance pays for the ship, but it doesn’t protect the lives of the seafarers.

Force Majeure: Major energy players like QatarEnergy have already declared force majeure on LNG shipments this week, signaling that even with insurance, the physical danger is currently deemed too high for some.

The Big Picture

The center of maritime finance is momentarily shifting from London to Washington. By using the DFC’s balance sheet, the U.S. is attempting to “force” the market back to life. If successful, it could become a blueprint for how global trade is maintained in future “contested” waters.

As of March 12, 2026, the U.S. government’s $20 billion “Sovereign Backstop” has moved from a concept to a live operation. While the program is designed to get oil moving, the “fine print” of who is eligible reveals it is as much a tool of foreign policy as it is a financial product.

Based on the latest updates from the DFC (International Development Finance Corporation) and their lead partner, Chubb, here are the specific eligibility criteria and constraints:

1. The “Preferred Partner” Requirement

To access the government-backed rates, shipowners cannot go to just any broker.

American Underwriting: Policies must be issued through “Preferred American Insurance Partners.” Chubb was named the lead underwriter on March 11, with other U.S.-listed firms like AIG and Travelers reportedly joining the consortium.

Direct DFC Application: While Chubb handles the front-end, businesses must register directly with the DFC (via maritime@dfc.gov) to be vetted for the sovereign guarantee.

2. Vessel & Cargo Constraints

The program is not a “blanket” cover for every ship in the Gulf. It is highly surgical:

Prioritized Commodities: The backstop is explicitly for “strategic trade.” This includes Crude Oil, LNG, Gasoline, Jet Fuel, and Fertilizer. Ships carrying luxury goods or non-essential consumer electronics are currently pushed to the back of the line.

Flag Requirements: While “all shipping lines” are technically eligible, priority is being given to U.S.-flagged vessels and those belonging to Allied Nations (specifically citing the UK, Israel, and GCC partners like Saudi Arabia and the UAE).

The “Shadow Fleet” Exclusion: Any vessel with ties to sanctioned entities or the so-called “Ghost Fleet” (often used to bypass previous price caps) is strictly barred from the program.

3. The “CENTCOM” Compliance Hook

This is the most controversial eligibility rule. To be “qualified,” a vessel must agree to operational oversight by U.S. Central Command (CENTCOM):

Assigned Corridors: Ships must stay within CENTCOM-designated “Safe Lanes.” Deviating from these coordinates for any reason (other than immediate safety of life at sea) can void the insurance instantly.

Escort Readiness: Eligibility is often tied to the ship’s ability to integrate with naval escort protocols. If a ship refuses to take on a U.S. security liaison or follow convoy timing, the DFC backstop is retracted.

4. Financial Limits

Initial Focus: The $20 billion pool currently only covers Hull & Machinery (H&M) and Cargo.

The P&I Gap: Crucially, the backstop does not yet cover third-party pollution liability (P&I). This means if a ship is hit and causes a massive spill, the owner still relies on their traditional P&I Club. Because those clubs are currently issuing 72-hour cancellation notices for the Gulf, many owners are still refusing to sail despite the U.S. H&M guarantee.

The Current Standoff

Even with this $20 billion “shield,” the Persian Gulf remains at a near-standstill. As of this morning, over 200 ships remain at anchor outside the Strait. The insurance is available, but shipowners are now citing crew safety as the primary barrier—insurers can replace a ship, but they cannot replace a crew.

While the U.S. government’s $20 billion insurance backstop addresses the financial risk of losing a ship, the human element—the crew—has become the ultimate bottleneck. As of March 12, 2026, the “Crew War Risk” landscape has shifted into a high-stakes negotiation between unions and shipowners.

Here is the current breakdown of the incentives and rights for seafarers currently operating in or near the Persian Gulf:

1. The “Warlike Operations Area” (WOA) Designation

On March 5, 2026, the International Bargaining Forum (IBF) officially upgraded the Persian Gulf, the Strait of Hormuz, and the Gulf of Oman from a “High Risk Area” to a Warlike Operations Area (WOA). This is the highest possible danger classification in maritime labor law.

The Financial Incentives (The “Double Pay” Rule)

For seafarers who choose to stay on board during a transit, the pay structure has become extremely lucrative:

100% Basic Wage Bonus: Crews receive a bonus equal to their full basic salary for every day the ship is within the WOA.

5-Day Minimum: Even if the transit through the Strait takes only 12 hours, the IBF rules mandate a minimum of five days’ worth of bonus pay.

Death & Disability: Compensation for death or permanent disability resulting from an incident in this zone is doubled (often reaching payouts of $200,000 to $500,000 depending on rank).

The “Combat Pay” Reality: An Able Seaman (AB) who typically earns $2,500/month in the Gulf could effectively earn an extra $400–$500 for a single week’s transit, while a Master (Captain) could see a bonus of several thousand dollars for the same period.

2. The Right to Refuse (Repatriation)

This is the “escape hatch” that is currently causing the massive backlog of 700+ tankers. Under the WOA designation:

The Refusal Clause: Any seafarer has the legal right to refuse to sail into the Persian Gulf.

Free Repatriation: If they refuse, the shipping company must fly them home at the company’s expense from the last “safe” port (often Fujairah or Muscat).

Two-Month Severance: In addition to the flight home, the seafarer is entitled to two months of basic wage as compensation for the loss of their contract.

3. The 2026 “Humanitarian Emergency”

Despite the high pay, we are seeing a mass exodus of crews. As of this week:

35,000 Stranded: Over 20,000 commercial seafarers and 15,000 cruise passengers are currently “trapped” in the Gulf.

Repatriation Gridlock: While crews have the right to leave, regional airspace closures and port lockdowns mean there are effectively no flights available to get them out.

The “Mental Health” Toll: Unions like the ITF are warning that the combination of missile threats and the inability to go home is creating a psychological crisis on board the “Ghost Fleet” currently anchored off the coast of Oman.

4. The IRGC’s “Permission” System

A new complication emerged yesterday (March 11): The IRGC Navy has declared that all vessels must seek Iranian permission to transit the Strait.

Crew Risk: Ships that ignore this “permission” (following U.S. orders to stay in “Safe Lanes”) are being specifically targeted.

The Choice: Crews are now caught between two “Safe Lanes”—the one protected by the U.S. Navy and the one “permitted” by Iran. For many seafarers, no amount of “Double Pay” is worth being the target of a USV (Unmanned Surface Vessel) strike.

Contains information related to marketing campaigns of the user. These are shared with Google AdWords / Google Ads when the Google Ads and Google Analytics accounts are linked together.

90 days

__utma

ID used to identify users and sessions

2 years after last activity

__utmt

Used to monitor number of Google Analytics server requests

10 minutes

__utmb

Used to distinguish new sessions and visits. This cookie is set when the GA.js javascript library is loaded and there is no existing __utmb cookie. The cookie is updated every time data is sent to the Google Analytics server.

30 minutes after last activity

__utmc

Used only with old Urchin versions of Google Analytics and not with GA.js. Was used to distinguish between new sessions and visits at the end of a session.

End of session (browser)

__utmz

Contains information about the traffic source or campaign that directed user to the website. The cookie is set when the GA.js javascript is loaded and updated when data is sent to the Google Anaytics server

6 months after last activity

__utmv

Contains custom information set by the web developer via the _setCustomVar method in Google Analytics. This cookie is updated every time new data is sent to the Google Analytics server.

2 years after last activity

__utmx

Used to determine whether a user is included in an A / B or Multivariate test.

18 months

_ga

ID used to identify users

2 years

_gali

Used by Google Analytics to determine which links on a page are being clicked

30 seconds

_ga_

ID used to identify users

2 years

_gid

ID used to identify users for 24 hours after last activity

24 hours

_gat

Used to monitor number of Google Analytics server requests when using Google Tag Manager