Your Tariff Refund

If you’re a business owner who has been dutifully paying the Trump administration’s “reciprocal” or “fentanyl” tariffs over the past year, February’s Supreme Court ruling in Learning Resources, Inc. v. Trump probably felt like a hard-won victory to get you a tariff refund. The Court’s 6-3 decision effectively dismantled the legal foundation for these tariffs, ruling that the President lacked the authority to impose them under the International Emergency Economic Powers Act (IEEPA).

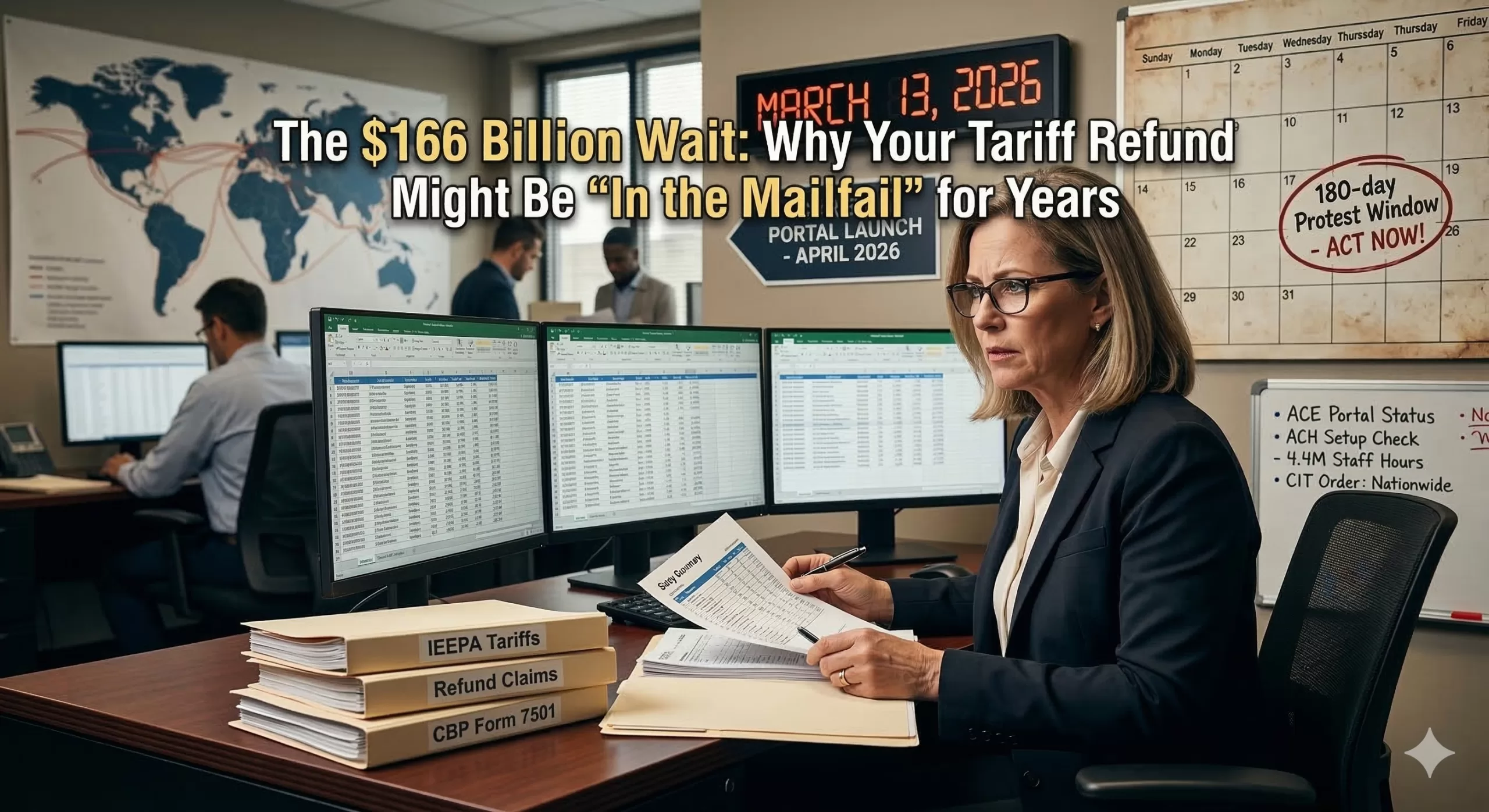

But don’t clear a spot in your budget for those refund checks just yet. While the Supreme Court was clear on the law, the White House and U.S. Customs and Border Protection (CBP) are signaling that returning that money—totaling an estimated $166 billion—will be anything but fast.

The “Logistical Nightmare” Defense

The administration’s current stance on refunds can be summarized in one word: Complexity. In recent court filings and public statements, officials have laid out a daunting timeline for processing the millions of entries subject to refunds. Here is the current state of play:

- The 4.4 Million Hour Problem: CBP officials recently testified that manually processing the 53 million individual entries affected by the ruling would require roughly 4.4 million staff hours.

- The “ACE” Upgrade: To avoid a decades-long wait, the government is rushing to build a new automated system within the Automated Commercial Environment (ACE) platform. While they hope to have a “self-service portal” ready by mid-April 2026, there are no guarantees it will work seamlessly on day one.

- Validation Hurdles: Even with automation, the government insists on a “review period” for every refund to ensure importers haven’t violated other customs laws. Treasury Secretary Scott Bessent has warned that the process could take “years to litigate and get to a payout.”

A Tactical Delay?

Critics and trade lawyers aren’t buying the “it’s just too hard” excuse. Many see the administration’s warnings as a tactical move to hold onto revenue while they pivot to new trade strategies.

Just hours after the IEEPA tariffs were struck down, the administration invoked Section 122 of the Trade Act of 1974 to impose a new 10% “temporary import surcharge.” This 150-day “emergency” measure keeps the tariff pressure high while the administration searches for more permanent legal footing—and while the refund battle plays out in the Court of International Trade (CIT).

What This Means for Your Business

If you are among the thousands of importers owed money, the path forward is becoming a “choose your own adventure” of red tape:

- The Wait-and-See Approach: You can wait for the CBP’s promised automated portal in April. However, this relies on the government’s ability to execute a massive tech project under extreme pressure.

- The Litigation Path: Many law firms are advising clients to join the ongoing lawsuits at the CIT. While the court has ordered “nationwide” refunds, the government is expected to appeal, potentially dragging the case back to the Supreme Court.

- The Interest Factor: One small silver lining? Under current law, these refunds should technically include interest. But as any business owner knows, interest is cold comfort when you need the cash flow now to pay suppliers or expand operations.

The Bottom Line

The Trump administration has made it clear: collecting tariffs is a “sprint,” but returning them is a “marathon.” With the government fighting the scope of refund orders and warning of massive administrative burdens, businesses should prepare for a long, litigious road to recovery.

As of March 2026, the path to recovering your share of the estimated $166 billion in invalidated IEEPA tariffs is finally taking shape. Following the Supreme Court’s ruling in Learning Resources, Inc. v. Trump, U.S. Customs and Border Protection (CBP) has committed to launching a streamlined refund functionality within the ACE (Automated Commercial Environment) platform by mid-April 2026.

However, this isn’t an automatic process. To ensure your business is at the front of the line—and to avoid the “4.4 million hour” manual processing delay the government warned about—you need to be “ACE-ready” today.

Phase 1: The “Digital Gateway” Requirements

The most significant change in 2026 is the mandatory transition to electronic refunds. As of February 6, 2026, the Treasury has ceased issuing paper checks for CBP refunds.

- [ ] ACE Portal Account: Ensure your company has an active ACE Secure Data Portal account. If you haven’t logged in recently, check that it isn’t “inactive” or “voided,” as reactivation can take several days.

- [ ] ACH Refund Enrollment: You must enroll in the Automated Clearing House (ACH) Refund program via the “ACH Refund Authorization” tab in the ACE Portal.

- Note: If you have multiple Importer of Record (IOR) numbers, you must ensure each suffix is correctly enrolled.

- [ ] U.S. Bank Account: Refunds must be deposited into a U.S. bank account. If you are a foreign importer, you must either establish a U.S. account or formally designate a third party (like a customs broker) via CBP Form 4811.

Phase 2: The Documentation Audit

When the “self-service” portal goes live in April, you will likely be required to file a declaration listing every entry for which you are claiming a refund. You should have the following data points organized and ready to upload:

- [ ] Entry Summaries (CBP Form 7501): The “smoking gun” for every claim. You’ll need the entry number, entry date, and port code.

- [ ] Specific Tariff Codes: Documentation must clearly separate IEEPA duties (the illegal ones) from “stacked” duties that remain legal, such as Section 301 (China) or Section 232 (Steel/Aluminum) duties.

- [ ] Proof of Payment: Evidence that the duties were actually paid to CBP (e.g., ACH debit confirmations or canceled checks).

- [ ] Liquidation Status: Identify which entries are unliquidated, newly liquidated (within the last 180 days), or finally liquidated (older than 180 days). This determines whether you file a “Post Summary Correction” or an “Administrative Protest.”

Phase 3: The “Gotcha” Protection

The administration has warned they will use a “review period” to check for other compliance issues before issuing refunds. Don’t give them a reason to deny your claim.

- [ ] Audit Your Classifications: Ensure the HTS codes used on your IEEPA entries were accurate. If CBP finds you undervalued goods or used the wrong code, they may “offset” your refund with new penalties.

- [ ] Check Protest Deadlines: For entries that liquidated recently, the 180-day protest window is your primary legal protection. Do not let these lapse while waiting for the April portal launch.

Pro-Tip: The “Interest” Calculation

Under 19 U.S.C. § 1505(c), these refunds should include interest. However, CBP has stated that if they attempt a refund and it fails because your ACH info is incorrect, interest stops accruing. Double-check your banking details today to keep the meter running in your favor.

This letter is designed to be sent to your customs broker immediately. It specifically addresses the March 2026 procedural landscape, including the mandatory transition to electronic ACH refunds and the expected April launch of the CBP’s automated refund portal.

[Company Letterhead]

Date: March 13, 2026

To: [Customs Brokerage Name] Attn: [Broker Name / Compliance Department] Re: Urgent Request for IEEPA Tariff Refund Documentation & ACE Setup Verification

Following the U.S. Supreme Court’s February 20, 2026, ruling in Learning Resources, Inc. v. Trump and the subsequent March 4, 2026, order from the Court of International Trade (CIT), we are preparing our claims for the recovery of all duties paid under the International Emergency Economic Powers Act (IEEPA).

To ensure we are prepared for the CBP’s automated “self-service” refund portal launch in mid-April 2026, please provide the following and confirm our account status by [Insert Date – Suggest 5 business days]:

1. Data Retrieval: Entry Summary (ES-003) Report

Please generate and transmit an ACE Entry Summary Detail Report (ES-003) in Excel format for all entries filed under our Importer of Record (IOR) number(s) from February 4, 2025, to February 24, 2026.

Specifically, please ensure the report captures all entries containing the following IEEPA-related HTSUS codes:

- 9903.01.XX (Reciprocal/Fentanyl-related measures)

- 9903.02.XX (Country-specific IEEPA measures)

2. Documentation Package for Validation

For each affected entry, please assemble a digital folder containing:

- CBP Form 7501 (Entry Summary)

- Commercial Invoices (specifically highlighting any IEEPA duty line items)

- Proof of Payment (ACH debit confirmations or payment receipts)

3. Electronic Refund (ACH) Verification

Per the Electronic Refunds Interim Final Rule that went into effect on February 6, 2026, we understand that paper checks are no longer being issued.

- Please confirm if our account currently designates you (the broker) as the “4811 Notify Party” for refunds.

- If you are the designated recipient, please provide written confirmation that your firm is fully enrolled in the CBP ACH Refund Program to prevent our refunds from being placed in “Reject Status.”

4. Liquidation and Protest Monitoring

While we await the automated portal, please provide a list of any affected entries that have liquidated within the last 150 days. We wish to ensure that administrative protest deadlines (180 days from liquidation) are monitored so we do not lose our legal right to these refunds during the government’s 45-day portal development period.

Please confirm receipt of this request and let us know if you require any further authorization to proceed.

Best regards,

[Your Name] [Your Title] [Company Name]

Contact Factoring Specialist, Chris Lehnes

Learn how to obtain some of your tariff refund now

Here is a list of the specific IEEPA-related tariff codes that were invalidated by the Supreme Court’s February 20, 2026, ruling. You can include this list as an addendum to your letter to help your broker filter your entry summaries more effectively.

IEEPA Refund Reference Codes

The following Chapter 99 subheadings were used to implement the now-invalidated IEEPA duties between February 4, 2025, and February 24, 2026.

| Region / Category | ACE / HTS Code | Details & Invalidated Rates |

| China | 9903.01.25 | Fentanyl-related supply chain (10% duty) |

| China | 9903.01.63 | Reciprocal trade measures (Rates varied: 84% to 125%) |

| Mexico | 9903.02.XX | Southern Border measures (25% base; 10% on potash) |

| Canada | 9903.02.XX | Northern Border measures (35% base; 10% on energy) |

| Global | 9903.01.34 | Reciprocal “Baseline” Tariff (10% global rate) |

| Brazil | 9903.02.40 | Non-exempted goods (40% “free speech” tariff) |

| India | 9903.02.25 | Russian Oil/secondary measures (25% on India-origin) |

Important Filter Notes for your Broker:

- The “USMCA” Distinction: Note that goods that qualified for USMCA (United States-Mexico-Canada Agreement) were generally exempt from these IEEPA codes. Your broker should focus on entries where the USMCA preference was not claimed or was denied.

- The “Section 122” Switch: Remind your broker that entries made after 12:01 a.m. ET on February 24, 2026, are likely subject to the new Section 122 10% surcharge. These are not currently eligible for the IEEPA refund and should be kept on a separate ledger.

- Interest Accrual: Under 19 U.S.C. § 1505(c), interest should be calculated from the date of deposit of the estimated duties to the date of the refund.