Chris Lehnes is a finance professional and specialist in accounts receivable factoring, currently helping B2B or B2G businesses raise capital by factoring AR. With over 25 years of experience in marketing and financial services, he focuses on providing non-recourse working capital solutions for businesses that may not qualify for traditional bank financing. [1, 2, 3, 4]

Professional Expertise

Lehnes operates primarily as an educator and intermediary in the factoring industry, helping companies bridge cash flow gaps through their receivables. His expertise includes: [1, 2]

- Target Industries: He provides funding for a variety of sectors including energy, healthcare, manufacturing, and staffing.

- Specialized Funding: He specializes in “challenging deals,” such as startups, companies with high customer concentrations, or those with weak personal credit.

- Financial Content: Lehnes is a prolific content creator, maintaining a YouTube channel focused on factoring tutorials, market analysis, and audiobook summaries related to leadership and business psychology. [1, 2, 3, 4, 5]

Career & Background

- Education: He studied Economics at Lafayette College and attended River Dell Regional High School.

- Online Presence: He actively shares insights on LinkedIn and Twitter/X, often discussing economic barometers like lumber price fluctuations and their impact on residential construction.

- Public Speaking: He frequently appears on podcasts and webinars, such as the Credit on the Go Podcast, to explain the strategic benefits of factoring. [1, 2, 3, 4, 5]

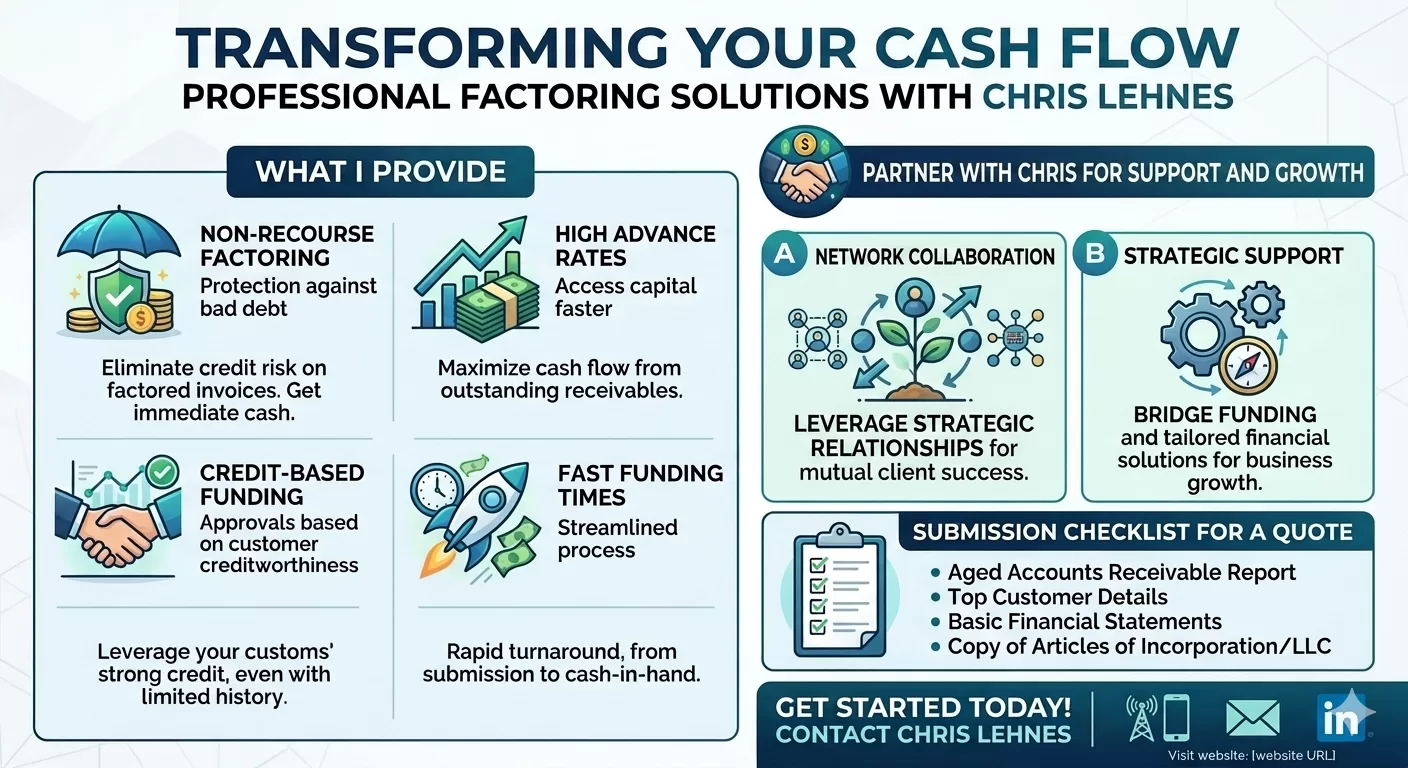

Chris Lehnes manages non-recourse factoring at Versant Funding, where the primary requirement for funding is the credit quality of the account debtor (the customer paying the invoice), rather than the financial strength of the business itself. [1, 2, 3]

Funding Criteria & Terms

- Sales Volume: Targets companies with B2B or B2G sales ranging from $100,000 to $30 million per month.

- Non-Recourse Protection: Versant assumes the credit risk; if the customer fails to pay due to insolvency, the business is not required to reimburse Versant.

- Flexible Concentration: Unlike many lenders, Lehnes often facilitates deals with 100% customer concentration, where a business has only one major client (e.g., a large municipality or multinational corporation).

- Funding Speed: Deals can often be funded within one week because traditional underwriting of the borrower’s balance sheet is not required.

- Typical Fees: Costs are generally around 2.5% of the invoice amount for each month it remains outstanding.

- Excluded Industries: Generally does not factor for the medical (provider-side) or construction industries. [1, 2, 3, 4, 5, 6, 7]

Latest Market Analysis (2025–2026)

Lehnes frequently updates his YouTube and Substack with analyses of the broader economy. Recent highlights include:

- Monetary Policy: He recently analyzed the Federal Reserve’s decision to maintain interest rates, discussing the “higher for longer” outlook and its pressure on small business borrowing costs.

- Economic Risks: His 2025–2026 content focuses on navigating stagflation and recession risks, specifically how businesses can use factoring to survive trade wars and tariff shifts.

- Industry Deep Dives: Recent updates cover the growth of SaaS factoring and funding for energy industry suppliers. [1, 2, 3, 4, 5]

Chris Lehnes frequently facilitates complex funding through Versant Funding LLC, often solving liquidity crises for businesses that traditional banks might reject. [1, 2]

Selected Case Studies

- $30 Million Furniture Manufacturer (2025): Provided a massive non-recourse facility to replace a non-renewed loan from a previous factor. This deal supported the company through a significant corporate restructuring.

- $1.4 Million Auto Equipment Manufacturer (2026): Funded a company supplying global automotive giants. Despite the client’s slow-paying receivables, Versant scaled the facility automatically because the customers were “the strongest on the planet”.

- $3 Million Housewares Distributor (2025): Stepped in when the client’s existing factor imposed funding limits that prevented them from fulfilling new orders. Versant consolidated existing loans and provided an advance against all outstanding receivables.

- $1.8 Million Adolescent Group Home (2024): Originated a facility for a newly formed social services provider. Because state and county organizations pay slowly, this factoring arrangement provided the necessary liquidity for them to expand into new regions.

- Energy Sector Support (2026): Recently focused on the oil and gas industry, helping suppliers bridge working capital gaps caused by the long payment cycles of major energy corporations. [1, 2, 3, 4, 5, 6, 7, 9]

Contact Information

You can reach Chris Lehnes directly for a pre-qualification review or to discuss a specific transaction:

- Phone: 203-664-1535

- Email: clehnes@VersantFunding.com or chris@chrislehnes.com

- Office: Versant Funding Main Office at 561-405-4101 [1, 2, 3, 4]

Chris Lehnes and Versant Funding prioritize non-recourse factoring because it allows them to fund high-growth or struggling businesses based solely on their customers’ creditworthiness rather than the business’s own financial history. [1, 2]

Recourse vs. Non-Recourse Factoring

The primary difference is who bears the financial risk if a customer fails to pay an invoice. [1, 2]

- Recourse Factoring: This is the most common and typically the least expensive option. Under this arrangement, if your customer does not pay their invoice within a set period (usually 60–90 days), your business is responsible for buying back that invoice or replacing it with a fresh one. You retain the ultimate credit risk.

- Non-Recourse Factoring: In this model, the factoring company (like Versant) assumes the credit risk. If your customer becomes insolvent or files for bankruptcy, you are not required to pay back the advanced funds. Because the factor takes on more risk, fees are typically higher, and they require strict credit approval of your customers. [1, 2, 3, 4, 5, 6, 7, 8, 9]

Referral Partnership Guidelines

Lehnes actively collaborates with intermediaries, including commercial loan brokers, accountants, and consultants, to source “difficult” deals that traditional banks cannot touch. [1, 2]

- Recurring Commissions: Unlike real estate or one-time loan fees, Lehnes offers recurring monthly commissions for the entire life of the deal. If a client factors for three years, the referral partner receives a check every month for those three years.

- Strategic Bridge: He encourages partners to use factoring as a short-term bridge (often 24 months) to help companies stabilize until they can qualify for bank financing or complete an equity raise.

- Simple Prequalification: To refer a client, you generally only need to provide the client’s industry and a list of their major customers (A/R Aging report). Because Versant does not require full financial audits of the borrower, pre-approval can happen very quickly. [1, 2, 3]

To move forward with a deal for Chris Lehnes at Versant Funding, you typically need a streamlined submission package because they do not underwrite the borrower’s financials—only the collateral (the invoices).

1. Required Documents for a Quote

You can typically get a term sheet or preliminary proposal by submitting just two or three items.

- Current A/R Aging Report: This is the most critical document. It must show the names of the customers (account debtors), the amounts they owe, and how long the invoices have been outstanding (0-30, 31-60, 60-90 days).

- Customer List with Limit Requests: A list of the specific customers the client wants to factor, including their addresses and the amount of credit limit requested for each. Versant uses this to run credit checks on the debtors.

- Sample Invoices: A few examples of the invoices they intend to factor to verify they represent completed work or delivered goods (not progress billing or guaranteed sales).

- Simple Application:

Next Step:

If you have a client ready, you can email the A/R Aging Report directly to chris@chrislehnes.com to request a term sheet.