Bloomingdale’s The iconic American chain, known for its curated selection, designer collaborations, and a certain “je ne sais quoi,” is thriving, even as rivals like Macy’s and Nordstrom face significant headwinds.

In a retail landscape dotted with defunct department stores and echoing food courts, one name seems to be bucking the trend:

So, what is it about Bloomingdale’s that has kept the store so relevant, so… resilient? Is it the famous little brown bags, or something more substantial? Let’s explore.

The Art of Curation

Bloomingdale’s has always been about the mix. They don’t just sell clothes; they present a point of view. A stroll through their stores isn’t a simple shopping trip; it’s an exploration of current trends, classic style, and unexpected finds.

Unlike other department stores that can feel overwhelmed with inventory, Bloomingdale’s feels edited. Their buyers seem to possess an unerring knack for spotting what’s next and bringing it to their customers first. This creates an unparalleled level of trust and loyalty.

Designer Collaborations That Matter

Long before every brand had a collaboration, Bloomingdale’s was pioneering this approach. Their partnerships with designers, both established and emerging, are legendary. These collections offer customers a chance to own pieces from coveted labels at a more accessible price point.

These collaborations don’t just drive traffic; they build excitement and a sense of exclusivity. You feel like you’re part of something, a member of the “in-the-know” crowd. This is a crucial element of Bloomingdale’s’ brand identity.

A Focus on Experience

In an age of online shopping, Bloomingdale’s understands that they need to offer something that Amazon can’t. That “something” is experience. They invest heavily in creating vibrant and inviting store environments.

From in-store events and trunk shows to the signature cafes and bars, Bloomingdale’s is designed to be a destination. They’re creating a community, a place where people can gather, socialize, and connect with other fashion enthusiasts.

The Power of Omni-Channel

While Bloomingdale’s physical stores are a cornerstone of their success, they haven’t ignored the digital landscape. Their online presence is strong, integrated with their physical footprint. They offer services like buy online, pick up in-store, and free shipping.

This seamless omni-channel approach allows customers to shop in a way that suits their needs. They’re not forced to choose between online and in-store; they can have both.

The Ultimate Question

So, is Bloomingdale’s truly defying the demise of department stores? The answer is a bit of a yes and no.

Yes, Bloomingdale’s is doing well. They’re making a profit, they’re growing, and they have a strong brand identity. But they’re also operating in a market that is increasingly volatile. Consumer habits are changing rapidly, and the retail landscape is unpredictable.

Bloomingdale’s has built a strong foundation, but they can’t afford to rest on their laurels. They need to continue to innovate, to evolve, and to meet the changing needs of their customers.

Perhaps the real question is not whether Bloomingdale’s is defying the demise, but whether they are adapting to the new retail reality. And on that score, the answer seems to be a resounding yes.

A Brighter Future for Department Stores?

The success of Bloomingdale’s offers a glimmer of hope for the future of department stores. It demonstrates that with the right strategy, a commitment to quality and curation, and a focus on experience, it’s possible not just to survive but to thrive.

But it’s important to remember that not all department stores are created equal. Bloomingdale’s success is a testament to its unique brand identity, its loyal customer base, and its forward-thinking management team. It’s not a formula that can easily be replicated.

Ultimately, the demise of department stores is not inevitable. It’s about a failure to adapt. Bloomingdale’s is proof that with a little creativity and a lot of hard work, department stores can continue to be a vibrant part of the retail landscape for years to come.

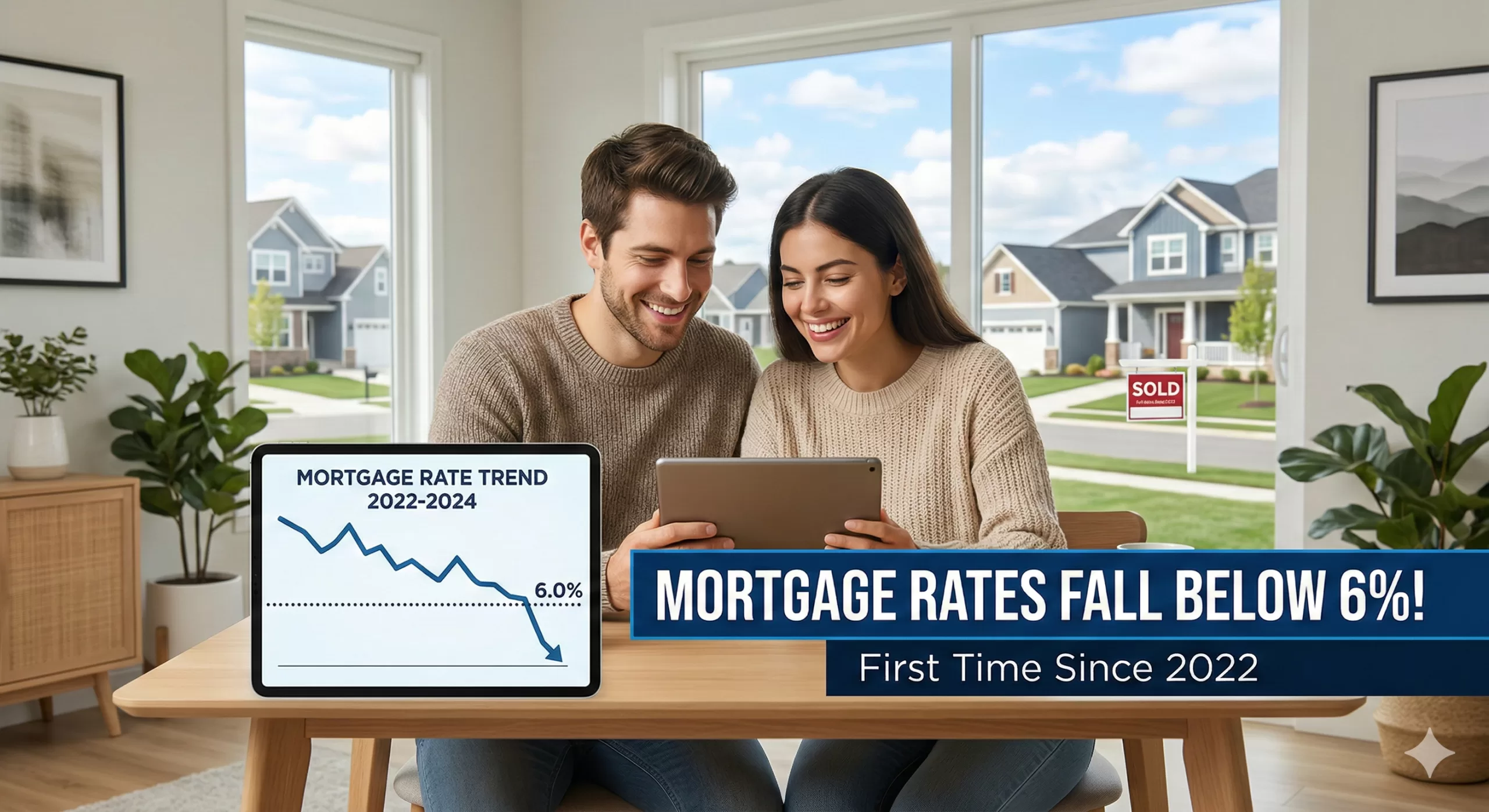

Mortgage Rates – The housing market has seen a welcome shift! Mortgage rates have fallen below 6% for the first time since 2022, offering a significant improvement for potential homebuyers. This news comes as a breath of fresh air after a period of steadily climbing rates that have put a strain on many budgets.

What Does This Mean for Potential Homebuyers?

The drop in mortgage rates translates directly into increased affordability for those looking to purchase a home. This can be beneficial in several ways:

Lower Monthly Payments: A lower interest rate means a smaller portion of your monthly payment goes towards interest, reducing your overall housing cost.

Increased Buying Power: With lower monthly payments, you may be able to qualify for a larger loan amount, potentially allowing you to purchase a more expensive home.

Refinancing Opportunities: Existing homeowners who currently have a higher mortgage rate may be able to refinance their loan and save money on their monthly payments.

Why Are Mortgage Rates Falling?

While the exact reasons behind the rate drop are complex, several factors may be contributing to the trend:

Lower Inflation: Inflation has shown signs of cooling down, which can influence interest rates.

Economic Growth: While economic growth has been moderate, some signs suggest it may be slowing, which can also affect mortgage rates.

Changes in the Bond Market: Bond yields, which are closely tied to mortgage rates, have also seen a decline.

What Should You Do Now?

If you’ve been on the fence about buying a home, this could be an excellent time to re-evaluate your options. Here are some steps to consider:

Get Pre-Approved for a Mortgage: This will give you a clear idea of how much you can borrow and help you understand your monthly payment.

Shop Around for Rates: Different lenders offer varying rates, so it’s essential to compare offers from multiple institutions.

Consider Your Long-Term Goals: While the lower rates are attractive, it’s crucial to ensure that buying a home is the right decision for your long-term financial goals.

Important Note: It’s important to remember that mortgage rates are subject to change based on economic conditions and other factors. While the current trend is encouraging, it’s essential to stay informed about any potential shifts in the market.

Conclusion:

The drop in mortgage rates below 6% is a significant development for the housing market, offering some much-needed relief to potential homebuyers and homeowners alike. If you’ve been considering buying a home, this could be the right time to take action. With lower monthly payments and increased buying power, you may be closer to achieving your homeownership goals than you thought. However, it’s crucial to act carefully and seek professional advice to make the best decision for your individual situation.

Primary Data Sources

Freddie Mac (Primary Mortgage Market Survey): The ultimate source for the 5.98% figure. Freddie Mac released its weekly report on February 26, 2026, confirming that the 30-year fixed-rate mortgage dipped below 6% for the first time in approximately 3.5 years.

The Federal Reserve (FRED): Used to verify historical trends, specifically confirming that the last time rates were at this level was September 8, 2022 (when they were 5.89%).

CBS News: Provided context on the White House’s initiatives (such as the $200 billion mortgage bond purchase plan) and expert commentary on the “spring home-buying season.”

Associated Press (AP): Detailed the influence of the 10-year Treasury yield on mortgage pricing and quoted housing economists regarding market entry for buyers and sellers.

Mortgage rates in 2026 forecast This video provides expert analysis on how these sub-6% rates impact monthly affordability and what to expect for the rest of the 2026 housing market

IEEPA Tariff While the Supreme Court invalidated the Administration’s ability to impose tariffs under IEEPA (International Emergency Economic Powers Act), it was deliberately silent with respect to refunds.

As the Administration’s stance is likely to be adversarial, it could take months if not years for businesses to receive IEEPA tariff refunds via conventional channels.

Prior to the Supreme Court Ruling, Hedge Funds were purchasing IEEPA tariff claims at an average of only 22% of the total claim due to the high risks involved. After the Ruling, due to mitigation of some of the uncertainty, they are currently purchasing claims at 40% to 45% of the total claim.

Instead of waiting 6, 12, 24 months or even longer to receive an IEEPA tariff refund, Hedge Funds can purchase claims within approximately 4 to 6 weeks depending on the quality of documentation assembled by the business.

How the Process of Selling an IEEPA Tariff Claim Works

Company X has paid ($10 Million) in tariffs since April 7, 2025Company X wants to de-risk prior to determination and finalization of the IEEPA tariff Refund Process.

Company X sells (50%, 100%, or some other percentage) of its tariff ‘claim’ to Buyer A in the form of a participation.

The Trade is nonrecourse to Company X as to the outcome of the Refund Process; but recourse to Company X only if the amount / validity of the claim is proven to be false, or too high.

Process for Selling IEEPA Tariff Claims:

Company X has paid $10 million in IEEPA Tariffs.

Company X agrees to “sell” its tariff claim to Buyer for 45% of the claim amount, i.e. $4.5 million..

Buyer sends Seller a Confirm, and then ultimately a Participation Agreement which will govern the transaction.

IMPORTANT – Company X retains its status as the “Plaintiff” / “Claimant” since these tariff claims are not transferable.

Buyer might ask Company X to commence litigation for the return of the IEEPA tariffs paid.

The rationale for this is that it is possible that only those parties who have commenced actual litigation are entitled to refunds.

Thus, Company X will need to commence litigation in order to receive their refund.Buyer will continue to monitor the situation and inform Company X of developments.If and when the refund is received on the claim, Company X will receive the refund and forward to the Buyer.

Key Points: Company X (as seller of the Claim) must be a financially healthy enough counterparty for Buyer A to enter into what could be a 2-to-3-year process of obtaining the refund.

Legal fees are split going forward based on risk percentage. If Company X sells 100% today, Buyer A will pay 100% of legal costs today.

Buyers are currently paying 40% to 45% to companies seeking to sell their IEEPA tariff claims. However, this is an evolving market and these percentages can either increase or decrease depending on the markets’ reaction to the Trump Administration’s expected obstructionism and the unresolved Court of International Trade’s procedural issues.

Prior to the Supreme Court decision, buyers were purchasing tariff claims at an average of 22% due to the high risks involved.

There would likely be an administrative process instituted such that companies that have paid these IEEPA tariffs will need to file special claims and wait to get refunded by the government. The process of receiving the refund payment from the government could take up to 12-to-18-to-24 months or even longer. Contact Chris Lehnes to learn if your client is a fit for this program

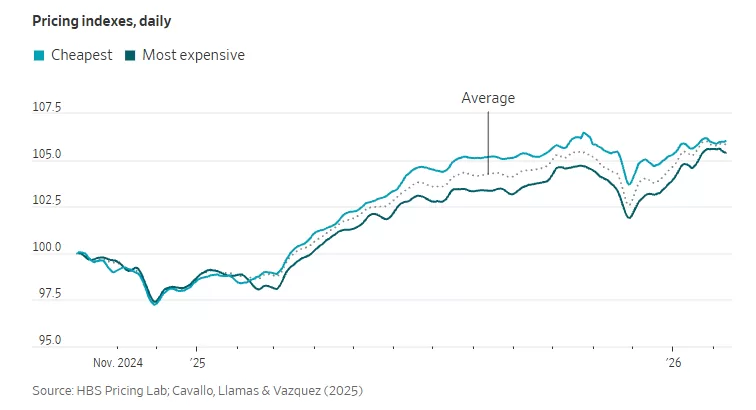

This details how investment firms are turning a legal and political mess into a new trading opportunity.

The situation stems from a recent Supreme Court ruling that tossed out several of President Trump’s sweeping tariffs. This has created a scramble for companies to claw back the levies they have already paid—estimated to be as high as $133 billion.

The Rise of “Claims Trading”: Large corporations (like retailers and manufacturers) that paid billions in tariffs are now selling the rights to their potential government refunds to Wall Street investors.

Why Companies Are Selling: Rather than waiting years for the government to process refunds or navigate complex litigation, companies are opting for immediate cash by selling their claims at a discount.

The Players: Specialist investment firms—including King Street Capital Management, Anchorage Capital Advisors, and Fulcrum Capital—are among those pouncing on these claims. They are betting that they can eventually collect the full refund from the Treasury, netting a significant profit.

Legal Uncertainty: The Supreme Court has not yet explicitly ruled on whether the government must issue refunds for the tariffs already collected. Despite this, investors are moving quickly to snap up these rights, treating them similarly to how they trade the debt of bankrupt companies.

The “Chaos” Factor: The process is currently a “long, drawn-out mess” with high administrative hurdles. Traders are effectively providing a “liquidity service” to companies that want the tariff money back on their balance sheets now rather than later.

In short, while the reversal of the tariffs has caused massive administrative and fiscal confusion for the government, Wall Street has identified it as a lucrative new asset class.

Factoring Proposal: After recently recovering from the devasting impacts of tariffs, this company requires PO financing to rebuild inventory. Their existing factor is uncooperative and must be replaced by Versant which has the ability to facilitate PO funding though a trusted partner.

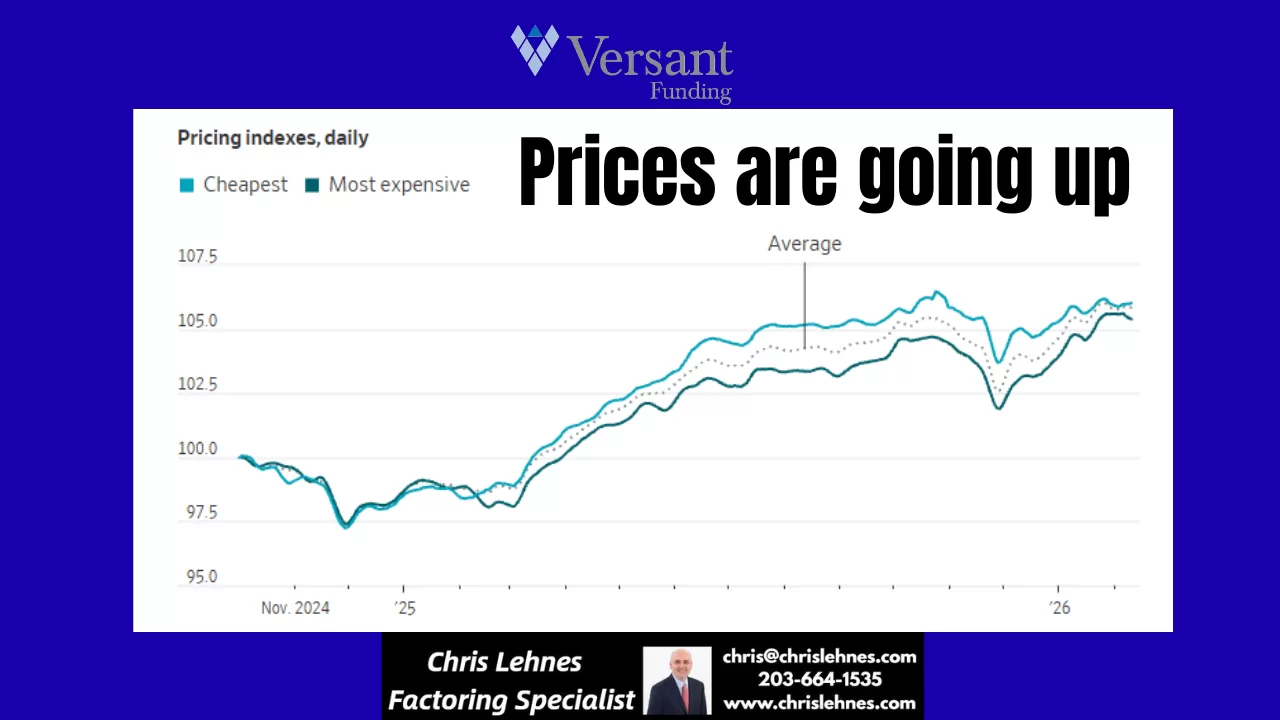

Remember that brief sigh of relief? The one where it felt like maybe, just maybe, the relentless march of price increases was slowing down? Well, if you’ve been to the grocery store, filled up your gas tank, or even just browsed online recently, you’ve probably noticed it: the break is over. Companies are jacking up prices again, and consumers are once again feeling the pinch.

For a while, many economists and analysts pointed to easing supply chain issues, stabilizing energy costs, and even a slight dip in consumer demand as potential signals that inflation was cooling. Some businesses even held the line on prices, perhaps hoping to retain market share or out of a genuine desire to give their customers a break.

But those days seem to be largely behind us. We’re seeing a resurgence in price hikes across a wide array of sectors. From everyday necessities to discretionary items, the numbers on the tags are climbing.

What’s Driving This Latest Surge?

Several factors are likely contributing to this renewed upward trend:

Persistent Input Costs: While some raw material costs have stabilized, others continue to be elevated. Labor costs are also a significant factor, with many businesses facing pressure to offer higher wages to attract and retain employees. These increased operational expenses often get passed on to the consumer.

Strong Consumer Demand (Still): Despite earlier predictions of a significant slowdown, consumer demand has proven remarkably resilient in many areas. When demand remains high, businesses have less incentive to lower prices and more leeway to raise them.

“Catch-Up” Pricing: Some companies might feel they absorbed increased costs for a period and are now playing catch-up, adjusting prices to reflect their sustained operational expenses.

Geopolitical Factors: Global events continue to create volatility in commodity markets, particularly for energy and certain raw materials, which inevitably impacts production and transportation costs.

Profit Margins: Let’s be honest, businesses are in the business of making a profit. If they perceive an opportunity to increase their margins without significantly impacting sales volume, many will take it.

What Does This Mean for You?

For the average household, this renewed wave of price increases means a continued squeeze on budgets. Discretionary spending may need to be curtailed further, and even essential purchases will require more careful planning. Savings might deplete faster, and the goal of financial stability could feel increasingly distant.

How Can Consumers Cope?

While we can’t control the broader economic forces at play, there are strategies consumers can employ to mitigate the impact:

Become a Savvy Shopper: Compare prices diligently, look for sales and discounts, and consider generic or store-brand alternatives.

Budgeting is Key: Revisit your budget and identify areas where you can cut back. Track your spending to understand exactly where your money is going.

Prioritize Needs vs. Wants: Distinguish between essential purchases and items that can be deferred or eliminated.

Support Local (Where Affordable): Sometimes local businesses, with lower overheads, can offer competitive pricing, or at least you’re supporting your community.

Advocate for Yourself: When possible, negotiate prices for services, or look for loyalty programs that offer discounts.

The “break” from rising prices was indeed short-lived. As companies continue to adjust their pricing strategies, it’s more important than ever for consumers to be vigilant, adapt their spending habits, and advocate for their financial well-being.

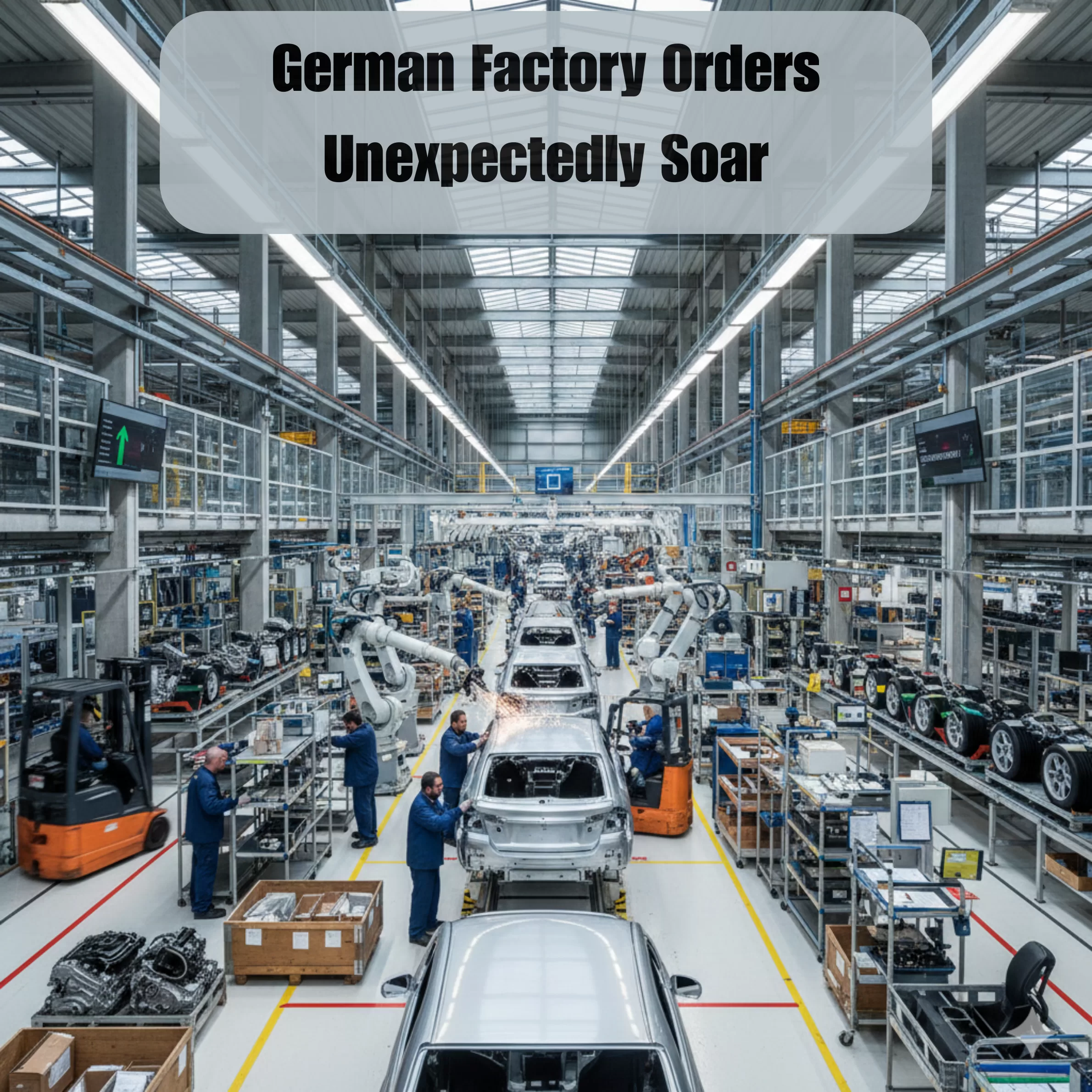

In a surprising turn of events, German factory orders in have shown an unexpected and robust surge, signaling a potentially stronger-than-anticipated rebound in the nation’s industrial sector. This latest data has instilled a renewed sense of optimism among economists and policymakers, suggesting that Europe’s largest economy might be on a more solid recovery path than previously estimated.

The Federal Statistical Office announced this morning that new factory orders jumped by a significant margin in the past month, far exceeding analyst expectations. This remarkable uptick follows a period of cautious growth and even some contractions, making the current surge all the more impactful. The increase was broad-based, with both domestic and international orders contributing substantially to the overall rise.

A Deeper Dive into the Numbers

The reported increase in orders was particularly driven by strong demand for capital goods, indicating that businesses are investing more in machinery and equipment – a key indicator of future production capacity and confidence. Intermediate goods also saw a healthy boost, suggesting renewed activity across various supply chains.

Economists are pointing to several factors contributing to this positive development. A resilient global demand, particularly from key trading partners, appears to be playing a significant role. Furthermore, a gradual easing of supply chain bottlenecks, which have plagued manufacturers for months, is allowing companies to fulfill orders more efficiently and take on new business.

Impact on the Broader Economy

This unexpected surge in factory orders is a shot in the arm for the German economy, which has been grappling with persistent inflation and the lingering effects of global uncertainties. A strong industrial sector is crucial for Germany’s economic health, as it is a major employer and a significant contributor to GDP. The improved outlook could lead to increased hiring, higher wages, and ultimately, stronger consumer spending.

Every February, Americans look forward to a Monday off, often marked by mattress sales and cherry pie. But the story of Presidents’ Day is more than just a break from work; it’s a quirky evolution of federal law, calendar shifting, and a bit of a tug-of-war between two of America’s most famous leaders.

It Started with George

Originally, this holiday had nothing to do with “Presidents” in the plural. It was strictly about George Washington.

After his death in 1799, his birthday (February 22) became a day of unofficial remembrance. By 1879, it became an official federal holiday for government workers in Washington, D.C., and by 1885, it expanded to the entire country. For decades, the logic was simple: Washington was the “Father of His Country,” so he got the day.

The Great Calendar Shift: The Uniform Monday Holiday Act

If you’re wondering why we never seem to celebrate on Washington’s actual birthday anymore, you can thank the late 1960s.

In 1968, Congress passed the Uniform Monday Holiday Act. The goal was practical, if a bit unromantic: move several federal holidays to predetermined Mondays to create more three-day weekends for the workforce.

The Goal: Boost industrial productivity by reducing mid-week disruptions and encourage consumer spending through long weekend travel and shopping.

When the law took effect in 1971, Washington’s Birthday was moved to the third Monday in February. Ironically, because of how the calendar falls, the holiday now never actually lands on Washington’s real birthday (February 22).

The “Lincoln” Factor

While Washington had the federal holiday, many states (especially in the North) also celebrated Abraham Lincoln’s birthday on February 12.

When the 1971 shift happened, there was a push to rename the day “Presidents’ Day” to honor both men—and eventually, all who served in the office. While the federal government still officially calls it “Washington’s Birthday,” the popular name “Presidents’ Day” took over the public consciousness by the mid-1980s, largely driven by retailers who found “Presidents’ Day Sales” to be a much more effective marketing tool.

How We Celebrate Today

Today, the holiday is a bit of a “choose your own adventure” for the 50 states:

Traditionalists: Some states still officially list it as “Washington’s Birthday.”

The Duo: Others, like Illinois, place a heavy emphasis on Lincoln.

The Inclusive: Most people treat it as a day to reflect on the presidency as an institution and the various leaders who have occupied the Oval Office.

Whether you’re spending the day studying Revolutionary War history or just catching up on sleep, you’re participating in a tradition that has evolved from a somber tribute into a celebration of American leadership.

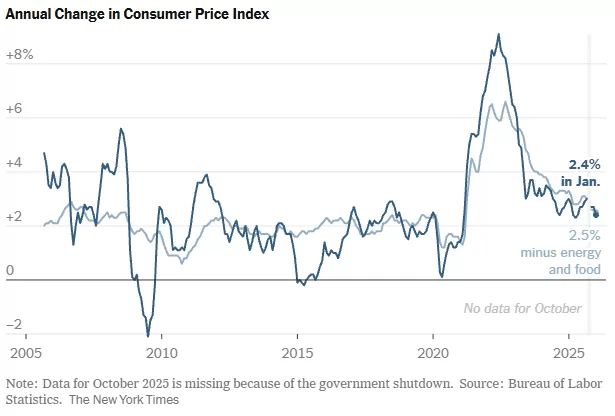

The latest economic data brings a sigh of relief for consumers and policymakers alike, as U.S. inflation has shown a more significant easing than anticipated at the beginning of the year. This positive development suggests that efforts to tame rising prices may be gaining traction, offering a glimmer of hope for greater economic stability in the months to come.

For much of the past year, inflation has been a persistent headwind, impacting everything from grocery bills to housing costs. The robust labor market, while a sign of economic strength, also contributed to upward price pressures. However, recent reports indicate a potential shift in this trend.

Several factors appear to be contributing to this welcome slowdown. Supply chain disruptions, which were a major catalyst for price increases, have largely improved. This has allowed for a more consistent flow of goods, reducing bottlenecks and associated costs. Additionally, the Federal Reserve’s aggressive monetary policy, including multiple interest rate hikes, seems to be having its intended effect of cooling demand and reining in inflationary expectations.

While the easing of inflation is certainly good news, it’s important to maintain a balanced perspective. The economy is a complex system, and various forces are constantly at play. Energy prices, geopolitical events, and shifts in consumer spending habits can all influence the trajectory of inflation. Therefore, continuous monitoring and adaptive policymaking will remain crucial.

What does this mean for the average American? For starters, it could translate into less pressure on household budgets over time. If the trend continues, we might see more stable prices for everyday goods and services, allowing purchasing power to stretch further. It also provides the Federal Reserve with more flexibility in its future policy decisions, potentially reducing the need for further aggressive rate hikes.

The journey to sustained price stability is an ongoing one, but the early signs from this year are undoubtedly encouraging. It’s a testament to the resilience of the U.S. economy and the effectiveness of concerted efforts to address inflationary pressures. As we move further into the year, economists and consumers alike will be watching closely to see if this promising trend continues, paving the way for a more predictable and stable economic environment.

Home Sales Take a January Dip: What Does It Mean for the Market?

The housing market, often a dynamic and unpredictable beast, just delivered a notable headline: home sales in January experienced their most significant monthly decline in nearly four years. This news might spark a bit of anxiety for some, and perhaps a glimmer of hope for others. But what’s truly behind this downturn, and what could it signal for the months ahead?

According to recent reports, the seasonally adjusted annual rate of existing home sales saw a substantial drop last month. This marks a notable shift after a period where the market showed some signs of stabilizing, or even modest recovery, in late 2023.

What’s Driving the Decline?

Several factors are likely at play in this January slump:

Mortgage Rate Volatility: While rates have come down from their peaks, they’ve also experienced some upward swings, creating uncertainty for prospective buyers. Higher rates directly impact affordability, pushing some buyers to the sidelines.

Persistent Inventory Shortages: Despite the dip in sales, the fundamental issue of low housing inventory remains a significant challenge in many areas. Fewer homes on the market mean less choice for buyers, and can still keep prices elevated, even with softening demand.

Seasonal Slowdown (Exacerbated): January is typically a slower month for real estate activity due to holidays and winter weather. However, the magnitude of this decline suggests more than just a typical seasonal lull. It could indicate that underlying market pressures are intensifying.

Affordability Challenges: The combination of elevated home prices and higher interest rates continues to stretch buyer budgets thin. For many, especially first-time homebuyers, the dream of homeownership remains a distant one.

Economic Uncertainty: Broader economic concerns, even if subtle, can influence consumer confidence. Worries about inflation, job security, or a potential recession can lead people to postpone major financial decisions like buying a home.

Is This the Start of a Larger Trend?

It’s crucial not to jump to conclusions based on a single month’s data. Real estate markets are complex and influenced by numerous variables. However, a decline of this magnitude certainly warrants close attention.

Potential for Price Adjustments: A sustained drop in demand, particularly if inventory levels begin to rise, could eventually lead to more significant price corrections in some markets. Buyers who have been waiting for prices to come down might see this as a positive sign.

Opportunity for Buyers? For those who are financially secure and ready to buy, a less competitive market could present opportunities. Fewer bidding wars and potentially more negotiating power could be on the horizon if the trend continues.

Impact on Sellers: Sellers might need to adjust their expectations. Pricing strategically and ensuring homes are in top condition will become even more critical in a market where buyers have more leverage.

Looking Ahead

The coming months will be telling. We’ll need to watch several key indicators:

Mortgage Rate Movements: Any significant and sustained drop in interest rates would likely bring buyers back into the market.

Inventory Levels: A notable increase in homes for sale would help alleviate pressure and potentially lead to more balanced market conditions.

Economic Data: Broader economic health, including inflation and employment figures, will continue to play a role in consumer confidence and housing demand.

While January’s numbers present a cautious start to the year for the housing market, they also highlight the ongoing adjustments and recalibrations happening. Whether this dip is a temporary blip or a harbinger of more significant changes remains to be seen, but it’s a clear reminder that the real estate landscape is always evolving.

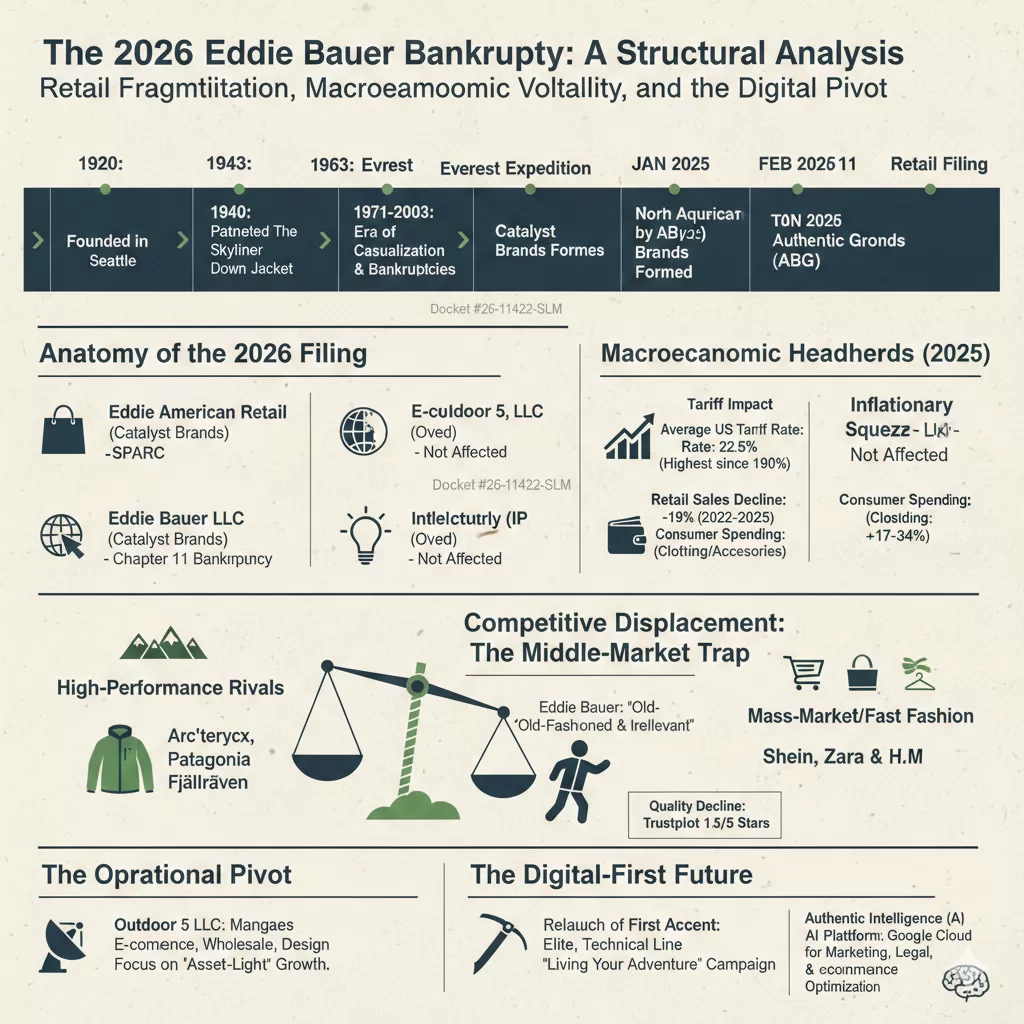

The 2026 Bankruptcy of Eddie Bauer: A Structural Analysis of Retail Fragmentation, Macroeconomic Volatility, and the Demise of the Traditional Outfitter

The voluntary filing for Chapter 11 bankruptcy protection by Eddie Bauer LLC on February 9, 2026, represents more than a singular corporate failure; it serves as a definitive case study in the structural fragmentation of legacy retail in the mid-2020s. This move, marking the third time the 106-year-old brand has sought creditor protection in a little over two decades, is the culmination of a sophisticated strategic carve-out executed within the complex ecosystem of modern brand management. While the physical store operations, housed under the Catalyst Brands umbrella, undergo a court-supervised wind-down or potential sale, the brand’s intellectual property, e-commerce, and wholesale divisions have been insulated from the filing. This analysis explores the causal mechanisms behind the 2026 filing, the macroeconomic headwinds of the preceding year, the competitive displacement of the brand, and the bifurcated future of the Eddie Bauer name in a digital-first economy.

The Anatomy of the 2026 Bankruptcy Filing

The filing in the United States Bankruptcy Court for the District of New Jersey under docket #26-11422-SLM specifically targets the retail operator of approximately 180 Eddie Bauer stores across the United States and Canada. The financial distress reported by the company is severe, with court documents indicating liabilities that could range from $1 billion to as high as $10 billion, set against assets valued at only $100 million to $500 million. At the time of the filing, the retail entity faced a critical liquidity crisis, reporting average weekly disbursements of approximately $1.6 million against a cash reserve of only $20 million.

A defining feature of this bankruptcy is its targeted scope. The Chapter 11 proceedings do not include Eddie Bauer’s e-commerce platforms, wholesale operations, manufacturing divisions, or international locations outside of North America. This structural insulation was achieved through a series of tactical transfers occurring just weeks before the filing. In January 2026, Authentic Brands Group (ABG), the owner of the Eddie Bauer intellectual property, transitioned the licenses for e-commerce and wholesale to a separate entity, Outdoor 5 LLC (Oved), effective February 2, 2026. This maneuver effectively separated the profitable digital and wholesale channels from the debt-burdened physical retail footprint, leaving the latter to navigate the bankruptcy process as a standalone entity.

Operational Segment

Entity Responsible (Feb 2026)

Bankruptcy Status

North American Retail Stores

Eddie Bauer LLC (Catalyst Brands)

Chapter 11 Filing

E-commerce & Digital Sales

Outdoor 5, LLC (Oved)

Not Affected

Wholesale & Manufacturing

Outdoor 5, LLC (Oved)

Not Affected

Intellectual Property (IP)

Authentic Brands Group (ABG)

Not Affected

International Operations

Various International Licensees

Not Affected

The retail operator entered into a Restructuring Support Agreement (RSA) with its secured lenders to facilitate what it calls a “dual-path” process. This strategy involves conducting immediate liquidation sales across its North American fleet while simultaneously seeking a “going concern” buyer for the physical store operations. If a suitable buyer is not secured by the court-mandated deadline of March 12, 2026, the company will proceed with an orderly total wind-down of its U.S. and Canadian brick-and-mortar presence by April 30, 2026.

Macroeconomic Catalysts: The 2025 Trade Regime and Inflationary Squeeze

While the internal structural issues of Eddie Bauer were longstanding, the “final blow” came from a series of macroeconomic shocks throughout 2025 that the company’s overleveraged business model could not absorb. CEO Marc Rosen of Catalyst Brands explicitly cited “ongoing tariff uncertainty” and persistent inflation as the primary accelerators of the retailer’s demise.

The 2025 Tariff Impact on the Apparel Sector

The trade environment of 2025 was characterized by aggressive new tariffs that fundamentally altered the cost structure of North American retail. Research from the Yale Budget Lab indicates that the overall average effective U.S. tariff rate reached 22.5 percent in 2025—the highest level recorded since 1909. These tariffs disproportionately targeted categories central to Eddie Bauer’s product mix, including apparel, footwear, and leather products.

Commodity Category

Short-Run Price Increase (2025)

Long-Run Projected Increase

General Apparel

17.0% – 34.0%

11.0% – 13.0%

Leather Products & Footwear

36.0% – 37.0%

12.0% – 13.0%

Textiles

21.0%

7.0%

These cost increases were rapidly passed on to consumers, pushing key price thresholds beyond what casual outdoor enthusiasts were willing to pay. For a brand like Eddie Bauer, which operated in the “middle-of-the-road” value segment, the inability to absorb these costs led to a significant collapse in discretionary spending. Data from Earnest Analytics revealed a 3.9 percent year-over-year drop in consumer spending at clothing and accessories establishments in early 2025, making it the worst-performing major retail segment of the year.

Inflationary Pressures and Consumer Sentiment

The residual effects of post-pandemic inflation further squeezed the profit margins of physical retail operations. Eddie Bauer’s retail sales saw a precipitous 19 percent decline between 2022 and 2025, driven by the increased cost of doing business and shifting consumer priorities. A survey conducted by Circana in October 2025 revealed that 38 percent of consumers intended to cut back on spending specifically due to tariff-induced price hikes, with clothing and footwear identified as the primary targets for reduced purchases. The combination of rising labor costs, increased rent in premium mall locations, and the higher cost of imported goods created a “sustained period of negative earnings” that ultimately made the retail entity unsustainable.

The Strategic Formation of Catalyst Brands

The formation of Catalyst Brands in January 2025 was an ambitious attempt to stabilize several struggling heritage labels through the economies of scale. This joint venture was created through the merger of SPARC Group—the operating partner for brands like Aéropostale, Brooks Brothers, Lucky Brand, and Nautica—and JCPenney. The venture brought together a portfolio of six iconic retail banners with combined annual revenue exceeding $9 billion.

The ownership structure of Catalyst Brands reflects a partnership between major mall landlords and brand management firms, including Simon Property Group, Brookfield Corporation, Authentic Brands Group, and Shein. This alliance was designed to leverage a robust distribution network of 1,800 store locations and 60,000 employees, with the hope that shared design, sourcing, and logistics capabilities would drive operational efficiencies.

Brand

Year Acquired by Catalyst/Predecessor

Original Founding Year

Eddie Bauer

2021 (by SPARC)

1920

Brooks Brothers

2020 (by SPARC)

1818

JCPenney

2020 (by Simon/Brookfield)

1902

Nautica

2018 (by SPARC)

1983

Aéropostale

2016 (by SPARC)

1987

Lucky Brand

2020 (by SPARC)

1990

Despite having $1 billion in liquidity at its launch, Catalyst Brands inherited a “challenged situation” at Eddie Bauer. Marc Rosen, the CEO of Catalyst Brands, noted that while the leadership team made significant strides in product development and marketing over the first year of the venture, these improvements could not be implemented fast enough to address the structural problems created over several decades. The bankruptcy of the Eddie Bauer retail operator suggests that the “zombie mall store” strategy—where landlords acquire their tenants to maintain occupancy—may have reached its financial limits in the face of the 2025-2026 economic headwinds.

Historical Context: The Erosion of a Technical Identity

The collapse of Eddie Bauer’s retail operations marks a stark departure from the brand’s origins as a premier technical outfitter. Founded by outdoorsman Eddie Bauer in Seattle in 1920, the company was responsible for some of the most significant innovations in outdoor gear of the 20th century.

The Legacy of Innovation (1920–1968)

Eddie Bauer’s early history was defined by a commitment to high-performance products, often developed out of personal necessity. After suffering hypothermia during a winter fishing trip, Bauer sought an alternative to heavy, water-logged wool garments. This led to the 1940 patent of “The Skyliner,” the first quilted goose-down-insulated jacket in the United States. This technical expertise earned the company massive government commissions during World War II, during which it manufactured over 50,000 B-9 Flight Parkas and 100,000 sleeping bags for the military. Notably, Eddie Bauer was the only government supplier granted permission to affix its logo to military-issue products.

This era of technical dominance culminated in the 1963 American Mount Everest Expedition, where Jim Whittaker wore Eddie Bauer gear to become the first American to summit the world’s highest peak. The brand’s creed—”To give you such outstanding quality, value, service and guarantee that we may be worthy of your high esteem”—was established during this period of innovation.

The Shift to Casual Apparel and Serial Ownership (1968–2021)

The retirement of Eddie Bauer in 1968 signaled the beginning of a decades-long transition from technical specialist to casual lifestyle brand. Successive ownership changes each prioritized different financial and market strategies, often at the expense of the brand’s performance-oriented heritage.

General Mills Era (1971–1988): Under the ownership of the food conglomerate, Eddie Bauer expanded its retail footprint to 60 stores and increasingly focused on casual apparel and home furnishings.

Spiegel Era (1988–2003): The brand underwent massive expansion but was dragged into bankruptcy along with its parent company in 2003.

Golden Gate Capital Era (2009–2021): After a second bankruptcy in 2009, private equity firm Golden Gate Capital acquired the brand, often focusing on cost-cutting measures and the expansion of the outlet channel.

By the time Authentic Brands Group acquired the brand in 2021, the product line had become “middle-of-the-road,” struggling to differentiate itself in an increasingly specialized market.

Competitive Displacement: The “Middle-Market Trap”

By 2025, the outdoor apparel market had become highly polarized, with consumers gravitating toward either high-performance specialist brands or trendy, low-cost athleisure. Eddie Bauer found itself caught in a “middle-market trap,” lacking the elite technical credibility of its high-end rivals while being unable to compete on price with mass-market discount retailers.

Technical Rivals and Brand Identity

Competitors such as Arc’teryx, Patagonia, and Fjällräven successfully built distinct identities that resonated with younger, tech-savvy consumers. While Eddie Bauer’s brand name remained well-known, it was increasingly perceived by younger shoppers as “old-fashioned and a bit irrelevant”.

Brand

Market Positioning

Key Strategy / Point of Difference

Arc’teryx

Elite Technical

Focus on alpine performance and “tech-wear” aesthetics

Patagonia

Activist / Heritage

Commitment to environmentalism and free lifelong repairs

Fjällräven

Trendy / Functional

Distinctive aesthetics and G-1000 material durability

Eddie Bauer

Traditional Casual

Reliance on outlets and perpetual 40% off discounting

The Decline of Quality and Service

A critical factor in Eddie Bauer’s loss of market share was a perceived decline in product quality. For an outdoor brand, whose value is intrinsically tied to the performance of its gear, this deterioration was particularly damaging. Industry analyst Neil Saunders of GlobalData Retail noted that the brand had not kept pace with the innovation cycles of its rivals.

By 2025, consumer sentiment reflected a significant loss of trust. Trustpilot ratings for the brand languished at 1.3 out of 5 stars, with shoppers citing frequent order errors, poor customer service, and materials that were “not like they used to be”. Furthermore, the watering down of the brand’s once-famous lifetime guarantee to a limited return policy in the mid-2010s had eroded a primary pillar of its customer loyalty.

Operational Fragmentation: The Digital Pivot and “Outdoor 5”

The 2026 bankruptcy of the retail operator must be viewed in the context of a broader shift toward an asset-light, digital-first business model. By carving out the profitable e-commerce and wholesale segments, Authentic Brands Group and its partners have essentially insulated the future of the Eddie Bauer brand from the failure of its physical stores.

The Role of Outdoor 5 LLC (Oved)

In January 2026, Outdoor 5 LLC (Oved) assumed responsibility for Eddie Bauer’s e-commerce, wholesale, design, and product development operations across the United States and Canada. Oved, a longtime partner of the brand for over two decades, brings specific expertise in the outdoor and performance apparel space. The company also manages other prominent brands in the Authentic portfolio, including Billabong, Quiksilver, and Hurley.

The strategic goal of this partnership is to align the brand’s channel mix with modern shopping behaviors. Authentic Brands Executive Vice President David Brooks noted that this approach provides the brand with greater flexibility, broader consumer access, and a more capital-efficient path to growth. By focusing on digital and wholesale channels, the brand can maintain its market presence while avoiding the high fixed costs associated with a 180-store physical retail fleet.

The Return of First Ascent

To revitalize the brand’s technical credibility, the new strategy centers on the relaunch of First Ascent, Eddie Bauer’s elite, performance-tested line. Originally developed for elite outdoor pursuits, the First Ascent collection features advanced technical specifications, including:

Waterproofing and taped seams.

High breathability and wind resistance.

800-fill down insulation.

The Spring 2026 campaign, “Living Your Adventure,” aims to integrate these high-performance features into the core brand offering, appealing to both serious adventurers and everyday outdoor enthusiasts. This return to technical roots is a direct response to the brand dilution that occurred during years of mall-dependent, casual-focused ownership.

Technological Integration: Authentic Intelligence and AI

A key component of the brand’s survival strategy in 2026 is the adoption of cutting-edge technology to drive efficiency and consumer engagement. Authentic Brands Group has partnered with Google Cloud to implement “Authentic Intelligence,” a proprietary AI platform built on Google’s Gemini and Vertex AI infrastructure.

This AI integration is being deployed across the brand’s operational spectrum to “supercharge collaboration and creativity” :

Marketing & Creative: AI-enhanced ad creative for brands in the portfolio has delivered up to 60 percent higher return on ad spend (ROAS) compared to traditional imagery.

Business Development: AI agents are used to build comprehensive profiles of potential licensing partners and accelerate lead generation.

Legal & Licensing: “Authentic Intelligence” assists with the rapid review and analysis of contracts, ensuring accuracy and faster turnaround times.

Digital Experience: Through a partnership with Pattern Group, the brand is expanding its presence on emerging platforms like TikTok Shop, utilizing AI-powered platforms to optimize conversion at scale.

This digital-first, data-driven approach is intended to provide clearer visibility into supply and demand, improve coordination across licensing partners, and ensure that the brand remains relevant in an environment that moves faster than traditional retail cycles.

Implications for Stakeholders: Landlords, Vendors, and Employees

The bankruptcy and potential wind-down of 180 physical store locations have immediate and severe consequences for the various stakeholders tied to the retail entity.

Landlord Risk and the “Dark Store” Threat

For shopping center owners, the filing by Eddie Bauer LLC creates significant operational and financial disruption. The company’s presence in approximately 180 locations means that landlords must navigate the risk of permanent vacancies. Key concerns for landlords include:

Lease Uncertainty: The uncertainty regarding whether the company will choose to assume or reject specific leases during the restructuring.

Co-tenancy Clauses: The closure of a prominent tenant like Eddie Bauer can trigger co-tenancy clauses in the leases of other tenants, allowing them to pay reduced rent or terminate their own leases.

Administrative Expenses: Landlords may face disruptions in rent payments and challenges regarding the recovery of administrative expenses during the bankruptcy process.

Vendor Exposure and Trade Credit

The fragmented corporate structure of Eddie Bauer creates a complex risk profile for vendors. Because the Chapter 11 filing only involves the store-operator entity, trade creditors must carefully identify which legal entity owes their outstanding invoices. Creditors of the retail operator may find their recoveries limited, as the most valuable assets—the intellectual property and the digital sales platforms—are held by entities not included in the bankruptcy proceedings.

Employee Impact

The potential closure of up to 180 retail locations puts thousands of jobs at risk across North America. While some employees involved in design and e-commerce may be absorbed by Outdoor 5 LLC as they scale their operations, the bulk of the retail staff faces the prospect of permanent displacement if a “going concern” buyer for the physical stores is not found by March 2026.

Conclusion: The Finality of the Mall-Based Era

The 2026 bankruptcy of Eddie Bauer’s retail operator represents the final chapter of the brand’s 106-year relationship with traditional American brick-and-mortar retail. The failure of the physical store model under Catalyst Brands is a clear signal that the combination of heavy debt, mall dependence, and macroeconomic volatility is no longer sustainable for heritage mid-market labels.

While the physical stores are being liquidated, the Eddie Bauer name itself is poised for a digital-first resurrection. The strategic bifurcation of the business—carving out the profitable digital and wholesale pieces while shedding the liabilities of the physical stores—is the new blueprint for legacy brand survival. By returning to its technical roots through the relaunch of First Ascent and leveraging AI-driven efficiencies, the brand owners hope to recapture the technical credibility that was lost during decades of casual-focused expansion. For the broader retail industry, the Eddie Bauer case serves as a cautionary tale: in the economy of the mid-2020s, a storied history and a well-known name are no longer enough to support the high fixed costs of a traditional retail fleet. The future of legacy retail is asset-light, digital-first, and increasingly separated from the physical malls that once defined it.

Contains information related to marketing campaigns of the user. These are shared with Google AdWords / Google Ads when the Google Ads and Google Analytics accounts are linked together.

90 days

__utma

ID used to identify users and sessions

2 years after last activity

__utmt

Used to monitor number of Google Analytics server requests

10 minutes

__utmb

Used to distinguish new sessions and visits. This cookie is set when the GA.js javascript library is loaded and there is no existing __utmb cookie. The cookie is updated every time data is sent to the Google Analytics server.

30 minutes after last activity

__utmc

Used only with old Urchin versions of Google Analytics and not with GA.js. Was used to distinguish between new sessions and visits at the end of a session.

End of session (browser)

__utmz

Contains information about the traffic source or campaign that directed user to the website. The cookie is set when the GA.js javascript is loaded and updated when data is sent to the Google Anaytics server

6 months after last activity

__utmv

Contains custom information set by the web developer via the _setCustomVar method in Google Analytics. This cookie is updated every time new data is sent to the Google Analytics server.

2 years after last activity

__utmx

Used to determine whether a user is included in an A / B or Multivariate test.

18 months

_ga

ID used to identify users

2 years

_gali

Used by Google Analytics to determine which links on a page are being clicked

30 seconds

_ga_

ID used to identify users

2 years

_gid

ID used to identify users for 24 hours after last activity

24 hours

_gat

Used to monitor number of Google Analytics server requests when using Google Tag Manager