The core themes and most important ideas presented in Hubert Joly’s book, “The Heart of Business.” The book advocates for a fundamental shift in business philosophy, moving away from a sole focus on profit to one centered on purpose and people, with the ultimate goal of transforming capitalism into a force for good.

I. The Crisis of Traditional Capitalism and the Imperative for Change

The sources highlight a critical juncture in the perception and practice of capitalism. Traditional models, heavily influenced by Milton Friedman’s doctrine of shareholder primacy, are seen as outdated, dangerous, and contributing to significant global issues.

Capitalism in Crisis: The current capitalist system is facing a crisis of legitimacy, with growing disenchantment, especially among younger generations. “Capitalism as we have known it for the past few decades is in crisis. More and more people hold the system responsible for social fractures and environmental degradation.” This sentiment is echoed by Salesforce CEO Marc Benioff, who declared, “Capitalism as we have known it is dead.”

The Flawed “Shareholder Primacy” Doctrine: The long-held belief that “the social responsibility of business is to increase its profits” (Milton Friedman) is actively challenged.

Profit as an Outcome, Not a Purpose: Joly argues that while profit is “vital,” it is “an outcome, not a purpose in itself.” It is “a symptom of other underlying conditions, not the condition itself.”

Misleading Metric: Profit alone fails to account for the true societal and environmental impact of a business. “The full cost of waste or carbon footprint on the environment does not appear on a financial statement, even though it is very real and can be very painful.”

Dangerous Focus: A singular focus on profit leads to short-term thinking, underinvestment in crucial assets (like people), stifles innovation, and can lead to corporate wrongdoing and scandals.

Antagonizes Stakeholders: This narrow focus alienates customers, who increasingly seek ethical and responsible companies, and employees, who are not motivated by “shareholder value.”

A Call for Reinvention: There is an urgent need to “rethink how our economic system works” and for “the necessary and urgent refoundation of business now under way.” Business leaders, investors, and institutions are increasingly recognizing this need for change, exemplified by Larry Fink’s 2018 letter to CEOs and the Business Roundtable’s 2019 statement embracing a broader stakeholder view.

II. The Purposeful Human Organization: A New Architectural Model for Business

Joly proposes a new framework for business centered on purpose and people, which he calls the “purposeful human organization.” This model emphasizes interdependence among all stakeholders and views companies as human entities.

Purpose at the Heart: The fundamental purpose of a company is “to contribute to the common good and serve all its stakeholders in a harmonious fashion.” This “noble purpose” (a term borrowed from Lisa Earle McLeod) is the “reason the company exists” and “the positive impact it is seeking to make on people’s lives and, by extension, its contribution to the common good.”

People at the Center: Employees are not merely “inputs” or “human capital,” but “individuals working together in support of an inspiring common purpose.” The “secret of business is to have great people do great work for customers in a way that delivers great results.”

The Causal Link: People ➞ Business ➞ Finance: This crucial sequence posits that excellence in developing and fulfilling employees leads to excellence in serving customers, which then leads to strong financial performance. “This makes profit an outcome of the first two imperatives.”

Declaration of Interdependence: The model views the company as a “community of their stakeholders,” where “all elements are connected in a closely interdependent, mutually reinforcing system.” This includes:

Employees: At the core, treated as individuals, valued for who they are, and provided an environment to thrive.

Customers: Seen as “human beings, not walking wallets,” and whose needs are genuinely understood and met.

Vendors: Partnered with collaboratively for mutual benefit and customer service.

Communities: Engaged with as vital for business flourishing and supported in addressing social issues.

Shareholders: Treated as human beings with diverse objectives, whose long-term interests are served by a purposeful and responsible business.

Benefits of the Approach:Expanded Horizons: A noble purpose creates an “expansive and enduring vision that opens up new markets and opportunities,” allowing companies to “weather change” and continuously strive to be their “best version.”

Inspiration and Engagement: A clear, meaningful purpose inspires employees and fosters deep loyalty from customers. “Cutting stones is tedious work. Building cathedrals is a noble purpose that inspires because it helps answer our human quest for meaning.”

Sustainability: This approach ensures that economic activity is sustainable, recognizing that “there can be no thriving business without healthy, thriving communities, and there can be no thriving business if our planet is on fire.”

Superior Financial Results: Companies that embrace these principles, referred to as “firms of endearment,” consistently outperform market averages. “Purpose indeed pays.”

III. The Meaning of Work: From Burden to Opportunity

A fundamental aspect of the purposeful human organization is a redefinition of work itself – shifting from a perception of work as a curse or a chore to an opportunity for meaning and fulfillment.

The Global Epidemic of Disengagement: “More than 8 out of 10 workers merely show up for work,” leading to “unfulfilled personal potential” and costing “a hefty $7 trillion in lost productivity.” This disengagement stems from a traditional view of work as a “necessary evil.”

Work as a Search for Meaning: Joly, drawing on personal reflection and various philosophical and religious traditions, argues that “work is love made visible” (Khalil Gibran) and “a fundamental element of what makes us human.” It is “an essential element of our humanity, a key to our search for meaning as individuals, and a way to find fulfillment in our life.”

Connecting Dreams to Purpose: Leaders must actively help employees connect their individual search for meaning with the company’s noble purpose. This involves asking “What drives you?” and understanding how personal dreams align with the organization’s mission, fostering “human magic.”

The Problem with Perfection: Striving for “perfection” is counterproductive. “Aiming for outstanding business performance is a good thing; expecting human perfection is not.”

Hinders Growth and Vulnerability: Perfectionism stifles feedback, limits human relationships, impedes innovation by fostering a fear of failure, and promotes a “fixed mindset” over a “growth mindset.”

Embracing Imperfection: Leaders must embrace their own vulnerabilities and imperfections to build genuine connections, trust, and create an environment where problems can be acknowledged and solved collaboratively. “There can be no genuine human connection without vulnerability, and no vulnerability without imperfection.”

IV. Unleashing Human Magic: The Ingredients for Extraordinary Performance

To realize the vision of the purposeful human organization, leaders must cultivate an environment that “unleashes human magic,” leading to “irrational performance.” This involves moving beyond outdated management approaches.

Beyond Carrots and Sticks: Traditional financial incentives are “outdated,” “misguided,” “potentially dangerous and poisonous,” and “hard to get right.” They focus on compliance rather than genuine engagement and tend to “narrow our focus and our minds” for complex tasks.

People as a Source, Not a Resource: The shift is to “view people as a source rather than a resource,” inspiring them by connecting with what genuinely matters to them.

Incentives’ True Role: Financial incentives can still be useful to “share good financial times with employees” and to “signal what is most important,” but not as primary motivators.

The Five Key Ingredients of Human Magic:Connecting Dreams: Aligning individual purpose and aspirations with the company’s noble purpose. This is achieved through articulating a “people-first philosophy,” exploring what drives individuals, capturing meaningful moments, sharing stories, and authentically framing the company’s purpose.

Developing Human Connections: Fostering environments where people feel respected, valued, and cared for. This involves treating everyone as an individual, creating safe and transparent environments, encouraging vulnerability, developing effective team dynamics, and promoting diversity and inclusion. “People do not give their best because they are blown away by superior intellect. How much of themselves they invest in their work is directly related to how much they feel respected, valued, and cared for.”

Fostering Autonomy: Empowering employees to control what they do, when, and with whom. This involves pushing decision-making “as far down as possible,” preferring participative processes, adopting agile work methods, and adjusting the degree of autonomy based on individual “skill and will.”

Achieving Mastery: Creating an environment that encourages continuous learning and becoming excellent at one’s work. This means focusing on “effort over results,” developing individuals rather than the masses, emphasizing coaching over traditional training, reassessing performance assessments to focus on development and strengths, and treating learning as a lifelong journey, while also “making space for failure.”

Putting the Wind at Your Back (Growth): Cultivating a mindset of possibilities and continuous growth, even in challenging environments. This involves thinking in terms of expansive possibilities, turning challenges into advantages, and always keeping purpose “front and center.” “Growth is an imperative. It creates space for promotion opportunities, productivity improvement without job loss, taking risks, and investing.”

V. The Purposeful Leader: A New Model for the 21st Century

The transformation of business requires a new kind of leader—one who embodies purpose, humanity, and authenticity, rejecting outdated myths of leadership.

Debunking Leadership Myths:Leaders as Superheroes: The idea of an “infallible leader prototype” who single-handedly saves the day is “outdated,” “inauthentic,” and “distant.” It also fosters an unhealthy ego. Leaders must aim to be “dispensable.”

Born Leaders: Leadership is not an innate ability but a set of skills and attributes that “can be learned” and developed over time.

Inability to Change: Leaders can and do change their approaches and philosophies over their careers, as evidenced by Joly’s own transformation.

The Five “Be’s” of Purposeful Leadership:Be clear about your purpose, the purpose of people around you, and how it connects with the purpose of the company: Understand personal drivers and how they align with organizational goals.

Be clear about your role as a leader: To “create energy, inspiration, and hope,” especially in challenging times. “You cannot choose circumstances, but you can control your mindset.”

Be clear about whom you serve: Leaders serve the front lines, colleagues, boards, and the people around them, not primarily their own ambition or ego. “The best leaders do not climb to the top… they are carried to the top.”

Be driven by values: Live by and explicitly promote values like honesty, respect, responsibility, fairness, and compassion, making them “part of the fabric of the business.”

Be authentic: Be “your true self, your whole self, the best version of yourself. Be vulnerable. Be authentic.” This fosters genuine social connection, which is at the heart of business.

VI. A Call to Action

The book concludes with a direct call to action for all stakeholders to contribute to this refoundation of business and capitalism.

For Leaders: Start with self-introspection to clarify personal purpose, be the change, and strive to be the best version of oneself.

For Companies: Cultivate a “fertile environment” where employees feel seen, belong, and matter before defining or redefining a noble purpose. Cocreate purpose and translate it into concrete strategic initiatives.

For Industry, Sector, and Community Leaders: Identify systemic changes to influence (e.g., racial inequality, environmental issues) and tackle them through collective action.

For Boards of Directors: Align responsibilities with purposeful leadership principles, ensuring that leadership selection, evaluation, compensation, and development reflect these values, and actively shape company culture.

For Investors, Analysts, Regulators, and Rating Agencies: Align evaluation and investment decisions with purposeful and human leadership principles, incorporating broader measures of performance like sustainability.

For Business Education Institutions: Incorporate purpose and human dimensions into leadership education, helping students become “better, more purposeful, more aligned, more human leaders, and not superheroes.”

In essence, “The Heart of Business” presents a compelling case, supported by practical experience and testimonials, that a focus on purpose and people is not just morally right but also the most powerful driver of long-term performance and value creation in the “next era of capitalism.”

The Heart of Business: A Comprehensive Study Guide

This study guide aims to help you review and deepen your understanding of Hubert Joly’s “The Heart of Business.” It covers the core philosophies, practical applications, and key insights presented in the book, as summarized by various leaders and through Joly’s own experiences.

Quiz: Short-Answer Questions

Answer each question in 2-3 sentences.

According to Hubert Joly, what is the primary purpose of a company, and how does this challenge traditional business thinking?

Explain the concept of “human magic” as described in the book. What are some of its key ingredients?

How does Joly argue against Milton Friedman’s doctrine regarding shareholder value?

Describe Joly’s personal transformation in his leadership approach. What specifically led him to shift from a purely analytical leader to a purpose-led one?

What role does vulnerability play in effective leadership, according to Joly and insights from Brené Brown?

How did Best Buy’s “Renew Blue” turnaround plan exemplify Joly’s principles of putting people first, even in a crisis?

What are the “five ‘Be’s” of purposeful leadership?

Explain why financial incentives are often considered “outdated” and “misguided” in modern business, according to the text.

How did Best Buy redefine its market and approach growth after its turnaround, moving away from traditional competitive strategies?

What is the significance of the “People ➞ Business ➞ Finance” sequence in Joly’s management philosophy?

Answer Key

Joly argues that the primary purpose of a company is not to maximize profit, but rather to contribute to the common good and serve all its stakeholders. This challenges traditional thinking by reprioritizing purpose and people over the singular pursuit of financial gain, treating profit as an outcome, not the goal.

“Human magic” is the extraordinary performance that results when individuals within a company are energized and engaged in support of a great cause. Key ingredients include connecting individual purpose with company purpose, developing authentic human connections, fostering autonomy, growing mastery, and nurturing a growth environment.

Joly argues against Friedman’s doctrine by stating that profit is merely an outcome and not a purpose itself. He asserts that an exclusive focus on profit is dangerous, can be a misleading measure of economic performance, antagonizes customers and employees, and is not good for the “soul” of the company or its people.

Joly’s personal transformation began when he felt disillusioned despite professional success, leading him to seek deeper meaning. Through spiritual exploration and observing effective leaders, he realized work could be a noble calling to serve others, shifting his focus from being the “smartest person at the table” to a passionate, compassionate, purpose-led leader.

Vulnerability is described as “the glue that binds relationships together,” fostering compassion, genuine belonging, and authentic connection. For leaders, showing vulnerability helps build trust, encourages others to be open, and allows for collective problem-solving rather than projecting an unrealistic image of perfection.

The “Renew Blue” plan prioritized growing the top line and cutting non-salary expenses before considering job cuts as a last resort. This approach maintained employee morale, recognized their vital role in the turnaround, and demonstrated a commitment to people as the company’s “lifeblood,” fostering energy and dedication.

The five “Be’s” of purposeful leadership are: Be clear about your purpose and its connection to the company’s; Be clear about your role as a leader; Be clear about whom you serve; Be driven by values; and Be authentic.

Financial incentives are considered outdated because they were designed for repetitive, manual tasks in an industrial age and are ineffective for today’s complex, creative work. They are misguided because they focus on compliance rather than fostering intrinsic motivation and engagement, often narrowing focus instead of encouraging innovation.

Best Buy redefined its market from solely selling consumer electronics hardware to addressing “human needs through technology,” including services and subscriptions. This expanded their market vision from approximately $250 billion to over $1 trillion, shifting from a focus on market share in a shrinking pie to creating new opportunities for growth and innovation.

The “People ➞ Business ➞ Finance” sequence highlights that focusing on the development and fulfillment of employees (People) leads to loyal customers and excellent products/services (Business), which then results in sustainable financial success (Finance). It positions profit as a result of a human-centric approach, rather than the initial driver.

Essay Format Questions (Do Not Answer)

Critically analyze Hubert Joly’s claim that “capitalism as we have known it for the past few decades is in crisis.” What evidence does he provide, and how does his “purposeful human organization” model propose to address these systemic issues?

Discuss the role of “imperfection” and “vulnerability” in Joly’s leadership philosophy. How do these concepts challenge traditional notions of leadership and contribute to both personal and organizational success, drawing on examples from his experience?

Examine the relationship between an individual’s personal purpose and a company’s “noble purpose.” How does Joly suggest leaders can effectively connect these two, and what are the benefits and potential pitfalls of this integration?

Compare and contrast Joly’s approach to managing during a “turnaround” versus a “growth strategy.” What core principles remain consistent, and what adaptations are necessary to effectively navigate each phase, according to his experiences at Best Buy?

Evaluate Joly’s arguments against the sole reliance on financial incentives for motivating employees. What alternative motivators does he propose, and how do these contribute to “human magic” and long-term performance?

Glossary of Key Terms

Human Magic: The extraordinary and often “irrational” performance that results when individuals within a company are deeply engaged, energized, and committed to a shared, inspiring purpose. It is unleashed when the right environment is created for people to flourish.

Noble Purpose: A term, borrowed from Lisa Earle McLeod, referring to the positive impact a company seeks to make on people’s lives and its contribution to the common good. It serves as the fundamental reason for the company’s existence, transcending mere profit.

People ➞ Business ➞ Finance: Hubert Joly’s management philosophy asserting that excellence in employee development and fulfillment (People) leads to loyal customers and superior products/services (Business), which then results in strong financial performance (Finance). Profit is thus an outcome, not the primary goal.

Purposeful Human Organization: A company viewed not as a soulless entity, but as a community of individuals working together towards an inspiring common purpose. This model prioritizes people and human relationships with all stakeholders, treating profit as a vital outcome.

Purposeful Leadership: A leadership style characterized by leaders who are clear about their own purpose, their role, whom they serve, are driven by values, and are authentic. It emphasizes putting purpose and people first to inspire and empower others.

Renew Blue: Best Buy’s turnaround plan, launched in 2012 under Hubert Joly’s leadership, focused on revitalizing the company by prioritizing people, customers, and operational improvements before considering drastic measures like widespread job cuts.

Shareholder Value Maximization: The traditional business doctrine, largely popularized by Milton Friedman, that asserts the sole social responsibility of a business is to increase profits for its shareholders. Joly critiques this as dangerous and misguided.

Stakeholder Capitalism: An evolving economic model where companies are accountable not only to shareholders but also to a broader group of stakeholders, including employees, customers, suppliers, and communities, and are expected to generate value for all.

VUCA World: An acronym (Volatile, Uncertain, Complex, Ambiguous) used to describe the rapidly changing and challenging economic environment of today, where agility, innovation, collaboration, and speed are crucial for success.

Vulnerability: The capacity to be open, authentic, and imperfect, which, according to Joly and Brené Brown’s research, is essential for building genuine human connections, trust, and fostering a supportive work environment.

Rate Cut – Over the course of this year, the U.S. economy has shown resilience in a context of sweeping changes in economic policy. In terms of the Fed’s dual-mandate goals, the labor market remains near maximum employment, and inflation, though still somewhat elevated, has come down a great deal from its post-pandemic highs. At the same time, the balance of risks appears to be shifting.

In my remarks today, I will first address the current economic situation and the near-term outlook for monetary policy. I will then turn to the results of our second public review of our monetary policy framework, as captured in the revised Statement on Longer-Run Goals and Monetary Policy Strategy that we released today.

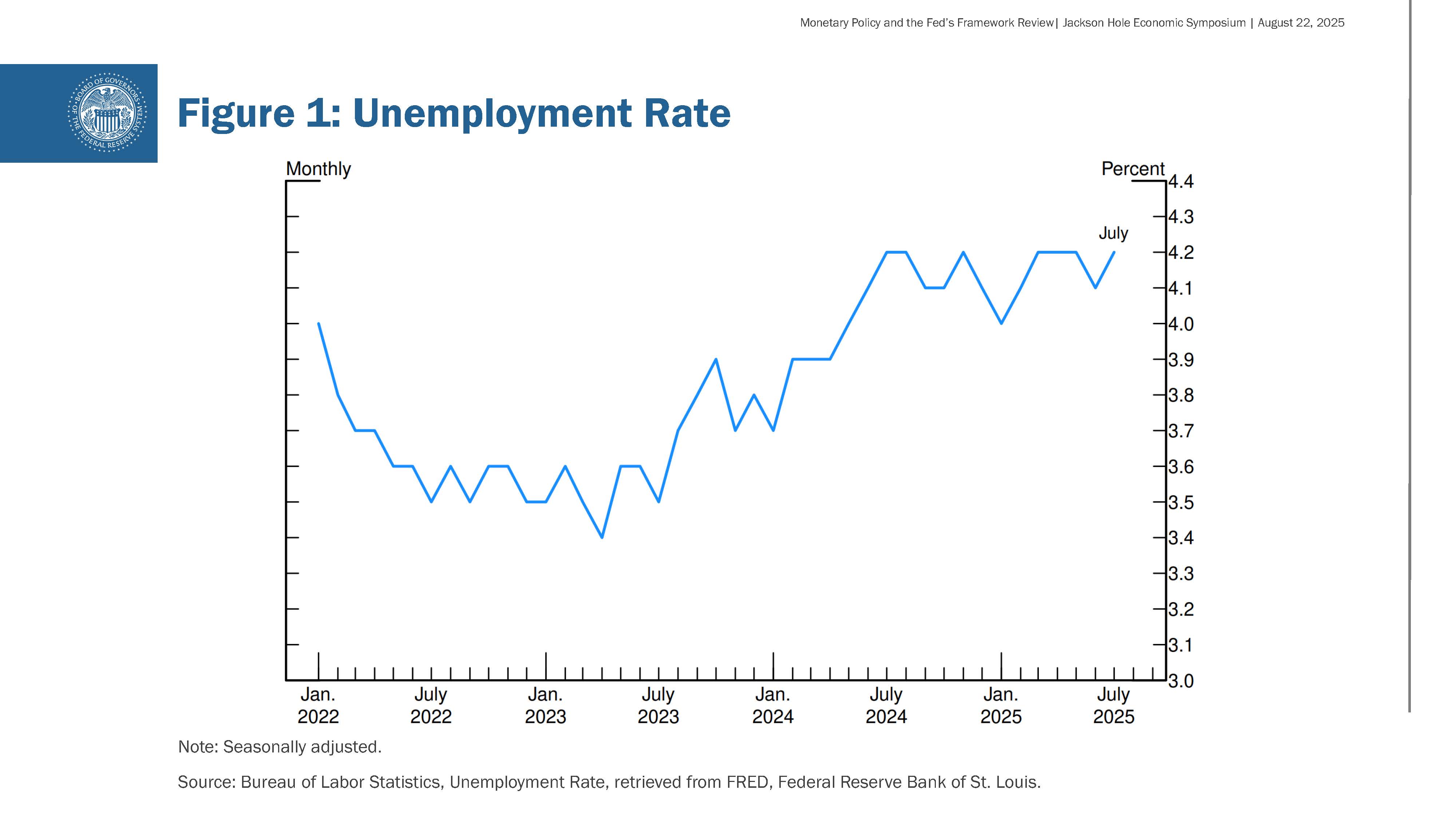

Current Economic Conditions and Near-Term Outlook When I appeared at this podium one year ago, the economy was at an inflection point. Our policy rate had stood at 5-1/4 to 5-1/2 percent for more than a year. That restrictive policy stance was appropriate to help bring down inflation and to foster a sustainable balance between aggregate demand and supply. Inflation had moved much closer to our objective, and the labor market had cooled from its formerly overheated state. Upside risks to inflation had diminished. But the unemployment rate had increased by almost a full percentage point, a development that historically has not occurred outside of recessions.1 Over the subsequent three Federal Open Market Committee (FOMC) meetings, we recalibrated our policy stance, setting the stage for the labor market to remain in balance near maximum employment over the past year (figure 1).

This year, the economy has faced new challenges. Significantly higher tariffs across our trading partners are remaking the global trading system. Tighter immigration policy has led to an abrupt slowdown in labor force growth. Over the longer run, changes in tax, spending, and regulatory policies may also have important implications for economic growth and productivity. There is significant uncertainty about where all of these polices will eventually settle and what their lasting effects on the economy will be.

Changes in trade and immigration policies are affecting both demand and supply. In this environment, distinguishing cyclical developments from trend, or structural, developments is difficult. This distinction is critical because monetary policy can work to stabilize cyclical fluctuations but can do little to alter structural changes.

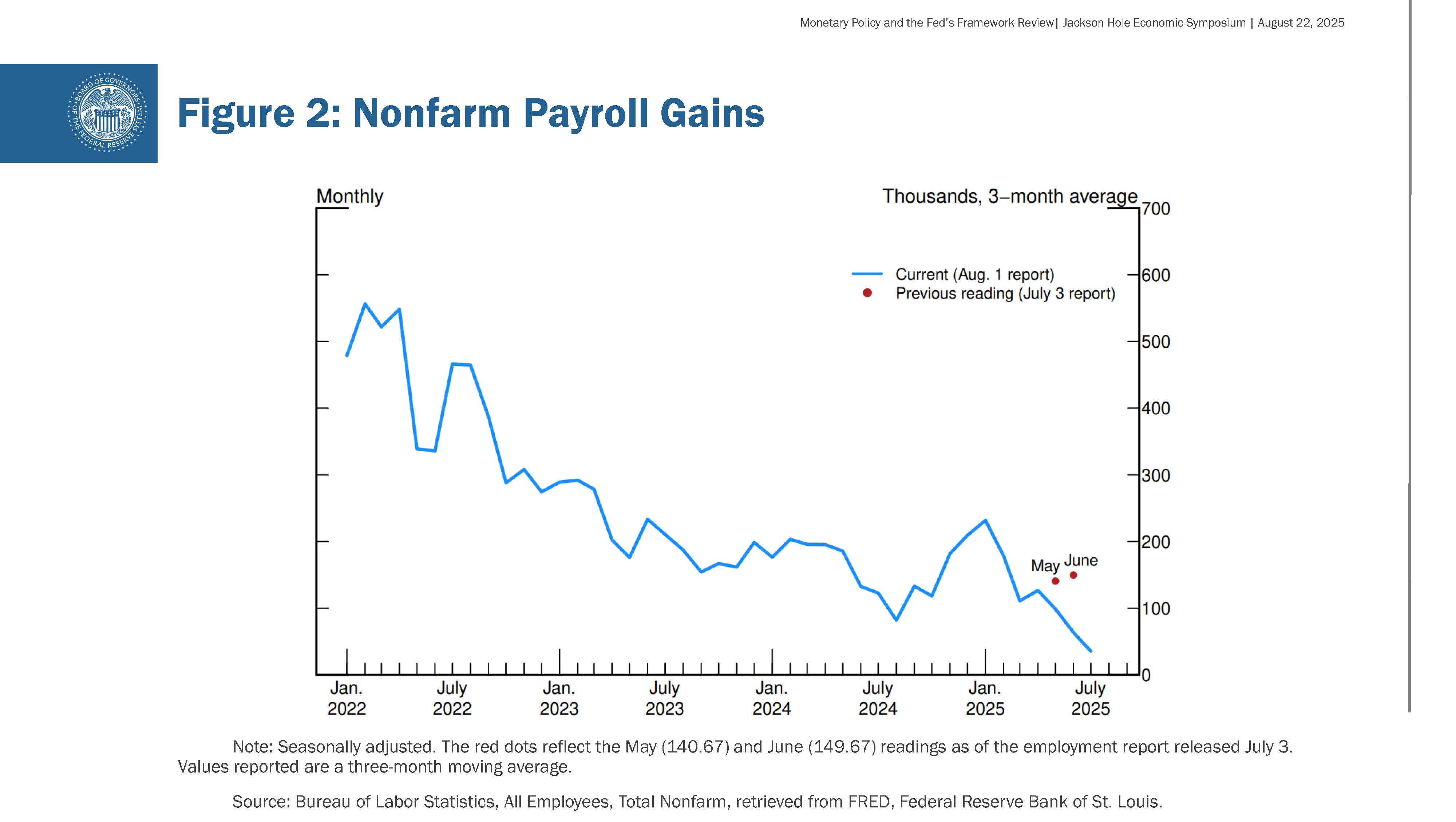

The labor market is a case in point. The July employment report released earlier this month showed that payroll job growth slowed to an average pace of only 35,000 per month over the past three months, down from 168,000 per month during 2024 (figure 2).2 This slowdown is much larger than assessed just a month ago, as the earlier figures for May and June were revised down substantially.3 But it does not appear that the slowdown in job growth has opened up a large margin of slack in the labor market—an outcome we want to avoid. The unemployment rate, while edging up in July, stands at a historically low level of 4.2 percent and has been broadly stable over the past year. Other indicators of labor market conditions are also little changed or have softened only modestly, including quits, layoffs, the ratio of vacancies to unemployment, and nominal wage growth. Labor supply has softened in line with demand, sharply lowering the “breakeven” rate of job creation needed to hold the unemployment rate constant. Indeed, labor force growth has slowed considerably this year with the sharp falloff in immigration, and the labor force participation rate has edged down in recent months.

Overall, while the labor market appears to be in balance, it is a curious kind of balance that results from a marked slowing in both the supply of and demand for workers. This unusual situation suggests that downside risks to employment are rising. And if those risks materialize, they can do so quickly in the form of sharply higher layoffs and rising unemployment.

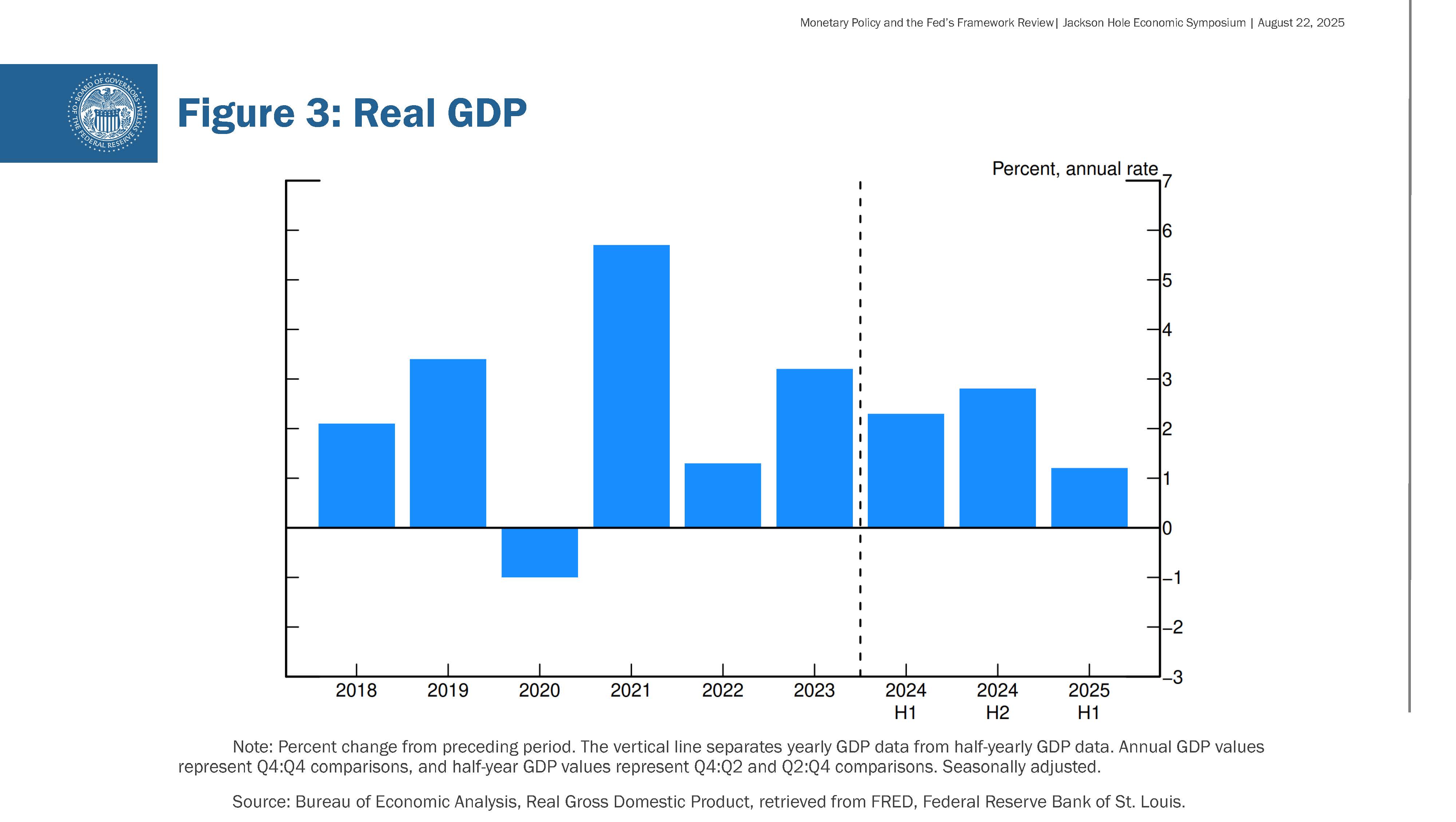

At the same time, GDP growth has slowed notably in the first half of this year to a pace of 1.2 percent, roughly half the 2.5 percent pace in 2024 (figure 3). The decline in growth has largely reflected a slowdown in consumer spending. As with the labor market, some of the slowing in GDP likely reflects slower growth of supply or potential output.

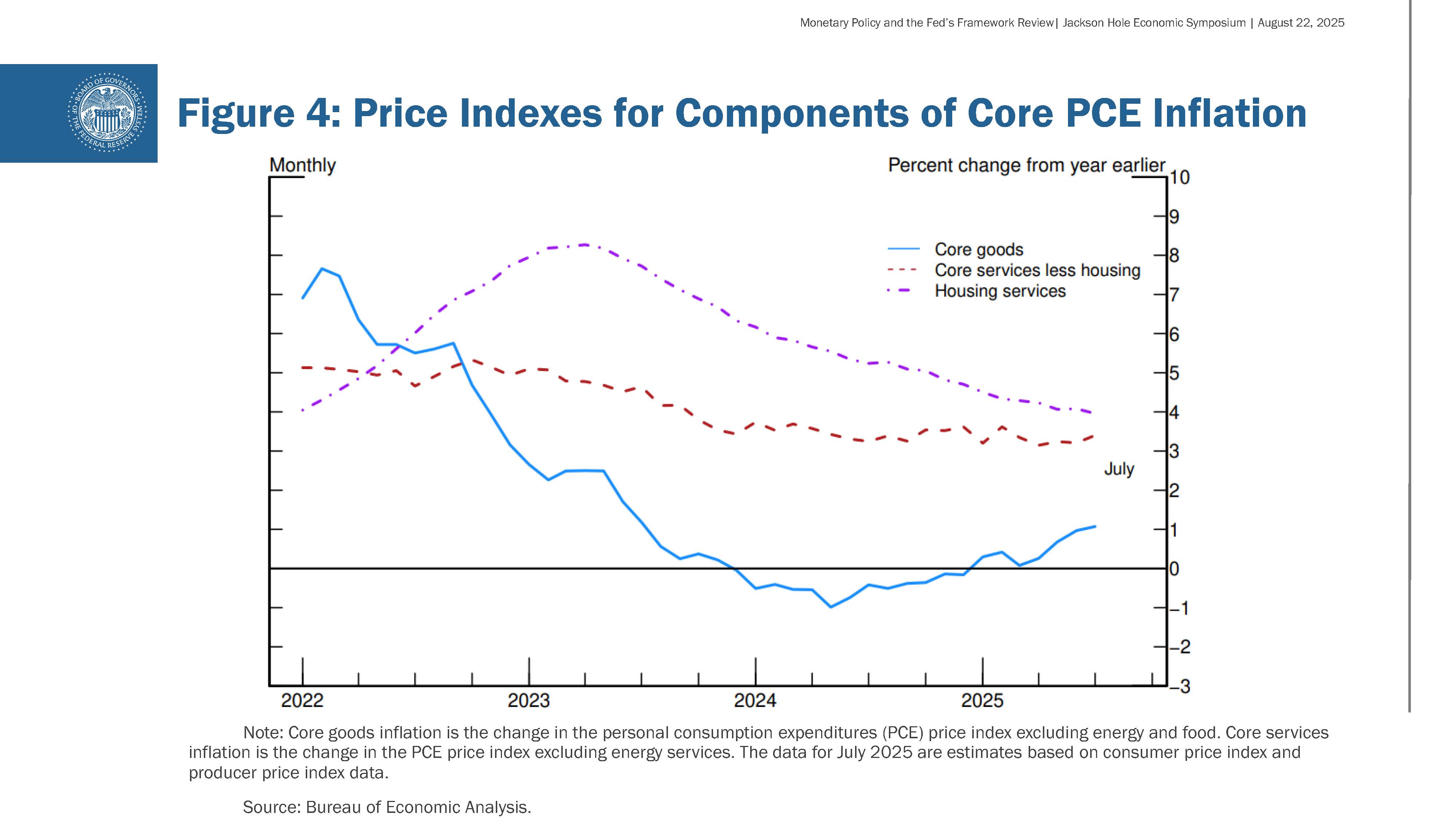

Turning to inflation, higher tariffs have begun to push up prices in some categories of goods. Estimates based on the latest available data indicate that total PCE prices rose 2.6 percent over the 12 months ending in July. Excluding the volatile food and energy categories, core PCE prices rose 2.9 percent, above their level a year ago. Within core, prices of goods increased 1.1 percent over the past 12 months, a notable shift from the modest decline seen over the course of 2024. In contrast, housing services inflation remains on a downward trend, and nonhousing services inflation is still running at a level a bit above what has been historically consistent with 2 percent inflation (figure 4).4

The effects of tariffs on consumer prices are now clearly visible. We expect those effects to accumulate over coming months, with high uncertainty about timing and amounts. The question that matters for monetary policy is whether these price increases are likely to materially raise the risk of an ongoing inflation problem. A reasonable base case is that the effects will be relatively short lived—a one-time shift in the price level. Of course, “one-time” does not mean “all at once.” It will continue to take time for tariff increases to work their way through supply chains and distribution networks. Moreover, tariff rates continue to evolve, potentially prolonging the adjustment process.

It is also possible, however, that the upward pressure on prices from tariffs could spur a more lasting inflation dynamic, and that is a risk to be assessed and managed. One possibility is that workers, who see their real incomes decline because of higher prices, demand and get higher wages from employers, setting off adverse wage–price dynamics. Given that the labor market is not particularly tight and faces increasing downside risks, that outcome does not seem likely.

Another possibility is that inflation expectations could move up, dragging actual inflation with them. Inflation has been above our target for more than four years and remains a prominent concern for households and businesses. Measures of longer-term inflation expectations, however, as reflected in market- and survey-based measures, appear to remain well anchored and consistent with our longer-run inflation objective of 2 percent.

Of course, we cannot take the stability of inflation expectations for granted. Come what may, we will not allow a one-time increase in the price level to become an ongoing inflation problem.

Putting the pieces together, what are the implications for monetary policy? In the near term, risks to inflation are tilted to the upside, and risks to employment to the downside—a challenging situation. When our goals are in tension like this, our framework calls for us to balance both sides of our dual mandate. Our policy rate is now 100 basis points closer to neutral than it was a year ago, and the stability of the unemployment rate and other labor market measures allows us to proceed carefully as we consider changes to our policy stance. Nonetheless, with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.

Monetary policy is not on a preset course. FOMC members will make these decisions, based solely on their assessment of the data and its implications for the economic outlook and the balance of risks. We will never deviate from that approach.

Evolution of Monetary Policy Framework Turning to my second topic, our monetary policy framework is built on the unchanging foundation of our mandate from Congress to foster maximum employment and stable prices for the American people. We remain fully committed to fulfilling our statutory mandate, and the revisions to our framework will support that mission across a broad range of economic conditions. Our revised Statement on Longer-Run Goals and Monetary Policy Strategy, which we refer to as our consensus statement, describes how we pursue our dual-mandate goals. It is designed to give the public a clear sense of how we think about monetary policy, and that understanding is important both for transparency and accountability, and for making monetary policy more effective.

The changes we made in this review are a natural progression, grounded in our ever-evolving understanding of our economy. We continue to build upon the initial consensus statement adopted in 2012 under Chair Ben Bernanke’s leadership. Today’s revised statement is the outcome of the second public review of our framework, which we conduct at five-year intervals. This year’s review included three elements: Fed Listens events at Reserve Banks around the country, a flagship research conference, and policymaker discussions and deliberations, supported by staff analysis, at a series of FOMC meetings.5

In approaching this year’s review, a key objective has been to make sure that our framework is suitable across a broad range of economic conditions. At the same time, the framework needs to evolve with changes in the structure of the economy and our understanding of those changes. The Great Depression presented different challenges from those of the Great Inflation and the Great Moderation, which in turn are different from the ones we face today.6

At the time of the last review, we were living in a new normal, characterized by the proximity of interest rates to the effective lower bound (ELB), along with low growth, low inflation, and a very flat Phillips curve—meaning that inflation was not very responsive to slack in the economy.7 To me, a statistic that captures that era is that our policy rate was stuck at the ELB for seven long years following the onset of the Global Financial Crisis (GFC) in late 2008. Many here will recall the sluggish growth and painfully slow recovery of that era. It appeared highly likely that if the economy experienced even a mild downturn, our policy rate would be back at the ELB very quickly, probably for another extended period. Inflation and inflation expectations could then decline in a weak economy, raising real interest rates as nominal rates were pinned near zero. Higher real rates would further weigh on job growth and reinforce the downward pressure on inflation and inflation expectations, triggering an adverse dynamic.

The economic conditions that brought the policy rate to the ELB and drove the 2020 framework changes were thought to be rooted in slow-moving global factors that would persist for an extended period—and might well have done so, if not for the pandemic.8 The 2020 consensus statement included several features that addressed the ELB-related risks that had become increasingly prominent over the preceding two decades. We emphasized the importance of anchored longer-term inflation expectations to support both our price-stability and maximum-employment goals. Drawing on an extensive literature on strategies to mitigate risks associated with the ELB, we adopted flexible average inflation targeting—a “makeup” strategy to ensure that inflation expectations would remain well anchored even with the ELB constraint.9 In particular, we said that, following periods when inflation had been running persistently below 2 percent, appropriate monetary policy would likely aim to achieve inflation moderately above 2 percent for some time.

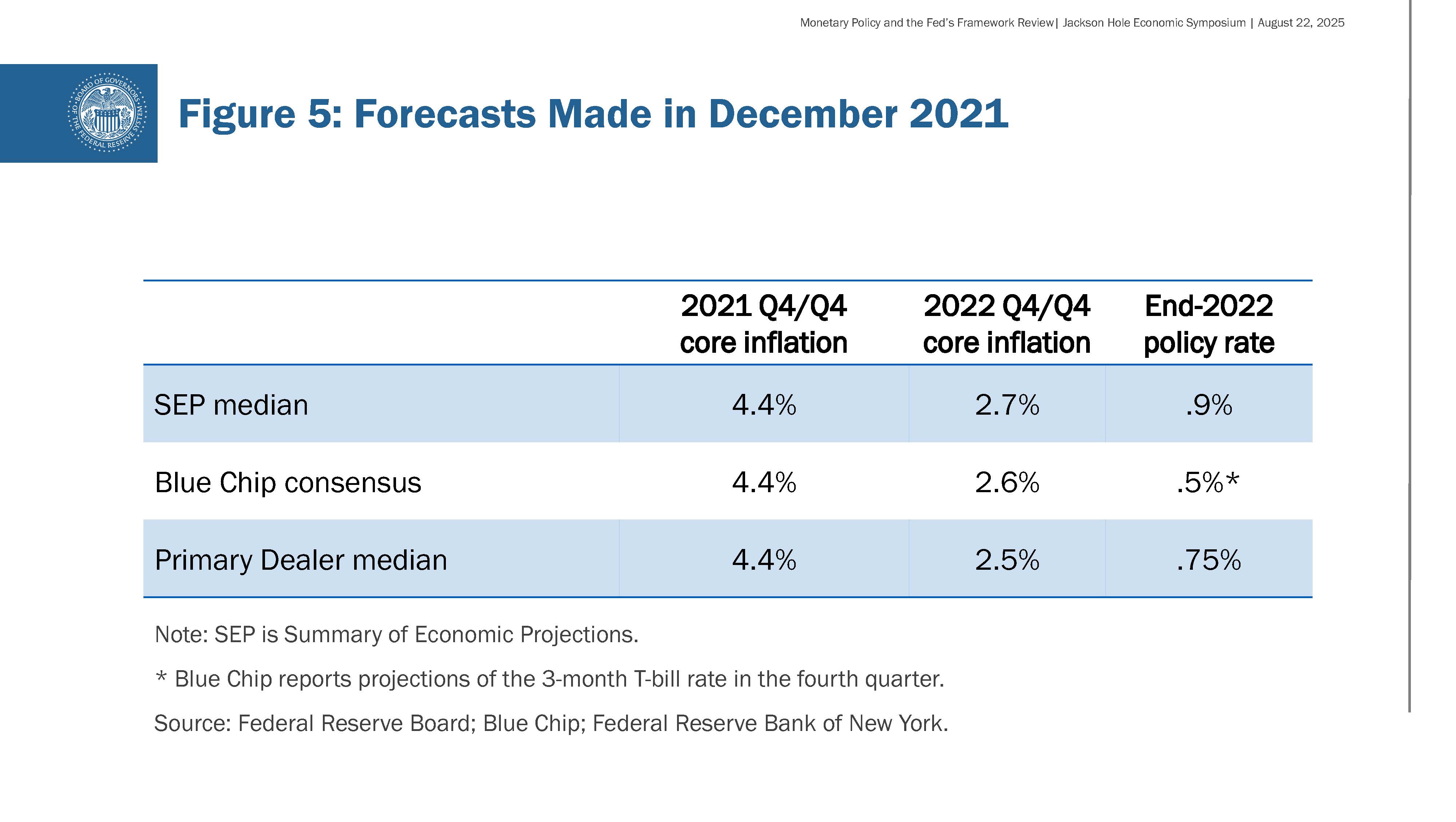

In the event, rather than low inflation and the ELB, the post-pandemic reopening brought the highest inflation in 40 years to economies around the world. Like most other central banks and private-sector analysts, through year-end 2021 we thought that inflation would subside fairly quickly without a sharp tightening in our policy stance (figure 5).10 When it became clear that this was not the case, we responded forcefully, raising our policy rate by 5.25 percentage points over 16 months. That action, combined with the unwinding of pandemic supply disruptions, contributed to inflation moving much closer to our target without the painful rise in unemployment that has accompanied previous efforts to counter high inflation.

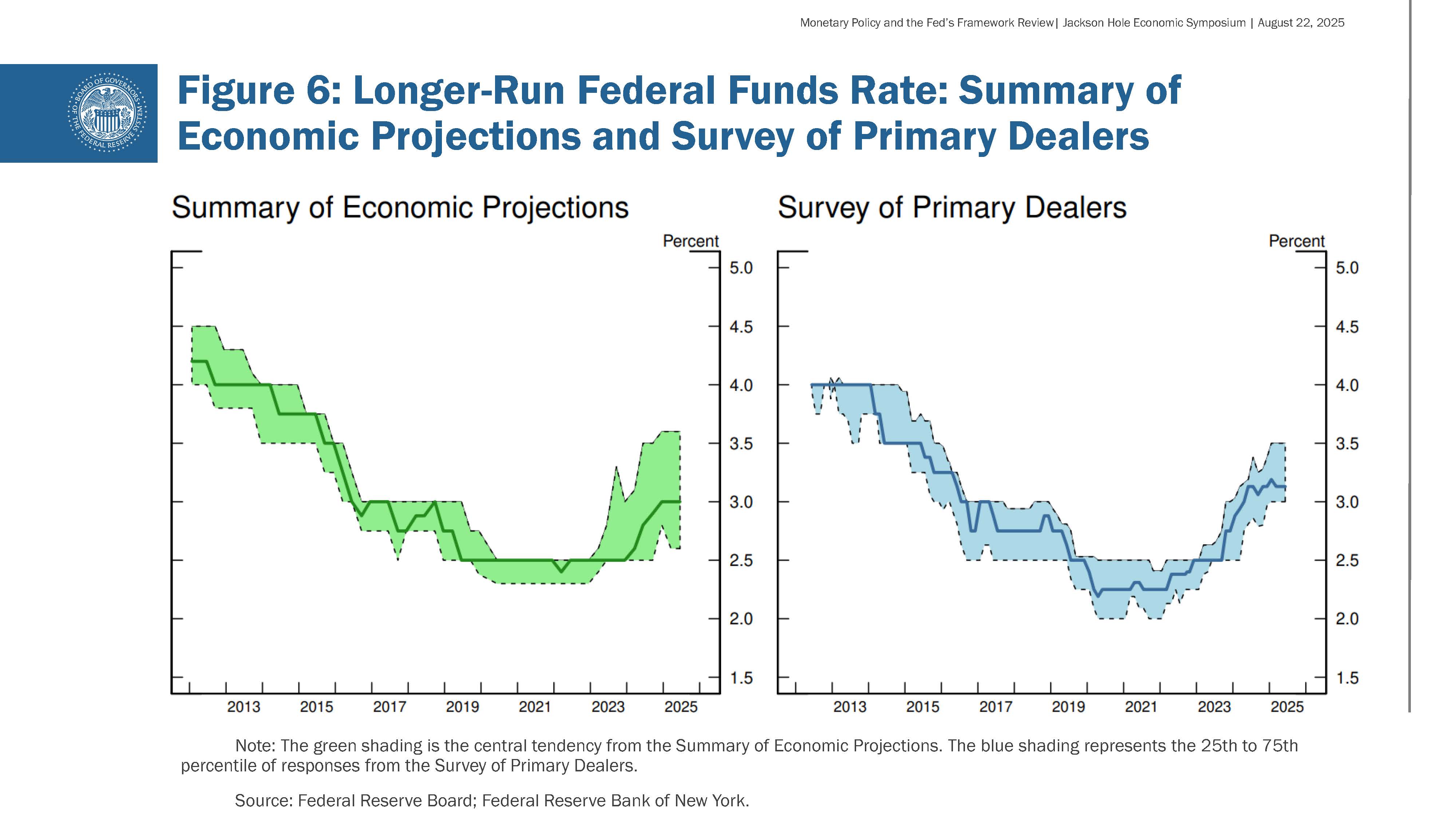

Elements of the Revised Consensus Statement This year’s review considered how economic conditions have evolved over the past five years. During this period, we saw that the inflation situation can change rapidly in the face of large shocks. In addition, interest rates are now substantially higher than was the case during the era between the GFC and the pandemic. With inflation above target, our policy rate is restrictive—modestly so, in my view. We cannot say for certain where rates will settle out over the longer run, but their neutral level may now be higher than during the 2010s, reflecting changes in productivity, demographics, fiscal policy, and other factors that affect the balance between saving and investment (figure 6). During the review, we discussed how the 2020 statement’s focus on the ELB may have complicated communications about our response to high inflation. We concluded that the emphasis on an overly specific set of economic conditions may have led to some confusion, and, as a result, we made several important changes to the consensus statement to reflect that insight.

First, we removed language indicating that the ELB was a defining feature of the economic landscape. Instead, we noted that our “monetary policy strategy is designed to promote maximum employment and stable prices across a broad range of economic conditions.” The difficulty of operating near the ELB remains a potential concern, but it is not our primary focus. The revised statement reiterates that the Committee is prepared to use its full range of tools to achieve its maximum-employment and price-stability goals, particularly if the federal funds rate is constrained by the ELB.

Second, we returned to a framework of flexible inflation targeting and eliminated the “makeup” strategy. As it turned out, the idea of an intentional, moderate inflation overshoot had proved irrelevant. There was nothing intentional or moderate about the inflation that arrived a few months after we announced our 2020 changes to the consensus statement, as I acknowledged publicly in 2021.11

Well-anchored inflation expectations were critical to our success in bringing down inflation without a sharp increase in unemployment. Anchored expectations promote the return of inflation to target when adverse shocks drive inflation higher, and limit the risk of deflation when the economy weakens.12 Further, they allow monetary policy to support maximum employment in economic downturns without compromising price stability. Our revised statement emphasizes our commitment to act forcefully to ensure that longer-term inflation expectations remain well anchored, to the benefit of both sides of our dual mandate. It also notes that “price stability is essential for a sound and stable economy and supports the well-being of all Americans.” This theme came through loud and clear at our Fed Listens events.13 The past five years have been a painful reminder of the hardship that high inflation imposes, especially on those least able to meet the higher costs of necessities.

Third, our 2020 statement said that we would mitigate “shortfalls,” rather than “deviations,” from maximum employment. The use of “shortfalls” reflected the insight that our real-time assessments of the natural rate of unemployment—and hence of “maximum employment”—are highly uncertain.14 The later years of the post-GFC recovery featured employment running for an extended period above mainstream estimates of its sustainable level, along with inflation running persistently below our 2 percent target. In the absence of inflationary pressures, it might not be necessary to tighten policy based solely on uncertain real-time estimates of the natural rate of unemployment.15

We still have that view, but our use of the term “shortfalls” was not always interpreted as intended, raising communications challenges. In particular, the use of “shortfalls” was not intended as a commitment to permanently forswear preemption or to ignore labor market tightness. Accordingly, we removed “shortfalls” from our statement. Instead, the revised document now states more precisely that “the Committee recognizes that employment may at times run above real-time assessments of maximum employment without necessarily creating risks to price stability.” Of course, preemptive action would likely be warranted if tightness in the labor market or other factors pose risks to price stability.

The revised statement also notes that maximum employment is “the highest level of employment that can be achieved on a sustained basis in a context of price stability.” This focus on promoting a strong labor market underscores the principle that “durably achieving maximum employment fosters broad-based economic opportunities and benefits for all Americans.”The feedback we received at Fed Listens events reinforced the value of a strong labor market for American households, employers, and communities.

Fourth, consistent with the removal of “shortfalls,” we made changes to clarify our approach in periods when our employment and inflation objectives are not complementary. In those circumstances, we will follow a balanced approach in promoting them. The revised statement now more closely aligns with the original 2012 language. We take into account the extent of departures from our goals and the potentially different time horizons over which each is projected to return to a level consistent with our dual mandate. These principles guide our policy decisions today, as they did over the 2022–24 period, when the departure from our 2 percent inflation target was the overriding concern.

In addition to these changes, there is a great deal of continuity with past statements. The document continues to explain how we interpret the mandate Congress has given us and describes the policy framework that we believe will best promote maximum employment and price stability. We continue to believe that monetary policy must be forward looking and consider the lags in its effects on the economy. For this reason, our policy actions depend on the economic outlook and the balance of risks to that outlook. We continue to believe that setting a numerical goal for employment is unwise, because the maximum level of employment is not directly measurable and changes over time for reasons unrelated to monetary policy.

We also continue to view a longer-run inflation rate of 2 percent as most consistent with our dual-mandate goals. We believe that our commitment to this target is a key factor helping keep longer-term inflation expectations well anchored. Experience has shown that 2 percent inflation is low enough to ensure that inflation is not a concern in household and business decisionmaking while also providing a central bank with some policy flexibility to provide accommodation during economic downturns.

Finally, the revised consensus statement retained our commitment to conduct a public review roughly every five years. There is nothing magic about a five-year pace. That frequency allows policymakers to reassess structural features of the economy and to engage with the public, practitioners, and academics on the performance of our framework. It is also consistent with several global peers.

Conclusion In closing, I want to thank President Schmid and all his staff who work so diligently to host this outstanding event annually. Counting a couple of virtual appearances during the pandemic, this is the eighth time I have had the honor to speak from this podium. Each year, this symposium offers the opportunity for Federal Reserve leaders to hear ideas from leading economic thinkers and focus on the challenges we face. The Kansas City Fed was wise to lure Chair Volcker to this national park more than 40 years ago, and I am proud to be part of that tradition.

1. For example, after the July 2024 employment report, the 3-month average of the unemployment rate had increased more than 0.5 percentage point above its lowest value over the previous 12 months. For more information, see Claudia Sahm (2019), “Direct Stimulus Payments to Individuals,” in Heather Boushey, Ryan Nunn, and Jay Shambaugh, eds., Recession Ready: Fiscal Policies to Stabilize the American Economy (PDF) (Washington: Hamilton Project and Washington Center for Equitable Growth, May), pp. 67–92. Return to text

2. In early September, the Bureau of Labor Statistics will publish a preliminary estimate of benchmark revisions to the level of nonfarm payrolls as of March 2025, based on data from the Quarterly Census of Employment and Wages. Data available to date suggest that the level of nonfarm payrolls will be revised down materially. The final benchmark revision will be incorporated into the monthly employment data in February 2026. Return to text

3. The total downward revision of 258,000 between May and June was spread across private-sector industries as well as state and local government employment, particularly education, and reflected both additional information from surveyed establishments and the re-estimation of seasonal factors. Return to text

4. Using the consumer price index and other information, an estimate of the contribution of housing services to 12-month core PCE inflation in July was 0.7 percentage point, while core services excluding housing contributed 2.0 percentage points. The contribution from each of these categories remains slightly above its average during the 2002–07 period, during which core PCE inflation averaged about 2 percent. In contrast, the contribution of core goods to 12-month core PCE inflation in July was about 0.25 percentage point, compared with the 2002–07 average of −0.25 percentage point. Return to text

8. A 2020 paper by Caldara and others discusses the structural factors behind the slow evolution of changes in the natural rate of unemployment, trend productivity growth, the natural rate of interest, and the slope of the Phillips curve; see Dario Caldara, Etienne Gagnon, Enrique Martínez-García, and Christopher J. Neely (2020), “Monetary Policy and Economic Performance since the Financial Crisis,” Finance and Economics Discussion Series 2020-065 (Washington: Board of Governors of the Federal Reserve System, August). Return to text

9. See David Reifschneider and John C. Williams (2000), “Three Lessons for Monetary Policy in a Low-Inflation Era,” Journal of Money, Credit and Banking, vol. 32 (November), pp. 936–66; Michael T. Kiley and John M. Roberts (2017), “Monetary Policy in a Low Interest Rate World (PDF),” Brookings Papers on Economic Activity, Spring, pp. 317–72; James Hebden, Edward P. Herbst, Jenny Tang, Giorgio Topa, and Fabian Winkler (2020), “How Robust Are Makeup Strategies to Key Alternative Assumptions?” Finance and Economics Discussion Series 2020-069 (Washington: Board of Governors of the Federal Reserve System, August); and Ben S. Bernanke, Michael T. Kiley, and John M. Roberts (2019), “Monetary Policy Strategies for a Low-Rate Environment,” AEA Papers and Proceedings, vol. 109 (May), pp. 421–26. On average inflation targeting, see Thomas M. Mertens and John C. Williams (2019), “Monetary Policy Frameworks and the Effective Lower Bound on Interest Rates,” AEA Papers and Proceedings, vol. 109 (May), pp. 427–32. Return to text

11. See Ina Hajdini, Adam Shapiro, A. Lee Smith, and Daniel Villar (2025), “Inflation since the Pandemic: Lessons and Challenges,” Finance and Economics Discussion Series 2025-070 (Washington: Board of Governors of the Federal Reserve System, August).

13. For additional information, see the report Fed Listens:Perspectives from the Public, which summarizes the 10 Fed Listens events hosted by the Board and the Federal Reserve Banks during 2025. Return to text

14. See Christopher Foote, Shigeru Fujita, Amanda Michaud, and Joshua Montes (2025), “Assessing Maximum Employment,” Finance and Economics Discussion Series 2025-067 (Washington: Board of Governors of the Federal Reserve System, August). Return to text

Main Street Millionaire – The Boring Path to Wealth by Codie Sanchez

“Main Street Millionaire” by Codie Sanchez advocates for acquiring established, cash-flowing small businesses as the most overlooked and effective path to extraordinary wealth and financial freedom. Challenging the conventional wisdom of high-stakes startups or corporate careers, Sanchez argues that “boring businesses”—such as laundromats, car washes, and repair shops—offer dependable profits, often for little or no money down, through strategies like seller financing. The book provides a detailed, four-step R.I.C.H. framework (Research, Invest, Command, Harness) for identifying, acquiring, operating, and scaling these businesses. It also serves as a “call to arms” to save America’s small businesses, many of which are owned by aging baby boomers without succession plans, presenting a significant economic opportunity for new owners.

II. Main Themes and Core Arguments

A. The “9-to-5 Trap” and the Power of Ownership

Sanchez critiques the traditional career path, calling it a “9-to-5 Trap” that keeps people poor despite hard work. She asserts that this system programs individuals for non-ownership, trading time for money, which ultimately limits financial freedom.

“Your salary will never set you free. Your financial freedom can only come through ownership. More specifically, through equity done the right way.”

She highlights that financial freedom is achieved through ownership, not merely a high salary or freelancing.

B. The “Secret Gold Mine on Main Street”

The core premise is that ordinary, often overlooked small businesses are a “secret gold mine.” These “Main Street” or “boring” businesses, like laundromats, car washes, and plumbing services, provide essential products or services, possess steady cash flow, and often have a long history of profitability.

“This is a book about seeing opportunities for financial freedom all around you, in the overlooked and unassuming businesses that we all take for granted. As someone who specializes in making good, profitable deals, I can promise you that success doesn’t require flashy start-ups or cutting-edge new products.”

These businesses benefit from the “Lindy effect,” meaning their longevity suggests continued success, making them a more reliable investment than flashy startups.

C. The Crisis of Aging Business Owners and Economic Opportunity

A significant theme is the impending crisis of baby boomer business owners (Main Street Millionaires, or MSMs) who are “getting too old for this sh*t” and lack succession plans. Many will simply shut down profitable businesses rather than sell them.

“Here’s the craziest part: most of these MSMs will end up permanently shutting down their businesses. When they retire, they won’t hand off or even sell their cash-printing machines. Instead, they will simply turn off the lights and put the CLOSED sign up one last time. Game over.” This phenomenon, already observed in Japan, represents a massive opportunity for new owners to acquire established, job-generating businesses, simultaneously gaining financial freedom and “saving America’s small businesses.”

D. The R.I.C.H. Framework for Acquisition

Sanchez presents a four-step framework:

R is for Research: Defining one’s “perfect fit” business by aligning personal skills (“Zone of Genius”), desired owner experience, and “Deal Box” criteria (valuation, revenue, profit, sector, etc.). This involves avoiding “deadly businesses” like restaurants and retail storefronts due to high failure rates and inherent risks.

I is for Invest: Strategies for buying cash-flowing businesses with little or no money down, primarily through “Profit Payback” (seller financing) and other creative financing methods (SBA loans, customer acquisition for referral fees, revenue share acquisition, employee acquisition).

“Your financial freedom can only come through ownership… Here’s your first and most important lesson: Your salary will never set you free. Your financial freedom can only come through ownership. More specifically, through equity done the right way.”

C is for Command: Avoiding the “whoops, I bought myself a job” trap by hiring and managing a competent operator. This section details finding, interviewing, and compensating operators, and provides a 30-60-90 day plan for business transfer and transition.

H is for Harness: Scaling profits and managing multiple businesses on “autopilot” through growth tactics, responsible expansion (platform acquisitions), and preparing for a profitable exit.

E. Practicality, Grit, and “Choosing Your Hard”

The book emphasizes a no-nonsense, realistic approach. Sanchez warns that the path to becoming a Main Street Millionaire is “hard” and “won’t be easy,” requiring significant grit and commitment.

“A lot of business books set the wrong expectations… The path I teach is hard. Becoming an owner is 10 percent the business you buy, 10 percent knowledge, 10 percent talent, and 70 percent don’t F-ing stop. Grit is the secret ingredient that makes it all work.” She contrasts this with the “cool” but often financially risky paths of startups or crypto, advocating for “stealth wealth” through boring businesses that offer “healthy profits and a monthly salary on Day 1.”

F. “Ownership is the Key to Your Freedom” and a Call to Action

Ultimately, the book frames the pursuit of small business ownership as a personal and societal imperative. It positions the “Main Street over Wall Street” movement as a fight against the concentration of wealth by large corporations and institutional investors.

“We are at war, whether we like it or not. It’s a battle that invisibly pits everyday men and women against the behemoths… The way to fight back is by using their strategy against them. In a word: Ownership.” Sanchez calls readers to “take on the mantle of ownership” to secure their own freedom and contribute to a healthier local economy and country.

III. Key Ideas and Facts

Wayne Huizenga as an Archetype: The book opens with the story of Wayne Huizenga, who built massive empires (Waste Management, AutoNation, Blockbuster) not by starting new companies, but by buying and scaling small, existing businesses. This story illustrates the potential for wealth creation through acquisitions.

The “Secret Seller Phenomenon”: Over 60% of business owners would consider selling their companies if the right offer and terms came along, even if they aren’t actively listing their business. This highlights a vast, often hidden, market of motivated sellers.

The “Seven Ds” of Motivated Sellers: Death, Divorce, Disease, Distress, Dullness, Departure, Disagreement are common reasons owners are willing to sell.

“Walking Billboard Strategy”: A painfully obvious yet underutilized method of finding motivated sellers by consistently telling everyone you meet that you buy businesses and asking if they own a business or know owners.

Avoid “Deadly Businesses”: Restaurants, hotels, retail storefronts, consulting firms, personal brands, Amazon FBA/drop-shipping, and dry cleaners are identified as high-risk ventures due to high failure rates, key person risk, platform risk, or environmental liabilities.

The S.O.W.S. Framework for Good Businesses: Sanchez looks for businesses that are Stale (minimal innovation), Old (established, 5+ years), Weak (lazy competition), and Simple (easy to understand/run).

The B.R.R.T. Method for Upside Potential: Businesses should be able to Buy (cash-flow), Resist (recessions), Raise (prices), and integrate Tech.

“Six Figures to Thee & Me” Rule: A business should generate enough profit to pay both the owner and a hired operator six-figure salaries (e.g., $100,000 each, requiring at least $200,000 in annual profits). This ensures a “margin of safety.”

Importance of Creative Financing (Profit Payback/Seller Financing): This is Sanchez’s “not-so-secret secret weapon.” It allows buyers to acquire businesses for little or no money down, using future profits to pay the seller. It offers benefits like increased purchase price, tax deferral, and faster closing for sellers.

Decentralized Management (The Warren Buffett Method): The strategy of hiring capable people, giving them autonomy, and focusing on high-level metrics rather than micromanaging daily operations.

Growth Tactics: Includes raising prices (5-30%), adding three-tiered pricing (sandwich method), implementing recurring revenue models, updating websites (focus on clear calls to action and testimonials), immediate lead response (within 60 seconds for 20x conversion rate), referral programs, and actively engaging in sales (Sale-EO not CEO).

Cash Flow Boomerang Process: Focus on shortening the “Cash Conversion Cycle” by taking more upfront payments, shortening payment terms, offering cash discounts, and using lines of credit.

C.A.D.O. Process for Cost Cutting:Cut, Automate, Delegate, Outsource unnecessary expenses and tasks.

Exit Strategy: Plan for selling the business from day one. Businesses are valued higher based on simple finances, documented SOPs, loyal employees, not being run by the owner, diversified customer base (eggs in many baskets), and a strong sales team. Add-backs (owner benefits and one-time expenses) are crucial for increasing the stated profit and, consequently, the sale price.

“Ownership Autopilot”: Managing businesses effectively requires a “Deal Driveway” (identifying key client journey metrics) and a high-level “Business Scorecard” with 3-5 critical output and input metrics.

“Who Not How” Principle: When facing a problem, ask “Who can fix it for me?” or “What can I buy that would fix this?” rather than “How can I fix it myself?” This encourages acquisitions and leveraging expertise.

IV. Conclusion

“Main Street Millionaire” presents a compelling case for acquiring “boring businesses” as a pragmatic and powerful strategy for building wealth and achieving financial freedom. It demystifies the acquisition process, offering actionable steps and mindset shifts to empower individuals to become owners. Beyond personal gain, the book positions this movement as critical for revitalizing local economies and counteracting the increasing consolidation of wealth by large entities, advocating for a future where more individuals embrace ownership.

Main Street Millionaire: Comprehensive Study Guide

This study guide is designed to help you review and solidify your understanding of the “Main Street Millionaire” source material. It covers key concepts, strategies, and advice for acquiring and growing small, “boring” businesses.

Quiz

Instructions: Answer each of the following questions in 2-3 sentences.

What is the “9-to-5 Trap” and how does the author suggest individuals escape it?

Explain the author’s argument for why “Main Street” or “boring” businesses are an underrated path to wealth.

Describe the R.I.C.H. acronym and what each letter represents in the business acquisition process.

What are the “Seven Deadly Businesses” that the author advises avoiding, and what common characteristics do they share?

What is the “Walking Billboard Strategy,” and why does the author advocate for it in finding motivated sellers?

Explain the SOWS framework used for rapidly evaluating boring businesses.

What is the BRRT Method, and what does each letter stand for in evaluating a business’s upside potential?

Describe the “Profit Payback Method” (seller financing) and its main advantage for buyers.

According to the author, what is the “Six Figures to Thee & Me” rule, and why is it important when hiring an operator?

What is the “Cashout Cake” in the context of selling a business, and what is its primary purpose?

Answer Key

The “9-to-5 Trap” refers to the system where individuals are programmed to believe a good job and salary lead to financial stability, but ultimately keep them poor by trading time for money. The author suggests escaping this trap through ownership, specifically by acquiring established, cash-flowing businesses rather than relying on a salary.

The author argues that “Main Street” or “boring” businesses are an underrated path to wealth because they offer steady cash flow, are often overlooked by larger investors, and are dependable. These businesses have a long history of success (Lindy effect) and are essential, providing opportunities for significant profit and financial freedom.

The R.I.C.H. acronym outlines the step-by-step process for becoming a Main Street business owner: Research (defining the right acquisition, finding sellers, evaluation), Invest (financing, making deals), Command (hiring operators, leadership, transition), and Harness (growth, management, scaling, exit). It represents an efficient path to financial freedom through ownership.

The “Seven Deadly Businesses” to avoid include restaurants, hotels, retail storefronts, consulting firms, personal brands, Amazon FBA/drop-shipping, and dry cleaners. They share common characteristics such as high failure rates, asymmetric risks, high expenses, low transferability, and often significant key person risk or platform dependence.

The “Walking Billboard Strategy” involves consistently telling everyone you meet that you buy businesses and asking small business owners if they own their establishment and would consider selling. This off-market approach helps uncover “secret sellers” who might be open to an offer but aren’t actively advertising their business for sale online.

The SOWS framework helps identify great boring businesses with high upside potential. STALE means minimal innovation, offering room for modernization; OLD signifies established businesses with a history of survival; WEAK indicates lazy competition, making it easy to outperform; and SIMPLE means the business model is easy to understand and run.

The BRRT Method is a second test to ensure a business has upside potential. BUY means acquiring a cash-flowing business; RESIST means it’s recession-resistant; RAISE means it can increase its prices; and TECH means technology can be meaningfully added to improve operations. This method helps quickly assess a business’s growth viability.

The “Profit Payback Method,” or seller financing, involves the buyer paying the seller for their business over time using the future profits generated by the business itself. Its main advantage for buyers is the ability to acquire a profitable business with little to no upfront cash, often avoiding bank loans and offering flexible, negotiable terms.

The “Six Figures to Thee & Me” rule suggests a business should generate enough profit to pay a six-figure salary to both the owner and the operator ($100,000 each). This rule is important because it ensures a sufficient “margin of safety” for the business to cover a quality operator’s salary and still provide a healthy income for the owner, preventing the owner from buying a “job” instead of a business.

The “Cashout Cake” refers to a recipe of seven key ingredients that make a business highly attractive and valuable for sale. Its primary purpose is to systematically prepare a business to maximize its sale price by making it easy for a buyer to understand, operate, and trust its profitability and longevity.

Essay Format Questions

Analyze how the “Main Street Millionaire” philosophy challenges traditional notions of career progression and wealth creation, particularly in contrast to the “9-to-5 Trap.” Discuss the author’s arguments for why ownership is superior to a salary.

Evaluate the importance of “due diligence” in the business acquisition process, referencing the author’s personal anecdote about losing $12 million. What are the critical phases and red flags, and how can a new owner mitigate risks during this stage?

Discuss the role of “creative financing,” specifically the “Profit Payback Method,” in enabling individuals to acquire businesses with little to no money down. Explain the benefits for both the buyer and the seller, and address common fears or misconceptions about debt.

Examine the author’s strategies for growing profits in an acquired business, using the power-washing example as a case study. Detail at least four specific growth tactics and explain how they contribute to a significant increase in annual profits.

How does the concept of “Hiring an Operator” enable business owners to manage multiple businesses and achieve “ownership autopilot”? Discuss the “Six Figures to Thee & Me” rule, strategies for attracting and short-listing talent, and the importance of a clear 30-60-90 plan for an operator’s success.

Glossary of Key Terms

9-to-5 Trap: The societal system that encourages individuals to pursue stable jobs and salaries, often leading to financial stress and limiting true wealth creation by trading time for money.

Add-backs: Benefits and one-time expenses that are added back to a business’s net income to calculate Seller’s Discretionary Earnings (SDE), crucial for determining a business’s true profitability to a potential owner.

Acqui-hire: A strategy where a company acquires another, primarily for its talented employees or team, rather than for its products or services.

Asset Acquisition: Buying only the assets of a business (e.g., equipment, inventory, real estate) rather than the entire company and its liabilities.

BRRT Method: A framework (Buy, Resist, Raise, Tech) used to evaluate a business’s upside potential, ensuring it’s cash-flowing, recession-resistant, capable of price increases, and open to technological improvements.

Cash-Flow Boomerang Process: A concept emphasizing the importance of shortening a business’s cash conversion cycle, ensuring money comes back quickly after a product or service is provided.

Cash-Flow Business: A business model where payment is received before or concurrently with the provision of service, often characterized by monthly recurring revenue and a diverse client base.

Cashout Cake: A metaphor for the seven essential ingredients (simple finances, SOPs, loyal employees, not run by you, matching outfits, eggs in many baskets, sales team) that make a business easy to sell for maximum profit.

Contrarian Thinking: The author’s financial media and investment company, focused on empowering individuals to achieve financial freedom through ownership.

Creative Financing: Non-traditional financing methods, often involving direct negotiation with the seller, to fund a business acquisition with little to no upfront cash, such as seller financing.

Deal Box: A defined set of specific criteria (e.g., valuation, revenue range, profit range, sector, seller type, geographic region) that helps an aspiring buyer narrow down potential business acquisitions.

Deal Driveway: The specific path or sequence of steps a business’s clients take to pay for services or products, used to identify key metrics for tracking success.

Decentralized Management: A management philosophy where decision-making authority is pushed down to lower levels of the organization, allowing the owner to focus on strategic oversight rather than day-to-day details.

Due Diligence: The process of thoroughly evaluating a business’s health, financials, operations, and risks before making an offer or finalizing an acquisition.

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization): A measure of a company’s financial performance, often used for valuing larger businesses.

Execution Triangle: A concept illustrating that what gets measured gets managed, what gets managed gets scheduled, and what gets scheduled gets done, emphasizing the importance of structured execution.

Golden Handcuffs: A term for incentives (like high salary or benefits) that make it difficult for an employee to leave a job, even if they are unhappy.

Goodwill: An intangible asset representing the value of a business beyond its tangible assets, including brand recognition, customer loyalty, and proprietary technology.

Horizontal Acquisition: Acquiring a business that offers complementary products or services, allowing for diversification of income streams within an existing platform.

Key Person Risk: The risk associated with a business being overly reliant on a single individual’s skills, relationships, or expertise, making it vulnerable if that person leaves.

KPIs (Key Performance Indicators): Measurable values that demonstrate how effectively a company is achieving key business objectives.

Labor-Moated Businesses: Professional service businesses that have a competitive barrier due to the need for unique skills, certifications, or licenses, making market entry more difficult for competitors.

Leveraged Buyout (LBO): An acquisition strategy where a buyer borrows a significant portion of the purchase price, often using the acquired company’s assets or cash flow as collateral.

Lindy Effect: A theory stating that the future life expectancy of a non-perishable item or idea is proportional to its current age, implying that something successful for a long time will likely continue to be successful.

LOI (Letter of Intent): A nonbinding or binding document outlining the preliminary terms and conditions of a proposed business acquisition, serving as a framework for negotiations.

Main Street Business: A small, local business, typically run by individuals, providing essential products or services with minimal intellectual property, often overlooked but offering steady cash flow.

Margin of Safety: A principle in investing, popularized by Warren Buffett, which advocates for buying assets at a significant discount to their intrinsic value to protect against potential losses.

Motivated Seller: A business owner who has compelling reasons (e.g., the “Seven Ds”: Death, Divorce, Disease, Distress, Dullness, Departure, Disagreement) to sell their business, making them more open to flexible terms.

North Star (KPI): A single, overarching metric that guides a business’s strategic direction and aligns the entire team’s efforts towards a common goal.

Operating Agreement/Shareholder Agreement: A legally binding document that outlines the structure, management, profit-sharing, and operational details of a business, especially important for partnerships.

Operator: A key player hired to manage the day-to-day operations of an acquired business, allowing the owner to focus on strategic oversight and further acquisitions.

OPM (Other People’s Money): The practice of using borrowed funds or investments from others to finance business acquisitions or growth, a common strategy among the wealthy.

Platform Acquisition: Buying a foundational business that can then be expanded through additional acquisitions (add-ons) or diversification of income streams.

Profit Payback Method: See Creative Financing / Seller Financing.

Purchase Agreement: The main, legally binding document in a business acquisition that details all final terms and conditions of the sale.

R.I.C.H. Method: An acronym (Research, Invest, Command, Harness) outlining the four main steps in the author’s process for buying, running, and growing small businesses.

Recurring Revenue: Income that is stable and predictable, generated from ongoing payments for services (e.g., subscriptions, maintenance contracts), highly valued in business.

Reticular Activating System (RAS): A part of the brain that filters information, which the author suggests can be activated to make individuals more aware of ownership opportunities.

SBA (Small Business Administration) Loan: Government-backed loans provided by banks to small businesses, offering more favorable terms than conventional loans, but with specific qualification requirements.

Secret Seller Phenomenon: The observation that a large percentage of business owners would consider selling their companies if the right offer came along, even if they aren’t actively listing them for sale.

Seller’s Discretionary Earnings (SDE): The total financial benefit an owner receives from a business, calculated as net profit plus owner’s salary, benefits, and one-time expenses (add-backs), used for valuing small businesses.

Seller Financing: A form of creative financing where the seller agrees to receive a portion of the purchase price over time, directly from the business’s future profits, rather than an upfront lump sum.

Six Figures to Thee & Me Rule: The author’s rule stating that a business should generate at least $200,000 in annual profit to comfortably pay a $100,000 salary to both the owner and a hired operator.

Skill Stack: A unique combination of an individual’s skills, where being in the top percentage for several skills can create a competitive advantage.

SOPs (Standard Operating Procedures): Step-by-step instructions that document how to perform specific tasks, ensuring consistency, efficiency, and scalability in business operations.

SOWS Framework: An acronym (Stale, Old, Weak, Simple) used to rapidly evaluate the potential of “boring” businesses, identifying those ripe for modernization and growth.

Stock Purchase: Buying the entire company, including all its assets and liabilities, by acquiring its stock.

Sweat Equity Deal: A partnership or acquisition where one party contributes labor, expertise, or other non-monetary assets in exchange for equity or a share of future profits.

Venmo Challenge: A practical exercise where individuals review their Venmo or bank statements to identify small businesses they frequently pay, then approach those owners about a sweat equity or profit-sharing deal.

Vertical Acquisition: Acquiring a business that operates at a different stage of the supply chain than your existing business (e.g., a laundry delivery service for a laundromat).

Walking Billboard Strategy: A method for finding motivated sellers by consistently informing people you meet that you buy businesses and directly inquiring with small business owners.

Zone of Genius: The intersection of an individual’s passion, experience/skills, and network, which helps define the most suitable type of business acquisition for them.

This podcast episode, hosted by Bob Shultz, publisher and co-founder of TCLM, and featuring Factoring Specialist, Chris Lehnes provides an in-depth exploration of factoring as a financing solution for businesses seeking improved liquidity.

Factoring is explained as the sale of a company’s accounts receivable to a third-party factor, which enables immediate cash flow without incurring debt. Lehnes outlines how the process works, from invoice verification to advancing 75 to 90 percent of its value and later releasing the balance upon customer payment, while also discussing the operational benefits, such as the factor handling collections. The conversation covers critical distinctions between recourse and non-recourse factoring, cost structures, and flexibility in factoring arrangements, including selective factoring by customer or invoice. The fees, typically 1.5 to 3 percent per month, are examined alongside aspects that influence pricing, such as credit risk, invoice volume, and payment timelines.

The discussion also offers practical guidance for businesses considering factoring, highlighting its applicability primarily for B2B and B2G companies with strong customers and urgent funding needs not being met by banks. Lehnnes addresses common concerns about customer perception, explaining that large enterprise clients are accustomed to factoring arrangements, and he emphasizes good receivables management practices to improve eligibility. The episode concludes with insights into Versant Funding’s unique position in the market, emphasizing its true non-recourse model, lack of reliance on traditional borrower qualifications, flexibility in factoring older receivables, and willingness to work with high customer concentration. This positions factoring not only as a cash flow solution but also as a strategic tool for growth, bridging financing gaps, and providing operational stability

Accounts Receivable Factoring $100,000 to $30 Million Quick AR Advances No Long-Term Commitment Non-recourse Funding in about a week

We are a great match for businesses with traits such as: Less than 2 years old Negative Net Worth Losses Customer Concentrations Weak Credit Character Issues

Chris Lehnes | Factoring Specialist | 203-664-1535 | chris@chrislehnes.com

Factoring is a valuable financial tool for businesses facing cash flow issues due to delayed customer payments. The core concept involves selling unpaid invoices (accounts receivable) to a third-party “factor” in exchange for immediate cash. The discussion highlights “non-recourse factoring,” where the factor assumes the risk of customer non-payment, and explores Versant’s unique approach, benefits, real-world applications, cost structure, and ideal use cases.

Key Themes and Ideas

1. What is Factoring?

Definition: Factoring is the process of “essentially selling those unpaid invoices… your accounts receivable… to a third party company called a factor.” This allows businesses to receive “immediate cash” rather than waiting “weeks or even months to actually get paid.”

Core Problem Solved: The primary benefit of factoring is addressing “a very common problem, cash flow,” which can be a “killer if you have bills piling up or you see a new opportunity but don’t have cash on hand to jump on it.”

Simplified Responsibility: The business owner sells the invoice, and the factor “take[s] on the responsibility of collecting from your customers.” This allows the business owner to “focus on running my business.”

2. Non-Recourse Factoring: Risk Transfer

Definition: Non-recourse factoring is a specific type where “the factor takes on the risk… that your customer might not pay.” If the customer defaults, “the factor is out of luck and you’re not on the hook.”

Factor’s Selectivity: Due to this risk, factoring companies “super picky about who they work with” and “carefully evaluate the creditworthiness… of your customers, not just your business’s overall financial history.”

Ideal Customer Profile: This model is most suitable if “your customers are large, stable companies with a good track record of paying their bills.” Conversely, if “most my customers are small startups with… limited financial history,” factoring “might not be the best fit.”

3. Versant’s Approach and Benefits

Speed: Versant’s “biggest selling points is speed,” often getting “cash into their clients hands quickly, sometimes within a week,” significantly faster than “traditional bank loans, which can take months to process.” This speed is possible because “they’re primarily focused on the receivables themselves,” assessing “the creditworthiness of your customers, not necessarily your company’s entire financial history.”

No Personal Guarantees: A significant advantage is that Versant “doesn’t require personal guarantees,” meaning “business owners aren’t putting their personal assets on the line.”

Performance Guarantee: While no personal guarantee, Versant requires a “performance guarantee.” This means the business owner “is vouching for the quality of the goods or services you’ve provided.” If a customer disputes an invoice due to “faulty” product or service, “that’s ultimately your responsibility to sort out.”

Transparency & Control: Versant provides “online tools so you can track the status of your invoices and see exactly where your money is,” offering “a constant pulse on your cash flow.”

Personalized Service: Each client receives a “dedicated account executive who works with them directly,” providing “a much more personalized experience than dealing with a giant impersonal financial institution.”