Remember that brief sigh of relief? The one where it felt like maybe, just maybe, the relentless march of price increases was slowing down? Well, if you’ve been to the grocery store, filled up your gas tank, or even just browsed online recently, you’ve probably noticed it: the break is over. Companies are jacking up prices again, and consumers are once again feeling the pinch.

For a while, many economists and analysts pointed to easing supply chain issues, stabilizing energy costs, and even a slight dip in consumer demand as potential signals that inflation was cooling. Some businesses even held the line on prices, perhaps hoping to retain market share or out of a genuine desire to give their customers a break.

But those days seem to be largely behind us. We’re seeing a resurgence in price hikes across a wide array of sectors. From everyday necessities to discretionary items, the numbers on the tags are climbing.

What’s Driving This Latest Surge?

Several factors are likely contributing to this renewed upward trend:

Persistent Input Costs: While some raw material costs have stabilized, others continue to be elevated. Labor costs are also a significant factor, with many businesses facing pressure to offer higher wages to attract and retain employees. These increased operational expenses often get passed on to the consumer.

Strong Consumer Demand (Still): Despite earlier predictions of a significant slowdown, consumer demand has proven remarkably resilient in many areas. When demand remains high, businesses have less incentive to lower prices and more leeway to raise them.

“Catch-Up” Pricing: Some companies might feel they absorbed increased costs for a period and are now playing catch-up, adjusting prices to reflect their sustained operational expenses.

Geopolitical Factors: Global events continue to create volatility in commodity markets, particularly for energy and certain raw materials, which inevitably impacts production and transportation costs.

Profit Margins: Let’s be honest, businesses are in the business of making a profit. If they perceive an opportunity to increase their margins without significantly impacting sales volume, many will take it.

What Does This Mean for You?

For the average household, this renewed wave of price increases means a continued squeeze on budgets. Discretionary spending may need to be curtailed further, and even essential purchases will require more careful planning. Savings might deplete faster, and the goal of financial stability could feel increasingly distant.

How Can Consumers Cope?

While we can’t control the broader economic forces at play, there are strategies consumers can employ to mitigate the impact:

Become a Savvy Shopper: Compare prices diligently, look for sales and discounts, and consider generic or store-brand alternatives.

Budgeting is Key: Revisit your budget and identify areas where you can cut back. Track your spending to understand exactly where your money is going.

Prioritize Needs vs. Wants: Distinguish between essential purchases and items that can be deferred or eliminated.

Support Local (Where Affordable): Sometimes local businesses, with lower overheads, can offer competitive pricing, or at least you’re supporting your community.

Advocate for Yourself: When possible, negotiate prices for services, or look for loyalty programs that offer discounts.

The “break” from rising prices was indeed short-lived. As companies continue to adjust their pricing strategies, it’s more important than ever for consumers to be vigilant, adapt their spending habits, and advocate for their financial well-being.

The latest economic data brings a sigh of relief for consumers and policymakers alike, as U.S. inflation has shown a more significant easing than anticipated at the beginning of the year. This positive development suggests that efforts to tame rising prices may be gaining traction, offering a glimmer of hope for greater economic stability in the months to come.

For much of the past year, inflation has been a persistent headwind, impacting everything from grocery bills to housing costs. The robust labor market, while a sign of economic strength, also contributed to upward price pressures. However, recent reports indicate a potential shift in this trend.

Several factors appear to be contributing to this welcome slowdown. Supply chain disruptions, which were a major catalyst for price increases, have largely improved. This has allowed for a more consistent flow of goods, reducing bottlenecks and associated costs. Additionally, the Federal Reserve’s aggressive monetary policy, including multiple interest rate hikes, seems to be having its intended effect of cooling demand and reining in inflationary expectations.

While the easing of inflation is certainly good news, it’s important to maintain a balanced perspective. The economy is a complex system, and various forces are constantly at play. Energy prices, geopolitical events, and shifts in consumer spending habits can all influence the trajectory of inflation. Therefore, continuous monitoring and adaptive policymaking will remain crucial.

What does this mean for the average American? For starters, it could translate into less pressure on household budgets over time. If the trend continues, we might see more stable prices for everyday goods and services, allowing purchasing power to stretch further. It also provides the Federal Reserve with more flexibility in its future policy decisions, potentially reducing the need for further aggressive rate hikes.

The journey to sustained price stability is an ongoing one, but the early signs from this year are undoubtedly encouraging. It’s a testament to the resilience of the U.S. economy and the effectiveness of concerted efforts to address inflationary pressures. As we move further into the year, economists and consumers alike will be watching closely to see if this promising trend continues, paving the way for a more predictable and stable economic environment.

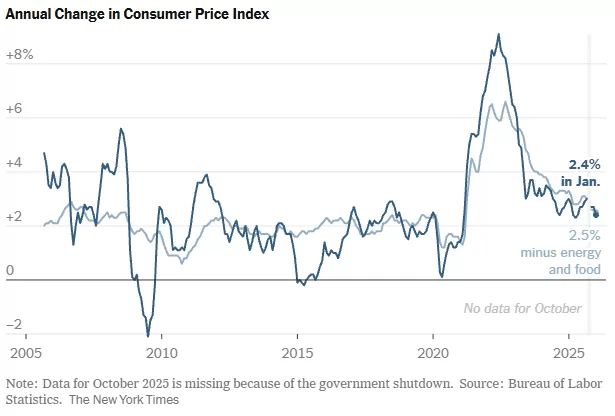

The Inflation “Split Screen”: What December’s CPI Numbers Really Mean

Inflation Stable. The latest data is in, and it paints a picture of an economy caught between cooling pressures and political friction. In December, consumer prices rose 2.7% from a year earlier—holding steady from November and landing exactly where economists predicted.

While the “headline” number suggests stability, the story beneath the surface is much more complex. Here are the key takeaways from the final inflation report of 2025.

1. Stability Amidst the Noise

For the second month in a row, inflation has leveled off at 2.7%. Meanwhile, “Core CPI” (which strips out volatile food and energy costs) rose 2.6%.

Interestingly, these numbers came in slightly better than the 2.8% core increase some experts feared. This suggests that despite the introduction of steep tariffs earlier in 2025, businesses haven’t yet passed the full weight of those costs onto consumers. However, the “last mile” of the journey back to the Fed’s 2% target remains stubbornly out of reach.

2. A Cloud of Data Uncertainty

This report is the first “clean” look at inflation we’ve had in months. Following a government shutdown last fall, the Labor Department had to rely on technical workarounds to fill data gaps.

The “Payback” Effect: Many economists believe November’s figures may have been artificially low due to those data collection issues.

The Verdict: While December’s numbers didn’t spike as much as feared, they likely reflect a correction for the missing data from previous months.

3. The Fed’s High-Stakes Balancing Act

The Federal Reserve is currently navigating a “split screen” economy. On one hand, growth remains solid; on the other, the labor market has cooled significantly. In fact, 2025 saw the lowest pace of job growth since 2003 (excluding major recessions).

The Fed cut rates three times at the end of 2025 to support the job market, but officials are now divided. With inflation still above 2%, some are hesitant to keep cutting—especially as they watch for the inflationary impact of the One Big Beautiful Bill Act and ongoing investments in AI.

4. Politics vs. Policy

Perhaps the most unusual backdrop to this report is the unprecedented political pressure on independent agencies.

The Labor Department: Its commissioner was fired in August amidst claims of “rigged” numbers.

The Fed: Chair Jerome Powell recently alleged that the administration has used threats of criminal prosecution to pressure the board into lowering interest rates.

What’s Next?

As we head into 2026, all eyes are on January and February. This is traditionally when businesses reset their pricing for the year. Whether they will hike prices to account for tariffs and tax-cut-driven demand remains the big question.

For now, the “meandering path” toward lower inflation continues, but with a cooling job market and political volatility, the road ahead looks anything but smooth.

Title: How the China Trade Deal Announced Today Will Impact Small Businesses

Introduction to impact of China Trade Deal

Today, the U.S. and China reached a tentative trade agreement that marks a significant, albeit partial, development in their ongoing economic standoff. This new arrangement preserves existing tariffs—55% on Chinese imports and 10% on U.S. exports—while introducing limited concessions on rare-earth minerals and export controls. The agreement provides minimal relief for most small businesses, which have borne the brunt of the past several years of tariff-induced uncertainty. This article will explore in detail the contents of the deal, assess its implications for various sectors of the small business community, and offer strategic recommendations for adaptation.

Part 1: Understanding the New U.S. – China Trade Deal

The June 11, 2025 deal between the United States and China was framed more as a temporary stabilization than a comprehensive resolution. Here are the key elements:

Tariffs Remain Largely Intact: The U.S. will maintain approximately 55% tariffs on a wide range of Chinese imports. China will reciprocate with 10% tariffs on American goods. The structure formalizes what had become the status quo over the last year.

Rare-Earth Concession: China agreed to issue six-month export licenses for rare-earth materials essential to U.S. electronics, automotive, and defense sectors.

Relaxation of Non-Tariff Measures: Export controls were modestly loosened, and restrictions on student visas for Chinese nationals have been relaxed, which may ease the climate for academic and professional exchange.

While headlines emphasized “agreement,” the reality is that the deal provides only narrow, conditional relief and does little to roll back the broader tariff architecture hurting American small enterprises.

Part 2: Current Landscape for Small Businesses & China

Before assessing the implications of the deal, it is important to understand the pressures already being experienced by small businesses:

Increased Supply Costs: Retailers, manufacturers, and e-commerce sellers reliant on imports have been particularly hard-hit by increased tariffs. The removal of the $800 “de minimis” exemption meant sudden cost spikes for previously low-tariff goods.

Planning Uncertainty: The unpredictability of trade negotiations has left small business owners unable to make informed decisions about inventory, pricing, or expansion.

Disrupted Cash Flow: Delays at ports and sudden changes in pricing structures have left many businesses with overstocked, overpriced inventory they cannot move.

Reduced Competitiveness: Higher input costs mean many small businesses can no longer compete with large corporations that have deeper reserves or more diversified supply chains.

Consumer Backlash: Price increases are alienating customers and diminishing brand loyalty for many small retailers.

Part 3: Sector-by-Sector Analysis – China

Let’s examine how this deal will impact different segments of the small business ecosystem.

Manufacturing

Impact: Moderate Relief.

For small manufacturers reliant on rare-earth materials, the six-month export licenses offer temporary breathing room. Sectors like electronics, defense subcontracting, and advanced manufacturing may see modest improvements in supply chain consistency.

Risks: The time-bound nature of the licenses makes long-term planning difficult. Any lapse in licensing will reintroduce chaos.

E-Commerce

Impact: Minimal to Negative.

Online sellers, particularly those importing fashion, gadgets, or toys, were previously protected by the de minimis exemption. With this gone and no rollback in tariffs, they are squeezed between rising costs and customer expectations for low prices.

Risks: Many sellers may exit the market or shift operations overseas.

Brick-and-Mortar Retail

Impact: Negative.

Stores relying on imported goods—from housewares to ethnic food supplies—will see no cost reduction. Without major economies of scale, small shops must raise prices or reduce product offerings.

Risks: Reduced foot traffic, lower profit margins, and possible closures.

Agriculture & Food Processing

Impact: Negligible.

Most food exports to China still face tariffs. While larger producers may negotiate their way through, small-scale farms and specialty producers face pricing disadvantages.

Risks: Loss of export competitiveness, oversupply in domestic markets.

Professional Services (Consulting, Legal, Educational)

Impact: Potentially Positive.

The easing of visa and academic restrictions may stimulate demand for consulting, education services, and cross-border partnerships.

Risks: Benefits are slow-moving and depend on broader geopolitical stabilization.

Part 4: What the Deal Does Not Address

Despite media attention, the deal sidesteps many of the deeper structural issues affecting small businesses:

No De-escalation Timeline: There is no roadmap for reducing tariffs further or restoring exemptions.

Temporary Nature of Relief: Six-month licenses are not sufficient for meaningful strategic planning.

No Domestic Support Programs: There is no corresponding federal relief for small firms affected by the tariffs.

No Infrastructure for Adaptation: Programs to help small businesses retool supply chains or go digital are still lacking.

No Harmonization of Standards: Differing regulations and standards continue to limit the ability of small businesses to export efficiently.

Part 5: Strategic Recommendations for Small Businesses and China

In light of these dynamics, small businesses must adopt proactive strategies:

1. Supply Chain Diversification

Identify suppliers in countries not subject to high tariffs. Consider nearshoring options such as Mexico, Canada, or domestic production where feasible.

2. Product Portfolio Optimization

Evaluate which products are most impacted by tariffs. Shift focus to less import-dependent or higher-margin offerings.

3. Financial Planning and Resilience

Engage in scenario planning. Consider factoring, SBA loans, or trade finance to stabilize cash flow in periods of uncertainty.

4. Advocacy and Alliances

Join trade associations or local chambers of commerce to advocate for small business interests in ongoing trade negotiations.

5. Customer Communication

Be transparent about price increases or product changes. Position your business as responsive and honest rather than reactive.

6. Digital Adaptation

Invest in e-commerce platforms, CRM tools, and logistics software to increase operational efficiency and customer engagement.

Part 6: The Broader Economic Picture

Small businesses are not isolated from macroeconomic trends. The deal may create the following broader conditions:

Improved Investor Confidence: Markets may respond positively to even temporary stability, which could ease borrowing conditions.

Inflation Management: Stabilizing trade could assist the Federal Reserve in maintaining inflation at the current 2.4% level.

Employment Outlook: Clarity in trade policy may encourage cautious hiring, particularly in sectors such as logistics, warehousing, and small-scale manufacturing.

However, these benefits are conditional and unevenly distributed. Without deeper structural reforms, the new agreement is unlikely to generate a large-scale recovery for the small business sector.

The June 11, 2025 U.S.-China trade agreement is a temporary truce rather than a resolution. While it introduces some modest benefits—particularly for manufacturing reliant on rare-earth minerals—it does little to ease the pain felt by the majority of small businesses still grappling with high tariffs, uncertain supply chains, and squeezed profit margins. Strategic adaptation, political advocacy, and operational resilience will be the keys to survival in this persistently volatile landscape. Until a more comprehensive agreement is reached, small businesses must continue to plan for instability and seize whatever limited advantages the current deal affords.

Briefing Document: Impact of the New U.S.-China Trade Deal on Small Businesses

Date: June 11, 2025 Source: Excerpts from “How the China Trade Deal Will Impact Small Businesses” by Chris Lehnes, Factoring Specialist

This briefing document summarizes the key themes, ideas, and facts presented in Chris Lehnes’ article “How the China Trade Deal Announced Today Will Impact Small Businesses,” published on June 11, 2025. The article assesses the implications of the new U.S.-China trade agreement for various small business sectors and offers strategic recommendations for adaptation.

1. Executive Summary: A “Temporary Stabilization” Not a “Comprehensive Resolution”

The recently announced U.S.-China trade agreement on June 11, 2025, is primarily described as a “temporary stabilization” rather than a significant breakthrough or “comprehensive resolution.” The deal maintains the “status quo” of existing high tariffs (55% on Chinese imports to the U.S. and 10% on U.S. exports to China), offering “minimal relief for most small businesses.” While it introduces limited concessions regarding rare-earth minerals and a relaxation of some non-tariff measures, it largely fails to address the deeper structural issues that have burdened small enterprises.

2. Key Elements of the New Trade Deal

The article highlights the following specific components of the June 11, 2025 agreement:

Tariffs Remain Largely Intact: “The U.S. will maintain approximately 55% tariffs on a wide range of Chinese imports. China will reciprocate with 10% tariffs on American goods.” This formalizes the existing tariff structure.

Rare-Earth Concession: China has agreed to “issue six-month export licenses for rare-earth materials essential to U.S. electronics, automotive, and defense sectors.”

Relaxation of Non-Tariff Measures: There has been a “modest loosening” of export controls and a relaxation of “restrictions on student visas for Chinese nationals,” which may “ease the climate for academic and professional exchange.”

Lehnes emphasizes that despite headlines, the deal offers “only narrow, conditional relief and does little to roll back the broader tariff architecture hurting American small enterprises.”

3. Current Landscape for Small Businesses: Pre-Existing Pressures

Before the deal, small businesses were already facing significant challenges due to the ongoing trade tensions:

Increased Supply Costs: Retailers, manufacturers, and e-commerce sellers dependent on imports “have been particularly hard-hit by increased tariffs.” The removal of the “$800 ‘de minimis’ exemption meant sudden cost spikes for previously low-tariff goods.”

Planning Uncertainty: “The unpredictability of trade negotiations has left small business owners unable to make informed decisions about inventory, pricing, or expansion.”

Disrupted Cash Flow: “Delays at ports and sudden changes in pricing structures have left many businesses with overstocked, overpriced inventory they cannot move.”

Reduced Competitiveness: “Higher input costs mean many small businesses can no longer compete with large corporations that have deeper reserves or more diversified supply chains.”

Consumer Backlash: “Price increases are alienating customers and diminishing brand loyalty for many small retailers.”

4. Sector-by-Sector Impact Analysis

The deal’s impact varies significantly across different small business sectors:

Manufacturing:Moderate Relief. Businesses reliant on rare-earth materials will experience “temporary breathing room” from the six-month export licenses. However, the “time-bound nature of the licenses makes long-term planning difficult.”

E-Commerce:Minimal to Negative. Online sellers previously protected by the “de minimis” exemption are now “squeezed between rising costs and customer expectations for low prices,” with many potentially having to “exit the market or shift operations overseas.”

Brick-and-Mortar Retail:Negative. Stores relying on imported goods “will see no cost reduction” and must “raise prices or reduce product offerings,” leading to “reduced foot traffic, lower profit margins, and possible closures.”

Agriculture & Food Processing:Negligible. Most food exports still face tariffs, making it difficult for “small-scale farms and specialty producers [to] face pricing disadvantages” and risk “loss of export competitiveness, oversupply in domestic markets.”

Professional Services (Consulting, Legal, Educational):Potentially Positive. The easing of visa and academic restrictions “may stimulate demand for consulting, education services, and cross-border partnerships,” though benefits are “slow-moving.”

5. What the Deal Does Not Address

The article identifies several critical omissions in the new agreement:

No De-escalation Timeline: “There is no roadmap for reducing tariffs further or restoring exemptions.”

Temporary Nature of Relief: “Six-month licenses are not sufficient for meaningful strategic planning.”

No Domestic Support Programs: “There is no corresponding federal relief for small firms affected by the tariffs.”

No Infrastructure for Adaptation: “Programs to help small businesses retool supply chains or go digital are still lacking.”

No Harmonization of Standards: “Differing regulations and standards continue to limit the ability of small businesses to export efficiently.”

6. Strategic Recommendations for Small Businesses

Given the persistent volatility, Lehnes advises small businesses to adopt proactive strategies:

Supply Chain Diversification: “Identify suppliers in countries not subject to high tariffs. Consider nearshoring options such as Mexico, Canada, or domestic production where feasible.”

Product Portfolio Optimization: “Evaluate which products are most impacted by tariffs. Shift focus to less import-dependent or higher-margin offerings.”

Financial Planning and Resilience: “Engage in scenario planning. Consider factoring, SBA loans, or trade finance to stabilize cash flow.”

Advocacy and Alliances: “Join trade associations or local chambers of commerce to advocate for small business interests.”

Customer Communication: “Be transparent about price increases or product changes.”

Digital Adaptation: “Invest in e-commerce platforms, CRM tools, and logistics software to increase operational efficiency.”

7. Broader Economic Picture and Conclusion

While the deal may lead to “improved investor confidence” and potentially assist with “inflation management” (currently at 2.4%), these benefits are “conditional and unevenly distributed.” The article concludes that “without deeper structural reforms, the new agreement is unlikely to generate a large-scale recovery for the small business sector.”

In essence, the June 11, 2025 U.S.-China trade agreement is a “temporary truce rather than a resolution.” Small businesses must continue to “plan for instability and seize whatever limited advantages the current deal affords.”

U.S.-China Trade Deal and Small Businesses: A Comprehensive Study Guide

I. Overview of the New U.S.-China Trade Deal (June 11, 2025)

Nature of the Agreement: A tentative, partial development aimed at temporary stabilization rather than a comprehensive resolution of economic tensions.

Tariff Structure:U.S. tariffs on Chinese imports: Approximately 55% (largely maintained).

China tariffs on U.S. exports: 10% (largely reciprocated).

Formalizes the status quo of the past year.

Key Concessions:Rare-Earth Materials: China to issue six-month export licenses for rare-earth materials vital to U.S. electronics, automotive, and defense sectors.

Non-Tariff Measures: Modest loosening of export controls and relaxation of student visa restrictions for Chinese nationals.

Overall Impact: Provides narrow, conditional relief and does little to roll back the broader tariff architecture impacting American small enterprises.

II. Current Landscape for Small Businesses Pre-Deal

Increased Supply Costs: Tariffs have significantly raised costs for retailers, manufacturers, and e-commerce sellers relying on imports. The removal of the $800 “de minimis” exemption exacerbated this.

Planning Uncertainty: Unpredictability of trade negotiations hinders informed decision-making on inventory, pricing, and expansion.

Disrupted Cash Flow: Delays at ports and sudden pricing changes lead to overstocked, overpriced inventory.

Reduced Competitiveness: Higher input costs make it difficult for small businesses to compete with large corporations with deeper reserves or diversified supply chains.

Consumer Backlash: Price increases alienate customers and diminish brand loyalty.

III. Sector-by-Sector Analysis of Deal Impact

Manufacturing:Impact: Moderate Relief. Temporary breathing room from six-month rare-earth export licenses for sectors like electronics, defense subcontracting, and advanced manufacturing.

Risks: Time-bound licenses make long-term planning difficult; potential reintroduction of chaos if licenses lapse.

E-Commerce:Impact: Minimal to Negative. No rollback of tariffs, and the removed de minimis exemption continues to squeeze online sellers.

Risks: Many sellers may exit the market or shift operations overseas.

Brick-and-Mortar Retail:Impact: Negative. No cost reduction for stores reliant on imported goods; must raise prices or reduce offerings without economies of scale.

Agriculture & Food Processing:Impact: Negligible. Most food exports to China still face tariffs; small-scale producers face pricing disadvantages.

Risks: Loss of export competitiveness, oversupply in domestic markets.

Professional Services (Consulting, Legal, Educational):Impact: Potentially Positive. Easing of visa and academic restrictions may stimulate demand for cross-border services and partnerships.

Risks: Benefits are slow-moving and contingent on broader geopolitical stabilization.

IV. What the Deal Does NOT Address

No De-escalation Timeline: Lacks a roadmap for further tariff reduction or exemption restoration.

Temporary Nature of Relief: Six-month licenses are insufficient for meaningful strategic planning.

No Domestic Support Programs: Absence of federal relief for small firms affected by tariffs.

No Infrastructure for Adaptation: Lacks programs to help small businesses retool supply chains or digitalize operations.

No Harmonization of Standards: Differing regulations continue to limit efficient small business exports.

V. Strategic Recommendations for Small Businesses

Supply Chain Diversification: Identify suppliers in low-tariff countries, consider nearshoring (Mexico, Canada), or domestic production.

Product Portfolio Optimization: Shift focus to less import-dependent or higher-margin offerings.

Financial Planning and Resilience: Engage in scenario planning, explore factoring, SBA loans, or trade finance to stabilize cash flow.

Advocacy and Alliances: Join trade associations or chambers of commerce to advocate for small business interests.

Customer Communication: Be transparent about price increases or product changes.

Digital Adaptation: Invest in e-commerce platforms, CRM tools, and logistics software.

Inflation Management: Could assist the Federal Reserve in maintaining inflation at 2.4%.

Employment Outlook: Clarity may encourage cautious hiring in logistics, warehousing, and small-scale manufacturing.

Overall Conclusion: The agreement is a temporary truce. Without deeper structural reforms, it’s unlikely to generate a large-scale recovery for the small business sector. Strategic adaptation and resilience are key to survival.

Quiz: U.S.-China Trade Deal Impact on Small Businesses

Instructions: Answer each question in 2-3 sentences.

What is the primary characteristic of the June 11, 2025, U.S.-China trade agreement, as described in the source?

How do the tariffs on Chinese imports and U.S. exports compare after the new deal?

Which specific material did China agree to issue export licenses for, and which U.S. sectors benefit?

Before the deal, what was a significant financial pressure on small businesses due to trade policies, specifically mentioned as being “gone”?

Why is the impact of the deal on the E-Commerce sector described as “Minimal to Negative”?

What is the primary risk for small manufacturers despite the temporary relief they might experience from the deal?

Beyond tariffs, what crucial aspect related to trade policy did the deal not address, which is vital for small business planning?

Name two specific strategic recommendations provided for small businesses to adapt to the current trade landscape.

How might the new trade deal indirectly impact broader investor confidence, according to the article?

What type of businesses within the “Professional Services” sector are expected to see a potentially positive impact from the deal?

Answer Key

The June 11, 2025, U.S.-China trade agreement is characterized as a tentative, partial development that offers temporary stabilization rather than a comprehensive resolution. It formalizes existing tariffs and provides only narrow, conditional relief.

After the new deal, the U.S. will maintain approximately 55% tariffs on a wide range of Chinese imports, while China will reciprocate with 10% tariffs on American goods. This structure largely formalizes the status quo of the past year.

China agreed to issue six-month export licenses for rare-earth materials. This concession is essential to U.S. electronics, automotive, and defense sectors, offering them temporary breathing room.

Before the deal, the removal of the $800 “de minimis” exemption was a significant financial pressure on small businesses, causing sudden cost spikes for previously low-tariff imported goods. This removal particularly affected retailers and e-commerce sellers.

The impact on the E-Commerce sector is “Minimal to Negative” because the deal did not roll back tariffs, and the prior protection offered by the de minimis exemption is gone. This leaves online sellers squeezed between rising costs and customer expectations for low prices, potentially forcing them to exit the market.

The primary risk for small manufacturers, despite the temporary relief from rare-earth licenses, is the time-bound nature of these licenses. This makes long-term planning difficult, as any lapse in licensing will reintroduce chaos and supply chain instability.

Beyond tariffs, the deal did not address a crucial aspect related to trade policy for small business planning: the lack of a de-escalation timeline. There is no roadmap for further reducing tariffs or restoring exemptions, leaving businesses with continued uncertainty.

Two strategic recommendations for small businesses are Supply Chain Diversification, which involves identifying suppliers in low-tariff countries or considering nearshoring, and Financial Planning and Resilience, which includes engaging in scenario planning and exploring financing options like SBA loans.

The new trade deal might indirectly impact broader investor confidence positively, as markets may respond to even temporary stability. This improved confidence could potentially ease borrowing conditions for businesses.

Businesses within the “Professional Services” sector, such as consulting, legal, and educational services, are expected to see a potentially positive impact. This is due to the easing of visa and academic restrictions, which may stimulate demand for cross-border partnerships and services.

Essay Format Questions

Analyze the primary characteristics of the June 11, 2025, U.S.-China trade agreement. Discuss how its “tentative” and “partial” nature distinguishes it from a comprehensive resolution, and explain the implications of maintaining existing tariff structures.

Evaluate the varying impacts of the new trade deal across different small business sectors (Manufacturing, E-Commerce, Brick-and-Mortar Retail, Agriculture & Food Processing, Professional Services). Why do some sectors experience “moderate relief” while others face “minimal to negative” consequences?

The article highlights several critical issues that the trade deal does not address. Discuss at least three of these unaddressed issues and explain how their omission continues to pose significant challenges for small businesses.

Propose a comprehensive strategic plan for a hypothetical small business (e.g., an e-commerce gadget seller or a small electronics manufacturer) based on the recommendations provided in the source. Justify how each chosen strategy directly addresses the specific challenges this business faces due to the current trade landscape.

Discuss the broader economic picture presented in the article. To what extent does the temporary stability offered by the deal contribute to “improved investor confidence,” “inflation management,” and a positive “employment outlook,” and what are the limitations or conditionalities of these benefits?

Glossary of Key Terms

Tariffs: Taxes imposed by a government on imported or exported goods. In this context, used by the U.S. and China to control trade flows.

Rare-Earth Materials: A group of 17 chemical elements essential for the production of high-tech devices, including electronics, electric vehicles, and defense systems. China is a dominant producer.

Export Controls: Government regulations that restrict or prohibit the export of certain goods, technologies, or services to specific destinations or entities.

De Minimis Exemption ($800): A U.S. Customs and Border Protection regulation that allowed imported goods valued at $800 or less to enter the country duty-free and with minimal formal entry procedures. Its removal significantly increased costs for many small businesses.

Supply Chain Diversification: The strategy of sourcing materials, components, or finished goods from multiple suppliers in different geographic locations to reduce reliance on a single source or region and mitigate risks.

Nearshoring: The practice of relocating business processes or production to a nearby country, often sharing a border or region, to reduce costs while maintaining geographical proximity.

Factoring: A financial transaction where a business sells its accounts receivable (invoices) to a third party (a “factor”) at a discount in exchange for immediate cash. Used to stabilize cash flow.

SBA Loans: Loans guaranteed by the U.S. Small Business Administration, designed to help small businesses access capital for various purposes, often with more favorable terms than traditional bank loans.

Trade Finance: Financial products and services that facilitate international trade and commerce, typically involving banks or financial institutions providing credit, guarantees, or insurance to mitigate risks for importers and exporters.

CRM Tools (Customer Relationship Management): Software systems designed to manage and analyze customer interactions and data throughout the customer lifecycle, with the goal of improving business relationships with customers and assisting in customer retention and sales growth.

Inflation Management: Actions taken by central banks or governments to control the rate at which prices for goods and services are rising, often targeting a specific inflation rate to maintain economic stability.

Latest OECD report states Trump Tariffs Will Drag Down Global Economy

The global economy stands at a critical juncture, and few forces have been as disruptive to recent economic stability as the imposition of sweeping tariffs by the Trump administration. As trade tensions escalate and markets adjust to the uncertainty, the Organization for Economic Cooperation and Development (OECD) has provided a sobering assessment of the economic outlook. Its most recent forecasts paint a picture of slowing growth, rising inflation, and waning consumer and business confidence. These effects are particularly acute in the United States and its closest trading partners, but the reverberations are felt globally.

This article examines the OECD’s latest outlook, exploring in detail how the Trump tariffs are affecting not only U.S. economic performance but also the broader global landscape. In doing so, it considers multiple dimensions of economic health, including GDP growth, inflation, employment, investment flows, and international trade dynamics.

A Shift Toward Protectionism with Tariffs

The Trump administration’s trade strategy marked a clear departure from decades of globalization and liberalized trade. Tariffs were framed as a means to protect American manufacturing, reduce trade deficits, and punish trading partners perceived to be engaging in unfair practices. The scope of these tariffs widened progressively, affecting steel, aluminum, electronics, textiles, autos, and more. In time, nearly all major U.S. trading partners were impacted, including China, the European Union, Canada, and Mexico.

What began as targeted tariffs quickly evolved into a broader trade confrontation, particularly with China. This escalation created significant distortions in global trade flows, forcing companies to reorganize supply chains and re-evaluate cross-border investments. These adjustments did not occur without cost.

Global Growth Slows due to tariffs

The most visible consequence of this new trade regime has been a sharp deceleration in global economic growth. Prior to the tariffs, global GDP was growing at a healthy pace, buoyed by rising demand, low interest rates, and expanding trade. However, in the aftermath of the tariffs, momentum has faltered. The OECD has lowered its growth forecasts for major economies across the board.

Many advanced economies are now projected to expand at a pace well below their long-term averages. Emerging markets, typically drivers of global growth, are also feeling the pinch, as they are highly sensitive to changes in global demand and commodity prices. The uncertainty generated by protectionist policies has caused companies to delay investments, curb hiring, and reduce output.

The U.S. Economy: Growth Dampened by Its Own Policies on tariffs

Ironically, the country that initiated the trade confrontation— the United States— is now among the hardest hit. The immediate impact of tariffs has been felt in consumer prices and business costs. With import duties increasing the price of foreign goods, businesses have faced higher input costs, particularly those reliant on complex global supply chains.

Manufacturers, especially in sectors like automotive, electronics, and machinery, have had to either absorb these higher costs or pass them on to consumers. This has triggered an uptick in inflation, even as wage growth and productivity gains remain modest. Consumer spending, a major driver of U.S. GDP, has started to show signs of fatigue.

Moreover, the uncertainty surrounding trade policy has led to a noticeable decline in private investment. Companies are reluctant to commit capital when future market access is uncertain or when tariffs could suddenly reshape competitive dynamics. This erosion of business confidence is directly undermining one of the traditional engines of U.S. economic growth.

Inflation Pressures Build due to tariffs

As tariffs raise the prices of imported goods, inflationary pressures are intensifying. While inflation can sometimes be a sign of economic strength, in this context it is more indicative of cost-push rather than demand-pull dynamics. Prices are rising not because of booming demand, but because of higher costs embedded in the supply chain.

The burden of these price increases falls disproportionately on consumers and small businesses. Lower-income households, which spend a larger share of their income on goods subject to tariffs, are particularly vulnerable. Similarly, small and medium-sized enterprises, which lack the pricing power and supply chain flexibility of larger firms, are experiencing severe financial strain.

Rising inflation also complicates monetary policy. Central banks, already constrained by low interest rates, face a dilemma: tightening policy to rein in inflation could further stifle growth, while maintaining loose conditions might entrench inflation expectations.

Investment Stalls

Uncertainty is the enemy of investment, and trade policy under the Trump administration has become a textbook example of unpredictability. The back-and-forth nature of trade negotiations, combined with the abrupt announcement of new tariffs, has left many firms hesitant to make long-term commitments.

Foreign direct investment into the U.S. has slowed, and American firms are increasingly looking to offshore operations in more stable regulatory environments. The ripple effects are evident in capital expenditure reports and survey-based measures of business sentiment, both of which show a marked decline.

In particular, industries that rely on complex global value chains are under pressure. These include high-tech manufacturing, aerospace, and consumer electronics. As costs rise and policy uncertainty persists, many of these firms are deferring or canceling expansion plans.

Impact on Employment from tariffs

The labor market has also begun to show signs of stress. While overall unemployment remains low by historical standards, job growth has moderated significantly. Sectors exposed to international trade, such as manufacturing and agriculture, have seen layoffs and reduced hours.

Farmers have been among the most vocal critics of the tariffs. Retaliatory measures by other countries have targeted U.S. agricultural exports, including soybeans, pork, and dairy products. This has led to a glut in domestic supply, falling prices, and rising financial distress in rural communities.

Moreover, the expected resurgence in domestic manufacturing employment has not materialized. While some firms have expanded operations, these gains have been modest and insufficient to offset losses in other areas. Many manufacturing jobs today require advanced skills and capital-intensive facilities, limiting the potential for large-scale employment gains.

Global Supply Chains Disrupted

Modern manufacturing is built on intricate supply chains that span multiple countries. Tariffs disrupt these networks by raising costs, increasing delays, and complicating logistics. In response, many companies are reconfiguring their sourcing strategies.

Some are seeking alternative suppliers in countries not affected by tariffs, while others are investing in new facilities closer to end markets. However, such adjustments are time-consuming and expensive. The short-term effect is reduced efficiency and higher costs, which are eventually passed on to consumers.

These disruptions are particularly problematic for industries that depend on just-in-time delivery and highly coordinated production processes. Automakers, for example, often rely on components manufactured in multiple countries. Tariffs on any part of the chain can compromise the entire system.

Spillover Effects on Trading Partners

The economic fallout from U.S. tariffs is not confined to American shores. Countries closely tied to the U.S. economy are experiencing significant secondary effects. Canada and Mexico, for example, are contending with both direct tariffs and the broader uncertainty created by fluctuating trade policy.

Export-oriented economies in Asia and Europe have also been affected. Lower demand from the U.S., combined with rising input costs, has slowed industrial output and exports. In some cases, retaliatory tariffs have further eroded market access for these countries’ producers.

Emerging markets face a dual challenge. On one hand, they suffer from reduced export opportunities; on the other, they face capital outflows as investors seek the relative safety of advanced economies. This has led to currency depreciation, inflation, and tighter monetary conditions in many developing countries.

Consumer Confidence Weakens

Tariffs may be abstract policy tools for policymakers, but their effects are very real for consumers. As prices rise and news of trade disputes dominates headlines, consumer sentiment has declined. Surveys indicate growing pessimism about future economic conditions, job security, and the affordability of essential goods.

This erosion in consumer confidence is worrisome, as it can feed into a self-reinforcing cycle. When consumers cut back on spending in anticipation of tougher times, demand weakens further, leading to slower growth and potentially higher unemployment.

Retailers are already reporting slower foot traffic and reduced sales in certain categories, especially those heavily dependent on imported goods. Discount chains and e-commerce platforms are faring better, but the overall retail environment has become more challenging.

Policy Uncertainty as a Drag on Growth

Beyond the immediate effects of tariffs, the broader issue of policy uncertainty is exerting a powerful drag on economic performance. Businesses operate best when rules are clear and stable. The abrupt shifts in trade policy, often announced via social media or in press conferences without prior consultation, have created a volatile environment.

This volatility not only affects investment and hiring decisions but also undermines global confidence in the reliability of the U.S. as a trading partner. Some countries are responding by pursuing trade agreements that exclude the United States, thereby reducing its influence in setting global economic rules.

Moreover, the politicization of trade policy has made it more difficult to reach bipartisan consensus on future directions. This increases the risk that trade tensions will persist, even as administrations change.

Long-Term Structural Implications

While some of the effects of tariffs are short-term and cyclical, others have longer-lasting implications. The erosion of multilateral trade institutions, the reorientation of supply chains, and the shift in global investment patterns all represent structural changes.

These shifts could lead to a more fragmented global economy, characterized by regional trading blocs and reduced efficiency. For the United States, this may mean diminished leadership in global economic governance and reduced access to emerging markets.

Domestically, the shift away from open markets may entrench inefficiencies and reduce the incentive for innovation. While some industries may benefit from temporary protection, the lack of competitive pressure can lead to complacency and stagnation.

Conclusion: Charting a Path Forward

The OECD’s latest outlook makes it clear that the economic costs of protectionism are mounting. The promise of reviving domestic manufacturing and reducing trade deficits has, so far, not materialized in a meaningful or sustainable way. Instead, the data shows slower growth, higher inflation, weaker investment, and declining consumer and business confidence.

To reverse these trends, policymakers will need to rethink their approach to trade. This means re-engaging with international partners, restoring faith in multilateral institutions, and crafting policies that support both competitiveness and inclusivity. Trade policy should be informed by data, guided by long-term strategy, and executed with transparency.

For businesses, the lesson is clear: agility and adaptability are more important than ever. Firms that can navigate complexity, diversify their markets, and invest in innovation will be best positioned to thrive in an uncertain world.

Ultimately, the path forward will require cooperation, not confrontation. In a deeply interconnected global economy, prosperity is best achieved not by building walls, but by building bridges.

1. A Shift Towards Protectionism and Its Broad Scope:

The Trump administration’s trade strategy marked a significant departure from decades of globalized and liberalized trade.

Tariffs were implemented with the stated goals of protecting American manufacturing, reducing trade deficits, and punishing perceived unfair trading practices.

The scope of these tariffs widened progressively, impacting “steel, aluminum, electronics, textiles, autos, and more,” eventually affecting “nearly all major U.S. trading partners, including China, the European Union, Canada, and Mexico.”

This escalation led to “significant distortions in global trade flows, forcing companies to reorganize supply chains and re-evaluate cross-border investments.”

2. Global Economic Slowdown:

The most visible consequence of the new trade regime has been a “sharp deceleration in global economic growth.”

The OECD (Organization for Economic Cooperation and Development) has “lowered its growth forecasts for major economies across the board.”

Advanced economies are projected to grow “well below their long-term averages,” and emerging markets are also “feeling the pinch.”

“The uncertainty generated by protectionist policies has caused companies to delay investments, curb hiring, and reduce output.”

3. Negative Impact on the U.S. Economy:

Ironically, the U.S. is “among the hardest hit” by its own policies.

Increased Costs and Inflation: Tariffs have led to “higher input costs” for businesses, especially those reliant on global supply chains. Manufacturers “have had to either absorb these higher costs or pass them on to consumers,” triggering an “uptick in inflation.”

Weakened Consumer Spending: “Consumer spending, a major driver of U.S. GDP, has started to show signs of fatigue.”

Decline in Private Investment: “The uncertainty surrounding trade policy has led to a noticeable decline in private investment.” Companies are “reluctant to commit capital when future market access is uncertain or when tariffs could suddenly reshape competitive dynamics.”

Cost-Push Inflation: Inflation is described as “cost-push rather than demand-pull dynamics,” meaning “prices are rising not because of booming demand, but because of higher costs embedded in the supply chain.” This disproportionately affects “consumers and small businesses,” particularly “lower-income households.”

Monetary Policy Dilemma: Rising inflation “complicates monetary policy,” as central banks face the dilemma of tightening policy to rein in inflation (which could stifle growth) or maintaining loose conditions (which might entrench inflation expectations).

4. Stalled Investment and Employment Concerns:

Uncertainty as an Investment Barrier: “Uncertainty is the enemy of investment, and trade policy under the Trump administration has become a textbook example of unpredictability.”

Reduced FDI: “Foreign direct investment into the U.S. has slowed, and American firms are increasingly looking to offshore operations in more stable regulatory environments.”

Stress on the Labor Market: While overall unemployment remains low, “job growth has moderated significantly.”

Impact on Specific Sectors: “Sectors exposed to international trade, such as manufacturing and agriculture, have seen layoffs and reduced hours.” Farmers have been particularly affected by “retaliatory measures by other countries” targeting U.S. agricultural exports.

Limited Manufacturing Gains: The “expected resurgence in domestic manufacturing employment has not materialized,” with gains being “modest and insufficient to offset losses in other areas.”

5. Disruption of Global Supply Chains:

Tariffs “disrupt these networks by raising costs, increasing delays, and complicating logistics.”

Companies are reconfiguring sourcing strategies, “seeking alternative suppliers” or “investing in new facilities closer to end markets.” These adjustments are “time-consuming and expensive,” leading to “reduced efficiency and higher costs.”

This is particularly problematic for industries relying on “just-in-time delivery and highly coordinated production processes,” such as automakers.

6. Spillover Effects on Trading Partners:

The economic fallout is not confined to the U.S. “Countries closely tied to the U.S. economy are experiencing significant secondary effects.”

Canada and Mexico face “direct tariffs and the broader uncertainty.”

Export-oriented economies in Asia and Europe have seen “slower industrial output and exports.”

Emerging markets face “reduced export opportunities” and “capital outflows,” leading to “currency depreciation, inflation, and tighter monetary conditions.”

7. Weakening Consumer Confidence:

Consumer sentiment has “declined” due to rising prices and trade disputes, leading to “growing pessimism about future economic conditions, job security, and the affordability of essential goods.”

This erosion in confidence can create a “self-reinforcing cycle” where reduced spending further weakens demand.

8. Policy Uncertainty as a Drag on Growth:

Beyond immediate tariff effects, “the broader issue of policy uncertainty is exerting a powerful drag on economic performance.”

“Abrupt shifts in trade policy, often announced via social media or in press conferences without prior consultation, have created a volatile environment.”

This volatility “undermines global confidence in the reliability of the U.S. as a trading partner,” leading some countries to “pursue trade agreements that exclude the United States.”

9. Long-Term Structural Implications:

The tariffs have “longer-lasting implications,” including the “erosion of multilateral trade institutions, the reorientation of supply chains, and the shift in global investment patterns.”

These shifts “could lead to a more fragmented global economy, characterized by regional trading blocs and reduced efficiency.”

Domestically, a shift away from open markets “may entrench inefficiencies and reduce the incentive for innovation.”

10. Conclusion and Path Forward:

The OECD’s outlook indicates that “the economic costs of protectionism are mounting.”

The promise of reviving domestic manufacturing and reducing trade deficits “has, so far, not materialized in a meaningful or sustainable way.”

To reverse these trends, policymakers need to “rethink their approach to trade,” including “re-engaging with international partners, restoring faith in multilateral institutions, and crafting policies that support both competitiveness and inclusivity.”

The article concludes that “prosperity is best achieved not by building walls, but by building bridges.”

The Economic Impact of Trump Tariffs: A Study Guide

This study guide is designed to help you review and deepen your understanding of the provided article, “Trump Tariffs Will Drag Down Global Economy” by Chris Lehnes.

I. Summary of Key Arguments

The article argues that the Trump administration’s tariffs have had a significant negative impact on the global economy, contrary to their stated goals of protecting American manufacturing and reducing trade deficits. The Organization for Economic Cooperation and Development (OECD) forecasts indicate slowing global growth, rising inflation, and declining consumer and business confidence. These effects are felt globally, with the U.S. and its trading partners being particularly affected. The article details how these tariffs have disrupted global supply chains, stifled investment, impacted employment, and weakened consumer confidence, ultimately leading to a more fragmented global economy and diminished U.S. economic leadership.

II. Study Questions

Answer the following questions to test your comprehension of the source material.

Short-Answer Questions:

What was the stated purpose of the Trump administration’s tariffs, and how did they differ from previous trade strategies? The Trump administration framed tariffs as a means to protect American manufacturing, reduce trade deficits, and punish perceived unfair trading practices. This marked a clear departure from decades of globalization and liberalized trade, as tariffs were broadened to affect nearly all major U.S. trading partners.

According to the OECD, what are the primary economic consequences of these tariffs? The OECD’s latest forecasts indicate a picture of slowing global growth, rising inflation, and waning consumer and business confidence. These negative effects are acutely felt in the United States and its closest trading partners, but their reverberations extend globally.

How have the tariffs ironically impacted the U.S. economy, the country that initiated them? The U.S. economy has been among the hardest hit, experiencing increased consumer prices and business costs due to import duties. This has led to higher input costs for businesses, particularly those with complex global supply chains, and a noticeable decline in private investment due to policy uncertainty.

Explain the nature of the inflation triggered by the tariffs. Is it demand-pull or cost-push? The inflation triggered by the tariffs is primarily cost-push, meaning prices are rising due to higher costs embedded in the supply chain rather than booming demand. This occurs as import duties increase the price of foreign goods and businesses pass these higher input costs on to consumers.

Why has investment stalled, both foreign and domestic, in the wake of the tariffs? Investment has stalled because policy uncertainty under the Trump administration created an unpredictable environment. The back-and-forth nature of trade negotiations and abrupt tariff announcements made firms hesitant to make long-term commitments, leading to reduced foreign direct investment and deferred domestic expansion plans.

Which sectors of the U.S. labor market have been particularly affected by the tariffs, and why? Sectors exposed to international trade, such as manufacturing and agriculture, have seen layoffs and reduced hours. Farmers, in particular, have been hit hard by retaliatory measures targeting U.S. agricultural exports, leading to domestic supply gluts and financial distress.

How have global supply chains been disrupted, and what are companies doing in response? Tariffs disrupt global supply chains by raising costs, increasing delays, and complicating logistics. In response, many companies are reconfiguring sourcing strategies, seeking alternative suppliers, or investing in new facilities closer to end markets, though these adjustments are time-consuming and expensive.

Describe the “spillover effects” on U.S. trading partners. Provide examples. U.S. trading partners, like Canada, Mexico, and export-oriented economies in Asia and Europe, have experienced significant secondary effects. These include lower demand from the U.S., rising input costs, slowed industrial output, and in some cases, retaliatory tariffs further eroding their market access.

How has consumer confidence been impacted, and what are the potential consequences of this decline? Consumer sentiment has declined due to rising prices and news of trade disputes, leading to growing pessimism about future economic conditions. This erosion is worrisome as it can create a self-reinforcing cycle where consumers cut back on spending, further weakening demand and leading to slower growth.

What are the long-term structural implications of the Trump administration’s trade policies mentioned in the article? Long-term implications include the erosion of multilateral trade institutions, reorientation of supply chains, and shifts in global investment patterns, potentially leading to a more fragmented global economy. For the U.S., this may mean diminished leadership and reduced access to emerging markets, while domestically, it could entrench inefficiencies.

Essay Format Questions:

Analyze the paradox presented in the article: how did the Trump administration’s tariffs, intended to benefit the U.S. economy, ultimately dampen its growth? Discuss the specific mechanisms (e.g., inflation, investment, employment) through which this occurred.

Evaluate the article’s claim that policy uncertainty has been a significant drag on economic performance. How does this uncertainty manifest, and what are its broad economic consequences for both businesses and global trade relations?

Discuss the concept of “cost-push inflation” as explained in the article. How do tariffs contribute to this type of inflation, and what are the disproportionate burdens it places on different economic actors?

Examine the ripple effects of the Trump tariffs on the global economy beyond the United States. How have emerging markets, advanced economies, and global supply chains been affected, and what does this suggest about the interconnectedness of the modern global economy?

Based on the article’s conclusion, what policy recommendations are suggested to reverse the negative economic trends caused by protectionism? Discuss the shift in approach called for and its potential benefits for global economic stability.

III. Glossary of Key Terms

Tariffs: Taxes or duties to be paid on a particular class of imports or exports. In the context of the article, these are import taxes imposed by the Trump administration.

OECD (Organization for Economic Cooperation and Development): An intergovernmental economic organization with 38 member countries, founded in 1961 to stimulate economic progress and world trade. The article refers to its economic forecasts.

Globalization: The process by which businesses or other organizations develop international influence or start operating on an international scale. The article states Trump’s strategy departed from decades of globalization.

Liberalized Trade: The process of reducing trade barriers such as tariffs and quotas between countries to promote free trade.

Trade Deficits: The amount by which the cost of a country’s imports exceeds the value of its exports. A stated goal of the Trump tariffs was to reduce these.

GDP (Gross Domestic Product): The total monetary or market value of all the finished goods and services produced within a country’s borders in a specific time period. A key measure of economic health.

Inflation: A general increase in prices and fall in the purchasing value of money. The article discusses cost-push inflation resulting from tariffs.

Consumer Confidence: An economic indicator that measures the degree of optimism consumers feel about the overall state of the economy and their personal financial situation. It influences consumer spending.

Business Confidence: An indicator that measures the level of optimism or pessimism among businesses about the future performance of the economy. It affects investment and hiring decisions.

Protectionism: The theory or practice of shielding a country’s domestic industries from foreign competition by taxing imports.

Supply Chains: The sequence of processes involved in the production and distribution of a commodity. Tariffs have caused significant disruptions to these global networks.

Private Investment: Spending by businesses on capital goods (e.g., machinery, buildings) and inventory. The article notes a decline in this due to uncertainty.

Cost-Push Inflation: Inflation caused by an increase in prices of inputs (e.g., raw materials, labor) which then pushes up the costs of production for firms.

Demand-Pull Inflation: Inflation caused by an excess of total demand over total supply in an economy.

Monetary Policy: The actions undertaken by a central bank to influence the availability and cost of money and credit to help promote national economic goals.

Foreign Direct Investment (FDI): An investment made by a company or individual in one country into business interests located in another country.

Capital Expenditure (CapEx): Funds used by a company to acquire, upgrade, and maintain physical assets such as property, plants, buildings, technology, or equipment.

Retaliatory Measures/Tariffs: Tariffs imposed by one country in response to tariffs imposed by another country, often targeting specific export goods.

Multilateral Trade Institutions: Organizations like the WTO (World Trade Organization) that facilitate trade agreements and resolve disputes among multiple countries. The article suggests their erosion.

Global Value Chains: The full range of activities that firms and workers perform to bring a product from its conception to end use, which are spread across multiple countries.

The Far-Reaching Economic Consequences of a U.S. Credit Rating Downgrade by Moody’s

When a credit rating agency like Moody’s downgrades the United States’ credit rating, it sends ripples not just through financial markets, but through every corner of the global economy. While the immediate headlines often focus on political dysfunction or fiscal sustainability, the longer-term ramifications of such a downgrade are far more complex, systemic, and potentially destabilizing. A Moody’s downgrade of U.S. sovereign debt signals a fundamental reassessment of America’s creditworthiness and forces investors, policymakers, and institutions to recalibrate their expectations about the world’s most important economy.

This article explores the deeper consequences such a downgrade can trigger—ranging from higher borrowing costs and currency volatility to systemic global shifts in capital allocation and long-term economic growth.

Understanding the Significance of a Credit Downgrade

Moody’s, along with Standard & Poor’s and Fitch Ratings, is one of the “Big Three” credit rating agencies that assess the ability of borrowers—from corporations to countries—to repay their debt. A downgrade of the U.S. credit rating means that Moody’s has lost some confidence in the federal government’s ability or willingness to meet its financial obligations.

Historically, U.S. debt has been viewed as the safest investment on the planet—a benchmark for global finance. A downgrade disrupts that perception and introduces doubt about America’s fiscal and political stability. This isn’t just symbolic. It has concrete consequences that ripple through every layer of the economy.

1. Higher Borrowing Costs Across the Board

Perhaps the most immediate impact of a credit downgrade is a rise in borrowing costs. U.S. Treasury yields serve as the benchmark interest rates for a vast array of financial products—from corporate loans and mortgages to municipal bonds and student loans. When Moody’s downgrades U.S. debt, it effectively tells the world that lending to the U.S. is riskier than before. Investors demand higher yields to compensate for that risk.

This increase in yields is not confined to the federal government. As Treasury rates rise, so do rates on other types of credit. The private sector finds it more expensive to borrow money for investment, expansion, or hiring. Consumers face higher mortgage rates, credit card interest, and auto loan costs.

Over time, these higher costs dampen economic activity, slow housing markets, reduce business investment, and weaken consumer spending—key drivers of GDP growth.

2. Fiscal Constraints and Deficit Challenges

The U.S. government already spends a significant portion of its annual budget servicing its debt. As interest rates rise due to a downgrade, the cost of servicing the national debt increases, further straining the federal budget. This leaves less room for essential spending on infrastructure, education, social programs, or national defense.

Moreover, larger interest payments make it harder to reduce budget deficits, potentially triggering a vicious cycle: higher deficits lead to lower credit ratings, which in turn lead to higher interest payments, and so on.

This dynamic threatens long-term fiscal sustainability and places added pressure on lawmakers to make politically difficult choices—cut spending, raise taxes, or both.

3. Loss of the U.S. Dollar’s Preeminence

One of the most profound long-term risks of a downgrade is its potential impact on the U.S. dollar’s status as the world’s primary reserve currency. This status gives the United States enormous advantages: it can borrow cheaply, influence global trade terms, and maintain geopolitical leverage.

However, a downgrade chips away at global confidence in the stability and reliability of U.S. financial governance. While there is currently no obvious alternative to the dollar, the downgrade may accelerate efforts by countries like China and Russia to promote alternative reserve currencies or diversify their foreign exchange reserves.

A diminished role for the dollar would reduce demand for U.S. assets, further raise borrowing costs, and weaken America’s global economic influence.

4. Investor Confidence and Market Volatility

Financial markets thrive on confidence and predictability—two qualities that a downgrade undermines. Investors, particularly institutional ones such as pension funds, sovereign wealth funds, and insurance companies, may be forced to reassess their U.S. holdings in light of new risk profiles.

Many of these institutions have mandates that require them to hold only top-rated assets. A downgrade from Moody’s could trigger automatic selling of U.S. Treasury securities, contributing to market volatility and raising yields further.

Stock markets also typically react negatively to such downgrades, as they signal macroeconomic instability. Drops in equity valuations can erode household wealth and consumer confidence, especially in a country where a significant portion of retirement savings is tied to the stock market.

5. Damage to U.S. Political Credibility

Credit rating agencies often cite political gridlock and dysfunctional governance as key reasons for a downgrade. For instance, prolonged battles over raising the debt ceiling or passing a federal budget suggest an inability or unwillingness to govern effectively.

Such perceptions damage the U.S.’s reputation not just as a borrower but as a global leader. Allies may question America’s reliability, while adversaries exploit the narrative of decline.

Domestically, a downgrade can become a political flashpoint, further deepening partisan divides and making it even harder to implement the structural reforms needed to restore fiscal balance.

6. Global Economic Repercussions

Because the U.S. economy is so deeply integrated into the global financial system, a downgrade does not stay contained within U.S. borders.

International investors, central banks, and governments hold trillions of dollars in U.S. debt. A downgrade can unsettle these holdings, reduce global confidence in U.S. monetary policy, and spark volatility in emerging markets, which often peg their currencies or base their financial models on the stability of the dollar.

Higher U.S. interest rates can lead to capital flight from developing countries, triggering currency crises, inflation, or debt defaults in those regions. This can contribute to global financial instability and economic slowdowns far from American shores.

7. Potential Policy Responses and Long-Term Adjustments

In response to a downgrade, the U.S. government and Federal Reserve may adopt countermeasures to stabilize the economy. The Fed could delay interest rate hikes or resume quantitative easing to keep borrowing costs manageable. The Treasury could restructure its debt issuance strategy.

However, these tools have limitations and risks. Loose monetary policy could stoke inflation, while fiscal tightening could slow the recovery or deepen a recession.

Long-term, the downgrade should serve as a wake-up call for more serious structural reforms. These include revisiting entitlement spending, tax reform, and implementing automatic stabilizers to reduce the frequency of political standoffs over the budget.

Conclusion: More Than Just a Symbolic Setback

A downgrade of the U.S. credit rating by Moody’s is far more than a symbolic black mark on the nation’s fiscal record. It is a powerful signal to markets, institutions, and policymakers that the foundations of America’s economic dominance are no longer unshakable. The downgrade has the potential to trigger a chain reaction—raising borrowing costs, reducing investment, and sowing doubt about the future of the global financial system anchored by the U.S. dollar.

The real danger lies not just in the immediate market reaction, but in the structural challenges it exposes and exacerbates. If left unaddressed, the consequences of a downgrade could reshape the global economic landscape for years to come.

Subject: Analysis of the potential economic ramifications of a downgrade to the United States’ credit rating by Moody’s.

Executive Summary:

A downgrade of the U.S. credit rating by Moody’s is not merely a symbolic event but a significant signal with far-reaching economic consequences. It signifies a loss of confidence in the U.S. government’s ability or willingness to meet its financial obligations, disrupting the perception of U.S. debt as the safest investment globally. The primary impacts include higher borrowing costs across the board, increased fiscal constraints on the government, potential erosion of the U.S. dollar’s preeminence, diminished investor confidence and market volatility, damage to U.S. political credibility, and significant global economic repercussions. Addressing the structural issues leading to a downgrade is crucial for long-term economic stability.

Key Themes and Most Important Ideas/Facts:

Significance of the Downgrade:

A downgrade by one of the “Big Three” agencies (Moody’s, S&P, Fitch) signifies a reassessment of the U.S.’s creditworthiness.

It directly challenges the historical perception of U.S. debt as the “safest investment on the planet.”

This disruption introduces “doubt about America’s fiscal and political stability” with tangible economic consequences.

Higher Borrowing Costs:

This is identified as “Perhaps the most immediate impact.”

U.S. Treasury yields serve as a benchmark for various financial products (corporate loans, mortgages, municipal bonds, student loans).

A downgrade makes lending to the U.S. riskier, prompting investors to “demand higher yields to compensate for that risk.”

This increase in borrowing costs extends beyond the federal government to the private sector and consumers, “dampen[ing] economic activity, slow[ing] housing markets, reduc[ing] business investment, and weaken[ing] consumer spending.”

Fiscal Constraints and Deficit Challenges:

Rising interest rates on U.S. debt due to a downgrade increase the cost of debt servicing, further straining the federal budget.

This limits available funds for essential spending on infrastructure, education, social programs, and defense.

It creates a “vicious cycle: higher deficits lead to lower credit ratings, which in turn lead to higher interest payments, and so on.”

This dynamic exacerbates the difficulty of reducing budget deficits and forces “politically difficult choices—cut spending, raise taxes, or both.”

Loss of U.S. Dollar’s Preeminence:

This is highlighted as “One of the most profound long-term risks.”

The dollar’s status as the primary reserve currency offers significant advantages (cheap borrowing, influence on trade, geopolitical leverage).

A downgrade “chips away at global confidence in the stability and reliability of U.S. financial governance.”

While no immediate alternative exists, it may “accelerate efforts by countries like China and Russia to promote alternative reserve currencies or diversify their foreign exchange reserves.”

A diminished dollar role would “reduce demand for U.S. assets, further raise borrowing costs, and weaken America’s global economic influence.”

Investor Confidence and Market Volatility:

Downgrades undermine the “confidence and predictability” on which financial markets rely.

Institutional investors (pension funds, sovereign wealth funds, insurance companies) may be forced to “reassess their U.S. holdings in light of new risk profiles.”

Mandates requiring holding only top-rated assets could trigger “automatic selling of U.S. Treasury securities,” contributing to volatility and higher yields.

Stock markets typically react negatively, as downgrades “signal macroeconomic instability,” eroding household wealth and consumer confidence.

Damage to U.S. Political Credibility:

Credit rating agencies often cite “political gridlock and dysfunctional governance” as reasons for a downgrade.

Issues like debt ceiling battles and budget standoffs suggest an inability to govern effectively.

This damages the U.S.’s reputation as a borrower and “as a global leader.”

Domestically, it can become a “political flashpoint, further deepening partisan divides,” making reforms harder.

Global Economic Repercussions:

Due to the U.S. economy’s global integration, a downgrade’s effects extend beyond U.S. borders.

It can “unsettle” the trillions of dollars in U.S. debt held by international investors, central banks, and governments.

Higher U.S. interest rates can trigger “capital flight from developing countries,” potentially leading to “currency crises, inflation, or debt defaults in those regions.”