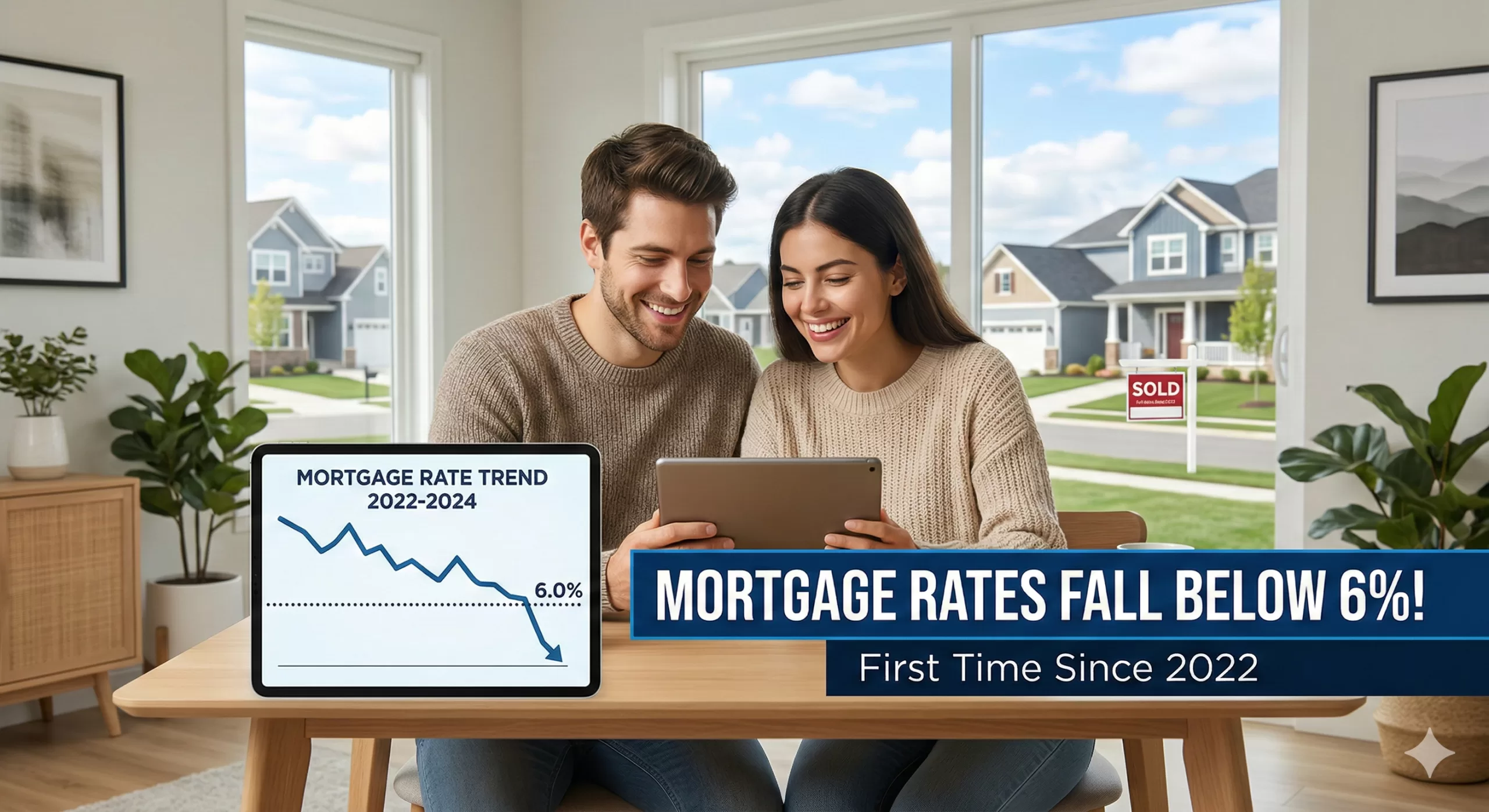

Mortgage Rates – The housing market has seen a welcome shift! Mortgage rates have fallen below 6% for the first time since 2022, offering a significant improvement for potential homebuyers. This news comes as a breath of fresh air after a period of steadily climbing rates that have put a strain on many budgets.

What Does This Mean for Potential Homebuyers?

The drop in mortgage rates translates directly into increased affordability for those looking to purchase a home. This can be beneficial in several ways:

Lower Monthly Payments: A lower interest rate means a smaller portion of your monthly payment goes towards interest, reducing your overall housing cost.

Increased Buying Power: With lower monthly payments, you may be able to qualify for a larger loan amount, potentially allowing you to purchase a more expensive home.

Refinancing Opportunities: Existing homeowners who currently have a higher mortgage rate may be able to refinance their loan and save money on their monthly payments.

Why Are Mortgage Rates Falling?

While the exact reasons behind the rate drop are complex, several factors may be contributing to the trend:

Lower Inflation: Inflation has shown signs of cooling down, which can influence interest rates.

Economic Growth: While economic growth has been moderate, some signs suggest it may be slowing, which can also affect mortgage rates.

Changes in the Bond Market: Bond yields, which are closely tied to mortgage rates, have also seen a decline.

What Should You Do Now?

If you’ve been on the fence about buying a home, this could be an excellent time to re-evaluate your options. Here are some steps to consider:

Get Pre-Approved for a Mortgage: This will give you a clear idea of how much you can borrow and help you understand your monthly payment.

Shop Around for Rates: Different lenders offer varying rates, so it’s essential to compare offers from multiple institutions.

Consider Your Long-Term Goals: While the lower rates are attractive, it’s crucial to ensure that buying a home is the right decision for your long-term financial goals.

Important Note: It’s important to remember that mortgage rates are subject to change based on economic conditions and other factors. While the current trend is encouraging, it’s essential to stay informed about any potential shifts in the market.

Conclusion:

The drop in mortgage rates below 6% is a significant development for the housing market, offering some much-needed relief to potential homebuyers and homeowners alike. If you’ve been considering buying a home, this could be the right time to take action. With lower monthly payments and increased buying power, you may be closer to achieving your homeownership goals than you thought. However, it’s crucial to act carefully and seek professional advice to make the best decision for your individual situation.

Primary Data Sources

Freddie Mac (Primary Mortgage Market Survey): The ultimate source for the 5.98% figure. Freddie Mac released its weekly report on February 26, 2026, confirming that the 30-year fixed-rate mortgage dipped below 6% for the first time in approximately 3.5 years.

The Federal Reserve (FRED): Used to verify historical trends, specifically confirming that the last time rates were at this level was September 8, 2022 (when they were 5.89%).

CBS News: Provided context on the White House’s initiatives (such as the $200 billion mortgage bond purchase plan) and expert commentary on the “spring home-buying season.”

Associated Press (AP): Detailed the influence of the 10-year Treasury yield on mortgage pricing and quoted housing economists regarding market entry for buyers and sellers.

Mortgage rates in 2026 forecast This video provides expert analysis on how these sub-6% rates impact monthly affordability and what to expect for the rest of the 2026 housing market

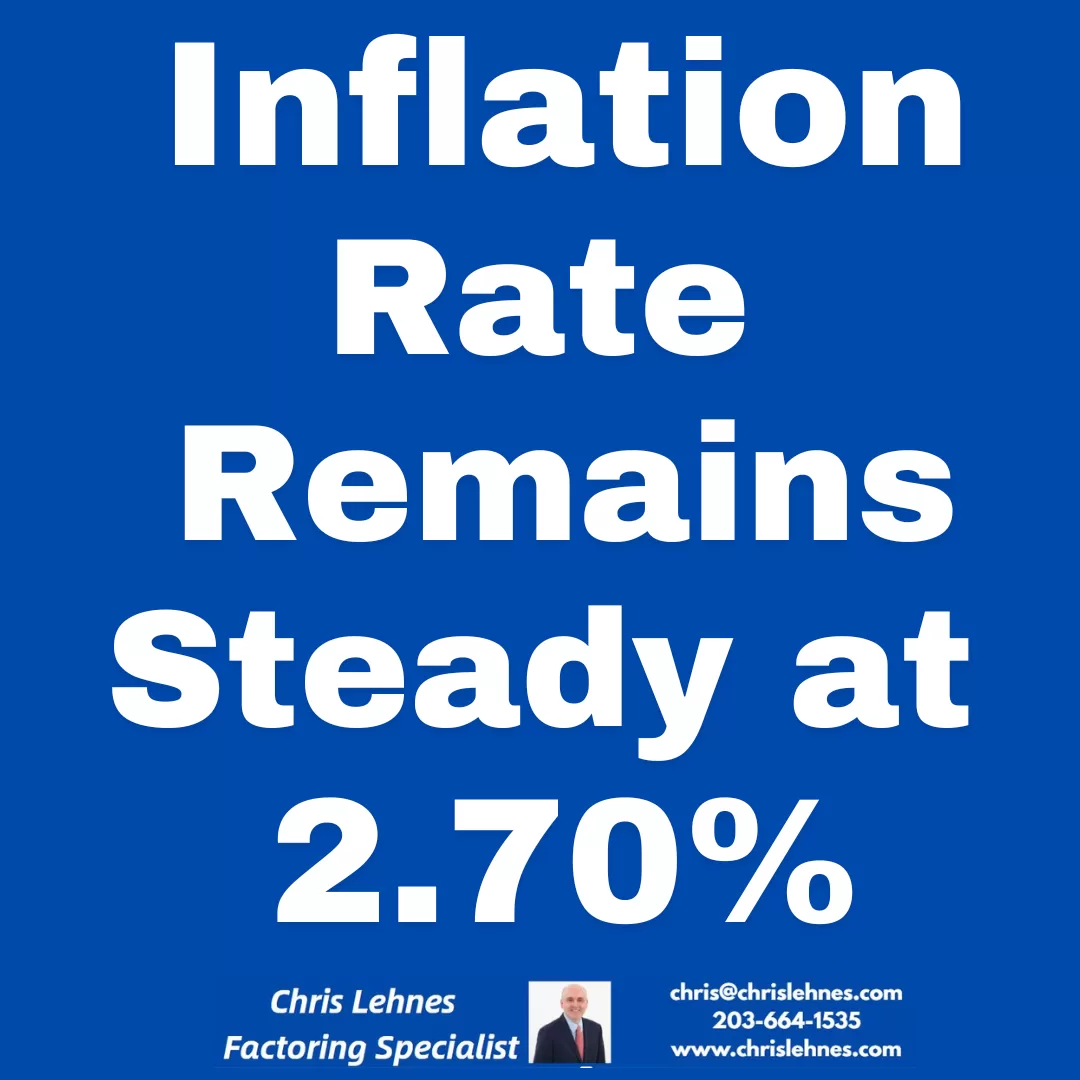

The Inflation “Split Screen”: What December’s CPI Numbers Really Mean

Inflation Stable. The latest data is in, and it paints a picture of an economy caught between cooling pressures and political friction. In December, consumer prices rose 2.7% from a year earlier—holding steady from November and landing exactly where economists predicted.

While the “headline” number suggests stability, the story beneath the surface is much more complex. Here are the key takeaways from the final inflation report of 2025.

1. Stability Amidst the Noise

For the second month in a row, inflation has leveled off at 2.7%. Meanwhile, “Core CPI” (which strips out volatile food and energy costs) rose 2.6%.

Interestingly, these numbers came in slightly better than the 2.8% core increase some experts feared. This suggests that despite the introduction of steep tariffs earlier in 2025, businesses haven’t yet passed the full weight of those costs onto consumers. However, the “last mile” of the journey back to the Fed’s 2% target remains stubbornly out of reach.

2. A Cloud of Data Uncertainty

This report is the first “clean” look at inflation we’ve had in months. Following a government shutdown last fall, the Labor Department had to rely on technical workarounds to fill data gaps.

The “Payback” Effect: Many economists believe November’s figures may have been artificially low due to those data collection issues.

The Verdict: While December’s numbers didn’t spike as much as feared, they likely reflect a correction for the missing data from previous months.

3. The Fed’s High-Stakes Balancing Act

The Federal Reserve is currently navigating a “split screen” economy. On one hand, growth remains solid; on the other, the labor market has cooled significantly. In fact, 2025 saw the lowest pace of job growth since 2003 (excluding major recessions).

The Fed cut rates three times at the end of 2025 to support the job market, but officials are now divided. With inflation still above 2%, some are hesitant to keep cutting—especially as they watch for the inflationary impact of the One Big Beautiful Bill Act and ongoing investments in AI.

4. Politics vs. Policy

Perhaps the most unusual backdrop to this report is the unprecedented political pressure on independent agencies.

The Labor Department: Its commissioner was fired in August amidst claims of “rigged” numbers.

The Fed: Chair Jerome Powell recently alleged that the administration has used threats of criminal prosecution to pressure the board into lowering interest rates.

What’s Next?

As we head into 2026, all eyes are on January and February. This is traditionally when businesses reset their pricing for the year. Whether they will hike prices to account for tariffs and tax-cut-driven demand remains the big question.

For now, the “meandering path” toward lower inflation continues, but with a cooling job market and political volatility, the road ahead looks anything but smooth.

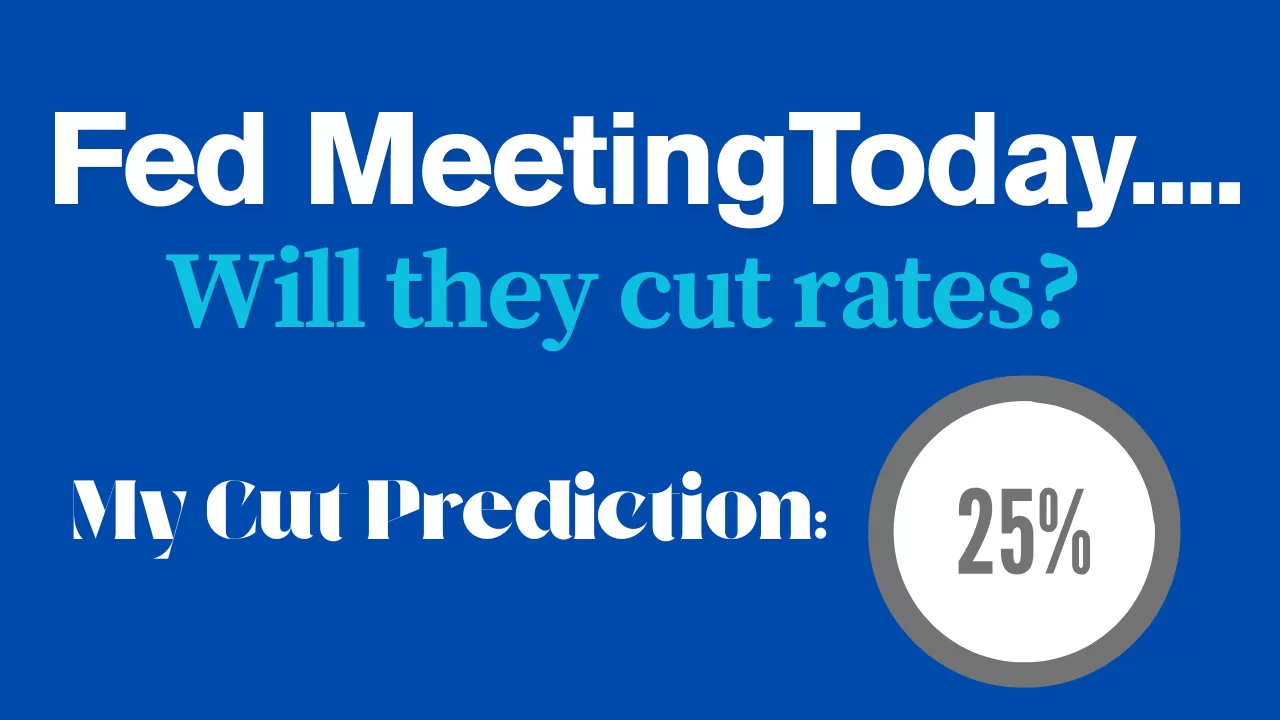

As the Federal Open Market Committee (FOMC) wraps up its final meeting of 2025 today, all eyes are on the 2:00 PM EST announcement. With the U.S. economy cooling and the labor market showing signs of strain, speculation is high that a Fed Cut in rates is imminent.

Here is a breakdown of the current predictions, the economic data driving the decision, and what odds makers are betting on.

The Consensus: A “December Cut” is Highly Likely

Market watchers are overwhelmingly pricing in a 25-basis-point (0.25%) rate cut.

According to the CME FedWatch Tool, which tracks trading in federal funds futures, there is currently an 87% probability that the Fed will lower the target range to 3.50%–3.75%. This would mark the third consecutive rate reduction, following cuts in September and October, signaling a definitive shift from fighting inflation to supporting the labor market.

Key Factors the Fed is Weighing

The Fed’s “dual mandate” requires it to balance stable prices with maximum employment. For the first time in years, the risks have shifted from overheating inflation to a cooling jobs market.

1. The Cooling Labor Market (The Primary Driver) The unemployment rate has ticked up to 4.4%, a figure that has caught the attention of Fed Chair Jerome Powell. While historically low, the steady rise suggests that high interest rates are finally biting into corporate hiring. Job growth has slowed, and layoffs in sensitive sectors have increased. The Fed is keen to avoid a “hard landing” where unemployment spikes uncontrollably.

2. Sticky but Manageable Inflation Inflation hasn’t disappeared, but it is no longer the five-alarm fire it was two years ago. The latest PCE (Personal Consumption Expenditures) data places headline inflation around 2.7%–2.9%, with core inflation hovering near 2.8%. While this is still above the Fed’s 2% target, it is trending in the right direction, giving the central bank “air cover” to cut rates to support jobs without immediately reigniting price hikes.

3. Economic Growth (GDP) GDP growth has moderated to an annualized rate of roughly 1.8%–2.0%. This suggests the economy is slowing down but not crashing—the definition of the elusive “soft landing.” A rate cut now is viewed as insurance to keep this momentum from stalling out completely in early 2026.

The “Wild Card”: A Divided Committee

Despite the high odds of a cut, this meeting is not without tension. Reports suggest the FOMC is sharply divided.

** The Doves (Cut Now):** Worried that waiting too long will cause a recession. They argue that with inflation falling, real interest rates are effectively rising, tightening financial conditions more than intended.

The Hawks (Pause/Hold): Concerned that cutting rates too quickly could cause inflation to flare up again, especially given that the economy is still growing.

Because of this division, the language in today’s statement will be just as important as the rate decision itself. Investors should look for clues about a “pause” in January. Many analysts believe the Fed may cut today but signal a skip in the next meeting to assess the impact of recent cuts.

What to Watch For

2:00 PM EST: The official statement and decision. Look for the “dot plot” (Summary of Economic Projections) to see where officials expect rates to be at the end of 2026.

2:30 PM EST: Chair Jerome Powell’s press conference. His tone regarding the “balance of risks” will move markets. If he sounds more worried about jobs than inflation, it will confirm that the easing cycle has further to go.

Bottom Line

While nothing is guaranteed until the gavel falls, the smart money is on a 0.25% cut today. The Fed likely views the rising unemployment rate as a warning light it cannot ignore, making a rate reduction the prudent move to secure a soft landing for 2026.

Category

Case for a Rate Cut (The “Doves”)

Case for Holding Steady (The “Hawks”)

Labor Market

Rising Risks: Unemployment has climbed to 4.4%. Doves argue that high rates are now doing unnecessary damage to hiring.

Hidden Strength: Some argue the job market is “normalizing” after the post-pandemic surge rather than collapsing.

Inflation

Progress Made: While at 2.8%, inflation is down significantly from its peak. High “real” rates (inflation vs. interest) are overly restrictive.

Sticky Prices: Inflation remains above the 2% target. Rate cuts could embolden businesses to keep prices high or raise them.

Economic Growth

Growth is Slowing: GDP growth has dipped toward 1.8%. A cut acts as “insurance” to prevent a recession in 2026.

Consumer Resilience: High durable goods spending suggests the economy is not yet in need of a stimulus.

Market Impact

Easing the Burden: Lower rates would provide immediate relief for credit card holders and small businesses facing high debt costs.

Asset Bubbles: Cutting too soon could overheat the stock and housing markets, leading to a boom-bust cycle.

The Federal Reserve has decided to cut the benchmark interest rate by 25 basis points (0.25%).

This move lowers the target range for the federal funds rate to 3.50% to 3.75%. This is the third consecutive rate cut this year and was made in light of elevated inflation and a weakening labor market.

Here are the key takeaways from the announcement and Chair Jerome Powell’s press conference:

✂️ Key Interest Rate Decision

The Cut: The Federal Open Market Committee (FOMC) voted to lower the target range for the federal funds rate by 25 basis points to 3.50%–3.75%.

The Vote: The decision was not unanimous, recording a 9:3 ratio of votes.

One member (Stephen I. Miran) preferred a larger, 50-basis-point cut.

Two members (Austan D. Goolsbee and Jeffrey R. Schmid) preferred no change, keeping the rate steady.

🎙️ Key Quotes and Context from Chair Powell

Powell’s remarks focused on the shifting balance of risks and the current policy stance:

Rationale for the Cut:“With today’s decision, we have lowered our policy rate three-quarters of a percentage point over our last three meetings. This further normalization of our policy stance should help stabilize the labor market while allowing inflation to resume its downward trend toward 2% once the effects of tariffs have passed through.”

The Dual Mandate Challenge: Powell acknowledged the difficulty of balancing the Fed’s two goals (maximum employment and price stability):”In the near term, risks to inflation are tilted to the upside and risks to employment to the downside—a challenging situation… We have one tool. It can’t do both of those—you can’t address both of those at once.”

Forward Guidance (What’s Next): The Fed indicated a cautious, data-dependent approach moving forward:”In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks.” When asked about a pause, Powell suggested the policy rate is now close to the “neutral” level: He indicated that the Fed’s benchmark rate is now likely somewhere close to the “neutral” level… which certainly indicates that he won’t be in a hurry to extend the string of cuts the Fed has made in recent months.

Economic Outlook and Projections (“Dot Plot”): The latest projections indicated a divided committee on future cuts.

The median Fed official is penciling in one rate cut for next year (2026), which is a more cautious outlook than some market expectations.

The Fed projects inflation (based on its preferred gauge) to ease to 2.4% by the end of 2026.

Based on the immediate market data and analyst reactions following the 2:00 PM announcement, here is how the decision is impacting mortgage rates and the stock market.

🏠 Impact on Mortgage Rates

The Verdict: Rates may hold steady or even tick up slightly, despite the Fed cutting rates.

Counter-Intuitive Movement: It often surprises borrowers, but mortgage rates do not move 1-for-1 with the Fed’s rate. Mortgage rates track the 10-year Treasury yield, which actually rose today (hitting roughly 4.21%).

Why? The market had already “priced in” this cut weeks ago. Investors are now looking ahead to 2026. Because the Fed signaled a slower pace for future cuts (a “hawkish cut”), bond markets reacted by pushing long-term yields higher.

Forecast: Experts expect 30-year fixed mortgage rates to hover in the low-to-mid 6% range for now. A significant drop below 6% is unlikely until investors see clearer signs that inflation is permanently defeated.

📈 Impact on the Stock Market

The Verdict: A “Santa Claus Rally” is likely, but 2026 looks choppier.

Immediate Reaction: The S&P 500 and Dow Jones both rose following the news, pushing close to all-time highs. The market “got what it wanted”—a cut to support the economy without panic.

Sector Watch:

Small Caps (Russell 2000): Often benefit most from rate cuts as they rely more on floating-rate debt.

Tech & Growth: Continued to show strength, though valuations remain high.

2026 Outlook: The Fed’s “dot plot” shows they plan to slow down, potentially cutting rates only once in 2026. This is fewer cuts than Wall Street hoped for, which suggests the “easy money” rally might face headwinds early next year as recession risks are still on the table (J.P. Morgan analysts cite a 35% recession probability for 2026).

Area

Short-Term Forecast (Dec ’25)

Why?

Mortgage Rates

Steady / Slight Rise

The cut was already priced in; long-term bond yields are rising.

Stocks

Bullish (Rally)

The “soft landing” narrative is intact; investors are relieved.

Savings Accounts

Slight Drop

High-yield savings rates will drop almost immediately by ~0.25%.

Federal Reserve Monetary Policy and Leadership Outlook

Executive Summary

The Federal Reserve has implemented its second consecutive monthly interest rate cut, lowering the target range by a quarter-point to 3.75%-4.0%. The 10-2 vote by the Federal Open Market Committee (FOMC) highlights internal division among policymakers regarding the path of monetary policy, a decision made amidst sustained pressure from President Donald Trump for more aggressive easing. The outlook for future cuts remains uncertain, complicated by an ongoing federal government shutdown that has postponed the release of critical economic data on inflation and unemployment. Despite this data blackout, investor sentiment currently favors another quarter-point reduction in December, supported by recent private-sector reports indicating a “softening” labor market. Concurrently, the administration is actively considering a successor for Fed Chair Jerome Powell, whose term expires in May 2026, with a list of five candidates being prepared for the President’s review.

——————————————————————————–

I. October 2025 Interest Rate Decision

The Federal Open Market Committee (FOMC) voted on Wednesday, October 29, 2025, to lower its benchmark interest rate, marking the second straight month of monetary easing.

Rate Adjustment: The committee approved a quarter-point reduction.

New Target Range: The interest rate is now set to a range between 3.75% and 4.0%.

Previous Target Range: This is down from the 4.0% to 4.25% range established at the previous month’s meeting.

Committee Vote: The decision passed with a 10-2 vote, indicating some dissent among policymakers regarding the move.

II. Influencing Factors and Economic Context

The Fed’s decision-making process is being influenced by a combination of political pressure, economic data limitations, and emerging concerns about the labor market.

A. Political Pressure

The rate cut follows months of public pressure and criticism from President Donald Trump.

The President has been advocating for steeper and more aggressive cuts to monetary policy.

B. Economic Data Blackout

An ongoing federal government shutdown has significantly hampered the Fed’s ability to assess the U.S. economy’s health.

Key economic reports, including those on inflation and unemployment, have been postponed.

Fed Governor Christopher Waller acknowledged the challenge, stating that because policymakers “don’t know which way the data will break on this conflict,” the FOMC must “move with care” when adjusting rates.

In the absence of official data, Waller noted he has spoken with “business contacts” to help form his economic outlook.

C. Labor Market Concerns

Fed Governor Christopher Waller indicated his focus has shifted from inflation to a “softening” labor market, a stance that supported his vote for the recent rate cut.

This view is corroborated by reports from several firms and economists released in recent weeks, which suggest the labor market has continued to deteriorate. This emerging private-sector data could provide the FOMC with a rationale for an additional rate cut.

III. Future Monetary Policy Outlook

Market expectations are leaning towards further easing, though Fed officials have previously expressed division on the matter.

Investor Expectations: According to CME’s FedWatch tool, investors are favoring an additional quarter-point interest rate reduction at the FOMC’s final 2025 meeting in December.

Potential December Rate: Such a cut would lower the target range to between 3.5% and 3.75%.

Official Division: Minutes from the previous month’s meeting showed that Fed officials were divided on whether a third rate cut in the year would be necessary.

IV. Federal Reserve Leadership Transition

The administration is actively planning for the future leadership of the central bank as the end of Chair Jerome Powell’s term approaches.

Chair’s Term: Jerome Powell’s term as Federal Reserve Chair is set to expire in May 2026.

Succession Plan: Treasury Secretary Scott Bessent confirmed on Monday that a list of candidates to succeed Powell would be presented to President Trump shortly after Thanksgiving.

Candidate Shortlist: Bessent identified five individuals currently under consideration for the role:

Four Cracks in the Foundation: What the Fed’s Rate Cut Really Reveals

Introduction: Beyond the Headlines

The Federal Reserve has cut interest rates for the second straight month, a headline that suggests a confident response to evolving economic conditions. But simmering beneath the surface are the persistent calls for even easier monetary policy from the White House, adding a layer of political drama to an already difficult decision.

A closer look reveals that this rate cut is not a confident step forward; it’s a hesitant move by a divided committee flying blind in a political storm. The real story isn’t the cut itself, but the four converging pressures that expose a deeper crisis of confidence inside our nation’s central bank. But what’s really happening behind those closed doors?

This analysis breaks down the four most impactful and surprising takeaways from the Federal Reserve’s latest move, revealing a clearer picture of the profound challenges shaping U.S. economic policy today and the volatility that may lie ahead.

1. The Fed is Divided: This Was Not a Unanimous Decision

The Federal Open Market Committee (FOMC) voted to lower its key interest rate by a quarter-point, setting the new range between 3.75% and 4%, down from the previous 4% to 4.25%. The critical detail, however, was the 10-2 vote. This rare public dissent reveals deep fractures in the FOMC’s consensus about the path forward.

For markets and businesses, a divided Fed is an unpredictable Fed. This lack of consensus makes it significantly harder to forecast future policy, injecting a fresh dose of potential volatility into the economy. This internal disagreement is hardly surprising, given that policymakers are being forced to navigate without their most trusted instruments.

2. Flying Blind: The Fed is Making Decisions Without Key Data

Compounding the internal division is a startling “data blackout.” An ongoing federal government shutdown has postponed the release of official reports on inflation and unemployment—the two most vital metrics the central bank relies on. This data vacuum forces the Fed to make billion-dollar decisions in a veritable fog.

Policymakers are left to rely on alternative, anecdotal evidence. Fed Governor Christopher Waller noted he has been speaking with “business contacts” to form his economic outlook. While necessary, this reliance on informal data is fraught with risk. It lacks statistical rigor, is potentially biased, and dramatically increases the danger of a policy misstep. As Governor Waller himself acknowledged, this precarious situation demands extreme caution.

…because policymakers “don’t know which way the data will break on this conflict,” the FOMC would “need to move with care” when adjusting interest rates.

3. The Focus is Shifting: A “Softening” Labor Market is the New Top Concern

For months, inflation has been the Fed’s primary dragon to slay. Now, a monumental shift is underway. Fed Governor Christopher Waller recently stated his focus has pivoted from inflation to the “softening” labor market.

The significance of this pivot cannot be overstated. It signals that the Fed’s tolerance for inflation may be increasing if the alternative is rising unemployment. This represents a critical change in the central bank’s risk assessment, prioritizing job preservation over absolute price stability for the first time in this cycle. With recent reports from private firms suggesting the labor market has continued to deteriorate, the committee may find the justification it needs for another cut in December.

4. Political Pressure and a Looming Leadership Change

The Fed’s internal challenges are amplified by significant external pressures, most notably from President Donald Trump, who has been publicly demanding “steeper cuts.” This external pressure from the White House further complicates the internal debates, potentially widening the rift between committee members who prioritize preemptive action and those who advocate for patience.

This political context is intensified by an impending leadership transition. Fed Chair Jerome Powell’s term expires in May 2026, and the conversation about his successor has already begun. Treasury Secretary Scott Bessent has confirmed five candidates are under consideration:

Fed Governor Christopher Waller

Fed Governor Michelle Bowman

Former Fed Governor Kevin Warsh

National Economic Council Director Kevin Hassett

BlackRock executive Rick Rieder

Conclusion: Navigating in a Fog

The Federal Reserve’s latest interest rate cut is not a sign of clear sailing but rather a reflection of an institution navigating through a dense fog. Plagued by internal fractures, a critical lack of official economic data, and persistent political pressure, the central bank is operating under an extraordinary degree of uncertainty. This complex reality is far more revealing than the simple headline of another rate cut.

With the economy’s true health obscured by a data blackout, can the divided Fed steer us clear of a downturn, or is more volatility inevitable?

The Fed’s Big Move: What an Interest Rate Cut Means for You and the Economy

Introduction: Demystifying the Fed’s Power

The Federal Reserve is one of the most powerful economic forces in the United States, and its decisions can ripple through the entire country. The purpose of this article is to explain, in plain language, what the Federal Reserve is, why it changes interest rates, and what its most recent decision means for the economy. At the heart of these critical decisions is a small but influential group known as the FOMC.

1. Who Decides? Meet the FOMC

The Federal Open Market Committee (FOMC) is the part of the Federal Reserve that votes on the nation’s monetary policy, including whether to raise or lower interest rates. Their decisions, however, are not always unanimous. The most recent vote, for instance, was 10-2, which shows that there can be differing opinions among the committee members on the best path forward for the economy.

Now that we know who makes the decision, let’s examine the specific action they took.

2. The Main Event: A Quarter-Point Rate Cut

The FOMC recently voted to lower its key interest rate. This marks the second straight month that the central bank has decided to ease its monetary policy.

Here is a clear breakdown of the change:

Previous Rate Range

New Rate Range

4% to 4.25%

3.75% to 4%

This “quarter-point” reduction simply means the rate was lowered by 0.25%. But a small change like this signals a significant shift in the Fed’s thinking, which leads to a crucial question: why did they make this change?

3. The ‘Why’ Behind the Cut: A Softening Economy

The primary reason for the rate cut is that policymakers are concerned about a “softening” labor market.

Fed Governor Christopher Waller highlighted this concern, indicating his focus had shifted to a “softening” labor market instead of inflation. His viewpoint is supported by recent data; reports from various firms and economists suggest that the labor market has “continued to deteriorate,” which could provide the FOMC with the evidence it needs to support an additional cut in the future.

Of course, not everyone agrees on the Fed’s actions or what should happen next.

4. A Contentious Decision: Different Views on the Economy

The Federal Reserve’s decisions are often the subject of intense debate and are made under significant outside pressure. The latest rate cut is no exception, with several competing viewpoints at play.

President Trump’s View: The President has been a vocal critic, applying pressure on the Fed and calling for “steeper cuts” to interest rates.

Internal Division: The 10-2 vote demonstrates a lack of consensus within the FOMC itself. Last month, Fed officials appeared “divided over whether to cut rates for a third time this year,” underscoring this internal disagreement.

A Data Dilemma: The Fed is facing a major challenge due to an “ongoing federal government shutdown,” which has postponed the release of key reports on inflation and unemployment. This data blackout has forced policymakers like Governor Waller to rely on conversations with their “business contacts” to form an outlook on the economy.

These debates and challenges naturally lead to questions about what the Federal Reserve might do in the future.

5. What Happens Next? Reading the Tea Leaves

Based on the current situation, the future path of interest rates remains uncertain, but there are several key things to watch.

Investor Expectations: According to CME’s FedWatch tool, investors are currently “favoring an additional quarter-point reduction” at the FOMC’s next meeting in December.

The Fed’s Caution: Governor Christopher Waller emphasized the need for prudence, stating that because policymakers “don’t know which way the data will break,” the FOMC would “need to move with care” when adjusting interest rates.

Leadership Questions: President Trump is expected to name his pick to succeed Fed Chair Jerome Powell, whose term expires in May 2026. The candidates under consideration include Fed governors Christopher Waller and Michelle Bowman, former Fed governor Kevin Warsh, National Economic Council Director Kevin Hassett, and BlackRock executive Rick Rieder.

These factors will shape the economic landscape in the months to come.

Conclusion: Your Key Takeaways

To wrap up, understanding the Federal Reserve doesn’t have to be complicated. Here are the most important lessons from their recent decision.

The Federal Reserve, through its FOMC, manages the economy by adjusting interest rates to respond to issues like a weakening labor market.

Lowering interest rates is a tool to encourage economic activity, but decisions on when and how much to cut are complex and often debated.

The Fed’s actions are influenced by economic data, political pressure, and differing expert opinions, making their future moves something that everyone, from investors to the general public, watches closely.

Business World Review – The health of the U.S. economy is currently a mixed bag, with recent data showing both surprising strength and underlying weaknesses.

The U.S. economy grew at a 3.0% annualized rate in the second quarter of 2025, a significant reversal from the 0.5% contraction in the first quarter.

A major factor in the Q2 growth was a sharp drop in imports, the largest since the COVID-19 pandemic. This decrease was largely a result of companies stockpiling goods in Q1 to get ahead of proposed tariff hikes. This has led some economists to caution that the headline GDP number is masking a slowing in underlying economic performance. A more stable measure of core growth, which excludes volatile items, slowed to 1.2% in Q2 from 1.9% in Q1.

Inflationary pressures have continued to moderate. The core Personal Consumption Expenditures (PCE) index, a key inflation gauge for the Federal Reserve, rose 2.5% in Q2, down from 3.5% in Q1. This has led to expectations that the Fed may consider cutting interest rates.

Job Growth Slowing: Recent reports indicate a softening labor market. The economy added just 73,000 jobs in July, with significant downward revisions to the May and June figures, suggesting a much weaker job market than previously thought.

Despite the slowdown in job creation, the overall unemployment rate remains low at 4.2% as of July. However, this masks disparities, with recent college graduates and younger workers facing a tougher job market. The labor force participation rate for prime-age workers (25-54) has been solid, but the rate for workers 55 or older has declined to an eighteen-year low, reflecting broader demographic trends.

The labor market is showing a unique pattern of gradual softening rather than a sharp downturn. Companies are pulling back on new hires but are not yet engaging in widespread layoffs. The voluntary resignation rate, a measure of worker confidence, has also dropped below pre-pandemic levels.

President Donald Trump’s trade policies, including newly reinstated import tariffs, are a central source of uncertainty. Economists are divided on the impact, with some arguing they will damage the economy by raising costs and others acknowledging they are meant to protect American jobs. The anticipation and implementation of these tariffs have caused significant volatility in trade and investment.

The Federal Reserve is under pressure to cut interest rates, but it has so far held off, citing low unemployment and elevated inflation. However, the recent weak jobs report has increased the likelihood of a rate cut in September.

Consumer spending has shown lackluster growth, and private investment has plunged. This suggests that households and businesses are becoming more cautious amid policy uncertainty.

The International Monetary Fund (IMF) has raised its global and U.S. growth forecasts for 2025, citing a weaker-than-expected impact from tariffs. However, the IMF warns that risks are still tilted to the downside if trade tensions escalate. The Federal Reserve Bank of Atlanta’s “GDPNow” model is currently forecasting a 2.1% growth rate for the third quarter of 2025.

Accounts Receivable Factoring can quickly provide cash to businesses which do not qualify for traditional bank financing.

When Will the Federal Reserve Raise Interest Rates?

An In-Depth Analysis of the Timing, Triggers, and Consequences of the Next Rate Hike

Introduction

The Federal Reserve stands at a critical crossroads in its long history of managing the U.S. economy. After a period of rapid interest rate hikes between 2022 and 2023 aimed at curbing inflation, the Fed has shifted to a more cautious and observant stance. Interest rates are at their highest levels in over two decades, and with inflation cooling and economic indicators giving mixed signals, the burning question among investors, economists, and policymakers alike is: When will the Federal Reserve raise interest rates again—if at all?

This article aims to offer a comprehensive and speculative exploration of the likely timeline and conditions under which the Federal Reserve could initiate its next rate hike. We’ll analyze historical patterns, dissect macroeconomic indicators, evaluate the central bank’s public communications, and simulate various economic scenarios that could trigger a shift in policy.

The Current Monetary Policy Landscape

As of mid-2025, the federal funds target rate sits in a range of 5.25% to 5.50%, where it has remained since the Fed’s last hike in 2023. This level, historically high by post-2008 standards, reflects the Fed’s aggressive response to the inflation surge that followed the COVID-19 pandemic and related fiscal stimulus measures.

Since the pause in hikes, inflation has receded significantly, but it has not returned fully to the Fed’s 2% target. The economy has shown signs of resilience, yet some indicators—like slowing job growth and weakening manufacturing—suggest fragility. Meanwhile, consumer spending remains surprisingly robust, adding to the complexity of the Fed’s decision-making calculus.

To speculate credibly on the next rate hike, we must first understand the Fed’s mandate, the tools at its disposal, and the historical context that informs its behavior.

The Fed’s Dual Mandate and Policy Tools

The Federal Reserve has a dual mandate: to promote maximum employment and price stability. Balancing these two goals often involves trade-offs. When inflation is too high, the Fed raises interest rates to cool demand. When unemployment rises or economic growth falters, the Fed cuts rates to stimulate activity.

Interest rate decisions are made by the Federal Open Market Committee (FOMC), which meets eight times a year to assess economic conditions. The key instrument is the federal funds rate—the interest rate at which banks lend reserves to each other overnight. By adjusting this rate, the Fed influences borrowing costs throughout the economy, affecting everything from mortgage rates to business investment decisions.

Historical Precedents: How the Fed Has Acted in Similar Environments

History is a valuable guide. In past cycles, the Fed has typically paused for 6 to 18 months after ending a hiking cycle before reversing course. For example:

1980s Volcker Era: After taming double-digit inflation, the Fed paused, then resumed hikes when inflation showed signs of reacceleration.

2006–2008: The Fed paused in 2006 after raising rates from 1% to 5.25%, then began cutting in 2007 as the housing market collapsed.

2015–2018 Cycle: Rates were hiked gradually and paused in 2019 before being cut again in response to trade tensions and a slowing global economy.

These cases show that the Fed prefers to pause for an extended period before changing course—unless dramatic data forces its hand.

Speculative Scenario 1: A Surprise Inflation Resurgence

One possible trigger for a rate hike is a renewed surge in inflation. While inflation has cooled from its peak, it remains above the Fed’s 2% target. Core inflation, particularly in services and housing, has proven sticky. Wage growth continues to outpace productivity, suggesting embedded price pressures.

If inflation, as measured by the Personal Consumption Expenditures (PCE) index, rises from the current 2.7% range back above 3% and remains elevated for multiple quarters, the Fed may be forced to act. In such a scenario, markets would likely price in another rate hike by late 2025 or early 2026.

Indicators to watch:

Monthly CPI and PCE reports

Wage growth (especially in services)

Commodity prices, particularly oil and food

Consumer inflation expectations

If these metrics rise and stay elevated, particularly in the absence of strong GDP growth, the Fed would likely consider at least one additional hike to maintain credibility.

Speculated Timing: Q1 2026 Likelihood: Moderate Market reaction: Short-term bond yields rise, equity markets sell off, dollar strengthens.

Speculative Scenario 2: Global Economic Shocks

The Fed’s policy is not shaped solely by domestic data. Global events—like a commodity shock, geopolitical crisis, or surge in foreign inflation—could impact U.S. inflation indirectly.

For example, if conflict in the Middle East disrupts oil supply, driving crude prices back above $120 per barrel, energy inflation could spread through the economy. Similarly, if China reopens more aggressively and global demand surges, prices for industrial commodities and goods may rise.

In such a scenario, even if U.S. growth remains moderate, the Fed may view inflationary pressure as externally driven but persistent enough to warrant another hike.

Speculated Timing: Q2 2026 Likelihood: Low to moderate Market reaction: Volatile; inflation-linked assets outperform, defensive stocks gain favor.

Speculative Scenario 3: A Hawkish Turn in Fed Leadership

Monetary policy is shaped not just by data, but by people. A change in Fed leadership or FOMC composition could lead to a more hawkish bias.

If President Biden (or a potential Republican successor in 2025) appoints a more inflation-wary Fed Chair or if regional bank presidents rotate into voting roles with more hawkish views, the center of gravity at the Fed could shift. This internal politics aspect is often overlooked but can significantly influence rate path projections.

Statements by Fed officials in 2025 have shown a growing divide between doves who favor rate cuts and hawks who want to maintain a restrictive stance. A shift in balance could accelerate discussions of further tightening.

Speculative Scenario 4: Reacceleration of the Economy

A fourth plausible scenario involves a reacceleration in GDP growth, driven by AI-led productivity gains, rising consumer demand, and robust corporate investment.

If unemployment falls below 3.5%, GDP prints exceed 3% annually, and corporate earnings outpace expectations, the Fed may begin to worry about overheating. Even in the absence of headline inflation, the Fed could hike to preemptively cool the economy.

This is akin to the late 1990s, when the Fed raised rates despite low inflation, out of concern for asset bubbles and financial stability.

Speculated Timing: Q4 2025 Likelihood: Moderate Market reaction: Initially bullish (due to growth), then cautious as rates rise.

Counterbalancing Forces: Why the Fed Might Not Hike

While multiple scenarios justify a hike, there are also compelling reasons the Fed may avoid further tightening:

Lag effects of past hikes: Monetary policy operates with lags of 12–24 months. The current restrictive stance may still be filtering through the economy, and a premature hike could tip the U.S. into recession.

Financial stability concerns: Higher rates strain bank balance sheets and raise risks in commercial real estate. The Fed may want to avoid destabilizing the financial system further.

Global divergence: If other central banks, particularly the ECB or Bank of Japan, keep rates low or cut, the dollar could strengthen too much, hurting exports and tightening financial conditions without further hikes.

Political pressure: In an election year (2026 midterms or a fresh presidential term), the Fed may avoid action that appears to favor or undermine political actors. While the Fed is independent, it is not immune to political realities.

Market Indicators and Fed Communication

Markets play a vital role in determining the Fed’s path. Fed funds futures, 2-year Treasury yields, and inflation breakevens all reflect collective expectations of future policy.

As of June 2025, futures markets largely price in no hikes through 2025, with potential cuts starting mid-2026. However, these expectations are highly sensitive to data.

Fed communication—especially the Summary of Economic Projections (SEP) and the Chair’s press conferences—will offer critical clues. If dot plots begin to show an upward drift in median rate forecasts, it could foreshadow renewed tightening.

Regional Disparities and Their Impact on Fed Thinking

Another layer in the analysis involves regional economic conditions. Inflation and labor market strength vary widely across the U.S. In some metro areas, housing inflation remains elevated; in others, joblessness is creeping up.

The Fed’s regional presidents (from banks like the Dallas Fed, Atlanta Fed, etc.) incorporate local economic data into their policy stances. If more hawkish regions see inflation persistence, they could push the national conversation toward renewed hikes.

The Role of Forward Guidance

One hallmark of recent Fed policy is forward guidance—the effort to shape market expectations through careful messaging. Even if the Fed doesn’t hike immediately, it may signal a willingness to do so, thereby achieving some tightening via higher long-term yields.

This “jawboning” technique allows the Fed to manage financial conditions without actually pulling the trigger on rates. If markets become too complacent, the Fed may talk tough to reintroduce discipline.

Fed Balance Sheet Policy: An Alternative Tool

If the Fed wants to tighten without raising rates, it could accelerate quantitative tightening (QT) by reducing its balance sheet more aggressively. Shrinking the Fed’s holdings of Treasuries and mortgage-backed securities tightens liquidity and can raise long-term interest rates indirectly.

This could act as a substitute—or precursor—to rate hikes. Watching the Fed’s QT pace can offer signals about its broader tightening intentions.

Summary of Speculative Timing Scenarios

Scenario

Conditions

Likely Timing

Probability

Inflation Resurgence

PCE > 3%, sticky core

Q1 2026

Moderate

Global Shock

Energy/commodity spike

Q2 2026

Low to Moderate

Hawkish Leadership

Fed Chair/FOMC shift

Q3 2025

Low

Growth Overheating

GDP > 3%, UE < 3.5%

Q4 2025

Moderate

No Hike

Weak data, fragility

No hike in 2025–2026

High

Conclusion: A Delicate Balancing Act

In conclusion, while the Fed has paused its hiking cycle for now, the story is far from over. Economic surprises, global developments, political shifts, and changes in Fed personnel could all reintroduce rate hikes as a viable policy response.

The most plausible path forward involves continued vigilance, with the Fed maintaining its current stance through at least early 2026. However, should inflation persist or growth reaccelerate, one or two additional hikes cannot be ruled out.

Ultimately, the Federal Reserve’s next move will hinge not on a single data point or event, but on the interplay of inflation dynamics, labor market strength, global risks, and political pressures. In an increasingly complex and interdependent world, monetary policy must remain both flexible and disciplined.

As we look ahead, the best guidance for market participants, business leaders, and households alike is to stay data-aware, anticipate uncertainty, and prepare for multiple outcomes. The Fed may have paused—but the era of monetary vigilance is far from over.

The Far-Reaching Economic Consequences of a U.S. Credit Rating Downgrade by Moody’s

When a credit rating agency like Moody’s downgrades the United States’ credit rating, it sends ripples not just through financial markets, but through every corner of the global economy. While the immediate headlines often focus on political dysfunction or fiscal sustainability, the longer-term ramifications of such a downgrade are far more complex, systemic, and potentially destabilizing. A Moody’s downgrade of U.S. sovereign debt signals a fundamental reassessment of America’s creditworthiness and forces investors, policymakers, and institutions to recalibrate their expectations about the world’s most important economy.

This article explores the deeper consequences such a downgrade can trigger—ranging from higher borrowing costs and currency volatility to systemic global shifts in capital allocation and long-term economic growth.

Understanding the Significance of a Credit Downgrade

Moody’s, along with Standard & Poor’s and Fitch Ratings, is one of the “Big Three” credit rating agencies that assess the ability of borrowers—from corporations to countries—to repay their debt. A downgrade of the U.S. credit rating means that Moody’s has lost some confidence in the federal government’s ability or willingness to meet its financial obligations.

Historically, U.S. debt has been viewed as the safest investment on the planet—a benchmark for global finance. A downgrade disrupts that perception and introduces doubt about America’s fiscal and political stability. This isn’t just symbolic. It has concrete consequences that ripple through every layer of the economy.

1. Higher Borrowing Costs Across the Board

Perhaps the most immediate impact of a credit downgrade is a rise in borrowing costs. U.S. Treasury yields serve as the benchmark interest rates for a vast array of financial products—from corporate loans and mortgages to municipal bonds and student loans. When Moody’s downgrades U.S. debt, it effectively tells the world that lending to the U.S. is riskier than before. Investors demand higher yields to compensate for that risk.

This increase in yields is not confined to the federal government. As Treasury rates rise, so do rates on other types of credit. The private sector finds it more expensive to borrow money for investment, expansion, or hiring. Consumers face higher mortgage rates, credit card interest, and auto loan costs.

Over time, these higher costs dampen economic activity, slow housing markets, reduce business investment, and weaken consumer spending—key drivers of GDP growth.

2. Fiscal Constraints and Deficit Challenges

The U.S. government already spends a significant portion of its annual budget servicing its debt. As interest rates rise due to a downgrade, the cost of servicing the national debt increases, further straining the federal budget. This leaves less room for essential spending on infrastructure, education, social programs, or national defense.

Moreover, larger interest payments make it harder to reduce budget deficits, potentially triggering a vicious cycle: higher deficits lead to lower credit ratings, which in turn lead to higher interest payments, and so on.

This dynamic threatens long-term fiscal sustainability and places added pressure on lawmakers to make politically difficult choices—cut spending, raise taxes, or both.

3. Loss of the U.S. Dollar’s Preeminence

One of the most profound long-term risks of a downgrade is its potential impact on the U.S. dollar’s status as the world’s primary reserve currency. This status gives the United States enormous advantages: it can borrow cheaply, influence global trade terms, and maintain geopolitical leverage.

However, a downgrade chips away at global confidence in the stability and reliability of U.S. financial governance. While there is currently no obvious alternative to the dollar, the downgrade may accelerate efforts by countries like China and Russia to promote alternative reserve currencies or diversify their foreign exchange reserves.

A diminished role for the dollar would reduce demand for U.S. assets, further raise borrowing costs, and weaken America’s global economic influence.

4. Investor Confidence and Market Volatility

Financial markets thrive on confidence and predictability—two qualities that a downgrade undermines. Investors, particularly institutional ones such as pension funds, sovereign wealth funds, and insurance companies, may be forced to reassess their U.S. holdings in light of new risk profiles.

Many of these institutions have mandates that require them to hold only top-rated assets. A downgrade from Moody’s could trigger automatic selling of U.S. Treasury securities, contributing to market volatility and raising yields further.

Stock markets also typically react negatively to such downgrades, as they signal macroeconomic instability. Drops in equity valuations can erode household wealth and consumer confidence, especially in a country where a significant portion of retirement savings is tied to the stock market.

5. Damage to U.S. Political Credibility

Credit rating agencies often cite political gridlock and dysfunctional governance as key reasons for a downgrade. For instance, prolonged battles over raising the debt ceiling or passing a federal budget suggest an inability or unwillingness to govern effectively.

Such perceptions damage the U.S.’s reputation not just as a borrower but as a global leader. Allies may question America’s reliability, while adversaries exploit the narrative of decline.

Domestically, a downgrade can become a political flashpoint, further deepening partisan divides and making it even harder to implement the structural reforms needed to restore fiscal balance.

6. Global Economic Repercussions

Because the U.S. economy is so deeply integrated into the global financial system, a downgrade does not stay contained within U.S. borders.

International investors, central banks, and governments hold trillions of dollars in U.S. debt. A downgrade can unsettle these holdings, reduce global confidence in U.S. monetary policy, and spark volatility in emerging markets, which often peg their currencies or base their financial models on the stability of the dollar.

Higher U.S. interest rates can lead to capital flight from developing countries, triggering currency crises, inflation, or debt defaults in those regions. This can contribute to global financial instability and economic slowdowns far from American shores.

7. Potential Policy Responses and Long-Term Adjustments

In response to a downgrade, the U.S. government and Federal Reserve may adopt countermeasures to stabilize the economy. The Fed could delay interest rate hikes or resume quantitative easing to keep borrowing costs manageable. The Treasury could restructure its debt issuance strategy.

However, these tools have limitations and risks. Loose monetary policy could stoke inflation, while fiscal tightening could slow the recovery or deepen a recession.

Long-term, the downgrade should serve as a wake-up call for more serious structural reforms. These include revisiting entitlement spending, tax reform, and implementing automatic stabilizers to reduce the frequency of political standoffs over the budget.

Conclusion: More Than Just a Symbolic Setback

A downgrade of the U.S. credit rating by Moody’s is far more than a symbolic black mark on the nation’s fiscal record. It is a powerful signal to markets, institutions, and policymakers that the foundations of America’s economic dominance are no longer unshakable. The downgrade has the potential to trigger a chain reaction—raising borrowing costs, reducing investment, and sowing doubt about the future of the global financial system anchored by the U.S. dollar.

The real danger lies not just in the immediate market reaction, but in the structural challenges it exposes and exacerbates. If left unaddressed, the consequences of a downgrade could reshape the global economic landscape for years to come.

Subject: Analysis of the potential economic ramifications of a downgrade to the United States’ credit rating by Moody’s.

Executive Summary:

A downgrade of the U.S. credit rating by Moody’s is not merely a symbolic event but a significant signal with far-reaching economic consequences. It signifies a loss of confidence in the U.S. government’s ability or willingness to meet its financial obligations, disrupting the perception of U.S. debt as the safest investment globally. The primary impacts include higher borrowing costs across the board, increased fiscal constraints on the government, potential erosion of the U.S. dollar’s preeminence, diminished investor confidence and market volatility, damage to U.S. political credibility, and significant global economic repercussions. Addressing the structural issues leading to a downgrade is crucial for long-term economic stability.

Key Themes and Most Important Ideas/Facts:

Significance of the Downgrade:

A downgrade by one of the “Big Three” agencies (Moody’s, S&P, Fitch) signifies a reassessment of the U.S.’s creditworthiness.

It directly challenges the historical perception of U.S. debt as the “safest investment on the planet.”

This disruption introduces “doubt about America’s fiscal and political stability” with tangible economic consequences.

Higher Borrowing Costs:

This is identified as “Perhaps the most immediate impact.”

U.S. Treasury yields serve as a benchmark for various financial products (corporate loans, mortgages, municipal bonds, student loans).

A downgrade makes lending to the U.S. riskier, prompting investors to “demand higher yields to compensate for that risk.”

This increase in borrowing costs extends beyond the federal government to the private sector and consumers, “dampen[ing] economic activity, slow[ing] housing markets, reduc[ing] business investment, and weaken[ing] consumer spending.”

Fiscal Constraints and Deficit Challenges:

Rising interest rates on U.S. debt due to a downgrade increase the cost of debt servicing, further straining the federal budget.

This limits available funds for essential spending on infrastructure, education, social programs, and defense.

It creates a “vicious cycle: higher deficits lead to lower credit ratings, which in turn lead to higher interest payments, and so on.”

This dynamic exacerbates the difficulty of reducing budget deficits and forces “politically difficult choices—cut spending, raise taxes, or both.”

Loss of U.S. Dollar’s Preeminence:

This is highlighted as “One of the most profound long-term risks.”

The dollar’s status as the primary reserve currency offers significant advantages (cheap borrowing, influence on trade, geopolitical leverage).

A downgrade “chips away at global confidence in the stability and reliability of U.S. financial governance.”

While no immediate alternative exists, it may “accelerate efforts by countries like China and Russia to promote alternative reserve currencies or diversify their foreign exchange reserves.”

A diminished dollar role would “reduce demand for U.S. assets, further raise borrowing costs, and weaken America’s global economic influence.”

Investor Confidence and Market Volatility:

Downgrades undermine the “confidence and predictability” on which financial markets rely.

Institutional investors (pension funds, sovereign wealth funds, insurance companies) may be forced to “reassess their U.S. holdings in light of new risk profiles.”

Mandates requiring holding only top-rated assets could trigger “automatic selling of U.S. Treasury securities,” contributing to volatility and higher yields.

Stock markets typically react negatively, as downgrades “signal macroeconomic instability,” eroding household wealth and consumer confidence.

Damage to U.S. Political Credibility:

Credit rating agencies often cite “political gridlock and dysfunctional governance” as reasons for a downgrade.

Issues like debt ceiling battles and budget standoffs suggest an inability to govern effectively.

This damages the U.S.’s reputation as a borrower and “as a global leader.”

Domestically, it can become a “political flashpoint, further deepening partisan divides,” making reforms harder.

Global Economic Repercussions:

Due to the U.S. economy’s global integration, a downgrade’s effects extend beyond U.S. borders.

It can “unsettle” the trillions of dollars in U.S. debt held by international investors, central banks, and governments.

Higher U.S. interest rates can trigger “capital flight from developing countries,” potentially leading to “currency crises, inflation, or debt defaults in those regions.”

This can contribute to “global financial instability and economic slowdowns.”

Potential Policy Responses and Long-Term Adjustments:

The U.S. government and Federal Reserve may employ countermeasures like delaying interest rate hikes or resuming quantitative easing.

The Treasury could also adjust debt issuance strategy.

These tools have limitations and risks (inflation from loose monetary policy, recession from fiscal tightening).

The downgrade should serve as a “wake-up call for more serious structural reforms,” including entitlement spending, tax reform, and automatic fiscal stabilizers.

Conclusion:

A U.S. credit rating downgrade by Moody’s is a serious event with cascading economic consequences. It highlights underlying structural challenges and has the potential to fundamentally alter global financial dynamics. The “real danger lies not just in the immediate market reaction, but in the structural challenges it exposes and exacerbates.” Addressing these challenges through serious reform is critical to mitigating the long-term impact of a downgrade and maintaining U.S. economic stability and global influence

Quiz

What are the “Big Three” credit rating agencies mentioned in the article?

How does a U.S. credit rating downgrade affect borrowing costs for both the government and private sector?

What is a key challenge for the U.S. federal budget resulting from higher interest rates due to a downgrade?

Why is the U.S. dollar’s status as the primary reserve currency significant, and how could a downgrade impact this?

How might a downgrade affect investor confidence and lead to market volatility?

What does the article suggest is a key reason cited by credit rating agencies for downgrades, related to governance?

How can a U.S. downgrade have repercussions for the global economy, particularly in emerging markets?

What are some potential policy responses the U.S. government and Federal Reserve might consider after a downgrade?

Beyond immediate market reactions, what does the article highlight as the “real danger” of a downgrade?

According to the article, why is a U.S. credit rating downgrade by Moody’s more than just a symbolic setback?

Essay Questions

Analyze the interconnectedness of the consequences of a U.S. credit rating downgrade as described in the article. How do higher borrowing costs, fiscal constraints, and potential loss of dollar preeminence feed into and exacerbate each other?

Discuss the long-term implications of a U.S. credit rating downgrade on the global economic landscape. Consider the potential shifts in capital allocation, the role of the dollar, and the impact on emerging markets.

Evaluate the political consequences of a U.S. credit rating downgrade. How does political dysfunction contribute to the likelihood of a downgrade, and how might a downgrade further deepen partisan divides and hinder necessary reforms?

Compare and contrast the immediate versus the long-term effects of a U.S. credit rating downgrade as presented in the article. Which set of consequences do you believe is more significant and why?

Based on the article, propose and justify potential structural reforms or policy adjustments that the U.S. could implement to address the underlying issues that might lead to or be exacerbated by a credit rating downgrade.

Glossary of Key Terms

Credit Rating Agency: A company that assesses the creditworthiness of individuals, businesses, or governments. The “Big Three” are Moody’s, Standard & Poor’s, and Fitch Ratings.

Credit Rating Downgrade: A reduction in the credit rating of a borrower, indicating that the agency has less confidence in their ability to repay debt.

Sovereign Debt: Debt issued by a national government.

U.S. Treasury Yields: The return an investor receives on U.S. government debt instruments like Treasury bonds or notes. They serve as a benchmark for many other interest rates.

Borrowing Costs: The interest rates and fees associated with taking out a loan or issuing debt.

Fiscal Sustainability: The ability of a government to maintain its spending and tax policies without threatening its solvency or the stability of the economy.

National Debt: The total amount of money that a country’s government owes to its creditors.

Budget Deficits: The amount by which a government’s spending exceeds its revenue in a given period.

Reserve Currency: A currency held in significant quantities by central banks and other financial institutions as part of their foreign exchange reserves. The U.S. dollar is currently the primary reserve currency.

Capital Allocation: The process by which financial resources are distributed among various investments or assets.

Investor Confidence: The level of optimism or pessimism investors have about the prospects of an economy or a particular investment.

Market Volatility: The degree of variation of a trading price over time. High volatility indicates that the price of an asset can change dramatically over a short time period in either direction.

Political Gridlock: A situation where there is difficulty in passing laws or making decisions due to disagreements between political parties or branches of government.

Debt Ceiling: A legislative limit on the amount of national debt that the U.S. Treasury can issue.

Quantitative Easing: A monetary policy where a central bank purchases government securities or other securities from the market in order to lower interest rates and increase the money supply.

Automatic Stabilizers: Government programs or policies, such as unemployment benefits or progressive taxation, that automatically adjust to cushion economic fluctuations without requiring explicit policy action.

Quiz Answer Key

The “Big Three” credit rating agencies mentioned are Moody’s, Standard & Poor’s, and Fitch Ratings.

A downgrade signals increased risk, causing investors to demand higher yields on U.S. debt, which in turn raises borrowing costs for both the government and the private sector, including businesses and consumers.

Higher interest rates resulting from a downgrade significantly increase the cost of servicing the national debt, straining the federal budget and leaving less money for other essential spending.

The dollar’s status allows the U.S. to borrow cheaply and wield global influence. A downgrade erodes confidence in its stability, potentially accelerating efforts by other countries to find alternatives and weakening the dollar’s role.

A downgrade undermines confidence and predictability, leading institutional investors to potentially sell U.S. Treasury holdings and causing broader volatility in both bond and stock markets.

The article suggests that political gridlock and dysfunctional governance, such as battles over the debt ceiling, are often cited by credit rating agencies as key reasons for a downgrade.

A U.S. downgrade can unsettle international investors and central banks holding U.S. debt, reduce global confidence in U.S. policy, and spark volatility in emerging markets, potentially leading to capital flight, currency crises, or defaults in those regions.

Potential policy responses include the Federal Reserve delaying interest rate hikes or resuming quantitative easing, and the Treasury restructuring its debt issuance strategy.

The “real danger” is not just the immediate market reaction but the structural challenges that the downgrade exposes and exacerbates, potentially reshaping the global economic landscape long-term.

It is more than symbolic because it is a powerful signal to markets and institutions that fundamentally reassesses America’s creditworthiness and forces a recalibration of expectations about the world’s most important economy, triggering concrete economic consequences.

In a widely anticipated decision, the Federal Reserve opted to keep interest rates unchanged at the conclusion of today’s Federal Open Market Committee (FOMC) meeting. The federal funds rate remains in the range of 5.25% to 5.50%, a 23-year high that has now persisted since July 2023. While investors and analysts had largely priced in a pause, the rationale behind the Fed’s decision reflects a complex balance of economic signals, inflation concerns, and a shifting labor market.

At the heart of the Fed’s policy stance remains its dual mandate: maximum employment and stable prices. While inflation has declined significantly from its peak in 2022, recent data show signs of stickiness in core prices—particularly in housing and services. The Consumer Price Index (CPI) for March showed headline inflation at 3.5% year-over-year, still well above the Fed’s 2% target. Core inflation, which excludes volatile food and energy prices, remains elevated.

Fed Chair Jerome Powell emphasized in his post-meeting press conference that “while inflation has moved down from its highs, it remains too high, and we are prepared to maintain our restrictive stance until we are confident inflation is sustainably headed toward 2%.”

Labor Market Shows Signs of Softening

A key factor behind the decision to hold rates steady is the evolving labor market. The April jobs report showed signs of cooling, with job creation falling below expectations and the unemployment rate ticking slightly higher. Wage growth has also moderated, suggesting that the tightness that once fueled inflationary pressures may be easing.

The Fed appears to be watching closely to avoid tipping the economy into recession. Maintaining current rates gives policymakers the flexibility to respond to further labor market deterioration while continuing to restrain inflationary pressures.

No Immediate Rate Cuts on the Horizon

Despite growing calls from some quarters for rate cuts to support growth, Powell made it clear that the central bank is not yet ready to pivot. “We do not expect it will be appropriate to reduce the target range until we have greater confidence that inflation is moving sustainably toward 2%,” he noted.

Markets have been forced to recalibrate their expectations. At the start of the year, many anticipated as many as six rate cuts in 2024. That outlook has now dramatically shifted, with investors largely pricing in one or two cuts at most—and not before late 2025, barring a sharp economic downturn.

Global Considerations and Financial Stability

The Fed’s cautious approach is also influenced by global developments. Sticky inflation in Europe, geopolitical tensions, and persistent supply chain disruptions all contribute to uncertainty. Moreover, the central bank remains attuned to the risks of financial instability. Keeping rates high—but not raising them further—helps reduce the chances of asset bubbles or excessive credit growth while avoiding additional strain on borrowers.

What Businesses and Investors Should Expect

The Fed’s message today is clear: patience is the prevailing policy. For businesses, this means continued pressure on borrowing costs, but also stability in monetary conditions. For investors, the outlook is one of reduced volatility in Fed policy, though rates may stay “higher for longer” than many had hoped.

In the months ahead, the data will continue to guide the Fed’s hand. Inflation progress will be crucial, but so too will the health of the consumer and the resilience of the job market. Until then, the pause continues—but the path forward remains data-dependent.\

In its March 19, 2025, meeting, the Federal Reserve announced that it would maintain the federal funds rate within the target range of 4.25% to 4.5%, marking the second consecutive meeting without a rate adjustment. This decision reflects the central bank’s cautious approach amid persistent economic uncertainties and evolving inflation dynamics.

Economic Context and Inflation Outlook

Recent data indicates that inflation has moderated, with the consumer price index rising at a more controlled pace, approaching the Fed’s 2% target. However, the central bank has revised its inflation forecast upward for the year, signaling ongoing concerns about price stability. Despite signs of improvement, inflationary pressures remain a focal point in policy deliberations.

Impact of Trade Policies and Tariffs

The economic landscape is further complicated by trade tensions and tariff policies, which have introduced volatility, affecting both growth prospects and inflation expectations. The Fed acknowledges that such policies contribute to heightened uncertainty, influencing its decision to hold rates steady while assessing their long-term impact on the economy. Fed Leaves Rates Unchanged

Labor Market and Employment Trends

Despite these challenges, the labor market remains resilient. Hiring continues at a steady pace, with the unemployment rate holding stable. Wage growth has been sustainable, outpacing inflation and contributing to consumer spending. The Fed’s decision to maintain current rates aims to support this employment stability while monitoring potential inflationary pressures.

Future Monetary Policy Projections

Looking ahead, Federal Reserve policymakers anticipate implementing two quarter-point rate cuts by the end of the year, contingent upon economic developments. This projection underscores the Fed’s commitment to flexibility in its monetary policy, allowing for adjustments in response to evolving economic indicators.

Conclusion

The Federal Reserve’s decision to leave interest rates unchanged reflects a measured approach to navigating current economic uncertainties. By closely monitoring inflation trends, trade policy impacts, and labor market conditions, the central bank aims to fulfill its dual mandate of promoting maximum employment and ensuring price stability. As the year progresses, the Fed’s policy decisions will continue to be data-dependent, adapting to the shifting economic landscape.

Retail sales in the United States saw a modest increase in February, signaling continued consumer resilience despite ongoing economic pressures. According to the latest data released by the U.S. Census Bureau, retail sales edged up by 0.3% from the previous month, following a slight decline in January.

Key Drivers of Growth The rise in retail sales was fueled primarily by increased consumer spending on essentials such as groceries, health products, and gasoline. Additionally, online retailers reported a steady uptick in sales, reflecting the sustained shift toward e-commerce. However, discretionary spending on items such as electronics, furniture, and apparel remained relatively flat, indicating cautious consumer behavior amid inflation concerns.

Sector-Specific Performance

Grocery Stores and Supermarkets: Sales at food and beverage retailers continued to climb as consumers prioritized household necessities.

Gasoline Stations: Rising fuel prices contributed to higher sales at gas stations, despite concerns over energy costs.

E-commerce: Online shopping remained strong, with digital platforms benefiting from ongoing convenience-driven purchases.

Department Stores and Apparel Retailers: Traditional brick-and-mortar retailers faced stagnation, with some segments experiencing slight declines in foot traffic.

Consumer Sentiment and Economic Outlook Despite the slight increase in retail sales, consumer sentiment remains mixed. Persistent inflation, higher interest rates, and economic uncertainty continue to influence spending habits. Analysts suggest that while the labor market remains strong, potential slowdowns in wage growth and employment trends could impact future retail performance.

Looking ahead, retailers are cautiously optimistic as they prepare for seasonal spending shifts, including spring promotions and mid-year sales events. However, they remain mindful of external economic factors that could influence consumer confidence in the coming months.

Overall, the modest rise in February’s retail sales reflects a steady but cautious consumer market, with spending trends closely tied to broader economic conditions.

Contains information related to marketing campaigns of the user. These are shared with Google AdWords / Google Ads when the Google Ads and Google Analytics accounts are linked together.

90 days

__utma

ID used to identify users and sessions

2 years after last activity

__utmt

Used to monitor number of Google Analytics server requests

10 minutes

__utmb

Used to distinguish new sessions and visits. This cookie is set when the GA.js javascript library is loaded and there is no existing __utmb cookie. The cookie is updated every time data is sent to the Google Analytics server.

30 minutes after last activity

__utmc

Used only with old Urchin versions of Google Analytics and not with GA.js. Was used to distinguish between new sessions and visits at the end of a session.

End of session (browser)

__utmz

Contains information about the traffic source or campaign that directed user to the website. The cookie is set when the GA.js javascript is loaded and updated when data is sent to the Google Anaytics server

6 months after last activity

__utmv

Contains custom information set by the web developer via the _setCustomVar method in Google Analytics. This cookie is updated every time new data is sent to the Google Analytics server.

2 years after last activity

__utmx

Used to determine whether a user is included in an A / B or Multivariate test.

18 months

_ga

ID used to identify users

2 years

_gali

Used by Google Analytics to determine which links on a page are being clicked

30 seconds

_ga_

ID used to identify users

2 years

_gid

ID used to identify users for 24 hours after last activity

24 hours

_gat

Used to monitor number of Google Analytics server requests when using Google Tag Manager