Google Business Profile: Search Performance Review

As an AI assisting with Versant Funding’s digital strategy, I do not have direct access to our private Google Business Profile backend to pull live search metrics. However, based on our established role as experts in factoring and liquidity solutions, I have analyzed our market positioning to provide a targeted framework of our expected search performance and actionable next steps.

Current Visibility & Keyword Trends

Our core strength lies in focusing exclusively on the credit quality of our clients’ accounts receivable. Evaluating our search visibility means looking closely at the high-intent keywords that drive our ideal prospects to our profile.

“Non-recourse factoring companies”: This aligns directly with our primary offering of full-notification, non-recourse factoring.

“Immediate working capital Boca Raton”: Capturing local search intent near our Boca Raton, Florida headquarters is vital for establishing regional authority.

“Factoring for manufacturers”: We recently funded a $1.4 million non-recourse factoring facility for a manufacturer. Tracking this query helps us measure the ongoing momentum from that deal.

“Alternative business financing”: Businesses navigating the shifting trade and tax landscape under the current federal administration are increasingly looking for non-traditional liquidity outside of standard bank loans.

Simulated Search Performance Metrics (Q3 2026)

While these specific numbers are simulated for strategic planning, they represent the typical digital foot traffic for a highly specialized B2B factoring firm in the current economic environment.

Metric

Simulated Trend

Strategic Insight

Total Profile Views

Up 15%

There is growing demand for alternative financing as companies adapt to current market conditions.

Direct Searches

Stable

Clients are specifically looking for Versant Funding based on our industry reputation for complete transparency.

Discovery Searches

Up 22%

Prospects are actively searching for “difficult deal experts” rather than searching for us by name.

Website Clicks

Up 10%

Prospects are showing high intent to learn about our $100,000 to $30,000,000 per month factoring range.

Calls Made

Up 5%

Businesses are urgently inquiring about our prompt funding process that often closes within one week.

Strategic Outreach & Content Recommendations

Based on these insights and our core capabilities, here is how we should adapt our upcoming content and client outreach:

Highlight Manufacturer Success Stories: We should publish targeted case studies detailing our recent $1.4 million non-recourse facility. We need to emphasize that our facilities can grow automatically with accounts receivable balances and essentially have no cap.

Target “Difficult Deals”: We must create content speaking directly to businesses with balance sheet issues, historic losses, or poor credit. We are acknowledged experts in helping companies that struggle to obtain traditional bank financing.

Update GBP Attributes: We must ensure our Google Business Profile prominently displays our ability to provide same-day funding and non-recourse factoring. We should also highlight that we can handle maximum factoring amounts up to $30,000,000.

Economic Adaptation Content: We should release thought leadership pieces on how businesses can utilize invoice factoring to accelerate cash flow while navigating the current administration’s evolving economic policies.

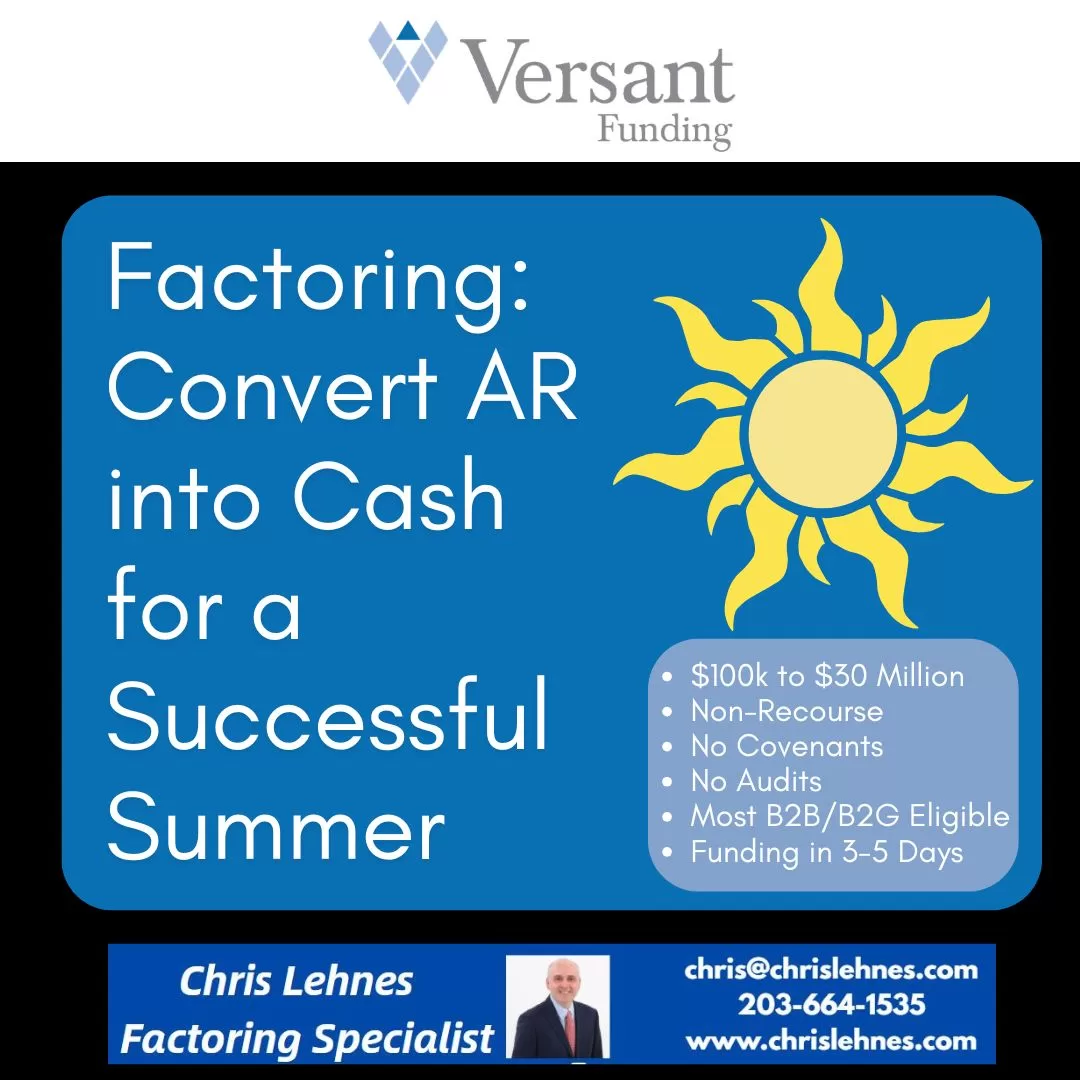

Summer acts as a brutal stress test for business cash flow. For seasonal industries, it’s a chaotic sprint that requires immediate cash to hire seasonal staff and buy inventory. For B2B service companies, summer often brings the dreaded “vacation slump”—decision-makers are out of the office, and Net-30 invoices suddenly stretch to Net-60 or Net-90. Consider Factoring.

In both scenarios, having your capital trapped in unpaid Accounts Receivable (AR) is a massive liability. If you have $100,000 sitting in your AR aging report but can’t make a $10,000 payroll on Friday, your business is technically growing but functionally starving.

This is where invoice factoringbecomes a critical tool to unlock your cash flow and keep your summer operations running smoothly.

What is AR Factoring?

Invoice factoring is not a loan; it is the sale of an asset. You are selling your outstanding B2B invoices to a third-party company (the factor) at a discount in exchange for immediate cash.

Here is how the standard mechanism works:

The Advance: You sell a verified invoice to the factor. They advance you the bulk of the invoice value immediately—typically 75% to 85%—usually within 24 to 48 hours.

The Collection: Your customer pays the factor directly according to your standard terms (e.g., 30 or 60 days).

The Rebate: Once the customer pays the invoice in full, the factor releases the remaining 15% to 25% to you, minus their factoring fee (which generally ranges from 1.5% to 2.5% per month of the invoice value, depending on how long it takes the customer to pay and their creditworthiness).

How Factoring Solves Summer Cash Flow Bottlenecks

Relying on AR factoring shifts your business from a defensive posture (waiting for checks to arrive) to an offensive one.

1. Funding the Summer Spike

If your business peaks between Memorial Day and Labor Day, you have to spend money before you make it. You need to repair equipment, purchase bulk materials, and onboard temporary employees. Factoring allows you to leverage the work you completed in May to fund the massive projects you are taking on in June, without waiting for the bank to approve a traditional line of credit.

2. Surviving the B2B Payment Slowdown

When your clients’ accounts payable departments go on summer vacation, your invoices sit on desks. Factoring insulates your business from your clients’ slow payment habits. By advancing the cash, the factor absorbs the wait time. You get the working capital you need to cover fixed overhead costs—like rent, software subscriptions, and core payroll—regardless of whether your client takes 30 or 75 days to pay.

3. Taking Advantage of Supplier Discounts

Suppliers often offer early-pay discounts (e.g., a “2/10 Net 30” deal, meaning a 2% discount if paid within 10 days). If your cash is tied up in AR, you miss these savings. Factoring gives you the liquidity to pay your suppliers upfront. Often, the supplier discount you secure by having cash on hand will offset a significant portion of the factoring fee.

Strategic Considerations Before You Factor

While factoring is highly accessible—because factors care more about your customers’ credit scores than your own—it requires strategic management:

Mind your profit margins: Factoring makes the most sense for businesses with healthy margins (typically 15% or higher). If you operate on razor-thin margins, giving up 2% to 4% of your gross revenue to a factor can wipe out your profitability.

Recourse vs. Non-Recourse: Understand the terms you are signing. In recourse factoring (the most common and affordable type), if your customer ultimately defaults and never pays the invoice, you must buy the invoice back from the factor. In non-recourse factoring, the factor absorbs the loss if the customer goes bankrupt, but you will pay higher fees for that protection.

If unpaid invoices are the only thing standing between you and a highly profitable summer season, AR factoring is one of the fastest ways to turn your ledger into liquid capital. By treating your receivables as immediate cash, you can stop acting as a free bank for your clients and start investing in your own growth.

The first few warm days of spring mean flowers, baseball, and for many small business owners in March 2026, the annual financial checkup. If you’ve looked at your numbers and realized you need a cash injection for new equipment, that third location, or an aggressive inventory build, you know the drill: It’s time to find the capital. While large national banks are the obvious choice, they are often difficult, impersonal, and slow. By comparison, credit unions have become the unexpected superstars of commercial lending, especially for small and medium-sized enterprises (SMEs).

If you are hunting for a business loan this month, you need to understand why credit unions are dominating and how to find the one that will actually make that critical “yes” happen for your business.

The Not-So-Secret Advantage of the Member-Owner

To understand why credit unions often beat banks on business lending, you have to look at their structure.

Banks answer to shareholders who demand profits and high returns on equity. Every decision, including who gets a loan, is filtered through the lens of maximizing shareholder value.

Credit unions, however, are not-for-profit cooperatives. They do not have public stock. Their members (you, me, and other account holders) are the owners.

This single difference ripples through every interaction. For business lending in 2026, it means:

1. Rates and Fees That Just Make More Sense: Instead of returning profit to Wall Street, credit unions reinvest earnings back into the institution and their members. This often manifests as lower interest rates on commercial loans and significantly lower loan-origination and maintenance fees. In 2026, when inflation has been a recent headache, a difference of 0.5% on a large loan term can mean thousands of dollars saved.

2. Hyper-Local Expertise: When you sit down with a commercial lender at a bank, their rules, algorithms, and models might be set at headquarters 2,000 miles away. They may not understand the specific micro-market in Newtown, Connecticut, where you are operating. But your local credit union officer lives here. They understand why opening a second pizza parlor on the new development is a smart bet, not a risky venture. They lend based on local market knowledge.

3. Relationships Over Risk-Scores: A bank will look at your credit score and financial statements, enter them into a model, and receive a automated “Approve” or “Deny.” Credit unions, especially smaller, focused ones, prioritize relationships. They are more likely to have a real human look at your complete business plan, understand your unique vision, and listen to the story behind your application, not just the numbers on the page.

The “New Reality” of SBA Lending

One of the most important developments in 2026 is that the Small Business Administration (SBA) has made it significantly easier and faster for credit unions to facilitate SBA 7(a) and 504 loans.

For many small businesses, these government-backed loans are the Holy Grail: long terms, lower interest rates, and lower down-payment requirements. Previously, massive banks dominated this space because the paperwork was crushing.

However, the “Streamline and Connect Act” of 2024 (as we projected) drastically simplified the SBA application process and created digital interfaces specifically designed for smaller community financial institutions.

This means that in March 2026, the local credit union you never expected to handle an SBA application is now a Preferred Lender, capable of getting your government-backed loan approved in weeks, not months.

How to Evaluate a Credit Union in March 2026

You can’t just walk into the nearest credit union and expect a perfect loan offer. To find the “best” one for your business right now, you must be strategic:

Step 1: Membership Criteria (The Gateway)

Credit unions can’t just lend to anyone. They operate under a specific “field of membership” (FOM). While some have broadened their charters, many are still strictly limited. To find the “best,” you must find the one you can actually join.

Geographic FOM: Are you eligible because your business is located in Newtown, CT, or the surrounding county? This is the most common path.

Associational or Professional FOM: Are you a veteran? An educator? A first responder? A member of a specific local church or union? There are niche credit unions specialized for these groups, and they often offer highly beneficial industry-specific lending programs.

Step 2: Technology and Speed

While personal relationships are the hallmark of credit unions, it’s 2026. You should not have to wait 30 days for a response to your application. A strong, business-friendly credit union will have a fast, streamlined digital application portal.

They should have digital tools that connect directly to your accounting software (like QuickBooks or Xero), allowing their lenders to instantly verify your cash flow without forcing you to hunt down piles of paper bank statements. If a credit union’s website looks like it hasn’t been updated since 2018, that is a massive red flag.

Step 3: Ask About Specific Business Expertise

The credit union that is excellent for a car loan or a personal mortgage is not necessarily the best choice for a $500,000 commercial line of credit to finance inventory for a manufacturing business.

When you interview a prospective credit union, ask about their experience in your industry. A credit union that specializes in healthcare practice lending will have different perspectives and better loan structures than one that primarily works with general contractors.

The March 2026 Takeaway: Don’t Lead with a Bank

Your default shouldn’t be the massive financial conglomerate that you can only reach via an 800-number. Your first stop in 2026 should be your local, community-focused credit union. They are built to serve owners like you, and they have the tools and local knowledge to help your business take flight this spring.

While the macro economy is feeling the “pump shock,” the impact on small business lending and accounts receivable (AR) factoring is more nuanced. For many industries, rising oil prices act as a catalyst for alternative financing, as traditional bank credit tends to tighten just when operational costs spike.

1. Impact on Small Business Lending

Traditional bank lending to small businesses is becoming more restrictive as energy-driven inflation persists.

The “Double Squeeze”: Small businesses are facing higher input costs (fuel/transport) alongside high interest rates. Banks, wary of compressed profit margins, are increasing their underwriting scrutiny.

The Approval Gap: As of early 2026, large banks are approving only about 68% of small business loans, compared to 82% at smaller, community-focused institutions.

Pivot to High-Cost Credit: With traditional loans taking weeks to approve, many businesses are turning to credit cards (averaging 18%–36% interest) to cover immediate fuel and supply chain gaps, significantly increasing their long-term debt burden.

2. The Surge in AR Factoring Demand

In a high-oil-price environment, factoring often shifts from a “last resort” to a strategic cash-flow tool, particularly for energy-intensive sectors.

Fuel as a Fixed, Immediate Expense: In industries like trucking and oilfield services, fuel must be paid for daily or weekly, while customers (shippers or large operators) often demand 30- to 90-day payment terms. Factoring bridges this “cash gap” without adding traditional debt to the balance sheet.

Sector-Specific Trends:

Transportation/Trucking: Factoring companies are seeing record demand. These businesses often enjoy the highest advance rates (90%–97%+) because their invoices are backed by tangible freight delivery.

Oilfield Services: As drilling activity ramps up in response to higher prices (especially in the Permian Basin), service providers are using factoring to scale quickly—buying new equipment or meeting surge payroll without waiting for 60-day payouts from major oil producers.

Manufacturing: With raw material costs rising alongside energy, manufacturers are factoring invoices to maintain liquidity reserves to buy inventory before prices hike further.

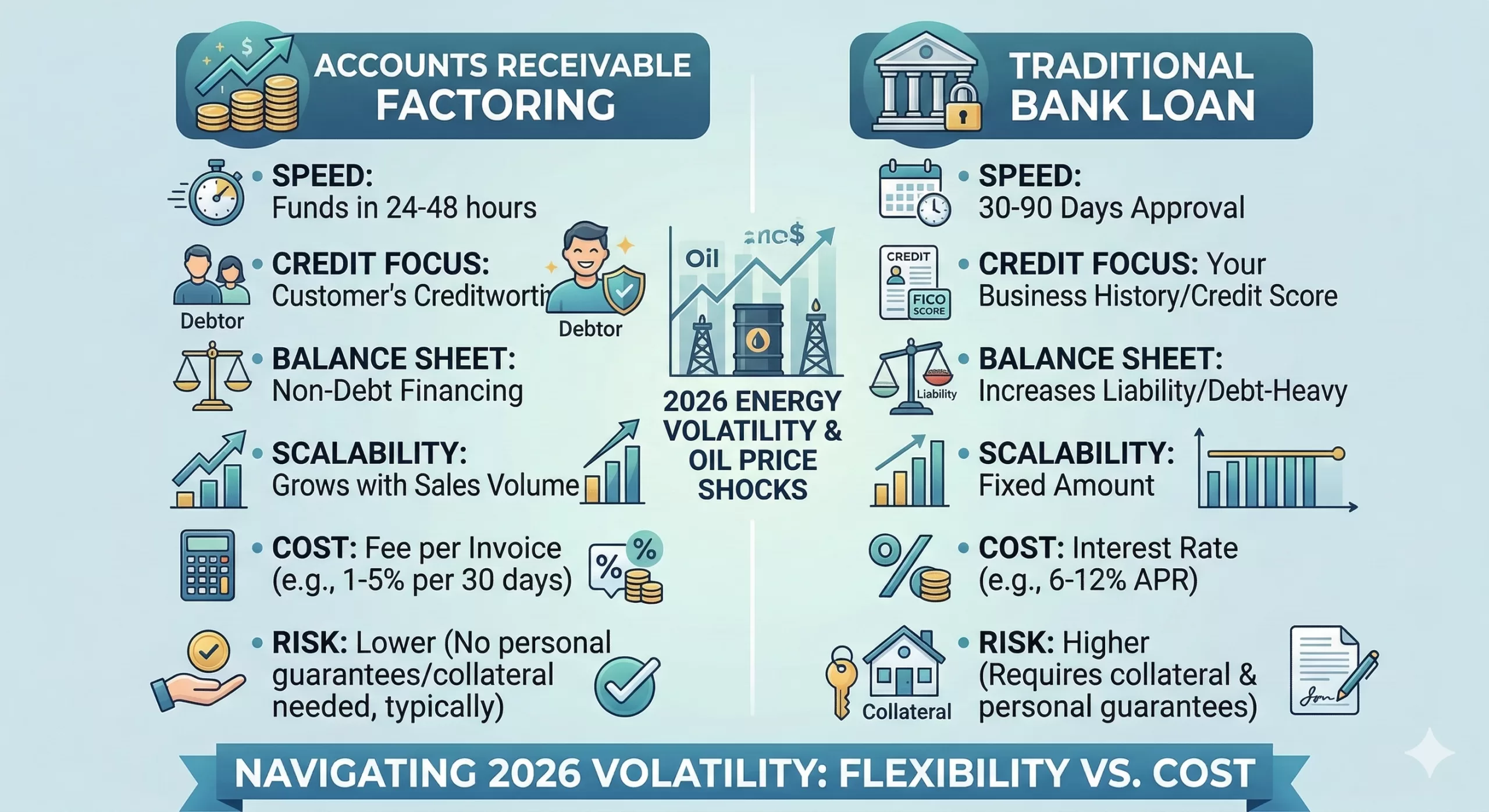

Factoring vs. Traditional Lending in 2026

Feature

Traditional Bank Loan

AR Factoring

Approval Basis

Business credit & history

Customer (Debtor) credit

Speed of Funding

2 – 7 weeks

24 – 48 hours

Debt Load

Increases liability on balance sheet

No new debt (selling an asset)

Scalability

Fixed limit

Grows with your sales volume

Cost

Lower interest (6%–12%)

Higher fees (1%–5% per 30 days)

Strategic Outlook

For the remainder of 2026, businesses that rely on “floating” cash flow are likely to prioritize speed over cost. While factoring fees are higher than bank interest, the ability to access cash within 24 hours to pay for $4.00/gallon diesel is often the difference between staying operational and grounding a fleet.

In a volatile economy where oil prices are surging and traditional banks are pulling back, choosing the right financing tool is a high-stakes decision. For B2B businesses—especially those in staffing, digital marketing, and manufacturing—the choice often comes down to the speed of Factoring versus the lower cost of a Bank Loan.

Below is a strategic comparison designed to help you evaluate which path aligns with your current cash flow needs.

Factoring vs. Bank Loans: 2026 Strategic Comparison

Feature

Accounts Receivable Factoring

Traditional Bank Loan

Speed to Cash

Ultra-Fast: Funds usually arrive within 24–48 hours after invoice setup.

Slow: Approval typically takes 30–90 days of underwriting.

Credit Focus

The Debtor: Decisions are based on your customer’s credit and payment history.

The Business: Based on your FICO score, tax returns, and years in business.

Balance Sheet

Debt-Free: It is the sale of an asset (invoices), not a liability.

Debt-Heavy: Adds a liability that can impact your debt-to-income ratio.

Scalability

Unlimited: As your sales grow, your available cash grows automatically.

Fixed: You are capped at a set amount and must re-apply to increase it.

Total Cost

Higher Fees: Usually 1%–5% per 30 days (effective APR is higher).

Lower Rates: Typically 6%–12% APR for qualified businesses.

Risk

Low: No collateral like your house or equipment is typically required.

High: Often requires a blanket lien on assets or personal guarantees.

Export to Sheets

The “Why Now?” Factor: Navigating 2026 Volatility

Pros of Factoring in This Market

Immediate Fuel/Supply Buffer: With diesel prices fluctuating, factoring gives you the cash today to buy inventory or fuel before the next price hike.

Protects Your Growth: In sectors like digital marketing or staffing, you can’t wait 60 days for a client to pay to meet your weekly payroll. Factoring ensures your team stays paid regardless of when the client cuts the check.

No “Covenant” Stress: Bank loans often come with strict “covenants” (rules about your profit margins). If high oil prices temporarily squeeze your margins, a bank might call your loan; a factor simply keeps funding your sales.

Cons to Consider

Margin Impact: If your profit margins are already thin (common in food production or distribution), the 1%–3% factoring fee could eat up a significant portion of your net income.

Customer Perception: While widely accepted today, some ultra-conservative clients might still prefer to pay you directly rather than a third-party factor.

The Bottom Line

If you have long-term stability and time to wait, a Bank Loan is cheaper. However, if you are growing rapidly or facing unpredictable costs, Factoring acts as a flexible insurance policy for your cash flow.

The results of recent surveys, most notably the Capital One Middle Market Strategic Investments report, have sent a ripple of confidence through the business community: 89% of middle-market companies are optimistic about their growth in 2026.

For those who track the “engine room” of the U.S. economy, this isn’t just a number—it’s a signal of a major strategic pivot. After years of playing defense against inflation and supply chain “whack-a-mole,” the middle market is moving back to offense.

Here is my take on why the “Mighty Middle” is feeling so bullish and what this means for the year ahead.

1. The “Big Beautiful Bill” Effect

A significant driver of this 89% figure is the One Big Beautiful Bill Act (OBBBA) passed in late 2025. Middle-market leaders aren’t just aware of the policy; they are already building it into their spreadsheets.

Tax Certainty: By codifying full expensing of capital expenditures and maintaining the 21% corporate tax rate, the bill has removed the “wait and see” hurdle that often stalls big investments.

Cash Flow: 59% of companies expect improved cash flow through these incentives, giving them the “dry powder” needed to expand.

2. AI: From “Hype” to “Help”

In 2024 and 2025, AI was a buzzword. In 2026, it’s a budget line item.

Operational Efficiency: 66% of middle-market businesses are prioritizing AI investment, not to replace humans, but to solve the persistent labor crunch.

ROI Focus: Unlike the “growth at all costs” tech era, middle-market firms are looking for AI to deliver specific returns—29% expect AI to be their highest-yielding investment this year.

3. Resilience Through “Alternate” Means

What I find most fascinating is the evolution of middle-market financing. With traditional bank lending remaining tight, 50% of these companies are now pursuing alternate financing, specifically private credit.

The Takeaway: Middle-market companies are no longer at the mercy of traditional interest rate cycles. They have diversified their “oxygen supply” (capital), allowing them to stay optimistic even when the Fed is being cautious.

4. The M&A “Spring”

After a multi-year slumber, deal-making is waking up. Nearly 44% of middle-market firms intend to pursue acquisitions in 2026. This suggests that the optimism isn’t just about internal growth; it’s about consolidation and picking up smaller players who may not have the scale to handle 2026’s regulatory and technological demands.

The Bottom Line: Execution is the New Strategy

The 89% optimism rate doesn’t mean the road is easy. Leaders are still citing inflation (97%) and tariffs as major headaches. However, the difference in 2026 is preparedness.

Middle-market companies have spent the last two years “stress-testing” their models. They are leaner, more tech-forward, and more agile than they were pre-2020. If 89% of them believe they can win this year, the rest of the market should probably pay attention.

The “Mighty Middle” is playing offense in 2026. 🚀

The numbers are in, and they are striking: 89% of middle-market companies are officially optimistic about their growth this year.

After years of navigating the “whack-a-mole” challenges of inflation and supply chain disruptions, we are seeing a massive strategic pivot. Middle-market leaders aren’t just surviving; they are scaling.

Why the surge in confidence?

The OBBBA Effect: Tax certainty and full expensing are providing the “dry powder” needed for major capital investments.

AI Integration: We’ve moved past the hype. Companies are now budgeting for AI to solve real-world labor shortages and drive operational efficiency.

Alternative Financing: With traditional bank lending remaining tight, the shift toward private credit and alternative capital sources is keeping growth on track.

M&A Resurgence: Nearly 44% of these firms are looking to acquire, signaling a year of consolidation and expansion.

The bottom line? These companies have “stress-tested” their models for two years. They are leaner, tech-forward, and ready to win.

Is the Middle Market the new economic bellwether for 2026? 📈

The data is hard to ignore: 89% of middle-market firms are entering 2026 with high optimism. This isn’t just “wishful thinking”—it’s a calculated response to a shifting fiscal and technological landscape.

Here are the four pillars driving this confidence:

Fiscal tailwinds: The One Big Beautiful Bill Act (OBBBA) has finally provided the tax certainty and full-expensing incentives required to move “wait-and-see” capital into active deployments.

Maturity in AI adoption: We have moved beyond the “hype cycle.” 66% of mid-cap leaders are now prioritizing AI as a tool for operational leverage, specifically targeting persistent labor bottlenecks.

The Rise of Alternative Credit: As traditional bank lending remains constrained, the pivot toward private credit and specialized liquidity solutions has decoupled middle-market growth from traditional interest rate volatility.

Strategic Consolidation: With 44% of firms pursuing M&A, we are entering a period of significant market “up-tiering.”

The “Mighty Middle” has spent the last 24 months stress-testing their balance sheets. In 2026, they aren’t just defending their position—they are expanding it.

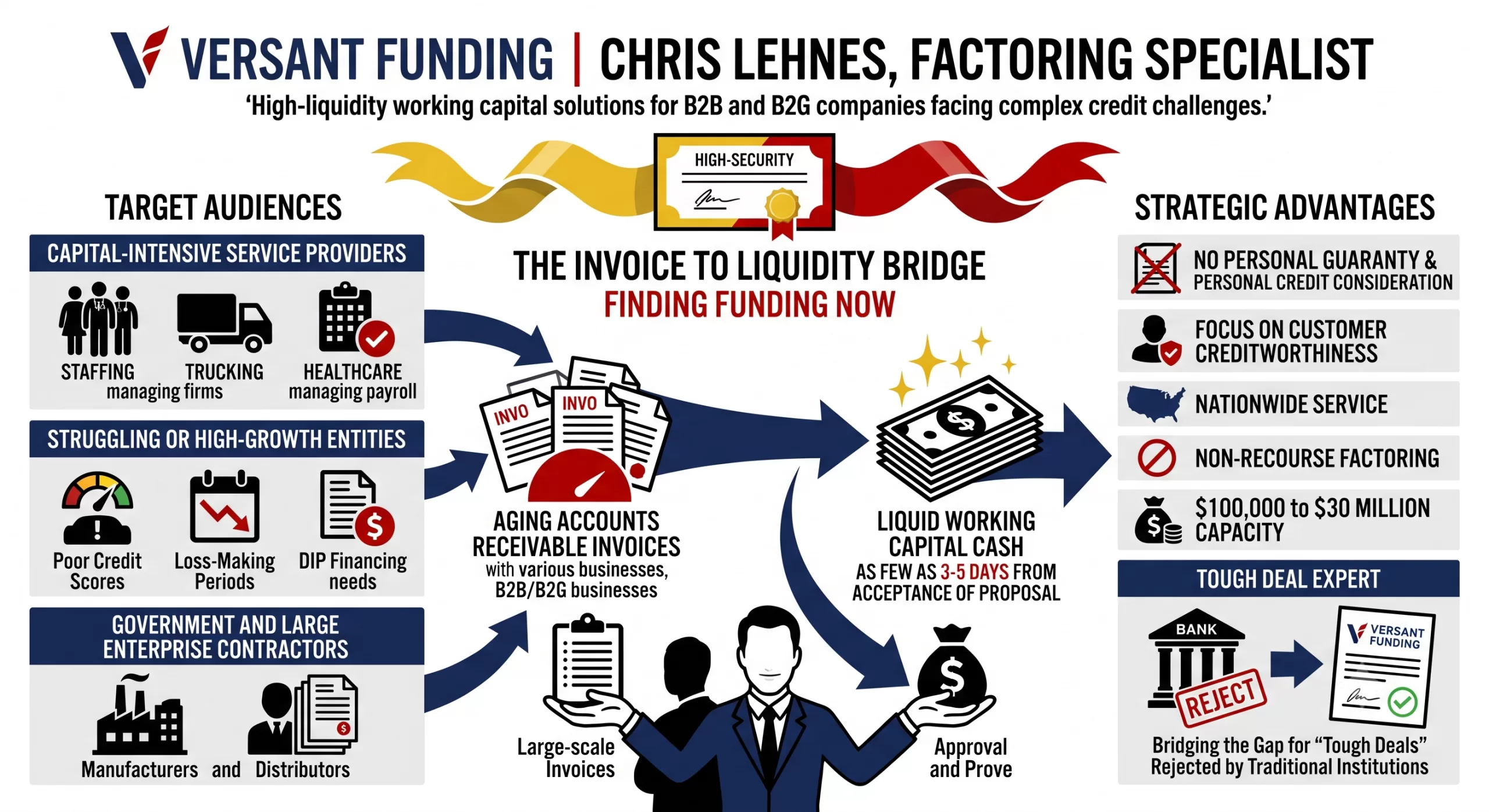

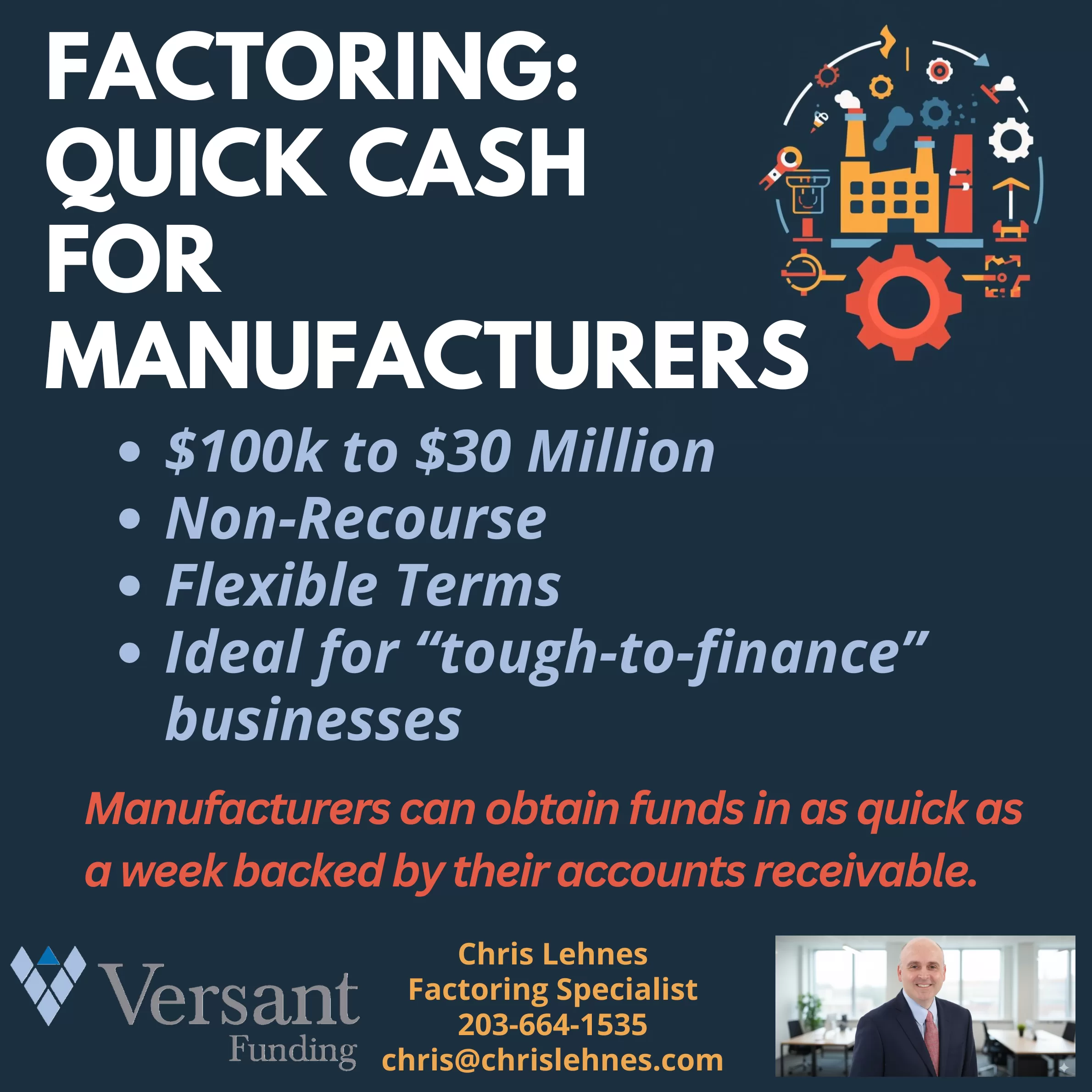

Factoring: The Quick Cash Solution Manufacturers Need Now

In today’s dynamic market, manufacturers face a unique set of challenges. From managing inventory and production schedules to navigating supply chain disruptions and fluctuating demand, the need for reliable, accessible capital is constant. That’s where factoring comes in, offering a powerful and often overlooked solution for quick cash.

At Versant Funding, we understand the specific financial pressures manufacturers endure. That’s why we specialize in providing tailored factoring services designed to get you the capital you need, when you need it. Our latest video, which you can watch above, highlights how factoring can be a game-changer for your business.

What is Factoring, and Why is it Perfect for Manufacturers?

Simply put, factoring allows you to sell your accounts receivable (invoices) to a third party (the factor) at a small discount in exchange for immediate cash. Instead of waiting 30, 60, or even 90 days for your customers to pay, you get the funds right away.

For manufacturers, this means:

Quick Cash Flow: No more cash flow gaps hindering your production or growth initiatives. Get funds in as quick as a week!

Significant Funding: We offer funding from $100,000 to $30 Million, providing substantial support whether you’re a growing mid-sized company or a large enterprise.

Non-Recourse Factoring: This is a crucial benefit for manufacturers. With non-recourse factoring, if your customer fails to pay due to bankruptcy or insolvency, you’re typically not responsible for repaying the advance. This transfers the credit risk away from your balance sheet.

Flexible Terms: We work with you to create terms that fit your unique business model and cash flow requirements.

Ideal for “Tough-to-Finance” Businesses: Traditional bank loans can be hard to secure, especially for newer companies, those with limited collateral, or those experiencing rapid growth. Factoring focuses on the quality of your accounts receivable, making it an accessible option when other avenues are closed.

How Manufacturers Benefit from Factoring:

Imagine being able to:

Purchase Raw Materials: Take advantage of bulk discounts or secure critical components without delay.

Meet Payroll: Ensure your skilled workforce is paid on time, every time.

Invest in New Equipment: Upgrade machinery or expand your production lines to increase efficiency and capacity.

Handle Large Orders: Don’t turn away big opportunities because of insufficient working capital.

Improve Credit Standing: Use the immediate cash to pay suppliers promptly, potentially earning early payment discounts and strengthening your vendor relationships.

Why?

We pride ourselves on being more than just a capital provider. We are your partner in growth. I am dedicated to understanding the intricacies of the manufacturing sector and crafting financial solutions that truly work.

Ready to unlock the potential of your accounts receivable?

To see how factoring can transform your manufacturing business reach out to Chris Lehnes today for a no-obligation consultation.

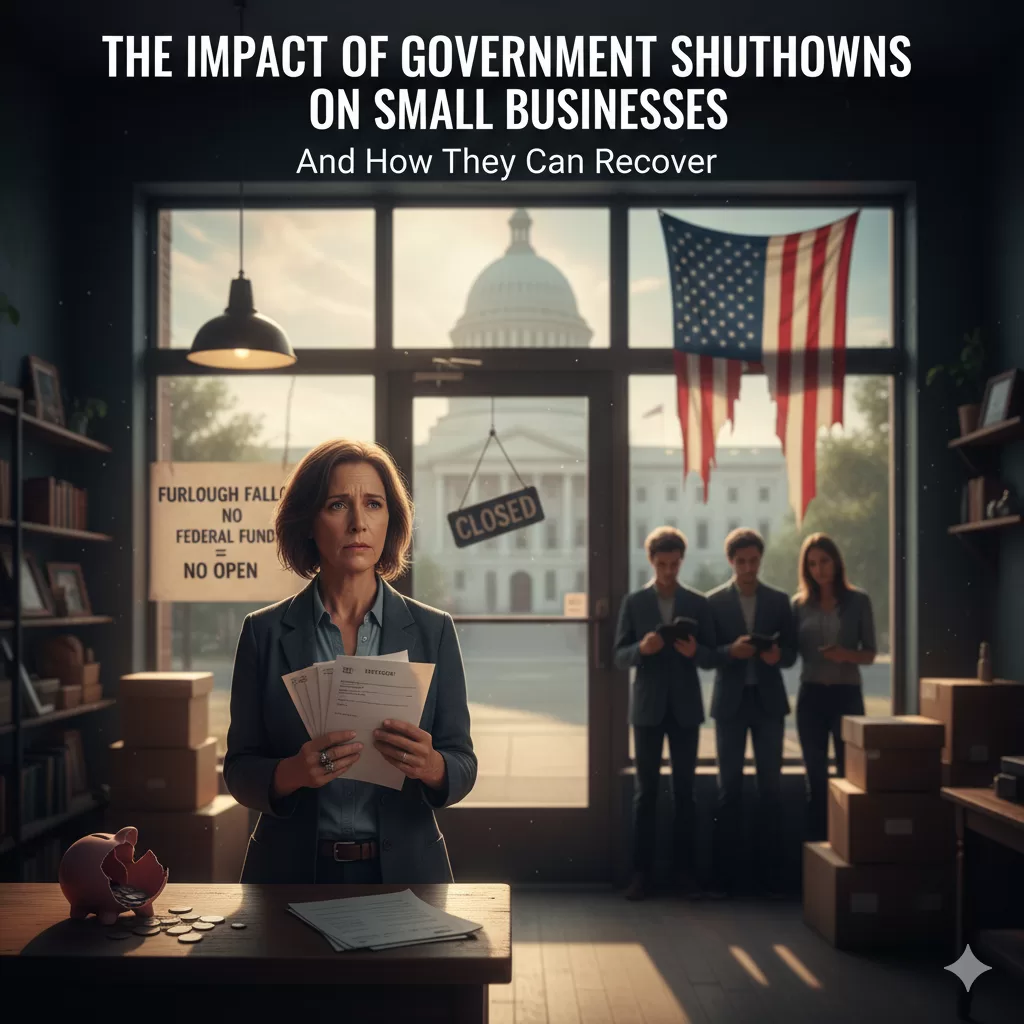

A government shutdown, defined as a lapse in federal appropriations, is frequently framed as a political skirmish in Washington D.C. Yet, its financial reverberations are immediately and intensely felt across the nation, striking at the heart of the U.S. economy: its small businesses. Comprising over 33 million firms and responsible for generating two-thirds of net new jobs, the small business ecosystem is the engine of American enterprise.

However, this vital sector is uniquely fragile when faced with political paralysis. A shutdown creates immediate, cascading, and disproportionate negative effects on small businesses, necessitating proactive recovery strategies from both the private and public sectors. This analysis details the mechanics of this damage—from frozen payments and suspended loans to depressed consumer spending—and outlines the essential steps small businesses must take to recover, mitigate future risk, and advocate for systemic protection.

🛑 II. Immediate and Direct Impacts of Shutdown

The moment a shutdown is triggered, the consequences for small businesses that interact directly with the federal apparatus are sudden, severe, and measurable.

The Freeze on Federal Contracts 📜

For the large segment of small businesses that operate as federal contractors, the shutdown delivers a direct financial shock:

Delayed Payments: The most critical blow is the cessation of payments, converting reliable accounts receivable into financial dead weight. Small contractors, operating on thin margins, are instantly thrust into a cash flow crisis. During the 2018-2019 shutdown, it was estimated that over 90% of federal contractor invoices went unpaid for the duration, causing thousands of small contractors to miss payroll.

Work Stoppage (Stop-Work Orders): For ongoing contracts, agencies issue stop-work orders. The business stops billing, losing revenue entirely, and must decide whether to retain specialized staff without pay or risk the loss of highly skilled talent.

Contracting Uncertainty: The entire procurement pipeline freezes. The Department of Defense (DOD) and NASA, major sources of small business contracting, halted the award of all non-essential contracts, stalling critical high-tech and defense projects.

Suspension of Critical Loans and Financial Support 💰

Small businesses rely heavily on the federal government for capital access, a lifeline that is severed during a shutdown.

SBA Loan Program Stoppage: The suspension of the SBA’s flagship loan programs—primarily the SBA 7(a) and 504 loan guarantee programs—halts guarantees. During the 2018-2019 event, the SBA stopped processing all new loan applications, estimated to have frozen approximately $2 billion in small business financing per week, crippling expansion plans nationwide.

Disaster Loan Delays: Businesses recovering from recent natural disasters also face an immediate freeze in the processing of Economic Injury Disaster Loan (EIDL) applications.

Regulatory and Licensing Paralysis 📝

For firms in regulated industries, the shutdown acts as an involuntary stop sign.

Permit and License Delays: A small craft brewery waiting for a TTB permit to launch a new product cannot proceed. The TTB’s closure in 2018-2019 created a significant backlog, delaying the opening of new breweries, wineries, and distilleries, as they could not legally bottle and sell their products.

Customs and Trade Complications: Small businesses involved in international trade can face delays in clearances and inspections required from furloughed personnel at various agencies, leading to supply chain snags.

📉 III. Indirect and Secondary Economic Impacts – Shutdown

The government shutdown rapidly produces a secondary layer of damage through channels far removed from D.C., primarily through reduced consumer spending and heightened market uncertainty.

The “Furlough Effect” on Consumer Demand 🛍️

The largest secondary impact stems from the sudden loss of income for hundreds of thousands of federal employees and non-essential contractors.

Loss of Federal Employee Income: Furloughed federal workers are placed on mandatory, unpaid leave, forcing them to drastically cut back on discretionary spending. The 35-day shutdown resulted in approximately 800,000 federal workers missing two full paychecks, translating into billions of dollars in lost spending power.

Impact on Local Economies: Businesses relying on the patronage of federal workers suffer immediately. Small restaurants and shops near federal hubs in the D.C. area, as well as businesses dependent on National Park Service tourists, reported revenue declines of 50% or more, with many having to temporarily close their doors. The lack of guaranteed back pay for contractors deepened the slump.

Financial Market and Investor Uncertainty 🏦

A shutdown injects volatility into financial and capital markets, altering the risk assessment for small businesses.

Lender Hesitation: Banks become more hesitant to underwrite new commercial loans, fearing a prolonged economic downturn. Anecdotal evidence from 2019 suggested that many community banks placed a temporary moratorium on all new small business lending until the appropriations process was resolved.

SEC Delays: Small, high-growth companies attempting to raise capital through public filings or private offerings find their efforts stalled. During the shutdown, the SEC could not process many filings, delaying the capital raises of emerging technology and biotech firms.

Data and Resource Loss 📊

Small businesses rely on accurate, timely federal data to make strategic decisions. A shutdown halts the release of critical economic intelligence.

Statistical Freeze: The cessation of data from agencies like the Bureau of Labor Statistics (BLS) and the Census Bureau leaves businesses flying blind. Key economic indicators, including reports on housing starts, retail sales, and GDP components, were delayed, forcing small business owners to make crucial expansion decisions without reliable, up-to-date data.

Loss of Free Technical Assistance: Key support networks like Small Business Development Centers (SBDCs) and the volunteer-based SCORE mentorship program often lose funding or access, cutting off cost-free assistance vital for struggling firms.

🧠 IV. Psychological and Operational Strain

The non-financial impacts inflict deep stress on owners and staff, often determining the long-term viability of the business.

Talent Exodus: Faced with prolonged unpaid leave or layoff risk, highly skilled employees often leave for stable work in the private sector, resulting in costly brain drain.

Cash Flow Crisis Management: Owners are forced into high-risk personal finance decisions. In 2019, many small business owners dependent on federal contracts revealed they had liquidated personal retirement accounts or taken out expensive home equity loans to cover their company’s payroll.

Damage to Business Reputation: The inability to fulfill contracts or meet delivery deadlines due to stop-work orders risks lost goodwill and potential exclusion from future partnership opportunities.

🛠️ V. Strategies for Small Business Recovery and Mitigation – Shutdown

The recovery phase demands proactive management, aggressive financial triage, and a fundamental reassessment of business risk.

5.1 Immediate Financial Triage: Stabilizing the Vessel

The 90-Day Cash Flow Plan (The Survival Budget): Create a hyper-detailed projection, categorizing expenses as Mission-Critical, Negotiable, or Eliminatable.

Aggressive Negotiation with Creditors: Proactively contact commercial lenders to request interest-only payments or short-term principal forbearance. In 2019, many banks, anticipating the back pay to federal workers, were quick to offer forbearance options, but contractors needed to be aggressive in requesting similar terms.

Accessing Local Capital: Immediately explore bridge loan options from local Credit Unions and CDFIs.

5.2 Re-Engaging Federal Systems and Documentation

Upon reopening, businesses must move swiftly and meticulously:

Prioritizing Re-activation: Immediately contact the Contracting Officer (CO) for a Written Resumption Order before restarting work. Be prepared to immediately re-file or re-activate stalled SBA loan applications.

Detailed Documentation: Meticulously document all incurred costs related to the shutdown. This documentation is crucial for negotiating future claims for Termination for Convenience costs.

5.3 Diversification and Risk Management: The Long-Term Shield

The most effective strategy is to ensure the business is never again so vulnerable to political instability.

Client Base Diversification: Actively work to cap federal revenue reliance (e.g., at 60-70% of total revenue) and pursue contracts with state and local governments or the private sector.

Building a Shutdown-Proof Emergency Fund: Adopt the financial discipline to build a dedicated cash reserve equal to 3 to 6 months of operational expenses. This reserve is strictly for maintaining payroll and core utilities during a non-economic disruption.

Operational Agility: Implement cross-training programs to utilize staff for internal projects if a stop-work order is issued, retaining skilled talent while maintaining some level of productivity.

5.4 Advocacy and Systemic Change

Small business owners must leverage their collective voice to push for legislative reform.

The “Wall Off” Principle: Advocate for legislation that grants Excepted Status to critical, non-political economic functions, most importantly the SBA Loan Guarantee Processing and the Payment of Existing, Obligated Federal Contractors. Shielding these functions from the appropriations fight is essential to maintaining the stability of the small business economy.

VI. Conclusion

The resilience of the small business sector is severely tested by government shutdowns. These events are not merely political theatre; they are systemic economic disruptions that destroy cash flow, erode consumer confidence, and inflict severe psychological stress on owners and employees. The 35-day shutdown of 2018-2019 provided undeniable proof that the small business community bears a disproportionate burden of political gridlock.

While recovery demands aggressive financial triage and meticulous documentation, the long-term solution lies in diversification and structural preparedness. Policymakers must recognize that failure to fund critical economic functions, even temporarily, causes an outsized and destructive ripple effect. Ensuring the continuity of SBA lending and contractor payments must be treated as a matter of essential economic stability, insulating the national engine of job creation from political gridlock.

More Than a Headline: 5 Ways a Government Shutdown Silently Cripples Main Street America

1.0 Introduction: Beyond the Beltway Drama

When the federal government shuts down, the news cycle often frames it as a distant political battle confined to Washington D.C. Yet, its financial reverberations are immediately and intensely felt across the nation, striking directly at the heart of the U.S. economy: its small businesses, the very engine of American enterprise responsible for creating two-thirds of all net new jobs.

This vital sector is uniquely and disproportionately vulnerable to the consequences of political paralysis. A shutdown creates an immediate cascade of damage that extends far beyond federal employees, impacting entrepreneurs and local economies nationwide. Here are the five most significant and surprising ways this political gridlock cripples small businesses, proving the damage is far more widespread than a headline can capture.

2.0 The Shutdown’s Ripple Effect: 5 Surprising Impacts on Small Business

2.1 Takeaway 1: The Instant Cash Flow Apocalypse

For the thousands of small businesses operating as federal contractors, a government shutdown triggers an immediate financial shock. During the 35-day shutdown of 2018-2019, an estimated 90% of federal contractor invoices went unpaid. This instantly converts reliable accounts receivable into dead weight, thrusting companies with thin margins into a severe cash flow crisis. Revenue doesn’t just get delayed—it stops entirely, as agencies issue formal “stop-work orders.” Major sources of small business contracting, like the Department of Defense (DOD) and NASA, halt the award of new projects, freezing the entire procurement pipeline and forcing owners into devastating choices, such as whether to miss payroll or attempt to retain highly skilled talent without any pay.

2.2 Takeaway 2: The $2 Billion Weekly Freeze on Ambition

A shutdown severs a critical lifeline for small businesses seeking to grow: access to capital. The Small Business Administration (SBA) is forced to suspend its flagship 7(a) and 504 loan guarantee programs. During the 2018-2019 shutdown, this stoppage was estimated to have frozen approximately $2 billion in small business financing per week. This freeze also extends to Economic Injury Disaster Loan (EIDL) applications, harming businesses already reeling from natural disasters and compounding their crisis. This number represents more than just money on hold; it signifies crippled expansion plans, delayed hiring, and stalled innovation for entrepreneurs across the country who suddenly find their ambitions on indefinite hold.

2.3 Takeaway 3: The Economic Paralysis Spreads Far From D.C.

The financial damage quickly spreads through the “Furlough Effect.” When approximately 800,000 federal workers missed two full paychecks during the extended shutdown, they were forced to drastically cut back on consumer spending. The impact on local economies was immediate and severe. Small restaurants and shops near federal hubs and businesses dependent on National Park Service tourists reported revenue declines of 50% or more. This secondary impact demonstrates how deeply intertwined Main Street is with government operations, even for businesses with no direct federal contracts.

2.4 Takeaway 4: It Puts New Ventures on Indefinite Hold

The impact extends beyond money, creating a regulatory and licensing paralysis that acts as an involuntary stop sign for new ventures. Consider a small craft brewery that has developed a new product but is waiting on a permit from the Alcohol and Tobacco Tax and Trade Bureau (TTB). When the government shuts down, the TTB closes. The brewery cannot legally bottle and sell its new product, killing entrepreneurial momentum. This specific example shows how a shutdown can delay the opening of new breweries, wineries, and distilleries entirely unrelated to government contracting, freezing the very spirit of enterprise.

2.5 Takeaway 5: The Hidden Human Cost for Owners and Employees

Beyond the financial statements, a shutdown inflicts deep psychological and operational strains. The uncertainty can trigger a “talent exodus,” as highly skilled employees leave for more stable private-sector work rather than risk prolonged layoffs. At the same time, owners are forced to take extreme personal risks to keep their businesses afloat. During the 2019 shutdown, many small business owners dependent on federal contracts revealed they had liquidated personal retirement accounts or taken out home equity loans simply to cover their company’s payroll. Finally, the inability to fulfill contracts due to stop-work orders causes lasting damage to a business’s reputation, risking lost goodwill and exclusion from future opportunities.

3.0 Conclusion: From Crisis to Resilience

Government shutdowns are not political theatre; they are systemic economic disruptions that inflict deep, lasting, and disproportionate damage on the nation’s primary job creators. While the immediate aftermath requires financial triage, the long-term solution for businesses lies in strategic preparation, including diversifying their client base and building robust emergency funds.

The 35-day shutdown of 2018-2019 provided undeniable proof that the small business community bears a disproportionate burden of political gridlock.

This repeated cycle of crisis demands a systemic solution, forcing policymakers to answer a fundamental question. It underscores the urgent need to protect the bedrock of the American economy from political instability. How can we insulate essential economic functions, like SBA lending and contractor payments, from future political gridlock to protect the engine of our economy?

The Economic Impact of Government Shutdowns on U.S. Small Businesses

Executive Summary

A government shutdown, or a lapse in federal appropriations, inflicts immediate, severe, and disproportionate harm on the U.S. small business sector—an ecosystem of over 33 million firms responsible for generating two-thirds of net new jobs. The financial repercussions extend far beyond political centers, creating a cascade of negative effects that destabilize this vital engine of the American economy.

The 35-day shutdown of 2018-2019 serves as definitive proof of this vulnerability, where an estimated $2 billion in small business financing was frozen per week due to the suspension of Small Business Administration (SBA) loan processing. During this period, over 90% of federal contractor invoices went unpaid, thrusting thousands of firms into a cash flow crisis. The shutdown’s impact is multifaceted, manifesting as direct financial shocks, indirect economic downturns, and severe operational strains.

Key Impacts Include:

Direct Financial Disruption: Federal contractors face an immediate freeze on payments and stop-work orders. Access to critical capital through SBA loan programs (7(a), 504) is severed, and regulatory processes, such as TTB permits for breweries and wineries, are halted.

Secondary Economic Damage: The furloughing of federal workers—approximately 800,000 during the 2018-2019 event—triggers a sharp decline in consumer spending, with local businesses reporting revenue drops of 50% or more. Market uncertainty causes banks to hesitate on lending and stalls capital-raising efforts at the SEC.

Operational and Psychological Strain: The crisis forces owners into high-risk personal financial decisions, such as liquidating retirement accounts to make payroll. It also triggers an exodus of skilled talent and damages business reputations.

Recovery requires immediate financial triage, proactive creditor negotiation, and meticulous documentation for future claims. However, long-term survival hinges on strategic diversification to reduce reliance on federal revenue (capping it at 60-70%) and building a robust emergency cash reserve of 3-6 months. Ultimately, the analysis advocates for systemic reform through legislation that would “wall off” critical economic functions, such as SBA loan processing and contractor payments, from political appropriations battles to ensure national economic stability.

——————————————————————————–

1. The Anatomy of a Shutdown’s Impact

Government shutdowns are systemic economic disruptions that deliver measurable damage through direct, indirect, and operational channels. The small business sector is uniquely fragile and bears a disproportionate burden of the consequences of political gridlock.

1.1. Direct Financial and Operational Shocks

The most immediate consequences are felt by businesses that interact directly with the federal government for contracts, financing, or regulatory approval.

Impact Area

Mechanism of Harm

2018-2019 Shutdown Case Data

Freeze on Federal Contracts

Delayed Payments: Reliable accounts receivable become financial dead weight, creating an instant cash flow crisis for contractors operating on thin margins. <br> Stop-Work Orders: Agencies halt ongoing contract work, stopping all revenue streams and forcing difficult staffing decisions.

Over 90% of federal contractor invoices went unpaid, causing thousands of small contractors to miss payroll. The DOD and NASA halted all non-essential contract awards.

Suspension of Financial Support

SBA Loan Stoppage: The suspension of the SBA’s 7(a) and 504 loan guarantee programs cuts off a critical lifeline for capital access. <br> Disaster Loan Delays: The processing of Economic Injury Disaster Loan (EIDL) applications is frozen.

The SBA stopped all new loan processing, freezing an estimated $2 billion in small business financing per week, crippling nationwide expansion plans.

Regulatory Paralysis

Permit and License Delays: Businesses in regulated industries cannot proceed with new products or operations. <br> Trade Complications: Furloughed personnel cause delays in customs clearances and inspections, creating supply chain disruptions.

The closure of the Alcohol and Tobacco Tax and Trade Bureau (TTB) created a significant backlog, delaying the opening of new breweries, wineries, and distilleries.

1.2. Indirect Economic Reverberations

The shutdown’s impact quickly radiates outward, depressing the broader economy through reduced spending, market volatility, and a loss of critical data.

The “Furlough Effect” on Consumer Demand: The furloughing of federal workers and non-essential contractors removes billions of dollars from the economy.

During the 35-day shutdown, approximately 800,000 federal workers missed two full paychecks.

This led to a drastic cutback in discretionary spending, causing small businesses near federal hubs and National Parks to report revenue declines of 50% or more.

Financial Market and Investor Uncertainty: Political paralysis creates economic volatility, making lenders more risk-averse.

Anecdotal evidence from 2019 suggests many community banks placed a temporary moratorium on new small business lending.

The Securities and Exchange Commission (SEC) could not process many filings, delaying capital raises for emerging technology and biotech firms.

Loss of Data and Resources: The halt in the release of federal data forces businesses to make strategic decisions without critical intelligence.

Agencies like the Bureau of Labor Statistics (BLS) and the Census Bureau delayed key economic indicators on retail sales, housing starts, and GDP components.

Federally funded support networks like Small Business Development Centers (SBDCs) and the SCORE mentorship program lost access or funding, cutting off free assistance.

1.3. Psychological and Operational Strain

Beyond the financial metrics, a shutdown imposes severe non-financial burdens that can determine a business’s long-term viability.

Talent Exodus: Highly skilled employees, facing layoff risks or unpaid leave, often seek more stable employment in the private sector, resulting in a costly “brain drain.”

Cash Flow Crisis Management: Owners are forced into high-risk personal financial decisions. During the 2019 shutdown, many small business owners reported liquidating personal retirement accounts or taking out expensive home equity loans to cover company payroll.

Damage to Business Reputation: Inability to fulfill contracts due to stop-work orders can damage goodwill with partners and risk exclusion from future opportunities.

2. A Framework for Recovery and Resilience

Recovery from a government shutdown requires a combination of immediate financial triage and long-term strategic adjustments to mitigate future risk.

2.1. Immediate Recovery Actions

Once government operations resume, small businesses must act swiftly and methodically to stabilize their finances and restart operations.

Financial Triage:

The 90-Day Cash Flow Plan: Develop a detailed “survival budget” that categorizes all expenses as Mission-Critical, Negotiable, or Eliminatable.

Aggressive Creditor Negotiation: Proactively contact lenders to request short-term forbearance or interest-only payments.

Access Local Capital: Explore bridge loan options from local Credit Unions and Community Development Financial Institutions (CDFIs).

Re-Engaging Federal Systems:

Prioritize Re-activation: Immediately contact the relevant Contracting Officer (CO) to obtain a Written Resumption Order before restarting any work.

Document Everything: Meticulously document all shutdown-related costs. This is crucial for negotiating any future claims for “Termination for Convenience” costs.

2.2. Long-Term Mitigation and Risk Management

The most effective strategy is to build a business model that is fundamentally less vulnerable to political instability.

Client Base Diversification: Actively work to reduce reliance on federal contracts by pursuing clients in the private sector or at the state and local government levels. The recommended target is to cap federal revenue reliance at 60-70% of total revenue.

Shutdown-Proof Emergency Fund: Build and maintain a dedicated cash reserve equivalent to 3 to 6 months of essential operational expenses (payroll, core utilities). This fund should be reserved strictly for non-economic disruptions.

Enhance Operational Agility: Implement staff cross-training programs. This allows employees to be repurposed for internal projects during a stop-work order, retaining skilled talent while maintaining productivity.

3. Proposed Systemic Reforms: The “Wall Off” Principle

To prevent future economic damage, small business owners are encouraged to advocate for legislative reforms that insulate core economic functions from political gridlock. The central proposal is the “Wall Off” principle, which calls for legislation that grants “Excepted Status” to critical, non-political economic functions. This would ensure their continuity during a lapse in appropriations.

The two most critical functions to be shielded are:

SBA Loan Guarantee Processing: To maintain the flow of capital to small businesses.

Payment of Existing, Obligated Federal Contractors: To prevent immediate cash flow crises for firms that have already performed work.

Treating the continuity of these functions as a matter of essential economic stability is paramount to protecting the national engine of job creation.

Core Principles and Applications of Upstream Thinking

This book synthesizes the core principles of “upstream thinking,” a framework for preventing problems rather than reacting to them. The central thesis is that society is disproportionately focused on downstream responses—addressing crises, emergencies, and failures after they occur. An upstream approach, conversely, involves proactively identifying and dismantling the systems that cause these problems in the first place. This shift is impeded by three primary barriers: Problem Blindness, the failure to see a problem or the belief that it is inevitable; Lack of Ownership, a mindset where those capable of fixing a problem believe it is not their responsibility; and Tunneling, a state of scarcity (of time, money, or bandwidth) that forces short-term, reactive thinking and precludes long-term planning. Successful upstream interventions require leaders to unite diverse teams, identify high-leverage points within complex systems, establish early warning signals, and secure funding for outcomes that are often invisible—the absence of problems. The analysis reveals that effective upstream work is not about finding a single “magic pill” solution but about creating data-rich “scoreboards” that enable continuous learning and systems-level change.

——————————————————————————–

1. The Upstream Philosophy: Prevention Over Reaction

The core concept of upstream thinking is captured in a public health parable: two friends rescuing an endless stream of drowning children from a river, until one goes upstream “to tackle the guy who’s throwing all these kids in the water.” This metaphor distinguishes between downstream actions, which react to problems, and upstream efforts, which aim to prevent them.

Defining Upstream vs. Downstream Action

Downstream Action: Reactive, tangible, and focused on restoration. Examples include a call center representative resolving a customer complaint, a doctor performing bypass surgery, or a police officer making an arrest after a crime. These actions are often demanded by circumstance.

Upstream Action: Proactive, preventative, and focused on systems change. It involves “systems thinking” to systematically reduce the harm caused by problems. Examples include redesigning a website so customers don’t need to call for help, promoting policies that support healthy lifestyles to prevent heart disease, or creating community opportunities that deter crime. These efforts are chosen, not demanded.

The further one moves upstream, the more complex, ambiguous, and slower the solutions become, but the potential for massive and long-lasting good increases significantly. An intervention can exist at many points along a spectrum; for example, swim lessons are further upstream than life preservers in preventing drowning.

The Case of Expedia: A Model for Upstream Intervention

The travel website Expedia provides a clear illustration of a successful upstream intervention.

The Downstream Problem: In 2012, 58 out of every 100 Expedia customers placed a support call after booking. The top reason, accounting for 20 million calls annually at a cost of roughly $100 million, was to request a copy of their itinerary.

The Downstream Mindset: The call center was managed for efficiency—minimizing call time—rather than questioning why the calls were necessary.

The Upstream Shift: A “war room” was created with a mandate to “Save customers from needing to call us.” They analyzed the root causes of the calls.

Upstream Solutions: For the itinerary issue, they implemented simple fixes: adding an automated voice-response option, changing email protocols to avoid spam filters, and creating an online self-service tool.

The Result: The 20 million itinerary-related calls were virtually eliminated. The overall percentage of customers needing to call for support dropped from 58% to approximately 15%. This success was achieved by integrating the work of different teams (product, tech, support) to solve a problem that no single group “owned.”

The Asymmetry of Attention: Why Society Favors Reaction

Despite the clear benefits of prevention, societal efforts are overwhelmingly skewed toward reaction.

Tangibility and Measurement: Downstream work is more tangible and easier to measure. A police officer who writes a stack of tickets has a visible output, while an officer whose presence on a dangerous corner prevents accidents has invisible victims and victories written only in declining data.

Funding and Resources: We spend billions to recover from disasters like hurricanes and earthquakes, while disaster preparedness is “perpetually starved for resources.” The U.S. healthcare system, a $3.5 trillion industry, is designed almost exclusively for reaction, functioning like a giant “Undo button” for ailments rather than a system for creating health.

Heroism: Society celebrates the rescue, the recovery, and the response. Upstream work creates a quieter breed of hero, one “actively fighting for a world in which rescues are no longer required.”

Case Study: Healthcare Spending in the U.S. vs. Norway

The contrast between U.S. and Norwegian healthcare spending illustrates the consequences of a downstream focus. While both nations spend a similar percentage of GDP on total health (combining formal healthcare with “social care” like housing, food, and childcare), their allocation is radically different.

Spending Metric

United States

Norway

Spending Ratio (Upstream:Downstream)

For every 1** spent downstream, the U.S. spends roughly **1 upstream.

For every 1** spent downstream, Norway spends roughly **2.50 upstream.

Focus

World leader in downstream, high-tech treatments (e.g., knee replacements, cancer treatment).

Focus on upstream support systems (e.g., free prenatal/delivery care, 49 weeks of paid parental leave, guaranteed high-quality daycare, free college).

Health Outcomes

34th in infant mortality, 29th in life expectancy, 21st in stress levels.

5th in infant mortality, 5th in life expectancy, 1st in stress levels.

The data suggests the U.S. is not necessarily spending “too much” on health, but that its allocation is radically different from its peers, prioritizing expensive cures over cost-effective prevention.

2. The Three Barriers to Upstream Thinking

Despite the logic of prevention, several powerful forces consistently push individuals and organizations downstream.

A. Problem Blindness: The Invisibility of Solvable Problems

Problem blindness is the belief that negative outcomes are natural, inevitable, or out of one’s control. It is treating a solvable problem like the weather.

Mechanism: It arises from inattentional blindness (intense focus on one task causing one to miss other information, like radiologists missing a gorilla in a CT scan) and habituation (growing accustomed to consistent stimuli until they become normal).

Example: Chicago Public Schools (CPS): In 1998, the 52.4% graduation rate was seen by many as an intractable problem caused by poverty and other societal ills—”that’s just how it is.” The problem was accepted as a regrettable but inevitable condition.

Example: Sexual Harassment: Before the term was coined in 1975 by Lin Farley, the behavior was so normalized that women were often encouraged to tolerate it. Giving the problem a name—”sexual harassment”—was an act of “problematizing the normal,” helping society awaken from problem blindness.

Example: C-Sections in Brazil: An 84% C-section rate in Brazil’s private health system was seen as normal by many doctors, driven by convenience and financial incentives. An activist movement led by mothers who felt pressured into the procedure successfully challenged this norm, reframing it as a public health problem.

B. Lack of Ownership: “Not My Problem to Fix”

This barrier exists when the people or groups best positioned to solve a problem declare, “That’s not mine to fix.” This can result from fragmented responsibilities, self-interest, or a perceived lack of legitimacy.

Fragmented Responsibility: At Expedia, no single team was measured on reducing customer calls, so no one “owned” the problem.

Lack of Psychological Standing: People may feel they lack the legitimacy to act on a problem that doesn’t affect them personally. Research shows that explicitly extending standing (e.g., naming a group “Men and Women Opposed to Proposition 174”) can dramatically increase participation from those without a direct vested interest.

Taking Ownership: Dr. Bob Sanders & Car Seats: Spurred by a 1975 article in Pediatrics that extended psychological standing to pediatricians on auto safety, Dr. Sanders took ownership of the issue. He successfully lobbied for Tennessee to become the first state to mandate child car seats in 1978. This micro-level action catalyzed a macro-level change, with all 50 states passing similar laws by 1985, saving an estimated 11,274 young lives by 2016.

Taking Ownership: Ray Anderson & Interface: The founder of carpet-tile firm Interface took ownership of his company’s environmental impact after reading Paul Hawken’s The Ecology of Commerce. He launched “Mission Zero,” a quest to eliminate the company’s negative environmental footprint by 2020. This was an optional, self-imposed burden that transformed the company’s culture and processes.

C. Tunneling: The Tyranny of Short-Term Crises

When experiencing scarcity of time, money, or mental bandwidth, people adopt “tunnel vision.” They stop long-term planning and focus solely on managing the immediate crisis, which prevents upstream thinking.

The Scarcity Trap: The experience of poverty reduces cognitive capacity more than a full night without sleep. It forces short-sighted decisions (like taking a payday loan) not because people are undisciplined, but because the tunnel of scarcity leaves no room for long-term considerations.

Organizational Tunneling: A study of nurses found they were constantly engaged in creative workarounds for recurring problems (e.g., missing equipment, lack of towels) but never engaged in fixing the underlying processes. Their scarce time and attention kept them in a reactive mode.

Escaping the Tunnel: Escaping requires creating slack—a reserve of time or resources dedicated to problem-solving. This can be structured, as with the “safety huddles” in hospitals or the “Freshman Success Teams” at CPS, which provide a guaranteed forum for emerging from the tunnel to address systems-level issues.

Co-opting the Tunnel: The Ozone Layer: To address the long-term threat of ozone depletion, advocates had to make an upstream problem feel downstream. They co-opted the power of tunneling by creating urgency through public advocacy, the memorable metaphor of an “ozone hole,” and negotiating international agreements like the Montreal Protocol that removed threats for opponents (like DuPont), thus reducing their need to fight the solution.

3. Key Strategies for Upstream Leaders

Successfully navigating the barriers requires addressing a series of fundamental questions.

A. How Will You Unite the Right People?

Upstream work is fundamentally collaborative, requiring leaders to “surround the problem” with all the necessary stakeholders.

Key Insight: Give every stakeholder a role. Progress hinges on voluntary effort, so maintaining a “big tent” is crucial.

Case Study: Iceland’s War on Teen Substance Abuse: In the 1990s, 42% of Icelandic teens reported being drunk in the past month. A coalition of researchers, policymakers, schools, parents, and community groups united to change the culture around teens.

Strategy: They focused on boosting “protective factors” (e.g., participation in formal sports, time spent with parents, “natural highs”) and reducing “risk factors” (unstructured, unsupervised time).

Tactics: They reinforced curfews, gave families “gift cards” for recreational activities, and professionalized coaching in sports clubs.

Result: Over 20 years, the percentage of teens getting drunk in the past 30 days fell from 42% to 5%. Daily smoking dropped from 23% to 3%.

Case Study: Domestic Violence in Newburyport, MA: After a woman was murdered by her estranged husband, the Jeanne Geiger Crisis Center united police, advocates, parole officers, and prosecutors to form a Domestic Violence High Risk Team.

Data-Driven Collaboration: The team meets monthly to review cases of women identified by the “Danger Assessment” tool as being at extreme risk of homicide. They use a by-name list to coordinate actions like police drive-bys and creating emergency plans.

Result: In the 14 years since the team’s formation, not one woman in the communities they serve has been killed in a domestic violence–related homicide, compared to 8 in the 10 years prior.

The Role of Data: In many successful upstream efforts, data is not used for top-down “inspection” but for frontline “learning.” Real-time, granular data (like a by-name list) becomes the centerpiece that unites diverse teams around a concrete and shared goal: “What are we going to do about Michael next week?”

B. How Will You Change the System?

Lasting upstream work must culminate in systems change, altering the “water” we swim in so that better outcomes happen by default.

Systems Determine Probabilities: A well-designed system makes success highly probable (e.g., fluoridated water preventing cavities). A flawed system rigs the game against certain people. As Dr. Anthony Iton discovered, disparities in life expectancy of up to 20 years between nearby ZIP codes are not caused by a few factors, but by entire systems (housing, education, crime, food access) that create “incubators of chronic stress.”

The California Endowment’s BHC Initiative: This $1 billion, 10-year program aims to fix these broken systems not by directly providing health services, but by empowering residents of 14 challenged communities to gain political power and win policy victories that reshape their environments.

The Danger of Enabling Bad Systems: Some well-intentioned downstream efforts can inadvertently prop up the flawed systems that create need. For example, while DonorsChoose provides vital classroom supplies, its success could excuse school districts from their funding obligations. The goal should be to push for a world where such crutches are no longer needed.

C. Where Can You Find a Point of Leverage?

In complex systems, the challenge is finding the right lever. This requires getting “proximate” to the problem.

Case Study: The UChicago Crime Lab & “Becoming a Man” (BAM): To understand youth violence, researchers read 200 consecutive homicide reports. They discovered that many deaths resulted not from strategic gang wars but from impulsive reactions to trivial disputes. This pointed to impulsivity as a leverage point.

The Intervention: They funded and studied “Becoming a Man” (BAM), a program that used small-group sessions and cognitive behavioral therapy (CBT) to help at-risk young men learn to manage anger and slow down their thinking in fraught situations.

The Result: A randomized controlled trial found that BAM participants had 45% fewer violent-crime arrests.

The Power of Proximity: Architects designing for the elderly donned an “age simulation suit” to experience navigation challenges firsthand. This direct experience revealed leverage points like the need for more benches, handrails, and three-step escalators.

D. How Will You Get Early Warning of the Problem?

Early warning signals provide the time and maneuvering room to prevent a problem or blunt its impact.

Predictive Analytics:

LinkedIn: Discovered that a customer’s product usage in the first 30 days could predict their likelihood of churning a year later. They shifted resources to intensive onboarding to ensure early engagement.

Northwell Health EMS: Uses historical data on 911 calls to predict where emergencies will occur (e.g., near nursing homes at mealtimes) and forward-deploys ambulances to reduce response times.

Human Sensors:

Sandy Hook Promise: After the 2012 school shooting, the organization realized that in most mass shootings, the perpetrator tells someone their plans in advance. They created the “Know the Signs” program to train students to spot warning signs and the “Say Something” anonymous tip line to report them. This system has averted multiple credible school shooting threats and led to hundreds of suicide interventions.

The Danger of False Positives: Early warning systems can backfire. An “epidemic” of thyroid cancer in South Korea was revealed to be an epidemic of overdiagnosis. Mass screening found huge numbers of slow-growing, nonlethal cancers (“turtles”), leading to unnecessary and harmful treatments for a problem that didn’t exist.

E. How Will You Measure Success and Avoid “Ghost Victories”?

Success in upstream work is often the absence of a negative event, making it hard to measure. This reliance on proxy measures can lead to “ghost victories”—superficial successes that cloak underlying failure.

Mistaking Macro Trends for Success: In the 1990s, police chiefs across the U.S. claimed credit for falling crime rates, when in fact they were mostly benefiting from a nationwide trend.

Misalignment of Measures and Mission: The City of Boston’s Public Works department measured its sidewalk repair success by spending per zone and 311 cases closed. This led them to fix sidewalks in wealthy neighborhoods (whose residents called 311) while neglecting crumbling sidewalks in poor neighborhoods, undermining their mission of equity and walkability.

Measures Becoming the Mission: This is the most destructive form, where people “game” the metrics. The NYPD’s CompStat system, which held precinct leaders accountable for crime statistics, led to the widespread downgrading of crimes. In a chilling example, a reported rape of a prostitute was nearly reclassified as a “theft of service” to keep the numbers down.

To avoid ghost victories, leaders should use paired measures (balancing quantity with quality, as CPS did with graduation rates and ACT scores) and “pre-game” how measures could be misused.

F. How Will You Avoid Doing Harm?

Upstream interventions tinker with complex systems and can create unintended negative consequences, known as the “cobra effect.”

Case Study: Macquarie Island: A decades-long effort to eradicate invasive species on a subantarctic island created a cascade of problems. Killing rabbits (to stop erosion) led cats to eat rare birds. Killing the cats led to a rabbit population explosion. Killing all pests led to invasive weeds running rampant.

Anticipating Second-Order Effects: Wise interventions require seeing the whole system. The “cobra effect” is when an attempted solution makes the problem worse. Examples include an open-office plan meant to increase face-to-face collaboration actually causing it to plunge by 70%, or a ban on thin plastic bags leading retailers to offer thicker plastic bags.

The Need for Feedback Loops: Because not all consequences can be foreseen, upstream work requires experimentation and fast, reliable feedback loops. A business that creates a feedback loop for its staff meetings (rating each meeting on a 1-5 scale) can continuously improve them, whereas most meetings never get better because there is no mechanism for learning.

G. Who Will Pay for What Does Not Happen?

Funding prevention is notoriously difficult because success is invisible and payment models are designed for reaction.

The “Wrong Pocket Problem”: This occurs when the entity that pays for an intervention is not the one that reaps the financial benefits.

Case Study: The Nurse-Family Partnership (NFP): This program, which provides nurse home visits to first-time, low-income mothers, has been proven by multiple RCTs to produce significant long-term social benefits (e.g., reduced child abuse, preterm births, crime, and welfare payments), yielding a return of over $6 for every $1 invested. However, it struggles to get funding because the benefits are scattered across many “pockets” (Medicaid, criminal justice, social services), while a single entity is asked to bear the upfront cost.

Innovative Funding Models:

Pay for Success: A model being used in South Carolina to fund NFP, where private investors and foundations provide upfront capital. If the program meets pre-agreed success metrics, the government repays the investors. This shifts the financial risk away from the government.

Accountable Care Organizations (ACOs): A model where Medicare shares savings with groups of doctors who succeed in keeping their patients healthier and out of the hospital, creating a direct financial incentive for prevention.

4. Addressing Distant and Improbable Threats (“Far Upstream”)

Upstream thinking can also be applied to one-off, improbable, or unpreventable threats.

The Prophet’s Dilemma: This is a prediction that prevents what it predicts from happening. The massive global effort to fix the Y2K bug is a prime example. When disaster didn’t strike, many claimed it was a hoax, but it is likely the frantic preparations were what prevented the catastrophe.

The Power of Rehearsal: The “Hurricane Pam” simulation, conducted 13 months before Hurricane Katrina, convened 300 stakeholders to game-plan a response to a catastrophic New Orleans hurricane. While the eventual Katrina response was a national failure in many respects, the planning from Pam led to a drastically improved “contraflow” evacuation plan, which is credited with reducing the death toll from a projected 60,000 to approximately 1,700. The lesson is that preparing for disaster requires practice, but organizations in a state of “tunneling” often fail to invest in it.

Existential Risk & The “Black Ball” Hypothesis: Philosopher Nick Bostrom posits that technological invention is like pulling balls from an urn. So far we have pulled white (beneficial) and gray (mixed-blessing) balls. But what if there is a black ball—a technology that is easily accessible and allows a small group to cause mass destruction, thereby destroying civilization? The response to the remote threat of “Moon germs” in the 1960s, which led to the creation of NASA’s Planetary Protection Officer and strict quarantine protocols, provides an early model for how humanity can collectively address improbable but high-stakes risks.

5. Conclusion: You, Upstream

The principles of upstream thinking can be applied by individuals to solve personal and organizational problems.

Personal Application: Identify recurring problems in life—from finding parking to marital friction—and devise systems to prevent them. The creation of “Daddy Dolls” by a military spouse to ease her children’s pain during deployment is a powerful example of an individual creating an upstream solution.

Engaging in Societal Problems: When seeking to contribute to larger issues, one should:

Be impatient for action but patient for outcomes: Upstream work is a long game of chipping away at a problem.

Recognize that macro starts with micro: You cannot help a thousand people until you understand how to help one. Deep, proximate understanding is key.

Favor “Scoreboards” over “Pills”: Prioritize initiatives that use real-time data for continuous learning and adaptation (a scoreboard) over those that seek a single, perfect, scalable solution that cannot be changed (a pill).

The Power of One Person: A single, retiring actuary at the Centers for Medicare & Medicaid Services wrote a “cry of the heart” letter to his boss, successfully arguing that the agency should not count “longer lives” as a cost when evaluating preventive programs. This quiet act of defiance changed a federal rule, unlocking funding for life-saving programs and demonstrating that even within vast bureaucracies, one person can achieve a profound upstream victory.

Upstream Thinking Study Guide

Quiz: Short-Answer Questions