What It Means for You

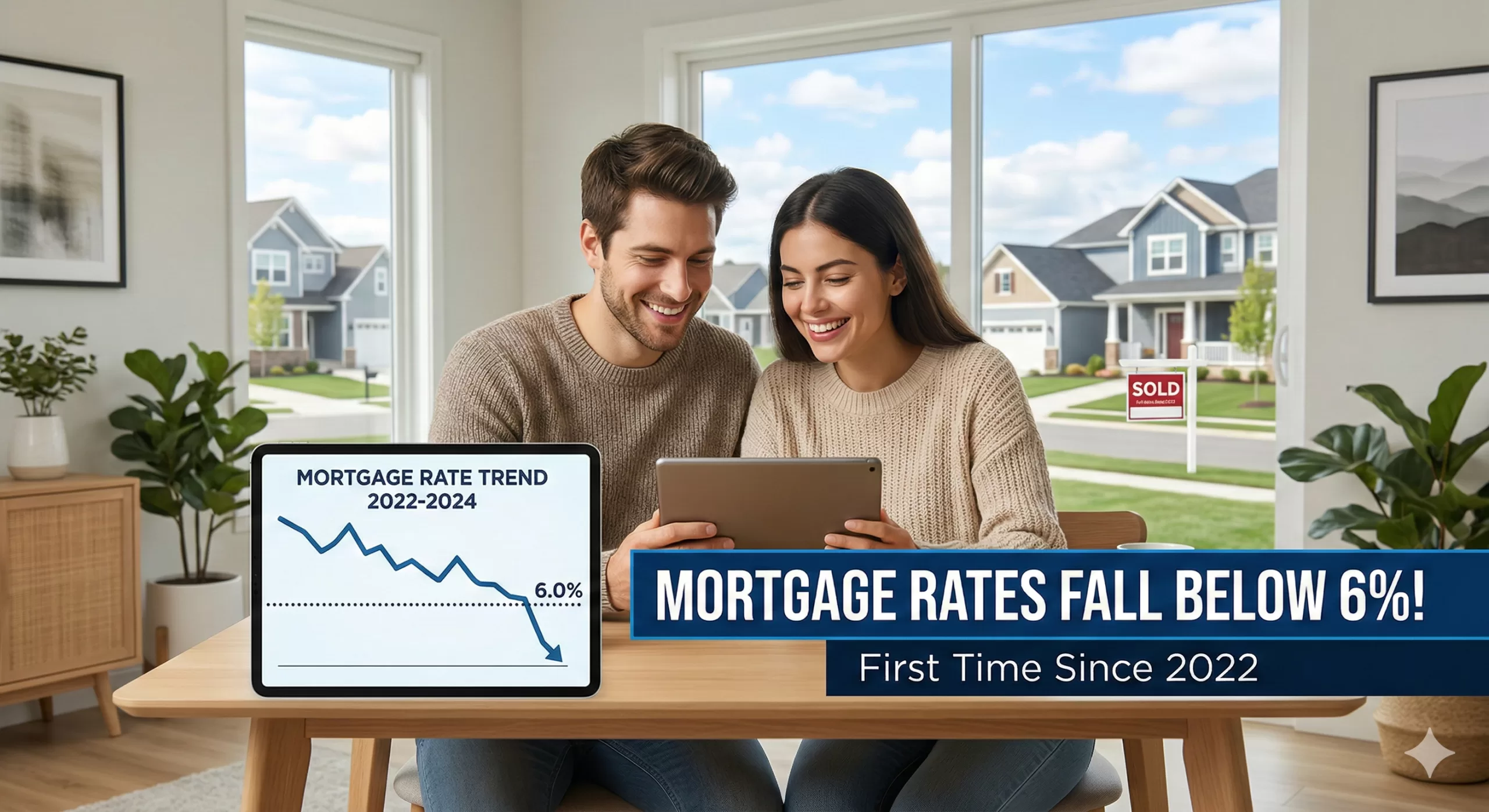

Mortgage Rates – The housing market has seen a welcome shift! Mortgage rates have fallen below 6% for the first time since 2022, offering a significant improvement for potential homebuyers. This news comes as a breath of fresh air after a period of steadily climbing rates that have put a strain on many budgets.

What Does This Mean for Potential Homebuyers?

The drop in mortgage rates translates directly into increased affordability for those looking to purchase a home. This can be beneficial in several ways:

- Lower Monthly Payments: A lower interest rate means a smaller portion of your monthly payment goes towards interest, reducing your overall housing cost.

- Increased Buying Power: With lower monthly payments, you may be able to qualify for a larger loan amount, potentially allowing you to purchase a more expensive home.

- Refinancing Opportunities: Existing homeowners who currently have a higher mortgage rate may be able to refinance their loan and save money on their monthly payments.

Why Are Mortgage Rates Falling?

While the exact reasons behind the rate drop are complex, several factors may be contributing to the trend:

- Lower Inflation: Inflation has shown signs of cooling down, which can influence interest rates.

- Economic Growth: While economic growth has been moderate, some signs suggest it may be slowing, which can also affect mortgage rates.

- Changes in the Bond Market: Bond yields, which are closely tied to mortgage rates, have also seen a decline.

What Should You Do Now?

If you’ve been on the fence about buying a home, this could be an excellent time to re-evaluate your options. Here are some steps to consider:

- Get Pre-Approved for a Mortgage: This will give you a clear idea of how much you can borrow and help you understand your monthly payment.

- Shop Around for Rates: Different lenders offer varying rates, so it’s essential to compare offers from multiple institutions.

- Consider Your Long-Term Goals: While the lower rates are attractive, it’s crucial to ensure that buying a home is the right decision for your long-term financial goals.

Important Note: It’s important to remember that mortgage rates are subject to change based on economic conditions and other factors. While the current trend is encouraging, it’s essential to stay informed about any potential shifts in the market.

Conclusion:

The drop in mortgage rates below 6% is a significant development for the housing market, offering some much-needed relief to potential homebuyers and homeowners alike. If you’ve been considering buying a home, this could be the right time to take action. With lower monthly payments and increased buying power, you may be closer to achieving your homeownership goals than you thought. However, it’s crucial to act carefully and seek professional advice to make the best decision for your individual situation.

Primary Data Sources

- Freddie Mac (Primary Mortgage Market Survey): The ultimate source for the 5.98% figure. Freddie Mac released its weekly report on February 26, 2026, confirming that the 30-year fixed-rate mortgage dipped below 6% for the first time in approximately 3.5 years.

- The Federal Reserve (FRED): Used to verify historical trends, specifically confirming that the last time rates were at this level was September 8, 2022 (when they were 5.89%).

News and Analysis Sources

- CBS News: Provided context on the White House’s initiatives (such as the $200 billion mortgage bond purchase plan) and expert commentary on the “spring home-buying season.”

- Associated Press (AP): Detailed the influence of the 10-year Treasury yield on mortgage pricing and quoted housing economists regarding market entry for buyers and sellers.

- Bankrate: Provided comparative data, including the national average APR for 15-year mortgages and historical context for the rate hikes of 2023-2025.

Mortgage rates in 2026 forecast This video provides expert analysis on how these sub-6% rates impact monthly affordability and what to expect for the rest of the 2026 housing market