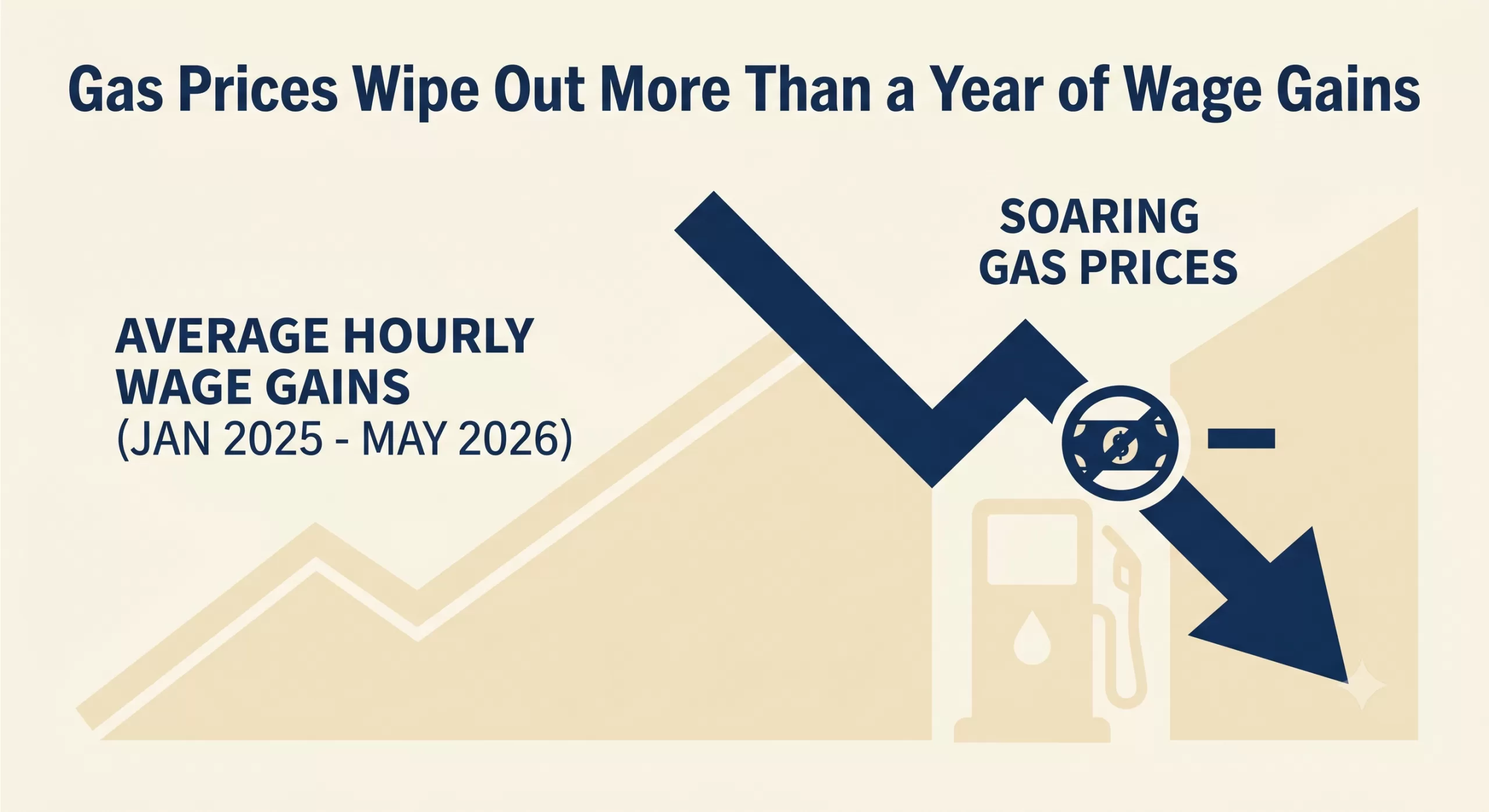

Impact of Iran War Ripple through the Economy Due to Gas Prices

The latest macroeconomic indicators including gas prices paint a challenging picture for both consumers and businesses. Following the Labor Department‘s recent reports, it is clear that soaring energy costs have effectively neutralized recent progress in worker compensation. With top-line inflation advancing to 4.2% in May—the highest level in three years—and gasoline prices surging, real average hourly earnings have been pushed all the way back to January 2025 levels.

For the second consecutive month, inflation has outpaced wage growth. The reality is that gas prices have wiped out more than a year of wage gains.

The Macroeconomic Squeeze

The ripple effects of this inflationary spike are significant. The Federal Reserve now faces a complex policy dilemma as they weigh interest rate decisions against a backdrop of stubborn inflation and squeezed household budgets. When wages lag behind inflation, consumer spending inevitably cools, particularly among middle- and lower-income brackets who are forced to allocate a larger share of their take-home pay to essentials like fuel and groceries.

What This Means for Business Owners

While the headlines focus on the consumer at the pump, small and mid-sized businesses are absorbing these shocks on multiple fronts:

Increased Operational Costs: Surging fuel prices directly inflate the cost of transportation, logistics, and supply chain operations.

Margin Compression: Businesses face the difficult choice of passing higher costs onto increasingly price-sensitive consumers or absorbing the losses and shrinking their profit margins.

Wage Pressure: Even though real wages are falling, nominal wage demands remain high as employees seek relief from the rising cost of living, straining payroll budgets.

Navigating the Cash Flow Crunch

During periods of high inflation and uncertain interest rates, liquidity becomes a paramount concern. Industries heavily reliant on steady cash flow—such as manufacturing, staffing, healthcare, and distribution—can find their working capital severely constrained when expenses rise faster than revenues can be collected.

Waiting 30, 60, or 90 days for clients to pay outstanding invoices is a luxury many companies cannot afford when the cost of doing business is escalating weekly. Accounts receivable factoring offers a strategic mechanism to bridge this gap. By converting outstanding B2B invoices into immediate working capital, business owners can cover rising operational costs, meet payroll obligations, and navigate economic volatility without taking on new debt or waiting on unpredictable macroeconomic shifts.

As we continue to monitor the inflation data and the Fed’s next moves, maintaining robust working capital will be the defining factor for businesses looking to weather this storm.

Today marks a significant turning point in European monetary policy: the European Central Bank (ECB) has officially reversed course, raising its key interest rates for the first time in nearly three years.

After an extended period of cuts and holds, the era of steadily declining borrowing costs in the Eurozone has temporarily hit a wall. Let’s break down the data, the underlying causes, and what this means for the broader economy.

The Decision: By the Numbers

In a move widely anticipated by financial markets and economists, the ECB’s Governing Council elected to raise its key interest rates by 0.25 percentage points (25 basis points).

Here is a quick breakdown of where the central bank’s key rates stand effective immediately:

ECB Facility

Previous Rate

New Rate (June 2026)

Deposit Facility

2.00%

2.25%

Main Refinancing Operations

2.15%

2.40%

Marginal Lending Facility

2.40%

2.65%

This decision officially ends a cycle that began back in September 2023, representing a decisive reaction to shifting economic realities on the ground.

Why is the ECB Hiking Rates Now?

The ECB has a single, primary mandate: to maintain price stability by targeting an inflation rate of 2.0%. The decision to hike rates is a direct response to recent data showing that inflation is moving in the wrong direction.

Headline Inflation Surge: In May 2026, Eurozone consumer prices rose to 3.2% year-over-year. This marks a significant acceleration from earlier in the year and blows past the central bank’s comfort zone.

The Energy Shock: A major driver behind this inflationary spike is the ongoing geopolitical conflict in the Middle East. Disrupted shipping routes and volatile commodity markets caused energy prices to jump nearly 11% last month compared to the same period last year.

Core Inflation Creep: The energy shock isn’t isolated. Core inflation—which strips out highly volatile food and energy costs—rose to 2.5%. This indicates that higher energy overheads are beginning to bleed into the broader costs of everyday goods and services.

What Does This Mean for the Eurozone?

When the ECB pulls the interest rate lever, the effects ripple through the entire financial system. Here is what to expect:

More Expensive Borrowing: For consumers and businesses, the cost of credit is going up. Homeowners holding variable-rate or tracker mortgages will see their monthly repayments increase almost immediately.

A Squeeze on Growth: While higher interest rates are necessary to cool down inflation, they simultaneously suppress economic activity. Reflecting the strain of higher energy costs and tighter financial conditions, the ECB has already revised its growth forecasts downward, anticipating the Eurozone economy will grow by a sluggish 0.8% in 2026.

Currency Impacts: Higher interest rates generally make a currency more attractive to yield-seeking investors. A hawkish stance from the ECB typically provides upward support for the Euro (EUR) against other major currencies, provided the broader economic outlook doesn’t deteriorate too sharply.

Looking Ahead: Is This the Start of a New Cycle?

The prevailing question for markets is whether this is a isolated adjustment or the beginning of a new tightening cycle.

Current market consensus suggests this won’t be a one-off event. Many analysts are pricing in at least one or two more quarter-point increases before the end of the year, which could bring the deposit rate up to 2.50% or 2.75%. However, ECB leadership has emphasized that future decisions will remain strictly “data-dependent.” The Governing Council will evaluate the ongoing impact of energy prices, geopolitical stability, and wage growth on a meeting-by-meeting basis.

The takeaway is clear: the ECB’s latest pivot highlights how rapidly external shocks can upend economic stability, forcing central banks to prioritize fighting inflation over stimulating growth.

If you’ve been keeping an eye on the economic headlines lately, you might have braced yourself for a sluggish jobs report this May. With rising inflation and the economic ripple effects of the ongoing conflict in Iran, many analysts were predicting a significant cooldown in hiring.

But the U.S. labor market just threw a massive curveball.

Here is a breakdown of the May 2026 jobs report, what the numbers actually mean, and why the American economy continues to show surprising resilience.

The Headline Numbers: Blowing Past Estimates

Economists were largely projecting a modest gain of around 85,000 jobs for May. Instead, the Labor Department revealed that U.S. employers added a robust 172,000 new jobs.

Total Jobs Added: 172,000 (vs. 85,000 expected)

Unemployment Rate: Held steady at 4.3%

Wage Growth: Average hourly earnings ticked up by 0.3% month-over-month.

April Revisions: April’s numbers were also sharply revised upward from 115,000 to an impressive 179,000.

This wasn’t just a slight beat; it was a doubling of expectations, indicating that businesses are still finding reasons to hire and expand, even in an uncertain macroeconomic climate.

Where Are the Jobs Coming From?

While the headline number is strong, the growth wasn’t entirely uniform across the board. The heavy lifting was done by a few key sectors:

Healthcare and Social Services: Continuing a long-running trend, healthcare remains a massive engine for job creation, accounting for a significant chunk of the new roles.

Leisure and Hospitality: As the weather warms up, consumer demand for travel and dining out remains steady, prompting strong hiring in this sector.

Local Government: Public sector hiring also saw notable gains.

Conversely, some sectors felt the pinch. Employment in financial activities slipped slightly, reflecting tighter borrowing conditions and shifting corporate strategies.

Resilience Amid Global Headwinds

The most fascinating takeaway from this report isn’t just the sheer number of jobs added—it’s the context in which they were created.

Since the escalation of the war in Iran earlier this year, global energy markets have been incredibly volatile. Spiking oil prices have renewed fears of inflation, putting pressure on consumer wallets and business operational costs alike. Despite these immense headwinds, the domestic labor market has absorbed the shock remarkably well.

The fact that employers are still confident enough to add 172,000 workers to their payrolls suggests an underlying structural strength in the U.S. economy that is, for now, overriding geopolitical anxieties.

What This Means for the Federal Reserve

Of course, a hot jobs report complicates things for the Federal Reserve.

When the labor market is strong and wage growth is steady, inflation tends to remain sticky. Prior to this report, there was speculation that the Fed might keep interest rates flat for the rest of the year. However, this display of economic resilience might push policymakers in a more hawkish direction. While the steady 4.3% unemployment rate means the labor market isn’t overheating, markets are now bracing for the possibility that the Fed could lift rates at least once by the end of 2026 to keep inflationary pressures in check.

The Bottom Line

The May 2026 jobs report is a potent reminder that the U.S. economy rarely behaves exactly as modeled. While the challenges of inflation and global conflict are very real, the underlying demand for labor remains undeniably robust. Whether this momentum can be sustained into the summer remains to be seen, but for now, the job market continues to defy the odds.

If your last trip to the gas station felt like a hit to your wallet, you aren’t alone. The latest Consumer Price Index (CPI) report is out, and the numbers confirm what we’ve all been feeling: U.S. inflation jumped to 3.8% in April, up from 3.3% in March.

This represents the highest inflation rate since 2023, and it marks a significant detour from the “path to 2%” that the Federal Reserve has been aiming for. While price increases have cooled in some sectors, the energy market is currently the primary engine driving these numbers higher.

Gasoline: The Primary Culprit

The standout figure in April’s report is the cost of energy. National average gas prices have surged to approximately $4.50 per gallon, a staggering jump from the sub-$3.00 levels seen just a few months ago in February.

This spike isn’t just a random market fluctuation. It is being driven heavily by geopolitical instability, specifically the ongoing conflict with Iran. The closure of the Strait of Hormuz—a vital artery for global oil supply—has sent shockwaves through the market. When a fifth of the world’s oil supply is threatened, the impact is immediate and felt directly at the local pump.

The “Trickle-Down” of High Energy Costs

High gas prices do more than just make commuting more expensive. They create a “cost-of-living” domino effect:

Transportation & Logistics: Shipping companies and airlines are facing massive fuel surcharges, which eventually get passed down to the consumer.

Food Prices: Agriculture and grocery distribution are energy-intensive. As diesel and gas prices rise, expect your grocery bill to remain stubbornly high.

Manufacturing: Factories that rely on heavy energy consumption are seeing their margins squeezed, leading to higher prices for finished goods.

What This Means for Interest Rates

For months, the big question in the financial world has been: When will the Fed cut interest rates?

This 3.8% reading makes that answer much more complicated. Outgoing Fed Chair Jerome Powell and incoming Chair Kevin Warsh are facing a “higher-for-longer” reality. Typically, the Fed raises interest rates to cool a hot economy and lower inflation. With inflation trending upward again, the prospect of rate cuts in 2026 is fading, and some economists are even whispering about the possibility of another hike if the energy crisis doesn’t stabilize.

The Bottom Line

The April inflation report is a sobering reminder of how interconnected our local economy is with global events. While the U.S. economy remains resilient in many areas, the “gasoline tax” created by geopolitical tension is a heavy burden for the average household.

For now, the focus remains on the Middle East. Until energy supply stabilizes, the Fed—and our bank accounts—will likely be in a defensive crouch.

What are you doing to offset rising costs? Are you changing your summer travel plans or looking into more fuel-efficient alternatives? Let us know in the comments below.

Mortgage Rates – The housing market has seen a welcome shift! Mortgage rates have fallen below 6% for the first time since 2022, offering a significant improvement for potential homebuyers. This news comes as a breath of fresh air after a period of steadily climbing rates that have put a strain on many budgets.

What Does This Mean for Potential Homebuyers?

The drop in mortgage rates translates directly into increased affordability for those looking to purchase a home. This can be beneficial in several ways:

Lower Monthly Payments: A lower interest rate means a smaller portion of your monthly payment goes towards interest, reducing your overall housing cost.

Increased Buying Power: With lower monthly payments, you may be able to qualify for a larger loan amount, potentially allowing you to purchase a more expensive home.

Refinancing Opportunities: Existing homeowners who currently have a higher mortgage rate may be able to refinance their loan and save money on their monthly payments.

Why Are Mortgage Rates Falling?

While the exact reasons behind the rate drop are complex, several factors may be contributing to the trend:

Lower Inflation: Inflation has shown signs of cooling down, which can influence interest rates.

Economic Growth: While economic growth has been moderate, some signs suggest it may be slowing, which can also affect mortgage rates.

Changes in the Bond Market: Bond yields, which are closely tied to mortgage rates, have also seen a decline.

What Should You Do Now?

If you’ve been on the fence about buying a home, this could be an excellent time to re-evaluate your options. Here are some steps to consider:

Get Pre-Approved for a Mortgage: This will give you a clear idea of how much you can borrow and help you understand your monthly payment.

Shop Around for Rates: Different lenders offer varying rates, so it’s essential to compare offers from multiple institutions.

Consider Your Long-Term Goals: While the lower rates are attractive, it’s crucial to ensure that buying a home is the right decision for your long-term financial goals.

Important Note: It’s important to remember that mortgage rates are subject to change based on economic conditions and other factors. While the current trend is encouraging, it’s essential to stay informed about any potential shifts in the market.

Conclusion:

The drop in mortgage rates below 6% is a significant development for the housing market, offering some much-needed relief to potential homebuyers and homeowners alike. If you’ve been considering buying a home, this could be the right time to take action. With lower monthly payments and increased buying power, you may be closer to achieving your homeownership goals than you thought. However, it’s crucial to act carefully and seek professional advice to make the best decision for your individual situation.

Primary Data Sources

Freddie Mac (Primary Mortgage Market Survey): The ultimate source for the 5.98% figure. Freddie Mac released its weekly report on February 26, 2026, confirming that the 30-year fixed-rate mortgage dipped below 6% for the first time in approximately 3.5 years.

The Federal Reserve (FRED): Used to verify historical trends, specifically confirming that the last time rates were at this level was September 8, 2022 (when they were 5.89%).

CBS News: Provided context on the White House’s initiatives (such as the $200 billion mortgage bond purchase plan) and expert commentary on the “spring home-buying season.”

Associated Press (AP): Detailed the influence of the 10-year Treasury yield on mortgage pricing and quoted housing economists regarding market entry for buyers and sellers.

Mortgage rates in 2026 forecast This video provides expert analysis on how these sub-6% rates impact monthly affordability and what to expect for the rest of the 2026 housing market

The latest economic data brings a sigh of relief for consumers and policymakers alike, as U.S. inflation has shown a more significant easing than anticipated at the beginning of the year. This positive development suggests that efforts to tame rising prices may be gaining traction, offering a glimmer of hope for greater economic stability in the months to come.

For much of the past year, inflation has been a persistent headwind, impacting everything from grocery bills to housing costs. The robust labor market, while a sign of economic strength, also contributed to upward price pressures. However, recent reports indicate a potential shift in this trend.

Several factors appear to be contributing to this welcome slowdown. Supply chain disruptions, which were a major catalyst for price increases, have largely improved. This has allowed for a more consistent flow of goods, reducing bottlenecks and associated costs. Additionally, the Federal Reserve’s aggressive monetary policy, including multiple interest rate hikes, seems to be having its intended effect of cooling demand and reining in inflationary expectations.

While the easing of inflation is certainly good news, it’s important to maintain a balanced perspective. The economy is a complex system, and various forces are constantly at play. Energy prices, geopolitical events, and shifts in consumer spending habits can all influence the trajectory of inflation. Therefore, continuous monitoring and adaptive policymaking will remain crucial.

What does this mean for the average American? For starters, it could translate into less pressure on household budgets over time. If the trend continues, we might see more stable prices for everyday goods and services, allowing purchasing power to stretch further. It also provides the Federal Reserve with more flexibility in its future policy decisions, potentially reducing the need for further aggressive rate hikes.

The journey to sustained price stability is an ongoing one, but the early signs from this year are undoubtedly encouraging. It’s a testament to the resilience of the U.S. economy and the effectiveness of concerted efforts to address inflationary pressures. As we move further into the year, economists and consumers alike will be watching closely to see if this promising trend continues, paving the way for a more predictable and stable economic environment.

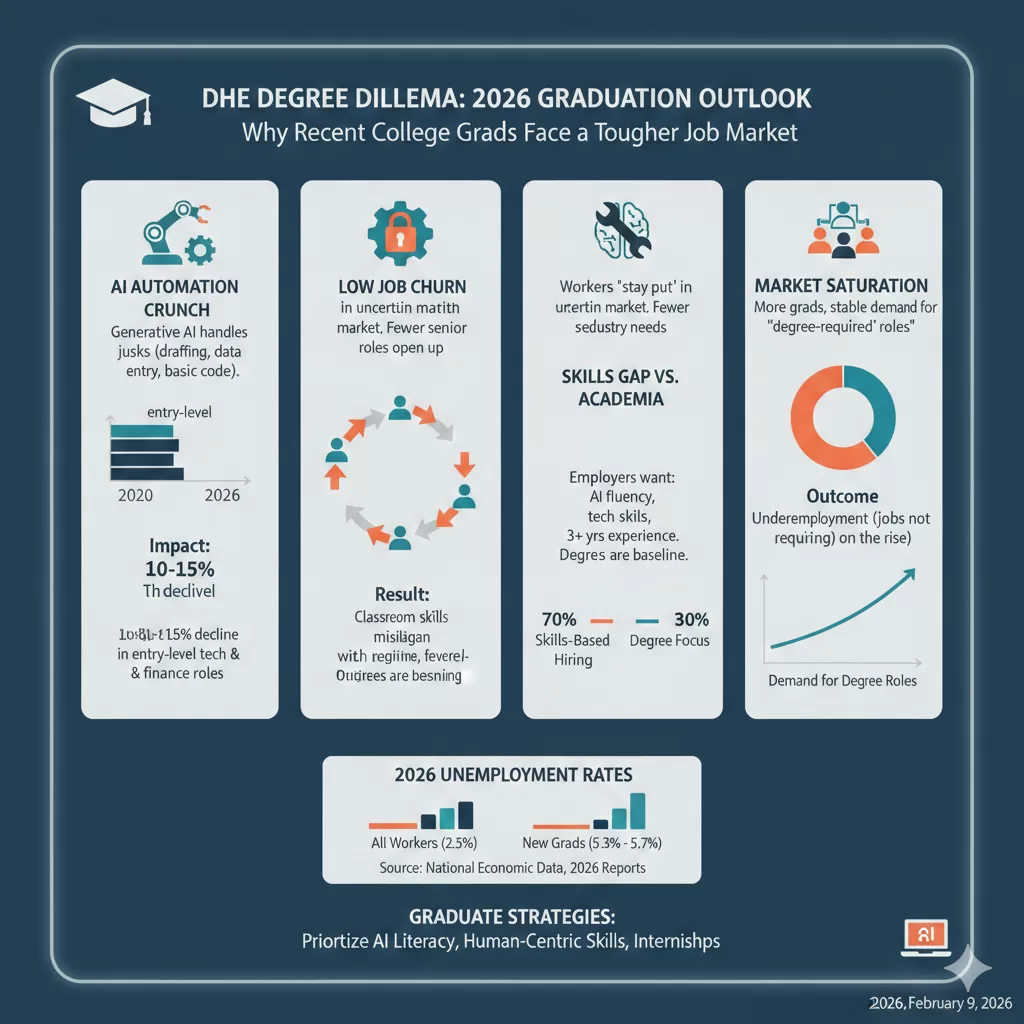

For decades, the path to employment followed a predictable script: graduate high school, earn a four-year degree, and step into a stable career. But for the Class of 2026 and other recent grads, that script has been heavily revised.

While the national unemployment rate remains relatively stable, a closer look reveals a “white-collar friction” that is hitting young graduates particularly hard. Recent data suggests that unemployment for workers aged 22–27 is significantly higher than for the general population, with some reports showing rates as high as 5.3% to 5.7% for new degree holders compared to just 2.5% for their more experienced counterparts.

Why is the “college advantage” seemingly cooling off? Here are the primary factors reshaping the entry-level landscape.

1. The “Bottom Rung” is Being Automated

Perhaps the most significant shift in 2026 is the impact of Generative AI. Historically, junior roles involved “intellectually mundane” tasks: drafting reports, organizing data, or basic coding. These were the “training wheels” of a career.

Today, AI agents handle these tasks with 90% accuracy in seconds.

The Result: Companies are becoming more “top-heavy.” They still need experienced managers to oversee AI, but they need fewer junior employees to do the legwork.

The Crunch: Entry-level hiring has seen double-digit declines in sectors like tech and finance, as firms use AI to boost productivity without expanding their headcount.

2. The Great “Stay Put” (Low Churn)

In a healthy economy, people switch jobs, creating “openings” at the bottom for new talent. In 2026, we are seeing a collapse in voluntary job switching.

“Workers are holding onto their roles because the market feels risky; as a result, the natural ‘churn’ that usually pulls recent grads into the workforce has stalled.”

When mid-level employees don’t move up or out, the entry-level pipeline remains clogged.

3. The Rising “Skills Gap” vs. Academic Focus

There is a growing disconnect between what is taught in the classroom and what is required in a modern office.

The Degree is the Baseline, Not the Finish Line: Employers are shifting toward skills-based hiring. According to NACE, 70% of employers now prioritize specific technical skills and AI fluency over the prestige of the degree itself.

Experience Over Everything: Job postings that once asked for 0–2 years of experience are increasingly demanding 3+ years or specific internships. For a recent grad, this creates the classic paradox: You can’t get the job without experience, but you can’t get experience without the job.

4. Market Saturation

We are currently seeing the result of “education-neutral” growth. The supply of college graduates has increased steadily, but demand for roles that specifically require a degree has leveled off. This has led to a rise in underemployment, where graduates find themselves in roles that don’t actually require their hard-earned credentials.

What Can Grads Do?

The market is tougher, but it isn’t closed. To stand out in the current environment, graduates must:

Prioritize AI Literacy: It’s no longer a “plus”; it’s a requirement. Show how you use AI to work faster and smarter.

Focus on “Human-Centric” Skills: Emphasize critical thinking, complex problem solving, and emotional intelligence—things AI still struggles to replicate.

Treat Internships as Essential: In 2026, an internship is often the only way to bypass the “3 years of experience” requirement.

The Inflation “Split Screen”: What December’s CPI Numbers Really Mean

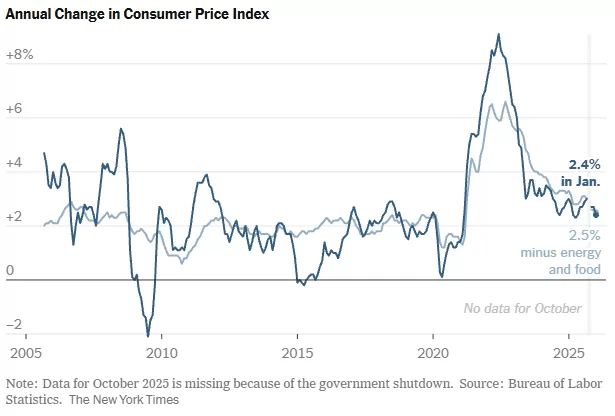

Inflation Stable. The latest data is in, and it paints a picture of an economy caught between cooling pressures and political friction. In December, consumer prices rose 2.7% from a year earlier—holding steady from November and landing exactly where economists predicted.

While the “headline” number suggests stability, the story beneath the surface is much more complex. Here are the key takeaways from the final inflation report of 2025.

1. Stability Amidst the Noise

For the second month in a row, inflation has leveled off at 2.7%. Meanwhile, “Core CPI” (which strips out volatile food and energy costs) rose 2.6%.

Interestingly, these numbers came in slightly better than the 2.8% core increase some experts feared. This suggests that despite the introduction of steep tariffs earlier in 2025, businesses haven’t yet passed the full weight of those costs onto consumers. However, the “last mile” of the journey back to the Fed’s 2% target remains stubbornly out of reach.

2. A Cloud of Data Uncertainty

This report is the first “clean” look at inflation we’ve had in months. Following a government shutdown last fall, the Labor Department had to rely on technical workarounds to fill data gaps.

The “Payback” Effect: Many economists believe November’s figures may have been artificially low due to those data collection issues.

The Verdict: While December’s numbers didn’t spike as much as feared, they likely reflect a correction for the missing data from previous months.

3. The Fed’s High-Stakes Balancing Act

The Federal Reserve is currently navigating a “split screen” economy. On one hand, growth remains solid; on the other, the labor market has cooled significantly. In fact, 2025 saw the lowest pace of job growth since 2003 (excluding major recessions).

The Fed cut rates three times at the end of 2025 to support the job market, but officials are now divided. With inflation still above 2%, some are hesitant to keep cutting—especially as they watch for the inflationary impact of the One Big Beautiful Bill Act and ongoing investments in AI.

4. Politics vs. Policy

Perhaps the most unusual backdrop to this report is the unprecedented political pressure on independent agencies.

The Labor Department: Its commissioner was fired in August amidst claims of “rigged” numbers.

The Fed: Chair Jerome Powell recently alleged that the administration has used threats of criminal prosecution to pressure the board into lowering interest rates.

What’s Next?

As we head into 2026, all eyes are on January and February. This is traditionally when businesses reset their pricing for the year. Whether they will hike prices to account for tariffs and tax-cut-driven demand remains the big question.

For now, the “meandering path” toward lower inflation continues, but with a cooling job market and political volatility, the road ahead looks anything but smooth.

Let’s explore the potential trends in its Gross Domestic Product (GDP) growth rate throughout 2025. While no one has a crystal ball, we can analyze current trajectories, expert projections, and potential influencing factors to paint a picture of what lies ahead.

The Current Economic Pulse (Briefly looking back at late 2024)

To understand 2025, it’s crucial to acknowledge the economic momentum (or lack thereof) leading into it. We’re likely seeing a continued moderation from the robust growth experienced in the immediate post-pandemic recovery. Inflation, while hopefully tamer, will still be a key variable, influencing consumer spending and investment. Interest rates, dictated by the Federal Reserve, will also play a significant role. Let’s imagine a snapshot of the US economy as we enter 2025.

Q1 2025: A Cautious Start?

As 2025 kicks off, many economists anticipate a period of continued cautious growth. Businesses may still be adjusting to lingering supply chain complexities and a potentially tighter labor market. Consumer spending, the bedrock of the US economy, might see moderate gains, influenced by real wage growth (or lack thereof) and household savings levels. Investment in new projects could be selective, driven by a desire for efficiency and technological advancement. We might see the GDP growth rate hover in the lower to mid-2% range during this initial quarter.

Q2 2025: Finding its Rhythm

Moving into the second quarter, we could witness the economy starting to find a more stable rhythm. Factors such as potentially easing inflationary pressures and a clearer outlook on monetary policy could provide more certainty for businesses and consumers. We might see a slight uptick in manufacturing activity and continued strength in the services sector. Technological innovation, particularly in areas like AI and green energy, could begin to show more tangible contributions to productivity.

Q3 2025: Potential for Acceleration

The third quarter often provides a good indicator of annual performance, and 2025 could see some positive momentum building. If global economic conditions stabilize and major geopolitical tensions remain subdued, US exports could see a boost. Domestically, renewed consumer confidence, perhaps fueled by a strong job market and stable prices, could lead to increased discretionary spending. Business investment might also pick up as companies look to capitalize on growth opportunities. This could be a quarter where GDP growth nudges closer to the mid-2% to even 3% range. Imagine the vibrancy of a thriving economy in full swing.

Q4 2025: A Strong Finish or Continued Moderation?

The final quarter of 2025 will be crucial in determining the overall annual growth rate. Much will depend on the preceding quarters’ performance and any new unforeseen global or domestic events. A strong holiday shopping season, robust corporate earnings, and continued investment in key sectors could lead to a solid finish. However, potential headwinds like persistent inflation or unexpected global economic slowdowns could temper growth. The Federal Reserve’s stance on interest rates will also be keenly watched. The year could conclude with growth stabilizing, setting the stage for 2026.

Key Influencing Factors for 2025:

Inflation and Interest Rates: The Fed’s ability to manage inflation without stifling growth will be paramount.

Consumer Spending: The health of the consumer, driven by wages, employment, and savings, is always a critical determinant.

Business Investment: Companies’ willingness to invest in expansion, R&D, and technology will fuel future growth.

Global Economic Health: International trade and geopolitical stability will have a ripple effect on the US economy.

Technological Advancement: Innovations in AI, automation, and green technologies could boost productivity.

In conclusion, 2025 is shaping up to be a year of continued adaptation and potential growth for the US economy. While we can anticipate some fluctuations, a path of cautious yet steady expansion seems to be the prevailing view among many analysts. The resilience and dynamism of the American economy will undoubtedly be tested, but its capacity for innovation and recovery remains a powerful force.

Federal Reserve Monetary Policy and Leadership Outlook

Executive Summary

The Federal Reserve has implemented its second consecutive monthly interest rate cut, lowering the target range by a quarter-point to 3.75%-4.0%. The 10-2 vote by the Federal Open Market Committee (FOMC) highlights internal division among policymakers regarding the path of monetary policy, a decision made amidst sustained pressure from President Donald Trump for more aggressive easing. The outlook for future cuts remains uncertain, complicated by an ongoing federal government shutdown that has postponed the release of critical economic data on inflation and unemployment. Despite this data blackout, investor sentiment currently favors another quarter-point reduction in December, supported by recent private-sector reports indicating a “softening” labor market. Concurrently, the administration is actively considering a successor for Fed Chair Jerome Powell, whose term expires in May 2026, with a list of five candidates being prepared for the President’s review.

——————————————————————————–

I. October 2025 Interest Rate Decision

The Federal Open Market Committee (FOMC) voted on Wednesday, October 29, 2025, to lower its benchmark interest rate, marking the second straight month of monetary easing.

Rate Adjustment: The committee approved a quarter-point reduction.

New Target Range: The interest rate is now set to a range between 3.75% and 4.0%.

Previous Target Range: This is down from the 4.0% to 4.25% range established at the previous month’s meeting.

Committee Vote: The decision passed with a 10-2 vote, indicating some dissent among policymakers regarding the move.

II. Influencing Factors and Economic Context

The Fed’s decision-making process is being influenced by a combination of political pressure, economic data limitations, and emerging concerns about the labor market.

A. Political Pressure

The rate cut follows months of public pressure and criticism from President Donald Trump.

The President has been advocating for steeper and more aggressive cuts to monetary policy.

B. Economic Data Blackout

An ongoing federal government shutdown has significantly hampered the Fed’s ability to assess the U.S. economy’s health.

Key economic reports, including those on inflation and unemployment, have been postponed.

Fed Governor Christopher Waller acknowledged the challenge, stating that because policymakers “don’t know which way the data will break on this conflict,” the FOMC must “move with care” when adjusting rates.

In the absence of official data, Waller noted he has spoken with “business contacts” to help form his economic outlook.

C. Labor Market Concerns

Fed Governor Christopher Waller indicated his focus has shifted from inflation to a “softening” labor market, a stance that supported his vote for the recent rate cut.

This view is corroborated by reports from several firms and economists released in recent weeks, which suggest the labor market has continued to deteriorate. This emerging private-sector data could provide the FOMC with a rationale for an additional rate cut.

III. Future Monetary Policy Outlook

Market expectations are leaning towards further easing, though Fed officials have previously expressed division on the matter.

Investor Expectations: According to CME’s FedWatch tool, investors are favoring an additional quarter-point interest rate reduction at the FOMC’s final 2025 meeting in December.

Potential December Rate: Such a cut would lower the target range to between 3.5% and 3.75%.

Official Division: Minutes from the previous month’s meeting showed that Fed officials were divided on whether a third rate cut in the year would be necessary.

IV. Federal Reserve Leadership Transition

The administration is actively planning for the future leadership of the central bank as the end of Chair Jerome Powell’s term approaches.

Chair’s Term: Jerome Powell’s term as Federal Reserve Chair is set to expire in May 2026.

Succession Plan: Treasury Secretary Scott Bessent confirmed on Monday that a list of candidates to succeed Powell would be presented to President Trump shortly after Thanksgiving.

Candidate Shortlist: Bessent identified five individuals currently under consideration for the role:

Four Cracks in the Foundation: What the Fed’s Rate Cut Really Reveals

Introduction: Beyond the Headlines

The Federal Reserve has cut interest rates for the second straight month, a headline that suggests a confident response to evolving economic conditions. But simmering beneath the surface are the persistent calls for even easier monetary policy from the White House, adding a layer of political drama to an already difficult decision.

A closer look reveals that this rate cut is not a confident step forward; it’s a hesitant move by a divided committee flying blind in a political storm. The real story isn’t the cut itself, but the four converging pressures that expose a deeper crisis of confidence inside our nation’s central bank. But what’s really happening behind those closed doors?

This analysis breaks down the four most impactful and surprising takeaways from the Federal Reserve’s latest move, revealing a clearer picture of the profound challenges shaping U.S. economic policy today and the volatility that may lie ahead.

1. The Fed is Divided: This Was Not a Unanimous Decision

The Federal Open Market Committee (FOMC) voted to lower its key interest rate by a quarter-point, setting the new range between 3.75% and 4%, down from the previous 4% to 4.25%. The critical detail, however, was the 10-2 vote. This rare public dissent reveals deep fractures in the FOMC’s consensus about the path forward.

For markets and businesses, a divided Fed is an unpredictable Fed. This lack of consensus makes it significantly harder to forecast future policy, injecting a fresh dose of potential volatility into the economy. This internal disagreement is hardly surprising, given that policymakers are being forced to navigate without their most trusted instruments.

2. Flying Blind: The Fed is Making Decisions Without Key Data

Compounding the internal division is a startling “data blackout.” An ongoing federal government shutdown has postponed the release of official reports on inflation and unemployment—the two most vital metrics the central bank relies on. This data vacuum forces the Fed to make billion-dollar decisions in a veritable fog.

Policymakers are left to rely on alternative, anecdotal evidence. Fed Governor Christopher Waller noted he has been speaking with “business contacts” to form his economic outlook. While necessary, this reliance on informal data is fraught with risk. It lacks statistical rigor, is potentially biased, and dramatically increases the danger of a policy misstep. As Governor Waller himself acknowledged, this precarious situation demands extreme caution.

…because policymakers “don’t know which way the data will break on this conflict,” the FOMC would “need to move with care” when adjusting interest rates.

3. The Focus is Shifting: A “Softening” Labor Market is the New Top Concern

For months, inflation has been the Fed’s primary dragon to slay. Now, a monumental shift is underway. Fed Governor Christopher Waller recently stated his focus has pivoted from inflation to the “softening” labor market.

The significance of this pivot cannot be overstated. It signals that the Fed’s tolerance for inflation may be increasing if the alternative is rising unemployment. This represents a critical change in the central bank’s risk assessment, prioritizing job preservation over absolute price stability for the first time in this cycle. With recent reports from private firms suggesting the labor market has continued to deteriorate, the committee may find the justification it needs for another cut in December.

4. Political Pressure and a Looming Leadership Change

The Fed’s internal challenges are amplified by significant external pressures, most notably from President Donald Trump, who has been publicly demanding “steeper cuts.” This external pressure from the White House further complicates the internal debates, potentially widening the rift between committee members who prioritize preemptive action and those who advocate for patience.

This political context is intensified by an impending leadership transition. Fed Chair Jerome Powell’s term expires in May 2026, and the conversation about his successor has already begun. Treasury Secretary Scott Bessent has confirmed five candidates are under consideration:

Fed Governor Christopher Waller

Fed Governor Michelle Bowman

Former Fed Governor Kevin Warsh

National Economic Council Director Kevin Hassett

BlackRock executive Rick Rieder

Conclusion: Navigating in a Fog

The Federal Reserve’s latest interest rate cut is not a sign of clear sailing but rather a reflection of an institution navigating through a dense fog. Plagued by internal fractures, a critical lack of official economic data, and persistent political pressure, the central bank is operating under an extraordinary degree of uncertainty. This complex reality is far more revealing than the simple headline of another rate cut.

With the economy’s true health obscured by a data blackout, can the divided Fed steer us clear of a downturn, or is more volatility inevitable?

The Fed’s Big Move: What an Interest Rate Cut Means for You and the Economy

Introduction: Demystifying the Fed’s Power

The Federal Reserve is one of the most powerful economic forces in the United States, and its decisions can ripple through the entire country. The purpose of this article is to explain, in plain language, what the Federal Reserve is, why it changes interest rates, and what its most recent decision means for the economy. At the heart of these critical decisions is a small but influential group known as the FOMC.

1. Who Decides? Meet the FOMC

The Federal Open Market Committee (FOMC) is the part of the Federal Reserve that votes on the nation’s monetary policy, including whether to raise or lower interest rates. Their decisions, however, are not always unanimous. The most recent vote, for instance, was 10-2, which shows that there can be differing opinions among the committee members on the best path forward for the economy.

Now that we know who makes the decision, let’s examine the specific action they took.

2. The Main Event: A Quarter-Point Rate Cut

The FOMC recently voted to lower its key interest rate. This marks the second straight month that the central bank has decided to ease its monetary policy.

Here is a clear breakdown of the change:

Previous Rate Range

New Rate Range

4% to 4.25%

3.75% to 4%

This “quarter-point” reduction simply means the rate was lowered by 0.25%. But a small change like this signals a significant shift in the Fed’s thinking, which leads to a crucial question: why did they make this change?

3. The ‘Why’ Behind the Cut: A Softening Economy

The primary reason for the rate cut is that policymakers are concerned about a “softening” labor market.

Fed Governor Christopher Waller highlighted this concern, indicating his focus had shifted to a “softening” labor market instead of inflation. His viewpoint is supported by recent data; reports from various firms and economists suggest that the labor market has “continued to deteriorate,” which could provide the FOMC with the evidence it needs to support an additional cut in the future.

Of course, not everyone agrees on the Fed’s actions or what should happen next.

4. A Contentious Decision: Different Views on the Economy

The Federal Reserve’s decisions are often the subject of intense debate and are made under significant outside pressure. The latest rate cut is no exception, with several competing viewpoints at play.

President Trump’s View: The President has been a vocal critic, applying pressure on the Fed and calling for “steeper cuts” to interest rates.

Internal Division: The 10-2 vote demonstrates a lack of consensus within the FOMC itself. Last month, Fed officials appeared “divided over whether to cut rates for a third time this year,” underscoring this internal disagreement.

A Data Dilemma: The Fed is facing a major challenge due to an “ongoing federal government shutdown,” which has postponed the release of key reports on inflation and unemployment. This data blackout has forced policymakers like Governor Waller to rely on conversations with their “business contacts” to form an outlook on the economy.

These debates and challenges naturally lead to questions about what the Federal Reserve might do in the future.

5. What Happens Next? Reading the Tea Leaves

Based on the current situation, the future path of interest rates remains uncertain, but there are several key things to watch.

Investor Expectations: According to CME’s FedWatch tool, investors are currently “favoring an additional quarter-point reduction” at the FOMC’s next meeting in December.

The Fed’s Caution: Governor Christopher Waller emphasized the need for prudence, stating that because policymakers “don’t know which way the data will break,” the FOMC would “need to move with care” when adjusting interest rates.

Leadership Questions: President Trump is expected to name his pick to succeed Fed Chair Jerome Powell, whose term expires in May 2026. The candidates under consideration include Fed governors Christopher Waller and Michelle Bowman, former Fed governor Kevin Warsh, National Economic Council Director Kevin Hassett, and BlackRock executive Rick Rieder.

These factors will shape the economic landscape in the months to come.

Conclusion: Your Key Takeaways

To wrap up, understanding the Federal Reserve doesn’t have to be complicated. Here are the most important lessons from their recent decision.

The Federal Reserve, through its FOMC, manages the economy by adjusting interest rates to respond to issues like a weakening labor market.

Lowering interest rates is a tool to encourage economic activity, but decisions on when and how much to cut are complex and often debated.

The Fed’s actions are influenced by economic data, political pressure, and differing expert opinions, making their future moves something that everyone, from investors to the general public, watches closely.