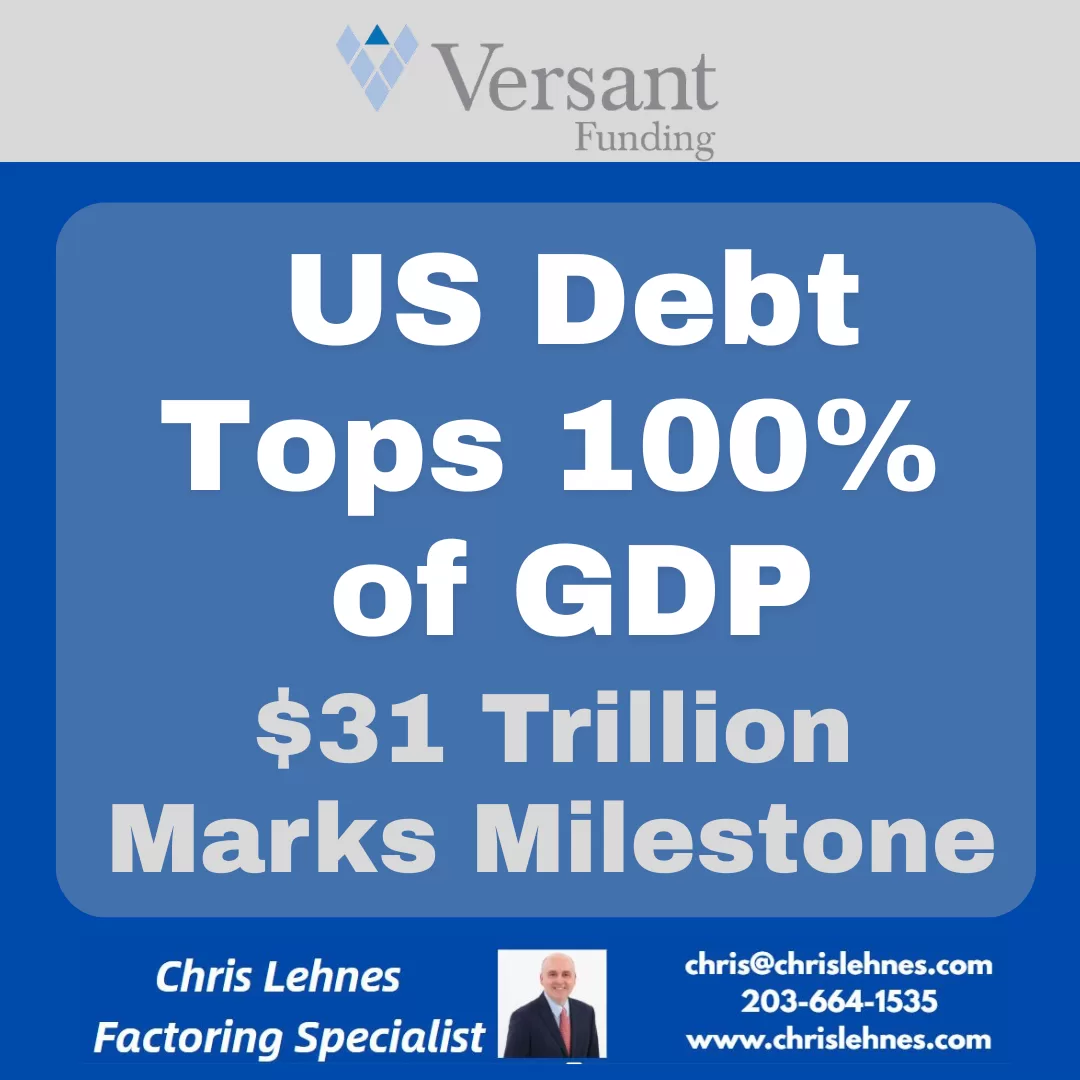

For the first time since the aftermath of World War II, the United States has reached a fiscal milestone that was once a distant “what-if” scenario: the national debt has officially surpassed 100% of the country’s Gross Domestic Product (GDP).

As of March 31, 2026, the debt held by the public reached $31.27 trillion, while the total annual economic output sat at $31.22 trillion. In simple terms, we now owe more as a nation than we produce in an entire year.

While “trillions” can feel like abstract Monopoly money, this 100.2% ratio represents a fundamental shift in the American economic landscape. Here is what you need to know about why this happened and what it means for the future.

How Did We Get Here?

This wasn’t an overnight accident. It is the result of decades of “fiscal kicking the can.” The surge to 100% was fueled by three primary engines:

Structural Deficits: For years, the government has spent roughly $1.33 for every $1.00 it collects in revenue.

The Interest Trap: As the total debt grows, so do the interest payments. In 2026, the U.S. is projected to spend approximately $1 trillion on interest alone—surpassing the entire national defense budget.

Demographic Shifts: An aging population is naturally drawing more heavily on Social Security and Medicare, programs that make up a massive portion of mandatory spending.

Why the 100% Threshold Matters

Economists often debate whether there is a “magic number” where debt becomes fatal. While 100% isn’t an immediate “cliff,” it serves as a critical psychological and economic warning light for several reasons:

Slower Economic Growth: Historical data suggests that when a nation’s debt exceeds 90% of GDP, average annual growth tends to slow. Resources that could be used for private investment or infrastructure are instead diverted to servicing old debt.

Reduced “Crisis Cushion”: When the next pandemic, recession, or war hits, the government has less “dry powder” to respond. Borrowing your way out of a crisis is much harder when your credit card is already maxed out relative to your income.

Generational Equity: The debt essentially represents a “tax” on future generations. Today’s spending is being financed by the earnings of Americans who haven’t even entered the workforce yet.

The Cost to the Average Household

To bring these massive numbers down to earth, the Senate Joint Economic Committee’s April 2026 update provides a sobering breakdown:

Debt per Person: Approximately $114,000

Debt per Household: Approximately $289,000

Is There a Way Out?

The U.S. has been here before. After 1945, the debt-to-GDP ratio was successfully whittled down to 34% by 1980. However, that was achieved through a unique combination of post-war industrial dominance, a massive “Baby Boom” workforce, and rapid GDP growth.

Today, the path is narrower. Solutions generally fall into three difficult categories:

Entitlement Reform: Adjusting Social Security and Medicare to match modern life expectancies.

Revenue Increases: Raising taxes or closing loopholes to narrow the deficit.

Growth Incentives: Policies designed to make the “GDP” side of the ratio grow faster than the “Debt” side.

The Bottom Line

Crossing the 100% threshold is a “reckoning” moment. It signals that the era of “cheap” borrowing is over. As interest payments continue to eat a larger slice of the federal pie, the pressure on the American taxpayer—and the pressure to make hard political choices—will only intensify.

The red line has been crossed. The question now is whether we have the political will to head back toward the black.

We continue to assist companies nationwide in converting IEEPA tariff refund claims into immediate cash, even after the launch of U.S. Customs and Border Protection’s(“CBP”) CAPE refund portal and the latest April 28th update from the U.S. Court of International Trade (“CIT”).

CIT’s April 28th status review confirmed that the lead IEEPA refund litigation has largely moved from the legal entitlement phase into the implementation and payment phase. In simple terms, the question is no longer primarily whether many importers are entitled to refunds, the issue is when those refunds will actually be paid.

While CBP officially launched CAPE on April 20th to process refunds, there was no new court order requiring immediate payment of all claims. Instead, the CIT is supervising execution, while Customs works through claim submissions, liquidation status, eligibility reviews, and administrative processing. This distinction matters. CBP has indicated that certain accepted claims may be paid within approximately 45–60 days plus statutory interest.

However, “acceptance” is not the same as submission. Importers must first complete filing requirements, resolve broker authority issues, verify liquidation status, satisfy procedural review, and clear compliance review before the payment clock truly begins. For many importers, especially those with older entries, previously liquidated claims, multiple brokers, documentation issues, or claims that may fall outside CAPE Phase 1, the actual recovery timeline could extend for many months or significantly longer. As a result, our buyers remain highly active in purchasing IEEPA tariff refund claims, with transactions from $250,000 to $7 million purchased at a Buy Rate of 85%, while claims exceeding $7 million have a Buy Rate of 90%.

Why Importers are still Selling Tariff Refund Claims after CAPE Opened

Judge Eaton of CIT did not order immediate universal payment of all claims. CBP’s estimated payment window begins only after formal claim acceptance, not submission.

Many claims do not clearly qualify for CAPE Phase 1 and may require later phases. Finally liquidated entries remain one of the largest unresolved issues. Previously liquidated entries may still require protests, reliquidation, or additional litigation. The right to a refund is clearer—but the timing of payment remains uncertain.

CSV upload issues, ACE access problems, and broker mismatches can delay acceptance. Documentation gaps and reconciliation issues remain common. Customs audit and compliance review may delay payment even after filing.

Trump Administration appeal deadlines and future legal developments could delay the timing of refund payments. Processing millions of entries may create substantial administrative backlogs. Port-by-port inconsistencies may slow recovery for certain importers. Working capital needs often cannot wait for government processing timelines/.

Importers Are Choosing To Monetize Now

Immediate working capital for inventory, payroll, and vendor obligations. Reduced lender pressure and improved borrowing base flexibility. Elimination of refund timing risk and litigation uncertainty. Improved balance sheet certainty. Faster access to liquidity without waiting for government disbursement. Stronger buyer pricing now that CAPE implementation is underway as Buy Rates increased from 45% in February to 85% today

For many businesses, immediate liquidity today is worth more than waiting for a larger payment later. Many importers are no longer asking. “Will I get paid?”, They are asking, “Is waiting worth the delay, uncertainty, and operational risk?”. For many companies, the answer is no. We work with importers with claims starting at $250,000, with no maximum limit across industries including food, seasonal goods, apparel, and home products.

Most transactions can be completed in approximately 10 business days, assuming proper documentation and credit quality.

Convert IEEPA Tariff Claims to Cashon an Expedited Basis

I have been actively assisting companies nationwide in converting their IEEPA tariff refund claims into immediate cash.

U.S. Customs and Border Protection is rolling out a centralized system (CAPE) to process refunds, and some trade experts believe that certain importers could begin receiving refunds within the next six months. However, there remains significant uncertainty around timing, and many industry participants believe that a large portion of claims could still take years to fully resolve.

Convert IEEPA Tariff Claims to Cash on an Expedited Basis

This divergence is driven by several factors, including: The complexity and scale of processing millions of entries The possibility that certain categories of claims may be prioritized over others, delaying recovery for more complex or lower-volume importers The need for new administrative procedures, as IEEPA does not clearly define a refund mechanism The potential for case-by-case eligibility determinations

Ongoing legal and procedural developments, including possible appeals by the Trump Administration and implementation challenges

Liquidation Status – Whether entries have already been liquidated, which in many cases may require formal protests or litigation to reopen and recover duties The likelihood of inconsistent treatment across ports (port-by-port) or entry types as CBP implements new processes in phases Documentation gaps and data reconciliation issues, particularly for older entries or those filed across multiple brokers The absence of clear guidance on how interest on refunds will be calculated and paid, which could lead to further disputes

Capacity constraints within CBP and the potential for processing backlogs as refund volumes scale

Continued legal challenges around the scope of eligibility, including disputes over classifications, valuation, or origin that could delay specific claims

As a result, while some importers may receive refunds within six months, others, particularly those with more complex or previously liquidated entries, could face a multi-year recovery timeline. To address this uncertainty, financial institutions and hedge funds are actively purchasing IEEPA tariff refund claims at a discount.

Current buy rates are as high as 85% of the expected refund value, depending on claim size, credit quality of the importer and documentation quality as these claims are not directly assignable. AES works with importers with claims starting at $250,000, with no maximum limit. Since entering this market five months ago, AES has facilitated the monetization of approximately $20 million in claims across industries including food, seasonal goods, apparel, and home products.

Market pricing has evolved significantly: Prior to the February 20, 2026, Supreme Court ruling, claims traded at approximately 20–25% Following the ruling, pricing increased to 40–50% More recently, improving legal clarity and market participation have driven pricing to current levels of up to 85% of the IEEPA tariff refund amount

While some importers initially adopted a “wait and see” approach in anticipation of near-term refunds, the combination of timing uncertainty and significantly improved pricing has led many to explore monetization as a way to eliminate risk and accelerate liquidity. The Funds AES works with are able to complete transactions in approximately 2–3 weeks, depending on the completeness and quality of documentation.

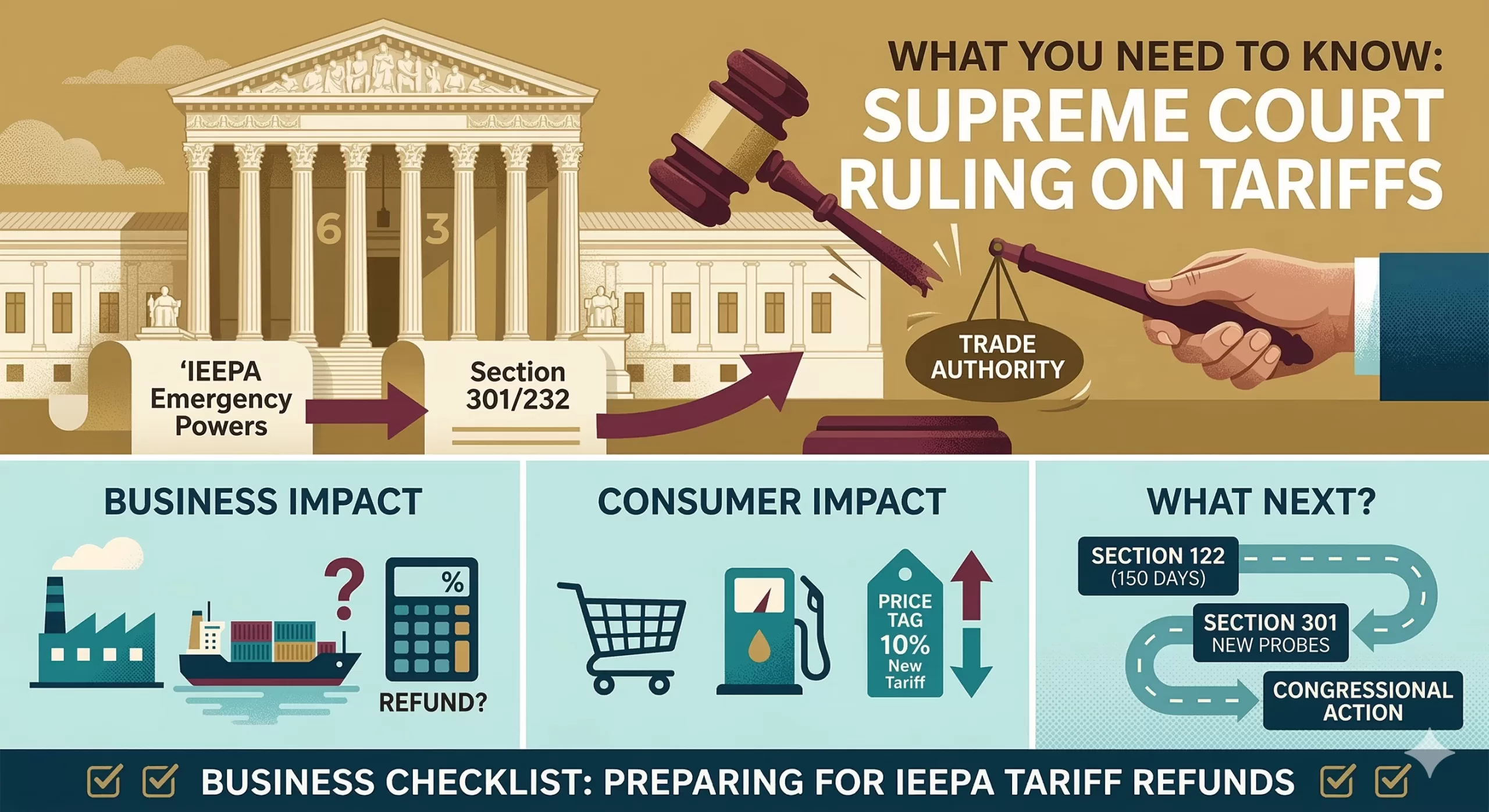

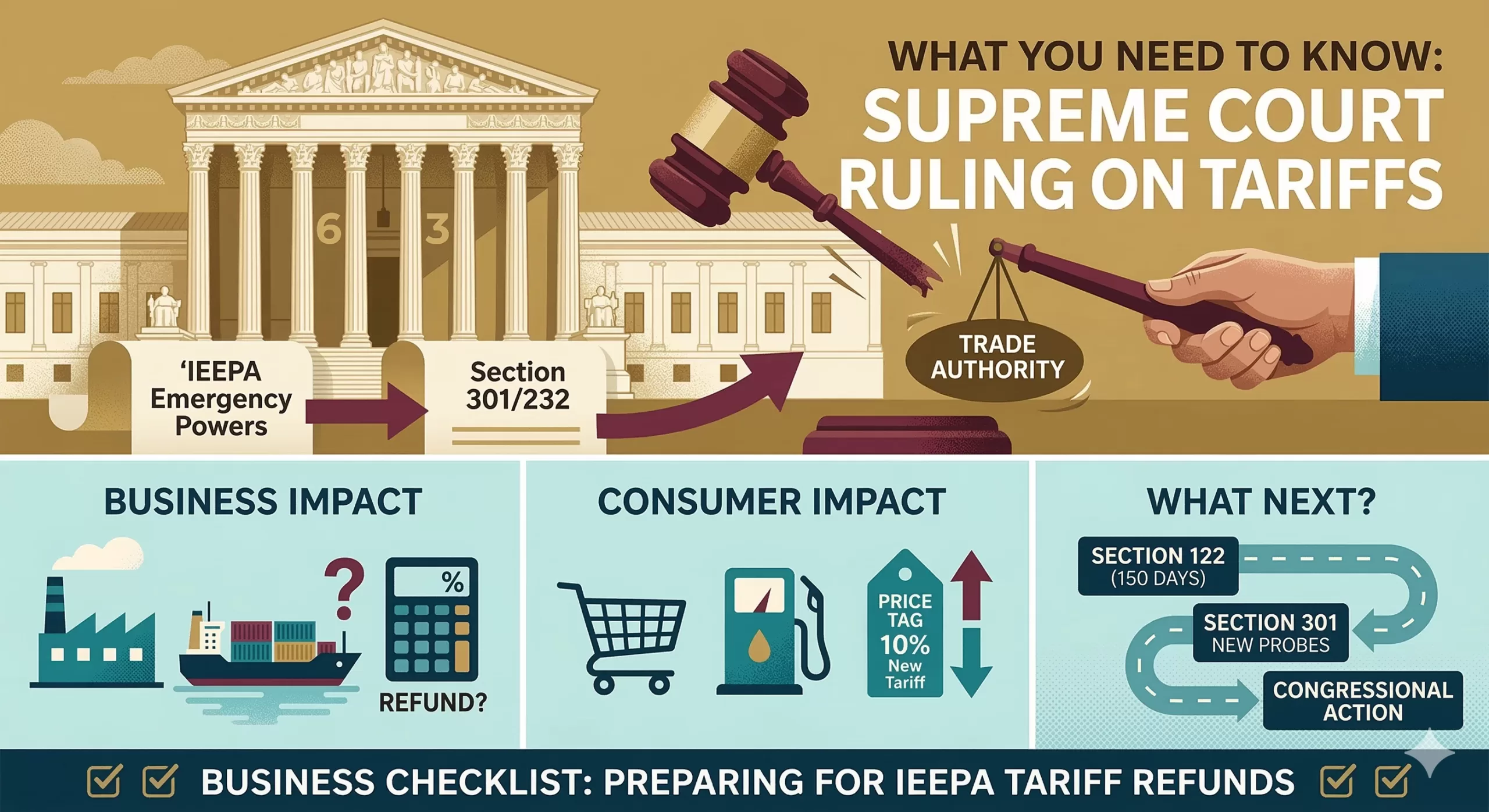

In a landmark decision that has reshaped the landscape of IEEPA Tariffs and American trade policy, the Supreme Court recently issued a ruling in Learning Resources, Inc. v. Trump. The 6-3 decision struck down a series of sweeping tariffs, delivering a significant blow to the administration’s use of emergency powers to regulate the economy.

If you’re a business owner, importer, or simply a consumer wondering why prices are shifting again, here is everything you need to know about this historic ruling about IEEPA Tariffs and what comes next.

The Heart of the Case: IEEPA Tariffs vs. The Taxing Power

The central question before the Court was whether the International Emergency Economic Powers Act (IEEPA) of 1977 gives the President the authority to impose tariffs.

The administration had used IEEPA to levy “reciprocal tariffs” and “trafficking tariffs” on products from China, Canada, and Mexico, arguing that trade imbalances and border security issues constituted a national emergency. However, the Supreme Court ruled that:

Tariffs are Taxes: Chief Justice John Roberts, writing for the majority, emphasized that the power to tax—which includes tariffs—belongs exclusively to Congress under Article I of the Constitution.

“Regulate” is not “Tax”: The Court held that IEEPA’s authority to “regulate importation” does not mean the President can unilaterally set tax rates

The Major Questions Doctrine: The Court applied this principle, stating that if Congress intended to delegate such massive economic power to the Executive Branch, it would have said so clearly and explicitly.

“The Framers did not vest any part of the taxing power in the Executive Branch,” wrote Chief Justice Roberts.

What Happens to the Money? The Refund “Mess”

One of the most pressing questions for businesses is the status of the billions of dollars already collected. Since 2025, the government has gathered an estimated $133 billion to $200 billion in IEEPA-based tariffs.

Court of International Trade (CIT) Action: Following the Supreme Court ruling, the CIT has ordered U.S. Customs and Border Protection (CBP) to begin preparing for a massive refund process.

The “Mess” Factor: Justice Brett Kavanaugh noted in his dissent that issuing these refunds will be a “mess.” It remains unclear exactly how and when businesses will see that money returned, as the Supreme Court did not provide a specific roadmap for the refund process

The Administration’s Pivot: Section 122 and 301

If you thought this ruling meant the end of tariffs, think again. Within hours of the decision, the administration began moving to alternative legal authorities:

Section 122 (Trade Act of 1974): The President implemented a temporary 10% global baseline tariff under this law. However, this power is limited to 150 days and a maximum rate of 15% unless Congress intervenes.

Section 301 Investigations: The U.S. Trade Representative (USTR) has launched new investigations into “structural excess capacity” and “forced labor” in countries like China and Mexico. These could lead to new, more legally “durable” tariffs in the coming months.

Section 232 Still Stands: Tariffs on steel and aluminum, which rely on a different national security statute, were not affected by this specific ruling and remain in place.

What This Means for You

For Businesses and Importers

The immediate relief from IEEPA tariffs is a win, but it is replaced by a new 10% surcharge under Section 122. You should:

Audit your entries: Identify which tariffs you paid were based on IEEPA to prepare for potential refund claims.

Stay Flexible: The trade environment remains volatile as the administration shifts its legal strategy to avoid future Court losses.

For Consumers

While the invalidation of billions in tariffs sounds like a price drop is coming, the introduction of the new 10% global tariff may offset those savings. Economists expect “trade-weighted” average tariff rates to remain higher than historical norms through 2026.

Summary of Key Impacts

Feature

IEEPA Tariffs (Struck Down)

Section 122 Tariffs (New)

Legal Status

Unconstitutional/Invalid

Currently Active

Current Rate

0% (Effective Feb 20, 2026)

10% (Effective Feb 24, 2026)

Duration

N/A

150 Days (Expires July 24, 2026)

Refunds

Likely, but process is TBD

No

The Supreme Court has drawn a firm line in the sand regarding the separation of powers. While the President still has significant tools to influence trade, the era of “unbounded” emergency tariffs appears to be over.

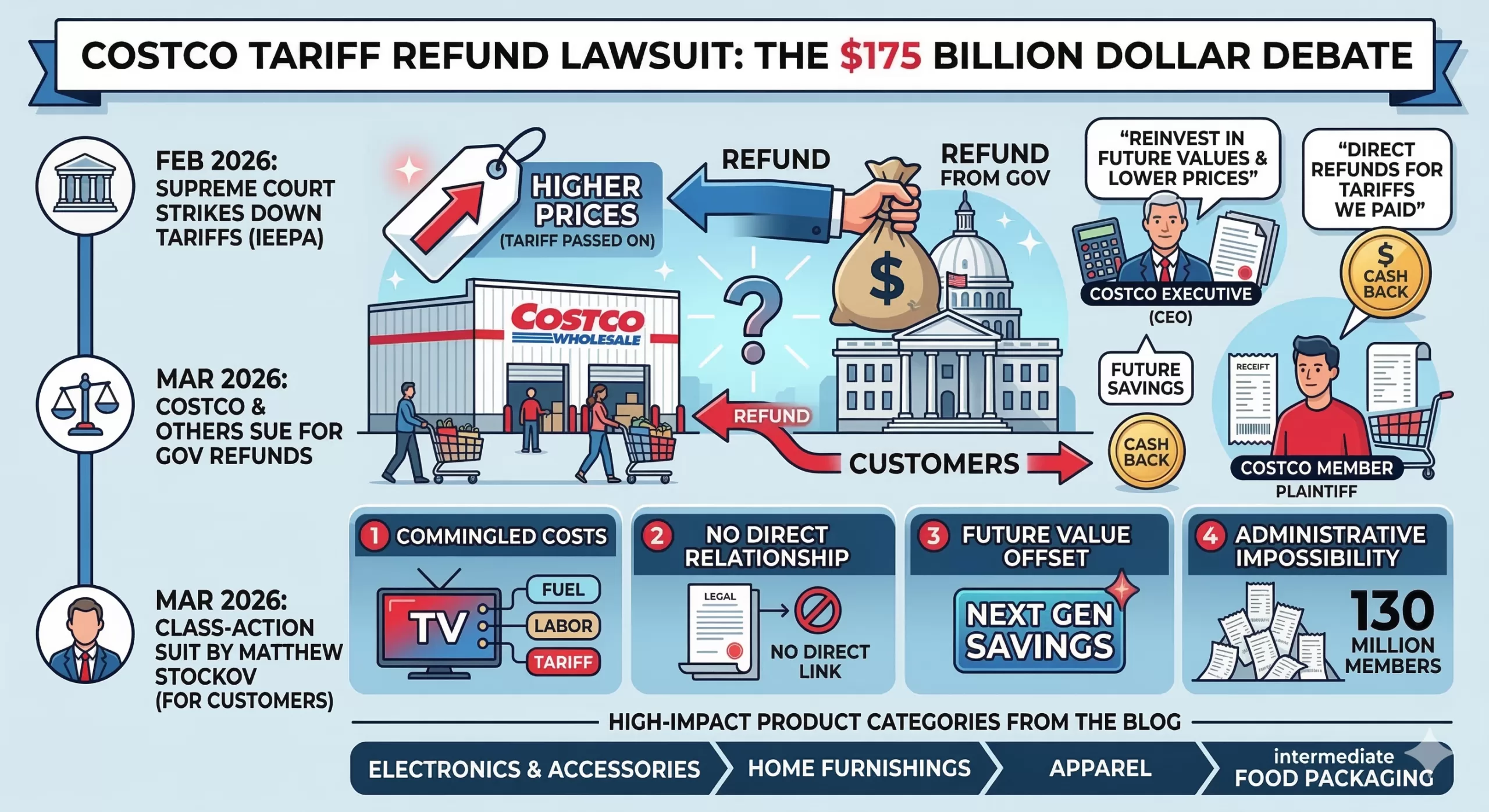

If you’ve noticed your Costco hauls getting a little pricier over the last year due to tariff passthrough, you aren’t alone. But a new legal battle is brewing that asks a multi-billion-dollar question: If a retailer gets a refund for the “illegal” tariff they passed on to you, who actually keeps the cash?

On Wednesday, March 11, 2026, a Costco member in Illinois filed a nationwide class-action lawsuit against the retail giant. The goal? To ensure that any tariff refunds Costco receives from the federal government end up back in the pockets of the shoppers who actually paid for them.

The Backdrop: A Supreme Court Shake-up

The drama started on February 20, 2026, when the U.S. Supreme Court ruled that the sweeping worldwide tariffs imposed last year under the International Emergency Economic Powers Act (IEEPA) were unlawful. The Court found that the executive branch had overstepped its authority, effectively turning roughly $130 billion to $175 billion in collected duties into a massive pot of refundable money.

Immediately, over 2,000 companies—including Costco—filed their own lawsuits against the government to claw that money back.

The Conflict: “Double Recovery” vs. “Better Value”

The new consumer lawsuit, led by plaintiff Matthew Stockov, argues that Costco acted as a “pass-through vehicle.” The logic is simple:

The Hike: Costco raised prices on electronics, household goods, and food to cover the cost of the tariffs.

The Refund: Now that the tariffs are struck down, Costco is suing the government to get that money back.

The “Double Dip”: If Costco keeps the refund and the extra money they already collected from shoppers via higher prices, the lawsuit alleges they are “unjustly enriched” at the expense of their members.

Costco CEO Ron Vachris recently addressed the situation, stating the company’s commitment is to return value to members through “lower prices and better values” in the future.

However, the lawsuit isn’t buying it. The legal team argues that a promise of future discounts for future shoppers doesn’t compensate the specific people who paid the “tariff tax” last year. They want direct restitution.

Is a Refund Actually Coming?

While the Supreme Court ruling is a win for importers, getting cash into the hands of individual shoppers is a legal uphill battle. Here is why:

Standing: Under federal trade law, only the “importer of record” (Costco) has the legal right to claim a refund from the government.

The Math: Proving exactly how much of a $0.50 price hike on a rotisserie chicken was due to a specific tariff vs. inflation or supply chain issues is a forensic accounting nightmare.

The Contract: Legal experts note that when you buy an item, the “contract” is the price on the tag. Retailers generally aren’t legally obligated to refund you if their internal costs go down later.

What’s Next?

Costco isn’t the only one in the crosshairs. Similar suits have been filed against FedEx and EssilorLuxottica (the makers of Ray-Ban).

If the court certifies this as a class action, it could set a massive precedent for how “corporate windfalls” are handled after major policy reversals. For now, Costco members should keep their receipts—and their eyes on the Court of International Trade.

If Costco decides to fight this in court rather than settle, their legal team will likely lean on a defense built around retail economics and contract law.

Here are the four “pillars” of defense they are expected to use:

1. The “Commingled Costs” Argument

Retail pricing isn’t a simple $1+1=2$ equation. When Costco raises the price of a television, that hike accounts for shipping fuel, labor, warehouse rent, insurance, and tariffs. Costco will likely argue that it is mathematically impossible to isolate exactly how many cents of a price increase were “just” for the tariff. Since the costs were commingled, they may argue that specific “tariff surcharges” were never actually charged to the customer.

2. Lack of “Privity” (Direct Relationship)

In trade law, the “Importer of Record” is the only entity with a legal relationship to U.S. Customs.

Costco’s stance: We paid the government; the government owes us.

The logic: There is no contract between Costco and a member that promises to pass through government refunds. When you buy a jar of almond butter, you agree to the price on the tag at that moment, regardless of Costco’s internal cost fluctuations.

3. The “Future Value” Offset

CEO Ron Vachris has already hinted at this strategy. Costco may argue that they are already fulfilling their duty to members by using anticipated refunds to lower prices across the board today. By proving they are reinvesting the money into “better values,” they can claim they are not being “unjustly enriched”—the core requirement for the plaintiff to win.

4. Administrative Impossibility

Costco has over 130 million members. Tracking every single purchase of tariff-affected goods (from socks to patio furniture) over a multi-year period and issuing individual checks would be an administrative nightmare that could cost more than the refunds themselves. They may argue that a “cy-près” award (like a general price drop or a donation to a relevant cause) is a more legal and practical remedy than individual refunds.

Comparison of Arguments

Argument

Plaintiff’s View (Shoppers)

Defense View (Costco)

Enrichment

Costco gets a “double recovery” (shoppers’ money + gov refund).

Costco is a low-margin business that “returns value” via lower future prices.

Pricing

Prices went up specifically because of tariffs.

Prices are set by market competition and total operating costs.

Equity

The specific people who paid the “tax” should get the cash.

It is impossible to track individual “tariff cents” per member.

While Costco is currently the primary target of this specific class-action pressure, other major retailers like Walmart and Target are taking noticeably different approaches to the $175 billion tariff refund opportunity.

Here is how the other giants are positioning themselves:

1. Walmart: The “Conservative Pivot”

Walmart has been more cautious in its public statements regarding specific consumer refunds. Instead of promising direct returns, they are focusing on their role as a “price stabilizer.”

The Strategy: During their recent February 2026 earnings call, Walmart leadership noted they are using their massive scale to absorb costs. Their official stance is that because they negotiate long-term contracts and used “inventory pull-forward” strategies to avoid the worst of the tariffs, they didn’t pass through costs as directly as others.

The Defense: They are positioning any potential refunds as “capital for reinvestment” into their operations and employees, which they argue ultimately benefits customers through lower prices over the long term.

2. Target: The “Supplier Squeeze”

Target’s response has been more aggressive toward its supply chain rather than the federal government.

The Strategy: Target made headlines earlier this year by reportedly asking its Chinese suppliers to absorb up to 50% of the tariff costs to keep shelf prices stable.

The Stance: Because Target forced suppliers to eat much of the cost, they may argue that they aren’t the ones owed the full refund—or that since they didn’t raise prices as much as competitors, there is no “excess profit” to return to consumers.

3. FedEx & UPS: The “Direct Pass-Through” Exception

Unlike retailers where tariff costs are buried in the price of a gallon of milk, shipping companies like FedEx and UPS often used explicit line-item surcharges labeled as “Tariff Fees.”

The Vulnerability: Because these fees were itemized, these companies are facing the most direct legal heat. FedEx has indicated in recent filings that if they receive refunds, they have a framework to pass them back to the original shippers, though the logistics of reaching the end consumer remain a “mess.”

Summary of Retailer Responses

Retailer

Public Stance on Refunds

Primary Defense

Costco

“Future value” through lower prices and better deals.

Administrative impossibility of tracking individual cents.

Walmart

Focused on reinvesting refunds into business operations.

Scaled absorption—claims they didn’t pass through 1:1 costs.

Target

Silent on customer refunds; focused on supplier negotiations.

Argues suppliers bore the cost burden, not just the retailer.

FedEx

Exploring pass-throughs for itemized surcharges.

Contractual obligations to the “shipper of record.”

Why the National Retail Federation (NRF) is Worried

The NRF, which represents all three of these companies, has called for a “seamless and automatic” refund process from the government. However, they are lobbying hard against the idea that retailers must “prove” they passed the money back to consumers, calling such requirements an “accounting nightmare” that would stall the economic boost the refunds are intended to provide.

While the lawsuit filed by Matthew Stockov seeks a blanket refund for “all affected products,” the actual legal battle centers on specific goods that were hit by the International Emergency Economic Powers Act (IEEPA) tariffs.

Because Costco sells such a wide variety of items, the impact is spread across several high-volume categories. Here are the product types most likely to be at the heart of the refund calculations:

1. Electronics and Accessories

This is a massive category for Costco and one of the hardest hit by the reciprocal tariffs.

Small Tech: Laptop bags, charging cables, and power banks.

Peripherals: Computer mice, keyboards, and monitors.

Smart Home: Security cameras and small connected appliances.

Note: Some major electronics (like certain computers) were protected under different trade laws, but “intermediate” components and accessories were often taxed at the full IEEPA rate.

2. Home Furnishings and Hard Goods

Furniture retailers have been among the first to join the “refund clamor.”

Large Furniture: Sofas, dining sets, and patio furniture.

Home Decor: Rugs, textiles, and lighting fixtures.

Kitchenware: Cookware sets and small appliances (like air fryers or coffee makers) imported from affected regions.

3. Apparel and Footwear

These items saw some of the most significant price fluctuations over the last 12 months.

Clothing: “Fast fashion” items, activewear, and outerwear.

Shoes: Sneakers and boots, particularly those where the supply chain relies heavily on international sourcing.

4. Food and Intermediate Packaging

This is the most complex category for Costco to untangle.

Imported Specialties: Specific wines, spirits, and olive oils that were subject to geopolitical surcharges.

Packaging Costs: Even for “American-made” products, the tariffs often applied to the packaging (plastic containers, coffee filters, or baby wipe canisters) imported from abroad. Proving how a tariff on a plastic tub affected the price of the 5-pound tub of animal crackers is a key hurdle for the lawsuit.

What is NOT Included?

It’s important to note that many items at Costco were taxed under different laws (like Section 232 or Section 301), which the Supreme Court did not strike down. You likely won’t see refunds for:

Steel and Aluminum products (including some appliances and car parts).

Specific Chinese-made goods covered under long-standing trade war sections.

Summary Table: Refund Potential by Category

Product Category

Refund Potential

Why?

Electronics Acc.

High

Many were hit with the 2025 “reciprocal” 10-25% tariffs.

Furniture

High

Home goods were a primary target for IEEPA-based levies.

Apparel

Medium

High volume, but often split between different tariff authorities.

Groceries

Low

Most food price hikes were tied to inflation/labor, not just tariffs.

IEEPA Tariff While the Supreme Court invalidated the Administration’s ability to impose tariffs under IEEPA (International Emergency Economic Powers Act), it was deliberately silent with respect to refunds.

As the Administration’s stance is likely to be adversarial, it could take months if not years for businesses to receive IEEPA tariff refunds via conventional channels.

Prior to the Supreme Court Ruling, Hedge Funds were purchasing IEEPA tariff claims at an average of only 22% of the total claim due to the high risks involved. After the Ruling, due to mitigation of some of the uncertainty, they are currently purchasing claims at 75% of the refund amount. Rates are based on claim size and credit quality as tariff refund claims are not assignable. Importers with IEEPA tariff refund claims starting at $500,000 are eligible and there is no maximum limit. AES has monetized $20 million in refund claims since its involvement in brokering IEEPA tariff refund claims commenced 5 months ago. Clients include those in the food, seasonal decoration, apparel and home goods industries.

Instead of waiting 6, 12, 24 months or even longer to receive an IEEPA tariff refund, Hedge Funds can purchase claims within approximately 4 to 6 weeks depending on the quality of documentation assembled by the business.

How the Process of Selling an IEEPA Tariff Claim Works

Concept is: As an example, Company X has paid ($10 Million) in tariffs since April 7, 2025 Company X wants to de-risk prior to determination and finalization of the IEEPA tariff

Refund Process. Company X sells (50%, 100%, or some other percentage) of its tariff ‘claim’ to Buyer A in the form of a participation.

The Trade is nonrecourse to Company X as to the outcome of the Refund Process; but recourse to Company X only if the amount / validity of the claim is proven to be false, or too high.

Process for Selling IEEPA Tariff Claims: As an example, Company X has paid $10 million in IEEPA Tariffs.

Company X agrees to “sell” its tariff claim to Buyer for 75% of the claim amount, i.e. $7.5 million.

Buyer sends Seller a Confirm, and then ultimately a Participation Agreement which will govern the transaction. IMPORTANT – Company X retains its status as the “Plaintiff” / “Claimant” since these tariff claims are not transferable.

Buyer might ask Company X to commence litigation for the return of the IEEPA tariffs paid. The rationale for this is that it is possible that only those parties who have commenced actual litigation are entitled to refunds. Thus, Company X will need to commence litigation in order to receive their refund.

Buyer will continue to monitor the situation and inform Company X of developments. If and when the refund is received on the claim, Company X will receive the refund and forward to the Buyer.

Using an IEEPA Tariff Claim as Collateral for a Loan

In lieu of selling an IEEPA Tariff Claim at a discount, it is possible to use this claim as collateral for a term loan. This term loan would be on a “recourse: basis to the borrower.

The potential loan amount could be up to approximately 50% to 60% of the total IEEPA claim amount. However, the claim must exceed $20 million to qualify for a loan. The interest rate would be in the low to mid-teens.

Key Points Regarding the Sale: Company X (as seller of the Claim) must be a financially healthy enough counterparty for Buyer A to enter into what could be a 2-to-5-year process of obtaining the refund. Legal fees are split going forward based on risk percentage. If Company X sells 100% today, Buyer A will pay 100% of legal costs today.

Buyers are currently paying up to 75% to companies seeking to sell their IEEPA tariff claims. However, this is an evolving market and these percentages can either increase or decrease depending on the markets’ reaction to the Trump Administration’s expected obstructionism and the unresolved Court of International Trade’s procedural issues. Prior to the Supreme Court decision, buyers were purchasing tariff claims at an average of 22% due to the high risks involved.

We will be monitoring on a daily basis the rates at which Buyers are purchasing IEEPA claims and we will update our website accordingly. Feel free to email us to ascertain what the rate is on any particular day.

There would likely be an administrative process instituted such that companies that have paid these IEEPA tariffs will need to file special claims and wait to get refunded by the government. The process of receiving the refund payment from the government could take up to 2 to 5 years according to trade experts.

This details how investment firms are turning a legal and political mess into a new trading opportunity.

The situation stems from a recent Supreme Court ruling that tossed out several of President Trump’s sweeping tariffs. This has created a scramble for companies to claw back the levies they have already paid—estimated to be as high as $133 billion.

The Rise of “Claims Trading”: Large corporations (like retailers and manufacturers) that paid billions in tariffs are now selling the rights to their potential government refunds to Wall Street investors.

Why Companies Are Selling: Rather than waiting years for the government to process refunds or navigate complex litigation, companies are opting for immediate cash by selling their claims at a discount.

The Players: Specialist investment firms—including King Street Capital Management, Anchorage Capital Advisors, and Fulcrum Capital—are among those pouncing on these claims. They are betting that they can eventually collect the full refund from the Treasury, netting a significant profit.

Legal Uncertainty: The Supreme Court has not yet explicitly ruled on whether the government must issue refunds for the tariffs already collected. Despite this, investors are moving quickly to snap up these rights, treating them similarly to how they trade the debt of bankrupt companies.

The “Chaos” Factor: The process is currently a “long, drawn-out mess” with high administrative hurdles. Traders are effectively providing a “liquidity service” to companies that want the tariff money back on their balance sheets now rather than later.

In short, while the reversal of the tariffs has caused massive administrative and fiscal confusion for the government, Wall Street has identified it as a lucrative new asset class.

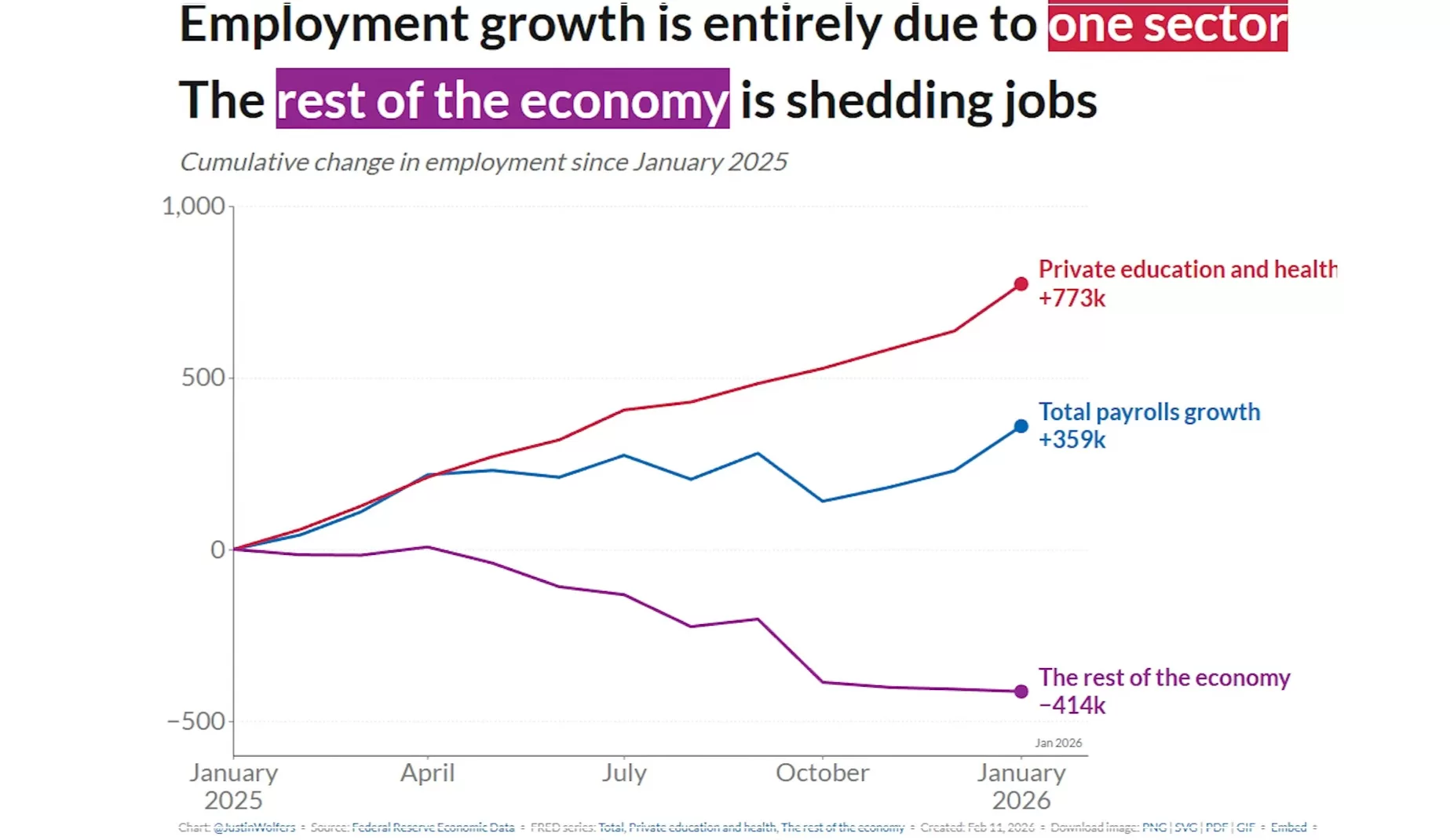

The U.S. labor market began 2026 with a surprising burst of energy, shaking off a sluggish 2025. According to the latest data from the Bureau of Labor Statistics (BLS) released on February 11, 2026, employers added 130,000 jobs in January—easily doubling December’s figures and blowing past economist expectations of roughly 70,000.

While the report was delayed by a week due to a brief federal government shutdown, the results suggest that the “hiring fatigue” seen late last year might be beginning to thaw.

The Numbers at a Glance

The January report offers a mix of resilience and necessary context for the year ahead:

Total Jobs Added: 130,000 (up from a revised 50,000 in December).

Unemployment Rate: Ticked down to 4.3% (from 4.4%).

Average Hourly Earnings: Rose by 0.4% in January, bringing the year-over-year increase to 3.7%.

Labor Force Participation: Remained steady at 62.5%.

Sector Winners and Losers

The growth wasn’t uniform across the board. In fact, a few key sectors carried the heavy lifting for the entire economy:

Healthcare & Social Assistance: This sector remains the titan of the U.S. job market, adding 124,000 jobs (82k in healthcare and 42k in social assistance).

Construction: Added a solid 33,000 jobs, largely driven by nonresidential specialty trade contractors.

The Tech & White-Collar Slump: Conversely, professional and business services and manufacturing continued to struggle, reflecting ongoing shifts in AI implementation and trade policy impacts.

Government: Federal employment saw a decline, partly a ripple effect of recent policy shifts and the temporary shutdown.

Why This Matters

After a tumultuous 2025—which was recently revised to show only 181,000 total jobs added for the entire year—this January figure is a massive sigh of relief. It suggests that while the economy isn’t sprinting, it’s found its footing.

“The January gains are a sign that the labor market is stabilizing,” says one economist. “However, the high concentration of growth in healthcare suggests a ‘one-legged stool’ economy that we need to watch closely.”

Looking Ahead

While 130,000 jobs is a “stronger footing,” the market remains complex. Layoffs in high-profile sectors like tech and transportation (notably Amazon and UPS) dominated January headlines, yet the aggregate data shows that other sectors are more than absorbing that displaced talent.

For job seekers, the message is clear: the opportunities are there, but they have shifted. Strategic hiring is the theme of 2026, with a high premium on specialized skills in healthcare, infrastructure, and adaptive technologies.

The January jobs report has effectively shifted the narrative for the Federal Reserve. While the 130,000 jobs added might seem modest by historical standards, it was a significant “beat” compared to expectations, and it has given the Fed a reason to tap the brakes on further interest rate cuts.

Here is how the latest data is influencing the Fed’s next move:

1. From “Easing” to “Holding”

Following three consecutive rate cuts in late 2025, the Federal Reserve held rates steady at its January 28, 2026 meeting, maintaining the federal funds rate at 3.5% to 3.75%. This jobs report reinforces that “pause.”

The Consensus: With the unemployment rate ticking down to 4.3% and job growth doubling December’s numbers, there is no longer an “emergency” need to stimulate the economy.

Market Sentiment: Before this report, some traders were betting on a March cut. Now, CME FedWatch tools show those odds have plummeted, with the consensus moving toward a “higher for longer” stance through at least the first half of the year.

2. Emerging Internal Division

The Fed is no longer acting in total unison. The January meeting saw a rare 10-2 vote, with two dissenting members actually pushing for another 25-basis-point cut due to lingering concerns about long-term hiring weakness.

The Hawks: Officials like Cleveland Fed President Beth Hammack and Dallas Fed President Lorie Logan have signaled that the Fed should “err on the side of patience,” arguing that current rates are “neutral”—neither helping nor hurting the economy.

The Doves: Those worried about the “one-legged stool” (growth coming only from healthcare) fear that without more cuts, sectors like tech and manufacturing will continue to bleed jobs.

3. The “Neutral Rate” Debate

Chair Jerome Powell recently noted that the economy is on a “firm footing” entering 2026. Analysts now believe the Fed is searching for the neutral rate—the sweet spot where inflation stays at 2% without triggering a recession.

Because average hourly earnings rose 0.4% in January (3.7% annually), the Fed is wary that cutting rates too soon could reignite inflation, especially with potential new trade tariffs on the horizon.

Key Dates to Watch

Event

Date

Significance

January CPI Report

Feb 13, 2026

Will confirm if the wage growth in the jobs report is driving up prices.

Fed “Beige Book”

Mar 4, 2026

Regional reports on how small businesses are actually feeling.

Next FOMC Meeting

Mar 17-18, 2026

The next formal window for a rate change decision.

For a small business owner, the January jobs report isn’t just about hiring statistics—it’s a leading indicator for the cost of your next loan or line of credit.

Following the stronger-than-expected labor data, the Federal Reserve has hit “pause” on interest rate cuts. For businesses at Versant Funding and across the U.S., this means a period of “stabilized high” borrowing costs. Here is what your business needs to know to navigate the financial landscape of early 2026.

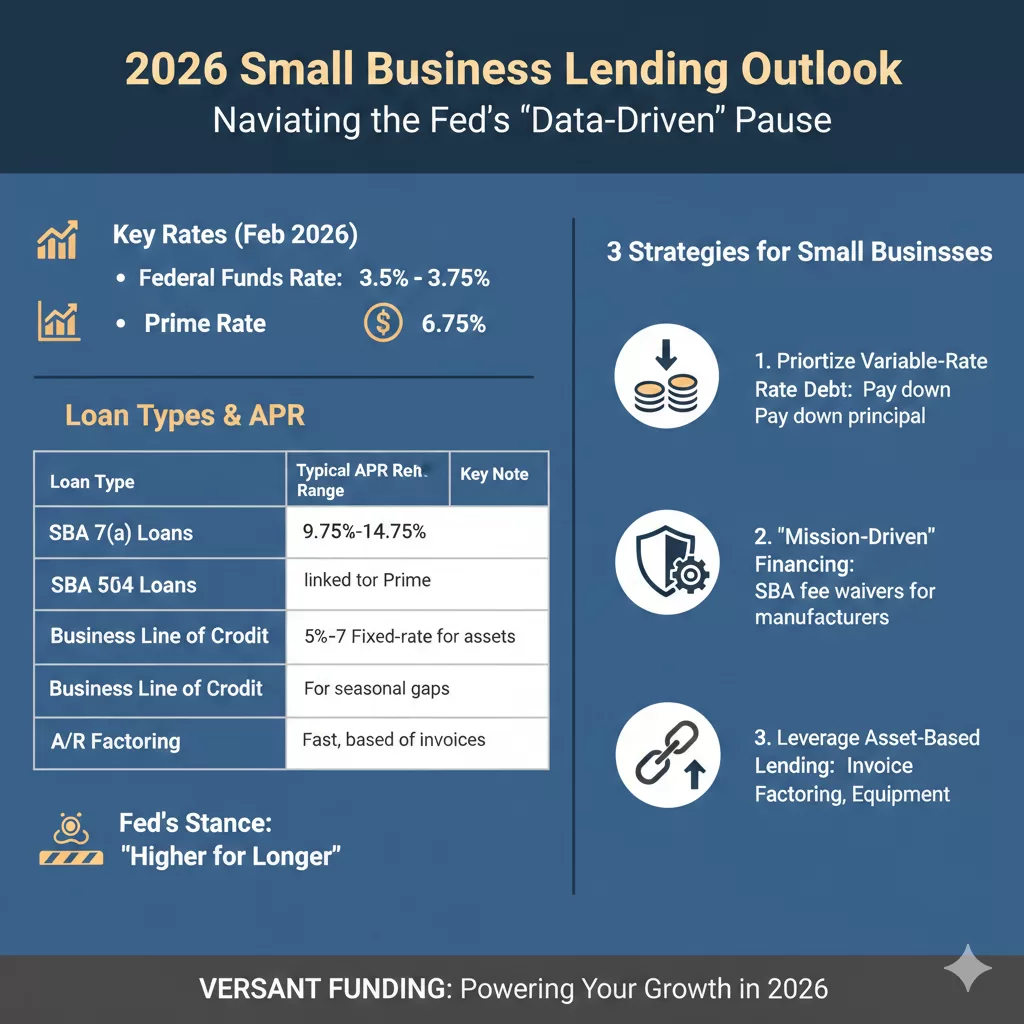

2026 Borrowing Outlook: The “Data-Driven” Pause

The Fed began 2026 by holding the federal funds rate steady at 3.5% to 3.75%. While the market had hoped for more aggressive easing, the surge of 130,000 new jobs in January has signaled to policymakers that the economy is not yet in need of more “cheap money.”

Current Lending Rates (As of February 2026)

Loan Type

Typical APR Range

Key Note

SBA 7(a) Loans

9.75% – 14.75%

Variable rates fluctuate with the Prime Rate (currently 6.75%).

SBA 504 Loans

5% – 7%

Fixed-rate; best for long-term real estate or equipment.

Business Lines of Credit

10% – 28%

Vital for seasonal inventory and payroll gaps.

Accounts Receivable Factoring

24% – 36%

High speed; based on invoice value rather than credit score.

Three Strategies for Small Businesses

With rates unlikely to drop significantly before the summer, owners should shift from “waiting for better rates” to “optimizing current cash flow.”

Prioritize Variable-Rate Debt: If you are carrying an SBA 7(a) loan or a variable line of credit, your payments will remain flat for now. Use this stability to pay down principal where possible, as the “higher for longer” stance means interest costs won’t be melting away anytime soon.

Look for “Mission-Driven” Financing: In 2026, the SBA is waiving guarantee fees for certain small manufacturers (NAICS 31-33). If your business fits this category, you could save thousands in upfront costs regardless of the interest rate.

Leverage Asset-Based Lending: If traditional bank term loans are too restrictive, consider Invoice Factoring or Equipment Financing. These options often focus more on the value of your assets (your unpaid invoices or machinery) than on the Fed’s baseline rates, providing more predictable access to capital during economic volatility.

The Bottom Line

The “stronger footing” of the U.S. labor market is a double-edged sword: it proves consumer demand is resilient, but it keeps the cost of capital elevated. For 2026, the most successful businesses will be those that prioritize liquidity and debt structure over simply chasing the lowest rate.

The results of recent surveys, most notably the Capital One Middle Market Strategic Investments report, have sent a ripple of confidence through the business community: 89% of middle-market companies are optimistic about their growth in 2026.

For those who track the “engine room” of the U.S. economy, this isn’t just a number—it’s a signal of a major strategic pivot. After years of playing defense against inflation and supply chain “whack-a-mole,” the middle market is moving back to offense.

Here is my take on why the “Mighty Middle” is feeling so bullish and what this means for the year ahead.

1. The “Big Beautiful Bill” Effect

A significant driver of this 89% figure is the One Big Beautiful Bill Act (OBBBA) passed in late 2025. Middle-market leaders aren’t just aware of the policy; they are already building it into their spreadsheets.

Tax Certainty: By codifying full expensing of capital expenditures and maintaining the 21% corporate tax rate, the bill has removed the “wait and see” hurdle that often stalls big investments.

Cash Flow: 59% of companies expect improved cash flow through these incentives, giving them the “dry powder” needed to expand.

2. AI: From “Hype” to “Help”

In 2024 and 2025, AI was a buzzword. In 2026, it’s a budget line item.

Operational Efficiency: 66% of middle-market businesses are prioritizing AI investment, not to replace humans, but to solve the persistent labor crunch.

ROI Focus: Unlike the “growth at all costs” tech era, middle-market firms are looking for AI to deliver specific returns—29% expect AI to be their highest-yielding investment this year.

3. Resilience Through “Alternate” Means

What I find most fascinating is the evolution of middle-market financing. With traditional bank lending remaining tight, 50% of these companies are now pursuing alternate financing, specifically private credit.

The Takeaway: Middle-market companies are no longer at the mercy of traditional interest rate cycles. They have diversified their “oxygen supply” (capital), allowing them to stay optimistic even when the Fed is being cautious.

4. The M&A “Spring”

After a multi-year slumber, deal-making is waking up. Nearly 44% of middle-market firms intend to pursue acquisitions in 2026. This suggests that the optimism isn’t just about internal growth; it’s about consolidation and picking up smaller players who may not have the scale to handle 2026’s regulatory and technological demands.

The Bottom Line: Execution is the New Strategy

The 89% optimism rate doesn’t mean the road is easy. Leaders are still citing inflation (97%) and tariffs as major headaches. However, the difference in 2026 is preparedness.

Middle-market companies have spent the last two years “stress-testing” their models. They are leaner, more tech-forward, and more agile than they were pre-2020. If 89% of them believe they can win this year, the rest of the market should probably pay attention.

The “Mighty Middle” is playing offense in 2026. 🚀

The numbers are in, and they are striking: 89% of middle-market companies are officially optimistic about their growth this year.

After years of navigating the “whack-a-mole” challenges of inflation and supply chain disruptions, we are seeing a massive strategic pivot. Middle-market leaders aren’t just surviving; they are scaling.

Why the surge in confidence?

The OBBBA Effect: Tax certainty and full expensing are providing the “dry powder” needed for major capital investments.

AI Integration: We’ve moved past the hype. Companies are now budgeting for AI to solve real-world labor shortages and drive operational efficiency.

Alternative Financing: With traditional bank lending remaining tight, the shift toward private credit and alternative capital sources is keeping growth on track.

M&A Resurgence: Nearly 44% of these firms are looking to acquire, signaling a year of consolidation and expansion.

The bottom line? These companies have “stress-tested” their models for two years. They are leaner, tech-forward, and ready to win.

Is the Middle Market the new economic bellwether for 2026? 📈

The data is hard to ignore: 89% of middle-market firms are entering 2026 with high optimism. This isn’t just “wishful thinking”—it’s a calculated response to a shifting fiscal and technological landscape.

Here are the four pillars driving this confidence:

Fiscal tailwinds: The One Big Beautiful Bill Act (OBBBA) has finally provided the tax certainty and full-expensing incentives required to move “wait-and-see” capital into active deployments.

Maturity in AI adoption: We have moved beyond the “hype cycle.” 66% of mid-cap leaders are now prioritizing AI as a tool for operational leverage, specifically targeting persistent labor bottlenecks.

The Rise of Alternative Credit: As traditional bank lending remains constrained, the pivot toward private credit and specialized liquidity solutions has decoupled middle-market growth from traditional interest rate volatility.

Strategic Consolidation: With 44% of firms pursuing M&A, we are entering a period of significant market “up-tiering.”

The “Mighty Middle” has spent the last 24 months stress-testing their balance sheets. In 2026, they aren’t just defending their position—they are expanding it.

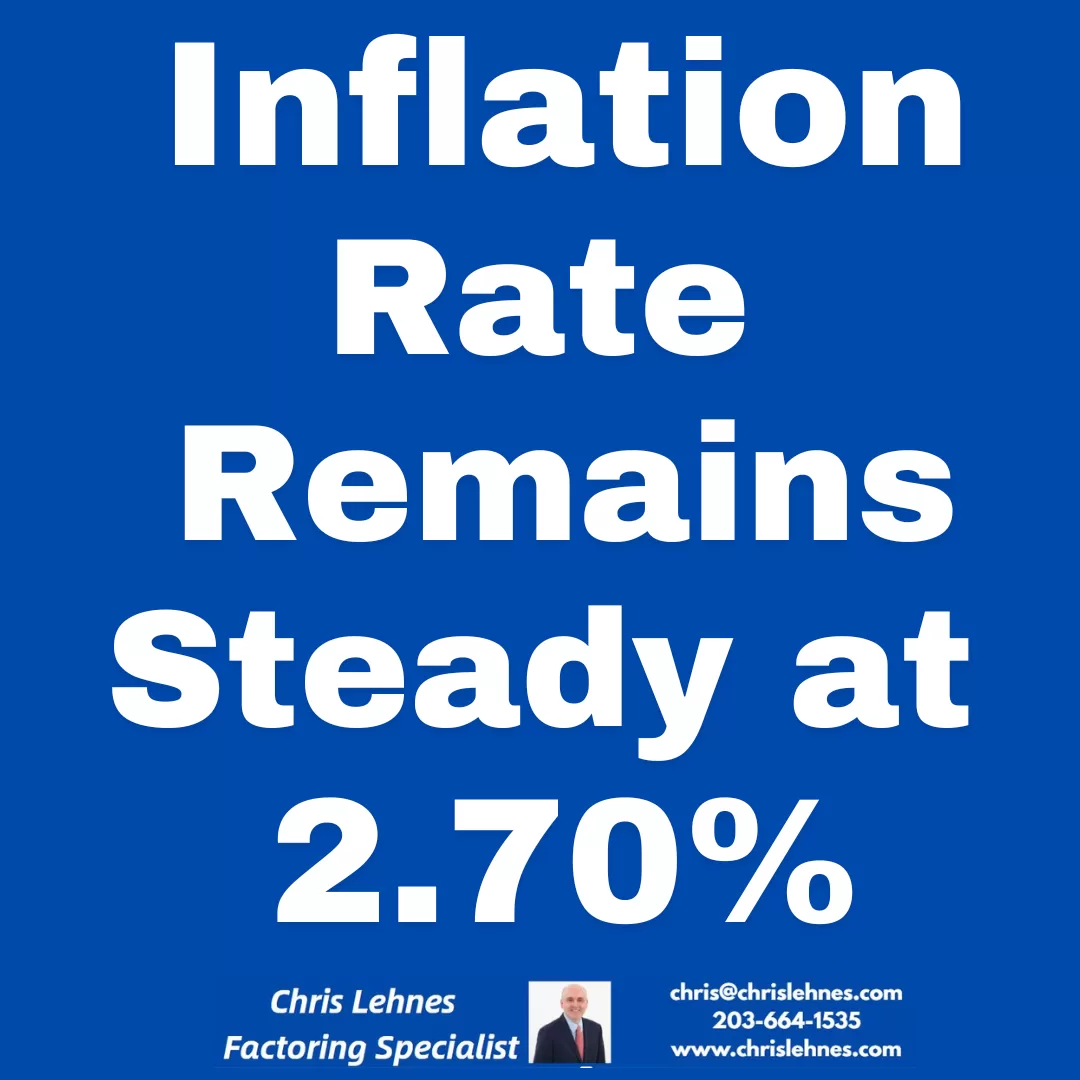

The Inflation “Split Screen”: What December’s CPI Numbers Really Mean

Inflation Stable. The latest data is in, and it paints a picture of an economy caught between cooling pressures and political friction. In December, consumer prices rose 2.7% from a year earlier—holding steady from November and landing exactly where economists predicted.

While the “headline” number suggests stability, the story beneath the surface is much more complex. Here are the key takeaways from the final inflation report of 2025.

1. Stability Amidst the Noise

For the second month in a row, inflation has leveled off at 2.7%. Meanwhile, “Core CPI” (which strips out volatile food and energy costs) rose 2.6%.

Interestingly, these numbers came in slightly better than the 2.8% core increase some experts feared. This suggests that despite the introduction of steep tariffs earlier in 2025, businesses haven’t yet passed the full weight of those costs onto consumers. However, the “last mile” of the journey back to the Fed’s 2% target remains stubbornly out of reach.

2. A Cloud of Data Uncertainty

This report is the first “clean” look at inflation we’ve had in months. Following a government shutdown last fall, the Labor Department had to rely on technical workarounds to fill data gaps.

The “Payback” Effect: Many economists believe November’s figures may have been artificially low due to those data collection issues.

The Verdict: While December’s numbers didn’t spike as much as feared, they likely reflect a correction for the missing data from previous months.

3. The Fed’s High-Stakes Balancing Act

The Federal Reserve is currently navigating a “split screen” economy. On one hand, growth remains solid; on the other, the labor market has cooled significantly. In fact, 2025 saw the lowest pace of job growth since 2003 (excluding major recessions).

The Fed cut rates three times at the end of 2025 to support the job market, but officials are now divided. With inflation still above 2%, some are hesitant to keep cutting—especially as they watch for the inflationary impact of the One Big Beautiful Bill Act and ongoing investments in AI.

4. Politics vs. Policy

Perhaps the most unusual backdrop to this report is the unprecedented political pressure on independent agencies.

The Labor Department: Its commissioner was fired in August amidst claims of “rigged” numbers.

The Fed: Chair Jerome Powell recently alleged that the administration has used threats of criminal prosecution to pressure the board into lowering interest rates.

What’s Next?

As we head into 2026, all eyes are on January and February. This is traditionally when businesses reset their pricing for the year. Whether they will hike prices to account for tariffs and tax-cut-driven demand remains the big question.

For now, the “meandering path” toward lower inflation continues, but with a cooling job market and political volatility, the road ahead looks anything but smooth.

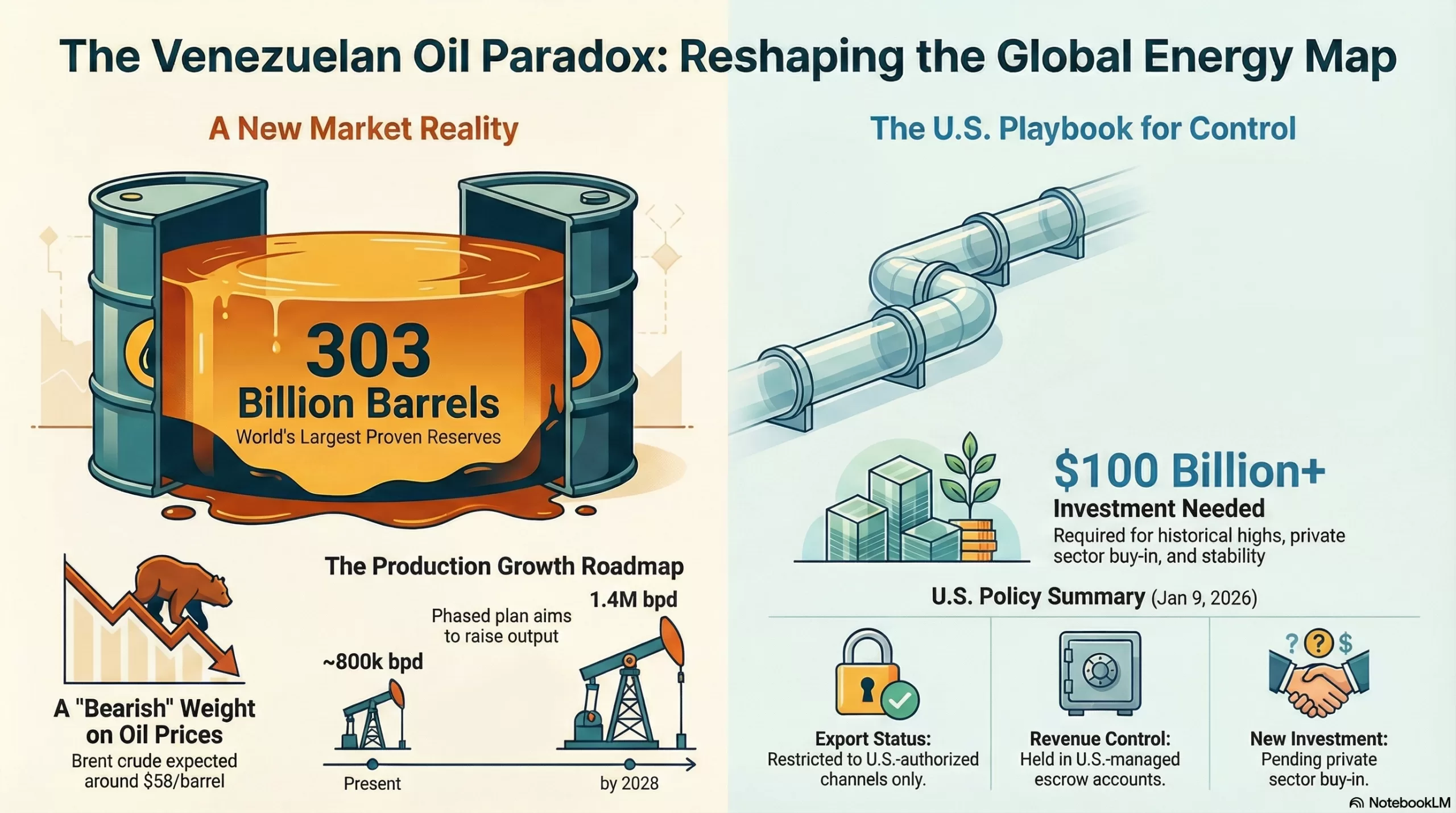

The start of 2026 has brought one of the most significant shifts in the energy sector in decades. With the recent capture of Nicolás Maduro on January 3, 2026, and the subsequent move by the U.S. administration to overhaul Venezuela’s energy infrastructure, the global oil market is facing a new “Venezuelan Paradox.”

While Venezuela holds the world’s largest proven oil reserves—estimated at over 303 billion barrels—its actual impact on the global market is currently a tug-of-war between massive long-term potential and a short-term supply glut.

1. The Immediate Shock: Volatility vs. the “Glut”

In the days following the January 3rd intervention, oil prices saw a brief “short squeeze” as traders priced in geopolitical risk, with prices nudging toward $60/barrel. However, the broader market remains in a state of oversupply.

Experts from J.P. Morgan and the IEA highlight that the market is currently facing a significant supply glut. Brent crude is forecasted to average around $58/barrel for the remainder of 2026. Because the world is already well-supplied by U.S. shale and Guyana, the return of Venezuelan barrels acts as a “bearish” weight on prices rather than a catalyst for a spike.

2. The Production Road Map: From 800k to 1.4M

As of early 2026, Venezuela’s production sits between 750,000 and 960,000 barrels per day (bpd). While the U.S. Department of Energy (DOE) is already moving to release millions of barrels of “sanctioned oil” held in floating storage, actual production growth will take time.

Short-term (End of 2026): Production could realistically ramp up to 1.1–1.2 million bpd if sanctions are selectively rolled back to allow for infrastructure repairs.

Medium-term (2027-2028): With sustained investment from firms like Chevron and others, output could hit 1.4 million bpd.

The Long Game: Reaching the historical highs of 3 million bpd is estimated to require over $100 billion in investment and at least a decade of stable governance.

3. Geopolitical Pivot: China’s Loss, the U.S. Gulf’s Gain

For years, Venezuela’s oil was the lifeblood of China’s “teapot” (independent) refineries, often sold at steep discounts to circumvent sanctions. That era is ending.

The U.S. administration has signaled that Venezuelan oil will now flow through “authorized channels,” prioritizing U.S. and Western markets. This creates a massive shift in trade flows:

U.S. Gulf Coast Refiners: These facilities were originally built to process the heavy, sour crude that Venezuela produces. They are expected to reclaim these volumes, reducing their reliance on more expensive alternatives.

China’s Response: Chinese refineries are likely to pivot toward Russian Urals or Iranian Heavy, potentially intensifying competition for those sanctioned grades.

4. The OPEC+ Balancing Act

Venezuela is a founding member of OPEC, but its production has been so low for so long that it has mostly been a “silent partner.” In response to the 2026 developments, OPEC+ has paused its planned output hikes for Q1 2026.

The group, led by Saudi Arabia and Russia, is wary of a “perfect storm”: a global slowdown combined with a sudden surge in Venezuelan exports. If Venezuela successfully rehabilitates its sector, OPEC+ may have to maintain deeper cuts for longer to prevent prices from sliding into the $40s.

The Bottom Line

The “Venezuelan effect” in 2026 is less about a sudden flood of oil and more about a reordering of the global energy map. For the first time in a generation, the “Western Hemisphere energy powerhouse” (U.S., Canada, Guyana, and Venezuela) looks like a unified block that could significantly challenge the pricing power of Middle Eastern and Russian suppliers.

For small businesses and consumers, this is generally good news. The presence of Venezuelan “upside risk” to supply acts as a ceiling for oil prices, likely keeping fuel and energy costs stable throughout the year.

The landscape for Venezuelan oil shifted dramatically following the capture of Nicolás Maduro on January 3, 2026.1 The U.S. administration has moved quickly to assert control over the sector, balancing long-term infrastructure goals with immediate market pressure.2

Here is a summary of the current U.S. policy changes and strategic directives as of January 9, 2026:

1. The “Approved Channels” Only Policy3

The U.S. has established a strict “quarantine” on all oil movements.

Controlled Sales: The Energy Department has mandated that the only oil allowed to leave Venezuela must flow through U.S.-approved channels.4

Vessel Seizures: The U.S. Coast Guard and DOJ have already begun seizing “dark fleet” tankers in the North Atlantic and Caribbean that were attempting to move sanctioned oil outside of these new channels.5

The 50M Barrel Release: Interim authorities have agreed to turn over 30 to 50 million barrels of existing storage to the U.S. for sale at market prices.6

2. Financial & Revenue Control

A central pillar of the new policy is the “purse strings” strategy:7

Escrow Accounts: Revenue from Venezuelan oil sales is being deposited into U.S.-controlled accounts at globally recognized banks.8

Disbursement: Funds are intended to be disbursed at the discretion of the U.S. government to support the “American and Venezuelan populations,” rather than the previous regime’s lieutenants.9

Conditionality: Further sanctions relief is tied to Venezuela severing all economic ties with China, Russia, Iran, and Cuba.10

3. “Selective” Sanctions Rollbacks

Instead of a broad lifting of all sanctions, the Treasury’s Office of Foreign Assets Control (OFAC) is issuing private waivers and specific licenses:11

Infrastructure Priority: Licenses are being granted specifically for the import of oil field equipment, parts, and services.12 This is designed to reverse decades of decay in the Orinoco Belt.

Diluent Imports: The U.S. is authorizing the shipment of diluents (thinners) to Venezuela, which are required to make their heavy crude liquid enough to pump through pipelines and onto tankers.13

Direct Waivers: Private trading firms are being granted specific waivers to resume purchases, provided the oil is sold to U.S.-based buyers.14

4. The “Private Sector Pivot”

President Trump is meeting with executives from ExxonMobil, Chevron, and others (as of Friday, Jan 9) to pitch a massive redevelopment plan:15

The Investment Goal: The administration is pushing for private companies to lead a $60B–$100B overhaul of the industry.

The Conflict: There is a stated policy goal of driving global oil prices down to $50/barrel.16 This creates a “profitability gap” for oil majors, who argue that the cost of extracting heavy Venezuelan crude may not be viable if prices fall that low.

Key Policy Benchmarks for 2026

Policy Area

Current Status (Jan 9, 2026)

Export Status

Restricted to U.S.-authorized channels only.

Revenue Control

Held in U.S.-managed accounts.

New Investment

Pending private sector “buy-in” and stability guarantees.

OPEC Status

Effectively suspended from quota participation during transition.

Briefing: The 2026 Venezuelan Oil Sector Transformation

Executive Summary

The capture of Nicolás Maduro on January 3, 2026, has triggered a fundamental and rapid transformation of Venezuela’s oil sector, creating what is termed the “Venezuelan Paradox.” While the nation possesses the world’s largest proven oil reserves at over 303 billion barrels, its immediate market impact is a bearish pressure on prices due to a global supply glut, rather than a price spike. The U.S. administration has swiftly implemented a strategy of direct control over Venezuela’s oil exports and revenue, mandating that all sales flow through “approved channels” and placing proceeds into U.S.-managed escrow accounts.

This strategic pivot is causing a significant reordering of the global energy map. U.S. Gulf Coast refiners, designed for Venezuelan heavy crude, are positioned to benefit, while China’s independent refineries lose a primary source of discounted oil. In response to the potential for increased Venezuelan supply, OPEC+ has paused planned output hikes, wary of a price collapse. The overarching outcome is the potential formation of a powerful, unified Western Hemisphere energy bloc (U.S., Canada, Guyana, and Venezuela) capable of challenging the pricing power of Middle Eastern and Russian suppliers. For consumers, this development is expected to act as a ceiling on oil prices, promoting stable energy costs through 2026.

1. The Venezuelan Paradox: Market Dynamics and Production Outlook

The events of early January 2026 have introduced a complex dynamic into the global oil market, defined by the conflict between Venezuela’s immense long-term potential and the immediate realities of its dilapidated infrastructure and a well-supplied global market.

Immediate Market Impact: Volatility vs. Glut

Initial Volatility: In the immediate aftermath of the January 3 intervention, oil prices experienced a brief “short squeeze” driven by geopolitical risk, temporarily pushing prices toward $60 per barrel.

Prevailing Glut: This volatility was short-lived, as the broader market remains in a state of oversupply. Analysis from J.P. Morgan and the IEA indicates a significant supply glut, reinforced by ample production from U.S. shale and Guyana.

Price Forecast: The re-entry of Venezuelan barrels is viewed as a “bearish” weight on the market. Brent crude is forecasted to average approximately $58 per barrel for the remainder of 2026.

Phased Production Roadmap

Venezuela’s current oil production stands between 750,000 and 960,000 barrels per day (bpd). A multi-stage recovery is anticipated, contingent on investment and stability.

Short-Term (End of 2026): Production could ramp up to 1.1–1.2 million bpd with selective rollbacks on sanctions to permit essential infrastructure repairs.

Medium-Term (2027-2028): Sustained investment from major firms like Chevron could elevate output to 1.4 million bpd.

Long-Term Goal: Reaching the historical peak production of 3 million bpd is a formidable challenge, estimated to require over $100 billion in capital investment and at least a decade of stable governance.

2. U.S. Strategic Control and Policy Directives

The U.S. administration has enacted a comprehensive policy framework to manage Venezuela’s oil sector, focusing on controlling exports, revenue, and the pace of redevelopment.

“Approved Channels” and Asset Control

Export Quarantine: The U.S. has instituted a strict policy mandating that the only oil permitted to leave Venezuela must move through U.S.-approved channels.

Enforcement Actions: The U.S. Coast Guard and Department of Justice have begun seizing “dark fleet” tankers in the North Atlantic and Caribbean attempting to transport sanctioned oil outside these new regulations.

Release of Stored Oil: Interim Venezuelan authorities have agreed to transfer 30 to 50 million barrels of oil from floating storage to U.S. control for sale at market prices.

Financial Controls and Sanctions Policy

A “purse strings” strategy is central to the U.S. approach, ensuring financial oversight and leveraging sanctions for policy goals.

Escrow Accounts: All revenue from authorized Venezuelan oil sales is being deposited into U.S.-controlled escrow accounts at major international banks. Funds are intended for the “American and Venezuelan populations.”

Conditional Relief: Further sanctions relief is explicitly tied to Venezuela severing all economic ties with China, Russia, Iran, and Cuba.

Selective Waivers: The Treasury’s Office of Foreign Assets Control (OFAC) is issuing private waivers and specific licenses rather than a blanket lifting of sanctions. These licenses prioritize:

Import of oil field equipment, parts, and services to repair the Orinoco Belt.

Shipment of diluents required to make Venezuela’s heavy crude transportable.

Waivers for private trading firms to purchase oil, provided it is sold to U.S.-based buyers.

The Private Sector Pivot and Investment Strategy

The U.S. is encouraging private investment to lead the sector’s revitalization, though a potential conflict exists between policy goals and corporate profitability.

Investment Goal: President Trump is actively meeting with executives from ExxonMobil, Chevron, and other firms to promote a massive redevelopment plan estimated to cost between $60 billion and $100 billion.

The Profitability Conflict: A stated administration policy goal is to drive global oil prices down to $50 per barrel. Oil majors have expressed concern that this price point may render the extraction of heavy Venezuelan crude unprofitable, creating a “profitability gap” that could hinder investment.

Key Policy Benchmarks (as of Jan 9, 2026)

Policy Area

Current Status

Export Status

Restricted to U.S.-authorized channels only.

Revenue Control

Held in U.S.-managed accounts.

New Investment

Pending private sector “buy-in” and stability guarantees.

OPEC Status

Effectively suspended from quota participation during transition.

3. Geopolitical Realignment and Global Impact

The shift in Venezuela’s oil policy is causing a significant reordering of global energy trade flows and prompting strategic recalculations by major market players.

Shifting Trade Flows: U.S. Gulf vs. China

U.S. Gulf Coast Gains: Refineries along the U.S. Gulf Coast, which were originally engineered to process Venezuela’s specific grade of heavy, sour crude, are expected to be the primary beneficiaries. They can now reclaim these volumes, reducing their dependence on more expensive alternatives.

China’s Loss: The era of China’s “teapot” (independent) refineries sourcing heavily discounted Venezuelan crude is ending. Chinese refiners are now expected to pivot toward other sanctioned grades, such as Russian Urals or Iranian Heavy, potentially increasing competition for these barrels.

OPEC+ Response and Price Stabilization

As a founding member of OPEC, Venezuela’s potential return to significant production levels presents a challenge to the cartel’s market management strategy.

Preemptive Action: In response to the developments, OPEC+ (led by Saudi Arabia and Russia) has paused its planned output hikes for Q1 2026.

Managing the “Perfect Storm”: The group is concerned about a “perfect storm” scenario where a global economic slowdown coincides with a surge in Venezuelan exports.

Future Cuts: If Venezuela successfully rehabilitates its oil sector, OPEC+ may be forced to maintain deeper and longer production cuts to prevent crude prices from sliding into the $40s per barrel range.

4. Conclusion: A New Energy Landscape

The “Venezuelan effect” in 2026 is less about an immediate flood of new oil and more about a fundamental reordering of the global energy map. For the first time in a generation, a unified “Western Hemisphere energy powerhouse”—comprising the United States, Canada, Guyana, and a revitalized Venezuela—appears poised to emerge. This bloc could significantly challenge the long-held pricing power of suppliers in the Middle East and Russia. For consumers and businesses, this shift introduces substantial “upside risk” to global supply, creating a natural ceiling for oil prices and likely contributing to stable fuel and energy costs throughout the year.