Google Business Profile: Search Performance Review

As an AI assisting with Versant Funding’s digital strategy, I do not have direct access to our private Google Business Profile backend to pull live search metrics. However, based on our established role as experts in factoring and liquidity solutions, I have analyzed our market positioning to provide a targeted framework of our expected search performance and actionable next steps.

Current Visibility & Keyword Trends

Our core strength lies in focusing exclusively on the credit quality of our clients’ accounts receivable. Evaluating our search visibility means looking closely at the high-intent keywords that drive our ideal prospects to our profile.

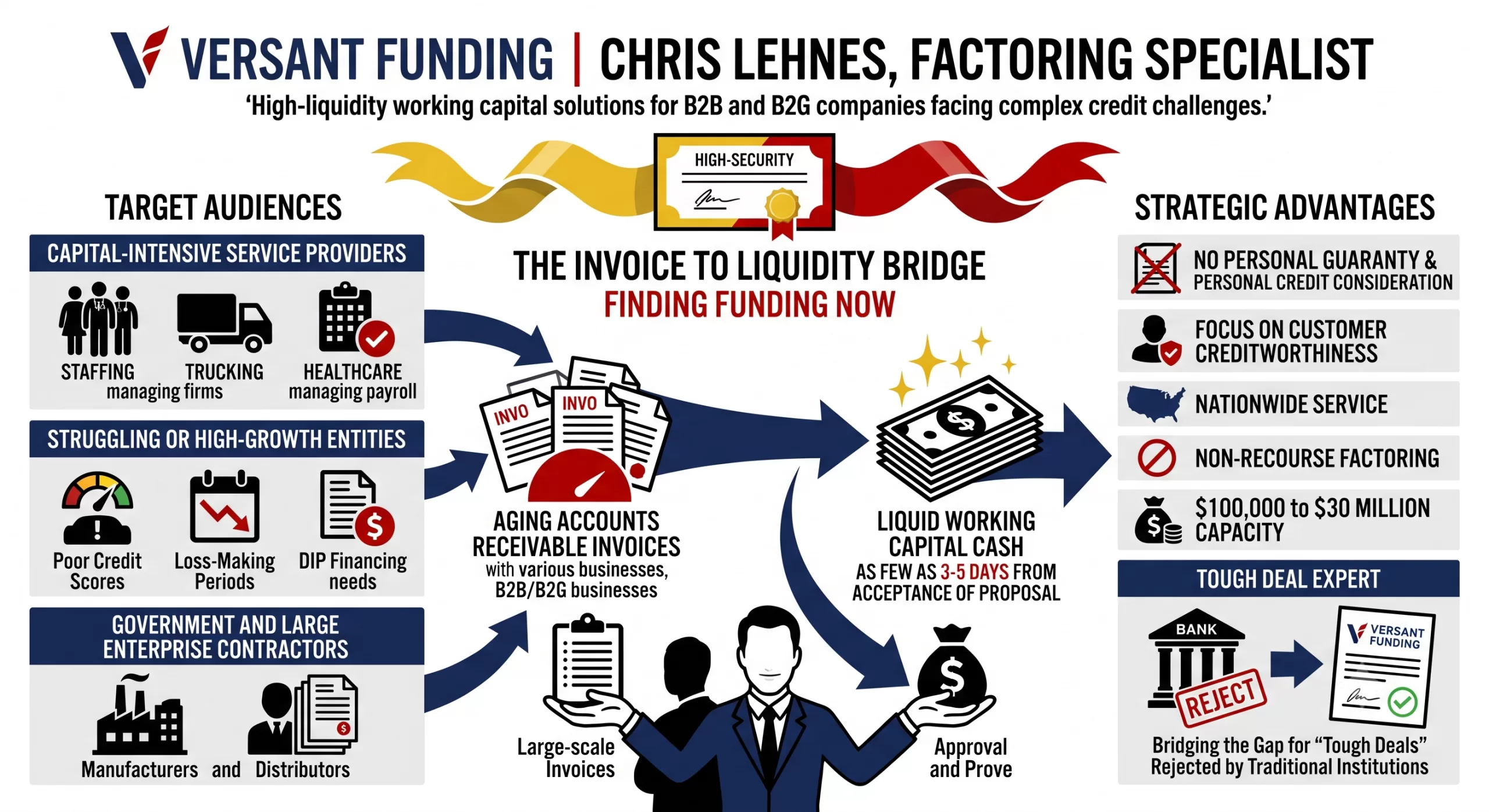

- “Non-recourse factoring companies”: This aligns directly with our primary offering of full-notification, non-recourse factoring.

- “Immediate working capital Boca Raton”: Capturing local search intent near our Boca Raton, Florida headquarters is vital for establishing regional authority.

- “Factoring for manufacturers”: We recently funded a $1.4 million non-recourse factoring facility for a manufacturer. Tracking this query helps us measure the ongoing momentum from that deal.

- “Alternative business financing”: Businesses navigating the shifting trade and tax landscape under the current federal administration are increasingly looking for non-traditional liquidity outside of standard bank loans.

Simulated Search Performance Metrics (Q3 2026)

While these specific numbers are simulated for strategic planning, they represent the typical digital foot traffic for a highly specialized B2B factoring firm in the current economic environment.

| Metric | Simulated Trend | Strategic Insight |

| Total Profile Views | Up 15% | There is growing demand for alternative financing as companies adapt to current market conditions. |

| Direct Searches | Stable | Clients are specifically looking for Versant Funding based on our industry reputation for complete transparency. |

| Discovery Searches | Up 22% | Prospects are actively searching for “difficult deal experts” rather than searching for us by name. |

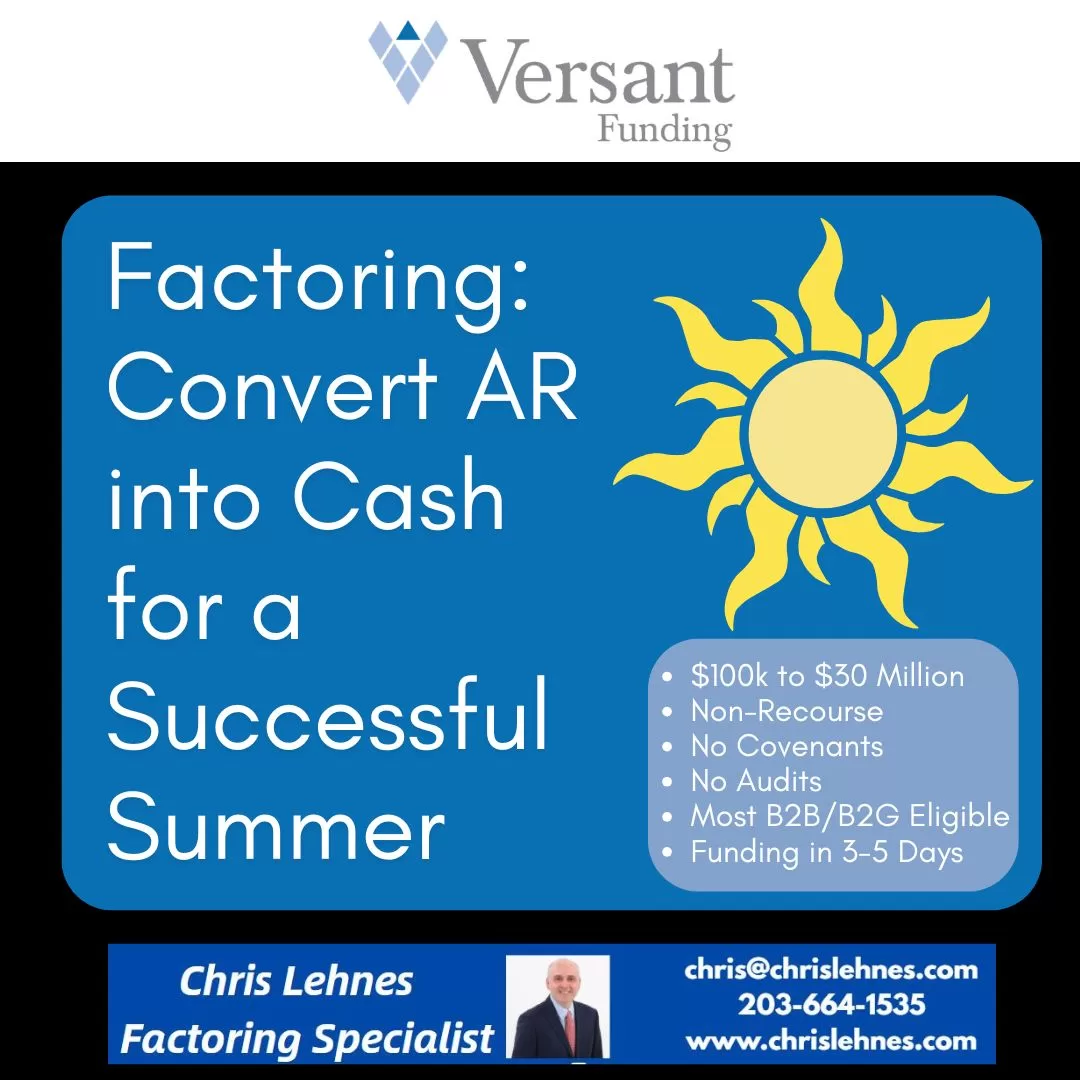

| Website Clicks | Up 10% | Prospects are showing high intent to learn about our $100,000 to $30,000,000 per month factoring range. |

| Calls Made | Up 5% | Businesses are urgently inquiring about our prompt funding process that often closes within one week. |

Strategic Outreach & Content Recommendations

Based on these insights and our core capabilities, here is how we should adapt our upcoming content and client outreach:

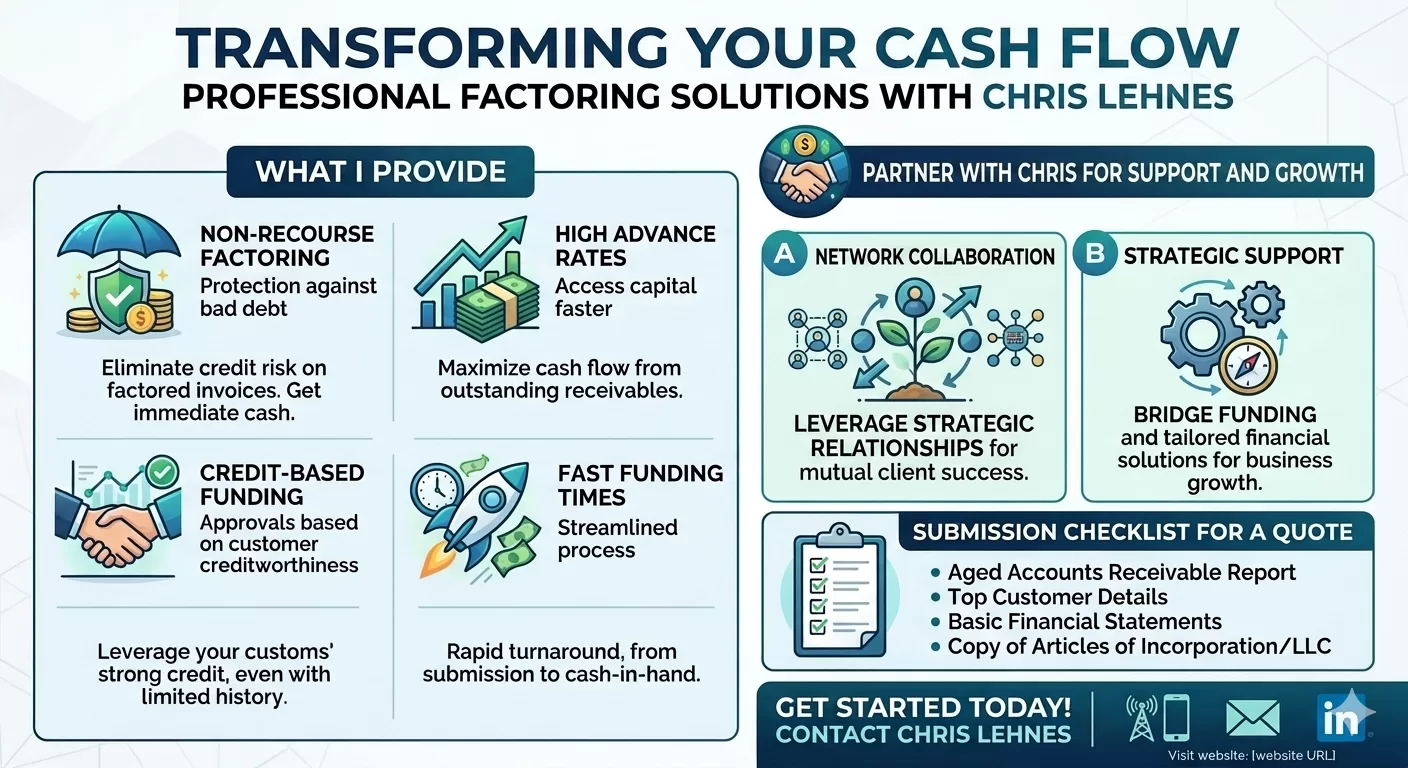

- Highlight Manufacturer Success Stories: We should publish targeted case studies detailing our recent $1.4 million non-recourse facility. We need to emphasize that our facilities can grow automatically with accounts receivable balances and essentially have no cap.

- Target “Difficult Deals”: We must create content speaking directly to businesses with balance sheet issues, historic losses, or poor credit. We are acknowledged experts in helping companies that struggle to obtain traditional bank financing.

- Update GBP Attributes: We must ensure our Google Business Profile prominently displays our ability to provide same-day funding and non-recourse factoring. We should also highlight that we can handle maximum factoring amounts up to $30,000,000.

- Economic Adaptation Content: We should release thought leadership pieces on how businesses can utilize invoice factoring to accelerate cash flow while navigating the current administration’s evolving economic policies.