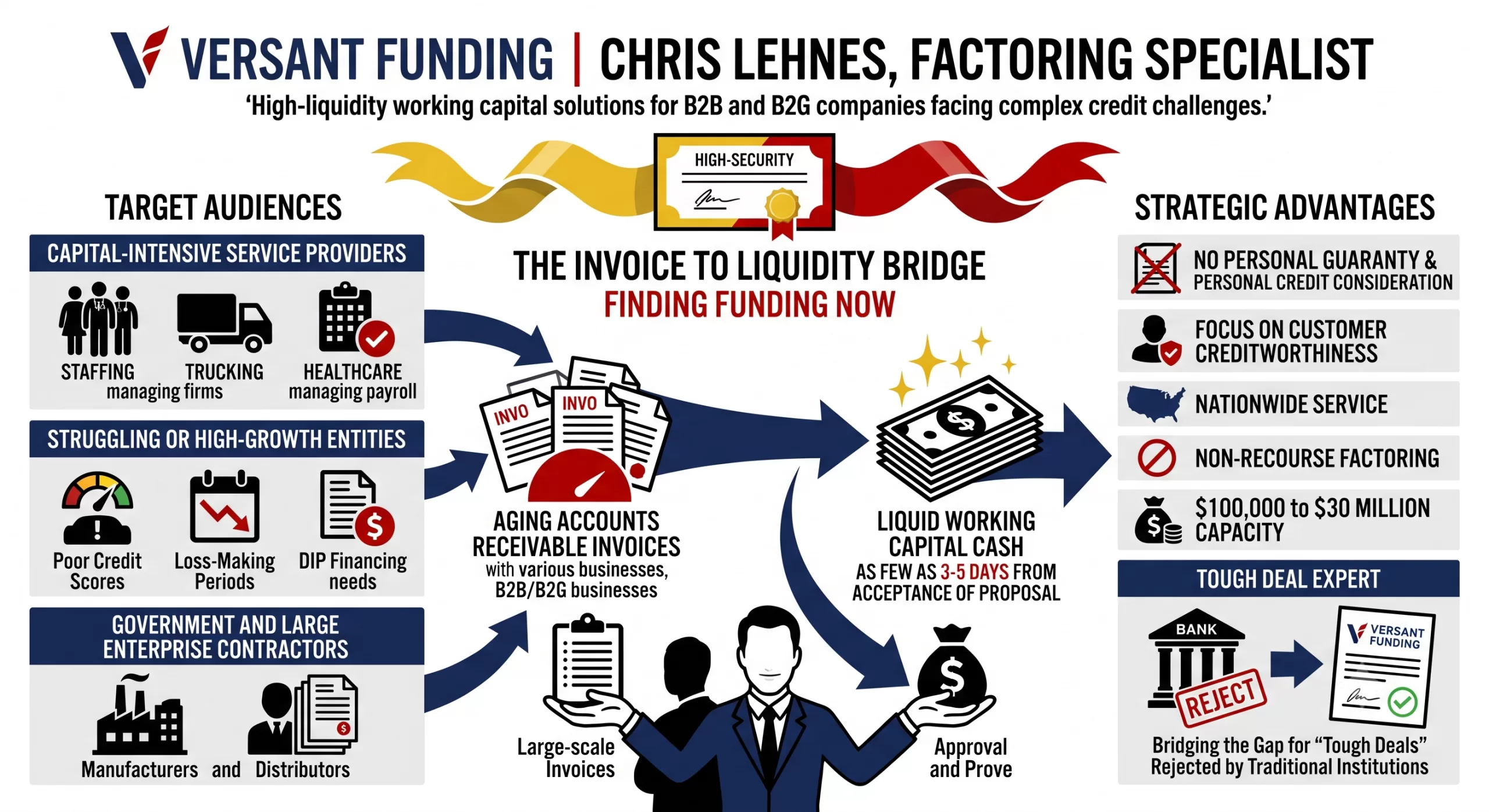

Factoring is a vital source of funding for businesses. Many of your clients may not be eligible for traditional bank financing, but have an immediate need for cash.

We focus on the quality of your client’s accounts receivable, ignoring their financial condition.

Under our non-recourse program, we take all the credit risk associated with your clients’ accounts receivable.

This enables us to move quickly and fund qualified businesses including Manufacturers, Distributors and a wide variety of Service Businesses – including SaaS – in as few as 3-5 days.

Factoring Program Overview

$100,000 to $30 Million

Quick Advance Against AR

No Audits

No Financial Covenants

No Long-Term Commitment

Most businesses with strong customers are eligible

Google Business Profile: Search Performance Review

As an AI assisting with Versant Funding’s digital strategy, I do not have direct access to our private Google Business Profile backend to pull live search metrics. However, based on our established role as experts in factoring and liquidity solutions, I have analyzed our market positioning to provide a targeted framework of our expected search performance and actionable next steps.

Current Visibility & Keyword Trends

Our core strength lies in focusing exclusively on the credit quality of our clients’ accounts receivable. Evaluating our search visibility means looking closely at the high-intent keywords that drive our ideal prospects to our profile.

“Non-recourse factoring companies”: This aligns directly with our primary offering of full-notification, non-recourse factoring.

“Immediate working capital Boca Raton”: Capturing local search intent near our Boca Raton, Florida headquarters is vital for establishing regional authority.

“Factoring for manufacturers”: We recently funded a $1.4 million non-recourse factoring facility for a manufacturer. Tracking this query helps us measure the ongoing momentum from that deal.

“Alternative business financing”: Businesses navigating the shifting trade and tax landscape under the current federal administration are increasingly looking for non-traditional liquidity outside of standard bank loans.

Simulated Search Performance Metrics (Q3 2026)

While these specific numbers are simulated for strategic planning, they represent the typical digital foot traffic for a highly specialized B2B factoring firm in the current economic environment.

Metric

Simulated Trend

Strategic Insight

Total Profile Views

Up 15%

There is growing demand for alternative financing as companies adapt to current market conditions.

Direct Searches

Stable

Clients are specifically looking for Versant Funding based on our industry reputation for complete transparency.

Discovery Searches

Up 22%

Prospects are actively searching for “difficult deal experts” rather than searching for us by name.

Website Clicks

Up 10%

Prospects are showing high intent to learn about our $100,000 to $30,000,000 per month factoring range.

Calls Made

Up 5%

Businesses are urgently inquiring about our prompt funding process that often closes within one week.

Strategic Outreach & Content Recommendations

Based on these insights and our core capabilities, here is how we should adapt our upcoming content and client outreach:

Highlight Manufacturer Success Stories: We should publish targeted case studies detailing our recent $1.4 million non-recourse facility. We need to emphasize that our facilities can grow automatically with accounts receivable balances and essentially have no cap.

Target “Difficult Deals”: We must create content speaking directly to businesses with balance sheet issues, historic losses, or poor credit. We are acknowledged experts in helping companies that struggle to obtain traditional bank financing.

Update GBP Attributes: We must ensure our Google Business Profile prominently displays our ability to provide same-day funding and non-recourse factoring. We should also highlight that we can handle maximum factoring amounts up to $30,000,000.

Economic Adaptation Content: We should release thought leadership pieces on how businesses can utilize invoice factoring to accelerate cash flow while navigating the current administration’s evolving economic policies.

Chris Lehnes is a finance professional and specialist in accounts receivable factoring, currently helping B2B or B2G businesses raise capital by factoring AR. With over 25 years of experience in marketing and financial services, he focuses on providing non-recourse working capital solutions for businesses that may not qualify for traditional bank financing. [1, 2, 3, 4]

Professional Expertise

Lehnes operates primarily as an educator and intermediary in the factoring industry, helping companies bridge cash flow gaps through their receivables. His expertise includes: [1, 2]

Target Industries: He provides funding for a variety of sectors including energy, healthcare, manufacturing, and staffing.

Specialized Funding: He specializes in “challenging deals,” such as startups, companies with high customer concentrations, or those with weak personal credit.

Financial Content: Lehnes is a prolific content creator, maintaining a YouTube channel focused on factoring tutorials, market analysis, and audiobook summaries related to leadership and business psychology. [1, 2, 3, 4, 5]

Career & Background

Education: He studied Economics at Lafayette College and attended River Dell Regional High School.

Online Presence: He actively shares insights on LinkedIn and Twitter/X, often discussing economic barometers like lumber price fluctuations and their impact on residential construction.

Public Speaking: He frequently appears on podcasts and webinars, such as the Credit on the Go Podcast, to explain the strategic benefits of factoring. [1, 2, 3, 4, 5]

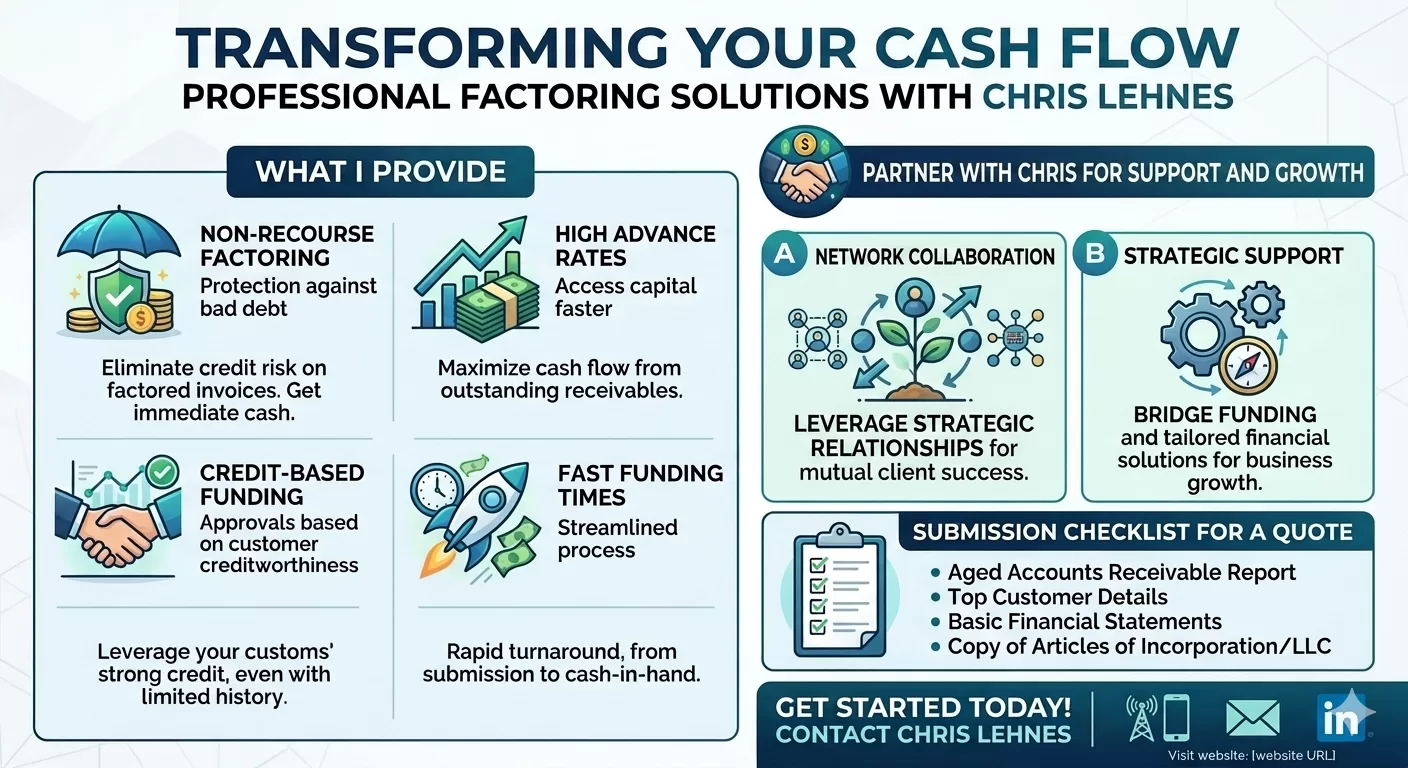

Chris Lehnes manages non-recourse factoring at Versant Funding, where the primary requirement for funding is the credit quality of the account debtor (the customer paying the invoice), rather than the financial strength of the business itself. [1, 2, 3]

Funding Criteria & Terms

Sales Volume: Targets companies with B2B or B2G sales ranging from $100,000 to $30 million per month.

Non-Recourse Protection: Versant assumes the credit risk; if the customer fails to pay due to insolvency, the business is not required to reimburse Versant.

Flexible Concentration: Unlike many lenders, Lehnes often facilitates deals with 100% customer concentration, where a business has only one major client (e.g., a large municipality or multinational corporation).

Funding Speed: Deals can often be funded within one week because traditional underwriting of the borrower’s balance sheet is not required.

Typical Fees: Costs are generally around 2.5% of the invoice amount for each month it remains outstanding.

Excluded Industries: Generally does not factor for the medical (provider-side) or construction industries. [1, 2, 3, 4, 5, 6, 7]

Latest Market Analysis (2025–2026)

Lehnes frequently updates his YouTube and Substack with analyses of the broader economy. Recent highlights include:

Monetary Policy: He recently analyzed the Federal Reserve’s decision to maintain interest rates, discussing the “higher for longer” outlook and its pressure on small business borrowing costs.

Chris Lehnes frequently facilitates complex funding through Versant Funding LLC, often solving liquidity crises for businesses that traditional banks might reject. [1, 2]

Selected Case Studies

$30 Million Furniture Manufacturer (2025): Provided a massive non-recourse facility to replace a non-renewed loan from a previous factor. This deal supported the company through a significant corporate restructuring.

$1.4 Million Auto Equipment Manufacturer (2026): Funded a company supplying global automotive giants. Despite the client’s slow-paying receivables, Versant scaled the facility automatically because the customers were “the strongest on the planet”.

$3 Million Housewares Distributor (2025): Stepped in when the client’s existing factor imposed funding limits that prevented them from fulfilling new orders. Versant consolidated existing loans and provided an advance against all outstanding receivables.

$1.8 Million Adolescent Group Home (2024): Originated a facility for a newly formed social services provider. Because state and county organizations pay slowly, this factoring arrangement provided the necessary liquidity for them to expand into new regions.

Energy Sector Support (2026): Recently focused on the oil and gas industry, helping suppliers bridge working capital gaps caused by the long payment cycles of major energy corporations. [1, 2, 3, 4, 5, 6, 7, 9]

Contact Information

You can reach Chris Lehnes directly for a pre-qualification review or to discuss a specific transaction:

Phone: 203-664-1535

Email: clehnes@VersantFunding.com or chris@chrislehnes.com

Chris Lehnes and Versant Funding prioritize non-recourse factoring because it allows them to fund high-growth or struggling businesses based solely on their customers’ creditworthiness rather than the business’s own financial history. [1, 2]

Recourse vs. Non-Recourse Factoring

The primary difference is who bears the financial risk if a customer fails to pay an invoice. [1, 2]

Recourse Factoring: This is the most common and typically the least expensive option. Under this arrangement, if your customer does not pay their invoice within a set period (usually 60–90 days), your business is responsible for buying back that invoice or replacing it with a fresh one. You retain the ultimate credit risk.

Non-Recourse Factoring: In this model, the factoring company (like Versant) assumes the credit risk. If your customer becomes insolvent or files for bankruptcy, you are not required to pay back the advanced funds. Because the factor takes on more risk, fees are typically higher, and they require strict credit approval of your customers. [1, 2, 3, 4, 5, 6, 7, 8, 9]

Referral Partnership Guidelines

Lehnes actively collaborates with intermediaries, including commercial loan brokers, accountants, and consultants, to source “difficult” deals that traditional banks cannot touch. [1, 2]

Recurring Commissions: Unlike real estate or one-time loan fees, Lehnes offers recurring monthly commissions for the entire life of the deal. If a client factors for three years, the referral partner receives a check every month for those three years.

Strategic Bridge: He encourages partners to use factoring as a short-term bridge (often 24 months) to help companies stabilize until they can qualify for bank financing or complete an equity raise.

Simple Prequalification: To refer a client, you generally only need to provide the client’s industry and a list of their major customers (A/R Aging report). Because Versant does not require full financial audits of the borrower, pre-approval can happen very quickly. [1, 2, 3]

To move forward with a deal for Chris Lehnes at Versant Funding, you typically need a streamlined submission package because they do not underwrite the borrower’s financials—only the collateral (the invoices).

1. Required Documents for a Quote

You can typically get a term sheet or preliminary proposal by submitting just two or three items.

Current A/R Aging Report: This is the most critical document. It must show the names of the customers (account debtors), the amounts they owe, and how long the invoices have been outstanding (0-30, 31-60, 60-90 days).

Customer List with Limit Requests: A list of the specific customers the client wants to factor, including their addresses and the amount of credit limit requested for each. Versant uses this to run credit checks on the debtors.

Sample Invoices: A few examples of the invoices they intend to factor to verify they represent completed work or delivered goods (not progress billing or guaranteed sales).

Simple Application:

Note: You generally do NOT need to submit tax returns, P&L statements, or balance sheets for a preliminary quote, as Versant relies on the credit of the account debtors. [1, 2, 3]

Next Step: If you have a client ready, you can email the A/R Aging Report directly to chris@chrislehnes.com to request a term sheet.

Press Release: (March 26, 2026) Versant Funding LLC is pleased to announce that it has funded a $1.4 Million non-recourse factoring facility to a manufacturer of equipment used by global auto companies.

While our newest client has successfully secured contracts with some of the world’s largest manufacturers, slow-paying accounts receivable are putting pressure on the company’s cash flow and preventing them from taking on new business.

“In evaluating a funding opportunity, Versant focuses exclusively on the quality of our client’s accounts receivable” according to Chris Lehnes, Business Development Officer for Versant Funding, and originator of this transaction. “Since this company’s customers are among the strongest on the planet, our facility will essentially have no cap and will grow automatically as the company’s AR balances increase, providing our client the cash needed to expand.”

About Versant Funding: Versant Funding’s custom Non-Recourse Factoring Facilities have been designed to fill a void in the market by focusing exclusively on the credit quality of a company’s accounts receivable. Versant Funding offers non-recourse factoring solutions to companies with B2B or B2G sales from $100,000 to $30 Million per month. All we care about is the credit quality of the A/R. To learn more contact: Chris Lehnes|203-664-1535 | chris@chrislehnes.com

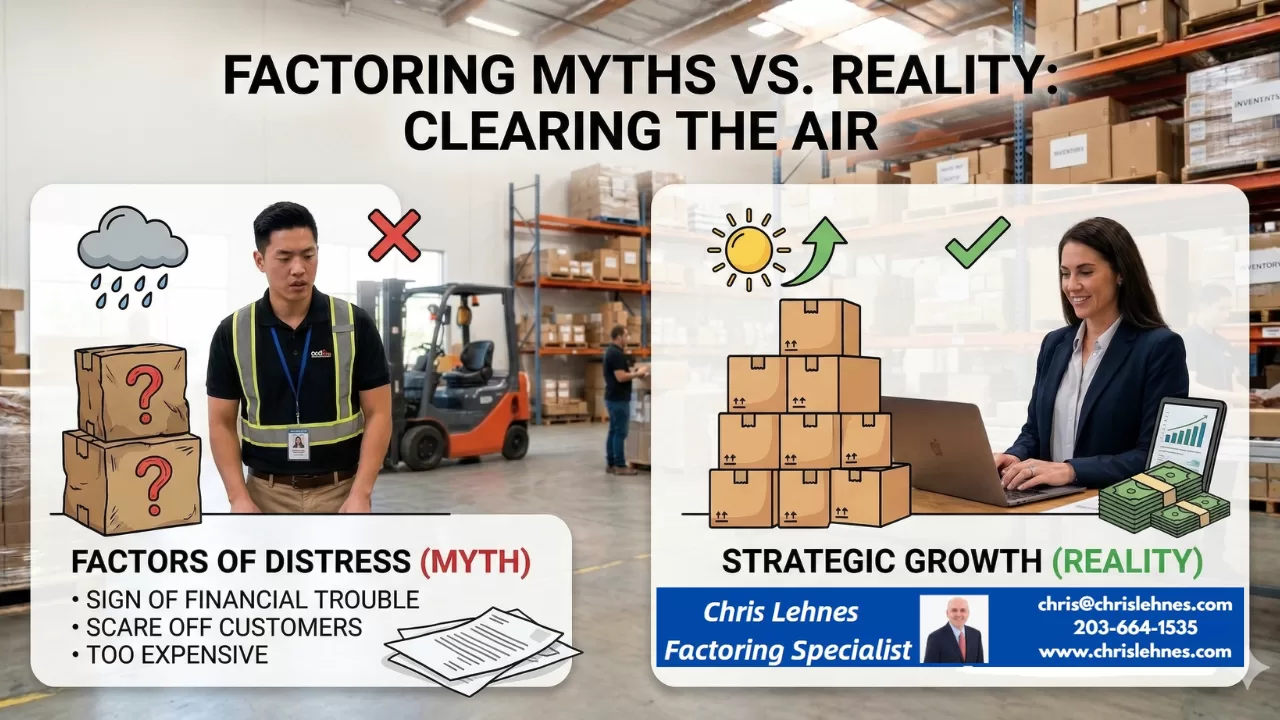

For many distributors, the word “factoring” carries some outdated baggage. If you’re hesitant to pull the trigger, it’s likely because of one of these common misconceptions. Let’s separate the noise from the facts:

The Myth

The Reality

“Factoring is a sign of financial trouble.”

Factoring is a sign of growth. Most companies use factoring because they are growing too fast for their cash flow to keep up. It’s a strategic choice to fuel expansion, not a last-ditch effort to stay afloat.

“My customers will think I’m going under.”

It’s a standard B2B practice. Major retailers and manufacturers deal with factors every day. In many industries, like apparel or electronics distribution, it’s actually the “gold standard” for managing receivables.

“It’s way too expensive.”

Look at the ROI. While the fee (1–3%) is higher than a bank loan, the “cost of waiting” 60 days for a check often means missing out on new inventory or early-pay discounts from your own suppliers that could actually save you more than the factoring fee.

“I’ll lose control of my customer relationships.”

You stay in the driver’s seat. Modern factoring companies act as a professional extension of your back office. They want your customers to stay happy so they keep buying (and paying). You still manage the sales and service; they just handle the math.

“It’s just like a high-interest loan.”

It’s not a loan at all. Because you are selling an asset (your invoice), you aren’t taking on debt. There are no monthly principal or interest payments to worry about—the “payment” comes from your customer, not your bank account.

The “Silent” Benefit: Professional Credit Checks

One “Reality” that distributors often overlook is that a factor acts as a free credit department. Before you ship $50,000 worth of goods to a new client, you can ask your factor to check their credit. If the factor won’t buy the invoice, that’s a massive red flag that you probably shouldn’t be selling to that customer on terms in the first place.

What you should know in selecting a factoring Partner

Choosing a factoring company is like choosing a long-term business partner. The right one will act as your back-office credit department; the wrong one can be an expensive administrative nightmare. Use this checklist to vet potential partners:

1. The Core Logistics

[ ] Industry Expertise: Do they have experience with the specific nuances of distribution (e.g., handling chargebacks, bill-backs, or progressive shipping)?

[ ] Advance Rate: Will they advance at least 80–90% of the invoice value?

[ ] Funding Speed: Can they provide “Same Day” or “Next Day” funding once an invoice is verified?

[ ] Funding Source: Are they a Direct Lender (bank-backed) or an independent factor? (Direct lenders often have lower rates and more stability).

2. Transparency & Fees

[ ] The “All-In” Rate: Ask for a breakdown of all fees. Look out for hidden “junk fees” like application fees, wire fees, or credit check fees.

[ ] Recourse vs. Non-Recourse: * Recourse: You must buy back the invoice if your customer doesn’t pay. (Lower fees).

Non-Recourse: The factor takes the credit risk if the customer goes bankrupt. (Higher fees).

[ ] Volume Requirements: Are there “Monthly Minimums”? If you don’t hit a certain volume, will you be penalized?

3. The “Relationship” Factor

[ ] Dedicated Account Manager: Will you have a single point of contact who knows your business, or a generic 1-800 help desk?

[ ] Customer Interaction Style: How do they contact your customers for verification? You want a partner who is professional and polite, as they represent your brand.

[ ] Technology Integration: Do they sync with your accounting software (QuickBooks, NetSuite, etc.) for easy invoice uploading?

4. Contract Flexibility

[ ] Contract Length: Avoid multi-year lock-ins. Look for month-to-month or one-year terms with clear exit clauses.

[ ] Termination Notice: How much notice is required to leave? (Usually 30–90 days).

[ ] Personal Guarantee: Is a personal guarantee required? (Standard for many small business factors, but worth clarifying).

The 2026 Growth Gap: How Accounts Receivable Factoring Fuels Small Business Success

Factoring: Quick Cash to Kick Off the Year: As we move through 2026, the economic landscape for small businesses is defined by a paradox: opportunity is everywhere, but cash is moving slower than ever. While sectors like high-tech manufacturing and professional services are seeing a resurgence, many entrepreneurs find themselves “asset rich but cash poor.”

You’ve landed the big contract, your team is working overtime, and your sales are climbing. Yet, your bank account doesn’t reflect that success because your capital is trapped in Accounts Receivable (AR). If you’re waiting 30, 60, or even 90 days for clients to pay their invoices, you aren’t just waiting for money—you’re waiting to grow.

This is where Accounts Receivable Factoring becomes a strategic engine for your business.

What is AR Factoring in 2026?

Accounts receivable factoring (or invoice factoring) is not a loan. It is the sale of your outstanding invoices to a third party (a “factor”) at a slight discount in exchange for immediate liquidity.

In 2026, the process has been revolutionized by fintech integrations. Most modern factoring platforms now sync directly with your accounting software (like QuickBooks or Xero), allowing for “one-click” funding that can land in your account within 24 hours.

Why Factoring is the “Secret Weapon” for 2026

While traditional bank loans focus on your credit score and years of profitability, factoring focuses on the creditworthiness of your customers. This makes it an ideal solution for:

Rapidly Growing Startups: When sales outpace your cash reserves.

Seasonal Businesses: Managing the “lumpy” cash flow of peak seasons.

Service Providers: Staffing agencies or consultants who must pay employees weekly but get paid by clients monthly.

3 Ways Factoring Helps You Thrive This Year

1. Turn “Net-90” into “Right Now”

The most significant barrier to growth in 2026 is the “Cash Gap.” If you have $100,000 in open invoices, that’s $100,000 you can’t use to buy inventory, hire talent, or pay for digital marketing. Factoring unlocks up to 90-95% of that value immediately, giving you the agility to say “yes” to new opportunities without checking your balance first.

2. Fuel Expansion Without Adding Debt

In an era of “snagflation”—where mild inflation persists alongside a shifting labor market—loading your balance sheet with high-interest debt can be risky. Because factoring is a purchase of assets, it doesn’t show up as a loan. You are simply accelerating the arrival of money you’ve already earned.

3. Outsourced Credit & Collections

Modern factoring companies do more than just provide cash. They often act as your back-office credit department. In 2026, where business bankruptcies are slightly on the rise, having a partner who vets the credit risk of your potential clients is a massive competitive advantage. They handle the collections, freeing you up to focus on your product.

Is it Right for You?

To help you decide, here is a quick comparison of how factoring stacks up against traditional financing in today’s market:

Feature

AR Factoring

Traditional Bank Loan

Speed

24–48 Hours

3–6 Weeks

Approval Basis

Customer’s Credit

Your Credit & Collateral

Debt

None (Asset Sale)

Increases Liabilities

Flexibility

Scales with Sales

Fixed Credit Limit

Cost

1%–5% Service Fee

Interest Rate + Fees

Final Thoughts: Don’t Let Your Invoices Hold You Back

In 2026, the winners won’t necessarily be the companies with the biggest ideas, but those with the highest liquidity. AR factoring provides a bridge over the cash flow gaps that sink 82% of small businesses. It turns your hard work into immediate fuel.

We fund tough deals and focus on the quality of your client’s accounts receivable, ignoring their financial condition. This enables us to move quickly and fund qualified businesses including Manufacturers, Distributors and a wide variety of Service Businesses in as quick as a week. Contact me today to learn if your client is a fit.