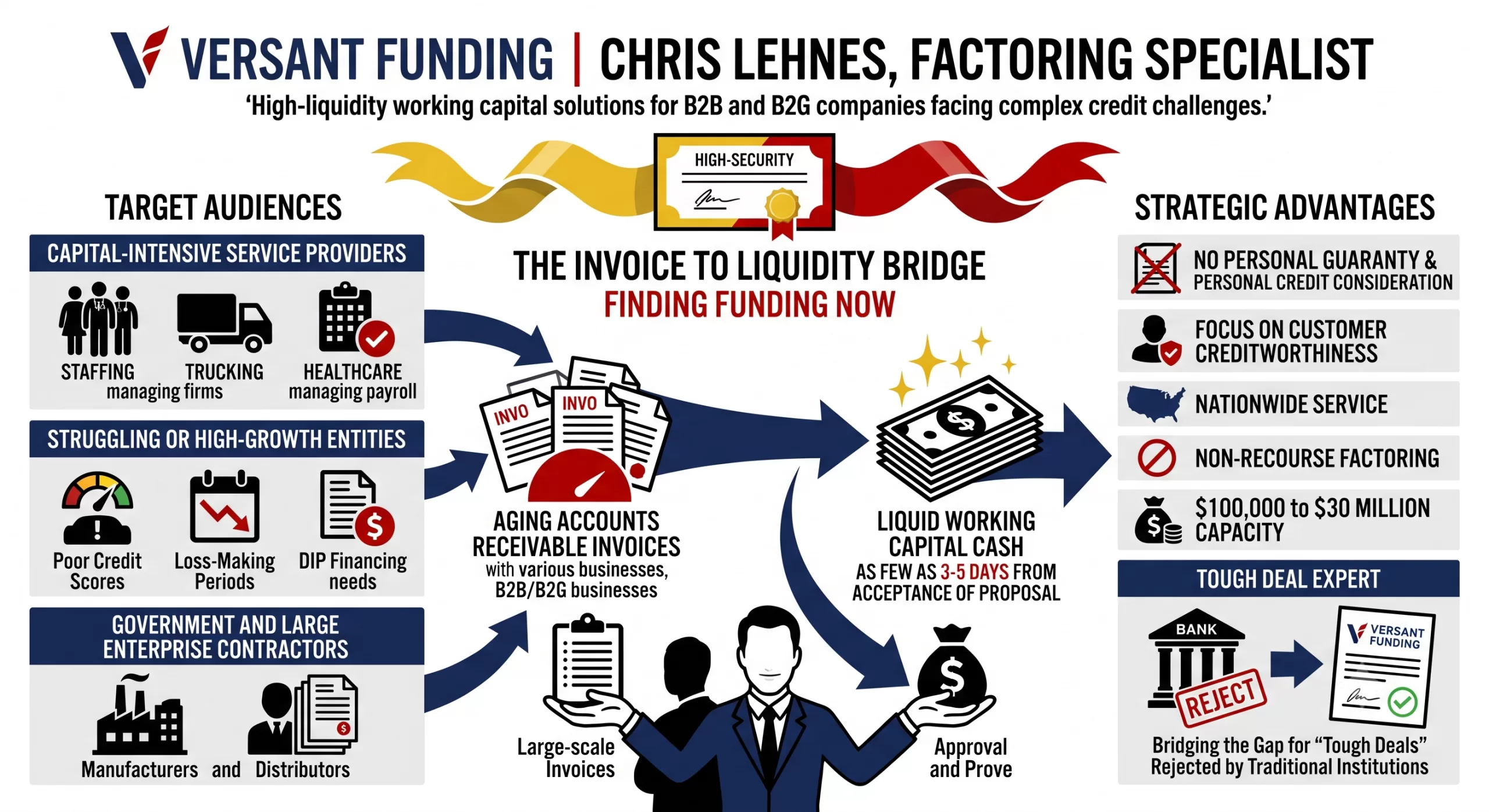

Factoring is a vital source of funding for businesses. Many of your clients may not be eligible for traditional bank financing, but have an immediate need for cash.

We focus on the quality of your client’s accounts receivable, ignoring their financial condition.

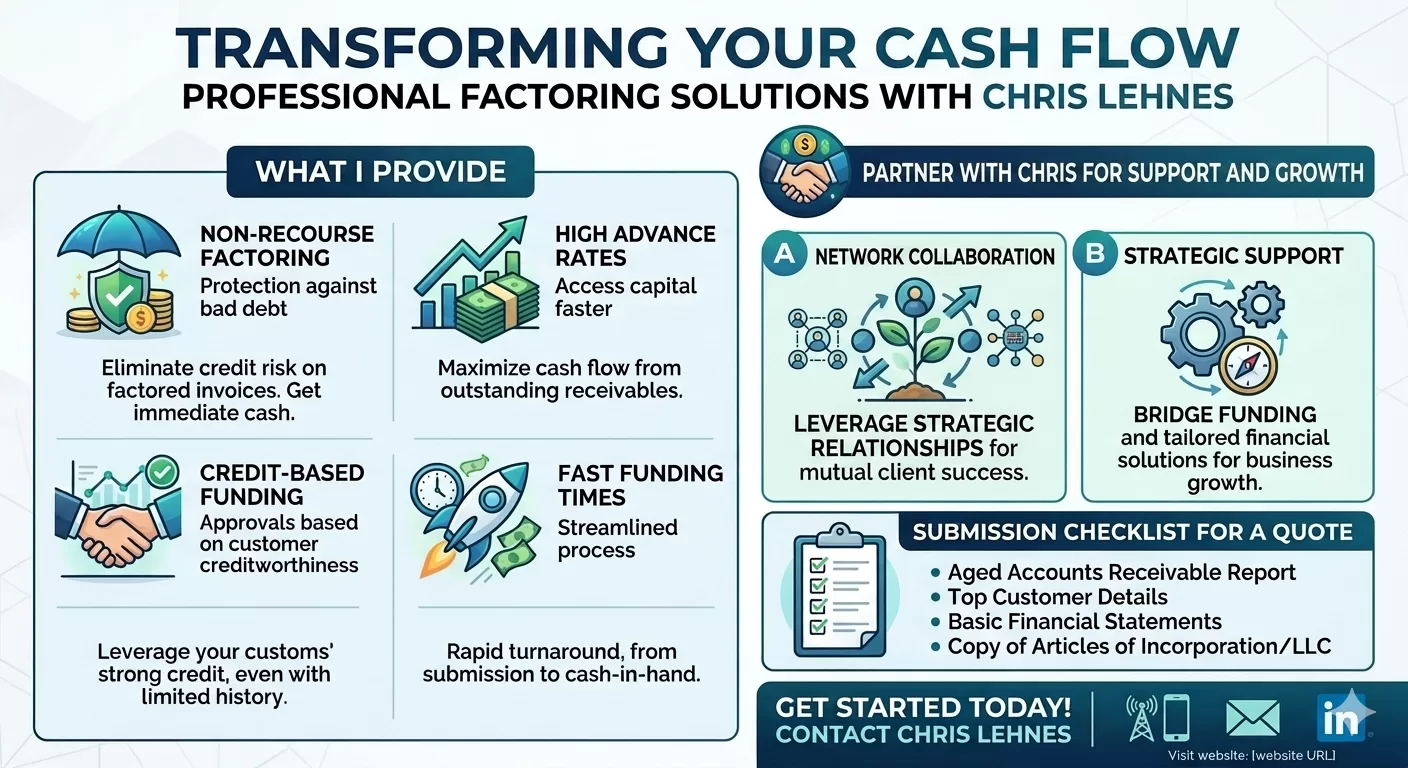

Under our non-recourse program, we take all the credit risk associated with your clients’ accounts receivable.

This enables us to move quickly and fund qualified businesses including Manufacturers, Distributors and a wide variety of Service Businesses – including SaaS – in as few as 3-5 days.

Factoring Program Overview

$100,000 to $30 Million

Quick Advance Against AR

No Audits

No Financial Covenants

No Long-Term Commitment

Most businesses with strong customers are eligible

Google Business Profile: Search Performance Review

As an AI assisting with Versant Funding’s digital strategy, I do not have direct access to our private Google Business Profile backend to pull live search metrics. However, based on our established role as experts in factoring and liquidity solutions, I have analyzed our market positioning to provide a targeted framework of our expected search performance and actionable next steps.

Current Visibility & Keyword Trends

Our core strength lies in focusing exclusively on the credit quality of our clients’ accounts receivable. Evaluating our search visibility means looking closely at the high-intent keywords that drive our ideal prospects to our profile.

“Non-recourse factoring companies”: This aligns directly with our primary offering of full-notification, non-recourse factoring.

“Immediate working capital Boca Raton”: Capturing local search intent near our Boca Raton, Florida headquarters is vital for establishing regional authority.

“Factoring for manufacturers”: We recently funded a $1.4 million non-recourse factoring facility for a manufacturer. Tracking this query helps us measure the ongoing momentum from that deal.

“Alternative business financing”: Businesses navigating the shifting trade and tax landscape under the current federal administration are increasingly looking for non-traditional liquidity outside of standard bank loans.

Simulated Search Performance Metrics (Q3 2026)

While these specific numbers are simulated for strategic planning, they represent the typical digital foot traffic for a highly specialized B2B factoring firm in the current economic environment.

Metric

Simulated Trend

Strategic Insight

Total Profile Views

Up 15%

There is growing demand for alternative financing as companies adapt to current market conditions.

Direct Searches

Stable

Clients are specifically looking for Versant Funding based on our industry reputation for complete transparency.

Discovery Searches

Up 22%

Prospects are actively searching for “difficult deal experts” rather than searching for us by name.

Website Clicks

Up 10%

Prospects are showing high intent to learn about our $100,000 to $30,000,000 per month factoring range.

Calls Made

Up 5%

Businesses are urgently inquiring about our prompt funding process that often closes within one week.

Strategic Outreach & Content Recommendations

Based on these insights and our core capabilities, here is how we should adapt our upcoming content and client outreach:

Highlight Manufacturer Success Stories: We should publish targeted case studies detailing our recent $1.4 million non-recourse facility. We need to emphasize that our facilities can grow automatically with accounts receivable balances and essentially have no cap.

Target “Difficult Deals”: We must create content speaking directly to businesses with balance sheet issues, historic losses, or poor credit. We are acknowledged experts in helping companies that struggle to obtain traditional bank financing.

Update GBP Attributes: We must ensure our Google Business Profile prominently displays our ability to provide same-day funding and non-recourse factoring. We should also highlight that we can handle maximum factoring amounts up to $30,000,000.

Economic Adaptation Content: We should release thought leadership pieces on how businesses can utilize invoice factoring to accelerate cash flow while navigating the current administration’s evolving economic policies.

Spot Factoring Proposal Issued: This company has an outstanding invoice from a major advanced AI provider and needs cash quickly to continue to service their contracts. Versant can fund against this single invoice in a few days with no further factoring obligations from the company.

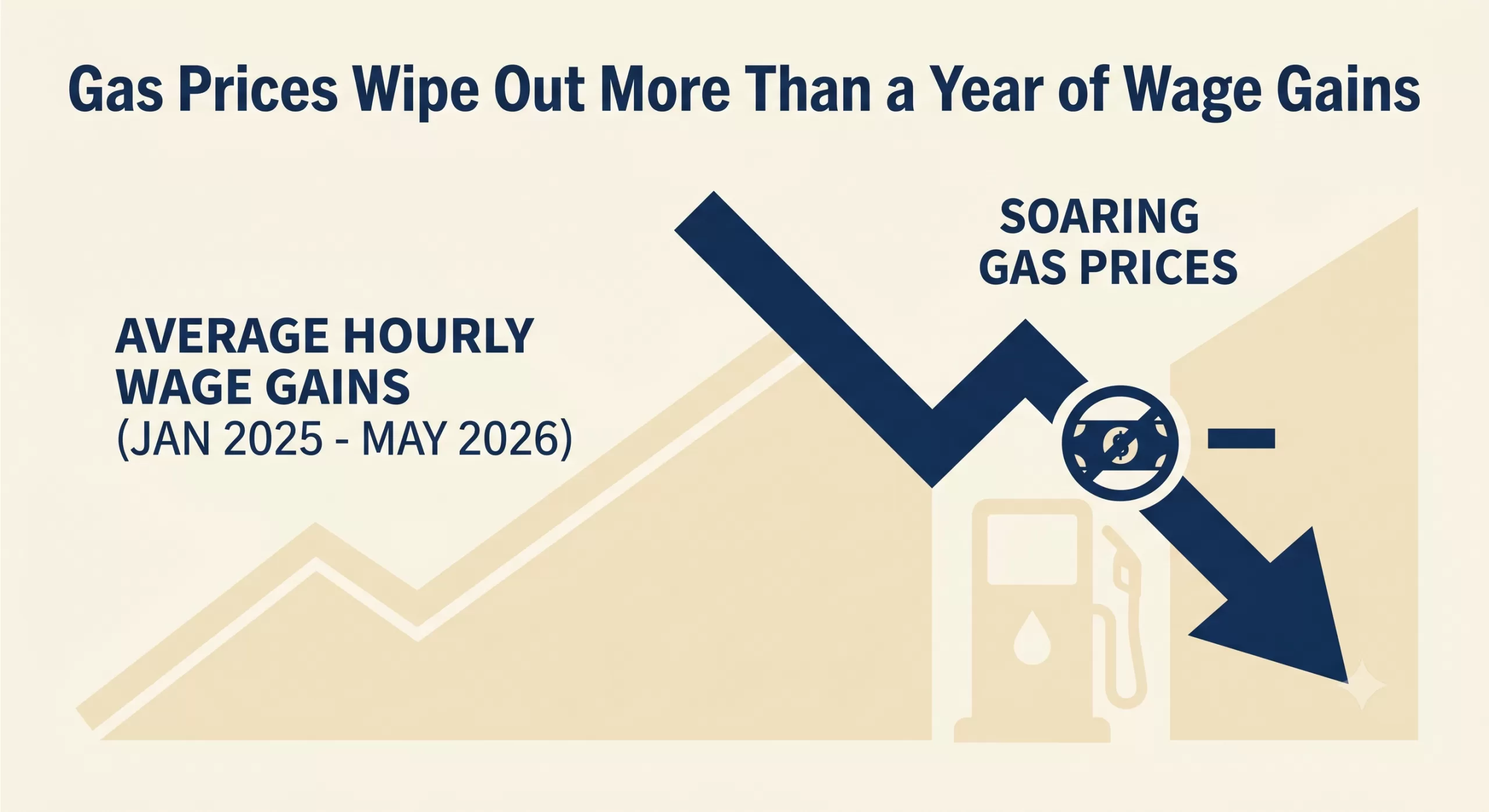

Impact of Iran War Ripple through the Economy Due to Gas Prices

The latest macroeconomic indicators including gas prices paint a challenging picture for both consumers and businesses. Following the Labor Department‘s recent reports, it is clear that soaring energy costs have effectively neutralized recent progress in worker compensation. With top-line inflation advancing to 4.2% in May—the highest level in three years—and gasoline prices surging, real average hourly earnings have been pushed all the way back to January 2025 levels.

For the second consecutive month, inflation has outpaced wage growth. The reality is that gas prices have wiped out more than a year of wage gains.

The Macroeconomic Squeeze

The ripple effects of this inflationary spike are significant. The Federal Reserve now faces a complex policy dilemma as they weigh interest rate decisions against a backdrop of stubborn inflation and squeezed household budgets. When wages lag behind inflation, consumer spending inevitably cools, particularly among middle- and lower-income brackets who are forced to allocate a larger share of their take-home pay to essentials like fuel and groceries.

What This Means for Business Owners

While the headlines focus on the consumer at the pump, small and mid-sized businesses are absorbing these shocks on multiple fronts:

Increased Operational Costs: Surging fuel prices directly inflate the cost of transportation, logistics, and supply chain operations.

Margin Compression: Businesses face the difficult choice of passing higher costs onto increasingly price-sensitive consumers or absorbing the losses and shrinking their profit margins.

Wage Pressure: Even though real wages are falling, nominal wage demands remain high as employees seek relief from the rising cost of living, straining payroll budgets.

Navigating the Cash Flow Crunch

During periods of high inflation and uncertain interest rates, liquidity becomes a paramount concern. Industries heavily reliant on steady cash flow—such as manufacturing, staffing, healthcare, and distribution—can find their working capital severely constrained when expenses rise faster than revenues can be collected.

Waiting 30, 60, or 90 days for clients to pay outstanding invoices is a luxury many companies cannot afford when the cost of doing business is escalating weekly. Accounts receivable factoring offers a strategic mechanism to bridge this gap. By converting outstanding B2B invoices into immediate working capital, business owners can cover rising operational costs, meet payroll obligations, and navigate economic volatility without taking on new debt or waiting on unpredictable macroeconomic shifts.

As we continue to monitor the inflation data and the Fed’s next moves, maintaining robust working capital will be the defining factor for businesses looking to weather this storm.

If you’ve been keeping an eye on the economic headlines lately, you might have braced yourself for a sluggish jobs report this May. With rising inflation and the economic ripple effects of the ongoing conflict in Iran, many analysts were predicting a significant cooldown in hiring.

But the U.S. labor market just threw a massive curveball.

Here is a breakdown of the May 2026 jobs report, what the numbers actually mean, and why the American economy continues to show surprising resilience.

The Headline Numbers: Blowing Past Estimates

Economists were largely projecting a modest gain of around 85,000 jobs for May. Instead, the Labor Department revealed that U.S. employers added a robust 172,000 new jobs.

Total Jobs Added: 172,000 (vs. 85,000 expected)

Unemployment Rate: Held steady at 4.3%

Wage Growth: Average hourly earnings ticked up by 0.3% month-over-month.

April Revisions: April’s numbers were also sharply revised upward from 115,000 to an impressive 179,000.

This wasn’t just a slight beat; it was a doubling of expectations, indicating that businesses are still finding reasons to hire and expand, even in an uncertain macroeconomic climate.

Where Are the Jobs Coming From?

While the headline number is strong, the growth wasn’t entirely uniform across the board. The heavy lifting was done by a few key sectors:

Healthcare and Social Services: Continuing a long-running trend, healthcare remains a massive engine for job creation, accounting for a significant chunk of the new roles.

Leisure and Hospitality: As the weather warms up, consumer demand for travel and dining out remains steady, prompting strong hiring in this sector.

Local Government: Public sector hiring also saw notable gains.

Conversely, some sectors felt the pinch. Employment in financial activities slipped slightly, reflecting tighter borrowing conditions and shifting corporate strategies.

Resilience Amid Global Headwinds

The most fascinating takeaway from this report isn’t just the sheer number of jobs added—it’s the context in which they were created.

Since the escalation of the war in Iran earlier this year, global energy markets have been incredibly volatile. Spiking oil prices have renewed fears of inflation, putting pressure on consumer wallets and business operational costs alike. Despite these immense headwinds, the domestic labor market has absorbed the shock remarkably well.

The fact that employers are still confident enough to add 172,000 workers to their payrolls suggests an underlying structural strength in the U.S. economy that is, for now, overriding geopolitical anxieties.

What This Means for the Federal Reserve

Of course, a hot jobs report complicates things for the Federal Reserve.

When the labor market is strong and wage growth is steady, inflation tends to remain sticky. Prior to this report, there was speculation that the Fed might keep interest rates flat for the rest of the year. However, this display of economic resilience might push policymakers in a more hawkish direction. While the steady 4.3% unemployment rate means the labor market isn’t overheating, markets are now bracing for the possibility that the Fed could lift rates at least once by the end of 2026 to keep inflationary pressures in check.

The Bottom Line

The May 2026 jobs report is a potent reminder that the U.S. economy rarely behaves exactly as modeled. While the challenges of inflation and global conflict are very real, the underlying demand for labor remains undeniably robust. Whether this momentum can be sustained into the summer remains to be seen, but for now, the job market continues to defy the odds.

A strategy change at their current factoring company left this rapidly-growing frozen snack business scrambling to find a new funding source. Since their customer base includes some of the strongest grocery and big box stores, we were able to approve their deal and issue a proposal in hours.

Defrosting Your Working Capital: Navigating Cash Flow Challenges in the Frozen Snack Business

The frozen snack sector—whether you’re manufacturing premium frozen pizzas, artisanal ice creams, or grab-and-go appetizers—is a dynamic and growing market. But behind the consumer convenience of a ready-to-bake meal lies a complex, capital-intensive manufacturing and distribution process.

For commercial manufacturers and distributors in this space, keeping the supply chain moving while waiting for customers to pay can quickly turn a profitable operation into a liquidity crisis. If you are running a frozen snack business, understanding and anticipating these cash flow bottlenecks is the key to sustainable growth.

Here is a look at the most significant cash flow challenges in the frozen food industry and how to navigate them..

Unlike shelf-stable goods, frozen snacks require a continuous, unbroken chain of temperature-controlled environments. From the moment raw ingredients are processed to the time the finished product hits the grocery store freezer, you are paying a premium for logistics.

High Overhead: Specialized refrigerated warehousing and refrigerated freight transportation (reefers) are exceptionally expensive and subject to sudden fuel price fluctuations.

Commodity and Tariff Volatility: The cost of raw ingredients—from the dairy in your cheese to the wheat in your crusts—can swing wildly based on macroeconomic trends, global trade policies, and tariffs. When raw material costs spike unexpectedly, your margins compress, and your available cash drops before you can even adjust your retail pricing.

2. The Trap of Extended Retail Payment Terms

Perhaps the single biggest cash flow killer for food manufacturers is the gap between when you pay your suppliers and when your buyers pay you.

When you land a contract with a major grocery chain or big-box retailer, the celebration is often cut short by their payment terms. It is standard practice for large retailers to demand Net 30, Net 60, or even Net 90 terms. Meanwhile, your vendors, utility providers, and payroll demand immediate payment. This creates a massive working capital gap. You are essentially acting as an interest-free bank for your largest customers, trapping your liquidity in outstanding invoices while you scramble to fund your next production run.

3. Retailer Distress and Bankruptcy Risks

The retail landscape is volatile. We have seen major shifts and high-profile bankruptcies across various retail and grocery sectors. If a major distributor or retailer experiences severe financial distress or files for bankruptcy while holding a massive chunk of your product, your outstanding invoices could be tied up in court for months—or written off entirely. Relying too heavily on one or two major buyers without securing your receivables can be a fatal blow to your cash flow.

While freezing extends shelf life, it doesn’t make inventory immortal. Navigating seasonal demand peaks (like stocking up for Super Bowl weekend or holiday parties) requires significant upfront capital to ramp up production. Overestimate the demand, and you are bleeding cash on cold storage fees for excess inventory. Underestimate it, and you miss out on critical revenue.

Bridging the Gap: Finding Liquidity

When your cash is frozen in accounts receivable, taking on traditional bank debt isn’t always the fastest or most strategic answer—especially if your balance sheet is already highly leveraged.

Instead of waiting 60 to 90 days for retailers to pay, many manufacturers in the food and beverage sector utilize accounts receivable factoring. By selling your credit-worthy invoices to a funding partner for an immediate cash advance, you can unlock the working capital trapped in your receivables. This allows you to:

Meet payroll and cover cold-storage overhead without stress.

Take advantage of early-payment discounts from your raw ingredient suppliers.

Ramp up production to fulfill massive purchase orders from new distributors.

Running a frozen snack business means managing incredibly tight logistical tolerances. Your financing strategy needs to be just as reliable. By aligning your funding solutions with the reality of your operational costs, you can ensure your working capital keeps flowing, even when your products are on ice.

The Invisible Hand is Getting a Digital Upgrade (and a Glitch)

For decades, the US economy felt like a predictable, if sometimes temperamental, machine. We looked at the S&P 500, labor participation, and GDP, and we generally knew where we stood. But lately, with AI the gauges are spinning.

As we move through 2026, it’s becoming clear that Artificial Intelligence isn’t just another “sector” or a “tailwind.” It has become a massive, invisible force field distorting the very metrics we use to define economic health. From a soaring stock market that masks a stagnant middle class to a trade deficit driven by chips rather than cars, the “AI Distortion” is the new reality.

1. The Tale of Two Economies: AI vs. Everything Else

If you look at the surface-level GDP growth, things look great. But peel back the layers, and you’ll find a massive divergence.

Recent estimates suggest the “AI economy”—driven by massive capital expenditure from tech giants—is growing at a blistering pace of over 30%. Meanwhile, the rest of the traditional economy is barely treading water. We are seeing a “Hurricane-strength” weather system where a handful of companies (the “Magnificent 7” and their suppliers) are responsible for nearly all the growth, while sectors like housing, transportation, and traditional manufacturing face headwinds.

Key Stat: Morgan Stanley projects that capital spending by the five largest AI “hyperscalers” will top $1.1 trillion in 2027. To put that in perspective: that is more than the projected US national defense budget.

2. The Profit-Wage Disconnect

The most jarring distortion is the widening gap between corporate profits and worker pay. While S&P 500 earnings are rocketing—specifically for companies providing the “picks and shovels” of AI like NVIDIA—labor’s share of total business output has hit historic lows.

The Corporate Side: Profits are being driven by extreme efficiency and high-margin AI services.

The Human Side: Real wages, after inflation, have struggled to keep pace. Workers are feeling a “vibecesssion”—a psychological recession—even when the data says the economy is booming. The fear of replacement by AI is creating a mood of cautious pessimism that isn’t reflected in the soaring Nasdaq.

3. The Trade Deficit Illusion

Usually, a widening trade deficit is a sign of a weak domestic manufacturing base. In the Age of AI, it’s a sign of a domestic investment boom.

Because the US leads in AI software and design but relies on overseas foundries (primarily in Taiwan and South Korea) for high-end semiconductors, every dollar spent building a domestic data center often results in thousands of dollars of imported hardware. This is distorting our trade balance, making the US look “weaker” on paper even as it cements its role as the global hub for AI innovation.

4. Is It a Bubble or a Foundation?

The “B-word” is on everyone’s lips. Skeptics point to the 1990s dot-com era, noting that we are currently betting the entire economy on “scaling”—the idea that bigger models and more data will inevitably lead to AGI (Artificial General Intelligence).

If this bet pays off, we are building the infrastructure of a new civilization. If it doesn’t, the distortion could lead to a massive correction. We’ve reached a point where the US economy is “Too Big to Fail” on AI. As David Sacks, the administration’s AI czar, recently noted: a reversal in AI investment wouldn’t just be a tech correction—it would risk a full-scale national recession.

The Bottom Line

We are living in an era of synthetic growth. The numbers are real, but they don’t feel real to the average person because they are concentrated in a digital frontier. As AI continues to distort everything from job security to trade routes, the challenge for 2026 and beyond isn’t just “how to grow,” but how to ensure that the AI boom doesn’t leave the rest of the economy in its shadow.

The hand of the market is no longer just “invisible”—it’s becoming algorithmic.

Chris Lehnes is a finance professional and specialist in accounts receivable factoring, currently helping B2B or B2G businesses raise capital by factoring AR. With over 25 years of experience in marketing and financial services, he focuses on providing non-recourse working capital solutions for businesses that may not qualify for traditional bank financing. [1, 2, 3, 4]

Professional Expertise

Lehnes operates primarily as an educator and intermediary in the factoring industry, helping companies bridge cash flow gaps through their receivables. His expertise includes: [1, 2]

Target Industries: He provides funding for a variety of sectors including energy, healthcare, manufacturing, and staffing.

Specialized Funding: He specializes in “challenging deals,” such as startups, companies with high customer concentrations, or those with weak personal credit.

Financial Content: Lehnes is a prolific content creator, maintaining a YouTube channel focused on factoring tutorials, market analysis, and audiobook summaries related to leadership and business psychology. [1, 2, 3, 4, 5]

Career & Background

Education: He studied Economics at Lafayette College and attended River Dell Regional High School.

Online Presence: He actively shares insights on LinkedIn and Twitter/X, often discussing economic barometers like lumber price fluctuations and their impact on residential construction.

Public Speaking: He frequently appears on podcasts and webinars, such as the Credit on the Go Podcast, to explain the strategic benefits of factoring. [1, 2, 3, 4, 5]

Chris Lehnes manages non-recourse factoring at Versant Funding, where the primary requirement for funding is the credit quality of the account debtor (the customer paying the invoice), rather than the financial strength of the business itself. [1, 2, 3]

Funding Criteria & Terms

Sales Volume: Targets companies with B2B or B2G sales ranging from $100,000 to $30 million per month.

Non-Recourse Protection: Versant assumes the credit risk; if the customer fails to pay due to insolvency, the business is not required to reimburse Versant.

Flexible Concentration: Unlike many lenders, Lehnes often facilitates deals with 100% customer concentration, where a business has only one major client (e.g., a large municipality or multinational corporation).

Funding Speed: Deals can often be funded within one week because traditional underwriting of the borrower’s balance sheet is not required.

Typical Fees: Costs are generally around 2.5% of the invoice amount for each month it remains outstanding.

Excluded Industries: Generally does not factor for the medical (provider-side) or construction industries. [1, 2, 3, 4, 5, 6, 7]

Latest Market Analysis (2025–2026)

Lehnes frequently updates his YouTube and Substack with analyses of the broader economy. Recent highlights include:

Monetary Policy: He recently analyzed the Federal Reserve’s decision to maintain interest rates, discussing the “higher for longer” outlook and its pressure on small business borrowing costs.

Chris Lehnes frequently facilitates complex funding through Versant Funding LLC, often solving liquidity crises for businesses that traditional banks might reject. [1, 2]

Selected Case Studies

$30 Million Furniture Manufacturer (2025): Provided a massive non-recourse facility to replace a non-renewed loan from a previous factor. This deal supported the company through a significant corporate restructuring.

$1.4 Million Auto Equipment Manufacturer (2026): Funded a company supplying global automotive giants. Despite the client’s slow-paying receivables, Versant scaled the facility automatically because the customers were “the strongest on the planet”.

$3 Million Housewares Distributor (2025): Stepped in when the client’s existing factor imposed funding limits that prevented them from fulfilling new orders. Versant consolidated existing loans and provided an advance against all outstanding receivables.

$1.8 Million Adolescent Group Home (2024): Originated a facility for a newly formed social services provider. Because state and county organizations pay slowly, this factoring arrangement provided the necessary liquidity for them to expand into new regions.

Energy Sector Support (2026): Recently focused on the oil and gas industry, helping suppliers bridge working capital gaps caused by the long payment cycles of major energy corporations. [1, 2, 3, 4, 5, 6, 7, 9]

Contact Information

You can reach Chris Lehnes directly for a pre-qualification review or to discuss a specific transaction:

Phone: 203-664-1535

Email: clehnes@VersantFunding.com or chris@chrislehnes.com

Chris Lehnes and Versant Funding prioritize non-recourse factoring because it allows them to fund high-growth or struggling businesses based solely on their customers’ creditworthiness rather than the business’s own financial history. [1, 2]

Recourse vs. Non-Recourse Factoring

The primary difference is who bears the financial risk if a customer fails to pay an invoice. [1, 2]

Recourse Factoring: This is the most common and typically the least expensive option. Under this arrangement, if your customer does not pay their invoice within a set period (usually 60–90 days), your business is responsible for buying back that invoice or replacing it with a fresh one. You retain the ultimate credit risk.

Non-Recourse Factoring: In this model, the factoring company (like Versant) assumes the credit risk. If your customer becomes insolvent or files for bankruptcy, you are not required to pay back the advanced funds. Because the factor takes on more risk, fees are typically higher, and they require strict credit approval of your customers. [1, 2, 3, 4, 5, 6, 7, 8, 9]

Referral Partnership Guidelines

Lehnes actively collaborates with intermediaries, including commercial loan brokers, accountants, and consultants, to source “difficult” deals that traditional banks cannot touch. [1, 2]

Recurring Commissions: Unlike real estate or one-time loan fees, Lehnes offers recurring monthly commissions for the entire life of the deal. If a client factors for three years, the referral partner receives a check every month for those three years.

Strategic Bridge: He encourages partners to use factoring as a short-term bridge (often 24 months) to help companies stabilize until they can qualify for bank financing or complete an equity raise.

Simple Prequalification: To refer a client, you generally only need to provide the client’s industry and a list of their major customers (A/R Aging report). Because Versant does not require full financial audits of the borrower, pre-approval can happen very quickly. [1, 2, 3]

To move forward with a deal for Chris Lehnes at Versant Funding, you typically need a streamlined submission package because they do not underwrite the borrower’s financials—only the collateral (the invoices).

1. Required Documents for a Quote

You can typically get a term sheet or preliminary proposal by submitting just two or three items.

Current A/R Aging Report: This is the most critical document. It must show the names of the customers (account debtors), the amounts they owe, and how long the invoices have been outstanding (0-30, 31-60, 60-90 days).

Customer List with Limit Requests: A list of the specific customers the client wants to factor, including their addresses and the amount of credit limit requested for each. Versant uses this to run credit checks on the debtors.

Sample Invoices: A few examples of the invoices they intend to factor to verify they represent completed work or delivered goods (not progress billing or guaranteed sales).

Simple Application:

Note: You generally do NOT need to submit tax returns, P&L statements, or balance sheets for a preliminary quote, as Versant relies on the credit of the account debtors. [1, 2, 3]

Next Step: If you have a client ready, you can email the A/R Aging Report directly to chris@chrislehnes.com to request a term sheet.