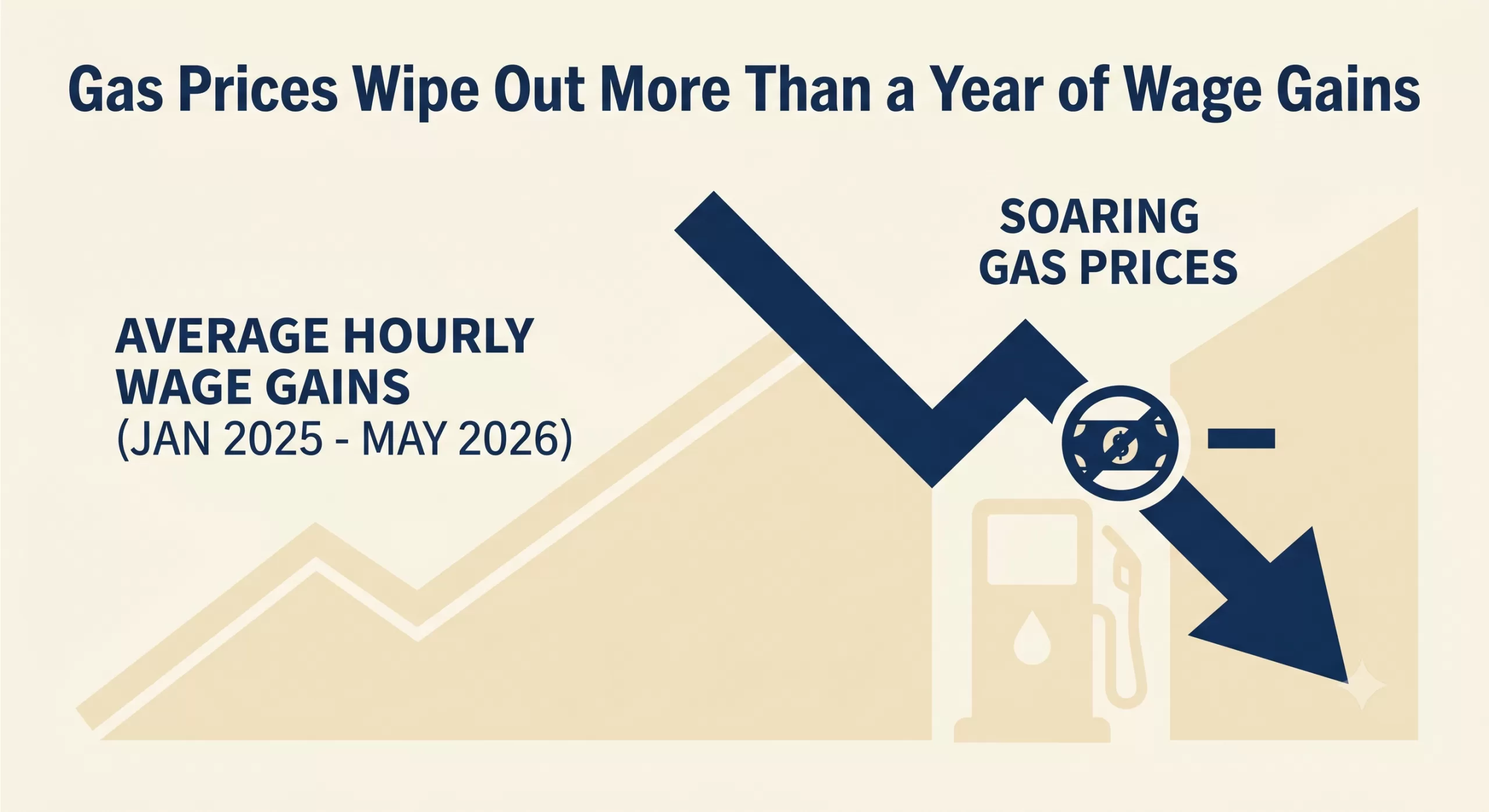

Impact of Iran War Ripple through the Economy Due to Gas Prices

The latest macroeconomic indicators including gas prices paint a challenging picture for both consumers and businesses. Following the Labor Department‘s recent reports, it is clear that soaring energy costs have effectively neutralized recent progress in worker compensation. With top-line inflation advancing to 4.2% in May—the highest level in three years—and gasoline prices surging, real average hourly earnings have been pushed all the way back to January 2025 levels.

For the second consecutive month, inflation has outpaced wage growth. The reality is that gas prices have wiped out more than a year of wage gains.

The Macroeconomic Squeeze

The ripple effects of this inflationary spike are significant. The Federal Reserve now faces a complex policy dilemma as they weigh interest rate decisions against a backdrop of stubborn inflation and squeezed household budgets. When wages lag behind inflation, consumer spending inevitably cools, particularly among middle- and lower-income brackets who are forced to allocate a larger share of their take-home pay to essentials like fuel and groceries.

What This Means for Business Owners

While the headlines focus on the consumer at the pump, small and mid-sized businesses are absorbing these shocks on multiple fronts:

Increased Operational Costs: Surging fuel prices directly inflate the cost of transportation, logistics, and supply chain operations.

Margin Compression: Businesses face the difficult choice of passing higher costs onto increasingly price-sensitive consumers or absorbing the losses and shrinking their profit margins.

Wage Pressure: Even though real wages are falling, nominal wage demands remain high as employees seek relief from the rising cost of living, straining payroll budgets.

Navigating the Cash Flow Crunch

During periods of high inflation and uncertain interest rates, liquidity becomes a paramount concern. Industries heavily reliant on steady cash flow—such as manufacturing, staffing, healthcare, and distribution—can find their working capital severely constrained when expenses rise faster than revenues can be collected.

Waiting 30, 60, or 90 days for clients to pay outstanding invoices is a luxury many companies cannot afford when the cost of doing business is escalating weekly. Accounts receivable factoring offers a strategic mechanism to bridge this gap. By converting outstanding B2B invoices into immediate working capital, business owners can cover rising operational costs, meet payroll obligations, and navigate economic volatility without taking on new debt or waiting on unpredictable macroeconomic shifts.

As we continue to monitor the inflation data and the Fed’s next moves, maintaining robust working capital will be the defining factor for businesses looking to weather this storm.

Today marks a significant turning point in European monetary policy: the European Central Bank (ECB) has officially reversed course, raising its key interest rates for the first time in nearly three years.

After an extended period of cuts and holds, the era of steadily declining borrowing costs in the Eurozone has temporarily hit a wall. Let’s break down the data, the underlying causes, and what this means for the broader economy.

The Decision: By the Numbers

In a move widely anticipated by financial markets and economists, the ECB’s Governing Council elected to raise its key interest rates by 0.25 percentage points (25 basis points).

Here is a quick breakdown of where the central bank’s key rates stand effective immediately:

ECB Facility

Previous Rate

New Rate (June 2026)

Deposit Facility

2.00%

2.25%

Main Refinancing Operations

2.15%

2.40%

Marginal Lending Facility

2.40%

2.65%

This decision officially ends a cycle that began back in September 2023, representing a decisive reaction to shifting economic realities on the ground.

Why is the ECB Hiking Rates Now?

The ECB has a single, primary mandate: to maintain price stability by targeting an inflation rate of 2.0%. The decision to hike rates is a direct response to recent data showing that inflation is moving in the wrong direction.

Headline Inflation Surge: In May 2026, Eurozone consumer prices rose to 3.2% year-over-year. This marks a significant acceleration from earlier in the year and blows past the central bank’s comfort zone.

The Energy Shock: A major driver behind this inflationary spike is the ongoing geopolitical conflict in the Middle East. Disrupted shipping routes and volatile commodity markets caused energy prices to jump nearly 11% last month compared to the same period last year.

Core Inflation Creep: The energy shock isn’t isolated. Core inflation—which strips out highly volatile food and energy costs—rose to 2.5%. This indicates that higher energy overheads are beginning to bleed into the broader costs of everyday goods and services.

What Does This Mean for the Eurozone?

When the ECB pulls the interest rate lever, the effects ripple through the entire financial system. Here is what to expect:

More Expensive Borrowing: For consumers and businesses, the cost of credit is going up. Homeowners holding variable-rate or tracker mortgages will see their monthly repayments increase almost immediately.

A Squeeze on Growth: While higher interest rates are necessary to cool down inflation, they simultaneously suppress economic activity. Reflecting the strain of higher energy costs and tighter financial conditions, the ECB has already revised its growth forecasts downward, anticipating the Eurozone economy will grow by a sluggish 0.8% in 2026.

Currency Impacts: Higher interest rates generally make a currency more attractive to yield-seeking investors. A hawkish stance from the ECB typically provides upward support for the Euro (EUR) against other major currencies, provided the broader economic outlook doesn’t deteriorate too sharply.

Looking Ahead: Is This the Start of a New Cycle?

The prevailing question for markets is whether this is a isolated adjustment or the beginning of a new tightening cycle.

Current market consensus suggests this won’t be a one-off event. Many analysts are pricing in at least one or two more quarter-point increases before the end of the year, which could bring the deposit rate up to 2.50% or 2.75%. However, ECB leadership has emphasized that future decisions will remain strictly “data-dependent.” The Governing Council will evaluate the ongoing impact of energy prices, geopolitical stability, and wage growth on a meeting-by-meeting basis.

The takeaway is clear: the ECB’s latest pivot highlights how rapidly external shocks can upend economic stability, forcing central banks to prioritize fighting inflation over stimulating growth.

If you’ve been keeping an eye on the economic headlines lately, you might have braced yourself for a sluggish jobs report this May. With rising inflation and the economic ripple effects of the ongoing conflict in Iran, many analysts were predicting a significant cooldown in hiring.

But the U.S. labor market just threw a massive curveball.

Here is a breakdown of the May 2026 jobs report, what the numbers actually mean, and why the American economy continues to show surprising resilience.

The Headline Numbers: Blowing Past Estimates

Economists were largely projecting a modest gain of around 85,000 jobs for May. Instead, the Labor Department revealed that U.S. employers added a robust 172,000 new jobs.

Total Jobs Added: 172,000 (vs. 85,000 expected)

Unemployment Rate: Held steady at 4.3%

Wage Growth: Average hourly earnings ticked up by 0.3% month-over-month.

April Revisions: April’s numbers were also sharply revised upward from 115,000 to an impressive 179,000.

This wasn’t just a slight beat; it was a doubling of expectations, indicating that businesses are still finding reasons to hire and expand, even in an uncertain macroeconomic climate.

Where Are the Jobs Coming From?

While the headline number is strong, the growth wasn’t entirely uniform across the board. The heavy lifting was done by a few key sectors:

Healthcare and Social Services: Continuing a long-running trend, healthcare remains a massive engine for job creation, accounting for a significant chunk of the new roles.

Leisure and Hospitality: As the weather warms up, consumer demand for travel and dining out remains steady, prompting strong hiring in this sector.

Local Government: Public sector hiring also saw notable gains.

Conversely, some sectors felt the pinch. Employment in financial activities slipped slightly, reflecting tighter borrowing conditions and shifting corporate strategies.

Resilience Amid Global Headwinds

The most fascinating takeaway from this report isn’t just the sheer number of jobs added—it’s the context in which they were created.

Since the escalation of the war in Iran earlier this year, global energy markets have been incredibly volatile. Spiking oil prices have renewed fears of inflation, putting pressure on consumer wallets and business operational costs alike. Despite these immense headwinds, the domestic labor market has absorbed the shock remarkably well.

The fact that employers are still confident enough to add 172,000 workers to their payrolls suggests an underlying structural strength in the U.S. economy that is, for now, overriding geopolitical anxieties.

What This Means for the Federal Reserve

Of course, a hot jobs report complicates things for the Federal Reserve.

When the labor market is strong and wage growth is steady, inflation tends to remain sticky. Prior to this report, there was speculation that the Fed might keep interest rates flat for the rest of the year. However, this display of economic resilience might push policymakers in a more hawkish direction. While the steady 4.3% unemployment rate means the labor market isn’t overheating, markets are now bracing for the possibility that the Fed could lift rates at least once by the end of 2026 to keep inflationary pressures in check.

The Bottom Line

The May 2026 jobs report is a potent reminder that the U.S. economy rarely behaves exactly as modeled. While the challenges of inflation and global conflict are very real, the underlying demand for labor remains undeniably robust. Whether this momentum can be sustained into the summer remains to be seen, but for now, the job market continues to defy the odds.

The Invisible Hand is Getting a Digital Upgrade (and a Glitch)

For decades, the US economy felt like a predictable, if sometimes temperamental, machine. We looked at the S&P 500, labor participation, and GDP, and we generally knew where we stood. But lately, with AI the gauges are spinning.

As we move through 2026, it’s becoming clear that Artificial Intelligence isn’t just another “sector” or a “tailwind.” It has become a massive, invisible force field distorting the very metrics we use to define economic health. From a soaring stock market that masks a stagnant middle class to a trade deficit driven by chips rather than cars, the “AI Distortion” is the new reality.

1. The Tale of Two Economies: AI vs. Everything Else

If you look at the surface-level GDP growth, things look great. But peel back the layers, and you’ll find a massive divergence.

Recent estimates suggest the “AI economy”—driven by massive capital expenditure from tech giants—is growing at a blistering pace of over 30%. Meanwhile, the rest of the traditional economy is barely treading water. We are seeing a “Hurricane-strength” weather system where a handful of companies (the “Magnificent 7” and their suppliers) are responsible for nearly all the growth, while sectors like housing, transportation, and traditional manufacturing face headwinds.

Key Stat: Morgan Stanley projects that capital spending by the five largest AI “hyperscalers” will top $1.1 trillion in 2027. To put that in perspective: that is more than the projected US national defense budget.

2. The Profit-Wage Disconnect

The most jarring distortion is the widening gap between corporate profits and worker pay. While S&P 500 earnings are rocketing—specifically for companies providing the “picks and shovels” of AI like NVIDIA—labor’s share of total business output has hit historic lows.

The Corporate Side: Profits are being driven by extreme efficiency and high-margin AI services.

The Human Side: Real wages, after inflation, have struggled to keep pace. Workers are feeling a “vibecesssion”—a psychological recession—even when the data says the economy is booming. The fear of replacement by AI is creating a mood of cautious pessimism that isn’t reflected in the soaring Nasdaq.

3. The Trade Deficit Illusion

Usually, a widening trade deficit is a sign of a weak domestic manufacturing base. In the Age of AI, it’s a sign of a domestic investment boom.

Because the US leads in AI software and design but relies on overseas foundries (primarily in Taiwan and South Korea) for high-end semiconductors, every dollar spent building a domestic data center often results in thousands of dollars of imported hardware. This is distorting our trade balance, making the US look “weaker” on paper even as it cements its role as the global hub for AI innovation.

4. Is It a Bubble or a Foundation?

The “B-word” is on everyone’s lips. Skeptics point to the 1990s dot-com era, noting that we are currently betting the entire economy on “scaling”—the idea that bigger models and more data will inevitably lead to AGI (Artificial General Intelligence).

If this bet pays off, we are building the infrastructure of a new civilization. If it doesn’t, the distortion could lead to a massive correction. We’ve reached a point where the US economy is “Too Big to Fail” on AI. As David Sacks, the administration’s AI czar, recently noted: a reversal in AI investment wouldn’t just be a tech correction—it would risk a full-scale national recession.

The Bottom Line

We are living in an era of synthetic growth. The numbers are real, but they don’t feel real to the average person because they are concentrated in a digital frontier. As AI continues to distort everything from job security to trade routes, the challenge for 2026 and beyond isn’t just “how to grow,” but how to ensure that the AI boom doesn’t leave the rest of the economy in its shadow.

The hand of the market is no longer just “invisible”—it’s becoming algorithmic.

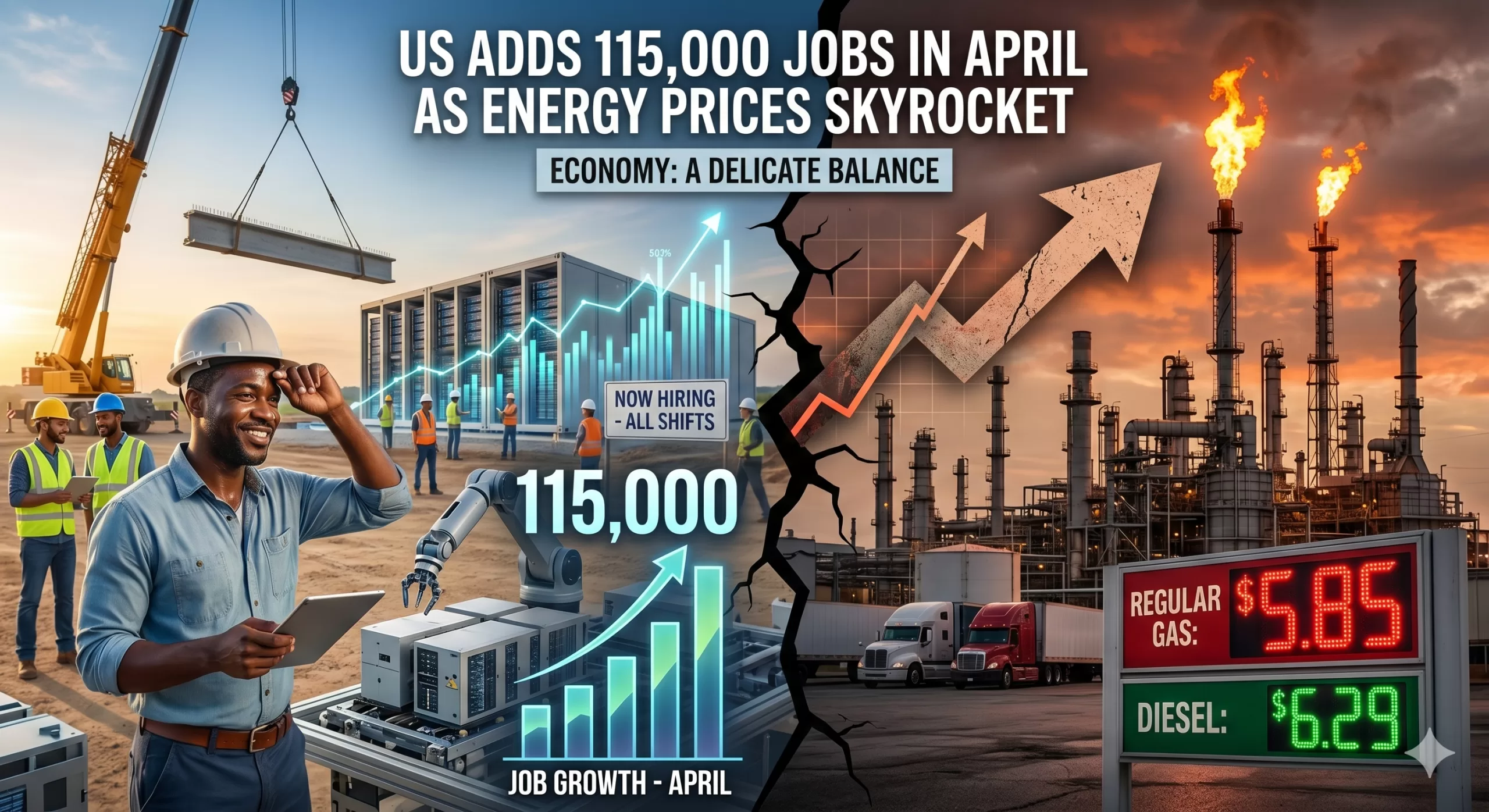

The latest Labor Department report released today, May 8, 2026, reveals a complex picture of the American economy. While the addition of 115,000 jobs in April far exceeded the conservative forecasts of 65,000, this hiring momentum is colliding with a volatile energy market and geopolitical tensions that are keeping consumers—and the Federal Reserve—on edge.

The April Jobs Numbers: A Surprising Resilience

Despite a year of uneven growth and high interest rates, the labor market continues to find its footing. The 115,000 gain marks a significant win for an economy that many feared was cooling too rapidly.

Unemployment Rate: Held steady at 4.3%, a remarkably low figure given the broader economic headwinds.

Sector Highlights: Growth was fueled by health services, education, and construction. Notably, the boom in AI data center construction is providing a sturdy floor for blue-collar employment.

Small Business Bounce: Much of the hiring surge came from small businesses (fewer than 20 employees), suggesting that local optimism remains resilient despite macro-level volatility.

The Energy Crisis: A Shadow Over the Recovery

While the job gains are a reason for celebration, they are being offset by a painful reality at the pump and in utility bills. Crude oil prices have breached the $100-per-barrel mark, driven largely by recent hostilities in the Strait of Hormuz.

For the average American household, the “energy tax” is real. Rising gas prices are eating into the gains from recent tax refunds and wage growth. This creates a “push-pull” dynamic:

The Push: Robust hiring and steady wages ($6.6\%$ growth for job-switchers) give consumers spending power.

The Pull: Skyrocketing energy costs increase the cost of goods and transportation, effectively neutralizing those wage gains for many families.

What This Means for the Federal Reserve

The Fed is now in a delicate position. Usually, a strong jobs report would signal that the economy can handle higher interest rates. However, with energy prices driving “cost-push” inflation, Fed Chair Jerome Powell and his team must decide if the labor market is stable enough to wait out the energy spike or if they need to pivot to protect growth.

Traders are currently betting on a “stable backdrop,” but the volatility in the Middle East remains the ultimate wildcard. If energy prices continue their upward trajectory, the modest 115,000-job gain might be harder to replicate in May.

Looking Ahead

The April report proves that the U.S. economy is more durable than skeptics predicted, but it also highlights our vulnerability to global supply shocks. As we move into the summer months, all eyes will be on two things: the price of a gallon of gas and whether the AI-driven infrastructure boom can continue to carry the weight of the labor market.

Bottom Line: The American worker is still in demand, but the cost of living—fueled by a chaotic energy market—is the primary threat to this hard-won stability.

For the first time since the aftermath of World War II, the United States has reached a fiscal milestone that was once a distant “what-if” scenario: the national debt has officially surpassed 100% of the country’s Gross Domestic Product (GDP).

As of March 31, 2026, the debt held by the public reached $31.27 trillion, while the total annual economic output sat at $31.22 trillion. In simple terms, we now owe more as a nation than we produce in an entire year.

While “trillions” can feel like abstract Monopoly money, this 100.2% ratio represents a fundamental shift in the American economic landscape. Here is what you need to know about why this happened and what it means for the future.

How Did We Get Here?

This wasn’t an overnight accident. It is the result of decades of “fiscal kicking the can.” The surge to 100% was fueled by three primary engines:

Structural Deficits: For years, the government has spent roughly $1.33 for every $1.00 it collects in revenue.

The Interest Trap: As the total debt grows, so do the interest payments. In 2026, the U.S. is projected to spend approximately $1 trillion on interest alone—surpassing the entire national defense budget.

Demographic Shifts: An aging population is naturally drawing more heavily on Social Security and Medicare, programs that make up a massive portion of mandatory spending.

Why the 100% Threshold Matters

Economists often debate whether there is a “magic number” where debt becomes fatal. While 100% isn’t an immediate “cliff,” it serves as a critical psychological and economic warning light for several reasons:

Slower Economic Growth: Historical data suggests that when a nation’s debt exceeds 90% of GDP, average annual growth tends to slow. Resources that could be used for private investment or infrastructure are instead diverted to servicing old debt.

Reduced “Crisis Cushion”: When the next pandemic, recession, or war hits, the government has less “dry powder” to respond. Borrowing your way out of a crisis is much harder when your credit card is already maxed out relative to your income.

Generational Equity: The debt essentially represents a “tax” on future generations. Today’s spending is being financed by the earnings of Americans who haven’t even entered the workforce yet.

The Cost to the Average Household

To bring these massive numbers down to earth, the Senate Joint Economic Committee’s April 2026 update provides a sobering breakdown:

Debt per Person: Approximately $114,000

Debt per Household: Approximately $289,000

Is There a Way Out?

The U.S. has been here before. After 1945, the debt-to-GDP ratio was successfully whittled down to 34% by 1980. However, that was achieved through a unique combination of post-war industrial dominance, a massive “Baby Boom” workforce, and rapid GDP growth.

Today, the path is narrower. Solutions generally fall into three difficult categories:

Entitlement Reform: Adjusting Social Security and Medicare to match modern life expectancies.

Revenue Increases: Raising taxes or closing loopholes to narrow the deficit.

Growth Incentives: Policies designed to make the “GDP” side of the ratio grow faster than the “Debt” side.

The Bottom Line

Crossing the 100% threshold is a “reckoning” moment. It signals that the era of “cheap” borrowing is over. As interest payments continue to eat a larger slice of the federal pie, the pressure on the American taxpayer—and the pressure to make hard political choices—will only intensify.

The red line has been crossed. The question now is whether we have the political will to head back toward the black.

Middle East War Will Slow Global Economic Growth. The global economy, which had shown surprising resilience through early 2026, is now facing a significant “speed bump.” In its latest World Economic Outlook released today, April 14, 2026, the International Monetary Fund (IMF) warned that the escalating conflict in the Middle East—specifically the war involving Iran—has halted global momentum and forced a downgrade of growth projections.

The Numbers: A Downward Shift

Just months ago, economists were optimistic that a tech-driven productivity boom and easing inflation would lead to a “soft landing.” However, the IMF has now lowered its 2026 global growth forecast to 3.1%, down from the 3.3% projected in January.

Scenario

2026 Growth Forecast

Key Drivers

Reference (Current)

3.1%

Short-lived conflict, oil averages $82/bbl

Adverse

2.5%

Prolonged disruption, oil stays at $100

Severe

2.0%

Extended war, oil spikes to $110+

The “Strait” Jacket on Energy

The primary engine of this slowdown is the volatility in energy markets. The closure of the Strait of Hormuz in March 2026—a chokepoint for 20% of the world’s oil and significant LNG volumes—sent Brent crude surging past $120 per barrel.

While prices have recently fluctuated around $98, the damage to supply chains is extensive. The IMF notes that:

Inflation is Rebounding: Global inflation expectations for 2026 have been revised up to 4.4%.

Fertilizer Shortages: With 20-30% of global fertilizer exports passing through the region, agricultural costs are rising, threatening food security in import-reliant nations.

Trade Disruptions: Maritime insurance premiums have skyrocketed, and major shipping routes are being rerouted, adding weeks to delivery times for consumer goods.

The Risk of a “Close Call” Recession

IMF Chief Economist Pierre-Olivier Gourinchas described the current situation as a pivot point. While the “Reference Scenario” assumes the war remains contained, a “Severe Scenario” could see growth drop to 2%—a level the IMF considers a global recession. This has only happened four times since 1980.

Central banks, which were expected to begin cutting interest rates this spring, may now be forced to keep rates “higher for longer” to combat the energy-driven inflationary spike.

“War in the Middle East has halted the global momentum we saw at the start of the year. The risks are now firmly tilted to the downside.”

— Pierre-Olivier Gourinchas, IMF Chief Economist

Looking Ahead

The path forward depends entirely on the duration of the hostilities. If a ceasefire holds and energy production in the Persian Gulf normalizes by mid-year, the IMF believes the global economy can avoid a total contraction. However, for emerging markets and developing economies, the impact is expected to be twice as severe as that on advanced nations, potentially undoing years of post-pandemic recovery.

A Surprising Spring: March Jobs Report Shatters Expectations

The U.S. labor market just delivered a spring surprise that few saw coming. According to the latest data released today by the Bureau of Labor Statistics (BLS), the U.S. economy added 178,000 jobs in March, vastly outperforming economist forecasts which had hovered around a modest 60,000 to 70,000.

After a dismal February that saw a revised loss of 133,000 jobs, this rebound signals a resilient—if complex—economic landscape.

The Numbers at a Glance

The March report offers a refreshing change of pace for a labor market that has felt “frozen” for much of the past year.

Nonfarm Payrolls: +178,000 (Expected: ~70,000)

Unemployment Rate: 4.3% (Down from 4.4% in February)

Revisions: January’s figures were revised upward to 160,000, though the two-month net revision slightly dampened the overall trend.

What’s Driving the Growth?

The recovery wasn’t uniform across the board. While the headline number is strong, the “engine” of the U.S. economy remains highly concentrated:

The Healthcare Titan: Once again, the health care and social assistance sector did the heavy lifting, adding 76,000 jobs last month. This sector has essentially been the primary life support for the labor market over the last year.

The “Bounce Back” Factor: Part of the March surge is attributed to the return of approximately 31,000 Kaiser Permanente employees who were on strike in February, along with more favorable weather conditions across the country.

The Gender Shift: Interestingly, recent trends show that women now hold more jobs than men in the nonfarm economy—a structural shift driven by the strength of female-dominated sectors like education and health, while male-concentrated sectors like manufacturing continue to cool.

The Shadows on the Horizon: Geopolitics and Oil

Despite the optimistic numbers, experts are urging caution. The report arrives amidst significant geopolitical tension, specifically the ongoing conflict in Iran.

“We’ve got a much more difficult spring job market than we had hoped given the higher prices at the pump and the supply chain disruptions that are going to come from the war,” says Diane Swonk, chief economist at KPMG.

With gas prices spiking above $4 a gallon for the first time since 2022, many fear that the March gains may be a “last hurrah” before the economic impact of the war and energy costs fully settle into corporate hiring plans.

The Bottom Line

The U.S. economy has shown it still has plenty of fight left. A 4.3% unemployment rate remains historically healthy, and the “low-hire, low-fire” stalemate of 2025 appears to be thawing.

However, for job seekers and businesses alike, the road ahead remains fogged by uncertainty. Between the rapid integration of Artificial Intelligence, fluctuating inflation (which dipped to 2.3% before ticking back up), and global instability, “cautious optimism” remains the phrase of the day.

If the global economy feels like a high-wire act lately, you aren’t alone. We are currently navigating a “polycrisis“—a fancy term for when multiple major headaches (inflation, geopolitical tension, and shifting labor markets) all hit the fan at the same time.

We are standing on a narrow ledge. One side leads to a hard landing; the other leads to a stabilized “new normal.” Here is a look at the forces threatening to push us off, and the safety nets that might just pull us back.

The Push: What Could Tip Us Over?

It doesn’t take a wrecking ball to cause a recession; sometimes, it just takes a few well-placed dominos. Here are the primary risks:

The “Higher for Longer” Fatigue: While central banks use interest rates to cool inflation, keeping them elevated for too long puts immense pressure on household debt and corporate margins. If the “lag effect” hits all at once, consumer spending—the engine of the economy—could stall.

Geopolitical Aftershocks: Energy prices are notoriously sensitive to global conflict. Any significant escalation in major trade corridors can reignite supply chain chaos, sending the cost of goods back into the stratosphere.

The Commercial Real Estate Ghost Town: With remote work now a permanent fixture, many office buildings are sitting half-empty. As these property loans come due for refinancing at higher rates, we could see a localized banking tremor.

The Pull: What Could Help Us Pull Through?

It’s not all doom and gloom. There are several structural “muscles” keeping the economy upright:

The Resilient Labor Market: Despite tech layoffs making headlines, overall unemployment remains historically low. As long as people have jobs, they tend to keep spending, which provides a powerful floor for the economy.

The Productivity “AI Bump”: We are at the beginning of a massive technological shift. Early adoption of generative AI is already beginning to streamline workflows and reduce operational costs, which could lead to a non-inflationary growth spurt.

Household Balance Sheets: Unlike the 2008 crash, many consumers and corporations locked in low interest rates years ago. This “debt buffer” has bought the private sector time to adjust to the new economic reality.

The Bottom Line: Balance, Not Freefall

The economy isn’t necessarily “broken,” but it is transitioning. We are moving away from an era of “free money” and into an era where efficiency and strategic investment matter again.

Scenario

Key Driver

Likely Outcome

The Hard Landing

Persistent inflation + high rates

Brief but sharp recession; rising unemployment.

The Soft Landing

Controlled cooling + tech growth

Flat growth for a year, followed by a steady recovery.

The No Landing

Continued high spending

Economy stays hot, but rates stay high indefinitely.

The Takeaway: While the ledge is narrow, the path across is still visible. Navigating the next twelve months will require agility from policymakers and patience from investors. We may be on the edge, but we aren’t over it yet..

The final numbers for 2025 are in, and there has been a GDP Downward Revision… they’ve arrived with a bit of a chill. On March 13, 2026, the Bureau of Economic Analysis (BEA) released its second estimate for the fourth quarter of 2025, significantly revising real GDP growth downward to an annualized rate of 0.7%.

This is a sharp departure from the initial “advance” estimate of 1.4% and a massive deceleration from the robust 4.4% growth seen in the third quarter. For the full year, the U.S. economy grew by 2.1%, a slight dip from previous projections.

So, what happened at the end of the year to take the wind out of the economy’s sails?

The Culprits: Shutdowns, Slumps, and Spending

Several factors converged in late 2025 to create this “soft landing” that felt a little more like a bump.

The 43-Day Government Shutdown: The most visible drag was the historic federal government shutdown that spanned October and November. While essential services remained, the lack of federal paychecks and halted government contracts took a measurable bite out of domestic demand.

A “Low-Hire” Labor Market: While mass layoffs weren’t the headline, a “low-hire, low-fire” environment took hold. Monthly job gains slowed to a crawl, and the unemployment rate ticked up to 4.6% by November, making consumers more cautious with their wallets.

The Trade Drag: Exports were revised downward as global demand softened, and a “front-loading” effect—where companies rushed to import goods earlier in the year to avoid new tariffs—faded out, leaving a gap in activity for the final months.

Sticky Inflation: Despite the slower growth, the PCE price index (the Fed’s favorite inflation gauge) remained at 2.9%. This combination of stagnant growth and persistent inflation has put the Federal Reserve in a difficult “wait-and-see” position.

Silver Linings in the Data

It’s not all doom and gloom. Even with the downward revision, there are signs of underlying resilience:

Investment is Picking Up: While consumer spending moderated, business investment—particularly in AI infrastructure—actually accelerated in Q4, acting as a critical floor for the economy.

Market Resilience: Interestingly, Wall Street took the news in stride. Markets actually rallied following the release, as investors bet that the soft GDP data would finally force the Federal Reserve to consider more aggressive rate cuts later in 2026.

Recouping the Loss: Economists expect much of the “lost” output from the government shutdown to be recovered in the first half of 2026 as backlogged projects and federal spending finally hit the books.

What’s Next for 2026?

The downward revision confirms that the “Goldilocks” era of high growth and falling inflation has hit a snag. Most forecasters, including the IMF and S&P Global, now project a steady but modest growth rate of around 1.8% to 2.0% for 2026.

The big question remains the Federal Reserve. With growth at 0.7% but inflation still above their 2% target, the path to interest rate cuts remains narrow. For now, the “wait-and-see” approach is the only game in town.

1. The Tech Sector: From Growth to Efficiency

While the broader economy slowed, Tech remained a relative fortress, but the “flavor” of investment is changing.

AI Infrastructure as a Life Raft: Business investment in “Intellectual Property Products” (tech speak for software and AI R&D) was one of the few areas that actually accelerated in Q4 2025. Companies are doubling down on AI to find the efficiencies they need to survive a low-growth environment.

The “Low-Hire” Reality: Expect the “low-hire” trend to persist in Silicon Valley. With GDP growth revised downward, tech giants are focusing on “AI-driven productivity” rather than aggressive headcount expansion.

Valuation Pressure: While the stock market has been resilient, persistent 2.9% inflation means the Federal Reserve isn’t in a rush to slash rates. High-growth tech stocks are sensitive to interest rates; if those rates stay “higher for longer,” we may see more volatility in tech valuations throughout 2026.

2. The Real Estate Market: A Tale of Two Interests

The GDP Downward Revision has created a paradoxical situation for housing.

Mortgage Rate Relief? Traditionally, weak GDP data pushes bond yields down, which can lower mortgage rates. Many analysts now expect the 30-year fixed rate to drift toward 6.0%–6.2% in 2026. This could finally “unlock” homeowners who have been trapped by high rates.

The “Sentiment” Gap: The revision highlights a cooling labor market (unemployment at 4.6%). Even if mortgage rates drop, buyer “jitters” may keep the market from exploding. J.P. Morgan research suggests national home prices may stall at 0% growth in 2026 as demand and supply reach a fragile equilibrium.

Commercial Real Estate (CRE) Stress: The 0.7% GDP print is toughest on office and retail CRE. Slower economic activity means less demand for physical space, likely leading to more “strategic defaults” or building repurposing projects in 2026.

The Federal Reserve’s “Tightrope”

The GDP Downward Revision puts the Fed in a bind. Usually, 0.7% growth would trigger an immediate rate cut to “save” the economy. However, with inflation still at 2.9%, they risk reigniting price hikes if they move too fast.

The Bottom Line: 2026 will be the year of the “Efficiency Play.” Whether you are a tech firm or a homebuyer, the goal is no longer “growth at any cost,” but rather finding value in a slower, more deliberate economic landscape.

Headline: 📉 GDP Revised to 0.7%: What it means for Tech & Real Estate in 2026.

The “Second Estimate” for Q4 2025 is out, and the numbers confirm a significant cooling of the U.S. economy. Real GDP growth was revised down to an annualized 0.7%—a sharp drop from the earlier 1.4% estimate.

While the 43-day government shutdown in late 2025 played a major role, the ripple effects for 2026 are already taking shape:

💻 TECH: The era of “growth at any cost” is officially over. We’re seeing a pivot toward Efficiency Tech. While broader spending is cooling, investment in AI infrastructure is accelerating as companies scramble to automate their way out of a low-growth environment.

🏠 REAL ESTATE: It’s a paradox. Slower growth usually means lower mortgage rates, and we’re already seeing 30-year fixed rates dip toward 6.0%. However, with unemployment ticking up to 4.6%, buyer “jitters” are real. J.P. Morgan predicts a 0% national price growth for 2026—a true flatline.

⚖️ THE FED: Chair Jerome Powell and the FOMC are walking a tightrope. With inflation still “sticky” at 2.4%–2.9%, they can’t rush to cut rates despite the sub-1% growth.

The Bottom Line: 2026 will reward the “Lean and Leaner.” Whether you’re managing a portfolio or a product roadmap, efficiency is the new growth.

1/ 🚨 BREAKING: U.S. Q4 2025 GDP revised DOWN to 0.7% (from 1.4%). The 2025 “Cold Snap” is official. Here’s the 30-second breakdown of what this means for your wallet in 2026. 🧵👇

2/ Why the drop? The 43-day government shutdown was a massive anchor, but we also saw a deceleration in consumer spending and exports. The economy didn’t crash, but it definitely pulled the emergency brake. 🛑

3/ 💻 TECH IMPACT: Silicon Valley is staying “Low-Hire.” With 0.7% growth, companies are prioritizing AI-driven productivity over expansion. If it doesn’t automate a process or save a dollar, it’s not getting funded this year.

4/ 🏠 HOUSING IMPACT: Good news? Mortgage rates are sliding toward 5.8%–6.0%. Bad news? A weaker labor market means fewer people are ready to jump. Expect a “sideways” year for home prices. 📉➡️

5/ 🏦 FED WATCH: All eyes on the March 18 FOMC meeting. The market was hoping for cuts, but with inflation at 2.4%, the Fed might stay “Higher for Longer” to ensure the fire is out.

6/Summary: 2026 is the year of the “Efficiency Play.” Growth is slow, money is still relatively expensive, and AI is the only engine still revving. Stay nimble. #GDP #Economy #Inflation

📸 Instagram/Threads: The Visual Summary

Caption:

The numbers are in: The U.S. economy hit a “speed bump” at the end of 2025. 📉 GDP growth was just revised down to 0.7%.

What this means for you: ✅ Mortgage Rates: Might actually get a bit friendlier (seeing 5.8% – 6% averages). ✅ Tech: More AI tools, fewer new job postings. Efficiency is 👑. ✅ Inflation: Still hanging around 2.4%, keeping the Fed on high alert.

It’s not a recession—it’s a recalibration. 2026 is about playing the long game. ♟️