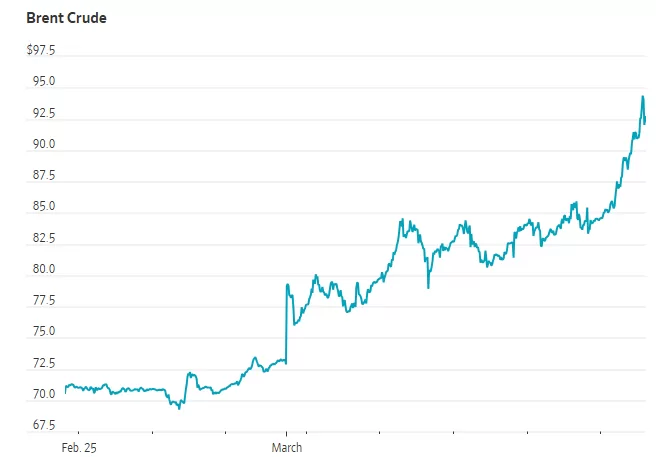

Tank Top Crisis Looms: In the world of global energy, we often focus on the flow of oil—the pipelines, the tankers, and the daily production quotas. But today, the headlines are focusing on something much more static and far more dangerous: storage.

As highlighted in a recent Wall Street Journal report, Kuwait has officially begun cutting its oil production. The reason isn’t a lack of demand or a diplomatic shift in OPEC+ policy. It is a physical reality known in the industry as reaching “tank tops.” Quite simply, Kuwait has run out of places to put its oil.

The Chokepoint Catalyst

The crisis stems from the effective closure of the Strait of Hormuz, a vital maritime artery through which roughly one-fifth of the world’s oil supply passes. Following a series of geopolitical escalations and strikes on energy assets in the Gulf, shipping traffic has ground to a near-halt.

For a nation like Kuwait, which relies heavily on this single export route, a blocked strait creates an immediate and literal backlog. When the tankers can’t leave, the oil has nowhere to go but into storage tanks. Once those tanks are full, the only remaining option is to stop the pumps.

A High-Stakes Domino Effect

Kuwait isn’t the first to hit this wall, and it likely won’t be the last.

Iraq has already slashed its production by more than half, losing roughly 1.5 million barrels per day.

The UAE is estimated to be only days away from its own storage limits.

Saudi Arabia, while possessing much larger storage capacity and alternative pipeline routes to the Red Sea, is also feeling the pressure as the backlog grows.

This “domino effect” of production shutdowns is what keeps energy analysts awake at night. Shutting down an oil well isn’t as simple as flipping a light switch. It is a technically complex and expensive process that can cause long-term damage to reservoir pressure. Restarting these wells once the crisis ends can take weeks, meaning the supply shock will linger long after the shipping lanes reopen.

The Global Fallout: $100 Oil?

The markets have reacted with predictable volatility. Brent crude has already surged past $90 a barrel, a 25% increase since the conflict began. Analysts warn that if the storage crisis forces more Gulf producers to “shut in” their wells, we could see prices easily breach the $100 mark, or even climb toward $150 according to some regional ministers.

Beyond the pump, this crisis threatens to reignite global inflation just as central banks were beginning to find their footing. It serves as a stark reminder of how fragile the global energy infrastructure remains and how a single geographic chokepoint can hold the world’s economy hostage.

The Bottom Line

The situation in Kuwait is a canary in the coal mine. It proves that in a modern energy crisis, the bottleneck isn’t just about who has the oil—it’s about who has the room to hold it when the world stops moving. As storage tanks across the Gulf reach their limits, the pressure isn’t just building in the pipes; it’s building on the global economy.

While the macro economy is feeling the “pump shock,” the impact on small business lending and accounts receivable (AR) factoring is more nuanced. For many industries, rising oil prices act as a catalyst for alternative financing, as traditional bank credit tends to tighten just when operational costs spike.

1. Impact on Small Business Lending

Traditional bank lending to small businesses is becoming more restrictive as energy-driven inflation persists.

The “Double Squeeze”: Small businesses are facing higher input costs (fuel/transport) alongside high interest rates. Banks, wary of compressed profit margins, are increasing their underwriting scrutiny.

The Approval Gap: As of early 2026, large banks are approving only about 68% of small business loans, compared to 82% at smaller, community-focused institutions.

Pivot to High-Cost Credit: With traditional loans taking weeks to approve, many businesses are turning to credit cards (averaging 18%–36% interest) to cover immediate fuel and supply chain gaps, significantly increasing their long-term debt burden.

2. The Surge in AR Factoring Demand

In a high-oil-price environment, factoring often shifts from a “last resort” to a strategic cash-flow tool, particularly for energy-intensive sectors.

Fuel as a Fixed, Immediate Expense: In industries like trucking and oilfield services, fuel must be paid for daily or weekly, while customers (shippers or large operators) often demand 30- to 90-day payment terms. Factoring bridges this “cash gap” without adding traditional debt to the balance sheet.

Sector-Specific Trends:

Transportation/Trucking: Factoring companies are seeing record demand. These businesses often enjoy the highest advance rates (90%–97%+) because their invoices are backed by tangible freight delivery.

Oilfield Services: As drilling activity ramps up in response to higher prices (especially in the Permian Basin), service providers are using factoring to scale quickly—buying new equipment or meeting surge payroll without waiting for 60-day payouts from major oil producers.

Manufacturing: With raw material costs rising alongside energy, manufacturers are factoring invoices to maintain liquidity reserves to buy inventory before prices hike further.

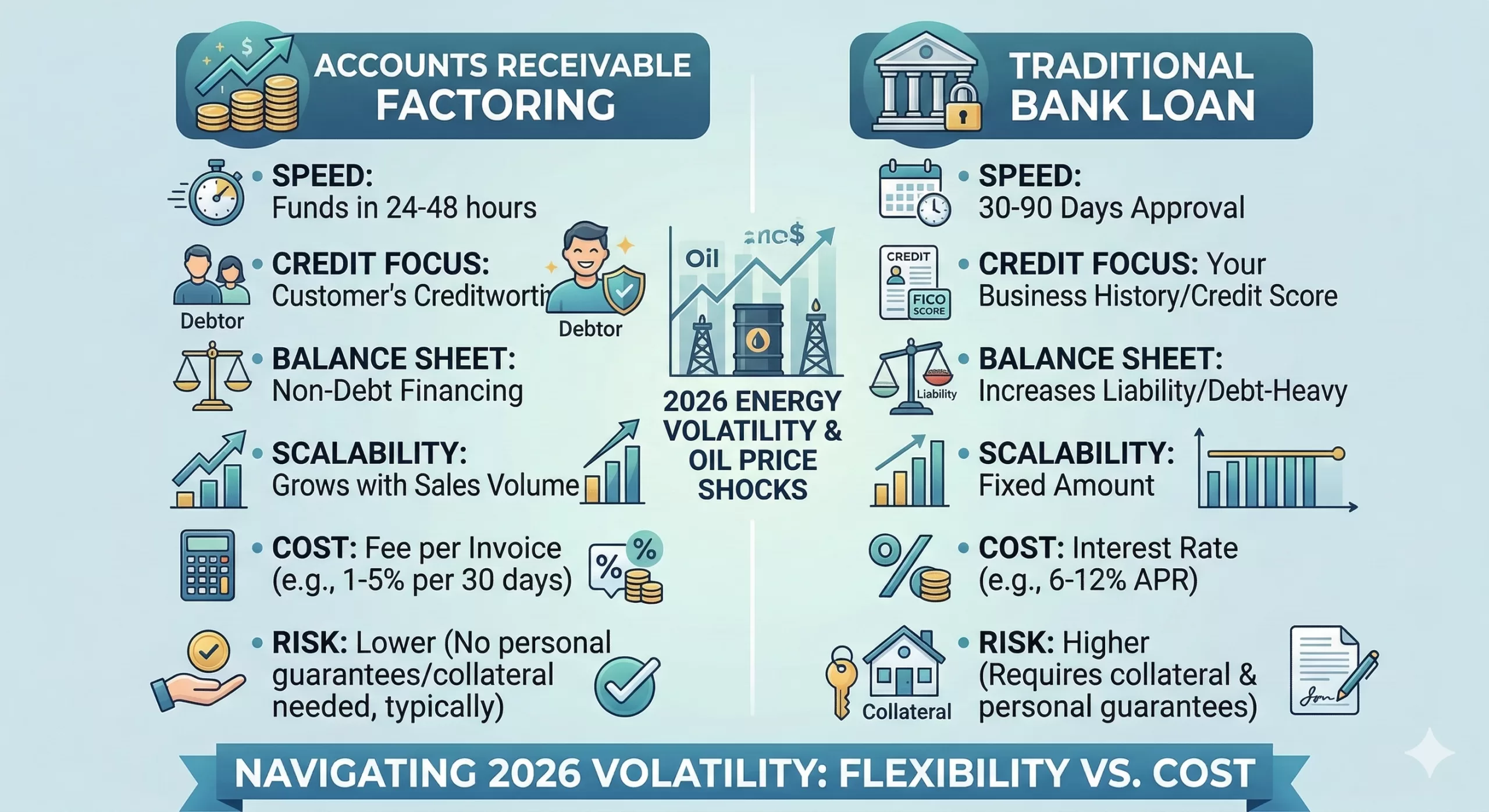

Factoring vs. Traditional Lending in 2026

Feature

Traditional Bank Loan

AR Factoring

Approval Basis

Business credit & history

Customer (Debtor) credit

Speed of Funding

2 – 7 weeks

24 – 48 hours

Debt Load

Increases liability on balance sheet

No new debt (selling an asset)

Scalability

Fixed limit

Grows with your sales volume

Cost

Lower interest (6%–12%)

Higher fees (1%–5% per 30 days)

Strategic Outlook

For the remainder of 2026, businesses that rely on “floating” cash flow are likely to prioritize speed over cost. While factoring fees are higher than bank interest, the ability to access cash within 24 hours to pay for $4.00/gallon diesel is often the difference between staying operational and grounding a fleet.

In a volatile economy where oil prices are surging and traditional banks are pulling back, choosing the right financing tool is a high-stakes decision. For B2B businesses—especially those in staffing, digital marketing, and manufacturing—the choice often comes down to the speed of Factoring versus the lower cost of a Bank Loan.

Below is a strategic comparison designed to help you evaluate which path aligns with your current cash flow needs.

Factoring vs. Bank Loans: 2026 Strategic Comparison

Feature

Accounts Receivable Factoring

Traditional Bank Loan

Speed to Cash

Ultra-Fast: Funds usually arrive within 24–48 hours after invoice setup.

Slow: Approval typically takes 30–90 days of underwriting.

Credit Focus

The Debtor: Decisions are based on your customer’s credit and payment history.

The Business: Based on your FICO score, tax returns, and years in business.

Balance Sheet

Debt-Free: It is the sale of an asset (invoices), not a liability.

Debt-Heavy: Adds a liability that can impact your debt-to-income ratio.

Scalability

Unlimited: As your sales grow, your available cash grows automatically.

Fixed: You are capped at a set amount and must re-apply to increase it.

Total Cost

Higher Fees: Usually 1%–5% per 30 days (effective APR is higher).

Lower Rates: Typically 6%–12% APR for qualified businesses.

Risk

Low: No collateral like your house or equipment is typically required.

High: Often requires a blanket lien on assets or personal guarantees.

Export to Sheets

The “Why Now?” Factor: Navigating 2026 Volatility

Pros of Factoring in This Market

Immediate Fuel/Supply Buffer: With diesel prices fluctuating, factoring gives you the cash today to buy inventory or fuel before the next price hike.

Protects Your Growth: In sectors like digital marketing or staffing, you can’t wait 60 days for a client to pay to meet your weekly payroll. Factoring ensures your team stays paid regardless of when the client cuts the check.

No “Covenant” Stress: Bank loans often come with strict “covenants” (rules about your profit margins). If high oil prices temporarily squeeze your margins, a bank might call your loan; a factor simply keeps funding your sales.

Cons to Consider

Margin Impact: If your profit margins are already thin (common in food production or distribution), the 1%–3% factoring fee could eat up a significant portion of your net income.

Customer Perception: While widely accepted today, some ultra-conservative clients might still prefer to pay you directly rather than a third-party factor.

The Bottom Line

If you have long-term stability and time to wait, a Bank Loan is cheaper. However, if you are growing rapidly or facing unpredictable costs, Factoring acts as a flexible insurance policy for your cash flow.

Our Accounts Receivable Factoring program can quickly meet the working capital needs of businesses in the energy industry.

Versant’s underwriting focus is solely on the quality of a company’s accounts receivable, which enables us to rapidly fund businesses which do not qualify for traditional lending.

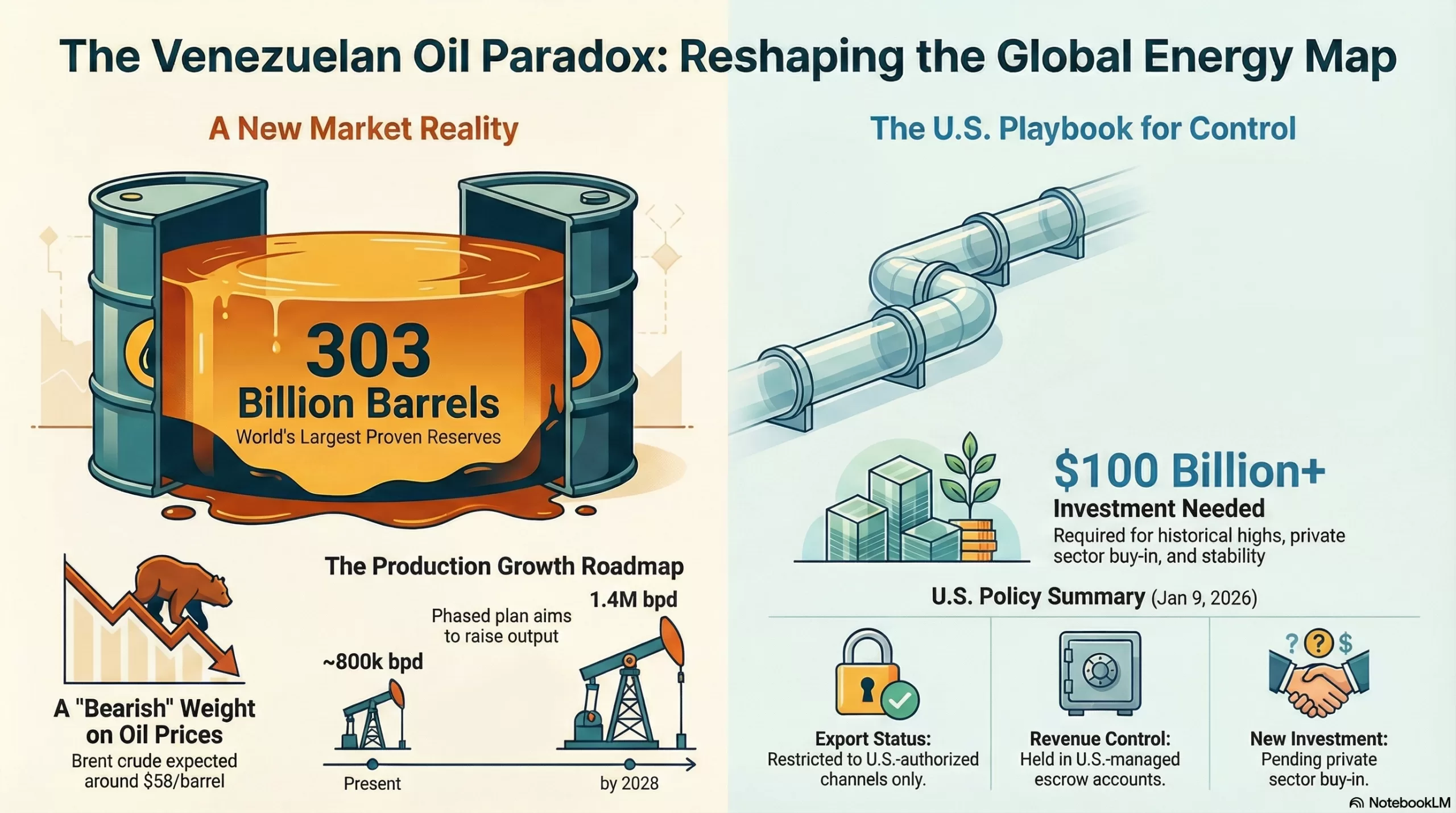

The start of 2026 has brought one of the most significant shifts in the energy sector in decades. With the recent capture of Nicolás Maduro on January 3, 2026, and the subsequent move by the U.S. administration to overhaul Venezuela’s energy infrastructure, the global oil market is facing a new “Venezuelan Paradox.”

While Venezuela holds the world’s largest proven oil reserves—estimated at over 303 billion barrels—its actual impact on the global market is currently a tug-of-war between massive long-term potential and a short-term supply glut.

1. The Immediate Shock: Volatility vs. the “Glut”

In the days following the January 3rd intervention, oil prices saw a brief “short squeeze” as traders priced in geopolitical risk, with prices nudging toward $60/barrel. However, the broader market remains in a state of oversupply.

Experts from J.P. Morgan and the IEA highlight that the market is currently facing a significant supply glut. Brent crude is forecasted to average around $58/barrel for the remainder of 2026. Because the world is already well-supplied by U.S. shale and Guyana, the return of Venezuelan barrels acts as a “bearish” weight on prices rather than a catalyst for a spike.

2. The Production Road Map: From 800k to 1.4M

As of early 2026, Venezuela’s production sits between 750,000 and 960,000 barrels per day (bpd). While the U.S. Department of Energy (DOE) is already moving to release millions of barrels of “sanctioned oil” held in floating storage, actual production growth will take time.

Short-term (End of 2026): Production could realistically ramp up to 1.1–1.2 million bpd if sanctions are selectively rolled back to allow for infrastructure repairs.

Medium-term (2027-2028): With sustained investment from firms like Chevron and others, output could hit 1.4 million bpd.

The Long Game: Reaching the historical highs of 3 million bpd is estimated to require over $100 billion in investment and at least a decade of stable governance.

3. Geopolitical Pivot: China’s Loss, the U.S. Gulf’s Gain

For years, Venezuela’s oil was the lifeblood of China’s “teapot” (independent) refineries, often sold at steep discounts to circumvent sanctions. That era is ending.

The U.S. administration has signaled that Venezuelan oil will now flow through “authorized channels,” prioritizing U.S. and Western markets. This creates a massive shift in trade flows:

U.S. Gulf Coast Refiners: These facilities were originally built to process the heavy, sour crude that Venezuela produces. They are expected to reclaim these volumes, reducing their reliance on more expensive alternatives.

China’s Response: Chinese refineries are likely to pivot toward Russian Urals or Iranian Heavy, potentially intensifying competition for those sanctioned grades.

4. The OPEC+ Balancing Act

Venezuela is a founding member of OPEC, but its production has been so low for so long that it has mostly been a “silent partner.” In response to the 2026 developments, OPEC+ has paused its planned output hikes for Q1 2026.

The group, led by Saudi Arabia and Russia, is wary of a “perfect storm”: a global slowdown combined with a sudden surge in Venezuelan exports. If Venezuela successfully rehabilitates its sector, OPEC+ may have to maintain deeper cuts for longer to prevent prices from sliding into the $40s.

The Bottom Line

The “Venezuelan effect” in 2026 is less about a sudden flood of oil and more about a reordering of the global energy map. For the first time in a generation, the “Western Hemisphere energy powerhouse” (U.S., Canada, Guyana, and Venezuela) looks like a unified block that could significantly challenge the pricing power of Middle Eastern and Russian suppliers.

For small businesses and consumers, this is generally good news. The presence of Venezuelan “upside risk” to supply acts as a ceiling for oil prices, likely keeping fuel and energy costs stable throughout the year.

The landscape for Venezuelan oil shifted dramatically following the capture of Nicolás Maduro on January 3, 2026.1 The U.S. administration has moved quickly to assert control over the sector, balancing long-term infrastructure goals with immediate market pressure.2

Here is a summary of the current U.S. policy changes and strategic directives as of January 9, 2026:

1. The “Approved Channels” Only Policy3

The U.S. has established a strict “quarantine” on all oil movements.

Controlled Sales: The Energy Department has mandated that the only oil allowed to leave Venezuela must flow through U.S.-approved channels.4

Vessel Seizures: The U.S. Coast Guard and DOJ have already begun seizing “dark fleet” tankers in the North Atlantic and Caribbean that were attempting to move sanctioned oil outside of these new channels.5

The 50M Barrel Release: Interim authorities have agreed to turn over 30 to 50 million barrels of existing storage to the U.S. for sale at market prices.6

2. Financial & Revenue Control

A central pillar of the new policy is the “purse strings” strategy:7

Escrow Accounts: Revenue from Venezuelan oil sales is being deposited into U.S.-controlled accounts at globally recognized banks.8

Disbursement: Funds are intended to be disbursed at the discretion of the U.S. government to support the “American and Venezuelan populations,” rather than the previous regime’s lieutenants.9

Conditionality: Further sanctions relief is tied to Venezuela severing all economic ties with China, Russia, Iran, and Cuba.10

3. “Selective” Sanctions Rollbacks

Instead of a broad lifting of all sanctions, the Treasury’s Office of Foreign Assets Control (OFAC) is issuing private waivers and specific licenses:11

Infrastructure Priority: Licenses are being granted specifically for the import of oil field equipment, parts, and services.12 This is designed to reverse decades of decay in the Orinoco Belt.

Diluent Imports: The U.S. is authorizing the shipment of diluents (thinners) to Venezuela, which are required to make their heavy crude liquid enough to pump through pipelines and onto tankers.13

Direct Waivers: Private trading firms are being granted specific waivers to resume purchases, provided the oil is sold to U.S.-based buyers.14

4. The “Private Sector Pivot”

President Trump is meeting with executives from ExxonMobil, Chevron, and others (as of Friday, Jan 9) to pitch a massive redevelopment plan:15

The Investment Goal: The administration is pushing for private companies to lead a $60B–$100B overhaul of the industry.

The Conflict: There is a stated policy goal of driving global oil prices down to $50/barrel.16 This creates a “profitability gap” for oil majors, who argue that the cost of extracting heavy Venezuelan crude may not be viable if prices fall that low.

Key Policy Benchmarks for 2026

Policy Area

Current Status (Jan 9, 2026)

Export Status

Restricted to U.S.-authorized channels only.

Revenue Control

Held in U.S.-managed accounts.

New Investment

Pending private sector “buy-in” and stability guarantees.

OPEC Status

Effectively suspended from quota participation during transition.

Briefing: The 2026 Venezuelan Oil Sector Transformation

Executive Summary

The capture of Nicolás Maduro on January 3, 2026, has triggered a fundamental and rapid transformation of Venezuela’s oil sector, creating what is termed the “Venezuelan Paradox.” While the nation possesses the world’s largest proven oil reserves at over 303 billion barrels, its immediate market impact is a bearish pressure on prices due to a global supply glut, rather than a price spike. The U.S. administration has swiftly implemented a strategy of direct control over Venezuela’s oil exports and revenue, mandating that all sales flow through “approved channels” and placing proceeds into U.S.-managed escrow accounts.

This strategic pivot is causing a significant reordering of the global energy map. U.S. Gulf Coast refiners, designed for Venezuelan heavy crude, are positioned to benefit, while China’s independent refineries lose a primary source of discounted oil. In response to the potential for increased Venezuelan supply, OPEC+ has paused planned output hikes, wary of a price collapse. The overarching outcome is the potential formation of a powerful, unified Western Hemisphere energy bloc (U.S., Canada, Guyana, and Venezuela) capable of challenging the pricing power of Middle Eastern and Russian suppliers. For consumers, this development is expected to act as a ceiling on oil prices, promoting stable energy costs through 2026.

1. The Venezuelan Paradox: Market Dynamics and Production Outlook

The events of early January 2026 have introduced a complex dynamic into the global oil market, defined by the conflict between Venezuela’s immense long-term potential and the immediate realities of its dilapidated infrastructure and a well-supplied global market.

Immediate Market Impact: Volatility vs. Glut

Initial Volatility: In the immediate aftermath of the January 3 intervention, oil prices experienced a brief “short squeeze” driven by geopolitical risk, temporarily pushing prices toward $60 per barrel.

Prevailing Glut: This volatility was short-lived, as the broader market remains in a state of oversupply. Analysis from J.P. Morgan and the IEA indicates a significant supply glut, reinforced by ample production from U.S. shale and Guyana.

Price Forecast: The re-entry of Venezuelan barrels is viewed as a “bearish” weight on the market. Brent crude is forecasted to average approximately $58 per barrel for the remainder of 2026.

Phased Production Roadmap

Venezuela’s current oil production stands between 750,000 and 960,000 barrels per day (bpd). A multi-stage recovery is anticipated, contingent on investment and stability.

Short-Term (End of 2026): Production could ramp up to 1.1–1.2 million bpd with selective rollbacks on sanctions to permit essential infrastructure repairs.

Medium-Term (2027-2028): Sustained investment from major firms like Chevron could elevate output to 1.4 million bpd.

Long-Term Goal: Reaching the historical peak production of 3 million bpd is a formidable challenge, estimated to require over $100 billion in capital investment and at least a decade of stable governance.

2. U.S. Strategic Control and Policy Directives

The U.S. administration has enacted a comprehensive policy framework to manage Venezuela’s oil sector, focusing on controlling exports, revenue, and the pace of redevelopment.

“Approved Channels” and Asset Control

Export Quarantine: The U.S. has instituted a strict policy mandating that the only oil permitted to leave Venezuela must move through U.S.-approved channels.

Enforcement Actions: The U.S. Coast Guard and Department of Justice have begun seizing “dark fleet” tankers in the North Atlantic and Caribbean attempting to transport sanctioned oil outside these new regulations.

Release of Stored Oil: Interim Venezuelan authorities have agreed to transfer 30 to 50 million barrels of oil from floating storage to U.S. control for sale at market prices.

Financial Controls and Sanctions Policy

A “purse strings” strategy is central to the U.S. approach, ensuring financial oversight and leveraging sanctions for policy goals.

Escrow Accounts: All revenue from authorized Venezuelan oil sales is being deposited into U.S.-controlled escrow accounts at major international banks. Funds are intended for the “American and Venezuelan populations.”

Conditional Relief: Further sanctions relief is explicitly tied to Venezuela severing all economic ties with China, Russia, Iran, and Cuba.

Selective Waivers: The Treasury’s Office of Foreign Assets Control (OFAC) is issuing private waivers and specific licenses rather than a blanket lifting of sanctions. These licenses prioritize:

Import of oil field equipment, parts, and services to repair the Orinoco Belt.

Shipment of diluents required to make Venezuela’s heavy crude transportable.

Waivers for private trading firms to purchase oil, provided it is sold to U.S.-based buyers.

The Private Sector Pivot and Investment Strategy

The U.S. is encouraging private investment to lead the sector’s revitalization, though a potential conflict exists between policy goals and corporate profitability.

Investment Goal: President Trump is actively meeting with executives from ExxonMobil, Chevron, and other firms to promote a massive redevelopment plan estimated to cost between $60 billion and $100 billion.

The Profitability Conflict: A stated administration policy goal is to drive global oil prices down to $50 per barrel. Oil majors have expressed concern that this price point may render the extraction of heavy Venezuelan crude unprofitable, creating a “profitability gap” that could hinder investment.

Key Policy Benchmarks (as of Jan 9, 2026)

Policy Area

Current Status

Export Status

Restricted to U.S.-authorized channels only.

Revenue Control

Held in U.S.-managed accounts.

New Investment

Pending private sector “buy-in” and stability guarantees.

OPEC Status

Effectively suspended from quota participation during transition.

3. Geopolitical Realignment and Global Impact

The shift in Venezuela’s oil policy is causing a significant reordering of global energy trade flows and prompting strategic recalculations by major market players.

Shifting Trade Flows: U.S. Gulf vs. China

U.S. Gulf Coast Gains: Refineries along the U.S. Gulf Coast, which were originally engineered to process Venezuela’s specific grade of heavy, sour crude, are expected to be the primary beneficiaries. They can now reclaim these volumes, reducing their dependence on more expensive alternatives.

China’s Loss: The era of China’s “teapot” (independent) refineries sourcing heavily discounted Venezuelan crude is ending. Chinese refiners are now expected to pivot toward other sanctioned grades, such as Russian Urals or Iranian Heavy, potentially increasing competition for these barrels.

OPEC+ Response and Price Stabilization

As a founding member of OPEC, Venezuela’s potential return to significant production levels presents a challenge to the cartel’s market management strategy.

Preemptive Action: In response to the developments, OPEC+ (led by Saudi Arabia and Russia) has paused its planned output hikes for Q1 2026.

Managing the “Perfect Storm”: The group is concerned about a “perfect storm” scenario where a global economic slowdown coincides with a surge in Venezuelan exports.

Future Cuts: If Venezuela successfully rehabilitates its oil sector, OPEC+ may be forced to maintain deeper and longer production cuts to prevent crude prices from sliding into the $40s per barrel range.

4. Conclusion: A New Energy Landscape

The “Venezuelan effect” in 2026 is less about an immediate flood of new oil and more about a fundamental reordering of the global energy map. For the first time in a generation, a unified “Western Hemisphere energy powerhouse”—comprising the United States, Canada, Guyana, and a revitalized Venezuela—appears poised to emerge. This bloc could significantly challenge the long-held pricing power of suppliers in the Middle East and Russia. For consumers and businesses, this shift introduces substantial “upside risk” to global supply, creating a natural ceiling for oil prices and likely contributing to stable fuel and energy costs throughout the year.

Introduction: The Strategic Importance of U.S.-Iran Relations in Global Energy

The United States and Iran have long shared a strained relationship, punctuated by moments of intense hostility and uneasy diplomacy. With Iran situated in the heart of the Middle East—a region home to the world’s most abundant oil and gas reserves—the threat of a full-scale U.S. war with Iran sends immediate shockwaves through global energy markets. For the American oil and gas industry, the repercussions would be multifaceted, affecting prices, supply chains, infrastructure, investment, geopolitics, and the transition to cleaner energy sources.

This article explores in depth how such a conflict would impact the U.S. oil and gas sector—from upstream operations to consumer prices—through both immediate disruptions and long-term structural shifts.

Chapter 1: The Strategic Oil Chokepoint — Strait of Hormuz

The Strait of Hormuz is a 21-mile-wide passage that handles approximately 20% of the world’s petroleum, including exports from Saudi Arabia, Iraq, Kuwait, UAE, and Iran. In the event of war, Iran has repeatedly threatened to close or disrupt this chokepoint. Even though the U.S. has become less reliant on Middle Eastern oil due to its shale revolution, the global oil price is still influenced by international supply-demand dynamics. Any disruption in the Strait of Hormuz could cause a sharp increase in oil prices worldwide.

While American oil production is mostly domestic, its downstream processes such as refining and petrochemical production, and even pricing, are globally integrated. A war scenario would cause massive volatility in Brent and WTI prices. It would also result in a spike in insurance rates for oil tankers, trigger panic-driven speculative trading, and affect the availability of heavy crudes used by Gulf Coast refiners.

Chapter 2: Immediate Impacts on U.S. Oil Prices and Gasoline Costs

Wars create uncertainty, and markets detest uncertainty. The last significant military tension with Iran, such as the killing of General Qassem Soleimani in 2020, caused oil prices to rise sharply overnight. A full-blown war would likely push crude oil prices well above $100 to $150 per barrel in the short term. Gasoline prices could exceed $6 to $7 per gallon depending on the duration and intensity of the conflict. The situation could also lead to fuel rationing or the implementation of emergency energy measures at the state level.

A sustained spike in oil prices would ripple through the broader economy. Higher transportation and shipping costs would lead to increased prices for goods and services. This inflationary pressure could influence the Federal Reserve’s interest rate policy, complicating economic recovery efforts.

Chapter 3: U.S. Energy Independence – Myth vs. Reality

Although America has become a net exporter of petroleum in recent years, it still imports specific grades of oil and relies on global benchmarks like Brent for pricing. The narrative of U.S. energy independence is more nuanced than it appears. American refiners still import heavy crude that domestic sources do not provide in sufficient quantities. Gasoline is priced globally, and global turmoil affects domestic sentiment and market behavior.

The Strategic Petroleum Reserve (SPR) holds around 350 to 400 million barrels of oil. In a prolonged conflict, the government may draw from it to stabilize prices. However, SPR withdrawals are temporary measures, and the physical logistics of release versus consumption are complex. Global traders may interpret SPR use as a desperation move, potentially worsening market volatility.

Chapter 4: Supply Chain and Infrastructure Vulnerabilities

Iran has demonstrated cyber capabilities that have previously targeted U.S. infrastructure. In a war scenario, the oil and gas industry would likely become a prime target for such cyberattacks. Pipeline control systems, such as those seen in the Colonial Pipeline incident, refineries, LNG terminals, and data centers connected to the grid interface could all be at risk.

Iran could also physically attack American oil infrastructure abroad, particularly in countries like Iraq or the UAE. Such actions could include drone or missile attacks on production sites, disruption of joint ventures with global oil majors, and targeting of U.S.-flagged tankers. These disruptions would further compound market instability.

Chapter 5: Domestic Oil Production Challenges and Opportunities

Higher oil prices typically benefit U.S. producers, especially shale companies. A war would likely trigger increased drilling and production activity, a spike in share prices of oil and gas firms, and a rise in job creation in oil-producing states such as Texas, North Dakota, and New Mexico.

However, expanding production is not seamless. The industry would likely face equipment shortages, including rigs, pipes, and sand, along with labor constraints. Permitting delays and environmental opposition could also impede growth.

Too much price fluctuation can negatively impact the planning cycles of oil companies, particularly for smaller producers with narrow margins, firms with high debt levels, and midstream companies that rely on steady throughput to maintain profitability.

Chapter 6: The LNG Market and Global Natural Gas Implications

The United States is the world’s top exporter of LNG. A war would likely increase global demand for LNG as Europe seeks alternatives to pipeline gas and shifts toward seaborne supply. This could create infrastructure bottlenecks at U.S. Gulf Coast terminals and drive up domestic natural gas prices, especially during the winter months.

Iran, which holds the world’s second-largest gas reserves, currently plays a minimal role in global gas markets due to sanctions. A war would likely delay Iran’s potential reintegration into global energy markets for decades, further tightening global supply.

Chapter 7: Environmental and Regulatory Ramifications

In a war-induced energy emergency, the U.S. may temporarily ease environmental restrictions on drilling and refining. This could also lead to delays in clean energy and emissions regulations and a possible expansion of offshore and federal land leases for hydrocarbon extraction.

The Biden administration’s clean energy targets could face political backlash if a war-driven oil crisis forces a renewed reliance on fossil fuels. This might result in the reopening of dormant coal and oil power plants, a slowdown in electric vehicle adoption due to higher battery costs, and a general reprioritization of energy security over climate objectives.

Chapter 8: Impact on Energy Investment and Financial Markets

A war would significantly alter investor behavior. Investors might shift toward safer assets such as gold, bonds, and oil, leading to increased valuation of oil majors and defense contractors. At the same time, renewable energy stocks could decline as national budgets are reprioritized.

Sovereign wealth funds, pension funds, and hedge funds would likely reallocate capital toward fossil fuel-related assets. They might invest more in energy infrastructure security, including both cyber and physical protections, and reduce their exposure to emerging markets located near the conflict zone.

Chapter 9: Strategic Realignment of U.S. Energy Policy

Following a conflict, the United States would likely prioritize rebuilding its strategic reserves, incentivizing domestic energy storage and refining capacity, and securing strategic minerals and battery components essential for energy security.

New federal policies could include tax breaks for domestic producers, fast-tracked permitting processes under national security exceptions, and increased Department of Energy funding for fossil fuel research and development.

Chapter 10: The Geopolitical Domino Effect on OPEC, Russia, and China

Iran is a key member of OPEC. A war could destabilize OPEC cohesion, empower countries like Saudi Arabia and the UAE diplomatically, and cause internal friction among oil-producing nations regarding production quotas.

Russia might benefit from the situation, as increased oil and gas demand from Europe and Asia could help it offset the impact of existing sanctions. Russia would also gain the ability to exert more pressure on energy-poor European countries.

China would likely pursue energy diversification strategies, seeking alternative suppliers in Africa, Venezuela, and Russia. At the same time, China might accelerate its investments in green energy and electric vehicles while engaging in diplomacy with Gulf states to protect its energy imports.

Chapter 11: Long-Term Shifts in Global Energy Landscape

The conflict would likely lead to the development of new pipelines, LNG terminals, and strategic corridors designed to bypass Iran. Projects connecting Africa to Europe, U.S. energy partnerships with India, and Central Asian oil routes could gain prominence.

Paradoxically, the war could also accelerate the global energy transition. Governments might increase support for renewable energy sources such as solar, wind, and hydrogen. Decentralized microgrids could become more popular to reduce geopolitical risks, and innovations in battery storage and energy efficiency could receive greater funding and attention.

Chapter 12: Preparedness and Risk Mitigation for U.S. Energy Firms

Energy firms must develop detailed war-contingency plans that include building supply chain redundancies, enhancing cybersecurity firewalls, and acquiring insurance hedges against operational shutdowns.

Companies offering a diversified energy portfolio that includes oil, gas, and renewables are likely to manage volatility more effectively. These firms may also attract long-term investors focused on environmental, social, and governance (ESG) factors and position themselves as future-ready enterprises.

Conclusion: A War of Energy Consequences

A U.S. war with Iran would be catastrophic not just for the region but for the delicate balance of the global energy economy. For the American oil and gas industry, the impacts would include price surges, cybersecurity threats, infrastructural challenges, and dramatic shifts in policy. In the short term, the industry might benefit from higher prices and increased domestic investment. However, long-term uncertainty, inflation, and global market disruption could severely impact both producers and consumers.

As the world edges closer to energy interdependence, conflicts like this underline the need for strategic planning, geopolitical awareness, and resilient infrastructure in America’s oil and gas industry.

In a decisive move to protect American industry and national security, President Joe Biden has intervened to block the proposed takeover of U.S. Steel Corporation by Japan’s Nippon Steel Corporation. The decision underscores the administration’s commitment to safeguarding critical domestic industries from foreign acquisition. Takeover of US Steel Blocked.

Takeover of US Steel by Nippon Steel Blocked

The proposed acquisition had raised concerns among policymakers and industry experts about the potential impact on the U.S. steel sector, a cornerstone of the nation’s infrastructure and defense industries. U.S. Steel, one of the oldest and largest steel manufacturers in the United States, plays a vital role in supplying materials for construction, transportation, and military applications.

According to administration officials, the move aligns with the broader policy agenda to ensure the resilience of U.S. supply chains and the protection of strategic assets. “We must prioritize the long-term economic and national security interests of the United States,” a White House spokesperson stated.

Nippon Steel, Japan’s largest steel producer, had expressed interest in the acquisition as part of its global expansion strategy. The company emphasized that the deal would benefit both parties by fostering technological collaboration and increasing production efficiency. However, U.S. officials remained unconvinced, citing risks related to foreign control over critical infrastructure.

Industry reactions to the decision have been mixed. Some stakeholders applauded the administration’s proactive stance in shielding a key domestic industry, while others voiced concerns about potential disruptions to foreign investment and trade relations with Japan.

“This decision sends a strong message about the importance of maintaining domestic control over critical industries,” said an industry analyst. “However, it also raises questions about the balance between protectionism and fostering global partnerships.”

The blocked acquisition comes amid a broader effort by the Biden administration to bolster the U.S. industrial base and reduce reliance on foreign entities for essential materials. Recent policies, such as the CHIPS and Science Act and the Inflation Reduction Act, highlight a similar focus on revitalizing domestic manufacturing and securing supply chains.

While Nippon Steel has yet to release an official statement regarding the blocked bid, analysts predict that the company may seek alternative avenues for collaboration with U.S.-based firms or pursue other international opportunities. Meanwhile, U.S. Steel has reaffirmed its commitment to remaining an independent leader in the global steel industry.

This move by President Biden is expected to influence future foreign investment strategies and could set a precedent for how the U.S. approaches similar situations involving critical industries. Connect with Factoring Specialist Chris Lehnes

Oil-Service Providers Say Producers Are Becoming More Cautious About Spending

As oil prices experience increased volatility and global economic uncertainties weigh on the energy market, oil-service companies report that producers are growing more conservative in their capital spending. This shift marks a notable change from the recent period of higher oil prices, when many oil producers were more aggressive in ramping up drilling activity and investing in new projects. The tightening of budgets reflects broader concerns about market stability, geopolitical risks, and the potential for a downturn in global demand for crude oil.

Spending Slowdown Amid Price Volatility

Oil-service providers, which offer critical equipment, technology, and expertise to exploration and production (E&P) companies, are seeing a cooling in demand for their services as oil producers scale back capital expenditures. After a relatively strong period driven by robust crude prices and rising demand, there is now a noticeable shift toward caution.

In recent months, oil prices have fluctuated significantly due to a range of factors, including concerns about slowing economic growth in major markets such as China, shifts in global energy policy, and uncertainty around OPEC’s production decisions. As a result, oil producers are adopting a more risk-averse approach, reducing drilling activity and delaying or cancelling some exploration projects.

Impact on Oil-Service Companies

For oil-service companies, this more cautious spending environment means reduced demand for their services. Many companies in the sector had anticipated continued growth in 2024, fueled by the expectation of stable or rising oil prices. However, the recent market environment has led some of them to revise their forecasts. The shift in producer spending could slow the recovery for service providers, who had already endured a challenging period during the pandemic when low oil prices caused a sharp pullback in drilling activity.

While some service providers have reported ongoing demand for maintenance and production-optimization services, new drilling projects have been more limited. Companies are focusing on improving efficiency and extending the life of existing wells rather than committing to large-scale exploration and production investments.

Factors Driving Producer Caution

Market Uncertainty: The volatility in oil prices is one of the main reasons for the more cautious approach from oil producers. The global oil market has faced a series of disruptions in recent years, ranging from the pandemic’s impact to the Russia-Ukraine conflict, which has created uncertainty in global energy markets.

Cost Inflation: Rising costs for labor, equipment, and materials have also contributed to the hesitation among producers. Higher input costs make new projects less attractive, particularly if oil prices are not expected to rise significantly in the near future.

Environmental, Social, and Governance (ESG) Pressure: Another factor influencing spending decisions is the growing pressure on oil companies to improve their environmental footprint. More companies are dedicating resources to low-carbon initiatives or considering how new regulations may affect future oil demand.

Concerns About Demand: Long-term demand for oil is increasingly in question as the global energy transition toward renewable sources gathers pace. This has led some companies to reevaluate their long-term strategies, focusing less on expanding oil production and more on maximizing returns from existing assets.

Outlook for 2024 and Beyond

The cautious stance among producers could have significant implications for the oil-service sector. If oil prices remain unstable or decline further, there could be prolonged reductions in capital spending, putting additional pressure on oil-service providers. However, if demand stabilizes and prices strengthen, there could be a resurgence in activity later in the year.

Additionally, service companies that can adapt to the changing needs of producers by offering innovative, cost-effective solutions may be better positioned to navigate the current environment. This includes technologies aimed at improving well productivity, lowering emissions, or enhancing operational efficiency.

In summary, while the oil industry remains essential to the global energy landscape, the current climate of uncertainty is prompting producers to exercise greater caution in their spending, impacting oil-service providers and the overall supply chain. The path forward will likely depend on the interplay of market forces, geopolitical developments, and the pace of the global energy transition.

Fuel Prices Down Amidst Global Economic Adjustments

In recent weeks, consumers and industries alike have welcomed a significant decrease in fuel prices. This decline, driven by a combination of global economic factors, has brought relief to various sectors, particularly transportation and logistics, which are heavily dependent on fuel.

Factors Contributing to the Decline:

Global Oil Supply Increase: A key factor in the recent drop in fuel prices is the increase in global oil supply. Major oil-producing countries, particularly those in the Middle East, have ramped up production. This surge in supply has outpaced demand, leading to a decrease in crude oil prices, which directly influences the cost of fuel.

Slowing Global Economic Growth: The global economy has experienced a slowdown, particularly in major economies like China and the Eurozone. This slowdown has led to reduced industrial activity, thereby decreasing the demand for oil and fuel. As demand diminishes, prices naturally follow suit.

Technological Advancements in Alternative Energy: Another contributing factor is the ongoing advancements in alternative energy sources. As renewable energy technologies become more efficient and widely adopted, the dependence on fossil fuels has started to wane. This shift has put additional pressure on fuel prices, pushing them downwards.

Geopolitical Stability: Recent geopolitical developments have also played a role in stabilizing fuel prices. In regions where conflict previously threatened oil supplies, diplomatic efforts have led to more stable production and exportation of oil, easing concerns about supply disruptions.

Impact on Consumers and Industries:

Transportation Sector: The transportation sector is one of the primary beneficiaries of the decline in fuel prices. Lower fuel costs have reduced operational expenses for airlines, shipping companies, and trucking firms, leading to potential savings that could be passed on to consumers.

Consumer Goods: With lower transportation costs, the prices of consumer goods could see a decrease, especially for products that rely heavily on logistics. This could provide a much-needed boost to consumer spending and overall economic activity.

Agriculture: The agriculture sector, which is highly dependent on fuel for machinery and transportation of goods, is also likely to benefit. Lower fuel costs can help reduce the overall cost of production, potentially leading to more competitive pricing of agricultural products.

Future Outlook:

While the current decline in fuel prices offers immediate benefits, experts caution that it may not be sustainable in the long term. Factors such as potential geopolitical tensions, environmental policies, and the unpredictable nature of global oil markets could reverse the trend. Additionally, as the global economy recovers, demand for fuel is expected to rise, which could put upward pressure on prices once again.

Conclusion:

The recent drop in fuel prices is a welcome development for both consumers and industries. However, the situation remains fluid, and it is important for stakeholders to remain vigilant and adaptable to future changes in the global economic landscape. For now, the decline provides a window of opportunity to explore more sustainable energy practices and strengthen economic resilience.

The supply chain has faced numerous challenges in recent years, exacerbated by global events such as the COVID-19 pandemic, geopolitical tensions, and natural disasters. Here are some of the key ongoing challenges:

Ongoing Supply Chain Challenges

Supply Chain Disruptions:

Pandemic Impact: COVID-19 led to factory shutdowns, port closures, and labor shortages, causing significant delays and shortages in various sectors.

Geopolitical Tensions: Trade wars, tariffs, and sanctions have disrupted international trade flows and created uncertainties in supply chain management.

Logistics and Transportation Issues:

Port Congestion: Major ports around the world have faced severe congestion, resulting in long wait times for ships to unload.

Freight Capacity Shortages: A lack of available shipping containers and trucks has hindered the movement of goods.

Labor Shortages:

Skilled Labor: There is a growing shortage of skilled workers in manufacturing, logistics, and transportation.

Workforce Retention: High turnover rates and the need for better working conditions have impacted the stability of labor supply.

Raw Material Shortages:

Semiconductors: The global chip shortage has affected industries ranging from automotive to electronics.

Other Raw Materials: Shortages in materials like lumber, steel, and plastics have led to increased costs and production delays.

Increasing Costs:

Transportation Costs: Rising fuel prices and transportation fees have driven up overall supply chain costs.

Commodity Prices: Inflation and increased demand have caused spikes in the prices of raw materials.

Environmental and Sustainability Concerns:

Carbon Footprint: Companies are under pressure to reduce their environmental impact, which requires significant changes in supply chain practices.

Sustainable Sourcing: There is an increasing demand for sustainably sourced materials, which can be more expensive and harder to secure.

Technological Challenges:

Integration of New Technologies: Implementing advanced technologies such as AI, IoT, and blockchain can be complex and require significant investment.

Cybersecurity: As supply chains become more digitized, they become more vulnerable to cyberattacks.

Regulatory Compliance:

Changing Regulations: Companies must navigate an evolving landscape of regulations related to trade, labor, and environmental standards.

Customs and Tariffs: Changes in customs procedures and tariff structures can cause delays and increase costs.

Risk Management:

Natural Disasters: Events like earthquakes, hurricanes, and floods can disrupt supply chains unexpectedly.

Political Instability: Political unrest in key manufacturing or shipping regions can cause sudden disruptions.

Demand Forecasting and Inventory Management:

Fluctuating Demand: Accurately predicting demand has become more challenging due to rapid changes in consumer behavior.

Inventory Levels: Balancing inventory to avoid overstocking or stockouts is increasingly complex in a volatile market.

Addressing these challenges requires a multifaceted approach involving better risk management, investment in technology, strategic partnerships, and a focus on sustainability. Companies must remain agile and adaptable to navigate the complex and ever-changing landscape of global supply chains.