If you’ve been keeping an eye on the economic headlines lately, you might have braced yourself for a sluggish jobs report this May. With rising inflation and the economic ripple effects of the ongoing conflict in Iran, many analysts were predicting a significant cooldown in hiring.

But the U.S. labor market just threw a massive curveball.

Here is a breakdown of the May 2026 jobs report, what the numbers actually mean, and why the American economy continues to show surprising resilience.

The Headline Numbers: Blowing Past Estimates

Economists were largely projecting a modest gain of around 85,000 jobs for May. Instead, the Labor Department revealed that U.S. employers added a robust 172,000 new jobs.

Total Jobs Added: 172,000 (vs. 85,000 expected)

Unemployment Rate: Held steady at 4.3%

Wage Growth: Average hourly earnings ticked up by 0.3% month-over-month.

April Revisions: April’s numbers were also sharply revised upward from 115,000 to an impressive 179,000.

This wasn’t just a slight beat; it was a doubling of expectations, indicating that businesses are still finding reasons to hire and expand, even in an uncertain macroeconomic climate.

Where Are the Jobs Coming From?

While the headline number is strong, the growth wasn’t entirely uniform across the board. The heavy lifting was done by a few key sectors:

Healthcare and Social Services: Continuing a long-running trend, healthcare remains a massive engine for job creation, accounting for a significant chunk of the new roles.

Leisure and Hospitality: As the weather warms up, consumer demand for travel and dining out remains steady, prompting strong hiring in this sector.

Local Government: Public sector hiring also saw notable gains.

Conversely, some sectors felt the pinch. Employment in financial activities slipped slightly, reflecting tighter borrowing conditions and shifting corporate strategies.

Resilience Amid Global Headwinds

The most fascinating takeaway from this report isn’t just the sheer number of jobs added—it’s the context in which they were created.

Since the escalation of the war in Iran earlier this year, global energy markets have been incredibly volatile. Spiking oil prices have renewed fears of inflation, putting pressure on consumer wallets and business operational costs alike. Despite these immense headwinds, the domestic labor market has absorbed the shock remarkably well.

The fact that employers are still confident enough to add 172,000 workers to their payrolls suggests an underlying structural strength in the U.S. economy that is, for now, overriding geopolitical anxieties.

What This Means for the Federal Reserve

Of course, a hot jobs report complicates things for the Federal Reserve.

When the labor market is strong and wage growth is steady, inflation tends to remain sticky. Prior to this report, there was speculation that the Fed might keep interest rates flat for the rest of the year. However, this display of economic resilience might push policymakers in a more hawkish direction. While the steady 4.3% unemployment rate means the labor market isn’t overheating, markets are now bracing for the possibility that the Fed could lift rates at least once by the end of 2026 to keep inflationary pressures in check.

The Bottom Line

The May 2026 jobs report is a potent reminder that the U.S. economy rarely behaves exactly as modeled. While the challenges of inflation and global conflict are very real, the underlying demand for labor remains undeniably robust. Whether this momentum can be sustained into the summer remains to be seen, but for now, the job market continues to defy the odds.

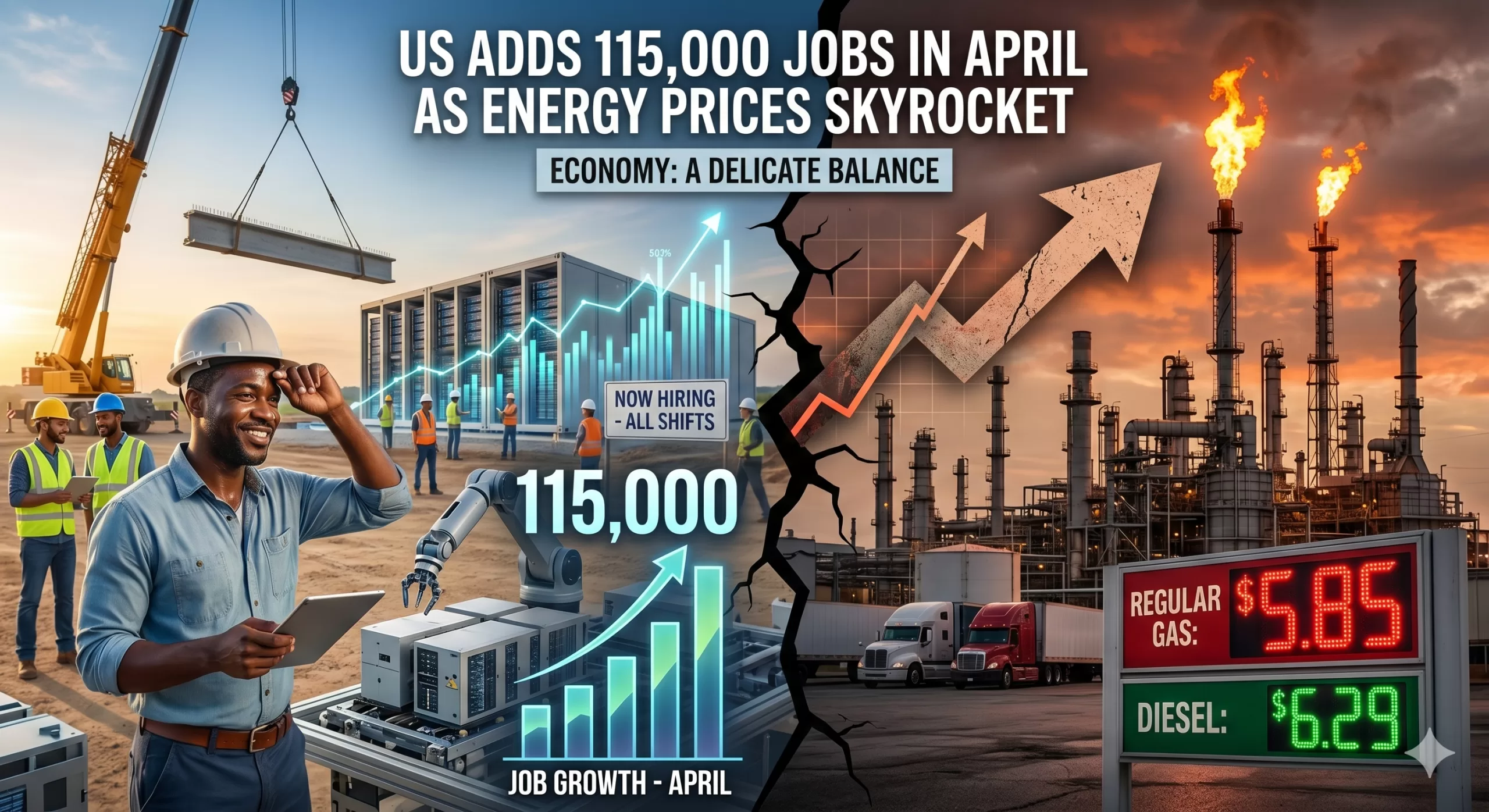

The latest Labor Department report released today, May 8, 2026, reveals a complex picture of the American economy. While the addition of 115,000 jobs in April far exceeded the conservative forecasts of 65,000, this hiring momentum is colliding with a volatile energy market and geopolitical tensions that are keeping consumers—and the Federal Reserve—on edge.

The April Jobs Numbers: A Surprising Resilience

Despite a year of uneven growth and high interest rates, the labor market continues to find its footing. The 115,000 gain marks a significant win for an economy that many feared was cooling too rapidly.

Unemployment Rate: Held steady at 4.3%, a remarkably low figure given the broader economic headwinds.

Sector Highlights: Growth was fueled by health services, education, and construction. Notably, the boom in AI data center construction is providing a sturdy floor for blue-collar employment.

Small Business Bounce: Much of the hiring surge came from small businesses (fewer than 20 employees), suggesting that local optimism remains resilient despite macro-level volatility.

The Energy Crisis: A Shadow Over the Recovery

While the job gains are a reason for celebration, they are being offset by a painful reality at the pump and in utility bills. Crude oil prices have breached the $100-per-barrel mark, driven largely by recent hostilities in the Strait of Hormuz.

For the average American household, the “energy tax” is real. Rising gas prices are eating into the gains from recent tax refunds and wage growth. This creates a “push-pull” dynamic:

The Push: Robust hiring and steady wages ($6.6\%$ growth for job-switchers) give consumers spending power.

The Pull: Skyrocketing energy costs increase the cost of goods and transportation, effectively neutralizing those wage gains for many families.

What This Means for the Federal Reserve

The Fed is now in a delicate position. Usually, a strong jobs report would signal that the economy can handle higher interest rates. However, with energy prices driving “cost-push” inflation, Fed Chair Jerome Powell and his team must decide if the labor market is stable enough to wait out the energy spike or if they need to pivot to protect growth.

Traders are currently betting on a “stable backdrop,” but the volatility in the Middle East remains the ultimate wildcard. If energy prices continue their upward trajectory, the modest 115,000-job gain might be harder to replicate in May.

Looking Ahead

The April report proves that the U.S. economy is more durable than skeptics predicted, but it also highlights our vulnerability to global supply shocks. As we move into the summer months, all eyes will be on two things: the price of a gallon of gas and whether the AI-driven infrastructure boom can continue to carry the weight of the labor market.

Bottom Line: The American worker is still in demand, but the cost of living—fueled by a chaotic energy market—is the primary threat to this hard-won stability.

A Surprising Spring: March Jobs Report Shatters Expectations

The U.S. labor market just delivered a spring surprise that few saw coming. According to the latest data released today by the Bureau of Labor Statistics (BLS), the U.S. economy added 178,000 jobs in March, vastly outperforming economist forecasts which had hovered around a modest 60,000 to 70,000.

After a dismal February that saw a revised loss of 133,000 jobs, this rebound signals a resilient—if complex—economic landscape.

The Numbers at a Glance

The March report offers a refreshing change of pace for a labor market that has felt “frozen” for much of the past year.

Nonfarm Payrolls: +178,000 (Expected: ~70,000)

Unemployment Rate: 4.3% (Down from 4.4% in February)

Revisions: January’s figures were revised upward to 160,000, though the two-month net revision slightly dampened the overall trend.

What’s Driving the Growth?

The recovery wasn’t uniform across the board. While the headline number is strong, the “engine” of the U.S. economy remains highly concentrated:

The Healthcare Titan: Once again, the health care and social assistance sector did the heavy lifting, adding 76,000 jobs last month. This sector has essentially been the primary life support for the labor market over the last year.

The “Bounce Back” Factor: Part of the March surge is attributed to the return of approximately 31,000 Kaiser Permanente employees who were on strike in February, along with more favorable weather conditions across the country.

The Gender Shift: Interestingly, recent trends show that women now hold more jobs than men in the nonfarm economy—a structural shift driven by the strength of female-dominated sectors like education and health, while male-concentrated sectors like manufacturing continue to cool.

The Shadows on the Horizon: Geopolitics and Oil

Despite the optimistic numbers, experts are urging caution. The report arrives amidst significant geopolitical tension, specifically the ongoing conflict in Iran.

“We’ve got a much more difficult spring job market than we had hoped given the higher prices at the pump and the supply chain disruptions that are going to come from the war,” says Diane Swonk, chief economist at KPMG.

With gas prices spiking above $4 a gallon for the first time since 2022, many fear that the March gains may be a “last hurrah” before the economic impact of the war and energy costs fully settle into corporate hiring plans.

The Bottom Line

The U.S. economy has shown it still has plenty of fight left. A 4.3% unemployment rate remains historically healthy, and the “low-hire, low-fire” stalemate of 2025 appears to be thawing.

However, for job seekers and businesses alike, the road ahead remains fogged by uncertainty. Between the rapid integration of Artificial Intelligence, fluctuating inflation (which dipped to 2.3% before ticking back up), and global instability, “cautious optimism” remains the phrase of the day.

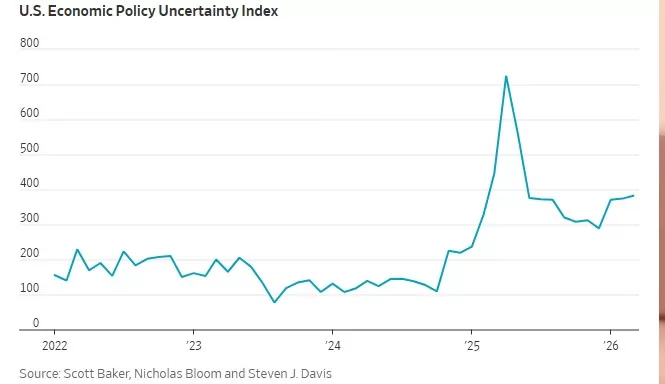

If the global economy feels like a high-wire act lately, you aren’t alone. We are currently navigating a “polycrisis“—a fancy term for when multiple major headaches (inflation, geopolitical tension, and shifting labor markets) all hit the fan at the same time.

We are standing on a narrow ledge. One side leads to a hard landing; the other leads to a stabilized “new normal.” Here is a look at the forces threatening to push us off, and the safety nets that might just pull us back.

The Push: What Could Tip Us Over?

It doesn’t take a wrecking ball to cause a recession; sometimes, it just takes a few well-placed dominos. Here are the primary risks:

The “Higher for Longer” Fatigue: While central banks use interest rates to cool inflation, keeping them elevated for too long puts immense pressure on household debt and corporate margins. If the “lag effect” hits all at once, consumer spending—the engine of the economy—could stall.

Geopolitical Aftershocks: Energy prices are notoriously sensitive to global conflict. Any significant escalation in major trade corridors can reignite supply chain chaos, sending the cost of goods back into the stratosphere.

The Commercial Real Estate Ghost Town: With remote work now a permanent fixture, many office buildings are sitting half-empty. As these property loans come due for refinancing at higher rates, we could see a localized banking tremor.

The Pull: What Could Help Us Pull Through?

It’s not all doom and gloom. There are several structural “muscles” keeping the economy upright:

The Resilient Labor Market: Despite tech layoffs making headlines, overall unemployment remains historically low. As long as people have jobs, they tend to keep spending, which provides a powerful floor for the economy.

The Productivity “AI Bump”: We are at the beginning of a massive technological shift. Early adoption of generative AI is already beginning to streamline workflows and reduce operational costs, which could lead to a non-inflationary growth spurt.

Household Balance Sheets: Unlike the 2008 crash, many consumers and corporations locked in low interest rates years ago. This “debt buffer” has bought the private sector time to adjust to the new economic reality.

The Bottom Line: Balance, Not Freefall

The economy isn’t necessarily “broken,” but it is transitioning. We are moving away from an era of “free money” and into an era where efficiency and strategic investment matter again.

Scenario

Key Driver

Likely Outcome

The Hard Landing

Persistent inflation + high rates

Brief but sharp recession; rising unemployment.

The Soft Landing

Controlled cooling + tech growth

Flat growth for a year, followed by a steady recovery.

The No Landing

Continued high spending

Economy stays hot, but rates stay high indefinitely.

The Takeaway: While the ledge is narrow, the path across is still visible. Navigating the next twelve months will require agility from policymakers and patience from investors. We may be on the edge, but we aren’t over it yet..

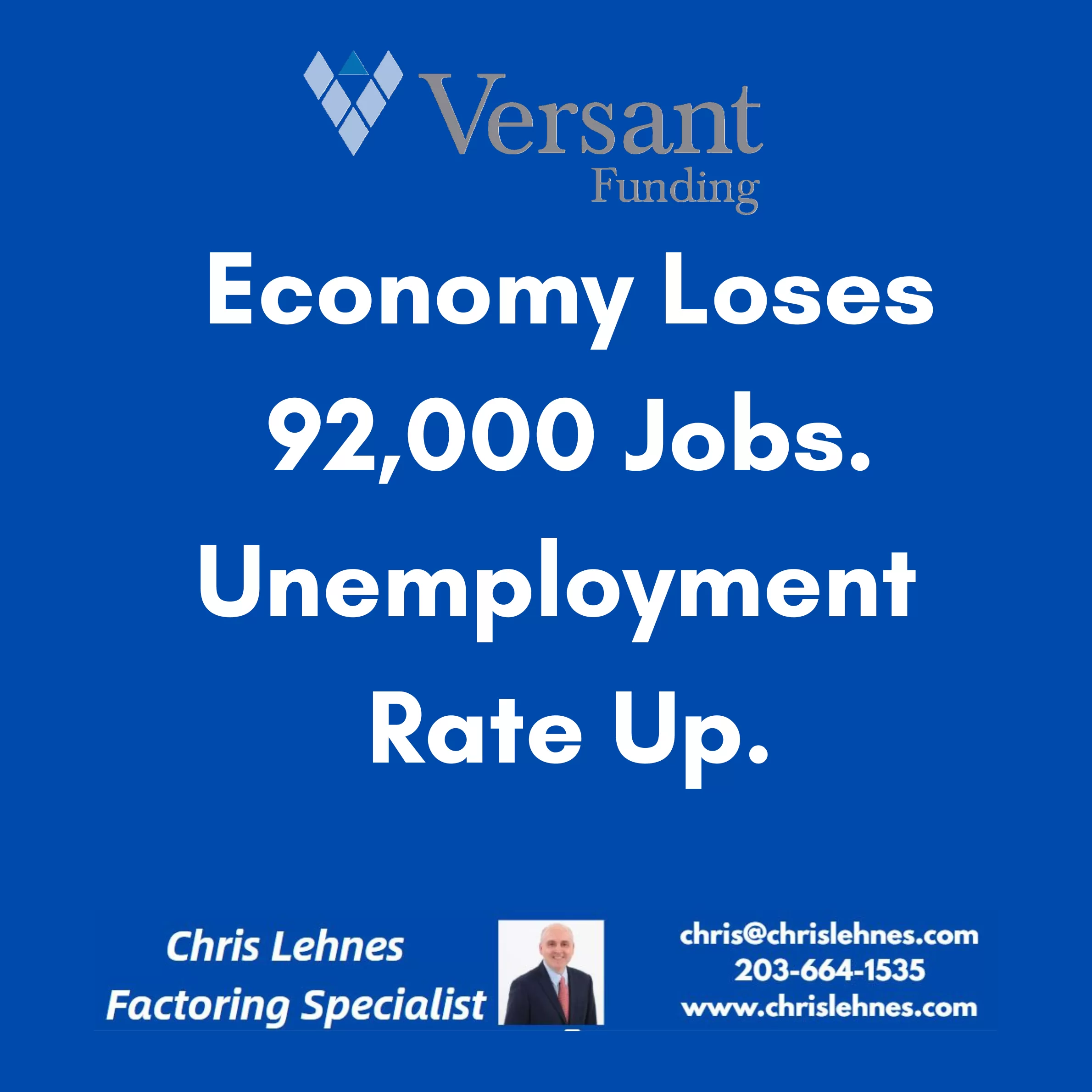

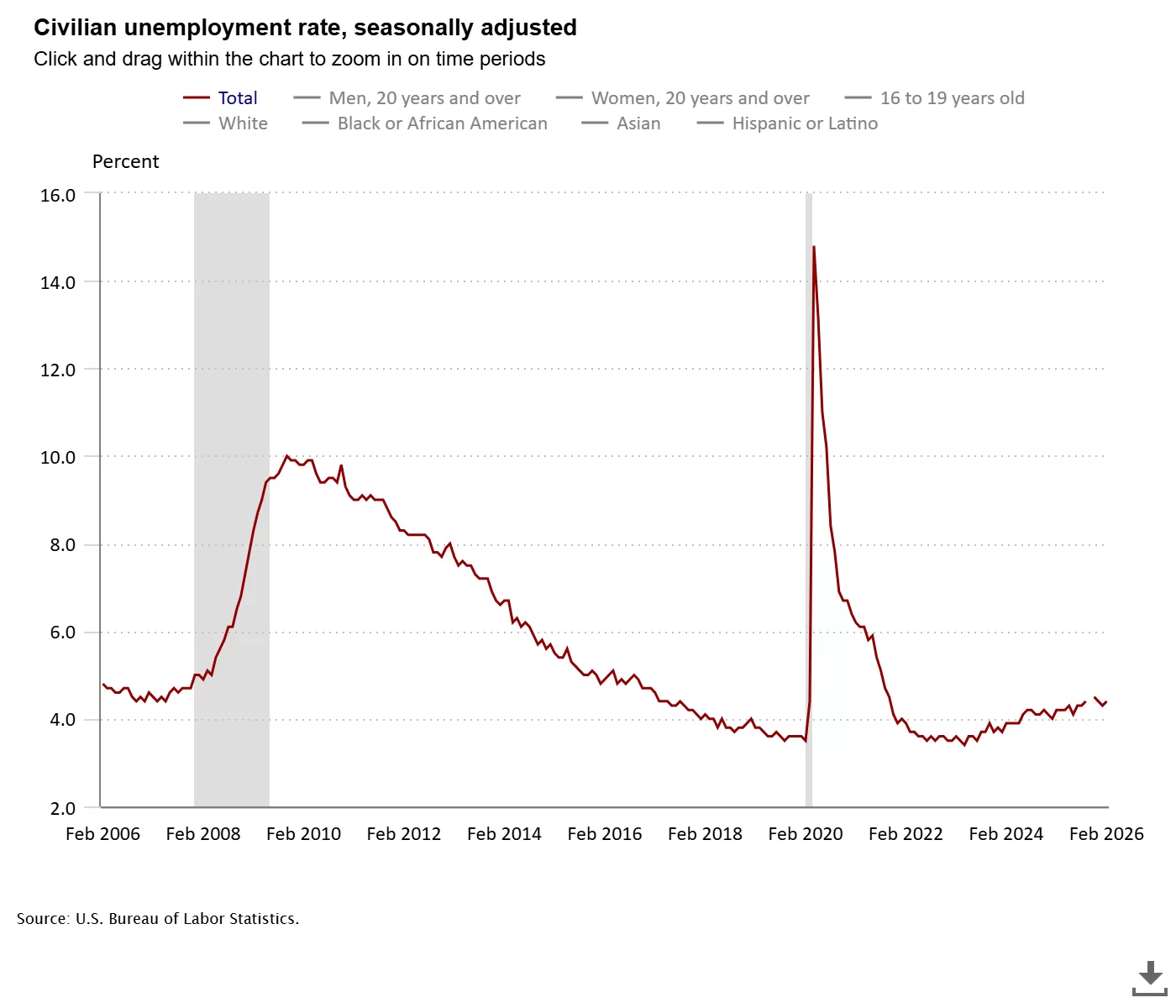

Economy Sheds 92,000 Jobs. The American labor market hit a significant speed bump last month, as the Bureau of Labor Statistics (BLS) reported a loss of 92,000 jobs for February 2026. This unexpected contraction caught economists off guard, as many had projected a modest gain of roughly 60,000 positions.

Coupled with the job losses, the national unemployment rate ticked up to 4.4%, rising from 4.3% in January. While the figure remains low by historical standards, the sudden reversal in momentum has reignited concerns about the underlying health of the economy amidst ongoing geopolitical tensions and domestic labor disputes.

The Numbers at a Glance

The February report was a stark contrast to the start of the year, which initially saw a healthy gain in January. However, even those numbers were revised downward, painting a picture of a job market that is struggling to maintain its footing.

Metric

February 2026 Data

Comparison

Nonfarm Payrolls

-92,000

Down from +126,000 (revised) in Jan

Unemployment Rate

4.4%

Up from 4.3%

December Revision

-17,000

Revised down from +48,000

Labor Force Participation

62.0%

Lowest level since December 2021

Key Drivers of the Decline

Several factors converged to create the “perfect storm” that led to February’s disappointing figures:

Labor Disputes: The healthcare sector, usually a reliable engine of growth, shed 28,000 jobs. Much of this was attributed to a major strike involving over 30,000 workers at Kaiser Permanente in California and Hawaii.

Harsh Winter Weather: Severe storms across the country likely hampered hiring in the construction sector, which saw a decline of 11,000 jobs.

Sector-Specific Weakness: The Information and Transportation/Warehousing sectors both lost 11,000 jobs, while the Federal Government continued its downward trend, losing 10,000 positions.

Geopolitical Uncertainty: The escalation of the conflict in the Middle East has driven up crude oil prices, injecting a new layer of caution into business spending and hiring plans.

“Just when it looked like the labor market was stabilizing, this report delivers a knock-down blow to that view. It’s bad news whichever way you look at it.”

— Olu Sonola, Head of U.S. Economics at Fitch Ratings.

Silver Linings and the Path Forward

Despite the gloomy headline, there were a few areas of resilience. Average hourly earnings rose by 0.4% for the month, representing a 3.8% increase year-over-year. This suggests that while hiring has slowed, those currently employed are still seeing wage growth that is largely keeping pace with inflation.

The Federal Reserve now faces a delicate balancing act. While the job losses might typically signal a need for interest rate cuts to stimulate the economy, the surge in energy prices due to the war in Iran keeps the threat of inflation high.

Economists will be looking toward the March report (scheduled for release on April 3rd) to determine if February was a temporary blip caused by weather and strikes, or the start of a more concerning long-term trend.

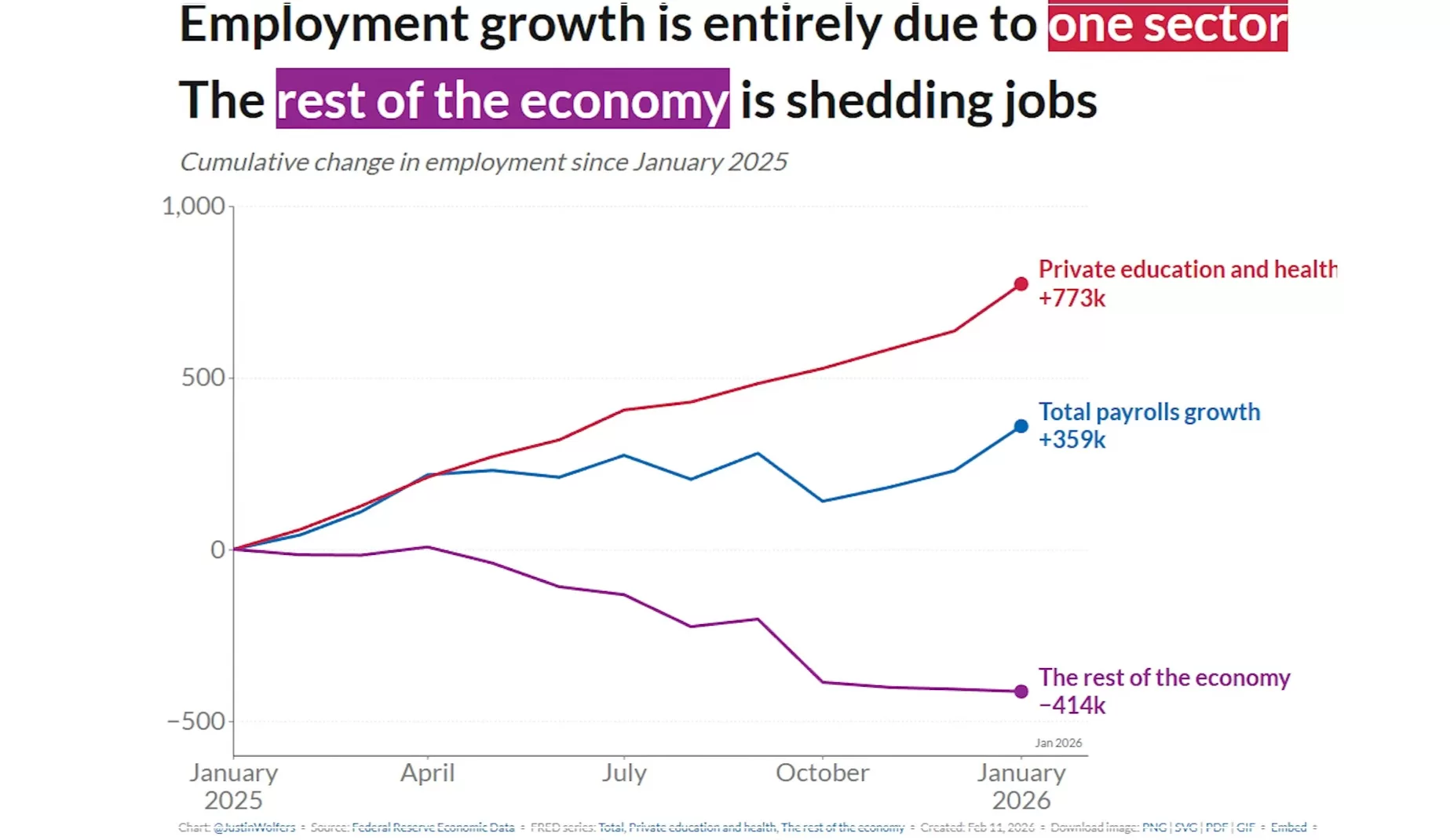

The U.S. labor market began 2026 with a surprising burst of energy, shaking off a sluggish 2025. According to the latest data from the Bureau of Labor Statistics (BLS) released on February 11, 2026, employers added 130,000 jobs in January—easily doubling December’s figures and blowing past economist expectations of roughly 70,000.

While the report was delayed by a week due to a brief federal government shutdown, the results suggest that the “hiring fatigue” seen late last year might be beginning to thaw.

The Numbers at a Glance

The January report offers a mix of resilience and necessary context for the year ahead:

Total Jobs Added: 130,000 (up from a revised 50,000 in December).

Unemployment Rate: Ticked down to 4.3% (from 4.4%).

Average Hourly Earnings: Rose by 0.4% in January, bringing the year-over-year increase to 3.7%.

Labor Force Participation: Remained steady at 62.5%.

Sector Winners and Losers

The growth wasn’t uniform across the board. In fact, a few key sectors carried the heavy lifting for the entire economy:

Healthcare & Social Assistance: This sector remains the titan of the U.S. job market, adding 124,000 jobs (82k in healthcare and 42k in social assistance).

Construction: Added a solid 33,000 jobs, largely driven by nonresidential specialty trade contractors.

The Tech & White-Collar Slump: Conversely, professional and business services and manufacturing continued to struggle, reflecting ongoing shifts in AI implementation and trade policy impacts.

Government: Federal employment saw a decline, partly a ripple effect of recent policy shifts and the temporary shutdown.

Why This Matters

After a tumultuous 2025—which was recently revised to show only 181,000 total jobs added for the entire year—this January figure is a massive sigh of relief. It suggests that while the economy isn’t sprinting, it’s found its footing.

“The January gains are a sign that the labor market is stabilizing,” says one economist. “However, the high concentration of growth in healthcare suggests a ‘one-legged stool’ economy that we need to watch closely.”

Looking Ahead

While 130,000 jobs is a “stronger footing,” the market remains complex. Layoffs in high-profile sectors like tech and transportation (notably Amazon and UPS) dominated January headlines, yet the aggregate data shows that other sectors are more than absorbing that displaced talent.

For job seekers, the message is clear: the opportunities are there, but they have shifted. Strategic hiring is the theme of 2026, with a high premium on specialized skills in healthcare, infrastructure, and adaptive technologies.

The January jobs report has effectively shifted the narrative for the Federal Reserve. While the 130,000 jobs added might seem modest by historical standards, it was a significant “beat” compared to expectations, and it has given the Fed a reason to tap the brakes on further interest rate cuts.

Here is how the latest data is influencing the Fed’s next move:

1. From “Easing” to “Holding”

Following three consecutive rate cuts in late 2025, the Federal Reserve held rates steady at its January 28, 2026 meeting, maintaining the federal funds rate at 3.5% to 3.75%. This jobs report reinforces that “pause.”

The Consensus: With the unemployment rate ticking down to 4.3% and job growth doubling December’s numbers, there is no longer an “emergency” need to stimulate the economy.

Market Sentiment: Before this report, some traders were betting on a March cut. Now, CME FedWatch tools show those odds have plummeted, with the consensus moving toward a “higher for longer” stance through at least the first half of the year.

2. Emerging Internal Division

The Fed is no longer acting in total unison. The January meeting saw a rare 10-2 vote, with two dissenting members actually pushing for another 25-basis-point cut due to lingering concerns about long-term hiring weakness.

The Hawks: Officials like Cleveland Fed President Beth Hammack and Dallas Fed President Lorie Logan have signaled that the Fed should “err on the side of patience,” arguing that current rates are “neutral”—neither helping nor hurting the economy.

The Doves: Those worried about the “one-legged stool” (growth coming only from healthcare) fear that without more cuts, sectors like tech and manufacturing will continue to bleed jobs.

3. The “Neutral Rate” Debate

Chair Jerome Powell recently noted that the economy is on a “firm footing” entering 2026. Analysts now believe the Fed is searching for the neutral rate—the sweet spot where inflation stays at 2% without triggering a recession.

Because average hourly earnings rose 0.4% in January (3.7% annually), the Fed is wary that cutting rates too soon could reignite inflation, especially with potential new trade tariffs on the horizon.

Key Dates to Watch

Event

Date

Significance

January CPI Report

Feb 13, 2026

Will confirm if the wage growth in the jobs report is driving up prices.

Fed “Beige Book”

Mar 4, 2026

Regional reports on how small businesses are actually feeling.

Next FOMC Meeting

Mar 17-18, 2026

The next formal window for a rate change decision.

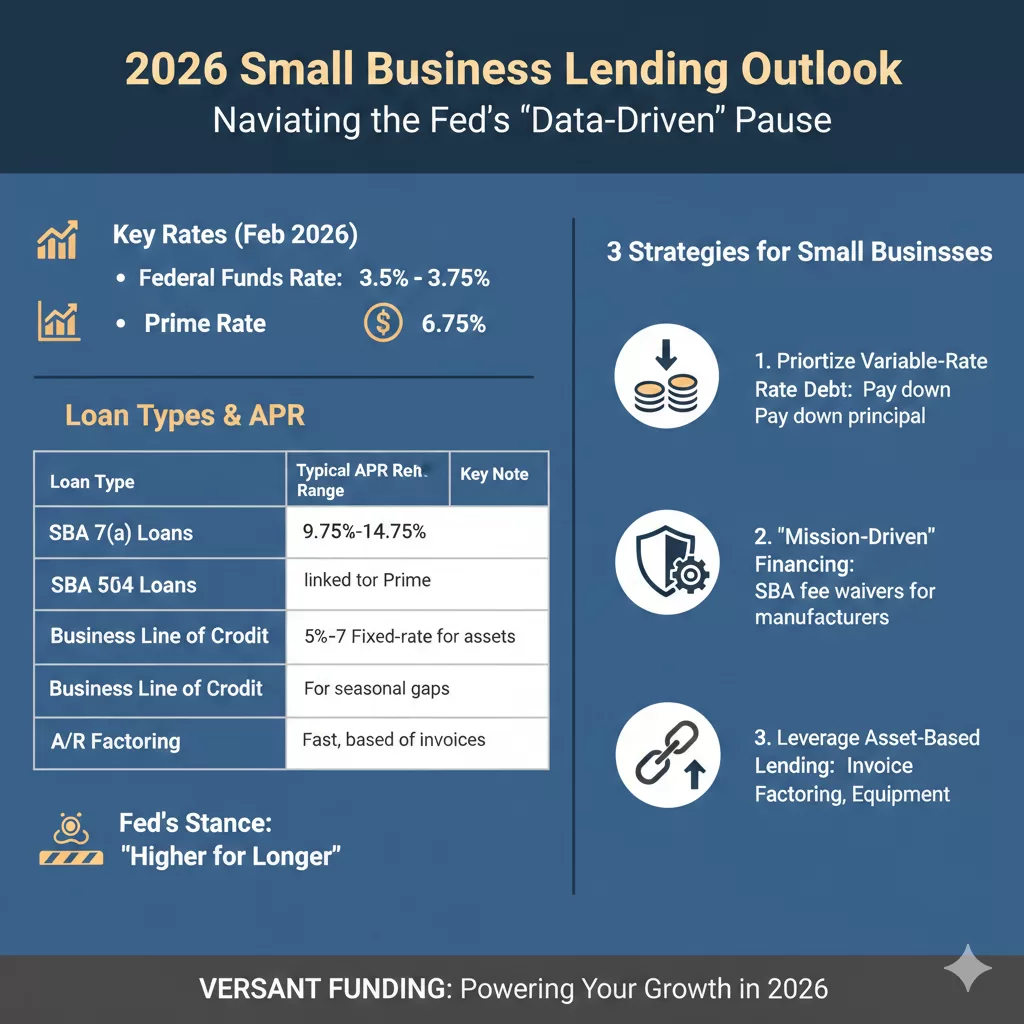

For a small business owner, the January jobs report isn’t just about hiring statistics—it’s a leading indicator for the cost of your next loan or line of credit.

Following the stronger-than-expected labor data, the Federal Reserve has hit “pause” on interest rate cuts. For businesses at Versant Funding and across the U.S., this means a period of “stabilized high” borrowing costs. Here is what your business needs to know to navigate the financial landscape of early 2026.

2026 Borrowing Outlook: The “Data-Driven” Pause

The Fed began 2026 by holding the federal funds rate steady at 3.5% to 3.75%. While the market had hoped for more aggressive easing, the surge of 130,000 new jobs in January has signaled to policymakers that the economy is not yet in need of more “cheap money.”

Current Lending Rates (As of February 2026)

Loan Type

Typical APR Range

Key Note

SBA 7(a) Loans

9.75% – 14.75%

Variable rates fluctuate with the Prime Rate (currently 6.75%).

SBA 504 Loans

5% – 7%

Fixed-rate; best for long-term real estate or equipment.

Business Lines of Credit

10% – 28%

Vital for seasonal inventory and payroll gaps.

Accounts Receivable Factoring

24% – 36%

High speed; based on invoice value rather than credit score.

Three Strategies for Small Businesses

With rates unlikely to drop significantly before the summer, owners should shift from “waiting for better rates” to “optimizing current cash flow.”

Prioritize Variable-Rate Debt: If you are carrying an SBA 7(a) loan or a variable line of credit, your payments will remain flat for now. Use this stability to pay down principal where possible, as the “higher for longer” stance means interest costs won’t be melting away anytime soon.

Look for “Mission-Driven” Financing: In 2026, the SBA is waiving guarantee fees for certain small manufacturers (NAICS 31-33). If your business fits this category, you could save thousands in upfront costs regardless of the interest rate.

Leverage Asset-Based Lending: If traditional bank term loans are too restrictive, consider Invoice Factoring or Equipment Financing. These options often focus more on the value of your assets (your unpaid invoices or machinery) than on the Fed’s baseline rates, providing more predictable access to capital during economic volatility.

The Bottom Line

The “stronger footing” of the U.S. labor market is a double-edged sword: it proves consumer demand is resilient, but it keeps the cost of capital elevated. For 2026, the most successful businesses will be those that prioritize liquidity and debt structure over simply chasing the lowest rate.

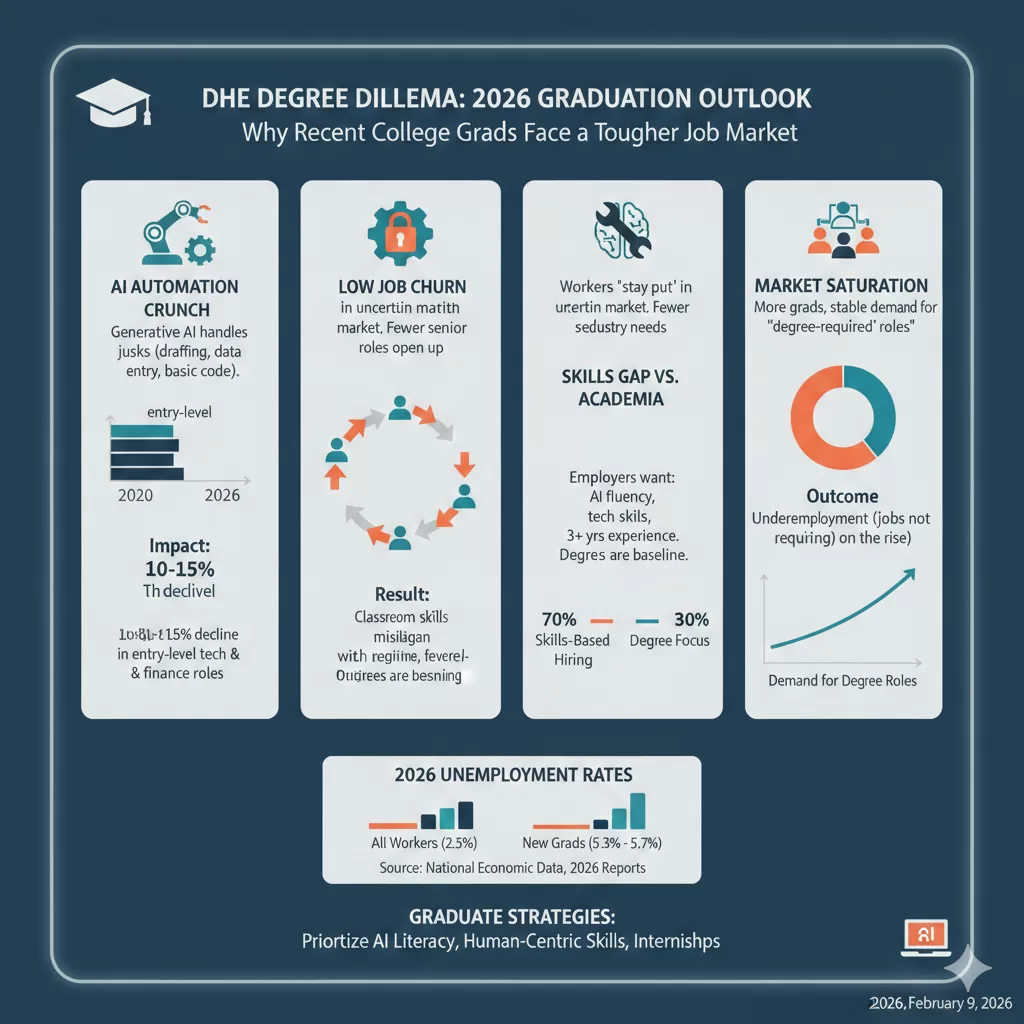

For decades, the path to employment followed a predictable script: graduate high school, earn a four-year degree, and step into a stable career. But for the Class of 2026 and other recent grads, that script has been heavily revised.

While the national unemployment rate remains relatively stable, a closer look reveals a “white-collar friction” that is hitting young graduates particularly hard. Recent data suggests that unemployment for workers aged 22–27 is significantly higher than for the general population, with some reports showing rates as high as 5.3% to 5.7% for new degree holders compared to just 2.5% for their more experienced counterparts.

Why is the “college advantage” seemingly cooling off? Here are the primary factors reshaping the entry-level landscape.

1. The “Bottom Rung” is Being Automated

Perhaps the most significant shift in 2026 is the impact of Generative AI. Historically, junior roles involved “intellectually mundane” tasks: drafting reports, organizing data, or basic coding. These were the “training wheels” of a career.

Today, AI agents handle these tasks with 90% accuracy in seconds.

The Result: Companies are becoming more “top-heavy.” They still need experienced managers to oversee AI, but they need fewer junior employees to do the legwork.

The Crunch: Entry-level hiring has seen double-digit declines in sectors like tech and finance, as firms use AI to boost productivity without expanding their headcount.

2. The Great “Stay Put” (Low Churn)

In a healthy economy, people switch jobs, creating “openings” at the bottom for new talent. In 2026, we are seeing a collapse in voluntary job switching.

“Workers are holding onto their roles because the market feels risky; as a result, the natural ‘churn’ that usually pulls recent grads into the workforce has stalled.”

When mid-level employees don’t move up or out, the entry-level pipeline remains clogged.

3. The Rising “Skills Gap” vs. Academic Focus

There is a growing disconnect between what is taught in the classroom and what is required in a modern office.

The Degree is the Baseline, Not the Finish Line: Employers are shifting toward skills-based hiring. According to NACE, 70% of employers now prioritize specific technical skills and AI fluency over the prestige of the degree itself.

Experience Over Everything: Job postings that once asked for 0–2 years of experience are increasingly demanding 3+ years or specific internships. For a recent grad, this creates the classic paradox: You can’t get the job without experience, but you can’t get experience without the job.

4. Market Saturation

We are currently seeing the result of “education-neutral” growth. The supply of college graduates has increased steadily, but demand for roles that specifically require a degree has leveled off. This has led to a rise in underemployment, where graduates find themselves in roles that don’t actually require their hard-earned credentials.

What Can Grads Do?

The market is tougher, but it isn’t closed. To stand out in the current environment, graduates must:

Prioritize AI Literacy: It’s no longer a “plus”; it’s a requirement. Show how you use AI to work faster and smarter.

Focus on “Human-Centric” Skills: Emphasize critical thinking, complex problem solving, and emotional intelligence—things AI still struggles to replicate.

Treat Internships as Essential: In 2026, an internship is often the only way to bypass the “3 years of experience” requirement.

In a widely anticipated decision, the Federal Reserve opted to keep interest rates unchanged at the conclusion of today’s Federal Open Market Committee (FOMC) meeting. The federal funds rate remains in the range of 5.25% to 5.50%, a 23-year high that has now persisted since July 2023. While investors and analysts had largely priced in a pause, the rationale behind the Fed’s decision reflects a complex balance of economic signals, inflation concerns, and a shifting labor market.

At the heart of the Fed’s policy stance remains its dual mandate: maximum employment and stable prices. While inflation has declined significantly from its peak in 2022, recent data show signs of stickiness in core prices—particularly in housing and services. The Consumer Price Index (CPI) for March showed headline inflation at 3.5% year-over-year, still well above the Fed’s 2% target. Core inflation, which excludes volatile food and energy prices, remains elevated.

Fed Chair Jerome Powell emphasized in his post-meeting press conference that “while inflation has moved down from its highs, it remains too high, and we are prepared to maintain our restrictive stance until we are confident inflation is sustainably headed toward 2%.”

Labor Market Shows Signs of Softening

A key factor behind the decision to hold rates steady is the evolving labor market. The April jobs report showed signs of cooling, with job creation falling below expectations and the unemployment rate ticking slightly higher. Wage growth has also moderated, suggesting that the tightness that once fueled inflationary pressures may be easing.

The Fed appears to be watching closely to avoid tipping the economy into recession. Maintaining current rates gives policymakers the flexibility to respond to further labor market deterioration while continuing to restrain inflationary pressures.

No Immediate Rate Cuts on the Horizon

Despite growing calls from some quarters for rate cuts to support growth, Powell made it clear that the central bank is not yet ready to pivot. “We do not expect it will be appropriate to reduce the target range until we have greater confidence that inflation is moving sustainably toward 2%,” he noted.

Markets have been forced to recalibrate their expectations. At the start of the year, many anticipated as many as six rate cuts in 2024. That outlook has now dramatically shifted, with investors largely pricing in one or two cuts at most—and not before late 2025, barring a sharp economic downturn.

Global Considerations and Financial Stability

The Fed’s cautious approach is also influenced by global developments. Sticky inflation in Europe, geopolitical tensions, and persistent supply chain disruptions all contribute to uncertainty. Moreover, the central bank remains attuned to the risks of financial instability. Keeping rates high—but not raising them further—helps reduce the chances of asset bubbles or excessive credit growth while avoiding additional strain on borrowers.

What Businesses and Investors Should Expect

The Fed’s message today is clear: patience is the prevailing policy. For businesses, this means continued pressure on borrowing costs, but also stability in monetary conditions. For investors, the outlook is one of reduced volatility in Fed policy, though rates may stay “higher for longer” than many had hoped.

In the months ahead, the data will continue to guide the Fed’s hand. Inflation progress will be crucial, but so too will the health of the consumer and the resilience of the job market. Until then, the pause continues—but the path forward remains data-dependent.\

In a decisive move to protect American industry and national security, President Joe Biden has intervened to block the proposed takeover of U.S. Steel Corporation by Japan’s Nippon Steel Corporation. The decision underscores the administration’s commitment to safeguarding critical domestic industries from foreign acquisition. Takeover of US Steel Blocked.

Takeover of US Steel by Nippon Steel Blocked

The proposed acquisition had raised concerns among policymakers and industry experts about the potential impact on the U.S. steel sector, a cornerstone of the nation’s infrastructure and defense industries. U.S. Steel, one of the oldest and largest steel manufacturers in the United States, plays a vital role in supplying materials for construction, transportation, and military applications.

According to administration officials, the move aligns with the broader policy agenda to ensure the resilience of U.S. supply chains and the protection of strategic assets. “We must prioritize the long-term economic and national security interests of the United States,” a White House spokesperson stated.

Nippon Steel, Japan’s largest steel producer, had expressed interest in the acquisition as part of its global expansion strategy. The company emphasized that the deal would benefit both parties by fostering technological collaboration and increasing production efficiency. However, U.S. officials remained unconvinced, citing risks related to foreign control over critical infrastructure.

Industry reactions to the decision have been mixed. Some stakeholders applauded the administration’s proactive stance in shielding a key domestic industry, while others voiced concerns about potential disruptions to foreign investment and trade relations with Japan.

“This decision sends a strong message about the importance of maintaining domestic control over critical industries,” said an industry analyst. “However, it also raises questions about the balance between protectionism and fostering global partnerships.”

The blocked acquisition comes amid a broader effort by the Biden administration to bolster the U.S. industrial base and reduce reliance on foreign entities for essential materials. Recent policies, such as the CHIPS and Science Act and the Inflation Reduction Act, highlight a similar focus on revitalizing domestic manufacturing and securing supply chains.

While Nippon Steel has yet to release an official statement regarding the blocked bid, analysts predict that the company may seek alternative avenues for collaboration with U.S.-based firms or pursue other international opportunities. Meanwhile, U.S. Steel has reaffirmed its commitment to remaining an independent leader in the global steel industry.

This move by President Biden is expected to influence future foreign investment strategies and could set a precedent for how the U.S. approaches similar situations involving critical industries. Connect with Factoring Specialist Chris Lehnes

Unemployment Claims Fall to 211,000 – Lowest Since March

The U.S. labor market continues to show signs of resilience as initial unemployment claims fell to 211,000 for the week ending [date], the lowest level since March. This figure, released by the Department of Labor, is a decline of 13,000 from the previous week’s revised total of 224,000. Economists had anticipated claims to remain relatively flat at around 220,000, making this drop a notable surprise.

Unemployment Claims Fall to 211,000 – Lowest Since March

What Are Unemployment Claims?

Unemployment Claims Fall to 211,000 – Lowest Since March

Why This Matters

This reduction underscores the continued strength of the U.S. economy, even in the face of high interest rates and inflationary pressures. Employers seem more inclined to retain workers despite concerns about economic growth slowing. This trend is consistent with other labor market indicators, including a low unemployment rate and steady job openings.

Regional and Sector Insights

The latest data shows that most regions reported decreases in claims, with notable declines. Industries such as hospitality, healthcare, and manufacturing appear to be driving this stability, as they continue to experience steady or increased demand.

Broader Economic Context

The Federal Reserve has been closely monitoring labor market conditions as it weighs future interest rate decisions. A strong labor market complicates efforts to tame inflation, as higher employment can lead to increased consumer spending. However, the drop in claims suggests that the economy may be navigating this delicate balance better than expected.

Looking Ahead

Analysts will be watching for the next round of employment reports and economic data to determine whether this trend is sustainable. A consistently low level of unemployment claims could signal ongoing economic strength, but it may also keep the Federal Reserve on alert regarding inflationary risks.

For now, the decrease in unemployment claims is a positive sign for workers and businesses alike, reinforcing confidence in the stability of the U.S. economy.