Impact of Iran War Ripple through the Economy Due to Gas Prices

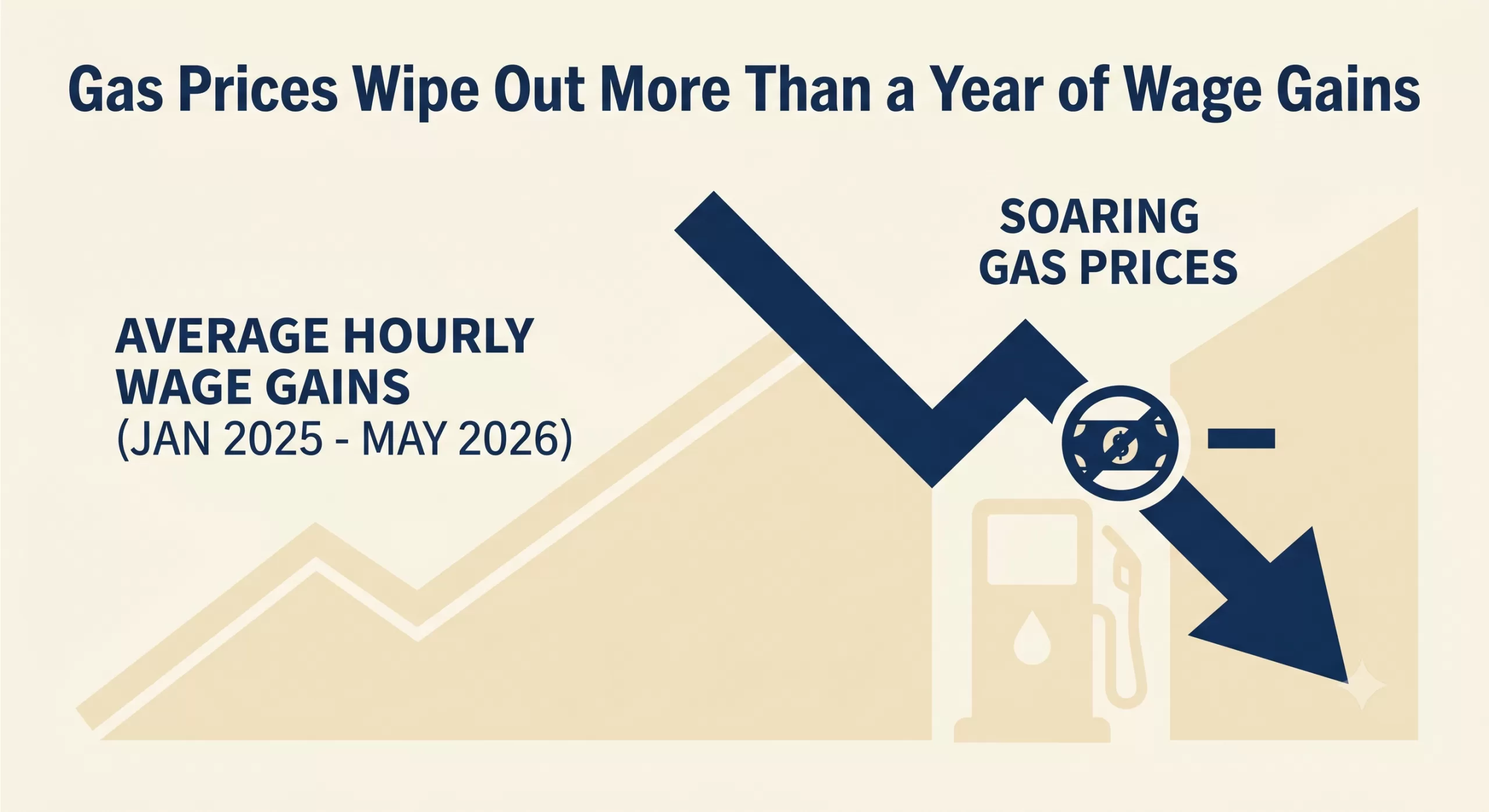

The latest macroeconomic indicators including gas prices paint a challenging picture for both consumers and businesses. Following the Labor Department‘s recent reports, it is clear that soaring energy costs have effectively neutralized recent progress in worker compensation. With top-line inflation advancing to 4.2% in May—the highest level in three years—and gasoline prices surging, real average hourly earnings have been pushed all the way back to January 2025 levels.

For the second consecutive month, inflation has outpaced wage growth. The reality is that gas prices have wiped out more than a year of wage gains.

The Macroeconomic Squeeze

The ripple effects of this inflationary spike are significant. The Federal Reserve now faces a complex policy dilemma as they weigh interest rate decisions against a backdrop of stubborn inflation and squeezed household budgets. When wages lag behind inflation, consumer spending inevitably cools, particularly among middle- and lower-income brackets who are forced to allocate a larger share of their take-home pay to essentials like fuel and groceries.

What This Means for Business Owners

While the headlines focus on the consumer at the pump, small and mid-sized businesses are absorbing these shocks on multiple fronts:

Increased Operational Costs: Surging fuel prices directly inflate the cost of transportation, logistics, and supply chain operations.

Margin Compression: Businesses face the difficult choice of passing higher costs onto increasingly price-sensitive consumers or absorbing the losses and shrinking their profit margins.

Wage Pressure: Even though real wages are falling, nominal wage demands remain high as employees seek relief from the rising cost of living, straining payroll budgets.

Navigating the Cash Flow Crunch

During periods of high inflation and uncertain interest rates, liquidity becomes a paramount concern. Industries heavily reliant on steady cash flow—such as manufacturing, staffing, healthcare, and distribution—can find their working capital severely constrained when expenses rise faster than revenues can be collected.

Waiting 30, 60, or 90 days for clients to pay outstanding invoices is a luxury many companies cannot afford when the cost of doing business is escalating weekly. Accounts receivable factoring offers a strategic mechanism to bridge this gap. By converting outstanding B2B invoices into immediate working capital, business owners can cover rising operational costs, meet payroll obligations, and navigate economic volatility without taking on new debt or waiting on unpredictable macroeconomic shifts.

As we continue to monitor the inflation data and the Fed’s next moves, maintaining robust working capital will be the defining factor for businesses looking to weather this storm.

Today marks a significant turning point in European monetary policy: the European Central Bank (ECB) has officially reversed course, raising its key interest rates for the first time in nearly three years.

After an extended period of cuts and holds, the era of steadily declining borrowing costs in the Eurozone has temporarily hit a wall. Let’s break down the data, the underlying causes, and what this means for the broader economy.

The Decision: By the Numbers

In a move widely anticipated by financial markets and economists, the ECB’s Governing Council elected to raise its key interest rates by 0.25 percentage points (25 basis points).

Here is a quick breakdown of where the central bank’s key rates stand effective immediately:

ECB Facility

Previous Rate

New Rate (June 2026)

Deposit Facility

2.00%

2.25%

Main Refinancing Operations

2.15%

2.40%

Marginal Lending Facility

2.40%

2.65%

This decision officially ends a cycle that began back in September 2023, representing a decisive reaction to shifting economic realities on the ground.

Why is the ECB Hiking Rates Now?

The ECB has a single, primary mandate: to maintain price stability by targeting an inflation rate of 2.0%. The decision to hike rates is a direct response to recent data showing that inflation is moving in the wrong direction.

Headline Inflation Surge: In May 2026, Eurozone consumer prices rose to 3.2% year-over-year. This marks a significant acceleration from earlier in the year and blows past the central bank’s comfort zone.

The Energy Shock: A major driver behind this inflationary spike is the ongoing geopolitical conflict in the Middle East. Disrupted shipping routes and volatile commodity markets caused energy prices to jump nearly 11% last month compared to the same period last year.

Core Inflation Creep: The energy shock isn’t isolated. Core inflation—which strips out highly volatile food and energy costs—rose to 2.5%. This indicates that higher energy overheads are beginning to bleed into the broader costs of everyday goods and services.

What Does This Mean for the Eurozone?

When the ECB pulls the interest rate lever, the effects ripple through the entire financial system. Here is what to expect:

More Expensive Borrowing: For consumers and businesses, the cost of credit is going up. Homeowners holding variable-rate or tracker mortgages will see their monthly repayments increase almost immediately.

A Squeeze on Growth: While higher interest rates are necessary to cool down inflation, they simultaneously suppress economic activity. Reflecting the strain of higher energy costs and tighter financial conditions, the ECB has already revised its growth forecasts downward, anticipating the Eurozone economy will grow by a sluggish 0.8% in 2026.

Currency Impacts: Higher interest rates generally make a currency more attractive to yield-seeking investors. A hawkish stance from the ECB typically provides upward support for the Euro (EUR) against other major currencies, provided the broader economic outlook doesn’t deteriorate too sharply.

Looking Ahead: Is This the Start of a New Cycle?

The prevailing question for markets is whether this is a isolated adjustment or the beginning of a new tightening cycle.

Current market consensus suggests this won’t be a one-off event. Many analysts are pricing in at least one or two more quarter-point increases before the end of the year, which could bring the deposit rate up to 2.50% or 2.75%. However, ECB leadership has emphasized that future decisions will remain strictly “data-dependent.” The Governing Council will evaluate the ongoing impact of energy prices, geopolitical stability, and wage growth on a meeting-by-meeting basis.

The takeaway is clear: the ECB’s latest pivot highlights how rapidly external shocks can upend economic stability, forcing central banks to prioritize fighting inflation over stimulating growth.

If your last trip to the gas station felt like a hit to your wallet, you aren’t alone. The latest Consumer Price Index (CPI) report is out, and the numbers confirm what we’ve all been feeling: U.S. inflation jumped to 3.8% in April, up from 3.3% in March.

This represents the highest inflation rate since 2023, and it marks a significant detour from the “path to 2%” that the Federal Reserve has been aiming for. While price increases have cooled in some sectors, the energy market is currently the primary engine driving these numbers higher.

Gasoline: The Primary Culprit

The standout figure in April’s report is the cost of energy. National average gas prices have surged to approximately $4.50 per gallon, a staggering jump from the sub-$3.00 levels seen just a few months ago in February.

This spike isn’t just a random market fluctuation. It is being driven heavily by geopolitical instability, specifically the ongoing conflict with Iran. The closure of the Strait of Hormuz—a vital artery for global oil supply—has sent shockwaves through the market. When a fifth of the world’s oil supply is threatened, the impact is immediate and felt directly at the local pump.

The “Trickle-Down” of High Energy Costs

High gas prices do more than just make commuting more expensive. They create a “cost-of-living” domino effect:

Transportation & Logistics: Shipping companies and airlines are facing massive fuel surcharges, which eventually get passed down to the consumer.

Food Prices: Agriculture and grocery distribution are energy-intensive. As diesel and gas prices rise, expect your grocery bill to remain stubbornly high.

Manufacturing: Factories that rely on heavy energy consumption are seeing their margins squeezed, leading to higher prices for finished goods.

What This Means for Interest Rates

For months, the big question in the financial world has been: When will the Fed cut interest rates?

This 3.8% reading makes that answer much more complicated. Outgoing Fed Chair Jerome Powell and incoming Chair Kevin Warsh are facing a “higher-for-longer” reality. Typically, the Fed raises interest rates to cool a hot economy and lower inflation. With inflation trending upward again, the prospect of rate cuts in 2026 is fading, and some economists are even whispering about the possibility of another hike if the energy crisis doesn’t stabilize.

The Bottom Line

The April inflation report is a sobering reminder of how interconnected our local economy is with global events. While the U.S. economy remains resilient in many areas, the “gasoline tax” created by geopolitical tension is a heavy burden for the average household.

For now, the focus remains on the Middle East. Until energy supply stabilizes, the Fed—and our bank accounts—will likely be in a defensive crouch.

What are you doing to offset rising costs? Are you changing your summer travel plans or looking into more fuel-efficient alternatives? Let us know in the comments below.

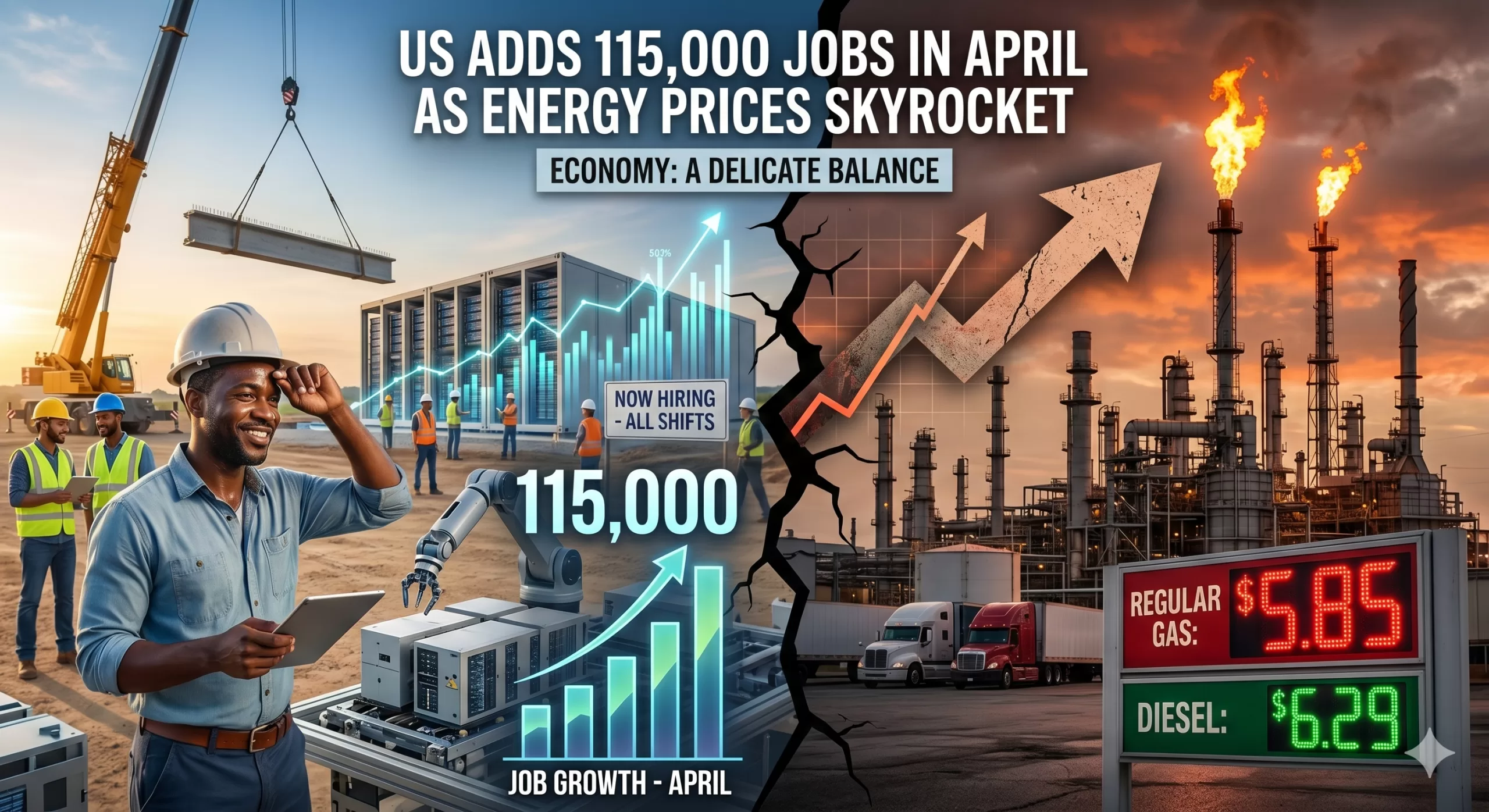

The latest Labor Department report released today, May 8, 2026, reveals a complex picture of the American economy. While the addition of 115,000 jobs in April far exceeded the conservative forecasts of 65,000, this hiring momentum is colliding with a volatile energy market and geopolitical tensions that are keeping consumers—and the Federal Reserve—on edge.

The April Jobs Numbers: A Surprising Resilience

Despite a year of uneven growth and high interest rates, the labor market continues to find its footing. The 115,000 gain marks a significant win for an economy that many feared was cooling too rapidly.

Unemployment Rate: Held steady at 4.3%, a remarkably low figure given the broader economic headwinds.

Sector Highlights: Growth was fueled by health services, education, and construction. Notably, the boom in AI data center construction is providing a sturdy floor for blue-collar employment.

Small Business Bounce: Much of the hiring surge came from small businesses (fewer than 20 employees), suggesting that local optimism remains resilient despite macro-level volatility.

The Energy Crisis: A Shadow Over the Recovery

While the job gains are a reason for celebration, they are being offset by a painful reality at the pump and in utility bills. Crude oil prices have breached the $100-per-barrel mark, driven largely by recent hostilities in the Strait of Hormuz.

For the average American household, the “energy tax” is real. Rising gas prices are eating into the gains from recent tax refunds and wage growth. This creates a “push-pull” dynamic:

The Push: Robust hiring and steady wages ($6.6\%$ growth for job-switchers) give consumers spending power.

The Pull: Skyrocketing energy costs increase the cost of goods and transportation, effectively neutralizing those wage gains for many families.

What This Means for the Federal Reserve

The Fed is now in a delicate position. Usually, a strong jobs report would signal that the economy can handle higher interest rates. However, with energy prices driving “cost-push” inflation, Fed Chair Jerome Powell and his team must decide if the labor market is stable enough to wait out the energy spike or if they need to pivot to protect growth.

Traders are currently betting on a “stable backdrop,” but the volatility in the Middle East remains the ultimate wildcard. If energy prices continue their upward trajectory, the modest 115,000-job gain might be harder to replicate in May.

Looking Ahead

The April report proves that the U.S. economy is more durable than skeptics predicted, but it also highlights our vulnerability to global supply shocks. As we move into the summer months, all eyes will be on two things: the price of a gallon of gas and whether the AI-driven infrastructure boom can continue to carry the weight of the labor market.

Bottom Line: The American worker is still in demand, but the cost of living—fueled by a chaotic energy market—is the primary threat to this hard-won stability.

Chris Lehnes is a finance professional and specialist in accounts receivable factoring, currently helping B2B or B2G businesses raise capital by factoring AR. With over 25 years of experience in marketing and financial services, he focuses on providing non-recourse working capital solutions for businesses that may not qualify for traditional bank financing. [1, 2, 3, 4]

Professional Expertise

Lehnes operates primarily as an educator and intermediary in the factoring industry, helping companies bridge cash flow gaps through their receivables. His expertise includes: [1, 2]

Target Industries: He provides funding for a variety of sectors including energy, healthcare, manufacturing, and staffing.

Specialized Funding: He specializes in “challenging deals,” such as startups, companies with high customer concentrations, or those with weak personal credit.

Financial Content: Lehnes is a prolific content creator, maintaining a YouTube channel focused on factoring tutorials, market analysis, and audiobook summaries related to leadership and business psychology. [1, 2, 3, 4, 5]

Career & Background

Education: He studied Economics at Lafayette College and attended River Dell Regional High School.

Online Presence: He actively shares insights on LinkedIn and Twitter/X, often discussing economic barometers like lumber price fluctuations and their impact on residential construction.

Public Speaking: He frequently appears on podcasts and webinars, such as the Credit on the Go Podcast, to explain the strategic benefits of factoring. [1, 2, 3, 4, 5]

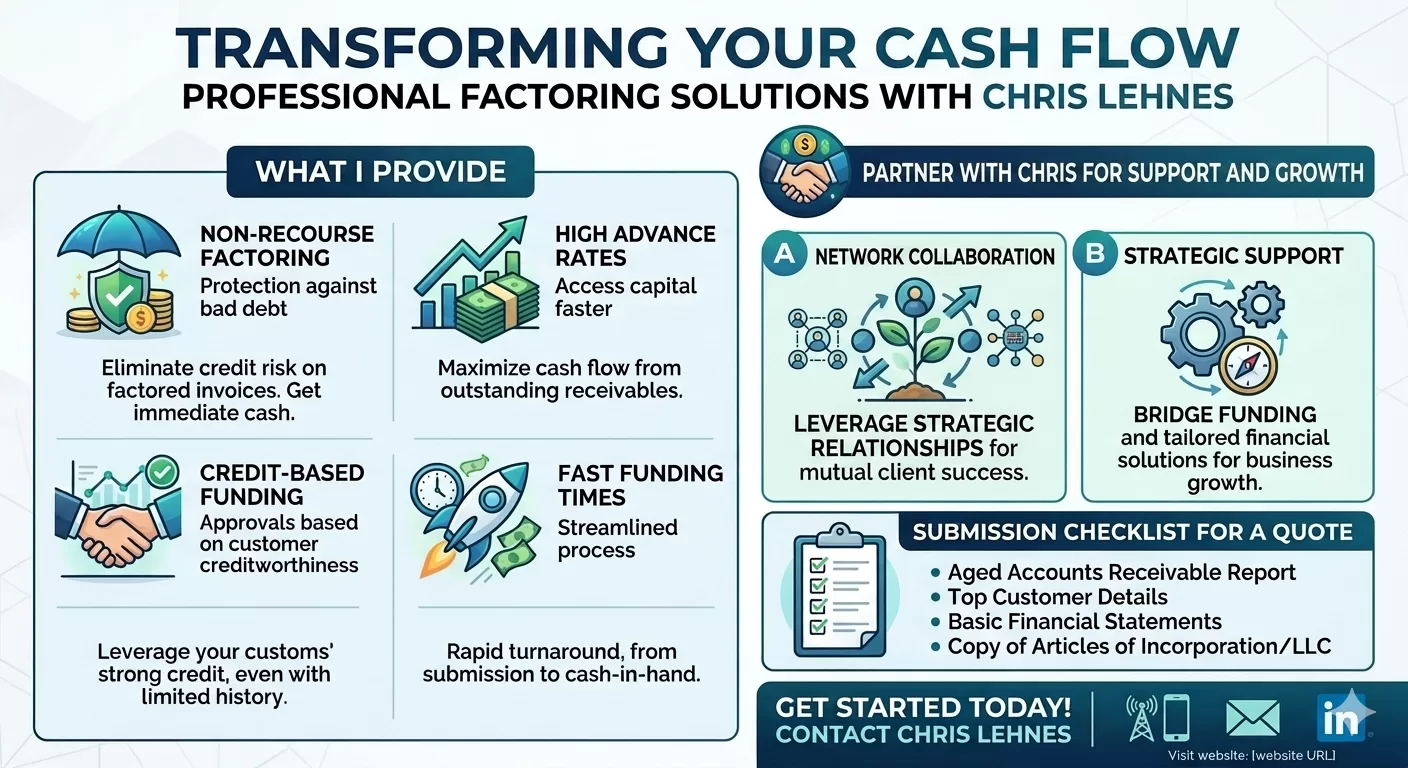

Chris Lehnes manages non-recourse factoring at Versant Funding, where the primary requirement for funding is the credit quality of the account debtor (the customer paying the invoice), rather than the financial strength of the business itself. [1, 2, 3]

Funding Criteria & Terms

Sales Volume: Targets companies with B2B or B2G sales ranging from $100,000 to $30 million per month.

Non-Recourse Protection: Versant assumes the credit risk; if the customer fails to pay due to insolvency, the business is not required to reimburse Versant.

Flexible Concentration: Unlike many lenders, Lehnes often facilitates deals with 100% customer concentration, where a business has only one major client (e.g., a large municipality or multinational corporation).

Funding Speed: Deals can often be funded within one week because traditional underwriting of the borrower’s balance sheet is not required.

Typical Fees: Costs are generally around 2.5% of the invoice amount for each month it remains outstanding.

Excluded Industries: Generally does not factor for the medical (provider-side) or construction industries. [1, 2, 3, 4, 5, 6, 7]

Latest Market Analysis (2025–2026)

Lehnes frequently updates his YouTube and Substack with analyses of the broader economy. Recent highlights include:

Monetary Policy: He recently analyzed the Federal Reserve’s decision to maintain interest rates, discussing the “higher for longer” outlook and its pressure on small business borrowing costs.

Chris Lehnes frequently facilitates complex funding through Versant Funding LLC, often solving liquidity crises for businesses that traditional banks might reject. [1, 2]

Selected Case Studies

$30 Million Furniture Manufacturer (2025): Provided a massive non-recourse facility to replace a non-renewed loan from a previous factor. This deal supported the company through a significant corporate restructuring.

$1.4 Million Auto Equipment Manufacturer (2026): Funded a company supplying global automotive giants. Despite the client’s slow-paying receivables, Versant scaled the facility automatically because the customers were “the strongest on the planet”.

$3 Million Housewares Distributor (2025): Stepped in when the client’s existing factor imposed funding limits that prevented them from fulfilling new orders. Versant consolidated existing loans and provided an advance against all outstanding receivables.

$1.8 Million Adolescent Group Home (2024): Originated a facility for a newly formed social services provider. Because state and county organizations pay slowly, this factoring arrangement provided the necessary liquidity for them to expand into new regions.

Energy Sector Support (2026): Recently focused on the oil and gas industry, helping suppliers bridge working capital gaps caused by the long payment cycles of major energy corporations. [1, 2, 3, 4, 5, 6, 7, 9]

Contact Information

You can reach Chris Lehnes directly for a pre-qualification review or to discuss a specific transaction:

Phone: 203-664-1535

Email: clehnes@VersantFunding.com or chris@chrislehnes.com

Chris Lehnes and Versant Funding prioritize non-recourse factoring because it allows them to fund high-growth or struggling businesses based solely on their customers’ creditworthiness rather than the business’s own financial history. [1, 2]

Recourse vs. Non-Recourse Factoring

The primary difference is who bears the financial risk if a customer fails to pay an invoice. [1, 2]

Recourse Factoring: This is the most common and typically the least expensive option. Under this arrangement, if your customer does not pay their invoice within a set period (usually 60–90 days), your business is responsible for buying back that invoice or replacing it with a fresh one. You retain the ultimate credit risk.

Non-Recourse Factoring: In this model, the factoring company (like Versant) assumes the credit risk. If your customer becomes insolvent or files for bankruptcy, you are not required to pay back the advanced funds. Because the factor takes on more risk, fees are typically higher, and they require strict credit approval of your customers. [1, 2, 3, 4, 5, 6, 7, 8, 9]

Referral Partnership Guidelines

Lehnes actively collaborates with intermediaries, including commercial loan brokers, accountants, and consultants, to source “difficult” deals that traditional banks cannot touch. [1, 2]

Recurring Commissions: Unlike real estate or one-time loan fees, Lehnes offers recurring monthly commissions for the entire life of the deal. If a client factors for three years, the referral partner receives a check every month for those three years.

Strategic Bridge: He encourages partners to use factoring as a short-term bridge (often 24 months) to help companies stabilize until they can qualify for bank financing or complete an equity raise.

Simple Prequalification: To refer a client, you generally only need to provide the client’s industry and a list of their major customers (A/R Aging report). Because Versant does not require full financial audits of the borrower, pre-approval can happen very quickly. [1, 2, 3]

To move forward with a deal for Chris Lehnes at Versant Funding, you typically need a streamlined submission package because they do not underwrite the borrower’s financials—only the collateral (the invoices).

1. Required Documents for a Quote

You can typically get a term sheet or preliminary proposal by submitting just two or three items.

Current A/R Aging Report: This is the most critical document. It must show the names of the customers (account debtors), the amounts they owe, and how long the invoices have been outstanding (0-30, 31-60, 60-90 days).

Customer List with Limit Requests: A list of the specific customers the client wants to factor, including their addresses and the amount of credit limit requested for each. Versant uses this to run credit checks on the debtors.

Sample Invoices: A few examples of the invoices they intend to factor to verify they represent completed work or delivered goods (not progress billing or guaranteed sales).

Simple Application:

Note: You generally do NOT need to submit tax returns, P&L statements, or balance sheets for a preliminary quote, as Versant relies on the credit of the account debtors. [1, 2, 3]

Next Step: If you have a client ready, you can email the A/R Aging Report directly to chris@chrislehnes.com to request a term sheet.

For the first time since the aftermath of World War II, the United States has reached a fiscal milestone that was once a distant “what-if” scenario: the national debt has officially surpassed 100% of the country’s Gross Domestic Product (GDP).

As of March 31, 2026, the debt held by the public reached $31.27 trillion, while the total annual economic output sat at $31.22 trillion. In simple terms, we now owe more as a nation than we produce in an entire year.

While “trillions” can feel like abstract Monopoly money, this 100.2% ratio represents a fundamental shift in the American economic landscape. Here is what you need to know about why this happened and what it means for the future.

How Did We Get Here?

This wasn’t an overnight accident. It is the result of decades of “fiscal kicking the can.” The surge to 100% was fueled by three primary engines:

Structural Deficits: For years, the government has spent roughly $1.33 for every $1.00 it collects in revenue.

The Interest Trap: As the total debt grows, so do the interest payments. In 2026, the U.S. is projected to spend approximately $1 trillion on interest alone—surpassing the entire national defense budget.

Demographic Shifts: An aging population is naturally drawing more heavily on Social Security and Medicare, programs that make up a massive portion of mandatory spending.

Why the 100% Threshold Matters

Economists often debate whether there is a “magic number” where debt becomes fatal. While 100% isn’t an immediate “cliff,” it serves as a critical psychological and economic warning light for several reasons:

Slower Economic Growth: Historical data suggests that when a nation’s debt exceeds 90% of GDP, average annual growth tends to slow. Resources that could be used for private investment or infrastructure are instead diverted to servicing old debt.

Reduced “Crisis Cushion”: When the next pandemic, recession, or war hits, the government has less “dry powder” to respond. Borrowing your way out of a crisis is much harder when your credit card is already maxed out relative to your income.

Generational Equity: The debt essentially represents a “tax” on future generations. Today’s spending is being financed by the earnings of Americans who haven’t even entered the workforce yet.

The Cost to the Average Household

To bring these massive numbers down to earth, the Senate Joint Economic Committee’s April 2026 update provides a sobering breakdown:

Debt per Person: Approximately $114,000

Debt per Household: Approximately $289,000

Is There a Way Out?

The U.S. has been here before. After 1945, the debt-to-GDP ratio was successfully whittled down to 34% by 1980. However, that was achieved through a unique combination of post-war industrial dominance, a massive “Baby Boom” workforce, and rapid GDP growth.

Today, the path is narrower. Solutions generally fall into three difficult categories:

Entitlement Reform: Adjusting Social Security and Medicare to match modern life expectancies.

Revenue Increases: Raising taxes or closing loopholes to narrow the deficit.

Growth Incentives: Policies designed to make the “GDP” side of the ratio grow faster than the “Debt” side.

The Bottom Line

Crossing the 100% threshold is a “reckoning” moment. It signals that the era of “cheap” borrowing is over. As interest payments continue to eat a larger slice of the federal pie, the pressure on the American taxpayer—and the pressure to make hard political choices—will only intensify.

The red line has been crossed. The question now is whether we have the political will to head back toward the black.

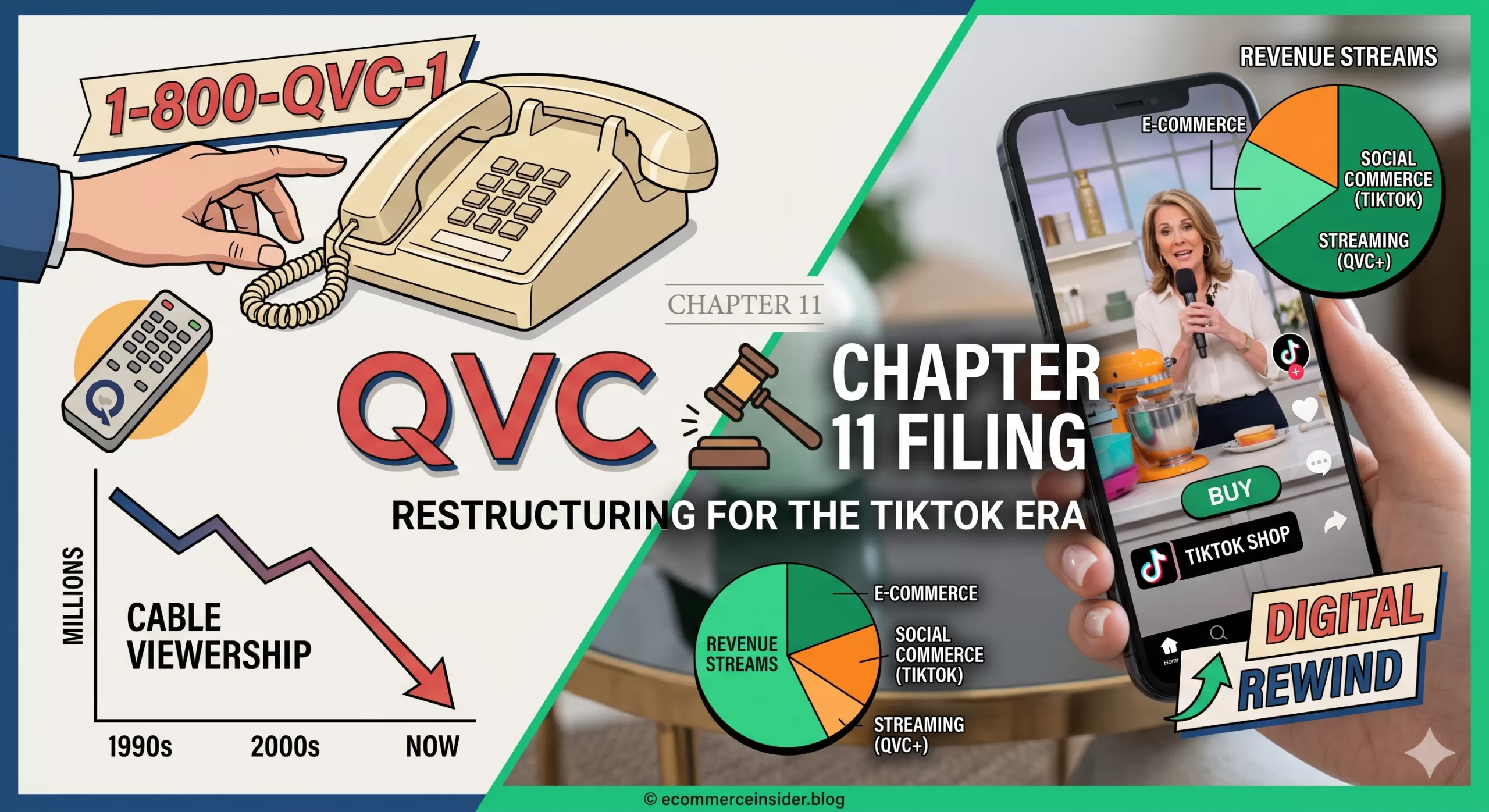

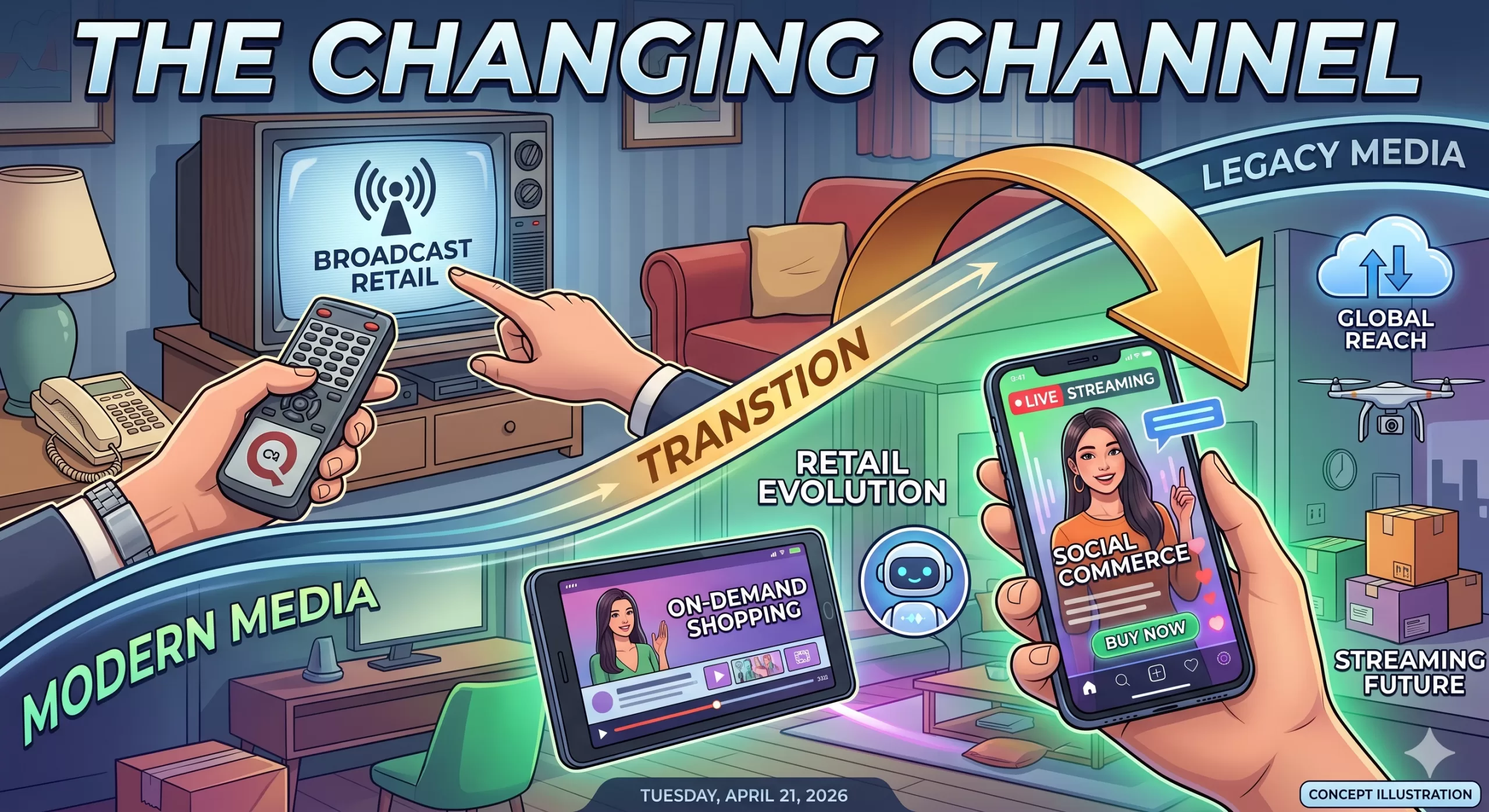

For decades, the familiar glow of QVCand HSNwas a staple of American living rooms. But in an era where “Add to Cart” happens on TikTok rather than over a landline, even the giants of home shopping have to hit the reset button.

On April 16, 2026, QVC Group, Inc. officially filed for Chapter 11 bankruptcy protection. While the word “bankruptcy” often sounds like an ending, for QVC, this appears to be a calculated “financial makeover” rather than a final curtain call.

The Numbers: Shedding a $5 Billion Weight

QVC didn’t enter the courtroom empty-handed. This is what’s known as a “prepackaged” bankruptcy, meaning the company already reached an agreement with most of its lenders before filing.

Debt Reduction: The primary goal is to slash the company’s debt from a staggering $6.6 billion down to $1.3 billion.

The Timeline: They aren’t planning on sticking around the courthouse for long; the company expects to emerge from the process within 90 days.

The Stock: It’s a rough week for investors. Nasdaq has already moved to delist QVC Group’s common and preferred stock, as the restructuring plan is expected to wipe out existing equity.

Why Now? The Death of the “Linear” Living Room

The filing highlights a hard truth: the structural decline of cable TV. QVC’s business model was built on a captive audience of cable subscribers. As cord-cutting accelerated and viewership moved to streaming and social media, the massive cash flows that once serviced QVC’s debt began to dry up.

Despite the struggle, QVC hasn’t been standing still. In 2025, the company saw a surprising spark of life:

TikTok Shop: QVC acquired nearly 1 million new customers through TikTok last year.

Streaming Growth: Viewership on their streaming apps, QVC+ and HSN+, grew by 19% in 2025.

The bankruptcy is essentially a way to align their “old world” debt with their “new world” digital revenue.

What This Means for You (The Shopper)

If you’re worried about your pending orders or that Vitamix you’ve been eyeing, take a deep breath. For the average customer, it is business as usual.

The Quick Checklist for Shoppers:

Orders & Shipping: Continuing as normal.

Gift Cards: Still valid and being honored.

Returns: Policies remain unchanged.

Customer Service: Teams are operating on their regular schedules.

Layoffs: The company stated there are no planned layoffs or furloughs as part of this specific restructuring.

The “WIN” Strategy

CEO David Rawlinson is betting on the “WIN” Growth Strategy, which focuses on being “Wherever She Shops.” By shedding $5 billion in debt, QVC hopes to have the flexibility to stop acting like a legacy cable channel and start acting like a “content-to-commerce” platform.

By the summer of 2026, QVC expects to emerge as a leaner, privately held (or newly listed) “Reorganized QVC, Inc.” The iconic “Quality, Value, Convenience” slogan isn’t going anywhere—it’s just getting a much-needed digital upgrade.

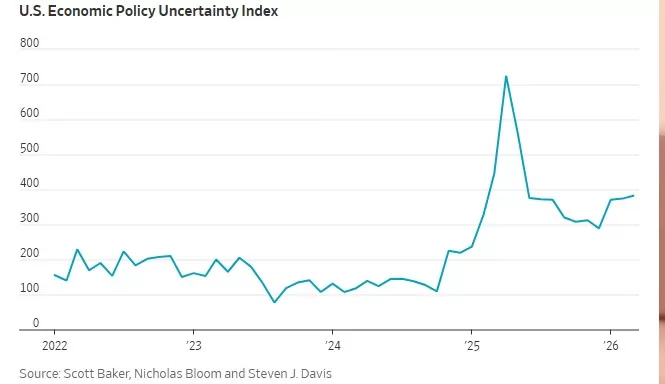

Middle East War Will Slow Global Economic Growth. The global economy, which had shown surprising resilience through early 2026, is now facing a significant “speed bump.” In its latest World Economic Outlook released today, April 14, 2026, the International Monetary Fund (IMF) warned that the escalating conflict in the Middle East—specifically the war involving Iran—has halted global momentum and forced a downgrade of growth projections.

The Numbers: A Downward Shift

Just months ago, economists were optimistic that a tech-driven productivity boom and easing inflation would lead to a “soft landing.” However, the IMF has now lowered its 2026 global growth forecast to 3.1%, down from the 3.3% projected in January.

Scenario

2026 Growth Forecast

Key Drivers

Reference (Current)

3.1%

Short-lived conflict, oil averages $82/bbl

Adverse

2.5%

Prolonged disruption, oil stays at $100

Severe

2.0%

Extended war, oil spikes to $110+

The “Strait” Jacket on Energy

The primary engine of this slowdown is the volatility in energy markets. The closure of the Strait of Hormuz in March 2026—a chokepoint for 20% of the world’s oil and significant LNG volumes—sent Brent crude surging past $120 per barrel.

While prices have recently fluctuated around $98, the damage to supply chains is extensive. The IMF notes that:

Inflation is Rebounding: Global inflation expectations for 2026 have been revised up to 4.4%.

Fertilizer Shortages: With 20-30% of global fertilizer exports passing through the region, agricultural costs are rising, threatening food security in import-reliant nations.

Trade Disruptions: Maritime insurance premiums have skyrocketed, and major shipping routes are being rerouted, adding weeks to delivery times for consumer goods.

The Risk of a “Close Call” Recession

IMF Chief Economist Pierre-Olivier Gourinchas described the current situation as a pivot point. While the “Reference Scenario” assumes the war remains contained, a “Severe Scenario” could see growth drop to 2%—a level the IMF considers a global recession. This has only happened four times since 1980.

Central banks, which were expected to begin cutting interest rates this spring, may now be forced to keep rates “higher for longer” to combat the energy-driven inflationary spike.

“War in the Middle East has halted the global momentum we saw at the start of the year. The risks are now firmly tilted to the downside.”

— Pierre-Olivier Gourinchas, IMF Chief Economist

Looking Ahead

The path forward depends entirely on the duration of the hostilities. If a ceasefire holds and energy production in the Persian Gulf normalizes by mid-year, the IMF believes the global economy can avoid a total contraction. However, for emerging markets and developing economies, the impact is expected to be twice as severe as that on advanced nations, potentially undoing years of post-pandemic recovery.

A Surprising Spring: March Jobs Report Shatters Expectations

The U.S. labor market just delivered a spring surprise that few saw coming. According to the latest data released today by the Bureau of Labor Statistics (BLS), the U.S. economy added 178,000 jobs in March, vastly outperforming economist forecasts which had hovered around a modest 60,000 to 70,000.

After a dismal February that saw a revised loss of 133,000 jobs, this rebound signals a resilient—if complex—economic landscape.

The Numbers at a Glance

The March report offers a refreshing change of pace for a labor market that has felt “frozen” for much of the past year.

Nonfarm Payrolls: +178,000 (Expected: ~70,000)

Unemployment Rate: 4.3% (Down from 4.4% in February)

Revisions: January’s figures were revised upward to 160,000, though the two-month net revision slightly dampened the overall trend.

What’s Driving the Growth?

The recovery wasn’t uniform across the board. While the headline number is strong, the “engine” of the U.S. economy remains highly concentrated:

The Healthcare Titan: Once again, the health care and social assistance sector did the heavy lifting, adding 76,000 jobs last month. This sector has essentially been the primary life support for the labor market over the last year.

The “Bounce Back” Factor: Part of the March surge is attributed to the return of approximately 31,000 Kaiser Permanente employees who were on strike in February, along with more favorable weather conditions across the country.

The Gender Shift: Interestingly, recent trends show that women now hold more jobs than men in the nonfarm economy—a structural shift driven by the strength of female-dominated sectors like education and health, while male-concentrated sectors like manufacturing continue to cool.

The Shadows on the Horizon: Geopolitics and Oil

Despite the optimistic numbers, experts are urging caution. The report arrives amidst significant geopolitical tension, specifically the ongoing conflict in Iran.

“We’ve got a much more difficult spring job market than we had hoped given the higher prices at the pump and the supply chain disruptions that are going to come from the war,” says Diane Swonk, chief economist at KPMG.

With gas prices spiking above $4 a gallon for the first time since 2022, many fear that the March gains may be a “last hurrah” before the economic impact of the war and energy costs fully settle into corporate hiring plans.

The Bottom Line

The U.S. economy has shown it still has plenty of fight left. A 4.3% unemployment rate remains historically healthy, and the “low-hire, low-fire” stalemate of 2025 appears to be thawing.

However, for job seekers and businesses alike, the road ahead remains fogged by uncertainty. Between the rapid integration of Artificial Intelligence, fluctuating inflation (which dipped to 2.3% before ticking back up), and global instability, “cautious optimism” remains the phrase of the day.

If the global economy feels like a high-wire act lately, you aren’t alone. We are currently navigating a “polycrisis“—a fancy term for when multiple major headaches (inflation, geopolitical tension, and shifting labor markets) all hit the fan at the same time.

We are standing on a narrow ledge. One side leads to a hard landing; the other leads to a stabilized “new normal.” Here is a look at the forces threatening to push us off, and the safety nets that might just pull us back.

The Push: What Could Tip Us Over?

It doesn’t take a wrecking ball to cause a recession; sometimes, it just takes a few well-placed dominos. Here are the primary risks:

The “Higher for Longer” Fatigue: While central banks use interest rates to cool inflation, keeping them elevated for too long puts immense pressure on household debt and corporate margins. If the “lag effect” hits all at once, consumer spending—the engine of the economy—could stall.

Geopolitical Aftershocks: Energy prices are notoriously sensitive to global conflict. Any significant escalation in major trade corridors can reignite supply chain chaos, sending the cost of goods back into the stratosphere.

The Commercial Real Estate Ghost Town: With remote work now a permanent fixture, many office buildings are sitting half-empty. As these property loans come due for refinancing at higher rates, we could see a localized banking tremor.

The Pull: What Could Help Us Pull Through?

It’s not all doom and gloom. There are several structural “muscles” keeping the economy upright:

The Resilient Labor Market: Despite tech layoffs making headlines, overall unemployment remains historically low. As long as people have jobs, they tend to keep spending, which provides a powerful floor for the economy.

The Productivity “AI Bump”: We are at the beginning of a massive technological shift. Early adoption of generative AI is already beginning to streamline workflows and reduce operational costs, which could lead to a non-inflationary growth spurt.

Household Balance Sheets: Unlike the 2008 crash, many consumers and corporations locked in low interest rates years ago. This “debt buffer” has bought the private sector time to adjust to the new economic reality.

The Bottom Line: Balance, Not Freefall

The economy isn’t necessarily “broken,” but it is transitioning. We are moving away from an era of “free money” and into an era where efficiency and strategic investment matter again.

Scenario

Key Driver

Likely Outcome

The Hard Landing

Persistent inflation + high rates

Brief but sharp recession; rising unemployment.

The Soft Landing

Controlled cooling + tech growth

Flat growth for a year, followed by a steady recovery.

The No Landing

Continued high spending

Economy stays hot, but rates stay high indefinitely.

The Takeaway: While the ledge is narrow, the path across is still visible. Navigating the next twelve months will require agility from policymakers and patience from investors. We may be on the edge, but we aren’t over it yet..