Convert IEEPA Tariff Claims to Cashon an Expedited Basis

I have been actively assisting companies nationwide in converting their IEEPA tariff refund claims into immediate cash.

U.S. Customs and Border Protection is rolling out a centralized system (CAPE) to process refunds, and some trade experts believe that certain importers could begin receiving refunds within the next six months. However, there remains significant uncertainty around timing, and many industry participants believe that a large portion of claims could still take years to fully resolve.

Convert IEEPA Tariff Claims to Cash on an Expedited Basis

This divergence is driven by several factors, including: The complexity and scale of processing millions of entries The possibility that certain categories of claims may be prioritized over others, delaying recovery for more complex or lower-volume importers The need for new administrative procedures, as IEEPA does not clearly define a refund mechanism The potential for case-by-case eligibility determinations

Ongoing legal and procedural developments, including possible appeals by the Trump Administration and implementation challenges

Liquidation Status – Whether entries have already been liquidated, which in many cases may require formal protests or litigation to reopen and recover duties The likelihood of inconsistent treatment across ports (port-by-port) or entry types as CBP implements new processes in phases Documentation gaps and data reconciliation issues, particularly for older entries or those filed across multiple brokers The absence of clear guidance on how interest on refunds will be calculated and paid, which could lead to further disputes

Capacity constraints within CBP and the potential for processing backlogs as refund volumes scale

Continued legal challenges around the scope of eligibility, including disputes over classifications, valuation, or origin that could delay specific claims

As a result, while some importers may receive refunds within six months, others, particularly those with more complex or previously liquidated entries, could face a multi-year recovery timeline. To address this uncertainty, financial institutions and hedge funds are actively purchasing IEEPA tariff refund claims at a discount.

Current buy rates are as high as 85% of the expected refund value, depending on claim size, credit quality of the importer and documentation quality as these claims are not directly assignable. AES works with importers with claims starting at $250,000, with no maximum limit. Since entering this market five months ago, AES has facilitated the monetization of approximately $20 million in claims across industries including food, seasonal goods, apparel, and home products.

Market pricing has evolved significantly: Prior to the February 20, 2026, Supreme Court ruling, claims traded at approximately 20–25% Following the ruling, pricing increased to 40–50% More recently, improving legal clarity and market participation have driven pricing to current levels of up to 85% of the IEEPA tariff refund amount

While some importers initially adopted a “wait and see” approach in anticipation of near-term refunds, the combination of timing uncertainty and significantly improved pricing has led many to explore monetization as a way to eliminate risk and accelerate liquidity. The Funds AES works with are able to complete transactions in approximately 2–3 weeks, depending on the completeness and quality of documentation.

The final numbers for 2025 are in, and there has been a GDP Downward Revision… they’ve arrived with a bit of a chill. On March 13, 2026, the Bureau of Economic Analysis (BEA) released its second estimate for the fourth quarter of 2025, significantly revising real GDP growth downward to an annualized rate of 0.7%.

This is a sharp departure from the initial “advance” estimate of 1.4% and a massive deceleration from the robust 4.4% growth seen in the third quarter. For the full year, the U.S. economy grew by 2.1%, a slight dip from previous projections.

So, what happened at the end of the year to take the wind out of the economy’s sails?

The Culprits: Shutdowns, Slumps, and Spending

Several factors converged in late 2025 to create this “soft landing” that felt a little more like a bump.

The 43-Day Government Shutdown: The most visible drag was the historic federal government shutdown that spanned October and November. While essential services remained, the lack of federal paychecks and halted government contracts took a measurable bite out of domestic demand.

A “Low-Hire” Labor Market: While mass layoffs weren’t the headline, a “low-hire, low-fire” environment took hold. Monthly job gains slowed to a crawl, and the unemployment rate ticked up to 4.6% by November, making consumers more cautious with their wallets.

The Trade Drag: Exports were revised downward as global demand softened, and a “front-loading” effect—where companies rushed to import goods earlier in the year to avoid new tariffs—faded out, leaving a gap in activity for the final months.

Sticky Inflation: Despite the slower growth, the PCE price index (the Fed’s favorite inflation gauge) remained at 2.9%. This combination of stagnant growth and persistent inflation has put the Federal Reserve in a difficult “wait-and-see” position.

Silver Linings in the Data

It’s not all doom and gloom. Even with the downward revision, there are signs of underlying resilience:

Investment is Picking Up: While consumer spending moderated, business investment—particularly in AI infrastructure—actually accelerated in Q4, acting as a critical floor for the economy.

Market Resilience: Interestingly, Wall Street took the news in stride. Markets actually rallied following the release, as investors bet that the soft GDP data would finally force the Federal Reserve to consider more aggressive rate cuts later in 2026.

Recouping the Loss: Economists expect much of the “lost” output from the government shutdown to be recovered in the first half of 2026 as backlogged projects and federal spending finally hit the books.

What’s Next for 2026?

The downward revision confirms that the “Goldilocks” era of high growth and falling inflation has hit a snag. Most forecasters, including the IMF and S&P Global, now project a steady but modest growth rate of around 1.8% to 2.0% for 2026.

The big question remains the Federal Reserve. With growth at 0.7% but inflation still above their 2% target, the path to interest rate cuts remains narrow. For now, the “wait-and-see” approach is the only game in town.

1. The Tech Sector: From Growth to Efficiency

While the broader economy slowed, Tech remained a relative fortress, but the “flavor” of investment is changing.

AI Infrastructure as a Life Raft: Business investment in “Intellectual Property Products” (tech speak for software and AI R&D) was one of the few areas that actually accelerated in Q4 2025. Companies are doubling down on AI to find the efficiencies they need to survive a low-growth environment.

The “Low-Hire” Reality: Expect the “low-hire” trend to persist in Silicon Valley. With GDP growth revised downward, tech giants are focusing on “AI-driven productivity” rather than aggressive headcount expansion.

Valuation Pressure: While the stock market has been resilient, persistent 2.9% inflation means the Federal Reserve isn’t in a rush to slash rates. High-growth tech stocks are sensitive to interest rates; if those rates stay “higher for longer,” we may see more volatility in tech valuations throughout 2026.

2. The Real Estate Market: A Tale of Two Interests

The GDP Downward Revision has created a paradoxical situation for housing.

Mortgage Rate Relief? Traditionally, weak GDP data pushes bond yields down, which can lower mortgage rates. Many analysts now expect the 30-year fixed rate to drift toward 6.0%–6.2% in 2026. This could finally “unlock” homeowners who have been trapped by high rates.

The “Sentiment” Gap: The revision highlights a cooling labor market (unemployment at 4.6%). Even if mortgage rates drop, buyer “jitters” may keep the market from exploding. J.P. Morgan research suggests national home prices may stall at 0% growth in 2026 as demand and supply reach a fragile equilibrium.

Commercial Real Estate (CRE) Stress: The 0.7% GDP print is toughest on office and retail CRE. Slower economic activity means less demand for physical space, likely leading to more “strategic defaults” or building repurposing projects in 2026.

The Federal Reserve’s “Tightrope”

The GDP Downward Revision puts the Fed in a bind. Usually, 0.7% growth would trigger an immediate rate cut to “save” the economy. However, with inflation still at 2.9%, they risk reigniting price hikes if they move too fast.

The Bottom Line: 2026 will be the year of the “Efficiency Play.” Whether you are a tech firm or a homebuyer, the goal is no longer “growth at any cost,” but rather finding value in a slower, more deliberate economic landscape.

Headline: 📉 GDP Revised to 0.7%: What it means for Tech & Real Estate in 2026.

The “Second Estimate” for Q4 2025 is out, and the numbers confirm a significant cooling of the U.S. economy. Real GDP growth was revised down to an annualized 0.7%—a sharp drop from the earlier 1.4% estimate.

While the 43-day government shutdown in late 2025 played a major role, the ripple effects for 2026 are already taking shape:

💻 TECH: The era of “growth at any cost” is officially over. We’re seeing a pivot toward Efficiency Tech. While broader spending is cooling, investment in AI infrastructure is accelerating as companies scramble to automate their way out of a low-growth environment.

🏠 REAL ESTATE: It’s a paradox. Slower growth usually means lower mortgage rates, and we’re already seeing 30-year fixed rates dip toward 6.0%. However, with unemployment ticking up to 4.6%, buyer “jitters” are real. J.P. Morgan predicts a 0% national price growth for 2026—a true flatline.

⚖️ THE FED: Chair Jerome Powell and the FOMC are walking a tightrope. With inflation still “sticky” at 2.4%–2.9%, they can’t rush to cut rates despite the sub-1% growth.

The Bottom Line: 2026 will reward the “Lean and Leaner.” Whether you’re managing a portfolio or a product roadmap, efficiency is the new growth.

1/ 🚨 BREAKING: U.S. Q4 2025 GDP revised DOWN to 0.7% (from 1.4%). The 2025 “Cold Snap” is official. Here’s the 30-second breakdown of what this means for your wallet in 2026. 🧵👇

2/ Why the drop? The 43-day government shutdown was a massive anchor, but we also saw a deceleration in consumer spending and exports. The economy didn’t crash, but it definitely pulled the emergency brake. 🛑

3/ 💻 TECH IMPACT: Silicon Valley is staying “Low-Hire.” With 0.7% growth, companies are prioritizing AI-driven productivity over expansion. If it doesn’t automate a process or save a dollar, it’s not getting funded this year.

4/ 🏠 HOUSING IMPACT: Good news? Mortgage rates are sliding toward 5.8%–6.0%. Bad news? A weaker labor market means fewer people are ready to jump. Expect a “sideways” year for home prices. 📉➡️

5/ 🏦 FED WATCH: All eyes on the March 18 FOMC meeting. The market was hoping for cuts, but with inflation at 2.4%, the Fed might stay “Higher for Longer” to ensure the fire is out.

6/Summary: 2026 is the year of the “Efficiency Play.” Growth is slow, money is still relatively expensive, and AI is the only engine still revving. Stay nimble. #GDP #Economy #Inflation

📸 Instagram/Threads: The Visual Summary

Caption:

The numbers are in: The U.S. economy hit a “speed bump” at the end of 2025. 📉 GDP growth was just revised down to 0.7%.

What this means for you: ✅ Mortgage Rates: Might actually get a bit friendlier (seeing 5.8% – 6% averages). ✅ Tech: More AI tools, fewer new job postings. Efficiency is 👑. ✅ Inflation: Still hanging around 2.4%, keeping the Fed on high alert.

It’s not a recession—it’s a recalibration. 2026 is about playing the long game. ♟️

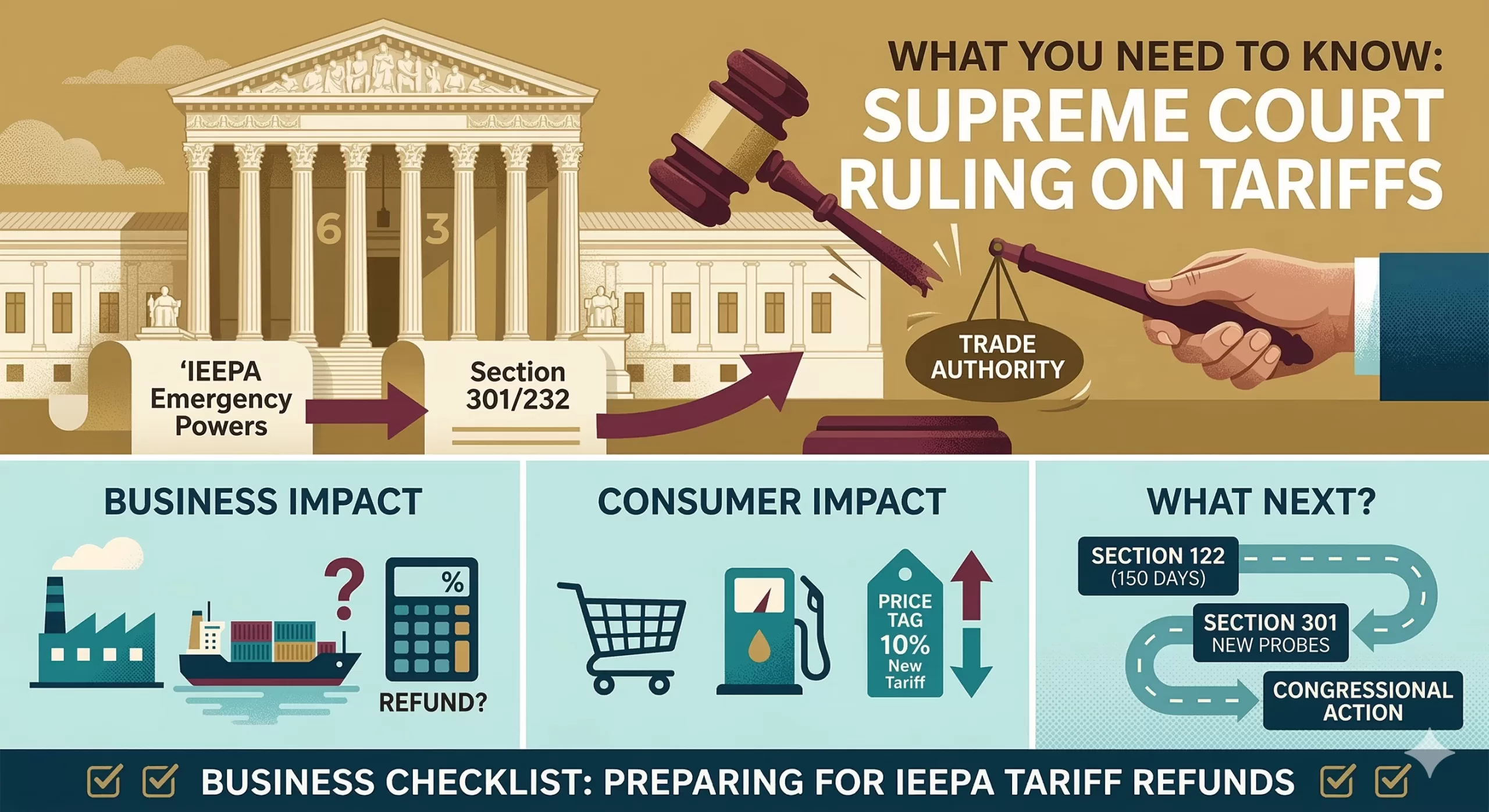

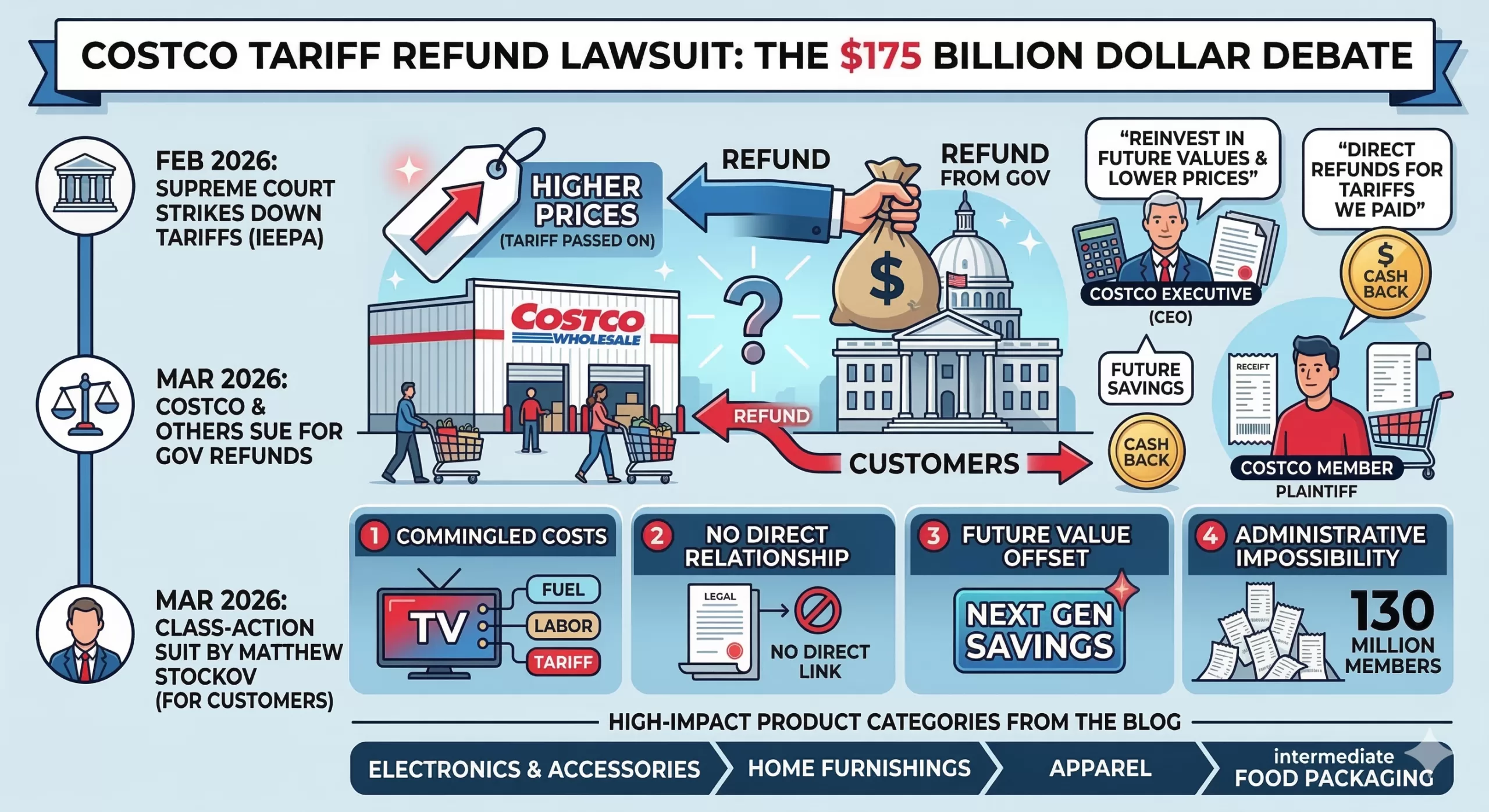

If you’ve noticed your Costco hauls getting a little pricier over the last year due to tariff passthrough, you aren’t alone. But a new legal battle is brewing that asks a multi-billion-dollar question: If a retailer gets a refund for the “illegal” tariff they passed on to you, who actually keeps the cash?

On Wednesday, March 11, 2026, a Costco member in Illinois filed a nationwide class-action lawsuit against the retail giant. The goal? To ensure that any tariff refunds Costco receives from the federal government end up back in the pockets of the shoppers who actually paid for them.

The Backdrop: A Supreme Court Shake-up

The drama started on February 20, 2026, when the U.S. Supreme Court ruled that the sweeping worldwide tariffs imposed last year under the International Emergency Economic Powers Act (IEEPA) were unlawful. The Court found that the executive branch had overstepped its authority, effectively turning roughly $130 billion to $175 billion in collected duties into a massive pot of refundable money.

Immediately, over 2,000 companies—including Costco—filed their own lawsuits against the government to claw that money back.

The Conflict: “Double Recovery” vs. “Better Value”

The new consumer lawsuit, led by plaintiff Matthew Stockov, argues that Costco acted as a “pass-through vehicle.” The logic is simple:

The Hike: Costco raised prices on electronics, household goods, and food to cover the cost of the tariffs.

The Refund: Now that the tariffs are struck down, Costco is suing the government to get that money back.

The “Double Dip”: If Costco keeps the refund and the extra money they already collected from shoppers via higher prices, the lawsuit alleges they are “unjustly enriched” at the expense of their members.

Costco CEO Ron Vachris recently addressed the situation, stating the company’s commitment is to return value to members through “lower prices and better values” in the future.

However, the lawsuit isn’t buying it. The legal team argues that a promise of future discounts for future shoppers doesn’t compensate the specific people who paid the “tariff tax” last year. They want direct restitution.

Is a Refund Actually Coming?

While the Supreme Court ruling is a win for importers, getting cash into the hands of individual shoppers is a legal uphill battle. Here is why:

Standing: Under federal trade law, only the “importer of record” (Costco) has the legal right to claim a refund from the government.

The Math: Proving exactly how much of a $0.50 price hike on a rotisserie chicken was due to a specific tariff vs. inflation or supply chain issues is a forensic accounting nightmare.

The Contract: Legal experts note that when you buy an item, the “contract” is the price on the tag. Retailers generally aren’t legally obligated to refund you if their internal costs go down later.

What’s Next?

Costco isn’t the only one in the crosshairs. Similar suits have been filed against FedEx and EssilorLuxottica (the makers of Ray-Ban).

If the court certifies this as a class action, it could set a massive precedent for how “corporate windfalls” are handled after major policy reversals. For now, Costco members should keep their receipts—and their eyes on the Court of International Trade.

If Costco decides to fight this in court rather than settle, their legal team will likely lean on a defense built around retail economics and contract law.

Here are the four “pillars” of defense they are expected to use:

1. The “Commingled Costs” Argument

Retail pricing isn’t a simple $1+1=2$ equation. When Costco raises the price of a television, that hike accounts for shipping fuel, labor, warehouse rent, insurance, and tariffs. Costco will likely argue that it is mathematically impossible to isolate exactly how many cents of a price increase were “just” for the tariff. Since the costs were commingled, they may argue that specific “tariff surcharges” were never actually charged to the customer.

2. Lack of “Privity” (Direct Relationship)

In trade law, the “Importer of Record” is the only entity with a legal relationship to U.S. Customs.

Costco’s stance: We paid the government; the government owes us.

The logic: There is no contract between Costco and a member that promises to pass through government refunds. When you buy a jar of almond butter, you agree to the price on the tag at that moment, regardless of Costco’s internal cost fluctuations.

3. The “Future Value” Offset

CEO Ron Vachris has already hinted at this strategy. Costco may argue that they are already fulfilling their duty to members by using anticipated refunds to lower prices across the board today. By proving they are reinvesting the money into “better values,” they can claim they are not being “unjustly enriched”—the core requirement for the plaintiff to win.

4. Administrative Impossibility

Costco has over 130 million members. Tracking every single purchase of tariff-affected goods (from socks to patio furniture) over a multi-year period and issuing individual checks would be an administrative nightmare that could cost more than the refunds themselves. They may argue that a “cy-près” award (like a general price drop or a donation to a relevant cause) is a more legal and practical remedy than individual refunds.

Comparison of Arguments

Argument

Plaintiff’s View (Shoppers)

Defense View (Costco)

Enrichment

Costco gets a “double recovery” (shoppers’ money + gov refund).

Costco is a low-margin business that “returns value” via lower future prices.

Pricing

Prices went up specifically because of tariffs.

Prices are set by market competition and total operating costs.

Equity

The specific people who paid the “tax” should get the cash.

It is impossible to track individual “tariff cents” per member.

While Costco is currently the primary target of this specific class-action pressure, other major retailers like Walmart and Target are taking noticeably different approaches to the $175 billion tariff refund opportunity.

Here is how the other giants are positioning themselves:

1. Walmart: The “Conservative Pivot”

Walmart has been more cautious in its public statements regarding specific consumer refunds. Instead of promising direct returns, they are focusing on their role as a “price stabilizer.”

The Strategy: During their recent February 2026 earnings call, Walmart leadership noted they are using their massive scale to absorb costs. Their official stance is that because they negotiate long-term contracts and used “inventory pull-forward” strategies to avoid the worst of the tariffs, they didn’t pass through costs as directly as others.

The Defense: They are positioning any potential refunds as “capital for reinvestment” into their operations and employees, which they argue ultimately benefits customers through lower prices over the long term.

2. Target: The “Supplier Squeeze”

Target’s response has been more aggressive toward its supply chain rather than the federal government.

The Strategy: Target made headlines earlier this year by reportedly asking its Chinese suppliers to absorb up to 50% of the tariff costs to keep shelf prices stable.

The Stance: Because Target forced suppliers to eat much of the cost, they may argue that they aren’t the ones owed the full refund—or that since they didn’t raise prices as much as competitors, there is no “excess profit” to return to consumers.

3. FedEx & UPS: The “Direct Pass-Through” Exception

Unlike retailers where tariff costs are buried in the price of a gallon of milk, shipping companies like FedEx and UPS often used explicit line-item surcharges labeled as “Tariff Fees.”

The Vulnerability: Because these fees were itemized, these companies are facing the most direct legal heat. FedEx has indicated in recent filings that if they receive refunds, they have a framework to pass them back to the original shippers, though the logistics of reaching the end consumer remain a “mess.”

Summary of Retailer Responses

Retailer

Public Stance on Refunds

Primary Defense

Costco

“Future value” through lower prices and better deals.

Administrative impossibility of tracking individual cents.

Walmart

Focused on reinvesting refunds into business operations.

Scaled absorption—claims they didn’t pass through 1:1 costs.

Target

Silent on customer refunds; focused on supplier negotiations.

Argues suppliers bore the cost burden, not just the retailer.

FedEx

Exploring pass-throughs for itemized surcharges.

Contractual obligations to the “shipper of record.”

Why the National Retail Federation (NRF) is Worried

The NRF, which represents all three of these companies, has called for a “seamless and automatic” refund process from the government. However, they are lobbying hard against the idea that retailers must “prove” they passed the money back to consumers, calling such requirements an “accounting nightmare” that would stall the economic boost the refunds are intended to provide.

While the lawsuit filed by Matthew Stockov seeks a blanket refund for “all affected products,” the actual legal battle centers on specific goods that were hit by the International Emergency Economic Powers Act (IEEPA) tariffs.

Because Costco sells such a wide variety of items, the impact is spread across several high-volume categories. Here are the product types most likely to be at the heart of the refund calculations:

1. Electronics and Accessories

This is a massive category for Costco and one of the hardest hit by the reciprocal tariffs.

Small Tech: Laptop bags, charging cables, and power banks.

Peripherals: Computer mice, keyboards, and monitors.

Smart Home: Security cameras and small connected appliances.

Note: Some major electronics (like certain computers) were protected under different trade laws, but “intermediate” components and accessories were often taxed at the full IEEPA rate.

2. Home Furnishings and Hard Goods

Furniture retailers have been among the first to join the “refund clamor.”

Large Furniture: Sofas, dining sets, and patio furniture.

Home Decor: Rugs, textiles, and lighting fixtures.

Kitchenware: Cookware sets and small appliances (like air fryers or coffee makers) imported from affected regions.

3. Apparel and Footwear

These items saw some of the most significant price fluctuations over the last 12 months.

Clothing: “Fast fashion” items, activewear, and outerwear.

Shoes: Sneakers and boots, particularly those where the supply chain relies heavily on international sourcing.

4. Food and Intermediate Packaging

This is the most complex category for Costco to untangle.

Imported Specialties: Specific wines, spirits, and olive oils that were subject to geopolitical surcharges.

Packaging Costs: Even for “American-made” products, the tariffs often applied to the packaging (plastic containers, coffee filters, or baby wipe canisters) imported from abroad. Proving how a tariff on a plastic tub affected the price of the 5-pound tub of animal crackers is a key hurdle for the lawsuit.

What is NOT Included?

It’s important to note that many items at Costco were taxed under different laws (like Section 232 or Section 301), which the Supreme Court did not strike down. You likely won’t see refunds for:

Steel and Aluminum products (including some appliances and car parts).

Specific Chinese-made goods covered under long-standing trade war sections.

Summary Table: Refund Potential by Category

Product Category

Refund Potential

Why?

Electronics Acc.

High

Many were hit with the 2025 “reciprocal” 10-25% tariffs.

Furniture

High

Home goods were a primary target for IEEPA-based levies.

Apparel

Medium

High volume, but often split between different tariff authorities.

Groceries

Low

Most food price hikes were tied to inflation/labor, not just tariffs.

IEEPA Tariff While the Supreme Court invalidated the Administration’s ability to impose tariffs under IEEPA (International Emergency Economic Powers Act), it was deliberately silent with respect to refunds.

As the Administration’s stance is likely to be adversarial, it could take months if not years for businesses to receive IEEPA tariff refunds via conventional channels.

Prior to the Supreme Court Ruling, Hedge Funds were purchasing IEEPA tariff claims at an average of only 22% of the total claim due to the high risks involved. After the Ruling, due to mitigation of some of the uncertainty, they are currently purchasing claims at 75% of the refund amount. Rates are based on claim size and credit quality as tariff refund claims are not assignable. Importers with IEEPA tariff refund claims starting at $500,000 are eligible and there is no maximum limit. AES has monetized $20 million in refund claims since its involvement in brokering IEEPA tariff refund claims commenced 5 months ago. Clients include those in the food, seasonal decoration, apparel and home goods industries.

Instead of waiting 6, 12, 24 months or even longer to receive an IEEPA tariff refund, Hedge Funds can purchase claims within approximately 4 to 6 weeks depending on the quality of documentation assembled by the business.

How the Process of Selling an IEEPA Tariff Claim Works

Concept is: As an example, Company X has paid ($10 Million) in tariffs since April 7, 2025 Company X wants to de-risk prior to determination and finalization of the IEEPA tariff

Refund Process. Company X sells (50%, 100%, or some other percentage) of its tariff ‘claim’ to Buyer A in the form of a participation.

The Trade is nonrecourse to Company X as to the outcome of the Refund Process; but recourse to Company X only if the amount / validity of the claim is proven to be false, or too high.

Process for Selling IEEPA Tariff Claims: As an example, Company X has paid $10 million in IEEPA Tariffs.

Company X agrees to “sell” its tariff claim to Buyer for 75% of the claim amount, i.e. $7.5 million.

Buyer sends Seller a Confirm, and then ultimately a Participation Agreement which will govern the transaction. IMPORTANT – Company X retains its status as the “Plaintiff” / “Claimant” since these tariff claims are not transferable.

Buyer might ask Company X to commence litigation for the return of the IEEPA tariffs paid. The rationale for this is that it is possible that only those parties who have commenced actual litigation are entitled to refunds. Thus, Company X will need to commence litigation in order to receive their refund.

Buyer will continue to monitor the situation and inform Company X of developments. If and when the refund is received on the claim, Company X will receive the refund and forward to the Buyer.

Using an IEEPA Tariff Claim as Collateral for a Loan

In lieu of selling an IEEPA Tariff Claim at a discount, it is possible to use this claim as collateral for a term loan. This term loan would be on a “recourse: basis to the borrower.

The potential loan amount could be up to approximately 50% to 60% of the total IEEPA claim amount. However, the claim must exceed $20 million to qualify for a loan. The interest rate would be in the low to mid-teens.

Key Points Regarding the Sale: Company X (as seller of the Claim) must be a financially healthy enough counterparty for Buyer A to enter into what could be a 2-to-5-year process of obtaining the refund. Legal fees are split going forward based on risk percentage. If Company X sells 100% today, Buyer A will pay 100% of legal costs today.

Buyers are currently paying up to 75% to companies seeking to sell their IEEPA tariff claims. However, this is an evolving market and these percentages can either increase or decrease depending on the markets’ reaction to the Trump Administration’s expected obstructionism and the unresolved Court of International Trade’s procedural issues. Prior to the Supreme Court decision, buyers were purchasing tariff claims at an average of 22% due to the high risks involved.

We will be monitoring on a daily basis the rates at which Buyers are purchasing IEEPA claims and we will update our website accordingly. Feel free to email us to ascertain what the rate is on any particular day.

There would likely be an administrative process instituted such that companies that have paid these IEEPA tariffs will need to file special claims and wait to get refunded by the government. The process of receiving the refund payment from the government could take up to 2 to 5 years according to trade experts.

This details how investment firms are turning a legal and political mess into a new trading opportunity.

The situation stems from a recent Supreme Court ruling that tossed out several of President Trump’s sweeping tariffs. This has created a scramble for companies to claw back the levies they have already paid—estimated to be as high as $133 billion.

The Rise of “Claims Trading”: Large corporations (like retailers and manufacturers) that paid billions in tariffs are now selling the rights to their potential government refunds to Wall Street investors.

Why Companies Are Selling: Rather than waiting years for the government to process refunds or navigate complex litigation, companies are opting for immediate cash by selling their claims at a discount.

The Players: Specialist investment firms—including King Street Capital Management, Anchorage Capital Advisors, and Fulcrum Capital—are among those pouncing on these claims. They are betting that they can eventually collect the full refund from the Treasury, netting a significant profit.

Legal Uncertainty: The Supreme Court has not yet explicitly ruled on whether the government must issue refunds for the tariffs already collected. Despite this, investors are moving quickly to snap up these rights, treating them similarly to how they trade the debt of bankrupt companies.

The “Chaos” Factor: The process is currently a “long, drawn-out mess” with high administrative hurdles. Traders are effectively providing a “liquidity service” to companies that want the tariff money back on their balance sheets now rather than later.

In short, while the reversal of the tariffs has caused massive administrative and fiscal confusion for the government, Wall Street has identified it as a lucrative new asset class.

Factoring Proposal: After recently recovering from the devasting impacts of tariffs, this company requires PO financing to rebuild inventory. Their existing factor is uncooperative and must be replaced by Versant which has the ability to facilitate PO funding though a trusted partner.

Accounts Receivable Factoring can quickly meet the working capital needs of manufacturers. Our underwriting focus is solely on the quality of a company’s accounts receivable, which enables us to rapidly fund businesses which do not qualify for traditional lending

Factoring Program Overview $100,000 to $30 Million Non-recourse Flexible Term Ideal for B2B or B2G

We fund challenging deals: Start-ups Losses Highly Leveraged Customer Concentrations Weak Personal Credit Character Issues

In about a week, we can advance against accounts receivable to qualified businesses which also include Distributors as well as a variety of Service Providers.

The Ripple Effect: Analyzing the Impact of Tariffs on India Imports on US Small Businesses

I. Executive Summary

The imposition of tariffs on imports from India by the United States marks a significant shift in global trade dynamics, with profound and often disproportionate consequences for US small businesses. This report meticulously examines the multifaceted impact of these tariffs, particularly the recently enacted 25% tariff alongside potential additional penalties. It is evident that these measures extend far beyond a simple increase in import costs, manifesting as a systemic shock that reverberates through various operational, financial, and strategic dimensions for small enterprises.

How Tariffs on Indian Imports Impact US Small Businesses

The imposition of a 25% tariff on Indian imports creates a systemic shock for US small businesses, extending far beyond a simple cost increase. This infographic breaks down the critical impacts, from squeezed profits to consumer reactions.

97%

of US Importers are Small Businesses

This highlights the widespread exposure of the small business sector to import tariff policies.

$2,400

Avg. Household Income Loss

Tariffs translate into higher prices, directly impacting consumer purchasing power and demand.

366,000

Jobs Lost in Micro-Businesses

Firms with fewer than 10 employees have seen a 3% employment drop under recent tariff policies.

The Core Problem: A Direct Financial Hit

Tariffs are a tax paid first by US importers. For small businesses, which often operate with minimal financial buffers, this initial cost increase triggers a cascade of negative financial effects.

Profit Margin Vulnerability

A significant portion of small businesses operate on thin profit margins, making them acutely sensitive to any increase in operational costs.

The Cascade of Rising Costs

Beyond the tariff itself, small businesses face a wave of secondary expenses that inflate operational costs and disrupt financial planning.

Supply Chains Under Stress

Small businesses’ reliance on a limited number of suppliers makes them highly vulnerable. Tariffs on a key partner like India create immediate and severe logistical and administrative challenges.

Concentrated Import Reliance

The vast majority of the smallest US companies rely on four or fewer import partner countries, concentrating their risk.

The Logistical Burden Flow

1. 25% Tariff Imposed

↓

2. US Importer Pays Tax Upfront

↓

3. Supply Chain Delays & Fee Hikes

↓

4. Increased Administrative Burden (Customs)

↓

5. Small Business Faces Disruption & Higher Costs

This flow illustrates how tariffs create friction at every step, consuming time, money, and resources for small businesses.

The Consumer Dilemma

Ultimately, tariff costs are passed to consumers. However, shoppers are highly price-sensitive, creating a difficult choice for small businesses: raise prices and risk losing customers, or absorb costs and risk profitability.

Willingness to Pay More for US-Made

👤👤👤👤👤👤👤👤👤

Only 54%

Just over half of consumers are willing to pay up to 10% more. Beyond that, brand loyalty evaporates quickly.

How Consumers React to Price Hikes

When prices for essentials rise, a vast majority of consumers change their behavior, primarily by seeking cheaper alternatives.

Sector Spotlight: Top Imports from India

The 25% tariff impacts a wide range of industries. This chart ranks the top import categories by value, highlighting the sectors where US small businesses face the most significant direct cost increases.

Sectors like Gems & Jewelry, Textiles, and Electronics face billions in tariff-related costs, putting immense pressure on small businesses throughout their supply chains.

A Toolkit for Resilience

Navigating this environment requires proactive and strategic responses. Small businesses must adapt to mitigate risks and build long-term resilience.

🗺️Supply Chain Diversification

Reduce over-reliance on a single country. Explore domestic alternatives and suppliers in non-tariff regions to build a more robust and flexible supply chain.

💲Adaptive Pricing Models

Implement strategic price adjustments. Be transparent with customers about cost pressures while balancing profitability and competitiveness.

⚙️Operational Efficiency

Streamline internal processes and cut non-essential expenses to help absorb tariff costs and improve the bottom line.

🤝Smarter Negotiations

Engage proactively with suppliers to explore cost-sharing solutions, better payment terms, or discounts for bulk orders.

💼Robust Financial Planning

Manage cash flow diligently and leverage lines of credit for emergencies. Review contracts for clauses that can provide relief.

💡Emphasize Quality & Value

Justify necessary price increases by highlighting superior quality, innovation, and the long-term value your products provide.

The analysis reveals that US small businesses, inherently more vulnerable due to their typically thinner profit margins, fewer diversified supplier networks, and limited access to capital, bear a substantial portion of this economic burden. Direct financial strains emerge from increased procurement costs, which often translate into squeezed profit margins and necessitate difficult decisions regarding pricing strategies. Operationally, these tariffs introduce complexities such as supply chain disruptions, heightened administrative burdens, and unpredictable vendor pricing, all of which erode efficiency and profitability. Furthermore, the impact extends to consumer behavior, as higher prices for imported goods lead to reduced demand and a propensity for consumers to seek cheaper alternatives, regardless of origin. Employment within the small business sector also faces headwinds, with evidence suggesting stalled hiring and job losses, particularly among the smallest firms.

In light of these challenges, this report underscores the critical need for both proactive business strategies and supportive policy frameworks. Key recommendations for small businesses include a rigorous and continuous analysis of supply chains, strategic diversification of sourcing to mitigate risks, the adoption of adaptive pricing models that balance profitability with customer retention, and an relentless pursuit of internal operational efficiencies. Concurrently, policymakers are urged to consider the disproportionate impact on small businesses when formulating trade policies, exploring targeted exemptions for critical goods, and enhancing government support programs to ensure their accessibility and effectiveness. The overarching objective is to foster resilience and enable growth for US small businesses within an increasingly unpredictable global trade environment.

II. Introduction: The Evolving Landscape of US-India Trade Relations

The commercial relationship between the United States and India is a dynamic and increasingly significant component of global trade. Understanding the contours of this relationship is essential to grasping the potential ramifications of tariff impositions.

Context of US-India Trade: Volume, Balance, and Key Goods Exchanged

In 2024, the total trade in goods and services between the U.S. and India reached an estimated $212.3 billion, marking an 8.3% increase from the previous year. Goods trade alone, encompassing both exports and imports, amounted to approximately $128.9 billion in the same year. A notable characteristic of this trade relationship is the persistent U.S. goods trade deficit with India, which stood at $45.8 billion in 2024, reflecting a 5.9% increase over 2023. This deficit indicates that the United States consistently imports a greater value of goods from India than it exports, a trend that has seen India’s trade surplus with the U.S. grow substantially from $11 billion in FY13 to an anticipated $43 billion by FY25.

The primary categories of goods imported by the U.S. from India are diverse and critical to various American industries and consumer markets. These include a significant volume of pharmaceutical products, particularly generic drugs and active pharmaceutical ingredients (APIs), and electrical components. Beyond these, the U.S. also imports substantial quantities of stones and jewelry (such as diamonds, gold, and silver), textiles and apparel (including cotton, knit clothing, bed linen, and towels), industrial and electrical machinery parts, iron and steel pipes, auto parts, spices, tea, and rice. Recent estimations suggest that American consumers purchase up to $90 billion worth of imports from India annually. Conversely, the largest U.S. exports to India typically comprise crude oil and various types of machinery, including agricultural and construction equipment. This trade composition highlights India’s role as a key supplier of both finished goods and critical components to the American market.

Historical and Recent Tariff Actions by the US on Indian Imports

The recent imposition of tariffs by the U.S. on Indian imports is not an isolated event but part of a broader strategy to address perceived trade imbalances and geopolitical concerns. In a significant move, former President Donald Trump announced a 25% tariff on all goods imported from India, effective August 1, coupled with an additional penalty related to India’s purchases of oil from Russia. This measure is particularly notable for its sweeping nature, as it applies uniformly across Indian imports and, unlike tariffs applied to other trading partners, denies India product-level exemptions that were previously granted.

Historically, the U.S. administration has characterized India as the “Tariff King,” citing India’s high duties on American goods. However, this perspective is often countered by experts and industry observers who point to the substantial duties levied by the U.S. on various imported items, such as 350% on beverages and tobacco, 200% on dairy products, and 132% on fruits and vegetables, according to World Trade Organization (WTO) data. The current 25% tariff on India is positioned as a “reciprocal” measure within a broader trade policy framework, where other nations face differing tariff rates. The inclusion of sectors previously exempt from tariffs, such as pharmaceuticals and electronics, further amplifies the potential impact of this new policy on the U.S. market. This approach signals a more aggressive stance aimed at recalibrating trade terms and leveraging economic pressure for strategic objectives.

The Strategic Importance of India as a Trading Partner and Sourcing Destination for US Businesses

India’s role in the global economy and its strategic importance to the United States extend beyond mere trade volumes. As the world’s most populous country, exceeding 1.4 billion people, India is increasingly viewed as a crucial geopolitical counterbalance to China. Economically, India has long provided U.S. companies with cost-effective outsourcing and sourcing opportunities, primarily due to lower factory wages and a lower cost of living. This economic advantage has made India an attractive destination for businesses seeking to minimize operational expenses and secure competitive pricing for their goods and components. Historically, the absence of Section 301 duties further enhanced India’s appeal as a cost-effective supplier.

The application of “reciprocal” tariffs, while ostensibly aimed at achieving fairness in trade, introduces a complex dynamic. While the stated goal is to address India’s high tariffs , the implementation of these tariffs on Indian imports, particularly the denial of exemptions granted to other countries , creates a significant disadvantage for U.S. businesses that rely on Indian supply chains. This selective application means that the “reciprocal” nature of the tariffs is not truly symmetrical, leading to a disproportionate cost burden on specific U.S. small businesses that source from India. Such an approach complicates diplomatic efforts to resolve trade disputes, as India perceives this targeting as unjustified. The consequence is an uneven playing field where U.S. businesses importing from India face higher costs compared to those sourcing from nations with lower tariff rates or exemptions, potentially distorting market competition and increasing the overall expense for American enterprises.

Furthermore, the tariffs are explicitly linked to broader geopolitical objectives, specifically India’s continued procurement of Russian oil and military equipment, which is seen as enabling Russia’s war efforts in Ukraine. India, in response, highlights the perceived hypocrisy of the U.S. and European Union, noting their own continued trade relations with Russia, including critical imports like uranium hexafluoride, palladium, fertilizers, and chemicals by the U.S.. This underscores that the tariffs are not solely economic instruments but are deeply intertwined with foreign policy and strategic leverage. This geopolitical dimension introduces a substantial layer of risk and unpredictability for U.S. small businesses. The potential for tariffs to be imposed or adjusted based on evolving international relations, rather than purely economic factors, makes long-term supply chain planning exceptionally challenging. Small businesses, which typically lack the extensive resources and diversified global operations of larger corporations, are particularly susceptible to these unpredictable shifts driven by geopolitical considerations. This dynamic also incentivizes India to accelerate its “Make in India” initiative and diversify its export markets , potentially reducing its long-term reliability as a consistently low-cost sourcing option for U.S. businesses.

III. Direct Financial Impacts on US Small Businesses

The imposition of tariffs on Indian imports directly translates into tangible financial pressures for U.S. small businesses, affecting their cost structures, profit margins, and overall operational viability.

Increased Costs and Squeezed Profit Margins

Tariffs, fundamentally, are a tax levied on imported goods, which are initially paid by U.S. importers and subsequently passed along the entire supply chain. This direct cost increase has led to significant financial strain for many small businesses, with reported cost spikes ranging from 10-20% due to the current tariff environment. These elevated costs directly erode the already thin profit margins characteristic of many small enterprises. Unlike larger corporations that often possess the financial cushion of substantial margins or extensive, diversified supplier networks, small businesses are acutely sensitive to these tariff-induced cost increases. For instance, the gems and jewelry industry, which heavily relies on Indian imports, finds the 25% tariff a “steep percentage” that is difficult to absorb.

The initial tariff payment by American importers creates a discernible multiplier effect on operational costs and overall profitability. This occurs because the initial cost increase, whether 10-20% or the full 25% for Indian goods, cascades through the supply chain. Importers, facing higher procurement expenses, typically pass these costs on to wholesalers and distributors, who in turn transfer them to retailers, and ultimately, to the end consumer. Even small businesses that do not directly import goods but rely on domestic suppliers are affected, as their vendors often pass along their own tariff-related cost increases. This compounding effect means that the initial tariff percentage can lead to even higher final price increases for small businesses. Their inherently “thin profit margins” leave them with limited capacity to absorb these escalating costs. Consequently, these businesses are often compelled to make a difficult choice: either raise their prices, risking a loss of competitiveness in the market, or absorb the increased costs, jeopardizing their financial viability and long-term sustainability. This situation also implies that the revenue generated by tariffs for the U.S. government is effectively borne by American businesses and consumers, rather than directly by foreign governments.

Rising Operational Expenses

Beyond the direct cost of the tariffs themselves, small businesses face a range of rising operational expenses that further compound their financial challenges.

Increased Vendor Rates to Offset Tariffs: Even if a small business does not engage in direct importing, their domestic suppliers are likely to be impacted by tariffs on their own imported materials or components. Many vendors, facing their own increased costs, will inevitably pass these along to their small business clients. This necessitates that small businesses remain vigilant for sudden price hikes or changes in contract terms from their existing suppliers.

Shipping and Customs Fee Hikes: Tariffs can introduce significant friction into global supply chains. This friction often manifests as delays in customs processing, which in turn can lead to higher shipping fees and additional surcharges. These unexpected costs can rapidly erode profit margins and disrupt carefully planned delivery timelines, adding an unpredictable layer of expense to operations.

Currency Shifts Inflating International Spend: The imposition of tariffs can trigger volatility in foreign exchange markets. For small businesses that pay vendors or contractors in foreign currencies, fluctuations in exchange rates can significantly drive up the cost of international transactions. This currency risk complicates budgeting and financial forecasting, making it harder for small businesses to predict and manage their international expenditures.

The cumulative effect of these factors extends beyond direct tariff costs, introducing a range of hidden expenses that profoundly impact small business operations. The research highlights that the “tariff impact on business extends beyond direct costs to include administrative burden, cash flow disruption, and strategic planning complications”. The overall “economy of uncertainty” fostered by unpredictable trade policies makes it exceedingly difficult for small businesses to engage in effective long-term planning. This uncertainty is not confined to the tariff rate itself but encompasses its potential duration, scope, and the likelihood of further adjustments. These hidden costs—including increased administrative overhead, disruptions to cash flow, and complexities in strategic planning —are particularly detrimental for small businesses. These firms typically lack the sophisticated financial modeling capabilities and diversified operational structures that larger companies possess. The constant shifts in trade policy create a “whiplash effect” that consumes valuable time, resources, and attention, diverting focus away from core business activities and hindering investments in growth and innovation.

IV. Supply Chain Disruptions and Operational Challenges

The implementation of tariffs on Indian imports introduces significant disruptions and operational hurdles for U.S. small businesses, exacerbating their inherent vulnerabilities within global supply chains.

Vulnerability of Small Business Supply Chains

Small businesses are particularly susceptible to the adverse effects of tariffs due to several structural characteristics. They often possess less purchasing power and maintain fewer trading partners compared to larger enterprises. For instance, a substantial 95% of companies with 1-19 employees rely on four or fewer import partner countries. This limited diversification means that when a key sourcing country like India is targeted with tariffs, the impact is immediate and concentrated. Small businesses also lack the financial buffer of large corporate margins or the flexibility afforded by extensive, diversified supplier networks. While specific data on U.S. small business reliance on Indian imports by sector is not extensively detailed, it is understood that small and medium-sized enterprises (SMEs) constitute a staggering 97% of all U.S. importers. Furthermore, SMEs account for 40% of known imports from China , a figure that, while specific to China, illustrates a general pattern of concentrated reliance on specific, potentially tariff-targeted, countries. This principle of concentrated reliance applies equally to imports from India, making these businesses highly exposed.

The disproportionate reliance on fewer import partners and a historical tendency to prioritize low-cost sourcing mean that the imposition of tariffs on a significant low-cost source like India immediately exposes a critical lack of supply chain diversification. Unlike larger firms that benefit from “more diversified production locations” and “greater negotiating power” , small businesses find it exceedingly difficult to pivot quickly to alternative sources. This structural vulnerability implies that tariffs on Indian imports create an “outsized burden” for small businesses. The immediate disruption is magnified, compelling these businesses to seek alternatives that may not be readily available or cost-effective. This reliance on previously inexpensive overseas products, now made significantly more expensive by tariffs, forces a fundamental re-evaluation of their entire business model and sourcing strategy.

Logistical and Administrative Burdens

The impact of tariffs extends beyond direct financial costs, creating cascading effects throughout a small business’s operations, particularly in logistics and administration. Tariffs can lead to significant supply chain delays and introduce unpredictable vendor pricing. A critical, yet often overlooked, administrative burden is the necessity of correctly classifying imports under complex tariff codes for accurate cost planning. Any misclassification can result in penalties or further delays, adding to the financial strain.

A particularly impactful change is the suspension of the “de minimis” exception, which previously allowed shipments valued under $800 to enter the U.S. duty-free. This suspension means that even very small, frequent imports will now incur duties and require proper classification and customs processing. This significantly increases the administrative load for small businesses, many of which lack dedicated import/export departments or the specialized expertise to navigate complex customs procedures. This creates a state of “business tariff chaos” and presents “complex logistical puzzles”. For small businesses, this administrative overhead is not a trivial expense; it consumes valuable time and resources that could otherwise be allocated to core business activities, innovation, or growth initiatives. The increased complexity can also lead to errors in classification, potential fines, and further delays, compounding the financial pressure and making international trade a more daunting prospect for smaller players.

V. Impact on US Consumers: Price Sensitivity and Demand Shifts

The economic consequences of tariffs on Indian imports extend directly to U.S. consumers, primarily through increased prices and subsequent shifts in purchasing behavior. These changes, in turn, exert further pressure on small businesses.

Passing on Costs to Consumers

Tariffs are a tax, and the burden of this tax is largely borne by U.S. consumers. Analyses suggest that prices could increase by approximately 1.8% in the short term as a direct result of trade disputes, translating to an estimated loss of $2,400 in income per U.S. household. SBI Research corroborates this, projecting a substantial financial burden for U.S. households, with an average cost of $2,400 in the short term due to increased prices. A study from 2019 indicated that American consumers and companies were absorbing nearly the full cost of these tariffs. When tariffs raise input costs for businesses, domestic manufacturers are compelled to increase their product prices to maintain their profit margins.

The financial impact of tariffs is not uniformly distributed across the consumer base. While the average household faces a $2,400 burden , a closer examination reveals a disproportionate effect on lower-income households. Low-income families, for instance, may experience losses of approximately $1,300, whereas higher earners, despite facing a larger nominal hit of up to $5,000, are generally less affected in terms of their overall financial stability. This observation highlights that tariffs, by increasing the cost of imported goods, function as a regressive tax. They consume a larger percentage of disposable income for lower-income households, which can lead to a reduction in overall consumer spending. This reduction is particularly pronounced for non-essential goods, subsequently impacting small businesses across various sectors, not exclusively those directly involved in importing from India.

Changes in Consumer Behavior

Rising prices directly influence consumer purchasing habits. If essential goods like groceries experience price increases due to tariffs, a significant 88% of Americans indicate they would alter their shopping behavior, with one-third cutting back on purchases and another third switching to more affordable brands. This suggests a strong inclination among consumers to seek cheaper alternatives when prices rise. While over half of Americans (54%) express a willingness to pay up to 10% more for U.S.-made goods, this willingness sharply declines beyond that threshold, with most consumers opting to “walk away” from higher-priced items. For a substantial 30% price increase, as many as 91% of consumers would hesitate or outright refuse to buy the product.

A notable aspect of consumer sentiment is the expectation that businesses should absorb tariff costs rather than pass them on. Only one in three Americans believe these costs should be transferred to consumers. Nearly half of consumers even suggest that companies should relocate manufacturing to the U.S. if tariffs lead to a 30% price increase. Despite a stated preference for supporting U.S.-made goods (68% believe it’s key to supporting the economy), a significant 9 out of 10 Americans do not actively check a product’s origin before purchasing. For one in three shoppers, price remains the sole determining factor. This creates a direct conflict for U.S. small businesses: while tariffs could theoretically stimulate demand for domestic alternatives, the reality is that consumers are highly price-sensitive. Small businesses that pass on tariff costs, even partially, risk losing customers to cheaper alternatives, whether these are imports from other countries or products offered by larger retailers with greater economies of scale. This situation places small businesses in a difficult position: absorb costs and compromise profitability, or raise prices and lose market share, potentially undermining the intended protective effect of the tariffs.

Reduced Product Choices and Market Innovation

Beyond direct financial impacts and behavioral shifts, tariffs can subtly diminish market vitality by reducing consumer choices and stifling innovation. By making certain imports unprofitable, tariffs can narrow the range of products available in stores. Consumers may find fewer options as some imported goods become prohibitively expensive to justify importing.

Furthermore, tariffs can weaken the incentives for businesses to innovate and develop streamlined processes that enhance productivity and maintain competitiveness. When businesses are preoccupied with navigating increased costs and supply chain disruptions, their focus shifts from long-term strategic investments in research and development or process optimization to short-term survival. Tariffs, by increasing costs and limiting supply choices , compel businesses to prioritize cost absorption or price increases. This environment can inadvertently favor less innovative domestic producers who are shielded from foreign competition. This long-term impact on innovation can undermine the overall dynamism and competitiveness of the U.S. economy, extending beyond the immediate price effects. Small businesses, often at the forefront of niche innovation, may find their capacity to experiment with new products or materials severely constrained by higher import costs and reduced access to a diverse array of global components.

VI. Employment Implications for US Small Businesses

The economic pressures exerted by tariffs on Indian imports have tangible consequences for employment within the U.S. small business sector, leading to job losses and a slowdown in hiring.

Job Losses and Stalled Hiring

The 25% tariff on Indian goods is anticipated to negatively affect several key employment-generating sectors. Broader economic analyses indicate that President Trump’s trade policies, including tariffs, are placing significant financial pressure on American households and small business owners, contributing to reduced take-home pay for workers. While not exclusively linked to India-specific tariffs, the manufacturing sector has already experienced job losses, with factories cutting 11,000 jobs in July, following reductions of 15,000 in June and 11,000 in May. This trend indicates a broader negative impact on manufacturing employment under tariff regimes.

More directly, employment among the smallest businesses (those with fewer than ten employees) has seen a notable decline of 3%, translating to a loss of 366,000 jobs since President Trump took office. This is particularly significant given that small businesses collectively constitute 97% of all U.S. importers. The pervasive uncertainty generated by tariff policies compels businesses nationwide to pause hiring, resulting in fewer new job opportunities for those entering or re-entering the labor market. This phenomenon has been characterized as a “low-hire, low-fire” labor market, reflecting a cautious approach by employers in an unpredictable economic climate.

The data explicitly highlights that the smallest businesses, those with fewer than ten employees, are disproportionately affected, experiencing a 3% drop in employment, equating to 366,000 jobs lost since the current administration took office. This is a critical observation, as these micro-businesses represent a vast majority of U.S. importers. This suggests that the employment impact of tariffs is not evenly distributed but rather concentrated among the most vulnerable small businesses. These firms, often operating on extremely thin margins and with limited cash flow, are forced to make “tough decisions” such as reducing staff or implementing layoffs to preserve profitability. This outcome directly contradicts the stated objective of tariffs, which is often to stimulate domestic job creation. The job losses observed in import-dependent small businesses may, in fact, offset or even outweigh any employment gains in protected domestic manufacturing sectors.

Competitive Disadvantage

Tariffs also exacerbate existing competitive disadvantages for small businesses. These enterprises typically possess fewer tools and resources to cope with unforeseen risks and unanticipated costs compared to their larger counterparts. As larger competitors leverage their economies of scale, extensive financial reserves, and diversified operations to navigate the challenges posed by tariffs, small businesses with less market power find themselves at a distinct disadvantage. This situation is particularly acute for small and mid-size retailers, who have fewer options than larger retailers when faced with drastically rising import costs, placing them in a significantly more difficult competitive position.

Tariffs impose a universal cost increase on imported goods. However, large businesses are equipped with “more diversified production locations,” “greater negotiating power with suppliers,” “extensive warehousing options for local storage,” and “complex pricing models” that allow them to minimize the impact on their business. Small businesses, by contrast, generally lack these strategic advantages. This inherent disparity means that the tariffs, rather than creating a level playing field, effectively widen the competitive gap between large and small businesses. Small businesses are forced into a reactive stance, struggling to absorb costs or pass them on to consumers, while larger firms can more effectively mitigate the impacts through their scale and resources. This dynamic could lead to market consolidation, where smaller players are either acquired, driven out of business, or compelled to significantly scale back their operations. Ultimately, this reduces market diversity and can diminish local economic vitality across the nation.

VII. Sector-Specific Deep Dive: Vulnerabilities and Adaptations

The impact of tariffs on Indian imports is not monolithic; it manifests differently across various U.S. sectors, depending on their reliance on Indian goods and their specific market dynamics.

Pharmaceuticals

The U.S. healthcare system relies heavily on pharmaceutical imports from India, particularly generic drugs and active pharmaceutical ingredients (APIs). India is a cornerstone of the global supply chain for affordable, high-quality medicines, supplying nearly 47% of the pharmaceutical needs of the U.S.. Indian pharmaceutical companies are crucial for the affordability and availability of essential medications, including life-saving oncology drugs, antibiotics, and treatments for chronic diseases.

The immediate consequence of a 25% tariff on these imports would be a rise in drug prices and potential shortages across the U.S.. The U.S. market’s substantial reliance on India for APIs and low-cost generics means that finding alternative sources capable of matching India’s scale, quality, and affordability could take a considerable period, estimated at 3-5 years.

The significant reliance on India for nearly half of U.S. pharmaceutical needs indicates that tariffs in this sector are not merely an economic concern but a critical public health and national security issue. The potential for “shortages and escalating prices” for “life-saving oncology drugs, antibiotics, and chronic disease treatments” directly affects the health and well-being of American citizens and the overall stability of the U.S. healthcare system. This highlights a critical dependency. Tariffs, while intended to create economic leverage, could inadvertently destabilize the U.S. healthcare supply chain, potentially leading to a crisis of access and affordability for essential medicines. This suggests that the economic cost of tariffs in the pharmaceutical sector could be overshadowed by the profound societal and public health costs, potentially necessitating a re-evaluation of tariff application in such critical industries.

Textiles and Apparel

Textiles and apparel represent significant import categories for the U.S. from India. The Indian textiles sector is largely composed of Micro, Small, and Medium Enterprises (MSMEs), accounting for nearly 80% of its structure. The imposition of a 25% tariff is projected to make Indian textile products 7-10% more expensive than those from competitors like Vietnam and China, thereby significantly impacting apparel exports to the U.S.. Already, U.S. buyers have begun to put new orders on hold or demand discounts from Indian suppliers. U.S. small businesses that import textiles face considerable challenges, particularly those operating on tight margins.

The tariffs render Indian textiles less competitive against rivals from Vietnam and China. While the tariff difference between India and China has narrowed (25% on Indian goods versus 30% on Chinese goods) , other countries like Bangladesh face a lower 20% duty rate. This places U.S. small businesses importing textiles from India at a disadvantage compared to those sourcing from other Asian nations. This creates a complex competitive landscape for U.S. small businesses. They are compelled to either absorb the higher costs, switch suppliers (which, as discussed, comes with its own set of challenges), or pass these increased costs on to consumers, thereby risking market share. The tariffs do not necessarily lead to a resurgence of manufacturing in the U.S. but rather shift sourcing to other low-cost countries, potentially undermining the stated goal of domestic job creation while still harming U.S. small businesses reliant on diversified global supply chains.

Gems and Jewelry

Stones and jewelry, including diamonds, gold, and silver, constitute major U.S. imports from India. The U.S. market is critically important for India’s gems and jewelry sector, accounting for over $10 billion in exports, which represents nearly 30% of India’s total global trade in this industry. While the industry previously attempted to absorb 10% tariffs, a 25% tariff is considered a “steep percentage for them to digest”. The U.S. market alone accounts for 28% of India’s total exports in this sector.

Gems and jewelry are typically discretionary purchases. When tariffs increase the cost of these items, consumers, who are already contending with higher prices for essential goods , are highly likely to reduce spending on non-essential items. The reported difficulty of the industry to absorb even a 10% tariff suggests either very thin profit margins or a high degree of price sensitivity among consumers for these products. For U.S. small businesses engaged in the sale of gems and jewelry, the tariffs present a dual challenge: higher import costs combined with a probable reduction in consumer demand for more expensive discretionary goods. This could lead to significant revenue declines and, in severe cases, business closures, as consumers prioritize necessities over luxury items in an inflationary economic environment.

Electronics and Machinery Parts

The U.S. imports a substantial volume of telecom and electrical components from India, which are vital for powering phone and internet networks. Industrial and electrical machinery parts are also key imports. The imposition of a 25% tariff introduces new variables for exporters, particularly in the electronics sector where supply chains are globally integrated. Indian electronics exports are expected to face a “short-term challenge that could disrupt supply chains and dent price competitiveness”.

The reliance on Indian electrical components for U.S. phone and internet networks highlights a critical interdependency within the digital economy. Tariffs on these components do not merely affect the final product price; they can disrupt the foundational infrastructure of the digital economy itself. The “globally integrated” nature of electronics supply chains means that a tariff on one component can trigger ripple effects that extend far beyond the initial import. For U.S. small businesses involved in IT services, telecommunications, or manufacturing that utilizes these components, tariffs on Indian electronics translate into higher input costs, potential supply chain delays, and reduced competitiveness. This can impede technological innovation and adoption across a wide array of businesses that depend on these foundational technologies, potentially leading to a broader economic slowdown rather than targeted domestic growth.

Seafood and Agricultural Products

Indian shrimp exporters are significantly affected by the tariffs, with the U.S. accounting for 40% of India’s total shrimp exports. In FY24, India exported 297,571 million tonnes of frozen shrimp valued at $4.8 billion to the U.S.. These tariffs represent a “significant setback for India’s exports” of seafood and agricultural products, causing disruptions in supply chains and exerting downward pressure on farm gate prices in India.

The tariffs directly impact a substantial portion of U.S. shrimp imports from India. This will inevitably lead to higher prices for seafood in the U.S., directly affecting consumers. The original data also notes the ripple effect on “farmers’ incomes and employment, especially in rural areas” in India. For U.S. small businesses in the food service, grocery, or specialty food retail sectors, higher costs for imported shrimp and other agricultural products will necessitate either price increases (to which consumers are sensitive, as noted in ) or the absorption of these costs, further squeezing already tight margins. This demonstrates how tariffs on specific food items contribute directly to inflation for U.S. consumers and can disrupt established supply chains for staple goods, affecting both business profitability and consumer affordability.

Table 1: Key US Import Categories from India and Tariff Impact

To provide a clearer picture of the specific sectors most affected and the magnitude of the trade involved, the following table summarizes key U.S. import categories from India and the anticipated impact of the 25% tariff. This table serves to quantify the direct financial burden on U.S. importers, which subsequently translates into higher costs for small businesses. It also aids in identifying sectors where small businesses will need to implement targeted mitigation strategies. For policymakers, this data highlights areas where the tariffs will have the most significant economic and social consequences, informing potential adjustments or support measures.

Product Category

Total US Imports from India (Value, FY24/25)

Previous Tariff Rate (if available)

New Tariff Rate (25%)

Key Impact on US Small Businesses

Relevant Snippet IDs

Pharmaceuticals (generic drugs, APIs)

$9.8 billion (FY25) , $8 billion (FY24) (47% of US needs)

Varied, some as low as 0%

25%

Increased input costs, rising drug prices, potential shortages, supply chain disruption, difficulty finding alternatives in scale/quality/affordability

Textiles/Apparel (cotton, knit, bed linen, towels)

$10.3 billion (FY25) , $11 billion (FY24)

Varied, often low

25%

Reduced competitiveness against rivals (Vietnam, China), increased input costs, potential loss of orders, squeezed margins

Gems and Jewelry (diamonds, gold, silver)

$12 billion (FY25) , $10 billion (FY24) (28-30% of India’s total exports)

Supply chain disruption, dented price competitiveness, increased cost structures, new variables for exporters

Seafood (shrimp)

$2.24 billion (FY25) , $4.8 billion (FY24) (40% of India’s shrimp exports to US)

Not specified

25%

Uncompetitive Indian shrimp exports, disrupted supply chains, pressure on farm gate prices, increased costs for US food businesses

Leather and Leather Products

$795.55 million (FY25, Apr-Dec)

Not specified

25%

Increased input costs, reduced competitiveness in US market

Auto Parts

Not specified

Not specified

25%

Increased input costs for US auto repair/manufacturing small businesses

Spices, Tea, Rice

Not specified

Not specified

25%

Increased costs for specialty food retailers, restaurants

VIII. Strategic Responses for US Small Businesses: A Comprehensive Toolkit

Navigating the complexities introduced by tariffs on Indian imports requires U.S. small businesses to adopt a multi-pronged strategic approach, encompassing supply chain optimization, adaptive pricing, enhanced operational efficiency, and robust financial management.

Supply Chain Optimization

A fundamental response to tariff impacts involves a thorough re-evaluation and optimization of existing supply chains.

Conducting Comprehensive Supply Chain Analysis: The initial step for any small business is to meticulously examine its current supply chain. This involves identifying precisely which products or raw materials are directly affected by the new tariffs and quantifying the potential cost increases associated with each impacted item. Understanding the specific tariff codes relevant to their imports is crucial for accurate cost planning. This detailed analysis allows businesses to pinpoint vulnerable points and prioritize actions accordingly.

Exploring Domestic Alternatives and Diversifying International Suppliers: Once vulnerabilities are identified, small businesses should actively explore domestic sourcing alternatives or seek suppliers from countries not subject to the new tariffs. This exploration requires a careful assessment of the trade-offs between cost and quality. Diversifying suppliers across different geographic regions is a key strategy to reduce over-reliance on any single source, thereby enhancing overall supply chain resilience.

While the notion of tariffs creating “opportunity in uncertainty” for some U.S. small businesses to boost domestic production or foster more resilient supply chains exists, this is a complex and often paradoxical reality. Tariffs, while painful for many small businesses , can indeed compel a re-evaluation of business models. However, the immediate transition to diversified or domestic sourcing is fraught with challenges. Sourcing from new countries presents hurdles such as fragmented supplier bases, inconsistent quality standards, and significant logistics and transportation issues (e.g., slower freight movement and higher logistics costs in India). Concerns regarding intellectual property protection and difficulties in managing new supplier relationships and communication also arise. Furthermore, “reshoring” production to the U.S. can entail higher costs and challenges in securing skilled labor or suitable facilities. This means that while the long-term goal may be more resilient supply chains, the immediate path requires substantial upfront investment and risk-taking, which many small businesses may not be equipped for without external support. Small businesses must “turn on their entrepreneurial gene” and proactively “work on their business” rather than just “in their business” to survive and potentially thrive in this new environment.

Pricing Strategies

In response to increased import costs, small businesses must carefully consider their pricing strategies to maintain profitability while retaining customer loyalty.

Implementing Strategic Price Adjustments: Businesses have two primary approaches to adjusting prices: adding a temporary surcharge or incorporating the increased cost into a general, permanent price increase. A tariff surcharge offers transparency, clearly communicating to customers that higher costs are due to external factors and allowing for easier reversal if tariffs are removed. Conversely, folding the cost into a general price increase simplifies invoicing and financial management, signaling a long-term cost adjustment. The choice between these methods depends on industry norms, customer sensitivity, and the anticipated duration of the tariffs.