The first few warm days of spring mean flowers, baseball, and for many small business owners in March 2026, the annual financial checkup. If you’ve looked at your numbers and realized you need a cash injection for new equipment, that third location, or an aggressive inventory build, you know the drill: It’s time to find the capital. While large national banks are the obvious choice, they are often difficult, impersonal, and slow. By comparison, credit unions have become the unexpected superstars of commercial lending, especially for small and medium-sized enterprises (SMEs).

If you are hunting for a business loan this month, you need to understand why credit unions are dominating and how to find the one that will actually make that critical “yes” happen for your business.

The Not-So-Secret Advantage of the Member-Owner

To understand why credit unions often beat banks on business lending, you have to look at their structure.

Banks answer to shareholders who demand profits and high returns on equity. Every decision, including who gets a loan, is filtered through the lens of maximizing shareholder value.

Credit unions, however, are not-for-profit cooperatives. They do not have public stock. Their members (you, me, and other account holders) are the owners.

This single difference ripples through every interaction. For business lending in 2026, it means:

1. Rates and Fees That Just Make More Sense: Instead of returning profit to Wall Street, credit unions reinvest earnings back into the institution and their members. This often manifests as lower interest rates on commercial loans and significantly lower loan-origination and maintenance fees. In 2026, when inflation has been a recent headache, a difference of 0.5% on a large loan term can mean thousands of dollars saved.

2. Hyper-Local Expertise: When you sit down with a commercial lender at a bank, their rules, algorithms, and models might be set at headquarters 2,000 miles away. They may not understand the specific micro-market in Newtown, Connecticut, where you are operating. But your local credit union officer lives here. They understand why opening a second pizza parlor on the new development is a smart bet, not a risky venture. They lend based on local market knowledge.

3. Relationships Over Risk-Scores: A bank will look at your credit score and financial statements, enter them into a model, and receive a automated “Approve” or “Deny.” Credit unions, especially smaller, focused ones, prioritize relationships. They are more likely to have a real human look at your complete business plan, understand your unique vision, and listen to the story behind your application, not just the numbers on the page.

The “New Reality” of SBA Lending

One of the most important developments in 2026 is that the Small Business Administration (SBA) has made it significantly easier and faster for credit unions to facilitate SBA 7(a) and 504 loans.

For many small businesses, these government-backed loans are the Holy Grail: long terms, lower interest rates, and lower down-payment requirements. Previously, massive banks dominated this space because the paperwork was crushing.

However, the “Streamline and Connect Act” of 2024 (as we projected) drastically simplified the SBA application process and created digital interfaces specifically designed for smaller community financial institutions.

This means that in March 2026, the local credit union you never expected to handle an SBA application is now a Preferred Lender, capable of getting your government-backed loan approved in weeks, not months.

How to Evaluate a Credit Union in March 2026

You can’t just walk into the nearest credit union and expect a perfect loan offer. To find the “best” one for your business right now, you must be strategic:

Step 1: Membership Criteria (The Gateway)

Credit unions can’t just lend to anyone. They operate under a specific “field of membership” (FOM). While some have broadened their charters, many are still strictly limited. To find the “best,” you must find the one you can actually join.

Geographic FOM: Are you eligible because your business is located in Newtown, CT, or the surrounding county? This is the most common path.

Associational or Professional FOM: Are you a veteran? An educator? A first responder? A member of a specific local church or union? There are niche credit unions specialized for these groups, and they often offer highly beneficial industry-specific lending programs.

Step 2: Technology and Speed

While personal relationships are the hallmark of credit unions, it’s 2026. You should not have to wait 30 days for a response to your application. A strong, business-friendly credit union will have a fast, streamlined digital application portal.

They should have digital tools that connect directly to your accounting software (like QuickBooks or Xero), allowing their lenders to instantly verify your cash flow without forcing you to hunt down piles of paper bank statements. If a credit union’s website looks like it hasn’t been updated since 2018, that is a massive red flag.

Step 3: Ask About Specific Business Expertise

The credit union that is excellent for a car loan or a personal mortgage is not necessarily the best choice for a $500,000 commercial line of credit to finance inventory for a manufacturing business.

When you interview a prospective credit union, ask about their experience in your industry. A credit union that specializes in healthcare practice lending will have different perspectives and better loan structures than one that primarily works with general contractors.

The March 2026 Takeaway: Don’t Lead with a Bank

Your default shouldn’t be the massive financial conglomerate that you can only reach via an 800-number. Your first stop in 2026 should be your local, community-focused credit union. They are built to serve owners like you, and they have the tools and local knowledge to help your business take flight this spring.

While the macro economy is feeling the “pump shock,” the impact on small business lending and accounts receivable (AR) factoring is more nuanced. For many industries, rising oil prices act as a catalyst for alternative financing, as traditional bank credit tends to tighten just when operational costs spike.

1. Impact on Small Business Lending

Traditional bank lending to small businesses is becoming more restrictive as energy-driven inflation persists.

The “Double Squeeze”: Small businesses are facing higher input costs (fuel/transport) alongside high interest rates. Banks, wary of compressed profit margins, are increasing their underwriting scrutiny.

The Approval Gap: As of early 2026, large banks are approving only about 68% of small business loans, compared to 82% at smaller, community-focused institutions.

Pivot to High-Cost Credit: With traditional loans taking weeks to approve, many businesses are turning to credit cards (averaging 18%–36% interest) to cover immediate fuel and supply chain gaps, significantly increasing their long-term debt burden.

2. The Surge in AR Factoring Demand

In a high-oil-price environment, factoring often shifts from a “last resort” to a strategic cash-flow tool, particularly for energy-intensive sectors.

Fuel as a Fixed, Immediate Expense: In industries like trucking and oilfield services, fuel must be paid for daily or weekly, while customers (shippers or large operators) often demand 30- to 90-day payment terms. Factoring bridges this “cash gap” without adding traditional debt to the balance sheet.

Sector-Specific Trends:

Transportation/Trucking: Factoring companies are seeing record demand. These businesses often enjoy the highest advance rates (90%–97%+) because their invoices are backed by tangible freight delivery.

Oilfield Services: As drilling activity ramps up in response to higher prices (especially in the Permian Basin), service providers are using factoring to scale quickly—buying new equipment or meeting surge payroll without waiting for 60-day payouts from major oil producers.

Manufacturing: With raw material costs rising alongside energy, manufacturers are factoring invoices to maintain liquidity reserves to buy inventory before prices hike further.

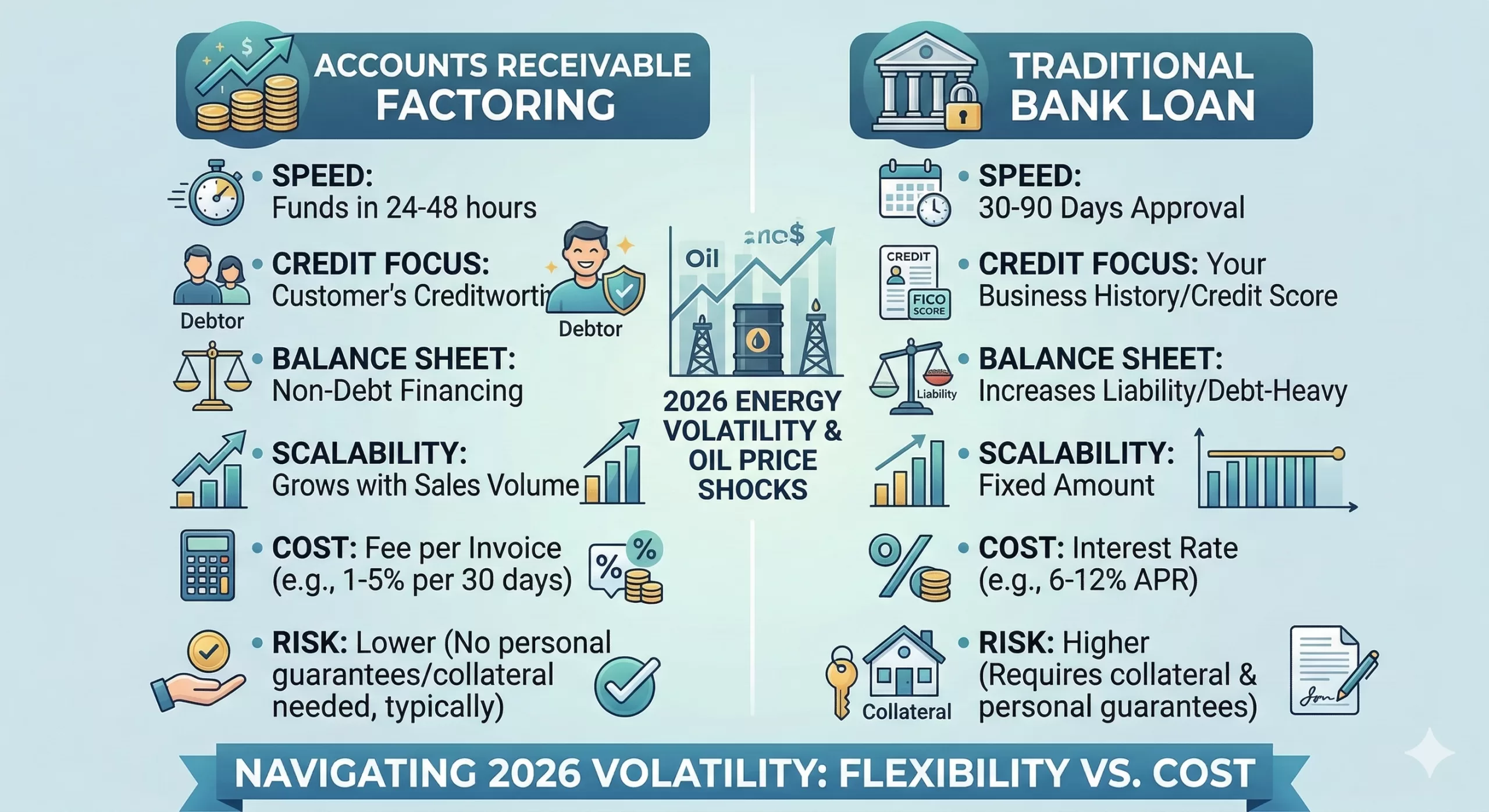

Factoring vs. Traditional Lending in 2026

Feature

Traditional Bank Loan

AR Factoring

Approval Basis

Business credit & history

Customer (Debtor) credit

Speed of Funding

2 – 7 weeks

24 – 48 hours

Debt Load

Increases liability on balance sheet

No new debt (selling an asset)

Scalability

Fixed limit

Grows with your sales volume

Cost

Lower interest (6%–12%)

Higher fees (1%–5% per 30 days)

Strategic Outlook

For the remainder of 2026, businesses that rely on “floating” cash flow are likely to prioritize speed over cost. While factoring fees are higher than bank interest, the ability to access cash within 24 hours to pay for $4.00/gallon diesel is often the difference between staying operational and grounding a fleet.

In a volatile economy where oil prices are surging and traditional banks are pulling back, choosing the right financing tool is a high-stakes decision. For B2B businesses—especially those in staffing, digital marketing, and manufacturing—the choice often comes down to the speed of Factoring versus the lower cost of a Bank Loan.

Below is a strategic comparison designed to help you evaluate which path aligns with your current cash flow needs.

Factoring vs. Bank Loans: 2026 Strategic Comparison

Feature

Accounts Receivable Factoring

Traditional Bank Loan

Speed to Cash

Ultra-Fast: Funds usually arrive within 24–48 hours after invoice setup.

Slow: Approval typically takes 30–90 days of underwriting.

Credit Focus

The Debtor: Decisions are based on your customer’s credit and payment history.

The Business: Based on your FICO score, tax returns, and years in business.

Balance Sheet

Debt-Free: It is the sale of an asset (invoices), not a liability.

Debt-Heavy: Adds a liability that can impact your debt-to-income ratio.

Scalability

Unlimited: As your sales grow, your available cash grows automatically.

Fixed: You are capped at a set amount and must re-apply to increase it.

Total Cost

Higher Fees: Usually 1%–5% per 30 days (effective APR is higher).

Lower Rates: Typically 6%–12% APR for qualified businesses.

Risk

Low: No collateral like your house or equipment is typically required.

High: Often requires a blanket lien on assets or personal guarantees.

Export to Sheets

The “Why Now?” Factor: Navigating 2026 Volatility

Pros of Factoring in This Market

Immediate Fuel/Supply Buffer: With diesel prices fluctuating, factoring gives you the cash today to buy inventory or fuel before the next price hike.

Protects Your Growth: In sectors like digital marketing or staffing, you can’t wait 60 days for a client to pay to meet your weekly payroll. Factoring ensures your team stays paid regardless of when the client cuts the check.

No “Covenant” Stress: Bank loans often come with strict “covenants” (rules about your profit margins). If high oil prices temporarily squeeze your margins, a bank might call your loan; a factor simply keeps funding your sales.

Cons to Consider

Margin Impact: If your profit margins are already thin (common in food production or distribution), the 1%–3% factoring fee could eat up a significant portion of your net income.

Customer Perception: While widely accepted today, some ultra-conservative clients might still prefer to pay you directly rather than a third-party factor.

The Bottom Line

If you have long-term stability and time to wait, a Bank Loan is cheaper. However, if you are growing rapidly or facing unpredictable costs, Factoring acts as a flexible insurance policy for your cash flow.

A government shutdown, defined as a lapse in federal appropriations, is frequently framed as a political skirmish in Washington D.C. Yet, its financial reverberations are immediately and intensely felt across the nation, striking at the heart of the U.S. economy: its small businesses. Comprising over 33 million firms and responsible for generating two-thirds of net new jobs, the small business ecosystem is the engine of American enterprise.

However, this vital sector is uniquely fragile when faced with political paralysis. A shutdown creates immediate, cascading, and disproportionate negative effects on small businesses, necessitating proactive recovery strategies from both the private and public sectors. This analysis details the mechanics of this damage—from frozen payments and suspended loans to depressed consumer spending—and outlines the essential steps small businesses must take to recover, mitigate future risk, and advocate for systemic protection.

🛑 II. Immediate and Direct Impacts of Shutdown

The moment a shutdown is triggered, the consequences for small businesses that interact directly with the federal apparatus are sudden, severe, and measurable.

The Freeze on Federal Contracts 📜

For the large segment of small businesses that operate as federal contractors, the shutdown delivers a direct financial shock:

Delayed Payments: The most critical blow is the cessation of payments, converting reliable accounts receivable into financial dead weight. Small contractors, operating on thin margins, are instantly thrust into a cash flow crisis. During the 2018-2019 shutdown, it was estimated that over 90% of federal contractor invoices went unpaid for the duration, causing thousands of small contractors to miss payroll.

Work Stoppage (Stop-Work Orders): For ongoing contracts, agencies issue stop-work orders. The business stops billing, losing revenue entirely, and must decide whether to retain specialized staff without pay or risk the loss of highly skilled talent.

Contracting Uncertainty: The entire procurement pipeline freezes. The Department of Defense (DOD) and NASA, major sources of small business contracting, halted the award of all non-essential contracts, stalling critical high-tech and defense projects.

Suspension of Critical Loans and Financial Support 💰

Small businesses rely heavily on the federal government for capital access, a lifeline that is severed during a shutdown.

SBA Loan Program Stoppage: The suspension of the SBA’s flagship loan programs—primarily the SBA 7(a) and 504 loan guarantee programs—halts guarantees. During the 2018-2019 event, the SBA stopped processing all new loan applications, estimated to have frozen approximately $2 billion in small business financing per week, crippling expansion plans nationwide.

Disaster Loan Delays: Businesses recovering from recent natural disasters also face an immediate freeze in the processing of Economic Injury Disaster Loan (EIDL) applications.

Regulatory and Licensing Paralysis 📝

For firms in regulated industries, the shutdown acts as an involuntary stop sign.

Permit and License Delays: A small craft brewery waiting for a TTB permit to launch a new product cannot proceed. The TTB’s closure in 2018-2019 created a significant backlog, delaying the opening of new breweries, wineries, and distilleries, as they could not legally bottle and sell their products.

Customs and Trade Complications: Small businesses involved in international trade can face delays in clearances and inspections required from furloughed personnel at various agencies, leading to supply chain snags.

📉 III. Indirect and Secondary Economic Impacts – Shutdown

The government shutdown rapidly produces a secondary layer of damage through channels far removed from D.C., primarily through reduced consumer spending and heightened market uncertainty.

The “Furlough Effect” on Consumer Demand 🛍️

The largest secondary impact stems from the sudden loss of income for hundreds of thousands of federal employees and non-essential contractors.

Loss of Federal Employee Income: Furloughed federal workers are placed on mandatory, unpaid leave, forcing them to drastically cut back on discretionary spending. The 35-day shutdown resulted in approximately 800,000 federal workers missing two full paychecks, translating into billions of dollars in lost spending power.

Impact on Local Economies: Businesses relying on the patronage of federal workers suffer immediately. Small restaurants and shops near federal hubs in the D.C. area, as well as businesses dependent on National Park Service tourists, reported revenue declines of 50% or more, with many having to temporarily close their doors. The lack of guaranteed back pay for contractors deepened the slump.

Financial Market and Investor Uncertainty 🏦

A shutdown injects volatility into financial and capital markets, altering the risk assessment for small businesses.

Lender Hesitation: Banks become more hesitant to underwrite new commercial loans, fearing a prolonged economic downturn. Anecdotal evidence from 2019 suggested that many community banks placed a temporary moratorium on all new small business lending until the appropriations process was resolved.

SEC Delays: Small, high-growth companies attempting to raise capital through public filings or private offerings find their efforts stalled. During the shutdown, the SEC could not process many filings, delaying the capital raises of emerging technology and biotech firms.

Data and Resource Loss 📊

Small businesses rely on accurate, timely federal data to make strategic decisions. A shutdown halts the release of critical economic intelligence.

Statistical Freeze: The cessation of data from agencies like the Bureau of Labor Statistics (BLS) and the Census Bureau leaves businesses flying blind. Key economic indicators, including reports on housing starts, retail sales, and GDP components, were delayed, forcing small business owners to make crucial expansion decisions without reliable, up-to-date data.

Loss of Free Technical Assistance: Key support networks like Small Business Development Centers (SBDCs) and the volunteer-based SCORE mentorship program often lose funding or access, cutting off cost-free assistance vital for struggling firms.

🧠 IV. Psychological and Operational Strain

The non-financial impacts inflict deep stress on owners and staff, often determining the long-term viability of the business.

Talent Exodus: Faced with prolonged unpaid leave or layoff risk, highly skilled employees often leave for stable work in the private sector, resulting in costly brain drain.

Cash Flow Crisis Management: Owners are forced into high-risk personal finance decisions. In 2019, many small business owners dependent on federal contracts revealed they had liquidated personal retirement accounts or taken out expensive home equity loans to cover their company’s payroll.

Damage to Business Reputation: The inability to fulfill contracts or meet delivery deadlines due to stop-work orders risks lost goodwill and potential exclusion from future partnership opportunities.

🛠️ V. Strategies for Small Business Recovery and Mitigation – Shutdown

The recovery phase demands proactive management, aggressive financial triage, and a fundamental reassessment of business risk.

5.1 Immediate Financial Triage: Stabilizing the Vessel

The 90-Day Cash Flow Plan (The Survival Budget): Create a hyper-detailed projection, categorizing expenses as Mission-Critical, Negotiable, or Eliminatable.

Aggressive Negotiation with Creditors: Proactively contact commercial lenders to request interest-only payments or short-term principal forbearance. In 2019, many banks, anticipating the back pay to federal workers, were quick to offer forbearance options, but contractors needed to be aggressive in requesting similar terms.

Accessing Local Capital: Immediately explore bridge loan options from local Credit Unions and CDFIs.

5.2 Re-Engaging Federal Systems and Documentation

Upon reopening, businesses must move swiftly and meticulously:

Prioritizing Re-activation: Immediately contact the Contracting Officer (CO) for a Written Resumption Order before restarting work. Be prepared to immediately re-file or re-activate stalled SBA loan applications.

Detailed Documentation: Meticulously document all incurred costs related to the shutdown. This documentation is crucial for negotiating future claims for Termination for Convenience costs.

5.3 Diversification and Risk Management: The Long-Term Shield

The most effective strategy is to ensure the business is never again so vulnerable to political instability.

Client Base Diversification: Actively work to cap federal revenue reliance (e.g., at 60-70% of total revenue) and pursue contracts with state and local governments or the private sector.

Building a Shutdown-Proof Emergency Fund: Adopt the financial discipline to build a dedicated cash reserve equal to 3 to 6 months of operational expenses. This reserve is strictly for maintaining payroll and core utilities during a non-economic disruption.

Operational Agility: Implement cross-training programs to utilize staff for internal projects if a stop-work order is issued, retaining skilled talent while maintaining some level of productivity.

5.4 Advocacy and Systemic Change

Small business owners must leverage their collective voice to push for legislative reform.

The “Wall Off” Principle: Advocate for legislation that grants Excepted Status to critical, non-political economic functions, most importantly the SBA Loan Guarantee Processing and the Payment of Existing, Obligated Federal Contractors. Shielding these functions from the appropriations fight is essential to maintaining the stability of the small business economy.

VI. Conclusion

The resilience of the small business sector is severely tested by government shutdowns. These events are not merely political theatre; they are systemic economic disruptions that destroy cash flow, erode consumer confidence, and inflict severe psychological stress on owners and employees. The 35-day shutdown of 2018-2019 provided undeniable proof that the small business community bears a disproportionate burden of political gridlock.

While recovery demands aggressive financial triage and meticulous documentation, the long-term solution lies in diversification and structural preparedness. Policymakers must recognize that failure to fund critical economic functions, even temporarily, causes an outsized and destructive ripple effect. Ensuring the continuity of SBA lending and contractor payments must be treated as a matter of essential economic stability, insulating the national engine of job creation from political gridlock.

More Than a Headline: 5 Ways a Government Shutdown Silently Cripples Main Street America

1.0 Introduction: Beyond the Beltway Drama

When the federal government shuts down, the news cycle often frames it as a distant political battle confined to Washington D.C. Yet, its financial reverberations are immediately and intensely felt across the nation, striking directly at the heart of the U.S. economy: its small businesses, the very engine of American enterprise responsible for creating two-thirds of all net new jobs.

This vital sector is uniquely and disproportionately vulnerable to the consequences of political paralysis. A shutdown creates an immediate cascade of damage that extends far beyond federal employees, impacting entrepreneurs and local economies nationwide. Here are the five most significant and surprising ways this political gridlock cripples small businesses, proving the damage is far more widespread than a headline can capture.

2.0 The Shutdown’s Ripple Effect: 5 Surprising Impacts on Small Business

2.1 Takeaway 1: The Instant Cash Flow Apocalypse

For the thousands of small businesses operating as federal contractors, a government shutdown triggers an immediate financial shock. During the 35-day shutdown of 2018-2019, an estimated 90% of federal contractor invoices went unpaid. This instantly converts reliable accounts receivable into dead weight, thrusting companies with thin margins into a severe cash flow crisis. Revenue doesn’t just get delayed—it stops entirely, as agencies issue formal “stop-work orders.” Major sources of small business contracting, like the Department of Defense (DOD) and NASA, halt the award of new projects, freezing the entire procurement pipeline and forcing owners into devastating choices, such as whether to miss payroll or attempt to retain highly skilled talent without any pay.

2.2 Takeaway 2: The $2 Billion Weekly Freeze on Ambition

A shutdown severs a critical lifeline for small businesses seeking to grow: access to capital. The Small Business Administration (SBA) is forced to suspend its flagship 7(a) and 504 loan guarantee programs. During the 2018-2019 shutdown, this stoppage was estimated to have frozen approximately $2 billion in small business financing per week. This freeze also extends to Economic Injury Disaster Loan (EIDL) applications, harming businesses already reeling from natural disasters and compounding their crisis. This number represents more than just money on hold; it signifies crippled expansion plans, delayed hiring, and stalled innovation for entrepreneurs across the country who suddenly find their ambitions on indefinite hold.

2.3 Takeaway 3: The Economic Paralysis Spreads Far From D.C.

The financial damage quickly spreads through the “Furlough Effect.” When approximately 800,000 federal workers missed two full paychecks during the extended shutdown, they were forced to drastically cut back on consumer spending. The impact on local economies was immediate and severe. Small restaurants and shops near federal hubs and businesses dependent on National Park Service tourists reported revenue declines of 50% or more. This secondary impact demonstrates how deeply intertwined Main Street is with government operations, even for businesses with no direct federal contracts.

2.4 Takeaway 4: It Puts New Ventures on Indefinite Hold

The impact extends beyond money, creating a regulatory and licensing paralysis that acts as an involuntary stop sign for new ventures. Consider a small craft brewery that has developed a new product but is waiting on a permit from the Alcohol and Tobacco Tax and Trade Bureau (TTB). When the government shuts down, the TTB closes. The brewery cannot legally bottle and sell its new product, killing entrepreneurial momentum. This specific example shows how a shutdown can delay the opening of new breweries, wineries, and distilleries entirely unrelated to government contracting, freezing the very spirit of enterprise.

2.5 Takeaway 5: The Hidden Human Cost for Owners and Employees

Beyond the financial statements, a shutdown inflicts deep psychological and operational strains. The uncertainty can trigger a “talent exodus,” as highly skilled employees leave for more stable private-sector work rather than risk prolonged layoffs. At the same time, owners are forced to take extreme personal risks to keep their businesses afloat. During the 2019 shutdown, many small business owners dependent on federal contracts revealed they had liquidated personal retirement accounts or taken out home equity loans simply to cover their company’s payroll. Finally, the inability to fulfill contracts due to stop-work orders causes lasting damage to a business’s reputation, risking lost goodwill and exclusion from future opportunities.

3.0 Conclusion: From Crisis to Resilience

Government shutdowns are not political theatre; they are systemic economic disruptions that inflict deep, lasting, and disproportionate damage on the nation’s primary job creators. While the immediate aftermath requires financial triage, the long-term solution for businesses lies in strategic preparation, including diversifying their client base and building robust emergency funds.

The 35-day shutdown of 2018-2019 provided undeniable proof that the small business community bears a disproportionate burden of political gridlock.

This repeated cycle of crisis demands a systemic solution, forcing policymakers to answer a fundamental question. It underscores the urgent need to protect the bedrock of the American economy from political instability. How can we insulate essential economic functions, like SBA lending and contractor payments, from future political gridlock to protect the engine of our economy?

The Economic Impact of Government Shutdowns on U.S. Small Businesses

Executive Summary

A government shutdown, or a lapse in federal appropriations, inflicts immediate, severe, and disproportionate harm on the U.S. small business sector—an ecosystem of over 33 million firms responsible for generating two-thirds of net new jobs. The financial repercussions extend far beyond political centers, creating a cascade of negative effects that destabilize this vital engine of the American economy.

The 35-day shutdown of 2018-2019 serves as definitive proof of this vulnerability, where an estimated $2 billion in small business financing was frozen per week due to the suspension of Small Business Administration (SBA) loan processing. During this period, over 90% of federal contractor invoices went unpaid, thrusting thousands of firms into a cash flow crisis. The shutdown’s impact is multifaceted, manifesting as direct financial shocks, indirect economic downturns, and severe operational strains.

Key Impacts Include:

Direct Financial Disruption: Federal contractors face an immediate freeze on payments and stop-work orders. Access to critical capital through SBA loan programs (7(a), 504) is severed, and regulatory processes, such as TTB permits for breweries and wineries, are halted.

Secondary Economic Damage: The furloughing of federal workers—approximately 800,000 during the 2018-2019 event—triggers a sharp decline in consumer spending, with local businesses reporting revenue drops of 50% or more. Market uncertainty causes banks to hesitate on lending and stalls capital-raising efforts at the SEC.

Operational and Psychological Strain: The crisis forces owners into high-risk personal financial decisions, such as liquidating retirement accounts to make payroll. It also triggers an exodus of skilled talent and damages business reputations.

Recovery requires immediate financial triage, proactive creditor negotiation, and meticulous documentation for future claims. However, long-term survival hinges on strategic diversification to reduce reliance on federal revenue (capping it at 60-70%) and building a robust emergency cash reserve of 3-6 months. Ultimately, the analysis advocates for systemic reform through legislation that would “wall off” critical economic functions, such as SBA loan processing and contractor payments, from political appropriations battles to ensure national economic stability.

——————————————————————————–

1. The Anatomy of a Shutdown’s Impact

Government shutdowns are systemic economic disruptions that deliver measurable damage through direct, indirect, and operational channels. The small business sector is uniquely fragile and bears a disproportionate burden of the consequences of political gridlock.

1.1. Direct Financial and Operational Shocks

The most immediate consequences are felt by businesses that interact directly with the federal government for contracts, financing, or regulatory approval.

Impact Area

Mechanism of Harm

2018-2019 Shutdown Case Data

Freeze on Federal Contracts

Delayed Payments: Reliable accounts receivable become financial dead weight, creating an instant cash flow crisis for contractors operating on thin margins. <br> Stop-Work Orders: Agencies halt ongoing contract work, stopping all revenue streams and forcing difficult staffing decisions.

Over 90% of federal contractor invoices went unpaid, causing thousands of small contractors to miss payroll. The DOD and NASA halted all non-essential contract awards.

Suspension of Financial Support

SBA Loan Stoppage: The suspension of the SBA’s 7(a) and 504 loan guarantee programs cuts off a critical lifeline for capital access. <br> Disaster Loan Delays: The processing of Economic Injury Disaster Loan (EIDL) applications is frozen.

The SBA stopped all new loan processing, freezing an estimated $2 billion in small business financing per week, crippling nationwide expansion plans.

Regulatory Paralysis

Permit and License Delays: Businesses in regulated industries cannot proceed with new products or operations. <br> Trade Complications: Furloughed personnel cause delays in customs clearances and inspections, creating supply chain disruptions.

The closure of the Alcohol and Tobacco Tax and Trade Bureau (TTB) created a significant backlog, delaying the opening of new breweries, wineries, and distilleries.

1.2. Indirect Economic Reverberations

The shutdown’s impact quickly radiates outward, depressing the broader economy through reduced spending, market volatility, and a loss of critical data.

The “Furlough Effect” on Consumer Demand: The furloughing of federal workers and non-essential contractors removes billions of dollars from the economy.

During the 35-day shutdown, approximately 800,000 federal workers missed two full paychecks.

This led to a drastic cutback in discretionary spending, causing small businesses near federal hubs and National Parks to report revenue declines of 50% or more.

Financial Market and Investor Uncertainty: Political paralysis creates economic volatility, making lenders more risk-averse.

Anecdotal evidence from 2019 suggests many community banks placed a temporary moratorium on new small business lending.

The Securities and Exchange Commission (SEC) could not process many filings, delaying capital raises for emerging technology and biotech firms.

Loss of Data and Resources: The halt in the release of federal data forces businesses to make strategic decisions without critical intelligence.

Agencies like the Bureau of Labor Statistics (BLS) and the Census Bureau delayed key economic indicators on retail sales, housing starts, and GDP components.

Federally funded support networks like Small Business Development Centers (SBDCs) and the SCORE mentorship program lost access or funding, cutting off free assistance.

1.3. Psychological and Operational Strain

Beyond the financial metrics, a shutdown imposes severe non-financial burdens that can determine a business’s long-term viability.

Talent Exodus: Highly skilled employees, facing layoff risks or unpaid leave, often seek more stable employment in the private sector, resulting in a costly “brain drain.”

Cash Flow Crisis Management: Owners are forced into high-risk personal financial decisions. During the 2019 shutdown, many small business owners reported liquidating personal retirement accounts or taking out expensive home equity loans to cover company payroll.

Damage to Business Reputation: Inability to fulfill contracts due to stop-work orders can damage goodwill with partners and risk exclusion from future opportunities.

2. A Framework for Recovery and Resilience

Recovery from a government shutdown requires a combination of immediate financial triage and long-term strategic adjustments to mitigate future risk.

2.1. Immediate Recovery Actions

Once government operations resume, small businesses must act swiftly and methodically to stabilize their finances and restart operations.

Financial Triage:

The 90-Day Cash Flow Plan: Develop a detailed “survival budget” that categorizes all expenses as Mission-Critical, Negotiable, or Eliminatable.

Aggressive Creditor Negotiation: Proactively contact lenders to request short-term forbearance or interest-only payments.

Access Local Capital: Explore bridge loan options from local Credit Unions and Community Development Financial Institutions (CDFIs).

Re-Engaging Federal Systems:

Prioritize Re-activation: Immediately contact the relevant Contracting Officer (CO) to obtain a Written Resumption Order before restarting any work.

Document Everything: Meticulously document all shutdown-related costs. This is crucial for negotiating any future claims for “Termination for Convenience” costs.

2.2. Long-Term Mitigation and Risk Management

The most effective strategy is to build a business model that is fundamentally less vulnerable to political instability.

Client Base Diversification: Actively work to reduce reliance on federal contracts by pursuing clients in the private sector or at the state and local government levels. The recommended target is to cap federal revenue reliance at 60-70% of total revenue.

Shutdown-Proof Emergency Fund: Build and maintain a dedicated cash reserve equivalent to 3 to 6 months of essential operational expenses (payroll, core utilities). This fund should be reserved strictly for non-economic disruptions.

Enhance Operational Agility: Implement staff cross-training programs. This allows employees to be repurposed for internal projects during a stop-work order, retaining skilled talent while maintaining productivity.

3. Proposed Systemic Reforms: The “Wall Off” Principle

To prevent future economic damage, small business owners are encouraged to advocate for legislative reforms that insulate core economic functions from political gridlock. The central proposal is the “Wall Off” principle, which calls for legislation that grants “Excepted Status” to critical, non-political economic functions. This would ensure their continuity during a lapse in appropriations.

The two most critical functions to be shielded are:

SBA Loan Guarantee Processing: To maintain the flow of capital to small businesses.

Payment of Existing, Obligated Federal Contractors: To prevent immediate cash flow crises for firms that have already performed work.

Treating the continuity of these functions as a matter of essential economic stability is paramount to protecting the national engine of job creation.

Introduction: Why We’re All Missing the Point About AI

The conversation around AI is dominated by extremes. On one side, there are anxieties of mass job loss and uncontrollable superintelligence. On the other, there are utopian dreams of automated abundance. But this focus on AI’s “intelligence” is a distraction from its real, more profound impact. We are so busy asking if the machine is smart enough to replace us that we’re failing to see how it’s already changing the entire system we operate in.

This article distills five counter-intuitive truths from Sangeet Paul Choudary’s book, Reshuffle, to offer a new framework for understanding AI’s true power. These insights will shift your perspective from the tool to the system, revealing where the real opportunities and threats lie.

——————————————————————————–

1. It’s Not About Intelligence, It’s About the System

We mistakenly judge AI by how human-like it seems, a phenomenon Choudary calls the “intelligence distraction.” We debate its creativity or consciousness while overlooking the one thing that truly matters: its effect on the systems it enters.

Consider the parable of Singapore’s second COVID-19 wave in 2021. The nation was a global model of pandemic response, armed with precise tools like virus-tight borders and obsessive contact tracing. Yet, it was defeated not by a technological failure, but by systemic blind spots. An outbreak was traced to hostesses—colloquially known as “butterflies”—working illegally in discreet KTV lounges after entering the country on a “Familial Ties Lane” visa. With contact tracing ignored in the venues and a clientele of well-heeled men unwilling to risk their reputations by coming forward, the nation’s high-tech system was rendered useless. Singapore’s precise tools were no match for the hidden logic of the system.

This illustrates a crucial lesson: the real story of AI is not in the technology itself, but in the system within which it is deployed. Our focus should not be on the machine’s capabilities in isolation.

Instead of asking How smart is the machine?, we should shift our frame to ask What do our systems look like once they adopt this new logic of the machine?

——————————————————————————–

2. AI’s Real Superpower is Coordination, Not Automation

We often mistake AI’s impact for simple automation—making individual parts of a process faster. But its most transformative power lies in coordination: making all the parts work together in new and more reliable ways.

The shipping container provides a powerful analogy. Its revolution wasn’t just faster loading at ports (automation). Its true impact came from imposing a new, reliable logic of coordination across global trade. Innovations by entrepreneurs like Malcolm McLean, such as the single bill of lading that unified contracts across trucks, trains, and ships, and the push for standardization during the Vietnam War, were deliberate efforts to overcome systemic inertia. By standardizing how goods were moved, the container restructured entire industries, enabled just-in-time manufacturing, and redrew the map of economic power.

AI is the shipping container for knowledge work. Its most profound impact comes from its ability to coordinate complex activities and align fragmented players in ways previously impossible—what the book calls “coordination without consensus.” It can create a shared understanding from unstructured data, allowing teams, organizations, and even entire ecosystems to move in sync without rigid, top-down control.

This reveals a self-reinforcing flywheel of economic growth: better coordination drives deeper specialization, as companies can rely on external partners. This specialization leads to further fragmentation of industries, which in turn demands even more powerful forms of coordination to manage the complexity. AI is the engine of this modern flywheel.

The real leverage in connected systems doesn’t come from optimizing individual components, but from coordinating them.

This new power of system-level coordination is precisely why the old, task-focused view of job security is no longer sufficient.

——————————————————————————–

3. The “Someone Using AI Will Take Your Job” Trope is a Trap

The popular refrain, “AI won’t take your job, but someone using AI will,” is a dangerously outdated framework. It encourages a narrow, task-centric view of work that misses the bigger picture.

The book uses the Maginot Line as an analogy. In the 1930s, France built a chain of impenetrable fortresses to defend against a German invasion, perfecting its defense for the trench warfare of World War I. But Germany had changed the entire system of combat. The Blitzkrieg integrated mechanized infantry, tank divisions, and dive bombers, all of which were coordinated through two-way radio communication, to simply bypass the useless fortifications. The key wasn’t better weapons; it was a new coordination technology that changed the system of warfare itself.

Focusing on using AI to get better at your current tasks is like reinforcing the Maginot Line. The real threat isn’t that someone will perform your tasks better; it’s that AI is unbundling and rebundling the entire system of work. When the system changes, the economic logic that holds a job together can collapse, rendering the role obsolete even if the individual tasks remain.

When the system itself changes due to the effects of AI, the logic of the job can collapse, even if the underlying tasks remain intact.

——————————————————————————–

4. Stop Chasing Skills. Start Hunting for Constraints.

In a world where AI makes knowledge and technical execution abundant, simply “reskilling” is a losing game. It puts you in a constant race to learn the next task that AI can’t yet perform. A more strategic approach is to hunt for the new constraints that emerge in the system.

Take the surprising example of the sommelier. When information about wine became widely available online, the sommelier’s role as an information provider should have disappeared. Instead, their value increased. Why? Because they shifted from providing information to resolving new constraints for diners. With endless choice came new problems: the risk of making a bad selection and the desire for a curated, confident experience. The sommelier’s value migrated to managing risk. Furthermore, as one form of scarcity disappeared (information), they helped manufacture a new one: certified taste, created through elite credentialing bodies like the Court of Master Sommeliers.

The core lesson is that value flows to whoever can solve the new problems that appear when old ones are eliminated by technology. The key to staying relevant is not to accumulate more skills, but to identify and rebundle your work around solving the system’s new constraints, such as managing risk, navigating ambiguity, and coordinating complexity.

The assumption baked into most reskilling narratives is that skills are a scarce resource. But in reality, skills are only valuable in relation to the constraint they resolve.

——————————————————————————–

5. Using AI as a “Tool” Is a Path to Irrelevance

There is a crucial distinction between using AI as a “tool” versus using it as an “engine.” Using AI as a tool simply optimizes existing processes. It makes you faster or more efficient at playing the same old game, leading to short-term gains but no lasting advantage.

The book contrasts the rise of TikTok with early social networks to illustrate this. Platforms like Facebook and Instagram used AI as a tool to enhance their existing social-graph model, improving feed ranking and photo tagging. Their competitive logic remained centered on who you knew. TikTok, however, used AI as its core engine. It built an entirely new model based on a behavior graph—what you watch determines what you see. This was enabled by a brilliant positive constraint: the initial 60-second video limit forced a massive volume of rapid-fire user interactions, generating the precise data needed to train its behavior-graph engine at a speed competitors couldn’t match. This new logic made the old rules of competition irrelevant.

Companies that fall into the “tool integration trap” by becoming dependent on third-party AI to optimize tasks risk outsourcing their competitive advantage. The strategic choice is to move beyond simply applying AI and instead rebuild your core operating model around it.

A company that utilizes AI as a tool may improve efficiency, but it still competes on the same basis. A company that treats AI as an engine unlocks entirely new levels of performance and changes the basis of how it competes.

——————————————————————————–

Conclusion: Reshuffle or Be Reshuffled

To truly understand AI, we must shift our focus from its intelligence to its systemic impact. The five truths reveal a clear pattern: AI’s power isn’t in automating tasks but in reconfiguring the systems of work, competition, and value creation. It’s a force for coordination, a reshaper of constraints, and an engine for new business models.

True advantage comes not from reacting to AI with better skills or faster tools, but from actively using it to reshape the systems around us. It requires moving from a task-level view to a systems-level perspective.

The question is no longer “How will AI change my job?” but “What new systems can I help build with it?” What will your answer be?

Upward Revision of Q2 GDP: The US economy saw a stronger rebound in the second quarter than initially estimated. The Bureau of Economic Analysis revised its Gross Domestic Product (GDP) figure for April through June to an annual rate of 3.3%, up from the previous estimate of 3.0%. The growth was primarily driven by a sharp drop in imports and an increase in consumer spending. This follows a 0.5% contraction in the first quarter of the year.

Consumer Confidence Falls:The Conference Board’s Consumer Confidence Index dropped slightly in August, marking a 1.3-point decrease from July. Consumers’ assessments of both current business and labor market conditions, as well as their short-term outlook, worsened. Concerns about higher prices and inflation, with tariffs being a notable contributing factor, were cited by consumers in their responses.

Tariffs and Trade Policy: The ongoing US trade policy and the imposition of tariffs continue to be a dominant theme in economic news. The recent 50% tariff on Indian goods, in particular, has created uncertainty and is weighing on market sentiment. The unpredictability of these policies has left businesses unsettled and cautious about investments and hiring.

News for Business Owners (Big and Small)

Small Business Lending: The Kansas City Federal Reserve reported an increase in demand for small business loans for the first time since the first quarter of 2022. However, the report also noted that fewer loan applications were approved, indicating tightening credit standards.

SBA Reforms: The Small Business Administration (SBA) has reinstated fees for its 7(a) loan program, which were previously waived. The SBA administrator also announced the relocation of several regional offices to new locations aimed at better serving the small business community.

Corporate Transparency Act: Enforcement of the Corporate Transparency Act’s beneficial ownership reporting requirement has been suspended, with the US Treasury Department making an announcement to that effect. This provides a reprieve for many US citizens and domestic reporting companies.

AI Adoption by Small Businesses: A recent survey by Goldman Sachs found that 68% of small businesses are now using artificial intelligence (AI), a significant jump from the previous year. The survey indicates that business owners are using AI to enhance their workforce rather than replace jobs.

“Choose Your Enemies Wisely” by Patrick Bet-David, with Greg Dinkin, presents a radical and emotionally-driven approach to business planning, challenging conventional wisdom that advocates for separating emotion from logic in professional endeavors. Bet-David argues that wisely chosen “enemies”—whether people, ideologies, or personal shortcomings—serve as a potent fuel for relentless drive and sustained success. The book outlines a 12-Building Block framework that integrates both emotional and logical elements, emphasizing that true audacity and long-term achievement stem from a deeply personal “why” that is then channeled into a methodical “how.”

The core message is that success is not merely about having a plan, but about having a plan fueled by emotion, specifically the desire to overcome perceived adversaries or personal limitations. This method, born from Bet-David’s own rags-to-riches story and extensive experience, aims to transform shame, anger, and disappointment into the impetus for extraordinary results in both business and life.

II. Main Themes and Key Ideas/Facts – Choose Your Enemies Wisely

A. The Power of Enemies as Fuel (Emotional Core)

Enemies as a Catalyst for Transformation: Bet-David asserts that “the most critical element for success in business planning is choosing your enemies wisely.” He views challenges, haters, betrayals, and even personal insecurities as sources of “fuel” that ignite the power to transform.

Quote: “What if I told you that these so-called enemies could become your greatest source of fuel? What if you could turn shame, guilt, anger, disappointment, and heartbreak into the fire that propels you toward your wildest dreams?”

The “Why to Win” vs. “How to Win”: The book shifts the focus from merely finding how to win to identifying a powerful why to win. This “why” often originates from past humiliations, manipulations, or a desire to prove doubters wrong.

Quote: “Sometimes we spend so much time trying to find how to win at life that we miss the entire point. Maybe you need to look for why to win in life. Did somebody humiliate you? Did somebody manipulate you? Is there a teacher or family member who made you feel ashamed? We’re all driven in different ways, but the right enemy can drive you in ways an ally never can.”

Embracing Emotion in Business: Contrary to common advice, Bet-David advocates for integrating emotion into business. He highlights successful figures like Elon Musk, Andy Grove, and Steve Jobs as examples of leaders who embraced and channeled their emotions strategically.

Quote: “When ‘experts’ say that you shouldn’t get emotional in business, I ask what kind of success they’ve had… Most of the time, they don’t have any business success to speak of. Maybe nobody offended them in life or maybe they were taught to keep that emotion bottled up and not bring it into business. No matter the reason, when I see that they don’t have enemies to fuel them, I realize that I am the privileged one.”

Distinguishing Emotion: The book differentiates between negative and productive emotion:

Emotion is not: impulsive, irrational, melodramatic, temperamental, or hot-blooded.

Emotion is: passionate, obsessed, maniacal, relentless, powerful, and purposeful.

Graduating to New Enemies: Success requires continuously identifying and “graduating” to new enemies to avoid complacency. Once an enemy is defeated or their purpose served, a new, more challenging adversary should be identified to maintain drive. Tom Brady’s career is used as a prime example of this continuous enemy selection.

Quote: “The process never ends, which is why you must keep graduating to new enemies. When most people reach a certain level of success, they flatline. Without new enemies to drive them, not only do they get complacent, but they also stop solidifying each building block.”

Choosing Enemies Wisely: The selection of enemies is crucial. Unworthy enemies (e.g., those you’ve surpassed, jealous relatives, toxic individuals) can drain energy and lead to grudges, which are counterproductive. The most powerful enemies are often those whose vision and accomplishments are greater than yours, driving you to elevate your own game.

Quote: “The minute you get successful, people will be gunning for you… These are annoyances that don’t deserve to be dignified with the word ‘enemy.'”

Quote: “The most powerful enemy is people who are beating you because their vision and accomplishments are greater than yours.”

B. The 12 Building Blocks: Integrating Logic and Emotion

The book’s central framework comprises 12 interconnected building blocks, pairing an emotional concept with a logical one. To be part of “the audacious few,” all 12 blocks must be completed.

Enemy (Emotional) & Competition (Logical): – Choose Your Enemies Wisely

Enemy: Identifies the emotional trigger – who or what “pisses you off” or makes you want to “prove them wrong.” Examples include doubters, bullies, or societal injustices.

Competition: A methodical analysis of direct and indirect competitors, including market trends, potential disruptors (like AI), and non-obvious threats (e.g., interest rates, shifts in public perception). The strategy includes deep research and understanding competitor weaknesses to gain an edge.

Fact: Tom Brady’s consistent success is attributed to his ability to continually choose new enemies (e.g., quarterbacks drafted before him, Bill Belichick’s perceived doubt, Max Kellerman’s criticism, Michael Jordan’s GOAT status).

Will (Emotional) & Skill (Logical): – Choose Your Enemies Wisely

Will: The “indomitable spirit” or “determination” to succeed, often triggered by fear of failure or a powerful sense of purpose. It’s about converting “wantpower” to “willpower.”

Quote: “Will is emotional. It’s wanting something in a way that you can’t describe.”

Quote: “When you have will, you don’t need motivation.”

Skill: The practical knowledge, abilities, and training required to execute one’s will. This involves identifying personal and team skill gaps, continuous learning (e.g., reading books, attending workshops), and strategic recruitment/delegation.

Quote: “Without these skills, all the will in the world will be wasted.”

Fact: Neil deGrasse Tyson’s indicators of success include ambition and capacity to recover from failure (will) alongside grades and social skills (skill). The Performance vs. Trust Matrix is introduced, emphasizing investing in high-will/high-trust individuals, even if they initially lack certain skills.

Mission (Emotional) & Plan (Logical): – Choose Your Enemies Wisely

Mission: The overarching, ongoing purpose that inspires and creates endurance. It answers questions like “What cause are you fighting for?” and “What injustice are you correcting?” and has no completion date.

Quote: “Having a mission creates endurance. It allows you to tolerate the pain you’re going to go through.”

Quote: “My mission was, and still is, to use entrepreneurship to solve the world’s problems and teach capitalism because the fate of the world depends on it.”

Plan: A logical, actionable roadmap derived from the mission, including SWOT analysis (Strengths, Weaknesses, Opportunities, Threats), anticipating crises (3-5 moves ahead thinking), and calendaring key activities.

Fact: George Will’s speech on the state of America was a pivotal moment for Bet-David in defining his personal and business mission. The importance of the word “because” is highlighted in making mission statements more powerful.

Dreams (Emotional) & Systems (Logical): – Choose Your Enemies Wisely

Dreams: Audacious, inspiring visions of future achievements, often personal, with deadlines and rewards. These spark emotion and make the “impossible” seem possible.

Quote: “Every great achievement starts with a thought, and every audacious goal begins with a dream.”

Quote: “Goals are the specific outcomes we aim for on our way to achieving our dreams. Dreams direct our energy; goals take that direction and create a laser focus.”

Systems: Duplicatable, efficient processes and structures that turn dreams into reality. This includes automation, data analysis, and strategic delegation to “buy back time.”

Quote: “I think of systems as dream-making machines.”

Quote: “You do not rise to the level of your goals. You fall to the level of your systems.” (James Clear, Atomic Habits)

Fact: Bet-David’s childhood dream of owning the New York Yankees (a crazy dream that became a reality) is used as an example. The Jiffy Lube oil change sticker is presented as a brilliant systematic reminder that impacts consumer behavior.

Culture (Emotional) & Team (Logical): – Choose Your Enemies Wisely

Culture: The shared behaviors, rituals, and traditions that define an organization’s identity and inspire loyalty. It’s “what people do when no one is watching” and is highly contagious.

Quote: “Culture eats strategy for breakfast.” (Peter Drucker)

Quote: “Culture is having people wanting to run through walls for you and your organization.”

Team: The strategic selection and development of individuals, from an inner circle to employees and vendors, emphasizing trust and placing people in roles where they thrive. The “rock-star principle” (paying significantly more for top talent) is discussed.

Fact: Japanese soccer fans cleaning stadiums after a World Cup win exemplifies culture as ingrained behavior. Elon Musk’s “hardcore” culture shift at Twitter is a modern example. The Netflix “rock-star principle” is advocated for hiring.

Vision (Emotional) & Capital (Logical):

Vision: A transcendent, long-term outlook that extends beyond personal dreams, aiming to create a lasting impact on the world and outlast the founder. It’s stubborn on core beliefs but flexible on details.

Quote: “Vision is what makes people never want to stop… It’s transcendent and will outlast even you.”

Quote: “Be stubborn on vision but flexible on details.” (Jeff Bezos)

Capital: The practical means (money, partnerships) to fund the vision. This involves a clear, concise elevator pitch, a crisp pitch deck, and a compelling narrative that articulates the “why” to potential investors, partners, and employees.

Fact: The USS John C. Stennis, a nuclear-powered aircraft carrier that can operate for 26 years without refueling, is a metaphor for a strong, self-sustaining vision. Domino’s and Papa John’s are compared on their vision of speed vs. quality. Elon Musk’s emotional response to Neil Armstrong’s criticism of commercial space flight highlights the deep emotional connection to his vision.

C. The Process and Implementation

Look Back Before Moving Forward: A critical initial step is to thoroughly review the past year, acknowledging failures, identifying “leaks” (weaknesses/distractions), and understanding personal patterns. This prevents repeating mistakes.

Quote: “The most important data for you is found in the year that just passed.”

Quote: “Those who cannot remember the past are condemned to repeat it.” (George Santayana)

Duration, Depth, and Magic: Successful ventures (and marriages) need more than just “duration” (staying in business); they require “depth” (passion, impact, financial growth) and “magic” (a feeling of meaning, excitement, and being part of something greater).

Quote: “Without magic, both a marriage and a business will fail.”

The “Audacious Few”: This approach is for “visionaries, dreamers, and psycho-competitors” willing to be “extreme” and honest about their blind spots, refusing shortcuts.

Rolling Out the Plan: After completing the 12 blocks, the plan must be effectively “rolled out” to all stakeholders (team, family, investors). This involves rehearsal, strategic presentations, setting KPIs, agreeing on incentives, calendaring, and creating visual reminders. The goal is to “enroll” people, not just inform them.

Continuous Improvement: The business plan is a “living document” that requires quarterly review, course-correction, and adaptation. Complacency is the enemy of sustained success, necessitating continuous identification of new enemies and refinement of all building blocks.

Quote: “A static business plan is a losing business plan.”

III. Conclusion

“Choose Your Enemies Wisely” is a manifesto for the ambitious, presenting a counter-intuitive yet deeply personal and pragmatic framework for achieving extraordinary success. It challenges leaders to delve into their deepest emotions and past experiences, transforming them into a powerful, sustainable drive. By meticulously integrating this emotional “why” with logical “how-to” strategies across 12 core building blocks, Bet-David promises a path to not only achieve audacious goals but also to build a business and a life of lasting impact and fulfillment. The book emphasizes that while talent and hard work are necessary, it is the strategic harnessing of emotion, particularly the drive to overcome “enemies,” that ultimately propels individuals and organizations to unprecedented heights.

A summary of the most interesting article on small businesses published in the previous 24 hours including cautious optimism.

A key article from the U.S. Chamber of Commerce highlights a mood of cautious optimism among small business owners, even as concerns about tariffs and hiring linger. The report, which includes data from a recent survey, indicates that a majority of small business owners are optimistic about their future and plan to grow their businesses. However, this optimism is tempered by significant concerns.

Here are some key takeaways:

Tariffs: Tariffs are a major concern for many small businesses, with 36% currently feeling their impact and 38% expecting to be negatively affected.

Hiring: While 45% of small businesses plan to increase their workforce, this is slightly lower than a previous survey, suggesting some hesitation.

Financing: A majority of small business owners (51%) believe that interest rates are too high to afford a loan.

Government Policy: Small business owners feel they are not a priority in Washington, D.C., with 81% expressing this sentiment. There is a strong desire for more tax certainty and for provisions like R&D expensing to be made permanent.

In essence, small businesses are feeling good about their own prospects but are worried about external economic factors and a lack of support from policymakers.

The phrase “cautiously optimistic” has been a staple of American economic commentary for decades, a linguistic barometer for a nation grappling with a complex and ever-shifting fiscal landscape. Far from being a simple platitude, this seemingly oxymoronic expression is a deliberate rhetorical tool used to convey a delicate balance of hope and pragmatism. It signifies a period of positive momentum that is nonetheless shadowed by lingering risks, demanding vigilance from policymakers, investors, and the public alike. To trace the history of this phrase is to chart the major inflection points of the US economy, from the post-war booms to the digital age, and to understand how a single turn of phrase can both reflect and shape public perception.

The origins of this economic cliché can be traced back to the early 20th century, a time when economic analysis was becoming a more formalized discipline. As far back as 1924, business statistician Roger W. Babson, a pioneering figure in investment advisory, used similar language to describe the economic outlook. In an article highlighted by the NKyTribune, Babson predicted 1924 would be a “fairly good” business period but cautioned against the dangers of excessive prosperity. His philosophy was rooted in a Newtonian “action and reaction” theory of economic cycles, which held that every boom would inevitably lead to a bust. Babson’s “cautious optimism” was not a gut feeling but a statistical conclusion, born from a scientific understanding of historical economic data. He saw the need for moderation, a middle ground between the “hot weather” of a boom and the “depression” of a bust. This early use of the phrase set the precedent for its future application: a measured, data-driven assessment that acknowledged positive signs while remaining acutely aware of inherent cyclical risks.

This delicate balancing act became particularly prominent in the latter half of the 20th century, especially within the hallowed halls of the Federal Reserve. The role of the Fed is, by its very nature, to be “cautiously optimistic.” The central bank must stimulate growth without triggering inflation and curb overheating without causing a recession—a pursuit often referred to as engineering a “soft landing.” This difficult objective naturally lends itself to the language of guarded hope.

One of the most frequent uses of “cautiously optimistic” came during periods of economic recovery following a downturn. In the aftermath of the 2008 financial crisis, for example, the phrase became a recurring theme in speeches by policymakers. In a May 2009 address, Christina Romer, the Chair of President Barack Obama’s Council of Economic Advisers, presented a “cautiously optimistic” picture of the US recovery. She cited the potential for “pent-up demand” and “the natural forces of inventory rebound” to drive growth, but she was careful to emphasize the need for a “sound regulatory framework” to prevent the formation of new asset bubbles. Her use of the term was a clear attempt to instill confidence in a shaken public without creating a false sense of security. It was a message that acknowledged the deep wounds of the recession while signaling that the patient was on the mend, albeit slowly and with a need for ongoing care.

Similarly, in 2015, as the US economy continued its long, slow march out of the Great Recession, then-Federal Reserve Chair Janet Yellen used the term to describe her outlook on the labor market. Speaking at a conference, Yellen expressed her “cautious optimism that, in the context of moderate growth in aggregate output and spending, labor market conditions are likely to improve further in coming months.” Her words were a signal that the Fed was seeing progress but wasn’t yet ready to declare victory. The “cautious” part of the optimism was a nod to the fact that the recovery was still fragile and the risks of a premature policy shift, such as raising interest rates too quickly, could derail the progress made.

The phrase has also been deployed in times of transition or uncertainty. The early 2000s, following the burst of the dot-com bubble and the September 11th attacks, was another period ripe for “cautious optimism.” Federal Reserve officials, such as Vice Chairman Roger Ferguson, used the term in their speeches to describe a business sector undergoing a “serious retrenchment” in spending and production. They noted that while a recovery was possible, a confluence of factors—including a stronger dollar, falling equity prices, and tighter lending standards—created a self-reinforcing downturn. The optimism was rooted in the long-term fundamentals of the American economy, such as technological innovation, but the caution was a sober acknowledgment of the immediate headwinds. The phrase allowed policymakers to communicate a belief in the eventual triumph of American ingenuity while simultaneously justifying a policy of continued vigilance and support.

This historical pattern reveals the phrase’s utility as a communication device. It is often used when a clear, simple narrative is impossible or misleading. If an economic situation were unambiguously good, the word “optimistic” would suffice. If it were unambiguously bad, “pessimistic” would be the clear choice. “Cautiously optimistic” occupies the gray area in between, a place where the signs are mixed and the path forward is uncertain. It is a phrase that allows a speaker to acknowledge both the “good news” and the “bad news” in a single breath, preserving their credibility and managing public expectations.

In recent years, the phrase has continued to evolve. With the rise of global trade tensions and the increasing complexity of the financial system, “cautious optimism” is no longer just about the domestic business cycle. It’s now applied to an environment of “policy uncertainty,” where factors like trade tariffs, international relations, and geopolitical shocks loom large. A 2025 report from Neuberger Berman, an investment management firm, used the phrase to describe the outlook “amid policy uncertainty.” The authors were “cautiously optimistic” due to resilient economic fundamentals but worried about “tariff-related volatility” and the potential for a “shift in capital flows.” Here, the caution is not just about the economy’s internal dynamics, but also about the external forces and policy decisions that could destabilize it.

In essence, “cautiously optimistic” has become a shorthand for “things are getting better, but don’t get complacent.” It is a phrase that embodies the very nature of economic forecasting: an attempt to project a future that is inherently unknowable, based on an imperfect understanding of the present. It has been used by economists, policymakers, and journalists to navigate recessions, bubbles, and periods of geopolitical flux. It is the language of a slow and steady recovery, of a fragile but improving situation, and of a future that is full of promise, but also potential pitfalls. Through its consistent use, “cautiously optimistic” has become more than just a phrase; it is a historical record of America’s enduring, yet always measured, faith in its economic future.

Which College Classes Should Small Business Owners Take to Improve Operations?

College Classes

Small business owners often wear many hats—CEO, bookkeeper, HR manager, marketer, and operations supervisor all rolled into one. While entrepreneurial passion is the lifeblood of a startup or small venture, managing and scaling a business requires a solid foundation of practical knowledge. College-level classes can be a strategic tool to sharpen your decision-making skills, streamline operations, and enhance your business’s profitability.

But which classes are worth the time and investment?

In this article, we’ll explore college courses that small business owners should consider to improve the efficiency, productivity, and long-term sustainability of their operations. These courses are typically found in business, technology, and liberal arts departments and can often be taken through community colleges, online platforms, or university extension programs.

1. Introduction to Business Administration – College Classes

Why It Matters:

This foundational course offers a broad overview of business principles including management, marketing, finance, and human resources. For new business owners or those without formal business training, this class serves as an essential primer.

Key Topics:

Organizational structure

Operational workflow

Business ethics

Financial statements

Strategic planning

Operational Benefits:

By understanding how different business components interconnect, small business owners can better align their departments and allocate resources more effectively.

2. Operations Management

Why It Matters:

Operations Management focuses on the internal processes that turn inputs into finished goods or services. It teaches how to make business operations more efficient, cost-effective, and customer-focused.

Key Topics:

Supply chain logistics

Inventory control

Quality assurance

Workflow optimization

Lean principles and Six Sigma

Operational Benefits:

You’ll learn how to reduce waste, manage time and resources more efficiently, and improve product quality—leading to higher customer satisfaction and reduced operational costs.

3. Accounting and Financial Management

Why It Matters:

Financial literacy is critical to sustaining and growing a business. This course teaches you how to read and interpret financial statements, manage cash flow, and make data-driven decisions.

Key Topics:

Balance sheets and income statements

Budgeting

Cash flow forecasting

Cost-benefit analysis

Tax planning basics

Operational Benefits:

Understanding your business’s financial health enables you to optimize spending, identify underperforming areas, and invest strategically in growth opportunities.

4. Marketing Principles

Why It Matters:

No matter how efficient your operations, your business can’t succeed without customers. Marketing courses teach you how to understand your target audience, position your brand, and drive sales through effective messaging.

Key Topics:

Market research

Consumer behavior

Branding

Digital marketing basics

Advertising strategy

Operational Benefits:

Better marketing means more consistent customer acquisition and retention, which leads to steadier cash flow and more predictable operational planning.

5. Business Communication

Why It Matters:

Effective communication is the backbone of good management. Whether you’re emailing clients, pitching investors, or instructing employees, how you communicate determines how your business is perceived.

Key Topics:

Verbal and nonverbal communication

Email etiquette

Writing proposals and reports

Public speaking and presentations

Operational Benefits:

Improved communication reduces misunderstandings, boosts team morale, and enhances client relationships, all of which contribute to smoother operations.

6. Human Resource Management

Why It Matters:

People are your most valuable resource. This course teaches how to recruit, manage, and retain talent while staying compliant with labor laws.

Key Topics:

Hiring and onboarding

Performance management

Employment law

Compensation and benefits

Conflict resolution

Operational Benefits:

A strong HR strategy minimizes turnover, boosts employee satisfaction, and ensures compliance with labor regulations—all crucial to maintaining smooth daily operations.

7. Project Management

Why It Matters:

Every initiative in your business—whether it’s launching a new product or revamping your website—is a project. This course offers tools and frameworks to ensure projects are completed on time and within budget.

Key Topics:

Project planning and execution

Resource allocation

Risk management

Agile and Waterfall methodologies

Gantt charts and timelines

Operational Benefits:

Strong project management skills improve your ability to execute ideas efficiently, avoid costly delays, and allocate time and personnel more effectively.

8. Entrepreneurship and Innovation

Why It Matters:

Entrepreneurship classes focus on business development, problem-solving, and innovative thinking. This class is ideal for owners looking to expand, pivot, or revitalize their business model.

Key Topics:

Opportunity identification

Business model innovation

Startup financing

Pitching to investors

Scalability

Operational Benefits:

You’ll gain the strategic insight to adapt quickly to market changes, test new ideas, and evaluate risk intelligently.

9. Information Systems and Technology for Business

Why It Matters:

Digital tools are central to running an efficient business. This course introduces systems like ERP, CRM, and POS, and discusses how to use data analytics to inform business decisions.

Key Topics:

Cloud computing

Cybersecurity basics

Data analytics

Workflow automation

Software selection and integration

Operational Benefits:

Integrating the right tech stack can streamline communication, track customer behavior, and automate repetitive tasks, freeing up time for strategic thinking.

10. Legal Environment of Business

Why It Matters:

Understanding the legal landscape helps you avoid costly lawsuits and regulatory headaches. This course offers insights into contracts, liabilities, and regulatory compliance.

Key Topics:

Business structures (LLC, S-corp, etc.)

Contracts and negotiations

Intellectual property

Employment law

Government regulations

Operational Benefits: