If the global economy feels like a high-wire act lately, you aren’t alone. We are currently navigating a “polycrisis“—a fancy term for when multiple major headaches (inflation, geopolitical tension, and shifting labor markets) all hit the fan at the same time.

We are standing on a narrow ledge. One side leads to a hard landing; the other leads to a stabilized “new normal.” Here is a look at the forces threatening to push us off, and the safety nets that might just pull us back.

The Push: What Could Tip Us Over?

It doesn’t take a wrecking ball to cause a recession; sometimes, it just takes a few well-placed dominos. Here are the primary risks:

The “Higher for Longer” Fatigue: While central banks use interest rates to cool inflation, keeping them elevated for too long puts immense pressure on household debt and corporate margins. If the “lag effect” hits all at once, consumer spending—the engine of the economy—could stall.

Geopolitical Aftershocks: Energy prices are notoriously sensitive to global conflict. Any significant escalation in major trade corridors can reignite supply chain chaos, sending the cost of goods back into the stratosphere.

The Commercial Real Estate Ghost Town: With remote work now a permanent fixture, many office buildings are sitting half-empty. As these property loans come due for refinancing at higher rates, we could see a localized banking tremor.

The Pull: What Could Help Us Pull Through?

It’s not all doom and gloom. There are several structural “muscles” keeping the economy upright:

The Resilient Labor Market: Despite tech layoffs making headlines, overall unemployment remains historically low. As long as people have jobs, they tend to keep spending, which provides a powerful floor for the economy.

The Productivity “AI Bump”: We are at the beginning of a massive technological shift. Early adoption of generative AI is already beginning to streamline workflows and reduce operational costs, which could lead to a non-inflationary growth spurt.

Household Balance Sheets: Unlike the 2008 crash, many consumers and corporations locked in low interest rates years ago. This “debt buffer” has bought the private sector time to adjust to the new economic reality.

The Bottom Line: Balance, Not Freefall

The economy isn’t necessarily “broken,” but it is transitioning. We are moving away from an era of “free money” and into an era where efficiency and strategic investment matter again.

Scenario

Key Driver

Likely Outcome

The Hard Landing

Persistent inflation + high rates

Brief but sharp recession; rising unemployment.

The Soft Landing

Controlled cooling + tech growth

Flat growth for a year, followed by a steady recovery.

The No Landing

Continued high spending

Economy stays hot, but rates stay high indefinitely.

The Takeaway: While the ledge is narrow, the path across is still visible. Navigating the next twelve months will require agility from policymakers and patience from investors. We may be on the edge, but we aren’t over it yet..

For many distributors, the word “factoring” carries some outdated baggage. If you’re hesitant to pull the trigger, it’s likely because of one of these common misconceptions. Let’s separate the noise from the facts:

The Myth

The Reality

“Factoring is a sign of financial trouble.”

Factoring is a sign of growth. Most companies use factoring because they are growing too fast for their cash flow to keep up. It’s a strategic choice to fuel expansion, not a last-ditch effort to stay afloat.

“My customers will think I’m going under.”

It’s a standard B2B practice. Major retailers and manufacturers deal with factors every day. In many industries, like apparel or electronics distribution, it’s actually the “gold standard” for managing receivables.

“It’s way too expensive.”

Look at the ROI. While the fee (1–3%) is higher than a bank loan, the “cost of waiting” 60 days for a check often means missing out on new inventory or early-pay discounts from your own suppliers that could actually save you more than the factoring fee.

“I’ll lose control of my customer relationships.”

You stay in the driver’s seat. Modern factoring companies act as a professional extension of your back office. They want your customers to stay happy so they keep buying (and paying). You still manage the sales and service; they just handle the math.

“It’s just like a high-interest loan.”

It’s not a loan at all. Because you are selling an asset (your invoice), you aren’t taking on debt. There are no monthly principal or interest payments to worry about—the “payment” comes from your customer, not your bank account.

The “Silent” Benefit: Professional Credit Checks

One “Reality” that distributors often overlook is that a factor acts as a free credit department. Before you ship $50,000 worth of goods to a new client, you can ask your factor to check their credit. If the factor won’t buy the invoice, that’s a massive red flag that you probably shouldn’t be selling to that customer on terms in the first place.

What you should know in selecting a factoring Partner

Choosing a factoring company is like choosing a long-term business partner. The right one will act as your back-office credit department; the wrong one can be an expensive administrative nightmare. Use this checklist to vet potential partners:

1. The Core Logistics

[ ] Industry Expertise: Do they have experience with the specific nuances of distribution (e.g., handling chargebacks, bill-backs, or progressive shipping)?

[ ] Advance Rate: Will they advance at least 80–90% of the invoice value?

[ ] Funding Speed: Can they provide “Same Day” or “Next Day” funding once an invoice is verified?

[ ] Funding Source: Are they a Direct Lender (bank-backed) or an independent factor? (Direct lenders often have lower rates and more stability).

2. Transparency & Fees

[ ] The “All-In” Rate: Ask for a breakdown of all fees. Look out for hidden “junk fees” like application fees, wire fees, or credit check fees.

[ ] Recourse vs. Non-Recourse: * Recourse: You must buy back the invoice if your customer doesn’t pay. (Lower fees).

Non-Recourse: The factor takes the credit risk if the customer goes bankrupt. (Higher fees).

[ ] Volume Requirements: Are there “Monthly Minimums”? If you don’t hit a certain volume, will you be penalized?

3. The “Relationship” Factor

[ ] Dedicated Account Manager: Will you have a single point of contact who knows your business, or a generic 1-800 help desk?

[ ] Customer Interaction Style: How do they contact your customers for verification? You want a partner who is professional and polite, as they represent your brand.

[ ] Technology Integration: Do they sync with your accounting software (QuickBooks, NetSuite, etc.) for easy invoice uploading?

4. Contract Flexibility

[ ] Contract Length: Avoid multi-year lock-ins. Look for month-to-month or one-year terms with clear exit clauses.

[ ] Termination Notice: How much notice is required to leave? (Usually 30–90 days).

[ ] Personal Guarantee: Is a personal guarantee required? (Standard for many small business factors, but worth clarifying).

What is Factoring: In the world of distribution, the “growth paradox” is a real headache. You land a massive new retail contract—which is great news—but suddenly you’re shelling out for inventory and shipping costs while your customer sits on a 60- or 90-day payment term.

For many distributors, waiting for those invoices to clear creates a suffocating bottleneck. This is where Accounts Receivable (AR) Factoring comes in. It’s not a loan; it’s a financial tool that turns your unpaid invoices into immediate working capital.

How It Works: The Quick Breakdown

Instead of waiting months for a customer to pay, you sell your outstanding invoices to a “factor” (a specialized financial company).

The Advance: The factor typically advances you 80% to 90% of the invoice value within 24 hours.

The Collection: The factor handles the collection from your customer.

The Rebate: Once the customer pays, the factor sends you the remaining balance, minus a small fee (usually 1–3%).

4 Major Benefits for Distributors

1. Bridge the Inventory Gap

Distributors often have to pay suppliers long before they get paid by their own clients. Factoring provides the liquidity to pay your manufacturers upfront, often allowing you to take advantage of early-payment discounts that can actually offset the cost of the factoring fee itself.

2. Fuel Rapid Scalability

Traditional bank loans are limited by your credit history or collateral. Factoring, however, scales with your sales. The more you sell to reputable customers, the more funding becomes available. It allows you to say “yes” to large orders that you otherwise couldn’t afford to fulfill.

3. Professional Credit Management

Many factoring companies act as an extension of your back office. They perform credit checks on your potential customers, helping you avoid “bad seeds” before you ship a single pallet. This reduces your risk of bad debt and saves your team the awkwardness of making collection calls.

4. No New Debt

Since factoring is the purchase of an asset (your invoice) rather than a loan, it doesn’t show up as debt on your balance sheet. This keeps your debt-to-equity ratio clean, making your business look much healthier to future investors or traditional lenders.

Is It Right For You?

Factoring is particularly powerful if you are:

A startup with a thin credit history but blue-chip customers.

Experiencing seasonal spikes that drain your cash reserves.

Tired of the “waiting game” associated with 30, 60, or 90-day terms.

While there is a cost involved, the ability to reinvest that cash immediately into new inventory or operations often outweighs the fee. In the fast-moving world of distribution, speed is a competitive advantage.

Factoring vs. A Traditional Line of Credit: A Distributor’s Comparison

While both tools solve cash flow problems, they operate very differently. Here is how they stack up for a growing distributor:

Feature

AR Factoring

Traditional Bank Line of Credit (LOC)

Funding Limit Based On…

The creditworthiness of your customers and your accounts receivable balance.

Your business’s credit history, profitability, and your collateral.

Speed of Funding

Extremely fast. Setup takes a few days; once active, funding often occurs within 24–48 hours of invoice verification.

Slow. The approval process can take weeks or even months.

Debt Type

Not Debt. It is the “asset purchase” of your invoices.

Debt. This is a loan that appears as a liability on your balance sheet.

Impact on Credit

Boosts Credit Score. It provides cash to pay your suppliers and operational debts on time.

Lowers “Available” Credit. Utilizing the full LOC can temporarily lower your score until it’s paid down.

Administrative Support

The factor often provides credit management and collection services, freeing up your back office.

You retain full responsibility for all collections and monitoring customer credit.

Scalability

Unlimited. As your credit-worthy sales grow, your available funding automatically increases.

Capped. Your limit is fixed and requires a re-application process to increase.

Gemini said

Certainly. Here is a comparison table and a section you can drop directly into your blog post.

Factoring vs. A Traditional Line of Credit: A Distributor’s Comparison

While both tools solve cash flow problems, they operate very differently. Here is how they stack up for a growing distributor:

Feature

AR Factoring

Traditional Bank Line of Credit (LOC)

Funding Limit Based On…

The creditworthiness of your customers and your accounts receivable balance.

Your business’s credit history, profitability, and your collateral.

Speed of Funding

Extremely fast. Setup takes a few days; once active, funding often occurs within 24–48 hours of invoice verification.

Slow. The approval process can take weeks or even months.

Debt Type

Not Debt. It is the “asset purchase” of your invoices.

Debt. This is a loan that appears as a liability on your balance sheet.

Impact on Credit

Boosts Credit Score. It provides cash to pay your suppliers and operational debts on time.

Lowers “Available” Credit. Utilizing the full LOC can temporarily lower your score until it’s paid down.

Administrative Support

The factor often provides credit management and collection services, freeing up your back office.

You retain full responsibility for all collections and monitoring customer credit.

Scalability

Unlimited. As your credit-worthy sales grow, your available funding automatically increases.

Capped. Your limit is fixed and requires a re-application process to increase.

Which One Wins for Distributors?

A bank line of credit is almost always the cheapest form of capital if you can get approved for a large enough limit.

However, for distributors in a hyper-growth phase, or those whose balance sheets don’t match their ambition, AR factoring offers unmatched speed and scalability. It allows you to leverage your customers’ financial strength to fund your own growth.

The Final Verdict: When to Choose Factoring

For a distributor, the choice between factoring and other financing boils down to your growth trajectory and customer base.

A traditional bank line of credit is often the lowest-cost option, but it is also the most rigid. If you have years of steady profitability and a “boring” (predictable) growth curve, the bank is your best friend.

However, AR factoring is the superior choice if:

You are growing faster than your cash flow allows: If a sudden 50% increase in orders would actually break your business because you can’t afford the inventory, you need factoring.

You have “lumpy” revenue: If you deal with seasonal spikes where you need $500k in October but only $50k in January, the flexibility of factoring is unmatched.

Your customers are larger than you: If you are a small distributor selling to giants like Walmart or Amazon, a factor will look at their multi-billion-dollar credit rating to fund you, rather than your own limited history.

Ultimately, factoring isn’t just a way to get paid early—it’s a way to weaponize your accounts receivable to outmaneuver competitors who are still stuck waiting for a check in the mail.

Factoring: Cash for Suppliers to the Healthcare Industry – Accounts Receivable Factoring can quickly meet the working capital needs of manufacturers and distributors which serve the healthcare industry.

Program Overview:

$100,000 to $30 Million

Quick AR Advances

No Audits

No Financial Covenants

Most Suppliers are Eligible

We specialize in challenging deals :

Start-ups

Turnarounds

Historic Losses

Customer Concentrations

Poor Personal Credit

Character Issues

Versant focuses on the quality of your client’s accounts receivable, ignoring their financial condition.

This enables us to move quickly and fund in as few as 3-5 days. Contact me today to learn if your client is a factoring fit.

IEEPA Tariff While the Supreme Court invalidated the Administration’s ability to impose tariffs under IEEPA (International Emergency Economic Powers Act), it was deliberately silent with respect to refunds.

As the Administration’s stance is likely to be adversarial, it could take months if not years for businesses to receive IEEPA tariff refunds via conventional channels.

Prior to the Supreme Court Ruling, Hedge Funds were purchasing IEEPA tariff claims at an average of only 22% of the total claim due to the high risks involved. After the Ruling, due to mitigation of some of the uncertainty, they are currently purchasing claims at 75% of the refund amount. Rates are based on claim size and credit quality as tariff refund claims are not assignable. Importers with IEEPA tariff refund claims starting at $500,000 are eligible and there is no maximum limit. AES has monetized $20 million in refund claims since its involvement in brokering IEEPA tariff refund claims commenced 5 months ago. Clients include those in the food, seasonal decoration, apparel and home goods industries.

Instead of waiting 6, 12, 24 months or even longer to receive an IEEPA tariff refund, Hedge Funds can purchase claims within approximately 4 to 6 weeks depending on the quality of documentation assembled by the business.

How the Process of Selling an IEEPA Tariff Claim Works

Concept is: As an example, Company X has paid ($10 Million) in tariffs since April 7, 2025 Company X wants to de-risk prior to determination and finalization of the IEEPA tariff

Refund Process. Company X sells (50%, 100%, or some other percentage) of its tariff ‘claim’ to Buyer A in the form of a participation.

The Trade is nonrecourse to Company X as to the outcome of the Refund Process; but recourse to Company X only if the amount / validity of the claim is proven to be false, or too high.

Process for Selling IEEPA Tariff Claims: As an example, Company X has paid $10 million in IEEPA Tariffs.

Company X agrees to “sell” its tariff claim to Buyer for 75% of the claim amount, i.e. $7.5 million.

Buyer sends Seller a Confirm, and then ultimately a Participation Agreement which will govern the transaction. IMPORTANT – Company X retains its status as the “Plaintiff” / “Claimant” since these tariff claims are not transferable.

Buyer might ask Company X to commence litigation for the return of the IEEPA tariffs paid. The rationale for this is that it is possible that only those parties who have commenced actual litigation are entitled to refunds. Thus, Company X will need to commence litigation in order to receive their refund.

Buyer will continue to monitor the situation and inform Company X of developments. If and when the refund is received on the claim, Company X will receive the refund and forward to the Buyer.

Using an IEEPA Tariff Claim as Collateral for a Loan

In lieu of selling an IEEPA Tariff Claim at a discount, it is possible to use this claim as collateral for a term loan. This term loan would be on a “recourse: basis to the borrower.

The potential loan amount could be up to approximately 50% to 60% of the total IEEPA claim amount. However, the claim must exceed $20 million to qualify for a loan. The interest rate would be in the low to mid-teens.

Key Points Regarding the Sale: Company X (as seller of the Claim) must be a financially healthy enough counterparty for Buyer A to enter into what could be a 2-to-5-year process of obtaining the refund. Legal fees are split going forward based on risk percentage. If Company X sells 100% today, Buyer A will pay 100% of legal costs today.

Buyers are currently paying up to 75% to companies seeking to sell their IEEPA tariff claims. However, this is an evolving market and these percentages can either increase or decrease depending on the markets’ reaction to the Trump Administration’s expected obstructionism and the unresolved Court of International Trade’s procedural issues. Prior to the Supreme Court decision, buyers were purchasing tariff claims at an average of 22% due to the high risks involved.

We will be monitoring on a daily basis the rates at which Buyers are purchasing IEEPA claims and we will update our website accordingly. Feel free to email us to ascertain what the rate is on any particular day.

There would likely be an administrative process instituted such that companies that have paid these IEEPA tariffs will need to file special claims and wait to get refunded by the government. The process of receiving the refund payment from the government could take up to 2 to 5 years according to trade experts.

This details how investment firms are turning a legal and political mess into a new trading opportunity.

The situation stems from a recent Supreme Court ruling that tossed out several of President Trump’s sweeping tariffs. This has created a scramble for companies to claw back the levies they have already paid—estimated to be as high as $133 billion.

The Rise of “Claims Trading”: Large corporations (like retailers and manufacturers) that paid billions in tariffs are now selling the rights to their potential government refunds to Wall Street investors.

Why Companies Are Selling: Rather than waiting years for the government to process refunds or navigate complex litigation, companies are opting for immediate cash by selling their claims at a discount.

The Players: Specialist investment firms—including King Street Capital Management, Anchorage Capital Advisors, and Fulcrum Capital—are among those pouncing on these claims. They are betting that they can eventually collect the full refund from the Treasury, netting a significant profit.

Legal Uncertainty: The Supreme Court has not yet explicitly ruled on whether the government must issue refunds for the tariffs already collected. Despite this, investors are moving quickly to snap up these rights, treating them similarly to how they trade the debt of bankrupt companies.

The “Chaos” Factor: The process is currently a “long, drawn-out mess” with high administrative hurdles. Traders are effectively providing a “liquidity service” to companies that want the tariff money back on their balance sheets now rather than later.

In short, while the reversal of the tariffs has caused massive administrative and fiscal confusion for the government, Wall Street has identified it as a lucrative new asset class.

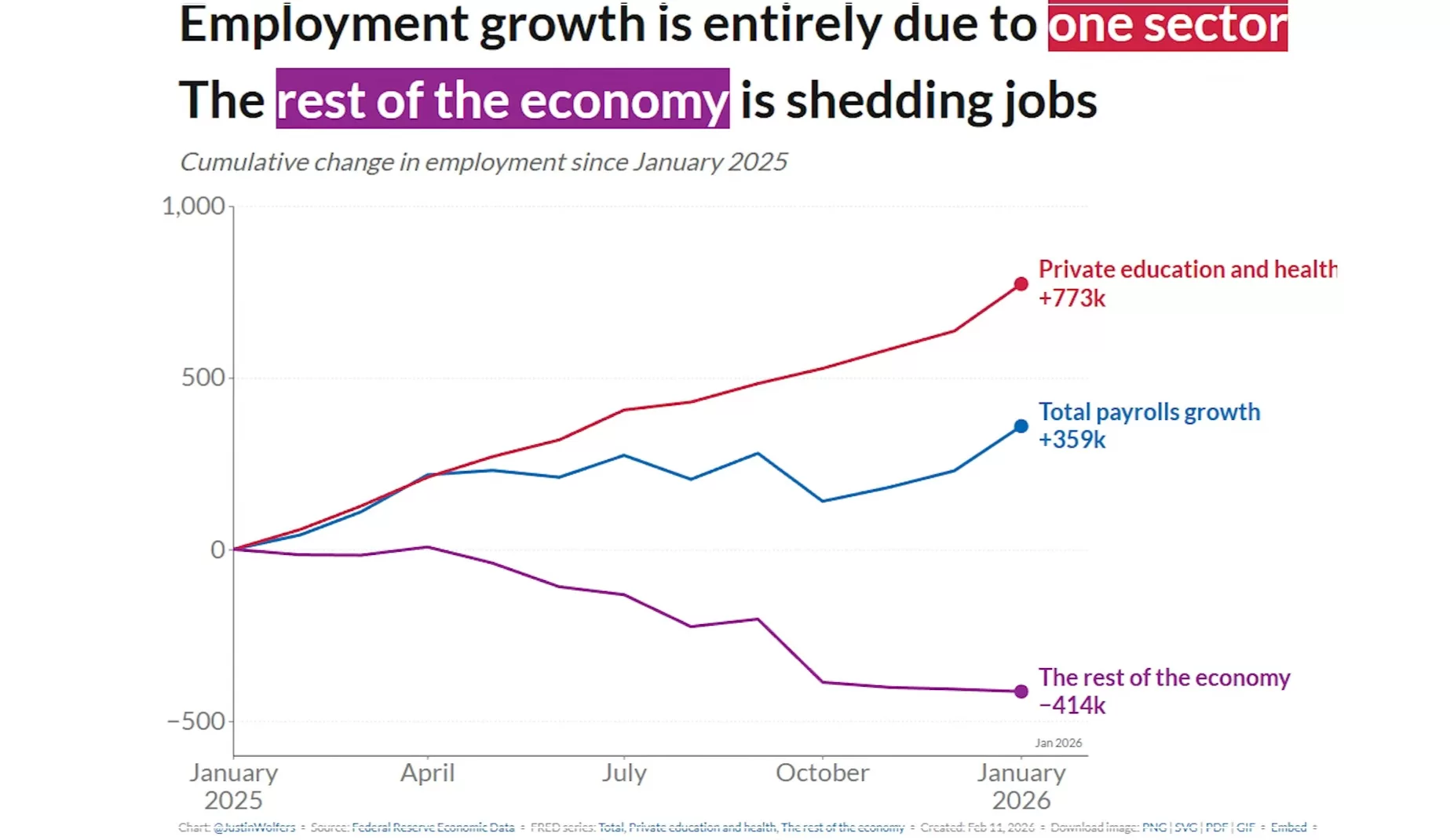

The U.S. labor market began 2026 with a surprising burst of energy, shaking off a sluggish 2025. According to the latest data from the Bureau of Labor Statistics (BLS) released on February 11, 2026, employers added 130,000 jobs in January—easily doubling December’s figures and blowing past economist expectations of roughly 70,000.

While the report was delayed by a week due to a brief federal government shutdown, the results suggest that the “hiring fatigue” seen late last year might be beginning to thaw.

The Numbers at a Glance

The January report offers a mix of resilience and necessary context for the year ahead:

Total Jobs Added: 130,000 (up from a revised 50,000 in December).

Unemployment Rate: Ticked down to 4.3% (from 4.4%).

Average Hourly Earnings: Rose by 0.4% in January, bringing the year-over-year increase to 3.7%.

Labor Force Participation: Remained steady at 62.5%.

Sector Winners and Losers

The growth wasn’t uniform across the board. In fact, a few key sectors carried the heavy lifting for the entire economy:

Healthcare & Social Assistance: This sector remains the titan of the U.S. job market, adding 124,000 jobs (82k in healthcare and 42k in social assistance).

Construction: Added a solid 33,000 jobs, largely driven by nonresidential specialty trade contractors.

The Tech & White-Collar Slump: Conversely, professional and business services and manufacturing continued to struggle, reflecting ongoing shifts in AI implementation and trade policy impacts.

Government: Federal employment saw a decline, partly a ripple effect of recent policy shifts and the temporary shutdown.

Why This Matters

After a tumultuous 2025—which was recently revised to show only 181,000 total jobs added for the entire year—this January figure is a massive sigh of relief. It suggests that while the economy isn’t sprinting, it’s found its footing.

“The January gains are a sign that the labor market is stabilizing,” says one economist. “However, the high concentration of growth in healthcare suggests a ‘one-legged stool’ economy that we need to watch closely.”

Looking Ahead

While 130,000 jobs is a “stronger footing,” the market remains complex. Layoffs in high-profile sectors like tech and transportation (notably Amazon and UPS) dominated January headlines, yet the aggregate data shows that other sectors are more than absorbing that displaced talent.

For job seekers, the message is clear: the opportunities are there, but they have shifted. Strategic hiring is the theme of 2026, with a high premium on specialized skills in healthcare, infrastructure, and adaptive technologies.

The January jobs report has effectively shifted the narrative for the Federal Reserve. While the 130,000 jobs added might seem modest by historical standards, it was a significant “beat” compared to expectations, and it has given the Fed a reason to tap the brakes on further interest rate cuts.

Here is how the latest data is influencing the Fed’s next move:

1. From “Easing” to “Holding”

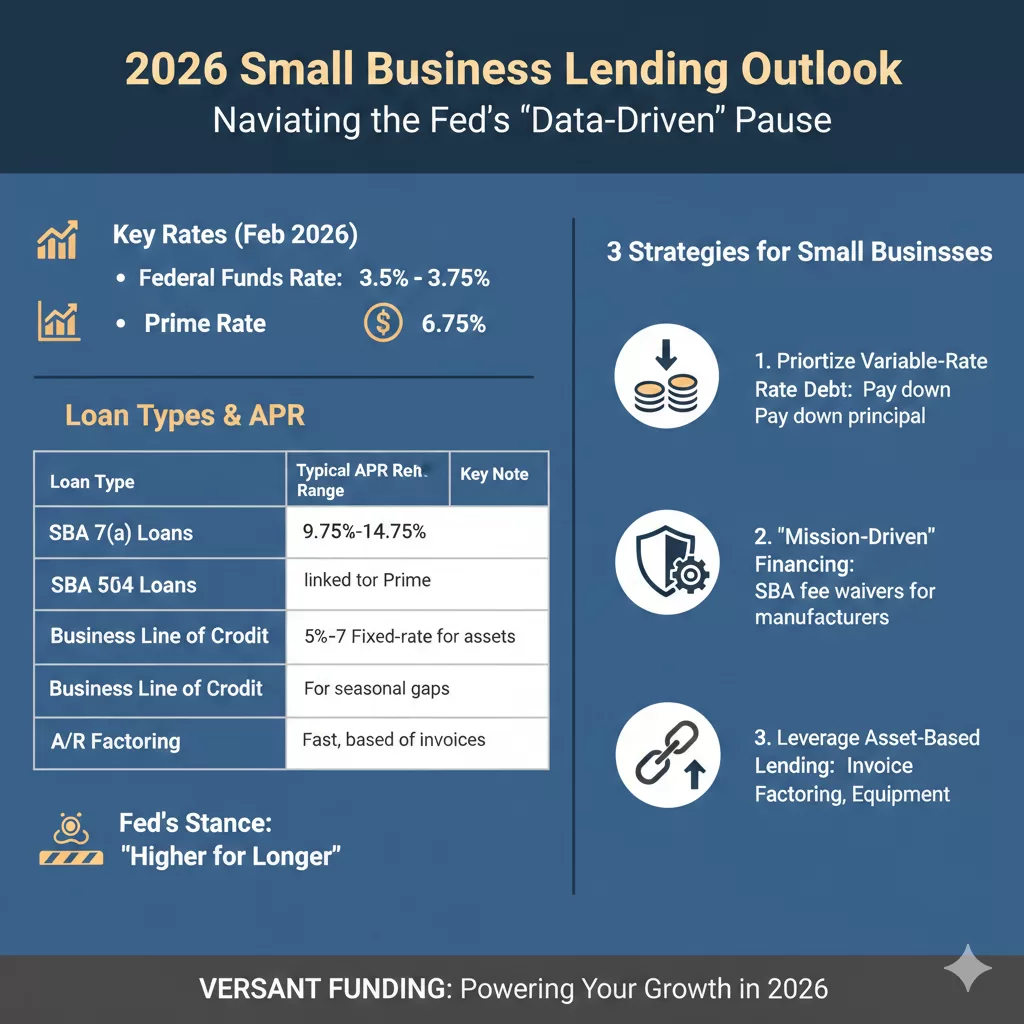

Following three consecutive rate cuts in late 2025, the Federal Reserve held rates steady at its January 28, 2026 meeting, maintaining the federal funds rate at 3.5% to 3.75%. This jobs report reinforces that “pause.”

The Consensus: With the unemployment rate ticking down to 4.3% and job growth doubling December’s numbers, there is no longer an “emergency” need to stimulate the economy.

Market Sentiment: Before this report, some traders were betting on a March cut. Now, CME FedWatch tools show those odds have plummeted, with the consensus moving toward a “higher for longer” stance through at least the first half of the year.

2. Emerging Internal Division

The Fed is no longer acting in total unison. The January meeting saw a rare 10-2 vote, with two dissenting members actually pushing for another 25-basis-point cut due to lingering concerns about long-term hiring weakness.

The Hawks: Officials like Cleveland Fed President Beth Hammack and Dallas Fed President Lorie Logan have signaled that the Fed should “err on the side of patience,” arguing that current rates are “neutral”—neither helping nor hurting the economy.

The Doves: Those worried about the “one-legged stool” (growth coming only from healthcare) fear that without more cuts, sectors like tech and manufacturing will continue to bleed jobs.

3. The “Neutral Rate” Debate

Chair Jerome Powell recently noted that the economy is on a “firm footing” entering 2026. Analysts now believe the Fed is searching for the neutral rate—the sweet spot where inflation stays at 2% without triggering a recession.

Because average hourly earnings rose 0.4% in January (3.7% annually), the Fed is wary that cutting rates too soon could reignite inflation, especially with potential new trade tariffs on the horizon.

Key Dates to Watch

Event

Date

Significance

January CPI Report

Feb 13, 2026

Will confirm if the wage growth in the jobs report is driving up prices.

Fed “Beige Book”

Mar 4, 2026

Regional reports on how small businesses are actually feeling.

Next FOMC Meeting

Mar 17-18, 2026

The next formal window for a rate change decision.

For a small business owner, the January jobs report isn’t just about hiring statistics—it’s a leading indicator for the cost of your next loan or line of credit.

Following the stronger-than-expected labor data, the Federal Reserve has hit “pause” on interest rate cuts. For businesses at Versant Funding and across the U.S., this means a period of “stabilized high” borrowing costs. Here is what your business needs to know to navigate the financial landscape of early 2026.

2026 Borrowing Outlook: The “Data-Driven” Pause

The Fed began 2026 by holding the federal funds rate steady at 3.5% to 3.75%. While the market had hoped for more aggressive easing, the surge of 130,000 new jobs in January has signaled to policymakers that the economy is not yet in need of more “cheap money.”

Current Lending Rates (As of February 2026)

Loan Type

Typical APR Range

Key Note

SBA 7(a) Loans

9.75% – 14.75%

Variable rates fluctuate with the Prime Rate (currently 6.75%).

SBA 504 Loans

5% – 7%

Fixed-rate; best for long-term real estate or equipment.

Business Lines of Credit

10% – 28%

Vital for seasonal inventory and payroll gaps.

Accounts Receivable Factoring

24% – 36%

High speed; based on invoice value rather than credit score.

Three Strategies for Small Businesses

With rates unlikely to drop significantly before the summer, owners should shift from “waiting for better rates” to “optimizing current cash flow.”

Prioritize Variable-Rate Debt: If you are carrying an SBA 7(a) loan or a variable line of credit, your payments will remain flat for now. Use this stability to pay down principal where possible, as the “higher for longer” stance means interest costs won’t be melting away anytime soon.

Look for “Mission-Driven” Financing: In 2026, the SBA is waiving guarantee fees for certain small manufacturers (NAICS 31-33). If your business fits this category, you could save thousands in upfront costs regardless of the interest rate.

Leverage Asset-Based Lending: If traditional bank term loans are too restrictive, consider Invoice Factoring or Equipment Financing. These options often focus more on the value of your assets (your unpaid invoices or machinery) than on the Fed’s baseline rates, providing more predictable access to capital during economic volatility.

The Bottom Line

The “stronger footing” of the U.S. labor market is a double-edged sword: it proves consumer demand is resilient, but it keeps the cost of capital elevated. For 2026, the most successful businesses will be those that prioritize liquidity and debt structure over simply chasing the lowest rate.

Factoring Proposal: With only a single major distributor as customer, this business was unable to find a lender willing to fund them. Our underwriting focuses solely on the quality of our client’s customer so time in business and customer concentration are irrelevant.

In the world of candy importing, timing is everything. You have to navigate seasonal peaks (think Halloween and Valentine’s Day), manage international shipping lead times, and juggle the demands of large retailers.

However, there is often a massive gap between the moment your colorful shipments clear customs and the moment your retail partners actually pay their invoices. If your capital is trapped in Accounts Receivable (AR), you might find yourself unable to jump on the next big inventory opportunity.

This is where Accounts Receivable Factoring—also known as invoice factoring—becomes a game-changer.

What Exactly is Factoring?

Factoring isn’t a loan; it’s the sale of your assets. You sell your outstanding invoices to a “factor” (a specialized financial company) at a slight discount. In return, you get immediate access to the cash that was previously tied up for 30, 60, or even 90 days.

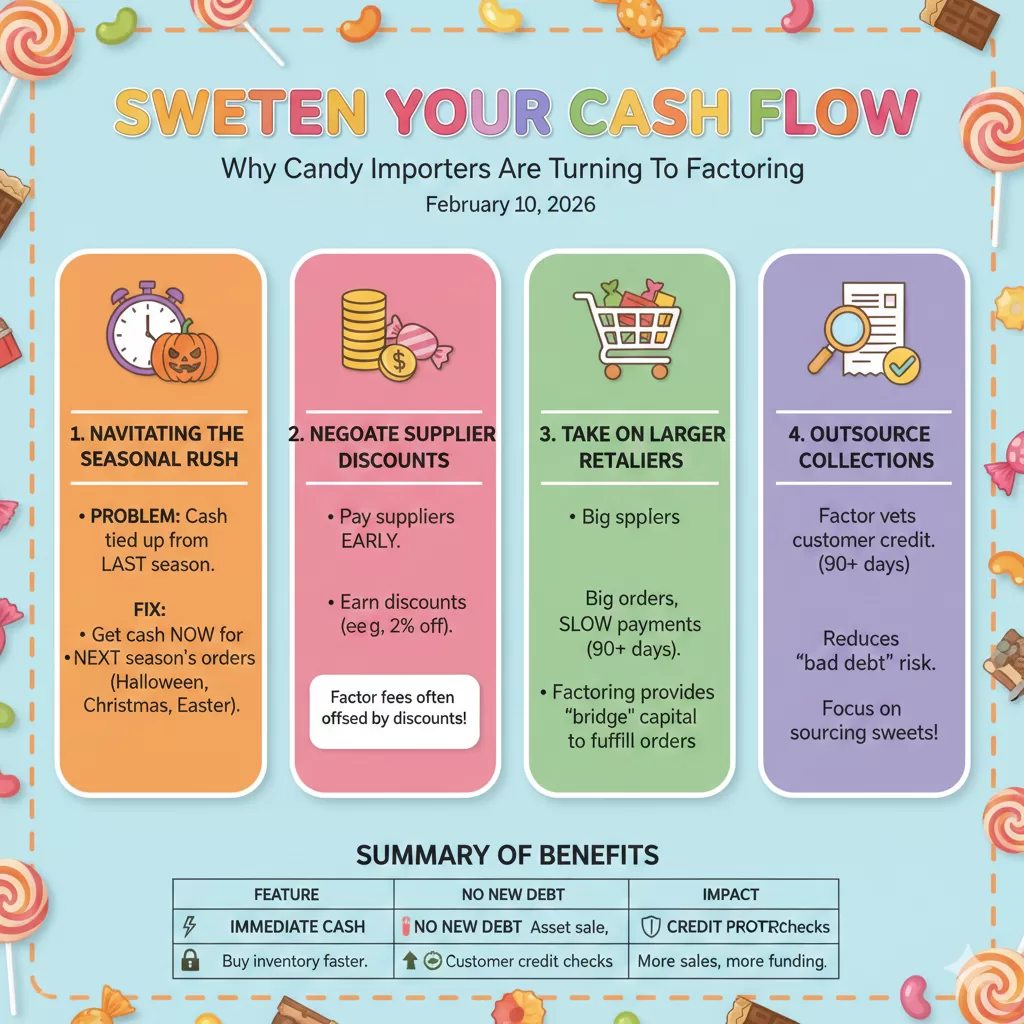

1. Navigating the Seasonal Rush

Candy is a highly seasonal business. To prepare for the “Big Three”—Halloween, Christmas, and Easter—importers must place massive orders months in advance.

The Problem: Your cash is tied up in invoices from the previous season while you need to pay suppliers for the next one.

The Factoring Fix: By factoring current invoices, you get an immediate cash injection to cover manufacturing and shipping costs for upcoming peak periods, ensuring you never miss a shelf-stocking deadline.

2. Negotiating Supplier Discounts

When you have “cash in hand” thanks to factoring, you move to the front of the line with global suppliers. Many international manufacturers offer early payment discounts (e.g., a 2% discount if paid within 10 days).

The small fee you pay for factoring is often completely offset by the discounts you earn from your suppliers by paying them early.

3. Taking on Larger Retailers

Big-box retailers are great for volume, but they are notorious for long payment terms. If a major chain wants to place a massive order but won’t pay for 90 days, a small-to-medium importer might have to say “no” simply because they can’t afford to wait that long for the payout.

Factoring provides the “bridge” capital. You can fulfill the order, factor the invoice the day the candy ships, and have the funds to keep the rest of your business running smoothly.

4. Outsourcing the “Headache” of Collections

Many factoring companies handle the back-end credit checking and collections process. For a lean importing team, this is a massive relief.

The factor vets the creditworthiness of your customers before you even ship, reducing your risk of “bad debt” and allowing you to focus on sourcing the best sweets rather than chasing down checks.

Summary of Benefits

Feature

Impact on Your Candy Business

Immediate Cash

Buy inventory for the next holiday season without waiting.

No New Debt

Factoring is an asset sale, not a bank loan with monthly interest.

Credit Protection

Many factors provide credit snapshots of your retail partners.

Scalability

The more you sell, the more funding becomes available.

Is Factoring Right for You?

If your candy importing business is growing faster than your bank account can keep up with, factoring provides the liquidity to keep your momentum. It turns your “sold” inventory back into “buying” power instantly.

Factoring: The Quick Cash Solution Manufacturers Need Now

In today’s dynamic market, manufacturers face a unique set of challenges. From managing inventory and production schedules to navigating supply chain disruptions and fluctuating demand, the need for reliable, accessible capital is constant. That’s where factoring comes in, offering a powerful and often overlooked solution for quick cash.

At Versant Funding, we understand the specific financial pressures manufacturers endure. That’s why we specialize in providing tailored factoring services designed to get you the capital you need, when you need it. Our latest video, which you can watch above, highlights how factoring can be a game-changer for your business.

What is Factoring, and Why is it Perfect for Manufacturers?

Simply put, factoring allows you to sell your accounts receivable (invoices) to a third party (the factor) at a small discount in exchange for immediate cash. Instead of waiting 30, 60, or even 90 days for your customers to pay, you get the funds right away.

For manufacturers, this means:

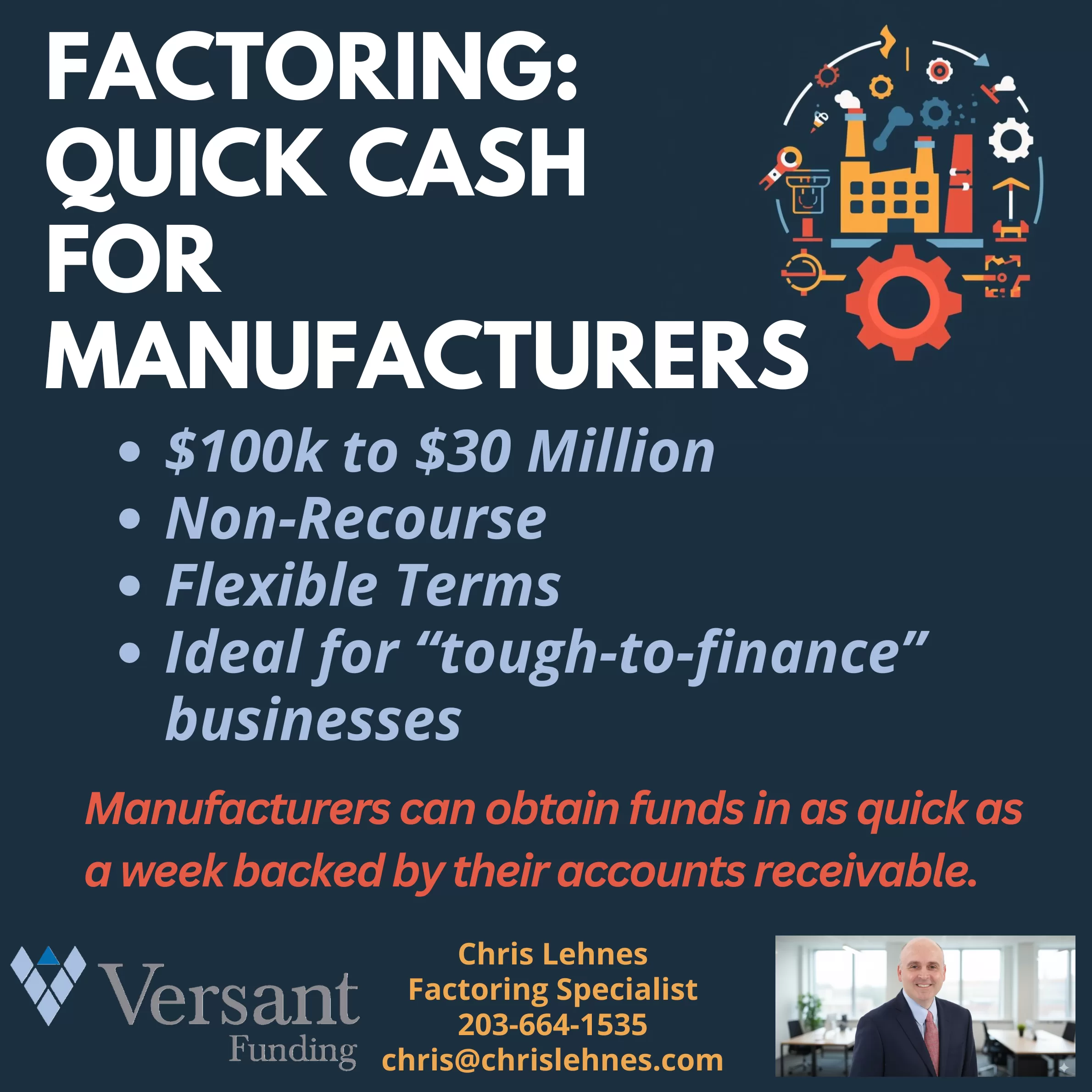

Quick Cash Flow: No more cash flow gaps hindering your production or growth initiatives. Get funds in as quick as a week!

Significant Funding: We offer funding from $100,000 to $30 Million, providing substantial support whether you’re a growing mid-sized company or a large enterprise.

Non-Recourse Factoring: This is a crucial benefit for manufacturers. With non-recourse factoring, if your customer fails to pay due to bankruptcy or insolvency, you’re typically not responsible for repaying the advance. This transfers the credit risk away from your balance sheet.

Flexible Terms: We work with you to create terms that fit your unique business model and cash flow requirements.

Ideal for “Tough-to-Finance” Businesses: Traditional bank loans can be hard to secure, especially for newer companies, those with limited collateral, or those experiencing rapid growth. Factoring focuses on the quality of your accounts receivable, making it an accessible option when other avenues are closed.

How Manufacturers Benefit from Factoring:

Imagine being able to:

Purchase Raw Materials: Take advantage of bulk discounts or secure critical components without delay.

Meet Payroll: Ensure your skilled workforce is paid on time, every time.

Invest in New Equipment: Upgrade machinery or expand your production lines to increase efficiency and capacity.

Handle Large Orders: Don’t turn away big opportunities because of insufficient working capital.

Improve Credit Standing: Use the immediate cash to pay suppliers promptly, potentially earning early payment discounts and strengthening your vendor relationships.

Why?

We pride ourselves on being more than just a capital provider. We are your partner in growth. I am dedicated to understanding the intricacies of the manufacturing sector and crafting financial solutions that truly work.

Ready to unlock the potential of your accounts receivable?

To see how factoring can transform your manufacturing business reach out to Chris Lehnes today for a no-obligation consultation.

The 2026 Growth Gap: How Accounts Receivable Factoring Fuels Small Business Success

Factoring: Quick Cash to Kick Off the Year: As we move through 2026, the economic landscape for small businesses is defined by a paradox: opportunity is everywhere, but cash is moving slower than ever. While sectors like high-tech manufacturing and professional services are seeing a resurgence, many entrepreneurs find themselves “asset rich but cash poor.”

You’ve landed the big contract, your team is working overtime, and your sales are climbing. Yet, your bank account doesn’t reflect that success because your capital is trapped in Accounts Receivable (AR). If you’re waiting 30, 60, or even 90 days for clients to pay their invoices, you aren’t just waiting for money—you’re waiting to grow.

This is where Accounts Receivable Factoring becomes a strategic engine for your business.

What is AR Factoring in 2026?

Accounts receivable factoring (or invoice factoring) is not a loan. It is the sale of your outstanding invoices to a third party (a “factor”) at a slight discount in exchange for immediate liquidity.

In 2026, the process has been revolutionized by fintech integrations. Most modern factoring platforms now sync directly with your accounting software (like QuickBooks or Xero), allowing for “one-click” funding that can land in your account within 24 hours.

Why Factoring is the “Secret Weapon” for 2026

While traditional bank loans focus on your credit score and years of profitability, factoring focuses on the creditworthiness of your customers. This makes it an ideal solution for:

Rapidly Growing Startups: When sales outpace your cash reserves.

Seasonal Businesses: Managing the “lumpy” cash flow of peak seasons.

Service Providers: Staffing agencies or consultants who must pay employees weekly but get paid by clients monthly.

3 Ways Factoring Helps You Thrive This Year

1. Turn “Net-90” into “Right Now”

The most significant barrier to growth in 2026 is the “Cash Gap.” If you have $100,000 in open invoices, that’s $100,000 you can’t use to buy inventory, hire talent, or pay for digital marketing. Factoring unlocks up to 90-95% of that value immediately, giving you the agility to say “yes” to new opportunities without checking your balance first.

2. Fuel Expansion Without Adding Debt

In an era of “snagflation”—where mild inflation persists alongside a shifting labor market—loading your balance sheet with high-interest debt can be risky. Because factoring is a purchase of assets, it doesn’t show up as a loan. You are simply accelerating the arrival of money you’ve already earned.

3. Outsourced Credit & Collections

Modern factoring companies do more than just provide cash. They often act as your back-office credit department. In 2026, where business bankruptcies are slightly on the rise, having a partner who vets the credit risk of your potential clients is a massive competitive advantage. They handle the collections, freeing you up to focus on your product.

Is it Right for You?

To help you decide, here is a quick comparison of how factoring stacks up against traditional financing in today’s market:

Feature

AR Factoring

Traditional Bank Loan

Speed

24–48 Hours

3–6 Weeks

Approval Basis

Customer’s Credit

Your Credit & Collateral

Debt

None (Asset Sale)

Increases Liabilities

Flexibility

Scales with Sales

Fixed Credit Limit

Cost

1%–5% Service Fee

Interest Rate + Fees

Final Thoughts: Don’t Let Your Invoices Hold You Back

In 2026, the winners won’t necessarily be the companies with the biggest ideas, but those with the highest liquidity. AR factoring provides a bridge over the cash flow gaps that sink 82% of small businesses. It turns your hard work into immediate fuel.