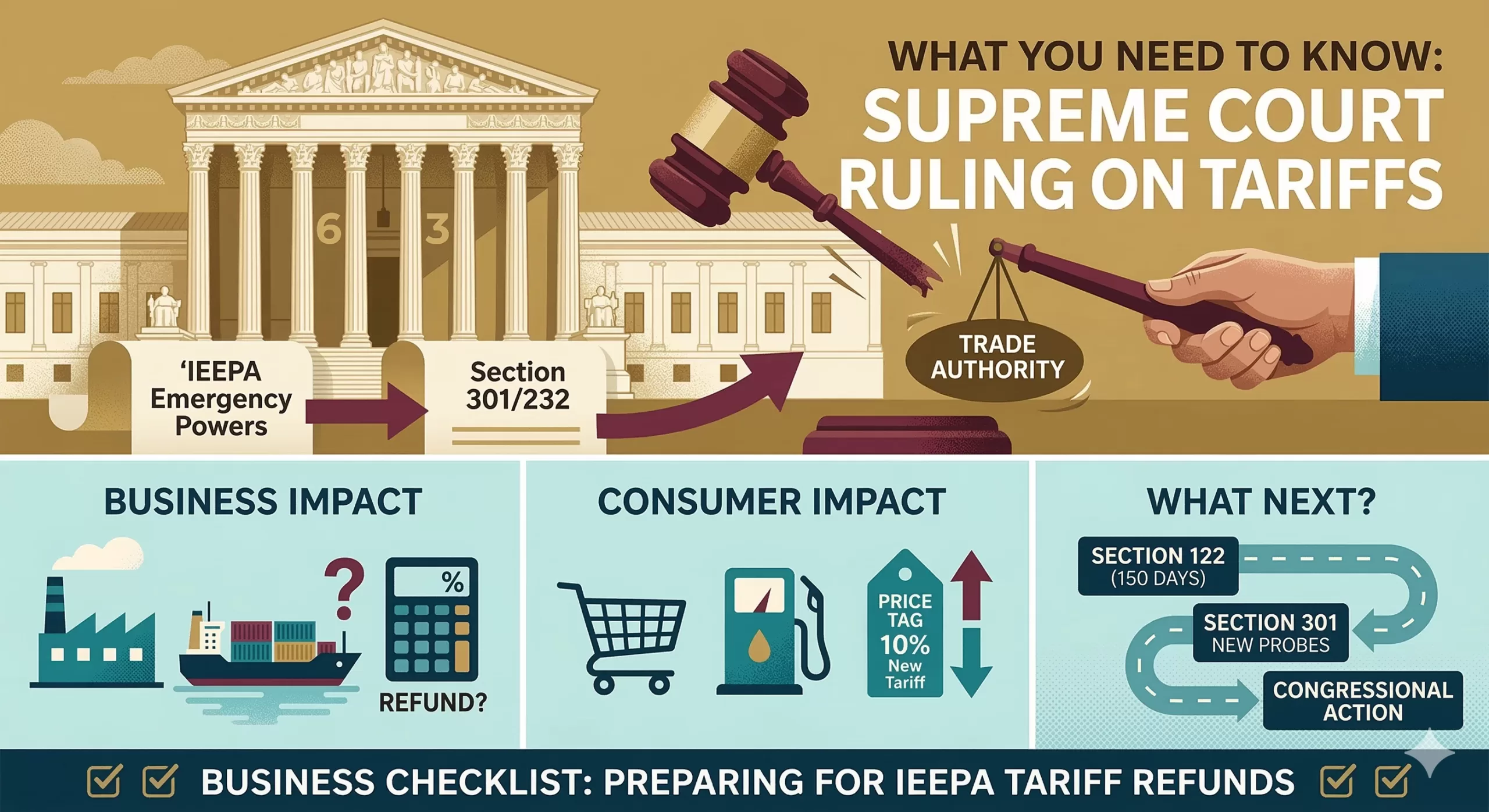

In a landmark decision that has reshaped the landscape of IEEPA Tariffs and American trade policy, the Supreme Court recently issued a ruling in Learning Resources, Inc. v. Trump. The 6-3 decision struck down a series of sweeping tariffs, delivering a significant blow to the administration’s use of emergency powers to regulate the economy.

If you’re a business owner, importer, or simply a consumer wondering why prices are shifting again, here is everything you need to know about this historic ruling about IEEPA Tariffs and what comes next.

The Heart of the Case: IEEPA Tariffs vs. The Taxing Power

The central question before the Court was whether the International Emergency Economic Powers Act (IEEPA) of 1977 gives the President the authority to impose tariffs.

The administration had used IEEPA to levy “reciprocal tariffs” and “trafficking tariffs” on products from China, Canada, and Mexico, arguing that trade imbalances and border security issues constituted a national emergency. However, the Supreme Court ruled that:

- Tariffs are Taxes: Chief Justice John Roberts, writing for the majority, emphasized that the power to tax—which includes tariffs—belongs exclusively to Congress under Article I of the Constitution.

- “Regulate” is not “Tax”: The Court held that IEEPA’s authority to “regulate importation” does not mean the President can unilaterally set tax rates

- The Major Questions Doctrine: The Court applied this principle, stating that if Congress intended to delegate such massive economic power to the Executive Branch, it would have said so clearly and explicitly.

“The Framers did not vest any part of the taxing power in the Executive Branch,” wrote Chief Justice Roberts.

What Happens to the Money? The Refund “Mess”

One of the most pressing questions for businesses is the status of the billions of dollars already collected. Since 2025, the government has gathered an estimated $133 billion to $200 billion in IEEPA-based tariffs.

- Court of International Trade (CIT) Action: Following the Supreme Court ruling, the CIT has ordered U.S. Customs and Border Protection (CBP) to begin preparing for a massive refund process.

- The “Mess” Factor: Justice Brett Kavanaugh noted in his dissent that issuing these refunds will be a “mess.” It remains unclear exactly how and when businesses will see that money returned, as the Supreme Court did not provide a specific roadmap for the refund process

The Administration’s Pivot: Section 122 and 301

If you thought this ruling meant the end of tariffs, think again. Within hours of the decision, the administration began moving to alternative legal authorities:

- Section 122 (Trade Act of 1974): The President implemented a temporary 10% global baseline tariff under this law. However, this power is limited to 150 days and a maximum rate of 15% unless Congress intervenes.

- Section 301 Investigations: The U.S. Trade Representative (USTR) has launched new investigations into “structural excess capacity” and “forced labor” in countries like China and Mexico. These could lead to new, more legally “durable” tariffs in the coming months.

- Section 232 Still Stands: Tariffs on steel and aluminum, which rely on a different national security statute, were not affected by this specific ruling and remain in place.

What This Means for You

For Businesses and Importers

The immediate relief from IEEPA tariffs is a win, but it is replaced by a new 10% surcharge under Section 122. You should:

- Audit your entries: Identify which tariffs you paid were based on IEEPA to prepare for potential refund claims.

- Stay Flexible: The trade environment remains volatile as the administration shifts its legal strategy to avoid future Court losses.

For Consumers

While the invalidation of billions in tariffs sounds like a price drop is coming, the introduction of the new 10% global tariff may offset those savings. Economists expect “trade-weighted” average tariff rates to remain higher than historical norms through 2026.

Summary of Key Impacts

| Feature | IEEPA Tariffs (Struck Down) | Section 122 Tariffs (New) |

| Legal Status | Unconstitutional/Invalid | Currently Active |

| Current Rate | 0% (Effective Feb 20, 2026) | 10% (Effective Feb 24, 2026) |

| Duration | N/A | 150 Days (Expires July 24, 2026) |

| Refunds | Likely, but process is TBD | No |

The Supreme Court has drawn a firm line in the sand regarding the separation of powers. While the President still has significant tools to influence trade, the era of “unbounded” emergency tariffs appears to be over.

Contact Factoring Specialist Chris Lehnes to learn how you can gain early access to tariff refunds