When Trump declared April 2, 2025, as “Liberation Day,” it was supposed to mark the beginning of a manufacturing renaissance. The promise was simple: by slapping aggressive tariffs on foreign goods, the administration would force production back to American soil, revitalize the Rust Belt, and end the “obliteration” of industrial towns.

However, as we move through early 2026, the data tells a different story. Far from a “roaring” comeback, the sector is in a documented retreat. While a recent January uptick in the ISM Manufacturing PMI https://tradingeconomics.com/united-states/business-confidence(52.6) offers a flicker of hope, the broader picture since the 2025 tariff rollout has been one of contraction and “stagflation-lite.”

1. The Numbers Don’t Lie: A Sector in Contraction

Despite the rhetoric, the U.S. manufacturing sector has struggled to keep its head above water over the last year.

Job Losses: Since the tariffs were announced, the sector has shed roughly 72,000 jobs. ADP data from January 2026 shows a further loss of 8,000 manufacturing positions, marking a persistent downward trend.

The PMI Slump: Before the unexpected January bounce, the sector experienced ten consecutive months of contraction. A reading below 50 indicates the industry is shrinking, and for most of 2025, it stayed firmly in the red.

Small Business Strain: For firms with 20 to 49 employees, employment levels have plummeted to their lowest point since 2022. These smaller shops often lack the capital to absorb tariff costs that larger corporations can sometimes weather.

2. The “Tax on Production” Problem

The fundamental issue with broad-based tariffs is that they don’t just tax finished goods; they tax the inputs that American factories need to build things.

“U.S. manufacturing is deeply integrated into global supply chains. When you tax steel, aluminum, and intermediate components, you aren’t just protecting a few domestic mills—you’re raising the cost of every car, appliance, and machine built in America.”

For example, Ford reported incurring nearly $2 billion in annual tariff costs in 2025. When domestic manufacturers face higher costs for their raw materials than their overseas competitors, they become less competitive on the global stage. Instead of hiring, they are forced to raise prices or implement hiring freezes to protect their margins.

3. Uncertainty is the Real Killer

Beyond the direct costs, the volatility of trade policy has created a “permanent risk mode” for supply chains.

Constant Shifts: In just the last few weeks, the administration increased tariffs on South Korea to 25% and threatened a 100% tariff on Canada.

Investment Freeze: Businesses hate uncertainty. Many firms have shifted their budgets away from efficiency-improving capital investments (like new machinery) toward “tariff mitigation” strategies.

The Supreme Court Factor: Markets are currently holding their breath for a SCOTUS ruling on the legality of using the International Emergency Economic Powers Act (IEEPA) to bypass Congress for these trade penalties.

The Bottom Line

The “manufacturing boom” is currently going in reverse. While the administration points to isolated gains in domestic metal production, the downstream effects—higher prices for consumers and job losses in tech-heavy and automotive sectors—are outweighing the benefits.

American factories are resilient, but they are currently caught between the hammer of high interest rates and the anvil of rising input costs. Until trade policy finds a steady, predictable rhythm, the “Golden Age” remains more of a slogan than a reality.

Our Accounts Receivable Factoring program can quickly meet the working capital needs of businesses in the energy industry.

Versant’s underwriting focus is solely on the quality of a company’s accounts receivable, which enables us to rapidly fund businesses which do not qualify for traditional lending.

Company has very large companies as clients which pay their invoices slowly. Our factoring facility will advance cash when invoices are issued allowing company to cover overhead .

Unlock Your Agency’s Growth: The Power of Accounts Receivable Factoring for Digital Marketing Firms

In the world of digital marketing, agility and access to capital are paramount. You land a big client, launch a successful campaign, and the invoices stack up. The problem? Those invoices might not get paid for 30, 60, or even 90 days. This lag, known as the “cash flow gap,” can stifle your growth, prevent you from taking on new projects, and even impact your ability to pay your team.

This is where Accounts Receivable (AR) Factoring comes in—a powerful financial tool that many digital marketing agencies are overlooking.

What is Accounts Receivable Factoring?

Simply put, AR factoring allows your agency to sell its outstanding invoices to a third-party financial company (the “factor”) at a slight discount. In return, you receive an immediate cash advance, typically 70-90% of the invoice value. The factor then collects the full payment from your client when it’s due, and you receive the remaining balance (minus the factoring fee) once the invoice is paid.

How AR Factoring Benefits Digital Marketing Agencies

Here’s why factoring can be a game-changer for your digital marketing business:

1. Immediate Cash Flow Injection

The Problem: You’ve delivered fantastic results, but your client’s payment terms are extended. You need cash now to cover payroll, invest in new software, or launch another campaign.

The Solution: Factoring turns those 30- or 60-day invoices into same-day cash. This immediate liquidity allows you to:

Pay employees and contractors on time.

Invest in new talent or technology.

Cover operational expenses without stress.

Take on larger projects without financial strain.

2. Fueling Growth and Expansion

The Problem: A potential big client comes along, but their project requires a significant upfront investment in ad spend, software licenses, or specialized talent that you don’t currently have liquid cash for.

The Solution: Factoring provides the working capital to pursue ambitious growth opportunities. You can:

Bid on bigger contracts with confidence.

Scale your ad campaigns rapidly.

Expand your service offerings.

Invest in business development to acquire new clients.

3. Reduced Financial Risk and Stress

The Problem: Chasing late payments is time-consuming, awkward, and can strain client relationships. Plus, the risk of non-payment always looms.

The Solution: With factoring, the responsibility of collections often shifts to the factor (depending on the agreement). This means:

Your team can focus on marketing, not collections.

Reduced administrative burden and operational costs.

Mitigated risk of bad debt (especially with “non-recourse factoring”).

The Problem: Traditional bank loans can be hard to secure for young or rapidly growing agencies, often requiring extensive collateral or a lengthy application process.

The Solution: Factoring is not a loan. You’re selling an asset (your invoice), not taking on debt. This makes it an attractive option because:

It doesn’t appear as debt on your balance sheet.

Approval is often based on your clients’ creditworthiness, not just yours.

It’s typically easier and faster to qualify for compared to traditional loans.

It preserves your existing credit lines for other needs.

5. Capitalizing on Seasonal Peaks and Valleys

The Problem: Digital marketing often has seasonal fluctuations. You might have huge projects during peak seasons, followed by leaner periods.

The Solution: Factoring offers flexible funding that scales with your business. You can factor invoices only when you need to, providing an agile solution to manage inconsistent cash flow throughout the year.

Is Factoring Right for Your Agency?

If your digital marketing agency deals with:

Slow-paying clients (even if they’re reliable payers).

Rapid growth that outpaces your cash reserves.

The need for immediate working capital without taking on debt.

A desire to streamline your collections process and reduce administrative overhead.

Then accounts receivable factoring deserves a serious look. It’s a strategic financial tool that can provide the stability and liquidity your agency needs to not just survive, but to truly thrive in the competitive digital landscape.

Factoring Press Release : Versant Funds $5 Million Non-Recourse Factoring Facility to Manufacturer

(January 27, 2026) Versant Funding LLC is pleased to announce that it has funded a $5 Million non-recourse factoring facility to a company that manufactures products for a large customer base which includes one of America’s largest municipalities.

After a transition to Private Equity ownership and management restructuring, our newest client required an infusion of working capital to meet an urgent cash need. While the company has hundreds of customers with AR outstanding, the most efficient way to fund was to factor only the AR of their largest customer, but most factoring companies would not permit 100% customer concentration.

“Versant focuses solely on the credit quality of our clients’ customers,” according to Chris Lehnes, Business Development Officer for Versant Funding, and originator of this financing opportunity. “Since the company’s largest account is a large US city, we were willing to allow 100% customer concentration and meet the client’s short-term funding need.”

About Versant Funding

Versant Funding’s custom Non-Recourse Factoring Facilities have been designed to fill a void in the market by focusing exclusively on the credit quality of a company’s accounts receivable. Versant Funding offers non-recourse factoring solutions to companies with B2B or B2G sales from $100,000 to $30 Million per month. All we care about is the credit quality of the A/R. To learn more contact: Chris Lehnes | 203-664-1535 | chis@chrislehnes.com

Immediate Cash Flow: The manufacturer gains immediate access to working capital by selling its invoices to Versant Funding, significantly improving liquidity.

Mitigation of Customer Concentration Risk: By utilizing non-recourse factoring, Versant Funding assumes the credit risk associated with the manufacturer’s customer, protecting the manufacturer from potential bad debt.

Support for Growth: The increased cash flow will enable the manufacturer to invest in new equipment, expand production, take on larger orders, and capitalize on new market opportunities.

Operational Efficiency: The manufacturer can focus on its core business operations and production, knowing its cash flow is stable and predictable.

Flexible and Scalable: The factoring facility is designed to grow with the manufacturer’s sales, providing ongoing access to capital as their business expands.

Podcast – Small Businesses face numerous challenges, among them is the ability to have access to sufficient working capital to meet the ongoing cash obligations of the business.

While this need can be met by a traditional line of credit for businesses which meet all traditional bank lending criteria, many businesses do not meet those standards and require an alternative.

One such option is accounts receivable factoring. With factoring, a B2B or B2G business can quickly convert their accounts receivable into cash.

Many factoring companies focus exclusively on the credit quality of the customer base and ignore the financial condition of the business and the personal financial condition of the owners.

This works well for businesses with traits such as:

Losses

Rapidly Growing

Highly Leveraged

Customer Concentrations

Out-of-favor Industries

Weak Personal Credit

Character Issues

Listen to this podcast to gain a greater understanding of the types of businesses which can benefit from this form of financing.

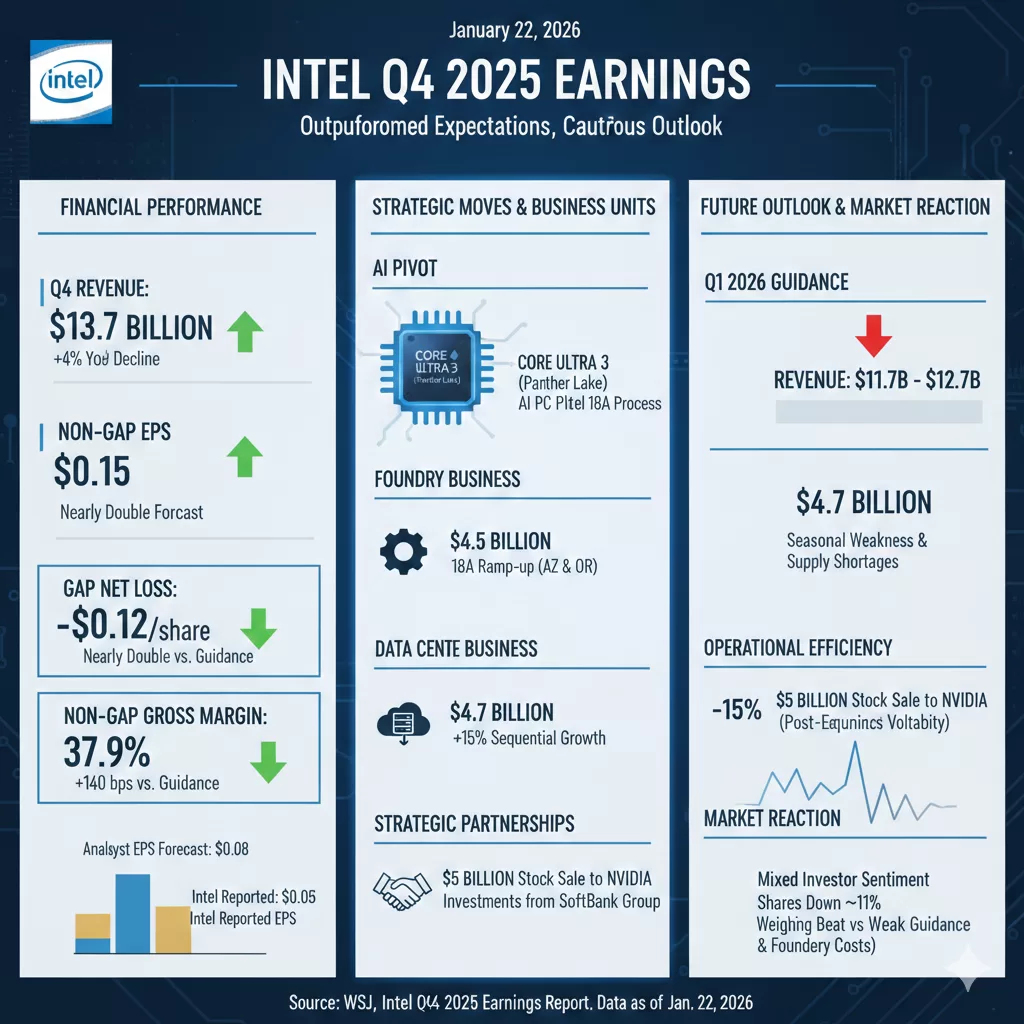

Intel fourth-quarter and full-year 2025 earnings report, as detailed in the Wall Street Journal and other financial outlets, highlights a company in the midst of a massive structural turnaround while grappling with a challenging semiconductor market.

According to the report released on January 22, 2026, Intel outperformed its own guidance and analyst expectations for the quarter, though it remains in a delicate financial position.

Financial Performance (Q4 2025)

Revenue: Intel reported $13.7 billion in Q4 revenue, a 4% decline year-over-year but higher than the forecasted $13.4 billion.

Earnings Per Share (EPS): The company posted a non-GAAP EPS of $0.15, nearly double the $0.08 analysts expected. However, on a GAAP basis, it recorded a net loss of $0.12 per share ($591 million total).

Gross Margin: Non-GAAP gross margin reached 37.9%, exceeding guidance by 140 basis points, driven by higher-than-expected revenue and disciplined spending.

Key Strategic Moves & Business Units

AI Pivot: CEO Lip-Bu Tan emphasized the “essential role of CPUs in the AI era.” Intel launched its Core Ultra Series 3 (Panther Lake), the first AI PC platform built on the advanced Intel 18A process.

Foundry Business: Intel Foundry reported $4.5 billion in revenue. The company is aggressively ramping up its 18A process in Arizona and Oregon to regain manufacturing leadership.

Data Center and AI (DCAI): This segment saw its fastest sequential growth of the decade, rising 15% to $4.7 billion, signaling a potential recovery in server demand.

Strategic Partnerships: The balance sheet was bolstered by a significant $5 billion stock sale to NVIDIA and new investments from SoftBank Group.

Future Outlook

Q1 2026 Guidance: Intel provided a cautious outlook for the coming quarter, projecting revenue between $11.7 billion and $12.7 billion. This lower forecast is attributed to “seasonal weakness” and industry-wide supply shortages, which the company expects to hit a low point in Q1 before improving.

Operational Efficiency: Intel reduced its full-year operating expenses by 15% (down to $16.5 billion) through organizational streamlining.

Market Reaction

Despite the earnings “beat,” investor sentiment remained mixed. Shares experienced volatility—trading down as much as 11% in some sessions following the report—as the market weighed the positive surprise against the weak Q1 2026 guidance and the heavy capital costs associated with the foundry transition.

Few voices carry as much weight as Jamie Dimon’s. So, when the JPMorgan Chase CEO uses words regarding Fed independence like “absolutely critical” and warns of “adverse consequences,” the markets—and the public—should probably lean in.

His recent comments regarding political interference with the Federal Reserve aren’t just about high-level banking theory; they are a direct warning about the stability of the American economy and the cost of living for every citizen.

The “Referee” of the Economy

To understand Dimon’s concern, you have to look at the Federal Reserve’s role. Think of the Fed as the “referee” of the economy. Their job is to manage inflation and employment by adjusting interest rates. For this to work, they have to be able to make tough, often unpopular decisions—like raising rates to cool down inflation—without worrying about whether those moves will cost a politician an election.

As Dimon pointed out during a recent earnings call, “The independence of the Fed is absolutely critical.” Why? Because the moment the public or investors believe the Fed is taking orders from the White House, trust in the U.S. dollar and the stability of our markets begins to crumble.

The Irony of Political Pressure

The current tension stems from persistent political pressure on Fed Chair Jerome Powell to lower interest rates. The logic from the political side is simple: lower rates usually mean more borrowing, more spending, and a short-term boost to the economy.

However, Dimon warns that this pressure can backfire spectacularly. He noted that “playing around with the Fed could have adverse consequences, the absolute opposite of what you might be hoping for.”

Here is the paradox: If the Fed lowers rates because a politician told them to, rather than because the data supports it, investors will fear that inflation is going to spiral out of control. To protect themselves, those same investors will demand higher returns on government bonds. This drives “long-term” interest rates up—the very rates that determine what you pay for a mortgage, a car loan, or a credit card balance.

By trying to force rates down for a political win, leaders could inadvertently push rates higher for the average consumer.

Why This Matters Now

Dimon’s warning comes at a delicate time. Between the potential for new tariffs (which can drive up prices) and a growing federal deficit, the U.S. economy is walking a tightrope.

If the Fed loses its autonomy, the “soft landing” we’ve all been hoping for—where inflation cools without a major recession—becomes much harder to achieve. As Dimon noted, asset prices are currently priced for perfection, and the margin for error is slim.

The Bottom Line

Jamie Dimon isn’t just defending a colleague in Jerome Powell; he is defending the institutional credibility that keeps the global financial system running.

In a world of hyper-partisan politics, some things need to remain “above the fray.” The Federal Reserve is one of them. If the independence of the central bank is compromised, we won’t just see it in the headlines—we’ll feel it in our monthly bills.

*** What do you think?Is political oversight of the Fed necessary for accountability, or is Jamie Dimon right that independence is the only way to keep the economy stable? Let’s discuss in the comments.

The Inflation “Split Screen”: What December’s CPI Numbers Really Mean

Inflation Stable. The latest data is in, and it paints a picture of an economy caught between cooling pressures and political friction. In December, consumer prices rose 2.7% from a year earlier—holding steady from November and landing exactly where economists predicted.

While the “headline” number suggests stability, the story beneath the surface is much more complex. Here are the key takeaways from the final inflation report of 2025.

1. Stability Amidst the Noise

For the second month in a row, inflation has leveled off at 2.7%. Meanwhile, “Core CPI” (which strips out volatile food and energy costs) rose 2.6%.

Interestingly, these numbers came in slightly better than the 2.8% core increase some experts feared. This suggests that despite the introduction of steep tariffs earlier in 2025, businesses haven’t yet passed the full weight of those costs onto consumers. However, the “last mile” of the journey back to the Fed’s 2% target remains stubbornly out of reach.

2. A Cloud of Data Uncertainty

This report is the first “clean” look at inflation we’ve had in months. Following a government shutdown last fall, the Labor Department had to rely on technical workarounds to fill data gaps.

The “Payback” Effect: Many economists believe November’s figures may have been artificially low due to those data collection issues.

The Verdict: While December’s numbers didn’t spike as much as feared, they likely reflect a correction for the missing data from previous months.

3. The Fed’s High-Stakes Balancing Act

The Federal Reserve is currently navigating a “split screen” economy. On one hand, growth remains solid; on the other, the labor market has cooled significantly. In fact, 2025 saw the lowest pace of job growth since 2003 (excluding major recessions).

The Fed cut rates three times at the end of 2025 to support the job market, but officials are now divided. With inflation still above 2%, some are hesitant to keep cutting—especially as they watch for the inflationary impact of the One Big Beautiful Bill Act and ongoing investments in AI.

4. Politics vs. Policy

Perhaps the most unusual backdrop to this report is the unprecedented political pressure on independent agencies.

The Labor Department: Its commissioner was fired in August amidst claims of “rigged” numbers.

The Fed: Chair Jerome Powell recently alleged that the administration has used threats of criminal prosecution to pressure the board into lowering interest rates.

What’s Next?

As we head into 2026, all eyes are on January and February. This is traditionally when businesses reset their pricing for the year. Whether they will hike prices to account for tariffs and tax-cut-driven demand remains the big question.

For now, the “meandering path” toward lower inflation continues, but with a cooling job market and political volatility, the road ahead looks anything but smooth.

Cimarron is a novel by Edna Ferber, published in April 1930 and based on development in Oklahoma after the Land Rush. The book was adapted into a critically acclaimed film of the same name, released in 1931 through RKO Pictures. The story was again adapted for the screen by Metro-Goldwyn-Mayer and was released in 1960, to meager success.

The Oklahoma Land Rush (also called the Oklahoma Land Race and Cherokee StripLand Run) plays a pivotal role in both the novel and film adaptations. “Manifest destiny” and the desperation of the settlers involved in the rush provides the opening drama and sets the stage for the twists and turns in the book. Every settler is desperate to stake his claim on the best piece of land (near water).

Photograph of the 1893 OklahomaLand Rush, depicted in Ferber’s book and films.

Cimarron involves two land runs. The first, for the Unassigned Lands, occurred on April 22, 1889. The second, for the Cherokee Outlet (commonly called the Cherokee Strip) occurred in 1893. The piece of land in question had been allotted to the Cherokee Nation as part of the 1828 Treaty of New Echota, while the rest of the Oklahoma Territory had been opened to settlers. As commerce grew across the area of Kansas and Oklahoma, cattlemen became increasingly annoyed by the presence of the Cherokee on prime land that they wanted to use to drive cattle from northern ranches to Texas. Some of this annoyance with the Native people can be attributed to the decision made by the Cherokees to side with the Confederate States of America during the American Civil War. In the 1880s, the government attempted to lease the land for cattle ranching, but the Native Americans refused. Eventually, the Cherokee people did sell the land to the government.

Throughout the remaining years of the 1880s various cattle associations and ranches fought over the land. Disputes even turned deadly, as large cattle companies and small ranchers both claimed the land as their own. This eventually led to a ban on cattle ranching in the area, and in 1893 the land, 58 miles (93 km) wide by 225 miles (362 km) long, was opened to homesteaders. The land was divided into 42,000 claims, and each homesteader had to literally stake (put a stake with a white flag attached) their claim, and pick up a certificate back at the starting place. Nearly 100,000 people arrived for the rush, and over half of them would be sent back home after the day was through.

Novel

Cover from a 1930 edition.

Cimarron derives its name from the Cimarron Territory. The Cimarron Territory was an unrecognized name for the No Man’s Land, an unsettled area of the West and Midwest, especially lands once inhabited by Native American tribes such as the Cherokee and Sioux. In 1886 the government declared such lands open to settlement. At the time of the novel’s opening, Oklahoma is one such “Cimarron Territory,” though in actuality the historical setting of the novel is somewhere in the Cherokee Outlet, also known as the Cherokee Strip, and probably the city of Guthrie, Oklahoma.

The novel is set in the Oklahoma of the late nineteenth and early twentieth centuries. It follows the lives of Yancey and Sabra Cravat, beginning with Yancey’s tale of his participation in the 1893 land rush. They emigrate from Wichita, Kansas, to the fictional town of Osage, Oklahoma with their son Cim and—unknowingly—a black boy named Isaiah. In Osage, the Cravats print their newspaper, the Oklahoma Wigwam, and build their fortune amongst Indian disputes, outlaws, and the discovery of oil in Oklahoma.

Upon its publication, Cimarron was a sensation in America and came to epitomize an era in American history. It was the best selling novel of 1930,[1] as it provided readers an outlet to escape their present suffering in the Great Depression. This novel became Ferber’s third successful novel and paved the way for many more Ferber-penned historical epics, and it was published as an Armed Services Edition during WWII.

While it became seen as a triumphant feminist story detailing Sabra Cravat’s growth from a traditional American housewife into a successful leader and politician, Ferber stated in her autobiography, A Peculiar Treasure, that the novel was originally intended as a satirical criticism of American womanhood and American sentimentality.[2][3] Throughout the novel, Sabra’s practice of imperial domesticity can be seen in her attempts to “civilize” Native Americans by forcing them to adopt white values, and her fixation on expanding her own sphere of influence, which as a woman, was traditionally her home.[4]

The character of Yancey Cravat is based on Temple Lea Houston, last child of Texas icon Sam Houston. Temple Houston was a brilliant trial lawyer known for his flamboyant courtroom theatrics. He was also a competent gunfighter who killed at least one man in a stand-up shootout.

Full Text of Cimarron

VINTAGE MOVIE CLASSICS

Vintage Movie Classics spotlights classic lms that have stood the test of time, now rediscovered through the publication of the novels on which they were based. OceanofPDF.com

Only the more fantastic and improbable events contained in this book are true. There is no attempt to set down a literal history of Oklahoma. All the characters, the towns, and many of the happenings contained herein are imaginary. But through reading the scant available records, documents, and histories (including the Oklahoma State Historical Library collection) and through many talks with men and women who have lived in Oklahoma since the day of the Opening, something of the spirit, the color, the movement, the life of that incredible commonwealth has, I hope, been caught. Certainly the Run, the Sunday service in the gambling tent, the death of Isaiah and of Arita Red Feather, the catching of the can of nitroglycerin, many of the shooting a rays, most descriptive passages, all of the oil phase, and the Osage Indian material complete—these are based on actual happenings. In many cases material entirely true was discarded as un t for use because it was so melodramatic, so absurd as to be too strange for the realm of ction. There is no city of Osage, Oklahoma. It is a composite of, perhaps, ve existent Oklahoma cities. The Kid is not meant to be the notorious Billy the Kid of an earlier day. There was no Yancey Cravat—he is a blending of a number of dashing Oklahoma gures of a past and present day. There is no Sabra Cravat, but she exists in a score of bright-eyed, white-haired, intensely interesting women of sixty- ve or thereabouts who told me many strange things as we talked and rocked on an Oklahoma front porch (tree-shaded now). Anything can have happened in Oklahoma. Practically everything has.

EDNA FERBER

1

All the Venables sat at Sunday dinner. All those handsome inbred Venable faces were turned, enthralled, toward Yancey Cravat, who was talking. The combined e ect was almost blinding, as of incandescence; but Yancey Cravat was not bedazzled. A sun surrounded by lesser planets, he gave out a radiance so powerful as to dim the luminous circle about him. Yancey had a disconcerting habit of abruptly concluding a meal— for himself, at least—by throwing down his napkin at the side of his plate, rising, and striding about the room, or even leaving it. It was not deliberate rudeness. He ate little. His appetite satis ed, he instinctively ceased to eat; ceased to wish to contemplate food. But the Venables sat hours at table, leisurely shelling almonds, sipping sherry; Cousin Dabney Venable peeling an orange for Cousin Bella French Vian with the absorbed concentration of a sculptor molding his clay. The Venables, dining, strangely resembled one of those fertile and dramatic family groups portrayed lolling unconventionally at meat in the less spiritual of those Biblical canvases that glow richly down at one from the great gallery walls of Europe. Though their garb was sober enough, being characteristic of the time—1889—and the place —Kansas—it yet conveyed an impression as of purple and scarlet robes enveloping these gracile shoulders. You would not have been surprised to see, moving silently about this board, Nubian blacks in loincloths, bearing aloft golden vessels piled with exotic fruits or steaming with strange pasties in which nightingales’ tongues gured

prominently. Blacks, as a matter of fact, did move about the Venable table, but these, too, wore the conventional garb of the servitor. This branch of the Venable family tree had been transplanted from Mississippi to Kansas more than two decades before, but the mid-west had failed to set her bourgeois stamp upon them. Straitened though it was, there still obtained in that household, by some genealogical miracle, many of those charming ways, remotely Oriental, that were of the South whence they had sprung. The midday meal was, more often than not, a sort of tribal feast at which sprawled hosts of impecunious kin, mysteriously sprung up at the sound of the dinner bell and the scent of baking meats. Unwilling émigrés, war ruined, Lewis Venable and his wife Felice had brought their dear customs with them into exile, as well as the superb mahogany oval at which they now sat, and the war-salvaged silver which gave elegance to the Wichita, Kansas, board. Certainly the mahogany had su ered in transit; and many of their Southern ways, transplanted to Kansas, seemed slightly silly—or would have, had they not been tinged with pathos. The hot breads of the South, heaped high at every meal, still wrought alimentary havoc. The frying pan and the deep-fat kettle (both, perhaps, as much as anything responsible for the tragedy of ’64) still spattered their deadly fusillade in this household. Indeed, the creamy pallor of the Venable women, so like that of a magnolia petal in their girlhood, and tending so surely toward the ocherous in middle age, was less a matter of pigment than of liver. Impecunious though the family now was, three or four negro servants went about the house, soft-footed, slack, charming. “Rest yo’ wrap?” they suggested, velvet voiced and hospitable, as you entered the wide hallway that was at once so bare and so cluttered. And, “Beat biscuit, Miss Adeline?” as they pro ered a fragrant plate. Even that Kansas garden was of another latitude. Lean hounds drowsed in the sun-drenched untidiness of the doorway, and that untidiness was hidden and transformed by a miracle of color and scent and bloom. Here were passion ower and wistaria and even Bougainvillea in season. Honeysuckle gave out its swooning sweetness. In the early spring lilies of the valley thrust the phantom

green of their spears up through the dead brown banking the lilac bushes. That coarse vulgarian, the Kansas sun ower, was a thing despised of the Venables. If one so much as showed its broad face among the scented élégantes of that garden it su ered instant decapitation. On one occasion Felice Venable had been known to ruin a pair of very ne-tempered embroidery scissors while impetuously acting as headsman. She had even been heard to bewail the absence of Spanish moss in this northerly climate. A neighboring midwest matron, mi ed, resented this. “But that’s a parasite! And real creepy, almost. I was in South Carolina and saw it. Kind of oating, like ghosts. And no earthly good.” “Do even the owers have to be useful in Kansas?” drawled Felice Venable. She was not very popular with the bustling wives of Wichita. They resented her ru ed and trailing white wrappers of cross-barred dimity; her pointed slippers, her arched instep, her indi erence to all that went on outside the hedge that surrounded the Venable yard; they resented the hedge itself, symbol of exclusiveness in that open-faced Kansas town. Sheathed in the velvet of Felice Venable’s languor was a sharp-edged poniard of wit inherited from her French forbears, the old Marcys of St. Louis; Missouri fur traders of almost a century earlier. You saw the Marcy mark in the black of her still bountiful hair, in the curve of the brows above the dark eyes—in the dark eyes themselves, so alive in the otherwise immobile face. As the family now sat at its noonday meal it was plain that while two decades of living in the Middle West had done little to quicken the speech or hasten the movements of Lewis Venable and his wife Felice (they still “you-alled”; they declared to goodness; the eighteenth letter of the alphabet would forever be ah to them) it had made a noticeable di erence in the younger generation. Up and down the long table they ranged, sons and daughters, sons-in-law and daughters-in-law; grandchildren; remoter kin such as visiting nieces and nephews and cousins, o shoots of this far- ung family. As the more northern-bred members of the company exclaimed at the tale they now were hearing you noted that their vowels were

shorter, their diction more clipped, the turn of the head, the lift of the hand less leisurely. In all those faces there was a resemblance, one to the other. Perhaps the listening look which all of them now wore served to accentuate this. It was late May, and unseasonably hot for the altitude. Then, too, there had been an early pest of moths and June ies this spring. High above the table, and directly over it, on a narrow board suspended by rods from the lofty ceiling sat perched Isaiah, the little black boy. With one hand he clung to the side rods of his precarious roost; with the other he wielded a shoo y of feathery asparagus ferns cut from the early garden. Its soft susurrus as he swished it back and forth was an obbligato to the music of Yancey Cravat’s golden voice. Clinging thus aloft the black boy looked a simian version of one of Raphael’s ceilinged angels. His round head, fuzzed with little tight tufts, as of woolly astrakhan through which the black of his poll gleamed richly, was cocked at an impish angle the better to catch the words that owed from the lips of the speaker. His eyes, popping with excitement, were xed in an entrancement on the great lounging gure of Yancey Cravat. So bewitched was the boy that frequently his hand fell limp and he forgot altogether his task of bestirring with his verdant fan the hot moist air above the food-laden table. An impatient upward glance from Felice Venable’s darting black eyes, together with a sharply admonitory “Ah-saiah!” would set him to swishing vigorously until the enchantment again stayed his arm. The Venables saw nothing untoward in this remnant of Mississippi feudalism. Dozens of Isaiah’s forbears had sat perched thus, bestirring the air so that generations of Mississippi Venables might the more agreeably sup and eat and talk. Wichita had rst beheld this phenomenon aghast; and even now, after twenty years, it was a subject for local tongue waggings. Yancey Cravat was talking. He had been talking for the better part of an hour. This very morning he had returned from the Oklahoma country—the newly opened Indian Territory where he had made the Run that marked the settling of this vast tract of virgin land known colloquially as the Nation. Now, as he talked, the faces of the others

had the rapt look of those who listen to a saga. It was the look that Jason’s listeners must have had, and Ulysses’; and the eager crowd that gathered about Francisco Vasquez de Coronado before they learned that his search for the Seven Cities of Cibolo had been in vain. The men at table leaned forward, their hands clasped rather loosely between their knees or on the cloth before them, their plates pushed away, their chairs shoved back. Now and then the sudden white ridge of a hardset muscle showed along the line of a masculine jaw. Their eyes were those of men who follow a game in which they would fain take part. The women listened, a little frightened, their lips parted. They shushed their children when they moved or whimpered, or, that failing, sent them, with a half-tender, half-admonitory slap behind, to play in the sunny dooryard. Sometimes a woman’s hand reached out possessively, remindingly, and was laid on the arm or the hand of the man seated beside her. “I am here,” the hand’s pressure said. “Your place is with me. Don’t listen to him like that. Don’t believe him. I am your wife. I am safety. I am security. I am comfort. I am habit. I am convention. Don’t listen like that. Don’t look like that.” But the man would shake o the hand, not roughly, but with absent-minded resentment. Of all that circlet of faces, linked by the enchantment of the tale now being unfolded before them, there stood out lambent as a ame the face of Sabra Cravat as she sat there at table, her child Cim in her lap. Though she, like her mother Felice Venable, was de nitely of the olive-skinned type, her face seemed luminously white as she listened to the amazing, incredible, and slightly ridiculous story now being unfolded by her husband. It was plain, too, that in her, as in her mother, the strain of the pioneering French Marcys was strong. Her abundant hair was as black, and her eyes; and the strong brows arched with a swooping curve like the twin scimitars that hung above the replace in the company room. Sabra was secretly ashamed of her heavy brows and given to surveying them disapprovingly in her mirror while running a fore nger (slightly moistened by her tongue) along their sable curves. For the rest,

there was something more New England than Southern in the directness of her glance, the quick turn of her head, the briskness of her speech and manner. Twenty-one now, married at sixteen, mother of a four-year-old boy, and still in love with her picturesque giant of a husband, there was about Sabra Cravat a bloom, a glow, sometimes seen at their exquisite and transitory time in a woman’s life when her chemical, emotional, and physical make-up attains its highest point and fuses. It was easy to trace the resemblance, both in face and spirit, between this glowing girl and the sallow woman at the foot of the table. But to turn from her to old Lewis Venable was to nd one’s self ba ed by the mysteries of paternity. Old Lewis Venable was not old, but aged; a futile, fumbling, gentle man, somewhat hag-ridden and rendered the more unvital by malaria. Face and hands had a yellow ivory quality born of generations subjected to hot breads, lowlands, bad liver, port wine. To say nothing of a resident unexplored bullet somewhere between the third and fth ribs, got at Murfreesboro as a member of Stanford’s Battery, Heavy Artillery, long long before Roentgen had conceived an eye like God’s. Lewis Venable, in his armchair at the head of the table, was as spellbound as black Isaiah in his high perch above it. Curiously enough, even the boy Cim had listened, or seemed to listen, as he sat in his mother’s lap. Sabra had eaten her dinner over the child’s head in absent-minded bites, her eyes always on her husband’s face. She rarely had had to say, “Hush, Cim, hush!” or to wrest a knife or fork or forbidden tidbit from his clutching ngers. Perhaps it was the curiously musical quality of the story-teller’s voice that lulled him. Sabra Venable’s disgruntled suitors had said when she married Yancey Cravat, a stranger, mysterious, out of Texas and the Cimarron, that it was his voice that had bewitched her. They were in a measure right, for though Yancey Cravat was verbose, frequently even windy, and though much that he said was dry enough in actual content, he had those priceless gifts of the born orator, a vibrant and exible voice, great sweetness and charm of manner, an hypnotic eye, and the power of making each listener feel

that what was being said was intended for his ear alone. Something of the charlatan was in him, much of the actor, a dash of the fanatic. Any tale told by Yancey Cravat was likely to contain enchantment, incredibility (though this last was not present while he was telling it), and a tinge of the absurd. Yancey himself, even at this early time, was a bizarre, glamorous, and slightly mythical gure. No room seemed big enough for his gigantic frame; no chair but dwindled beneath the breadth of his shoulders. He seemed actually to loom more than his six feet two. His black locks he wore overlong, so that they curled a little about his neck in the manner of Booth. His cheeks and forehead were, in places, deeply pitted, as with the pox. Women, perversely enough, found this attractive. But rst of all you noted his head, his huge head, like a bu alo’s, so heavy that it seemed to loll of its own weight. It was with a shock of astonishment that you remarked about him certain things totally at variance with his bulk, his virility, his appearance of enormous power. His mouth, full and sensual, had still an expression of great sweetness. His eyelashes were long and curling, like a beautiful girl’s, and when he raised his heavy head to look at you, beneath the long black locks and the dark lashes you saw with something of bewilderment that his eyes were a deep and unfathomable ocean gray. Now, in the course of his story, and under the excitement of it, he left the table and sprang to his feet, striding about and talking as he strode. His step was amazingly light and graceful for a man of his powerful frame. Fascinated, you saw that his feet were small and arched like a woman’s, and he wore, even in this year of 1889, Texas star boots of ne soft exible calf, very high heeled, thin soled, and ornamented with cunningly wrought gold stars around the tops. His hands, too, were disproportionate to a man of his stature; slim, pliant, white. He used them as he talked, and the eye followed their movements bewitched. For the rest, his costume was a Prince Albert of ne black broadcloth whose skirts swooped and spread with the vigor of his movements; a pleated white shirt, soft and exquisite material; a black string tie; trousers tucked into the gay boot-tops; and, always, a white felt hat, broad-brimmed and

rolling. On occasion he simply blubbered Shakespeare, the Old Testament, the Odyssey, the Iliad. His speech was spattered with bits of Latin, and with occasional Spanish phrases, relic of his Texas days. He attered you with his ne eyes; he bewitched you with his voice; he mesmerized you with his hands. He drank a quart of whisky a day; was almost never drunk, but on rare occasions when the liquor fumes bested him he would invariably select a hapless victim and, whipping out the pair of mother-o’-pearl-handled six- shooters he always wore at his belt, would force him to dance by shooting at his feet—a pleasing fancy brought with him from Texas and the Cimarron. Afterward, sobered, he was always lled with shame. Wine, he quoted sadly, is a mocker, strong drink is raging. Yancey Cravat could have been (in fact was, though most of America never knew it) the greatest criminal lawyer of his day. It was said that he hypnotized a jury with his eyes and his hands and his voice. His law practice yielded him nothing, or less than that, for being sentimental and melodramatic he usually found himself out of pocket following his brilliant and successful defense of some Dodge City dance-hall girl or roistering cowboy whose six-shooter had been pointed the wrong way. His past, before his coming to Wichita, was clouded with myths and surmises. Gossip said this; slander whispered that. Rumor, romantic, unsavory, fantastic, shifting and changing like clouds on a mountain peak, oated about the head of Yancey Cravat. They say he has Indian blood in him. They say he has an Indian wife somewhere, and a lot of papooses. Cherokee. They say he used to be known as “Cimarron” Cravat, hence his son’s name, corrupted to Cim. They say his real name is Cimarron Seven, of the Choctaw Indian family of Sevens; he was raised in a tepee; a wickiup had been his bedroom, a blanket his robe. It was known he had been one of the early Boomers who followed the banner of the picturesque and splendidly mad David Payne in the rst wild dash of that adventurer into Indian Territory. He had dwelt, others whispered, in that sinister strip, thirty-four miles wide and almost two hundred miles long, called No-Man’s-Land as early as 1854, and, later, known as the Cimarron, a Spanish word meaning wild or unruly.

Here, in this strange unowned empire without laws and without a government, a paradise for horse thieves, murderers, desperadoes it was rumored he had spent at least a year (and for good reason). They said the evidences of his Indian blood were plain; look at his skin, his hair, his manner of walking. And why did he protest in his newspaper against the government’s treatment of those dirty, thieving, lazy, good-for-nothing wards of a bene cent country! As for his newspaper—its very name was a scandal: The Wichita Wigwam. And just below this: All the news. Any Scandal Not Libelous. Published Once a Week if Convenient. For that matter, who ever heard of a practising lawyer who ran a newspaper at the same time? Its columns were echoes of his own thundering oratory in the courtroom or on the platform. He had started his paper in opposition to the old established Wichita Eagle. Wichita, roaring, said he should have called his sheet the Rooster. The combination law and newspaper o ce itself was a jumble and welter of pied type, unopened exchanges, boiler plate, legal volumes, paste pots, loose tobacco, old coats, and racing posters. Wichita, professing scorn of the Wigwam, read it. Wichita perused his maiden editorial entitled Shall the Blue Blood of the Decayed South Poison the Red Blood of the Great Middle West? and saw him, two months later, carry o in triumph as his bride Sabra Venable, daughter of that same Decay; Sabra Venable, whose cerulean stream might have mingled with the more vulgarly sanguine life uid of any youth in Wichita. In spite of the garden hedge, the parental pride, the arched insteps, the colored servants, and the general air of what-would-you- varlet that pervaded the Venable household at the entrance of a local male a-wooing, Sabra Venable, at sixteen, might have had her pick of the red-blooded lads of Kansas, all the way from Salina to Win eld. Not to mention more legitimate suitors of blue-blooded stock up from the South, such as Dabney Venable himself, Sabra’s cousin, who resembled at once Lafayette and old Lewis, even to the premature silver of his hair, the length of the ne, dolichocephalic, slightly decadent head, and the black stock at sight of which Wichita gasped. When, from among all these eligibles, Sabra had chosen the romantic but mysterious Cravat, Wichita mothers of

marriageable daughters felt themselves revenged of the Venable airs. Strangely enough, the marriageable daughters seemed more resentful than ever, and there was a noticeable falling o in the number of young ladies who had been wont to drop around at the Wigwam o ce with notices of this or that meeting or social event to be inserted in the columns of the paper. During the course of the bountiful meal with which the Venable table was spread Yancey Cravat had eaten almost nothing. Here was an audience to his liking. Here was a tale to his taste. His story, wild, unbelievable, yet true, was of the opening of the Oklahoma country; of a wilderness made populous in an hour; of cities numbering thousands literally sprung up overnight, where the day before had been only prairie, coyotes, rattlesnakes, red clay, scrub oak, and an occasional nester hidden in the security of a weedy draw. He had been a month absent. Like thousands of others he had gone in search of free land and a fortune. Here was an empire to be had for the taking. He talked, as always, in the highfalutin terms of the speaker who is ever conscious of his audience. Yet, fantastic as it was, all that he said was woven of the warp and woof of truth. Whole scenes, as he talked, seemed to be happening before his listeners’ eyes.

2

Coat tails swishing, eyes ashing, arms waving, voice soaring. “Folks, there’s never been anything like it since Creation. Creation! Hell! That took six days. This was done in one. It was History made in an hour—and I helped make it. Thousands and thousands of people from all over this vast commonwealth of ours” (he talked like that) “traveled hundreds of miles to get a bare piece of land for nothing. But what land! Virgin, except when the Indians had roamed it. ‘Lands of lost gods, and godlike men!’ They came like a procession—a crazy procession—all the way to the Border, covering the ground as fast as they could, by any means at hand— scrambling over the ground, pushing and shoving each other into the ditches to get there rst. God knows why—for they all knew that once arrived there they’d have to wait like penned cattle for the ring of the signal shot that opened the promised land. As I got nearer the line it was like ants swarming on sugar. Over the little hills they came, and out of the scrub-oak woods and across the prairie. They came from Texas, and Arkansas and Colorado and Missouri. They came on foot, by God, all the way from Iowa and Nebraska! They came in buggies and wagons and on horseback and muleback. In prairie schooners and ox carts and carriages. I saw a surrey, honey colored, with a fringe around the top, and two elegant bays drawing it, still stepping high along those rutted clay roads as if out for a drive in the Presidio. There was a black boy driving it, brass buttons and all, and in the back seat was a dude in a light tan coat and a cigar in his mouth and a diamond in his shirtfront; and a woman beside him in a big hat and a pink dress laughing and urging

the horses along the red dust that was halfway up to the wheel spokes and t to choke you. They had driven like that from Denver, damned if they hadn’t. I met up with one old homesteader by the roadside—a face dried and wrinkled as a nutmeg—who told me he had started weeks and weeks before, and had made the long trip as best he could, on foot or by rail and boat and wagon, just as kind- hearted people along the way would pick him up. I wonder if he ever got his piece of land in that savage rush—poor old devil.” He paused a moment, perhaps in retrospect, perhaps cunningly to whet the appetites of his listeners. He wrung a breathless, “Oh, Yancey, go on! Go on!” from Sabra. “Well, the Border at last, and it was like a Fourth of July celebration on Judgment Day. The militia was lined up at the boundary. No one was allowed to set foot on the new land until noon next day, at the ring of the guns. Two million acres of land were to be given away for the grabbing. Noon was the time. They all knew it by heart. April twenty-second, at noon. It takes generations of people hundreds of years to settle a new land. This was going to be made livable territory over night—was made—like a miracle out of the Old Testament. Compared to this, the Loaves and the Fishes and the parting of the Red Sea were nothing—mere tricks.” “Don’t be blasphemous, Yancey!” spoke up Aunt Cassandra Venable. Cousin Dabney Venable tittered into his stock. “A wilderness one day—except for an occasional wandering band of Indians—an empire the next. If that isn’t a modern miracle——” “Indians, h’m?” sneered Cousin Dabney, meaningly. “Oh, Dabney!” exclaimed Sabra, sharply. “Why do you interrupt? Why don’t you just listen!” Yancey Cravat raised a pacifying hand, but the great bu alo head was lowered toward Cousin Dabney, as though charging. The sweetest of smiles wreathed his lips. “It’s all right, Sabra. Let Cousin Dabney speak. And why not? Un cabello haze sombra.” Cousin Dabney’s ivory face ushed a delicate pink. “What’s that, Cravat? Cherokee talk?”

“Spanish, my lad. Spanish.” A little moment of silent expectation. Yancey did not explain. A plump and pretty daughter-in-law (not a Venable born) put the question. “Spanish, Cousin Yancey! I declare! Whatever in the world does it mean? Something romantic, I do hope.” “Not exactly. A Spanish proverb. It means, literally ‘Even a hair casts a shadow.’ ” Another second’s silence. The pretty daughter-in-law’s face became quite vacuous. “Oh. A hair—but I don’t see what that’s got to do with …” The time had come for Felice Venable to take charge. Her drawling, querulous voice dripped its slow sweetness upon the bitter feud that lay, a poisonous pool, between the two men. “Well, I must say I call it downright bad manners, I do indeed. Here we all are with our ears just a- apping to hear the rst sound of the militia guns at high noon on the Border, and here’s Cousin Jouett Goforth all the way up from Louisiana the rst time in fteen years, and just a-quivering with curiosity, and what do we hear but chit-chat about Spanish proverbs and shadows.” She broke o abruptly, cast a lightning glance aloft, and in a tone that would have been called a shout had it issued from the throat of any but a Venable, said, “Ah-saiah!” The black boy’s shoo- y, hanging limp from his inert hand, took up its frantic swishing. The air was cleared. The gures around the table relaxed. Their faces again turned toward Yancey Cravat. Yancey glanced at Sabra. Sabra’s lips puckered into a phantom kiss. They formed two words, unseen, unheard by the rest of the company. “Please, darling.” “Cede Deo,” said Yancey, with a little bow to her. Then, with a still slighter bow, he turned to Cousin Dabney. “ ‘Let there be no strife, I pray thee, between thee and me.’ You may not recognize that either, Dabney. It’s from the Old Testament.” Cousin Dabney Venable ran a nger along the top of his black silk stock, as though to ease his throat.

With a switch of his coat tails Yancey was o again, pausing only a moment at the sideboard to toss o three ngers of Spanish brandy, like burning liquid amber. He patted his lips with his ne linen handkerchief. “I’ve tasted nothing like that in a month, I can tell you. Raw corn whisky t to tear your throat out. And as for the water! Red mud. There wasn’t a drink of water to be had in the town after the rst twenty-four hours. There we were, thousands and thousands of us, milling around the Border like cattle, with the burning sun baking us all day, nowhere to go for shade, and the thick red dust clogging eyes and nose and mouth. No place to wash, no place to sleep, nothing to eat. Queer enough, they didn’t seem to mind. Didn’t seem to notice. They were feeding on a kind of crazy excitement, and there was a wild light in their eyes. They laughed and joked and just milled around, all day and all night and until near noon next day. If you had a bit of food you divided it with someone. I nally got a cup of water for a dollar, after standing in line for three hours, and then a woman just behind me——” “A woman!” Cousin Arminta Greenwood (of the Georgia Greenwoods). And Sabra Cravat echoed the words in a shocked whisper. “You wouldn’t believe, would you, that women would go it alone in a fracas like that. But they did. They were there with their husbands, some of them, but there were women who made the Run alone.” “What kind of women?” Felice Venable’s tone was not one of inquiry but of condemnation. “Women with iron in ’em. Women who wanted land and a home. Pioneer women.” From Aunt Cassandra Venable’s end of the table there came a word that sounded like, “Hussies!” Yancey Cravat caught the word beneath his teeth and spat it back. “Hussies, heh! The one behind me in the line was a woman of forty —or looked it—in a calico dress and a sunbonnet. She had driven across the prairies all the way from the north of Arkansas in a springless wagon. She was like the women who crossed the continent to California in ’49. A gaunt woman, with a weather-

beaten face; the terribly neglected skin”—he glanced at Sabra with her creamy coloring—“that means alkali water and sun and dust and wind. Rough hair, and unlovely hands, and boots with the mud caked on them. It’s women like her who’ve made this country what it is. You can’t read the history of the United States, my friends” (all this he later used in an Oklahoma Fourth of July speech when they tried to make him Governor) “without learning the great story of those thousands of unnamed women—women like this one I’ve described—women in mud-caked boots and calico dresses and sunbonnets, crossing the prairie and the desert and the mountains enduring hardship and privation. Good women, with a terrible and rigid goodness that comes of work and self-denial. Nothing picturesque or romantic about them, I suppose—though occasionally one of them ashes—Belle Starr the outlaw—Rose of the Cimarron —Jeannette Daisy who jumped from a moving Santa Fé train to stake her claim—but the others—no, their story’s never really been told. But it’s there, just the same. And if it’s ever told straight you’ll know it’s the sunbonnet and not the sombrero that has settled this country.” “Talking nonsense,” drawled Felice Venable. Yancey whirled on his high heels to face her, his ne eyes blazing. “You’re one of them. You came up from the South with your husband to make a new home in this Kansas——” “I am not!” retorted Felice Venable, with enormous dignity. “And I’ll thank you not to say any such thing. Sunbonnet indeed! I’ve never worn a sunbonnet in my life. And as for my skin and hair and hands, they were the toast of the South, as I can prove by anyone here, all the way from Louisiana to Tennessee. And feet so small my slippers had to be made to order. Calico and muddy boots indeed!” “Oh, Mamma, Yancey didn’t mean—he meant courage to leave your home in the South and come up—he wasn’t thinking of— Yancey, do get on with your story of the Run. You got a drink of water for a dollar—dear me!—and shared it with the woman in the calico and the sunbonnet …” He looked a little sheepish. “Well, matter of fact, it turned out she didn’t have a dollar to spare, or anywhere near it, but even if she

had it wouldn’t have done her any good. The fellow selling it was a rat-faced hombre with one eye and Mexican pants. The trigger nger of his right hand had been shot away in some fracas or other, so he ladled out water with that hand and toted his gun in his left. Bunged up he was, plenty. A scar on his nose, healed up, but showing the marks of where human teeth had bit him in a ght, as neat and clear as a dentist’s signboard. By the time I got to him there was one cup of water left in the bucket. He tipped it while I held the dipper, and it trickled out, just an even dipperful. The last cup of water on the Border. The crowd waiting in line behind me gave a kind of sound between a groan and a moan. The sound you hear a herd of cow animals give, out on the prairie, when their tongues are hanging out for water in the dry spell. I tipped up the dipper and had down a big mouthful— lthy tasting stu it was, too. Gyp water. You could feel the alkali cake on your tongue. Well, my head went back as I drank, and I got one look at that woman’s face. Her eyes were on me—on my throat, where the Adam’s apple had just given that one big gulp after the rst swallow. All bloodshot the whites of her eyes, and a look in them like a dying man looks at a light. Her mouth was open, and her lips were all split with the heat and the dust and the sun, and dry and aky as ashes. And then she shut her lips a little and tried to swallow nothing, and couldn’t. There wasn’t any spit in her mouth. I couldn’t down another mouthful, parching as I was. I’d have seen her terrible face to the last day of my life. So I righted it, and held it out to her and said, ‘Here, sister, take the rest of it. I’m through.’ ” Cousin Jouett Goforth essayed his little joke. “Are you right sure she was forty, Yancey, and weather-beaten? And that about her hair and boots and hands?” Cravat, standing behind his wife’s chair, looked down at her; at the ne white line that marked the parting of her thick black hair. With one fore nger he touched her cheek, gently. He allowed the nger to slip down the creamy surface of her skin, from cheek bone to chin. “Dead sure, Jouett. I left out one thing, though.” Cousin Jouett made a sound signifying, ah, I thought so. “Her teeth,”

Yancey Cravat went on thoughtfully. “Broken and discolored like those of a woman of seventy. And most of them gone at the side.” Here Yancey could not resist charging up and down, irting his coat tails and generally ruining the ne avor of his victory over the Venable mind. The Venable mind (or the prospect of escaping it) had been one of the reasons for his dash into the wild mêlée of the Run in the rst place. Now he stood surveying these handsome futile faces, and a great impatience shook him, and a ame of rage shot through him, and a tongue of malice icked him. With these to goad him, and the knowledge of how he had failed, he plunged again into his story to the end. “I had planned to try and get a place on the Santa Fé train that was standing, steam up, ready to run into the Nation. But you couldn’t get on. There wasn’t room for a ea. They were hanging on the cow-catcher and swarming all over the engine, and sitting on top of the cars. It was keyed down to make no more speed than a horse. It turned out they didn’t even do that. They went twenty miles in ninety minutes. I decided I’d use my Indian pony. I knew I’d get endurance, anyway, if not speed. And that’s what counted in the end. “There we stood, by the thousands, all night. Morning, and we began to line up at the Border, as near as they’d let us go. Militia all along to keep us back. They had burned the prairie ahead for miles into the Nation, so as to keep the grass down and make the way clearer. To smoke out the Sooners, too, who had sneaked in and were hiding in the scrub oaks, in the draws, wherever they could. Most of the killing was due to them. They had crawled in and staked the land and stood ready to shoot those of us who came in, fair and square, in the Run. I knew the piece I wanted. An old freighters’ trail, out of use, but still marked with deep ruts, led almost straight to it, once you found the trail, all overgrown as it was. A little creek ran through the land, and the prairie rolled a little there, too. Nothing but blackjacks for miles around it, but on that section, because of the water, I suppose, there were elms and persimmons and cottonwoods and even a grove of pecans. I had noticed it many a time, riding the range.”

(H’m! Riding the range! All the Venables made a quick mental note of that. It was thus, by stray bits and snatches, that they managed to piece together something of Yancey Cravat’s past.) “Ten o’clock, and the crowd was nervous and restless. Hundreds of us had been followers of Payne and had gone as Boomers in the old Payne colonies, and had been driven out, and had come back again. Thousands from all parts of the country had waited ten years for this day when the land-hungry would be fed. They were like people starving. I’ve seen the same look exactly on the faces of men who were ravenous for food. “Well, eleven o’clock, and they were crowding and cursing and ghting for places near the Line. They shouted and sang and yelled and argued, and the sound they made wasn’t human at all, but like thousands of wild animals penned up. The sun blazed down. It was cruel. The dust hung over everything in a thick cloud, blinding you and choking you. The black dust of the burned prairie was over everything. We were like a horde of ends with our red eyes and our cracked lips and our blackened faces. Eleven-thirty. It was a picture straight out of hell. The roar grew louder. People fought for an inch of gain on the Border. Just next to me was a girl who looked about eighteen—she turned out to be twenty- ve—and a beauty she was, too—on a coal-black thoroughbred.” “Aha!” said Cousin Jouett Goforth. He was the kind of man who says, “Aha.” “On the other side was an old fellow with a long gray beard—a plainsman, he was—a six-shooter in his belt, one wooden leg, and a ask of whisky. He took a pull out of that every minute or two. He was mounted on an Indian pony like mine. Every now and then he’d throw back his head and let out a yell that would curdle your blood, even in that chorus of ends. As we waited we fell to talking, the three of us, though you couldn’t hear much in that uproar. The girl said she had trained her thoroughbred for the race. He was from Kentucky, and so was she. She was bound to get her husband and sixty acres, she said. She had to have it. She didn’t say why, and I didn’t ask her. We were all too keyed up, anyway, to make sense. Oh, I forgot. She had on a get-up that took the attention of anyone

that saw her, even in that crazy mob. The better to cut the wind, she had shortened sail and wore a short skirt, black tights, and a skullcap.” Here there was quite a bombardment of sound as silver spoons and knives and forks were dropped from shocked and nerveless feminine Venable ngers. “It turned out that the three of us, there in the front line, were headed down the old freighters’ trail toward the creek land. I said, ‘I’ll be the rst in the Run to reach Little Bear.’ That was the name of the creek on the section. The girl pulled her cap down tight over her ears. ‘Follow me,’ she laughed. ‘I’ll show you the way.’ Then the old fellow with the wooden leg and the whiskers yelled out, ‘Whoop-ee! I’ll tell ’em along the Little Bear you’re both a-comin.’ “There we were, the girl on my left, the old plainsman on my right. Eleven forty- ve. Along the Border were the soldiers, their guns in one hand, their watches in the other. Those last ve minutes seemed years long; and funny, they’d quieted till there wasn’t a sound. Listening. The last minute was an eternity. Twelve o’clock. There went up a roar that drowned the crack of the soldiers’ musketry as they red in the air as the signal of noon and the start of the Run. You could see the pu s of smoke from their guns, but you couldn’t hear a sound. The thousands surged over the Line. It was like water going over a broken dam. The rush had started, and it was devil take the hindmost. We swept across the prairie in a cloud of black and red dust that covered our faces and hands in a minute, so that we looked like black demons from hell. O we went, down the old freight trail that was two wheel ruts, a foot wide each, worn into the prairie soil. The old man on his pony kept in one rut, the girl on her thoroughbred in the other, and I on my Whitefoot on the raised place in the middle. That rst half mile was almost a neck-and-neck race. The old fellow was yelling and waving one arm and hanging on somehow. He was beating his pony with the ask on his anks. Then he began to drop behind. Next thing I heard a terrible scream and a great shouting behind me. I threw a quick glance over my shoulder. The old plainsman’s pony had stumbled and fallen. His bottle smashed into bits, his six-shooter ew in

another direction, and he lay sprawling full length in the rut of the trail. The next instant he was hidden in a welter of pounding hoofs and ying dirt and cinders and wagon wheels.” A dramatic pause. Black Isaiah was hanging from his perch like a monkey on a branch. His asparagus shoo- y was limp. The faces around the table were balloons pulled by a single string. They swung this way and that with Yancey Cravat’s pace as he strode the room, his Prince Albert coat tails billowing. This way—the faces turned toward the sideboard. That way—they turned toward the windows. Yancey held the little moment of silence like a jewel in the circlet of faces. Sabra Cravat’s voice, high and sharp with suspense, cut the stillness. “What happened? What happened to the old man?” Yancey’s pliant hands ew up in a gesture of inevitability. “Oh, he was trampled to death in the mad mob that charged over him. Crazy. They couldn’t stop for a one-legged old whiskers with a quart ask.” Out of the well-bred murmur of horror that now arose about the Venable board there emerged the voice of Felice Venable, sharp- edged with disapproval. “And the girl. The girl with the black——” Unable to say it. Southern. “The girl and I—funny, I never did learn her name—were in the lead because we had stuck to the old trail, rutted though it was, rather than strike out across the prairie that by this time was beyond the burned area and was covered with a heavy growth of blue stem grass almost six feet high in places. A horse could only be forced through that at slow pace. That jungle of grass kept many a racer from winning his section that day. “The girl followed close behind me. That thoroughbred she rode was built for speed, not distance. A race horse, blooded. I could hear him blowing. He was trained to short bursts. My Indian pony was just getting his second wind as her horse slackened into a trot. We had come nearly sixteen miles. I was well in the lead by that time, with the girl following. She was crouched low over his neck, like a jockey, and I could hear her talking to him, low and sweet and eager, as if he were a human being. We were far in the lead now.

We had left the others behind, hundreds going this way, hundreds that, scattering for miles over the prairie. Then I saw that the prairie ahead was a re. The tall grass was blazing. Only the narrow trail down which we were galloping was open. On either side of it was a wall of ame. Some skunk of a Sooner, sneaking in ahead of the Run, had set the blaze to keep the Boomers o , saving the land for himself. The dry grass burned like oiled paper. I turned around. The girl was there, her racer stumbling, breaking and going on, his head lolling now. I saw her motion with her hand. She was coming. I whipped o my hat and clapped it over Whitefoot’s eyes, gave him the spurs, crouched down low and tight, shut my own eyes, and down the trail we went into the furnace. Hot! It was hell! The crackling and snapping on either side was like a fusillade. I could smell the singed hair on the anks of the mustang. My own hair was singeing. I could feel the ames licking my legs and back. Another hundred yards and neither the horse nor I could have come through it. But we broke out into the open choking and blinded and half su ocated. I looked down the lane of ame. The girl hung on her horse’s neck. Her skullcap was pulled down over her eyes. She was coming through game. I knew that my land—the piece that I had come through hell for—was not more than a mile ahead. I knew that hanging around here would probably get me a shot through the head, for the Sooner that started that re must be lurking somewhere in the high grass ready to kill anybody that tried to lay claim to his land. I began to wonder, too, if that girl wasn’t headed for the same section that I was bound for. I made up my mind that, woman or no woman, this was a race and devil take the hindmost. My poor little pony was coughing and sneezing and trembling. Her racer must have been ready to drop. I wheeled and went on. I kept thinking how, when I came to Little Bear Creek, I’d bathe my little mustang’s nose and face and his poor heaving anks, and how I mustn’t let him drink too much, once he got his muzzle in the water. “Just before I reached the land I was riding for I had to leave the trail and cut across the prairie. I could see a clump of elms ahead. I knew the creek was near by. But just before I got to it I came to one of those deep gullies you nd in the plains country. Drought does it

—a crack in the dry earth to begin with, widening with every rain until it becomes a small cañon. Almost ten feet across this one was, and deep. No way around it that I could see, and no time to look for one. I put Whitefoot to the leap and, by God, he took it, landing on the other side with hardly an inch to spare. I heard a wild scream behind me. I turned. The girl on her spent racer had tried to make the gulch. He had actually taken it—a thoroughbred and a gentleman, that animal—but he came down on his knees just on the farther edge, rolled, and slid down the gully side into the ditch. The girl had ung herself free. My claim was fty yards away. So was the girl, with her dying horse. She lay there on the prairie. As I raced toward her—my own poor little mount was nearly gone by this time—she scrambled to her knees. I can see her face now, black with cinders and soot and dirt, her hair all over her shoulders, her cheek bleeding where she had struck a stone in her fall, her black tights torn, her little short skirt sagging. She sort of sat up and looked around her. Then she staggered to her feet before I reached her and stood there swaying, and pushing her hair out of her eyes like someone who’d been asleep. She pointed down the gully. The black of her face was streaked with tears. “ ‘Shoot him!’ she said. ‘I can’t. His two forelegs are broken. I heard them crack. Shoot him! For God’s sake!’ “So I o my horse and down to the gully’s edge. There the animal lay, his eyes all whites, his poor legs doubled under him, his anks black and sticky with sweat and dirt. He was done for, all right. I took out my six-shooter and aimed right between his eyes. He kicked once, sort of leaped—or tried to, and then lay still. I stood there a minute, to see if he had to have another. He was so game that, some way, I didn’t want to give him more than he needed. “Then something made me turn around. The girl had mounted my mustang. She was o toward the creek section. Before I had moved ten paces she had reached the very piece I had marked in my mind for my own. She leaped from the horse, ripped o her skirt, tied it to her riding whip that she still held tight in her hand, dug the whip butt into the soil of the prairie—planted her ag—and the land was hers by right of claim.”

Yancey Cravat stopped talking. There was a moment of stricken silence. Sabra Cravat staring, staring at her husband with great round eyes. Lewis Venable, limp, yellow, tremulous. Felice Venable, upright and quivering. It was she who spoke rst. And when she did she was every inch the thrifty descendant of French forbears; nothing of the Southern belle about her. “Yancey Cravat, do you mean that you let her have your quarter section on the creek that you had gone to the Indian Territory for! That you had been gone a month for! That you had left your wife and child for! That——” “Now, Mamma!” You saw that all the Venable in Sabra was summoned to keep the tears from her eyes, and that thus denied they had crowded themselves into her trembling voice. “Now, Mamma!” “Don’t you ‘now Mamma’ me! What of the land that you were to have had! It was bad enough to think of your going to that wilderness, but to——” She paused. Her voice took on a new and more sinister note. “I don’t believe a word of it.” She whirled on Yancey, her black eyes blazing. “Why did you let that trollop in the black tights have that land?” Yancey regarded this question with considerable judicial calm, but Felice, knowing him, might have been warned by the way his great head was lowered like that of a charging bull bu alo. “If it had been a man I could have shot him. A good many had to, to keep the land they’d run fairly for. But you can’t shoot a woman.” “Why not?” demanded the erstwhile Southern belle, sharply. The Venables, as one man, gave a little jump. A nervous sound, that was half gasp and half shocked titter, went round the Venable board. A startled “Felice!” was wrung from Lewis Venable. “Why, Mamma!” said Sabra. Yancey Cravat, enormously vital, felt rising within him the tide of irritability which this vitiated family always stirred in him. Something now about their shocked and staring faces, their lolling and graceful forms, roused in him an unreasoning rebellion. He suddenly hated them. He wanted to be free of them. He wanted to be free of them—of Wichita—of convention—of smooth custom—of

—no, not of her. He now smiled his brilliant sweet smile which alone should have warned Felice Venable. But that intrepid matriarch was not one to let a tale go unpointed. “I’m mighty pleased, for one, that it turned out as it did. Do you suppose I’d have allowed a daughter of mine—a Venable—to go traipsing down into the wilderness to live among drunken one- legged plainsmen, and toothless scrags in calico, and trollops in tights! Never! It’s over now, and a mighty good thing, too. Perhaps now, Yancey, you’ll stop this ramping up and down and be content to run that newspaper of yours and conduct your law practice—such as it is—with no more talk of this Indian Territory. A daughter of mine in boots and calico and sunbonnet, if you please, a-pioneering among savages. Reared as she was! No, indeed.” Yancey was strangely silent. He was surveying his ne white hands critically, interestedly, as though seeing them in admiration for the rst time—another sign that should have warned the brash Felice. When he spoke it was with utter gentleness. “I’m no farmer. I’m no rancher. I didn’t want a section of farm land, anyway. The town’s where I belong, and I should have made for the town sites. There were towns of ten thousand and over sprung up in a night during the Run. Wagallala—Sperry— Wawhuska—Osage. It’s the last frontier in America, that new country. There isn’t a newspaper in one of those towns—or wasn’t, when I left. I want to go back there and help build a state out of prairie and Indians and scrub oaks and red clay. For it’ll be a state some day—mark my words.” “That wilderness a state!” sneered Cousin Dabney Venable. “With an Osage buck or a Cherokee chief for governor, I suppose.” “Why not? What a revenge on a government that has cheated them and driven them like cattle from place to place and broken its treaties with them and robbed them of their land. Look at Georgia! Look at Mississippi! Remember the Trail of Tears!” “Ho hum,” yawned Cousin Jouett Goforth, and rose, fumblingly. “This has all been very interesting—odd, but interesting. But if you will excuse me now I shall have my little siesta. I am accustomed after dinner …”