Factoring Proposal: After recently recovering from the devasting impacts of tariffs, this company requires PO financing to rebuild inventory. Their existing factor is uncooperative and must be replaced by Versant which has the ability to facilitate PO funding though a trusted partner.

Factoring Proposal: With only a single major distributor as customer, this business was unable to find a lender willing to fund them. Our underwriting focuses solely on the quality of our client’s customer so time in business and customer concentration are irrelevant.

In the world of candy importing, timing is everything. You have to navigate seasonal peaks (think Halloween and Valentine’s Day), manage international shipping lead times, and juggle the demands of large retailers.

However, there is often a massive gap between the moment your colorful shipments clear customs and the moment your retail partners actually pay their invoices. If your capital is trapped in Accounts Receivable (AR), you might find yourself unable to jump on the next big inventory opportunity.

This is where Accounts Receivable Factoring—also known as invoice factoring—becomes a game-changer.

What Exactly is Factoring?

Factoring isn’t a loan; it’s the sale of your assets. You sell your outstanding invoices to a “factor” (a specialized financial company) at a slight discount. In return, you get immediate access to the cash that was previously tied up for 30, 60, or even 90 days.

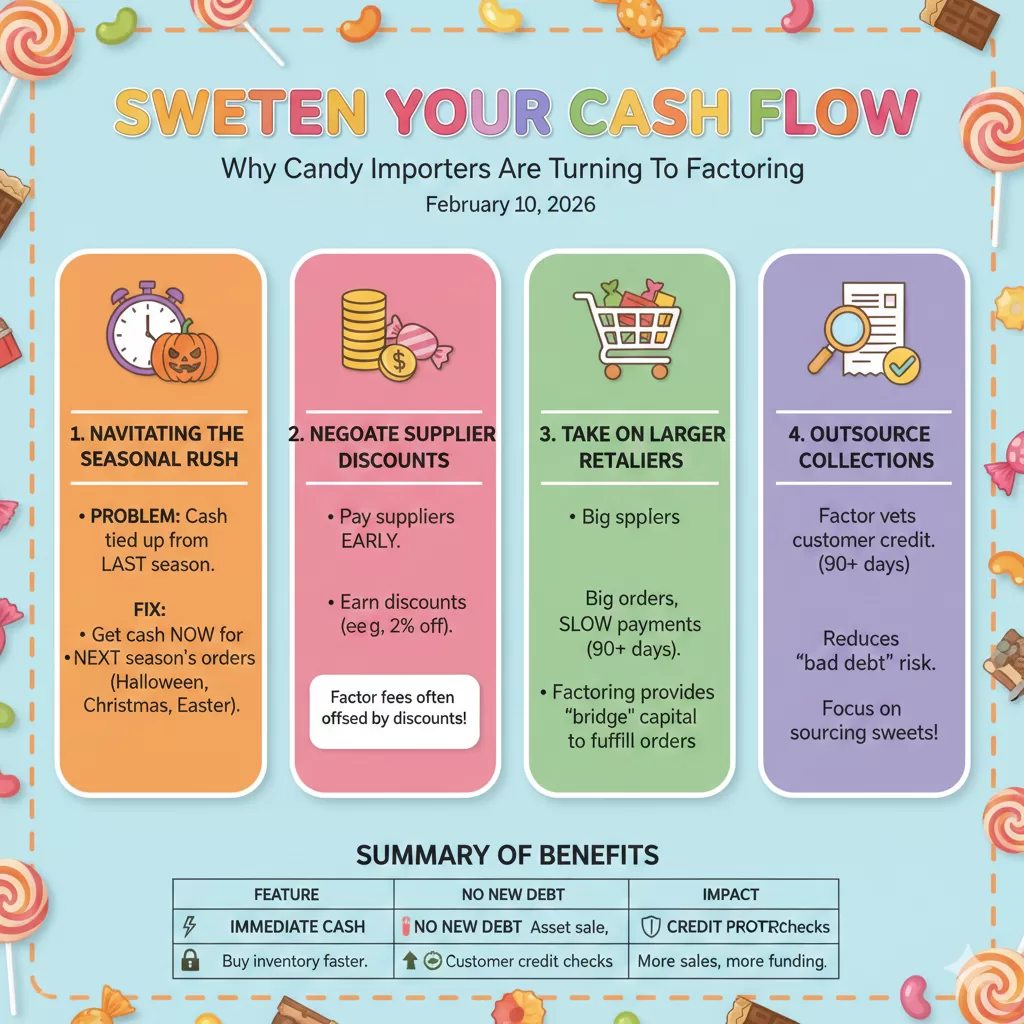

1. Navigating the Seasonal Rush

Candy is a highly seasonal business. To prepare for the “Big Three”—Halloween, Christmas, and Easter—importers must place massive orders months in advance.

The Problem: Your cash is tied up in invoices from the previous season while you need to pay suppliers for the next one.

The Factoring Fix: By factoring current invoices, you get an immediate cash injection to cover manufacturing and shipping costs for upcoming peak periods, ensuring you never miss a shelf-stocking deadline.

2. Negotiating Supplier Discounts

When you have “cash in hand” thanks to factoring, you move to the front of the line with global suppliers. Many international manufacturers offer early payment discounts (e.g., a 2% discount if paid within 10 days).

The small fee you pay for factoring is often completely offset by the discounts you earn from your suppliers by paying them early.

3. Taking on Larger Retailers

Big-box retailers are great for volume, but they are notorious for long payment terms. If a major chain wants to place a massive order but won’t pay for 90 days, a small-to-medium importer might have to say “no” simply because they can’t afford to wait that long for the payout.

Factoring provides the “bridge” capital. You can fulfill the order, factor the invoice the day the candy ships, and have the funds to keep the rest of your business running smoothly.

4. Outsourcing the “Headache” of Collections

Many factoring companies handle the back-end credit checking and collections process. For a lean importing team, this is a massive relief.

The factor vets the creditworthiness of your customers before you even ship, reducing your risk of “bad debt” and allowing you to focus on sourcing the best sweets rather than chasing down checks.

Summary of Benefits

Feature

Impact on Your Candy Business

Immediate Cash

Buy inventory for the next holiday season without waiting.

No New Debt

Factoring is an asset sale, not a bank loan with monthly interest.

Credit Protection

Many factors provide credit snapshots of your retail partners.

Scalability

The more you sell, the more funding becomes available.

Is Factoring Right for You?

If your candy importing business is growing faster than your bank account can keep up with, factoring provides the liquidity to keep your momentum. It turns your “sold” inventory back into “buying” power instantly.

Our Accounts Receivable Factoring program can quickly meet the working capital needs of businesses in the energy industry.

Versant’s underwriting focus is solely on the quality of a company’s accounts receivable, which enables us to rapidly fund businesses which do not qualify for traditional lending.

Factoring Press Release : Versant Funds $5 Million Non-Recourse Factoring Facility to Manufacturer

(January 27, 2026) Versant Funding LLC is pleased to announce that it has funded a $5 Million non-recourse factoring facility to a company that manufactures products for a large customer base which includes one of America’s largest municipalities.

After a transition to Private Equity ownership and management restructuring, our newest client required an infusion of working capital to meet an urgent cash need. While the company has hundreds of customers with AR outstanding, the most efficient way to fund was to factor only the AR of their largest customer, but most factoring companies would not permit 100% customer concentration.

“Versant focuses solely on the credit quality of our clients’ customers,” according to Chris Lehnes, Business Development Officer for Versant Funding, and originator of this financing opportunity. “Since the company’s largest account is a large US city, we were willing to allow 100% customer concentration and meet the client’s short-term funding need.”

About Versant Funding

Versant Funding’s custom Non-Recourse Factoring Facilities have been designed to fill a void in the market by focusing exclusively on the credit quality of a company’s accounts receivable. Versant Funding offers non-recourse factoring solutions to companies with B2B or B2G sales from $100,000 to $30 Million per month. All we care about is the credit quality of the A/R. To learn more contact: Chris Lehnes | 203-664-1535 | chis@chrislehnes.com

Key Benefits of this Non-Recourse Factoring Deal:

Immediate Cash Flow: The manufacturer gains immediate access to working capital by selling its invoices to Versant Funding, significantly improving liquidity.

Mitigation of Customer Concentration Risk: By utilizing non-recourse factoring, Versant Funding assumes the credit risk associated with the manufacturer’s customer, protecting the manufacturer from potential bad debt.

Support for Growth: The increased cash flow will enable the manufacturer to invest in new equipment, expand production, take on larger orders, and capitalize on new market opportunities.

Operational Efficiency: The manufacturer can focus on its core business operations and production, knowing its cash flow is stable and predictable.

Flexible and Scalable: The factoring facility is designed to grow with the manufacturer’s sales, providing ongoing access to capital as their business expands.

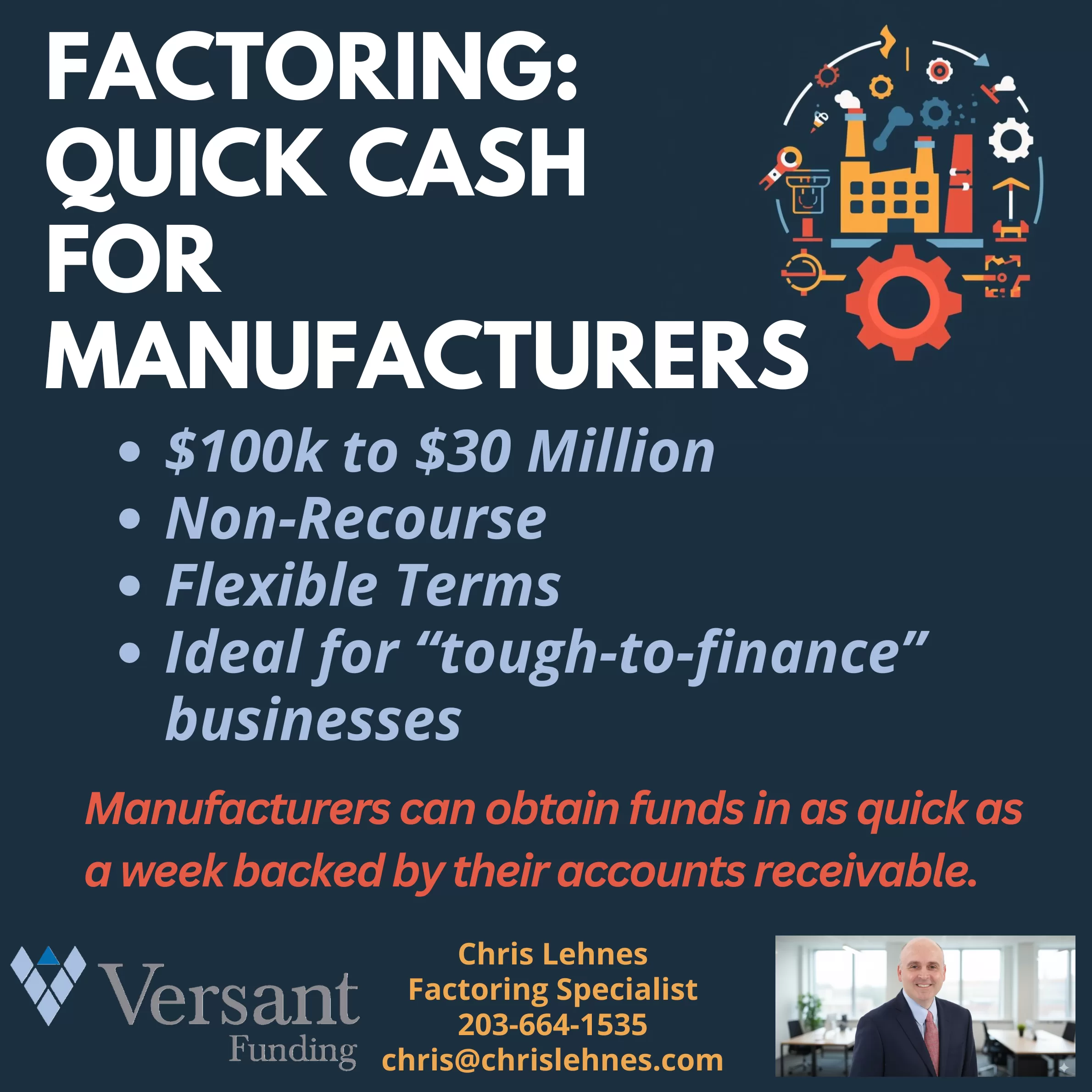

Factoring: The Quick Cash Solution Manufacturers Need Now

In today’s dynamic market, manufacturers face a unique set of challenges. From managing inventory and production schedules to navigating supply chain disruptions and fluctuating demand, the need for reliable, accessible capital is constant. That’s where factoring comes in, offering a powerful and often overlooked solution for quick cash.

At Versant Funding, we understand the specific financial pressures manufacturers endure. That’s why we specialize in providing tailored factoring services designed to get you the capital you need, when you need it. Our latest video, which you can watch above, highlights how factoring can be a game-changer for your business.

What is Factoring, and Why is it Perfect for Manufacturers?

Simply put, factoring allows you to sell your accounts receivable (invoices) to a third party (the factor) at a small discount in exchange for immediate cash. Instead of waiting 30, 60, or even 90 days for your customers to pay, you get the funds right away.

For manufacturers, this means:

Quick Cash Flow: No more cash flow gaps hindering your production or growth initiatives. Get funds in as quick as a week!

Significant Funding: We offer funding from $100,000 to $30 Million, providing substantial support whether you’re a growing mid-sized company or a large enterprise.

Non-Recourse Factoring: This is a crucial benefit for manufacturers. With non-recourse factoring, if your customer fails to pay due to bankruptcy or insolvency, you’re typically not responsible for repaying the advance. This transfers the credit risk away from your balance sheet.

Flexible Terms: We work with you to create terms that fit your unique business model and cash flow requirements.

Ideal for “Tough-to-Finance” Businesses: Traditional bank loans can be hard to secure, especially for newer companies, those with limited collateral, or those experiencing rapid growth. Factoring focuses on the quality of your accounts receivable, making it an accessible option when other avenues are closed.

How Manufacturers Benefit from Factoring:

Imagine being able to:

Purchase Raw Materials: Take advantage of bulk discounts or secure critical components without delay.

Meet Payroll: Ensure your skilled workforce is paid on time, every time.

Invest in New Equipment: Upgrade machinery or expand your production lines to increase efficiency and capacity.

Handle Large Orders: Don’t turn away big opportunities because of insufficient working capital.

Improve Credit Standing: Use the immediate cash to pay suppliers promptly, potentially earning early payment discounts and strengthening your vendor relationships.

Why?

We pride ourselves on being more than just a capital provider. We are your partner in growth. I am dedicated to understanding the intricacies of the manufacturing sector and crafting financial solutions that truly work.

Ready to unlock the potential of your accounts receivable?

To see how factoring can transform your manufacturing business reach out to Chris Lehnes today for a no-obligation consultation.

The 2026 Growth Gap: How Accounts Receivable Factoring Fuels Small Business Success

Factoring: Quick Cash to Kick Off the Year: As we move through 2026, the economic landscape for small businesses is defined by a paradox: opportunity is everywhere, but cash is moving slower than ever. While sectors like high-tech manufacturing and professional services are seeing a resurgence, many entrepreneurs find themselves “asset rich but cash poor.”

You’ve landed the big contract, your team is working overtime, and your sales are climbing. Yet, your bank account doesn’t reflect that success because your capital is trapped in Accounts Receivable (AR). If you’re waiting 30, 60, or even 90 days for clients to pay their invoices, you aren’t just waiting for money—you’re waiting to grow.

This is where Accounts Receivable Factoring becomes a strategic engine for your business.

What is AR Factoring in 2026?

Accounts receivable factoring (or invoice factoring) is not a loan. It is the sale of your outstanding invoices to a third party (a “factor”) at a slight discount in exchange for immediate liquidity.

In 2026, the process has been revolutionized by fintech integrations. Most modern factoring platforms now sync directly with your accounting software (like QuickBooks or Xero), allowing for “one-click” funding that can land in your account within 24 hours.

Why Factoring is the “Secret Weapon” for 2026

While traditional bank loans focus on your credit score and years of profitability, factoring focuses on the creditworthiness of your customers. This makes it an ideal solution for:

Rapidly Growing Startups: When sales outpace your cash reserves.

Seasonal Businesses: Managing the “lumpy” cash flow of peak seasons.

Service Providers: Staffing agencies or consultants who must pay employees weekly but get paid by clients monthly.

3 Ways Factoring Helps You Thrive This Year

1. Turn “Net-90” into “Right Now”

The most significant barrier to growth in 2026 is the “Cash Gap.” If you have $100,000 in open invoices, that’s $100,000 you can’t use to buy inventory, hire talent, or pay for digital marketing. Factoring unlocks up to 90-95% of that value immediately, giving you the agility to say “yes” to new opportunities without checking your balance first.

2. Fuel Expansion Without Adding Debt

In an era of “snagflation”—where mild inflation persists alongside a shifting labor market—loading your balance sheet with high-interest debt can be risky. Because factoring is a purchase of assets, it doesn’t show up as a loan. You are simply accelerating the arrival of money you’ve already earned.

3. Outsourced Credit & Collections

Modern factoring companies do more than just provide cash. They often act as your back-office credit department. In 2026, where business bankruptcies are slightly on the rise, having a partner who vets the credit risk of your potential clients is a massive competitive advantage. They handle the collections, freeing you up to focus on your product.

Is it Right for You?

To help you decide, here is a quick comparison of how factoring stacks up against traditional financing in today’s market:

Feature

AR Factoring

Traditional Bank Loan

Speed

24–48 Hours

3–6 Weeks

Approval Basis

Customer’s Credit

Your Credit & Collateral

Debt

None (Asset Sale)

Increases Liabilities

Flexibility

Scales with Sales

Fixed Credit Limit

Cost

1%–5% Service Fee

Interest Rate + Fees

Final Thoughts: Don’t Let Your Invoices Hold You Back

In 2026, the winners won’t necessarily be the companies with the biggest ideas, but those with the highest liquidity. AR factoring provides a bridge over the cash flow gaps that sink 82% of small businesses. It turns your hard work into immediate fuel.

For B2B businesses, accounts receivable (AR) factoring is essentially a tool to accelerate cash flow. It allows you to trade the “waiting game” of Net-30 or Net-60 terms for immediate liquidity.

Instead of waiting for a client to pay an invoice, you sell that invoice to a third party (a “factor”) who advances you the majority of the funds immediately. This converts a stagnant asset (an unpaid invoice) into active working capital you can use to fund operations, payroll, or growth.

The following guide details how B2B businesses can utilize this strategy to meet working capital needs.

1. The Core Mechanism: How it Works

Factoring is technically an asset sale, not a loan. You are selling the right to collect on the invoice.

Step 1: Invoicing. You deliver your goods/services and send an invoice to your B2B customer as usual.

Step 2: Sale. You submit a copy of that invoice to the factoring company.

Step 3: The Advance. The factor verifies the invoice and wires you an advance—typically 80% to 90% of the invoice value—within 24 to 48 hours.

Step 4: Collection. The factor waits for your customer to pay them directly according to the invoice terms (e.g., 30 or 60 days).

Step 5: The Rebate. Once the customer pays the full amount, the factor releases the remaining 10–20% to you, minus their fee (usually 1–5%).

2. Strategic Uses for Working Capital

You can use the immediate infusion of cash to solve specific operational friction points common in B2B models:

Bridging the “Gap”: If your expenses (payroll, rent, utilities) are due weekly or bi-weekly, but your customers pay monthly, you have a cash flow gap. Factoring aligns your revenue intake with your expense outflow.

Fulfilling Large Orders: B2B growth often hurts cash flow before helping it. If you land a massive contract, you need cash now to buy raw materials and hire labor to fulfill it. Factoring existing invoices gives you the capital to fund these new orders without taking on debt.

Negotiating Supplier Discounts: With cash on hand, you can pay your own suppliers early. often unlocking “2/10 Net 30” discounts (a 2% discount if paid within 10 days). This discount can sometimes offset the cost of the factoring fee itself.

Smoothing Seasonality: For businesses with peak seasons (e.g., manufacturing for holiday retail), factoring during the busy season ensures you have the liquidity to maximize production when it matters most.

3. Critical Decisions: Configuring Your Factoring

To use this effectively, you must choose the right “type” of factoring for your risk profile.

Recourse vs. Non-Recourse

This determines who is liable if your client never pays (e.g., they go bankrupt).

Recourse Factoring: You are liable. If the client doesn’t pay, you must buy the invoice back from the factor. Benefit: Lower fees.

Non-Recourse Factoring: The factor assumes the credit risk. If the client defaults due to insolvency, the factor absorbs the loss. Benefit: Zero risk for you, but higher fees.

Notification vs. Non-Notification

Notification: Your customer is notified to pay the factor directly. This is standard but can sometimes signal to customers that you are tight on cash.

Non-Notification (White Label): The customer pays into a bank account that looks like yours but is controlled by the factor. The customer is unaware of the factoring arrangement.

4. Who Qualifies?

Unlike a bank loan, approval for factoring is based primarily on your customer’s creditworthiness, not yours.

Ideal Candidate: A B2B business (startups included) with reliable, large corporate or government clients who pay slowly but surely.

Less Ideal: Businesses with B2C customers (individuals) or clients with poor credit histories.

Factoring can provide your client the cash they need through the holiday season. Contact me to learn how to get your client funded by year-end.

We focus on the quality of your client’s accounts receivable, ignoring their financial condition.

This enables us to move quickly and fund qualified businesses including Manufacturers, Distributors and a variety of Service Businessesin as few as 3-5 days. Contact me today to learn if your client is a factoring fit.

Factoring offers a strategic financial solution for your clients to maintain cash flow stability during the busy holiday period. As businesses experience increased sales and operational expenses, access to immediate funds becomes crucial for seizing opportunities, managing payroll, and covering inventory costs. Unlike traditional loans that may involve lengthy approval processes or stringent credit requirements, factoring provides quick and flexible funding based on accounts receivable.

By leveraging factoring, your clients can unlock working capital without adding debt or risking their creditworthiness. This ensures they remain agile and competitive during a critical time of the year when customer payments may be delayed or unpredictable. Additionally, factoring can help sustain growth initiatives, support seasonal staffing needs, and enhance overall financial resilience.

I invite you to reach out to discuss how this financing option can be tailored to meet your client’s specific needs. With our streamlined process and focus on quality receivables, we can facilitate funding in as few as 3-5 days—empowering your client to maximize their holiday sales and finish the year strong. Contact me today to explore how we can assist in securing the necessary capital before the year concludes.

Accounts Receivable Factoring can quickly meet the working capital needs of Distributors impacted by rising tariffs.

Our underwriting focus is solely on the quality of a company’s accounts receivable, which enables us to rapidly fund businesses which do not qualify for traditional lending such as those experiencing losses or where the owners have weak personal credit or even “character issues.”

(October 16, 2025) Versant Funding LLC is pleased to announce that it has funded a $2.5 Million non-recourse factoring facility to a company that provides software and consulting services to major multinational companies.

The factoring company this business had relied upon for many years to meet its working capital needs refused to fund against invoices from a few key accounts. The resulting cash shortfall was reducing the company’s ability to service its customers.

“Versant focuses solely on the credit quality of our clients’ customers,” according to Chris Lehnes, Business Development Officer for Versant Funding, and originator of this financing opportunity. “Since the company’s key accounts were financially strong entities, we were willing to factor all their invoices, greatly improving the company’s cashflow and ability to meet customer expectations.”

About Versant Funding: Versant Funding’s custom Non-Recourse Factoring Facilities have been designed to fill a void in the market by focusing exclusively on the credit quality of a company’s accounts receivable. Versant Funding offers non-recourse factoring solutions to companies with B2B or B2G sales from $100,000 to $30 Million per month. All we care about is the credit quality of the A/R. To learn more contact: Chris Lehnes|203-664-1535 | chris@chrislehnes.com

Software as a Service (SaaS): The Engine of the Modern Digital Economy

Software as a Service (SaaS) is, in the simplest terms, the delivery of software applications over the internet, on demand, and typically on a subscription basis.1 It represents a fundamental shift in how software is consumed, moving away from the traditional model of purchasing a perpetual license, installing the software on local servers or individual computers (on-premise), and managing all the associated infrastructure and maintenance.

Instead, with SaaS, the software vendor hosts the application and data on their own or a third-party cloud provider’s servers, and customers simply access it via a web browser or a dedicated mobile application.2 This paradigm shift has made software far more accessible, scalable, and cost-effective, fueling the digital transformation of businesses across every sector.

The Foundational Model and Key Characteristics

To understand why SaaS is so disruptive, one must look at its core technical and business characteristics.

1. Cloud-Native and Subscription-Based Access

The core characteristic of SaaS is that the software is hosted in the cloud and accessed via an internet connection.3 This eliminates the need for the customer to invest in servers, storage, or operating systems to run the application.4

Remote Accessibility: Users can access the application from any device, anywhere in the world, so long as they have an internet connection, making it ideal for remote, hybrid, and global workforces.5

Subscription Pricing: SaaS is overwhelmingly sold through a subscription model, usually billed monthly or annually.6 This changes software from a capital expense (a large one-time purchase, or CapEx) to an operating expense (predictable, ongoing cost, or OpEx), which is financially favorable for most businesses.7

2. Multi-Tenant Architecture

The technical backbone of most modern SaaS applications is the multi-tenant architecture.8 This is the key element that makes the model efficient and scalable.

In a multi-tenant environment, a single instance of the software application and its underlying infrastructure serves multiple customers (tenants).9 While all customers share the same application, their data and customizations are logically isolated and secured, preventing one customer from accessing another’s information.10

Efficiency: Sharing a single code base and infrastructure across thousands of users dramatically lowers the cost for the vendor, which can then pass on savings to the customer.

Automatic Updates: Since there is only one version of the software, the vendor can roll out updates, security patches, and new features instantly and simultaneously to all users without the customer having to lift a finger for manual installation.11

3. Vendor Responsibility

In the SaaS model, the provider manages the entire technology stack, taking the burden of IT management off the customer.12 This includes:

Application Maintenance: Bug fixes, new feature releases, and version control.13

Data Security and Backup: Implementing robust cybersecurity protocols, performing regular data backups, and ensuring compliance with regional data regulations.14

Infrastructure Management: Managing the servers, networking, and operating systems necessary to run the application.15

The Benefits of the SaaS Model

The advantages of adopting SaaS solutions have driven their massive global proliferation, moving beyond just simple tools to mission-critical enterprise systems.

1. Reduced Cost and Predictability

The shift from CapEx to OpEx is perhaps the most significant benefit for small and medium-sized businesses.

Lower Upfront Investment: There are no massive upfront license fees or hardware purchases.16 Businesses only pay the monthly subscription fee.17

Cost Efficiency: Customers are not paying for server capacity they don’t use and can easily scale their subscription up or down based on current business needs.18

2. Rapid Deployment and Ease of Use

Implementing a new SaaS application can often be done in hours or days, not the months required for traditional on-premise software.19 Users simply log in via a web URL. This rapid deployment allows businesses to realize value almost instantly.20

3. Scalability and Performance

SaaS applications are built on scalable cloud infrastructure.21 If a customer needs to add 100 new users or dramatically increase their storage, the vendor handles the backend resource allocation seamlessly.22 The customer never has to worry about hitting an infrastructure bottleneck.

4. Continuous Innovation

In the on-premise world, major software updates (versions 1.0 to 2.0) often occurred years apart. With SaaS, the vendor constantly deploys minor, incremental updates and new features, ensuring the customer is always using the most advanced and secure version of the product.23

The “As-a-Service” Trilogy: SaaS vs. PaaS vs. IaaS

SaaS is the most customer-facing layer of the three main cloud service models, often referred to as the “As-a-Service” trilogy.24 The difference lies in how much of the technology stack the customer manages versus the cloud provider.

Model

What is it?

Customer Manages

Provider Manages

Examples

SaaS

Software Application

Nothing (just the application’s data)

All of it: Application, Data, Runtime, Servers, Networking, etc.

Salesforce, Google Workspace, Microsoft 365, Zoom, Dropbox

Amazon Web Services (EC2), Microsoft Azure (VMs), Google Compute Engine

SaaS is akin to a fully furnished, serviced apartment: you simply move in and use the appliances. PaaS is like renting the building structure and utilities, but you’re responsible for furnishing and decorating. IaaS is like renting the empty land and laying the foundation for a structure you’ll build and manage entirely yourself.

The Business of SaaS: Key Metrics

The subscription model of SaaS necessitates tracking a distinct set of financial and operational metrics, which are crucial for evaluating a company’s health and growth potential.25

Monthly Recurring Revenue (MRR) / Annual Recurring Revenue (ARR): The lifeblood of a SaaS business. This is the predictable revenue the company expects to receive every month or year from its subscription base, excluding one-time fees.26

Churn Rate: This is the rate at which customers or revenue is lost over a given period.27

Customer Churn: The percentage of customers who cancel their subscription.

Revenue Churn: The percentage of MRR/ARR lost due to cancellations or downgrades.28 A low churn rate (ideally under 2% monthly) is vital for long-term growth.

Customer Lifetime Value (CLV or LTV): The total predicted revenue a business can expect from a single customer account over the entire period of their relationship.29

Customer Acquisition Cost (CAC): The total sales and marketing spend required to acquire a new, paying customer.30

The financial goal for a healthy SaaS business is to have a CLV that significantly outweighs the CAC, typically a ratio of 3:1 or better, supported by a low churn rate.

Evolution and Future of SaaS

SaaS traces its roots back to the 1960s concept of time-sharing, but the modern model truly began with the founding of Salesforce.com in 1999, which popularized the delivery of enterprise applications entirely over the web via a multi-tenant architecture.31

Today, SaaS dominates major software categories, including:

ERP (Enterprise Resource Planning): Oracle Cloud, SAP S/4HANA Cloud33

Collaboration & Productivity: Google Workspace, Microsoft 365, Slack, Zoom34

HR and Finance: Workday, QuickBooks Online

The future of SaaS is increasingly integrated with emerging technologies:

Vertical SaaS: Applications tailored to specific, niche industries (e.g., software for dentists, gyms, or construction management) that combine software with industry-specific data and workflow.35

Embedded AI/ML: Integrating Artificial Intelligence and Machine Learning directly into SaaS applications to automate tasks, provide predictive analytics, and enhance user experience without the user having to manage separate AI infrastructure.36

Composable Architecture: Moving toward microservices that allow businesses to easily integrate and “compose” best-of-breed SaaS tools rather than relying on a single, monolithic suite.

In conclusion, Software as a Service is more than just a software delivery method; it is a business model and a technological philosophy that has democratized access to powerful computing tools.37 By transferring the complexity of IT management to the vendor and enabling a flexible, subscription-based financial structure, SaaS has become the essential foundation upon which the modern, globally distributed, and agile digital economy operates.

Cookie Consent

We use cookies to improve your experience on our site. By using our site, you consent to cookies.

Contains information related to marketing campaigns of the user. These are shared with Google AdWords / Google Ads when the Google Ads and Google Analytics accounts are linked together.

90 days

__utma

ID used to identify users and sessions

2 years after last activity

__utmt

Used to monitor number of Google Analytics server requests

10 minutes

__utmb

Used to distinguish new sessions and visits. This cookie is set when the GA.js javascript library is loaded and there is no existing __utmb cookie. The cookie is updated every time data is sent to the Google Analytics server.

30 minutes after last activity

__utmc

Used only with old Urchin versions of Google Analytics and not with GA.js. Was used to distinguish between new sessions and visits at the end of a session.

End of session (browser)

__utmz

Contains information about the traffic source or campaign that directed user to the website. The cookie is set when the GA.js javascript is loaded and updated when data is sent to the Google Anaytics server

6 months after last activity

__utmv

Contains custom information set by the web developer via the _setCustomVar method in Google Analytics. This cookie is updated every time new data is sent to the Google Analytics server.

2 years after last activity

__utmx

Used to determine whether a user is included in an A / B or Multivariate test.

18 months

_ga

ID used to identify users

2 years

_gali

Used by Google Analytics to determine which links on a page are being clicked

30 seconds

_ga_

ID used to identify users

2 years

_gid

ID used to identify users for 24 hours after last activity

24 hours

_gat

Used to monitor number of Google Analytics server requests when using Google Tag Manager