Accounts Receivable Factoring can quickly meet the working capital needs of a manufacturer.

Versant’s underwriting focus is solely on the quality of a company’s accounts receivable, which enables us to rapidly fund businesses which do not qualify for traditional lending.

Factoring Program Overview

$100,000 to $30 Million

Non-recourse

Flexible Term

Ideal for B2B or B2G

We fund challenging deals:

Start-ups

Losses

Highly Leveraged

Customer Concentrations

Weak Personal Credit

Character Issues

In about a week, we can advance against accounts receivable to qualified businesses which include Distributors as well as Service Providers.

Accounts receivable factoring is a financial strategy that allows businesses to convert their outstanding invoices into immediate cash. This comprehensive summary explores the significant benefits that accounts receivable factoring offers, particularly for small and medium-sized enterprises (SMEs) and businesses experiencing rapid growth or facing cash flow challenges.

At its core, accounts receivable factoring involves a business (the seller) selling its invoices to a third-party financial institution (the factor) at a discount. In return, the business receives a substantial portion of the invoice value upfront, typically between 70% and 95%. The remaining balance, minus the factor’s fee, is paid to the business once the customer settles the invoice with the factor. This mechanism effectively transforms a future payment into current working capital, bridging the gap between providing goods or services and receiving payment.

One of the most compelling benefits of accounts receivable factoring is its ability to improve cash flow instantly. Many businesses, especially those operating on credit terms (e.g., Net 30, Net 60), often face periods of tight cash flow due to delayed payments from customers. Factoring eliminates this waiting period, providing immediate access to funds that can be used to cover operational expenses, purchase inventory, meet payroll, or seize new opportunities. This rapid liquidity is a game-changer for businesses that cannot afford to wait weeks or months for their invoices to be paid.

Beyond immediate cash, factoring offers enhanced working capital. Unlike traditional loans, factoring is not a debt. It’s the sale of an asset (your invoices). This means it doesn’t add liabilities to your balance sheet, making your financial position appear stronger to potential lenders or investors. The funds obtained through factoring can be continuously reinvested into the business, supporting ongoing growth and stability without incurring new debt.

Another significant advantage is access to funding regardless of credit history. Traditional bank loans often require a strong credit score, substantial collateral, and a lengthy application process. Accounts receivable factoring, however, primarily focuses on the creditworthiness of your customers. If your customers have a good payment history, your business is likely to qualify for factoring, even if your own credit history is less than perfect or if you’re a new business with limited financial history. This makes it an accessible funding option for a wider range of businesses.

Factoring also provides protection against slow-paying customers, particularly with “non-recourse” factoring. In non-recourse factoring, the factor assumes the credit risk associated with the invoice. If the customer fails to pay due to bankruptcy or insolvency, the factor bears the loss, not your business. This offers a valuable layer of financial security, allowing businesses to extend credit terms with greater confidence. While non-recourse factoring typically comes with a slightly higher fee, the peace of mind it offers can be invaluable. Even in “recourse” factoring, where your business remains responsible for unpaid invoices, the immediate cash flow benefit is still substantial.

Furthermore, factoring can reduce administrative burden and collection costs. When you factor your invoices, the factor often takes over the responsibility of credit checking customers and collecting payments. This frees up your internal resources, allowing your team to focus on core business activities like sales, production, and customer service, rather than spending time on collections. For businesses without dedicated collections departments, this can be a significant cost and time saver.

For businesses experiencing rapid growth, accounts receivable factoring provides the necessary capital to scale operations. As sales increase, so does the need for working capital to fund production, acquire raw materials, and manage increased overheads. Factoring ensures that cash flow keeps pace with growth, preventing a cash crunch that could otherwise hinder expansion. It provides a flexible funding solution that grows with your sales volume – the more invoices you generate, the more funding you can access.

Lastly, factoring can offer improved financial predictability. By converting fluctuating customer payment cycles into a consistent influx of cash, businesses can better forecast their finances and plan for future expenditures. This stability allows for more strategic decision-making and reduces the stress associated with unpredictable cash flow.

While accounts receivable factoring offers numerous benefits, businesses should also consider the costs (the factoring fee), the relationship with the factor, and how the process might impact customer relations (as customers will be dealing with the factor for payments). However, for many businesses seeking immediate liquidity, flexible funding, and reduced financial risk, accounts receivable factoring stands out as a powerful and effective financial tool. It empowers businesses to unlock the value of their outstanding invoices, turning potential cash flow challenges into opportunities for growth and stability.

Accounts Receivable Factoring $100,000 to $30 Million Quick AR Advances No Long-Term Commitment Non-recourse Funding in about a week

We are a great match for businesses with traits such as: Less than 2 years old Negative Net Worth Losses Customer Concentrations Weak Credit Character Issues

Chris Lehnes | Factoring Specialist | 203-664-1535 | chris@chrislehnes.com

SaaS companies are often challenged to obtain the working capital needed to continue to innovate, increase revenue and expand their customer base, but raising equity prematurely can unnecessarily dilute founder’s equity.

By factoring, SaaS companies get quick access to the funds needed to leverage their technology for success without giving up equity.

Accounts Receivable Factoring

$100,000 to $30 Million

Quick AR Advances

No Long-Term Commitment

Non-recourse

Funding in about a week

We are a great match for businesses with traits such as:

Discover how accounts receivable factoring can transform your small business by providing the essential working capital you need to grow and thrive. In under 60 seconds, learn how selling your unpaid invoices to a factoring company can improve cash flow, reduce financial stress, and empower you to seize new opportunities. Featuring inspiring visuals of successful retail owners, this quick guide highlights why factoring is a smart solution for managing finances without taking on debt. Whether you’re looking to expand inventory, cover payroll, or invest in marketing, factoring offers a flexible and reliable cash flow boost. Don’t miss out on unlocking your business’s full potential today!

Accounts Receivable Factoring $100,000 to $30 Million Quick AR Advances No Long-Term Commitment Non-recourse Funding in about a week

We are a great match for businesses with traits such as: Less than 2 years old Negative Net Worth Losses Customer Concentrations Weak Credit Character Issues

Chris Lehnes | Factoring Specialist | 203-664-1535 | chris@chrislehnes.com

If your clients are like many small business owners, they have probably faced the frustrating gap between sending an invoice and actually getting paid.

Our Non-Recourse Accounts Receivable Factoring Program offers a smart solution.

Instead of waiting for customers to pay, factoring provides immediate access to the funds tied up in unpaid invoices. That means more money to meet payroll, restock inventory, invest in growth, or simply keep operations running smoothly.

Program Overview

$100,000 to $30 Million

Non-Recourse

No Audits

No Financial Covenants

Most businesses with strong customers eligible

We specialize in difficult deals:

Start-ups

Weak Balance Sheets

Historic Losses

Customer Concentrations

Poor Personal Credit

Character Issues

We focus on the quality of your client’s accounts receivable, ignoring their financial condition.

This enables us to move quickly and fund qualified businesses including Manufacturers, Distributors and a wide variety of Service Businesses in as few as 3-5 days. Contact me today to learn if your client is a fit.

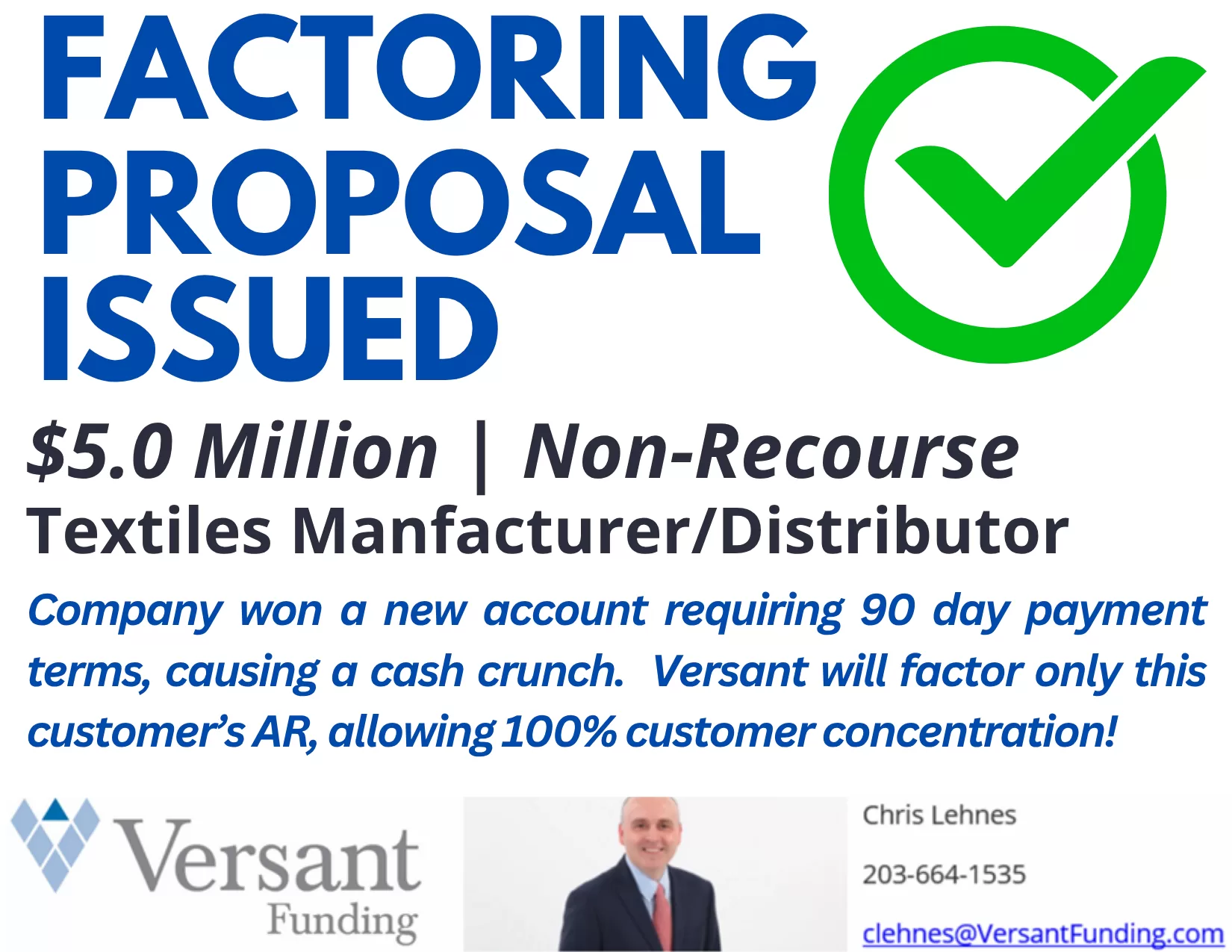

Non-Recourse Factoring Proposal Issued – $5 Million – Textiles

Company won a new account requiring 90 day payment terms, causing a cash crunch. Versant will factor only this customer’s AR, allowing 100% customer concentration!

Accounts Receivable Factoring $100,000 to $30 Million Quick AR Advances No Long-Term Commitment Non-recourse Funding in about a week

We are a great match for businesses with traits such as: Less than 2 years old Negative Net Worth Losses Customer Concentrations Weak Credit Character Issues

Chris Lehnes | Factoring Specialist | 203-664-1535 | chris@chrislehnes.com

Leveraging SaaS to Boost Efficiency in Small Businesses

Small Businesses and SaaS

In an increasingly digital world, small businesses face immense pressure to remain competitive, agile, and efficient. Fortunately, Software as a Service (SaaS) has emerged as a transformative solution, offering access to powerful tools and platforms without the need for heavy infrastructure or extensive IT staff. From customer relationship management to accounting and collaboration, SaaS empowers small businesses to streamline operations, reduce costs, and scale effectively. This article explores how small businesses can leverage SaaS to improve efficiency across various facets of their operations.

What is SaaS?

Software as a Service (SaaS) is a cloud-based model that delivers software applications over the internet. Unlike traditional software, which requires installation and maintenance on individual machines, SaaS applications are hosted remotely and accessed via web browsers. This eliminates the need for on-premise infrastructure and provides real-time access to data and tools.

Key Characteristics of SaaS:

Subscription-based pricing

Cloud-hosted and accessible via the internet

Automatic updates and maintenance

Scalability and flexibility

Cross-device compatibility

Popular examples of SaaS include Google Workspace, Salesforce, QuickBooks Online, and Slack. These platforms are designed to help businesses manage workflows, communicate effectively, and enhance customer relationships

Benefits of SaaS for Small Businesses

1. Cost Efficiency

One of the most appealing aspects of SaaS for small businesses is its affordability. Traditional software often requires a significant upfront investment for licenses, hardware, and IT support. SaaS, by contrast, operates on a subscription model, allowing businesses to pay a manageable monthly or annual fee. This model significantly reduces capital expenditures and allows for predictable budgeting.

Moreover, SaaS providers handle updates, maintenance, and security, further reducing the need for an in-house IT team.

2. Scalability and Flexibility

As businesses grow, their software needs evolve. SaaS platforms are inherently scalable, allowing small businesses to upgrade their plans or add users without major disruptions. Whether a company is hiring new employees or expanding into new markets, SaaS solutions can be adjusted to match the pace of growth.

3. Accessibility and Remote Work Enablement

With SaaS, employees can access work-related applications from anywhere with an internet connection. This flexibility supports remote work and enables teams to collaborate across locations. In the wake of the COVID-19 pandemic, the ability to work from home has become essential for business continuity.

4. Integration and Automation

SaaS applications often come with APIs and integration capabilities, allowing them to connect with other tools and platforms. This interoperability reduces manual data entry and streamlines workflows. For example, a CRM tool can be integrated with email marketing software to automate customer outreach based on user behavior.

5. Enhanced Security

Leading SaaS providers invest heavily in security protocols to protect customer data. These measures typically exceed what small businesses could afford on their own. Features such as encryption, multi-factor authentication, and regular backups are standard in many SaaS offerings.

6. Rapid Deployment and Ease of Use

SaaS applications are typically user-friendly and require minimal setup. This means small businesses can implement new tools quickly and start seeing benefits immediately. Many SaaS providers also offer training resources and customer support to assist with onboarding.

Key Areas Where SaaS Enhances Efficiency

1. Customer Relationship Management (CRM)

CRM systems help businesses manage interactions with current and potential customers. SaaS-based CRMs like Salesforce, HubSpot, and Zoho CRM provide a centralized platform to track leads, sales, and customer communications.

Efficiency Gains:

Automated follow-ups and reminders

Real-time sales analytics

Improved customer segmentation and targeting

Enhanced customer service through shared data access

2. Accounting and Finance

SaaS accounting platforms such as QuickBooks Online, Xero, and FreshBooks simplify bookkeeping, invoicing, and financial reporting. These tools reduce the need for manual data entry and help ensure compliance with tax regulations.

Efficiency Gains:

Real-time financial tracking

Automated invoice generation and reminders

Seamless bank integration

Easy collaboration with accountants and financial advisors

3. Project Management and Collaboration

Platforms like Trello, Asana, Monday.com, and ClickUp facilitate task management and team collaboration. These tools allow small businesses to track progress, assign responsibilities, and communicate effectively.

Efficiency Gains:

Centralized task and project tracking

Integrated communication channels

Time tracking and deadline management

Improved accountability and transparency

4. Marketing and Sales Automation

SaaS marketing tools such as Mailchimp, ActiveCampaign, and Hootsuite enable small businesses to execute marketing campaigns with minimal effort. These platforms often include features like email automation, social media scheduling, and customer analytics.

Efficiency Gains:

Automated email workflows

Audience segmentation

Social media management from a single dashboard

Performance analytics and A/B testing

5. Human Resources and Payroll

SaaS solutions for HR, like Gusto, BambooHR, and Zenefits, simplify employee onboarding, time tracking, benefits administration, and payroll processing.

Efficiency Gains:

Automated payroll and tax filing

Self-service portals for employees

Centralized employee records

Compliance tracking and reporting

6. E-commerce and Point of Sale (POS)

Platforms like Shopify, Square, and WooCommerce provide small businesses with end-to-end solutions for online and in-store sales. These systems integrate inventory management, sales reporting, and customer insights.

Efficiency Gains:

Seamless online store setup

Integrated payment processing

Inventory and order tracking

Marketing and SEO tools

7. Document Management and eSignatures

Tools like DocuSign, Adobe Acrobat Sign, and PandaDoc allow businesses to manage contracts and obtain electronic signatures securely.

Efficiency Gains:

Faster document turnaround

Secure and compliant digital signature solutions

Template creation and reuse

Reduced reliance on physical paperwork

Industry-Specific SaaS Solutions

While general-purpose SaaS platforms offer broad utility, industry-specific tools provide tailored functionality to meet niche requirements.

1. Healthcare

Practice management: Kareo, SimplePractice

Telehealth: Doxy.me, Amwell

2. Retail

Inventory management: Vend, Lightspeed

POS systems: Clover, Shopify POS

3. Legal Services

Case management: Clio, MyCase

Billing and time tracking: TimeSolv, Bill4Time

4. Real Estate

CRM and listing management: BoomTown, Follow Up Boss

Document signing and storage: Dotloop, DocuSign

5. Construction

Project management: Procore, Buildertrend

Estimating and bidding: CoConstruct, JobNimbus

Strategies for Successful SaaS Implementation

1. Identify Business Needs

Before selecting a SaaS solution, small businesses should assess their pain points and define clear objectives. This ensures that the chosen software aligns with actual business needs and priorities.

2. Evaluate Vendors

Factors to consider when choosing a SaaS provider include:

Pricing and contract terms

Features and scalability

User reviews and case studies

Customer support and onboarding services

3. Ensure Data Security and Compliance

Businesses must understand how their data is stored, who has access, and what compliance standards the provider follows (e.g., GDPR, HIPAA). A thorough review of the provider’s security policies is essential.

4. Plan for Integration

Choose SaaS tools that integrate with existing systems. This reduces data silos and improves overall efficiency. API availability and third-party integrations should be part of the selection criteria.

5. Train Employees

Even the best software is only as effective as its users. Provide comprehensive training to ensure that staff can utilize the tools efficiently. Many SaaS providers offer tutorials, webinars, and support resources.

6. Monitor Performance

Track key performance indicators (KPIs) to measure the impact of SaaS tools on business operations. Common metrics include productivity, cost savings, customer satisfaction, and revenue growth.

Common Challenges and How to Overcome Them

1. Resistance to Change

Employees may be hesitant to adopt new tools. Overcome this by involving them early in the selection process and highlighting the benefits of the new system.

2. Overwhelming Choice

With thousands of SaaS products on the market, it can be difficult to choose the right one. Focus on specific business needs and prioritize platforms with a proven track record.

3. Subscription Creep

Using too many SaaS tools can lead to higher costs and overlapping functionality. Regularly audit your subscriptions to eliminate redundancy and consolidate where possible.

4. Data Migration Issues

Transitioning from legacy systems to SaaS platforms can involve complex data migration. Work with vendors who offer migration support and test the new system thoroughly before going live.

5. Dependence on Internet Connectivity

SaaS tools require a stable internet connection. Ensure that your business has reliable connectivity and consider offline-access features where necessary.

Case Studies

Case Study 1: Boosting Productivity with a CRM

A small digital marketing agency struggled to manage client communication and track leads. After implementing HubSpot CRM, they automated follow-ups, centralized contact data, and improved client retention by 25%.

Case Study 2: Streamlining Accounting Processes

A family-run retail store adopted QuickBooks Online to replace manual bookkeeping. This move reduced accounting errors by 40% and saved over 10 hours per week in administrative work.

Case Study 3: Enhancing Team Collaboration

A remote design firm used Trello and Slack to coordinate projects across multiple time zones. These tools allowed them to manage deadlines more effectively and reduce project delivery times by 30%.

Case Study 4: Automating Marketing for Growth

An e-commerce startup used Mailchimp to automate their email campaigns. By segmenting their audience and using A/B testing, they increased their email open rates by 20% and sales by 15% in three months.

The Future of SaaS for Small Businesses

The SaaS market is poised for continued growth, with innovations such as artificial intelligence (AI), machine learning (ML), and advanced analytics reshaping how businesses operate. Future SaaS tools will offer even more automation, predictive insights, and personalization.

Emerging Trends:

AI-powered chatbots and customer service

Predictive analytics for sales and marketing

Workflow automation across departments

Industry-specific microservices

As these tools become more accessible, small businesses will be better equipped to compete with larger enterprises.

Conclusion

SaaS offers small businesses an unparalleled opportunity to improve efficiency, reduce costs, and scale operations. From CRM and accounting to marketing and HR, SaaS tools provide the agility and functionality that modern businesses need to thrive. By selecting the right solutions, integrating them effectively, and fostering a culture of continuous improvement, small businesses can harness the full potential of SaaS and position themselves for sustained success.

As technology continues to evolve, staying informed and adaptable will be key. Small businesses that embrace SaaS not only survive in a competitive marketplace but also unlock new avenues for innovation and growth.

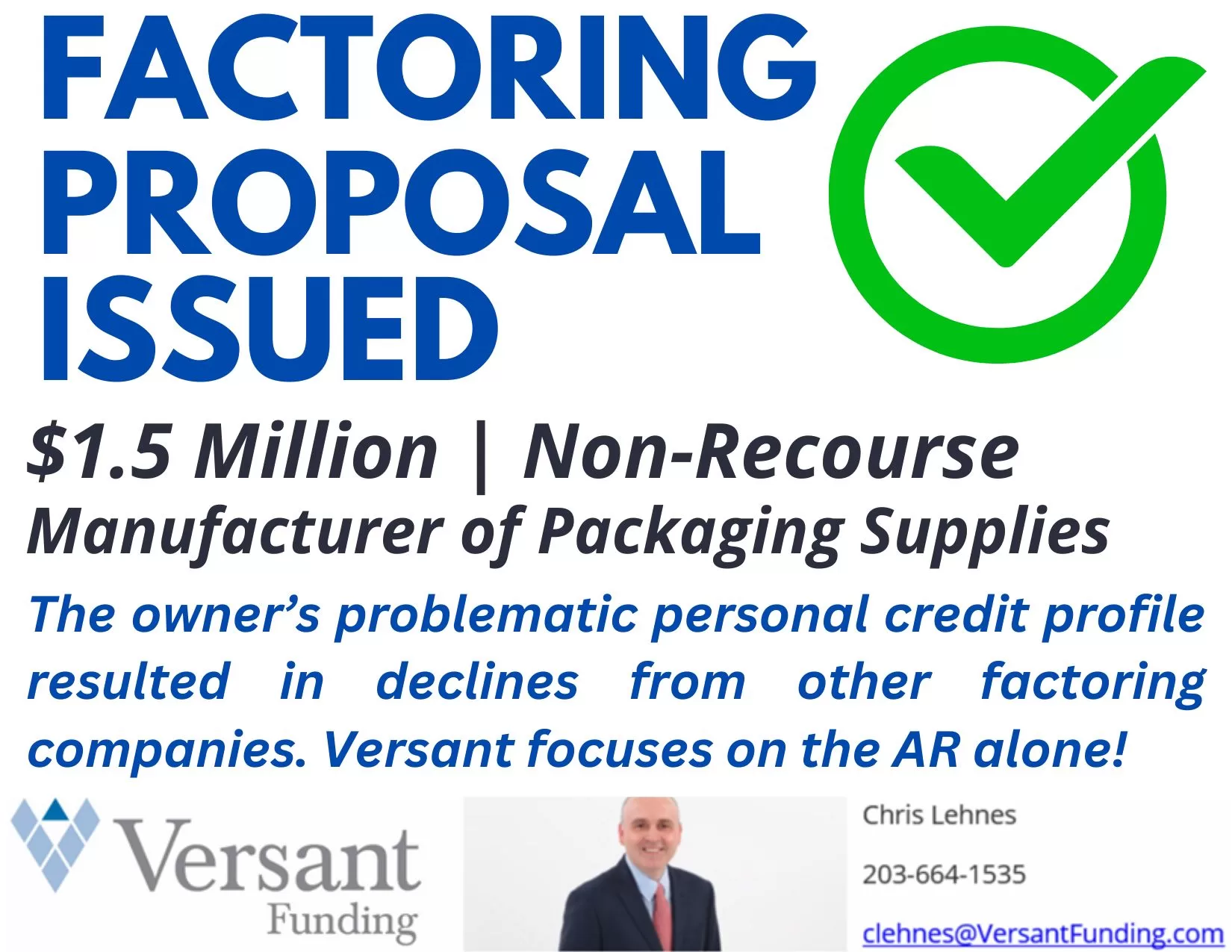

Factoring Proposal Issued: $1.5 Million | Manufacturer: The owner’s problematic personal credit profile resulted in declines from other factoring companies. Versant focuses on the AR alone!

Accounts Receivable Factoring $100,000 to $30 Million Quick AR Advances No Long-Term Commitment Non-recourse Funding in about a week

We are a great match for businesses with traits such as: Less than 2 years old Negative Net Worth Losses Customer Concentrations Weak Credit Character Issues

Chris Lehnes | Factoring Specialist | 203-664-1535 | chris@chrislehnes.com

The Small Business Administration (SBA) has historically served as a lifeline for entrepreneurs across the United States. By facilitating access to loans, offering training and mentorship programs, and providing disaster relief, the SBA has played a critical role in supporting the country’s economic backbone: small businesses. However, recent federal budgetary decisions and administrative restructuring have led to significant cuts within the agency. These changes are having far-reaching consequences for small businesses, especially those in underserved or rural areas.

Strategic SBA Reorganization or Service Erosion?

In early 2025, the SBA announced a sweeping reorganization initiative aimed at increasing efficiency and aligning the agency more closely with its core missions. Key elements of the plan included a 43% reduction in staff and the decentralization of services from the central office to regional and field locations. The agency maintained that these steps were designed to streamline operations, focus on disaster response and capital access, and eliminate redundant positions created during the COVID-19 pandemic.

While the SBA leadership emphasized that essential services would not be impacted, many stakeholders expressed skepticism. Reducing the workforce by nearly half is likely to limit the SBA’s capacity to respond to the diverse and often urgent needs of small businesses. The decrease in personnel could result in slower loan processing times, fewer outreach initiatives, and diminished ability to provide personalized guidance and mentorship.

Budget Cuts to Core SBA Programs

In addition to organizational restructuring, the SBA has faced deep funding cuts under recent federal budget proposals. These proposed reductions affect multiple programs that are crucial to the vitality and success of small businesses.

Entrepreneurial Development

One of the most significant impacts is to entrepreneurial development programs. Funding reductions threaten the future of Women’s Business Centers, Veteran Business Outreach Centers, and mentorship networks like SCORE. These programs have helped thousands of entrepreneurs gain business knowledge, refine their strategies, and connect with experienced mentors. With fewer resources, their ability to serve communities will inevitably diminish.

Access to Capital in Underserved Areas

Cuts to funding for Community Development Financial Institutions (CDFIs) represent another major setback. CDFIs provide critical capital to minority-owned businesses, startups, and entrepreneurs in economically disadvantaged areas who often struggle to secure traditional financing. Reducing this support could curtail business development in communities already facing economic hardship.

Rural Business Support

Small businesses in rural America may be among the hardest hit. Rural Development programs—formerly bolstered through agencies such as the USDA—have experienced reductions that could jeopardize initiatives like broadband expansion and renewable energy improvements. Without these investments, rural entrepreneurs may face increasing difficulty in competing with their urban counterparts.

Real-World Effects: Entrepreneurs Speak Out

The ramifications of these policy shifts are not merely theoretical; they are being felt on the ground by small business owners across the country.

Jacob Thomas, a third-generation farmer in Kansas, has seen his family’s modest farm struggle after the elimination of federal programs that once purchased produce directly from small farms. This loss of income has led to a 10% drop in revenue, threatening the long-term viability of the operation.

Similarly, small manufacturers and food producers in rural areas have made investments in energy-efficient infrastructure based on the expectation of receiving government rebates and support. With those programs now on hold or dramatically scaled back, these businesses are left shouldering costs they hadn’t planned to bear alone.

Additionally, entrepreneurs from underserved communities report increasing difficulties in accessing capital. Many relied on CDFI loans or SBA microloans to start or expand their businesses. With fewer funds and staff available to process these applications, many find themselves unable to move forward with business plans.

Political Responses and Public Pushback

These cuts have not gone unnoticed on Capitol Hill. Lawmakers from both parties have voiced concern about the potential consequences of reducing SBA resources. Some argue that in an already challenging economic environment, it is shortsighted to cut support for the very entities that generate two-thirds of net new jobs in the U.S. economy.

There is also concern about the SBA’s ability to respond effectively to future disasters. In past crises—from hurricanes to wildfires to the pandemic—the SBA was instrumental in providing emergency funding and guidance. With a smaller workforce and fewer resources, the agency’s capacity to respond quickly and efficiently to future events could be severely compromised.

In response to public and political outcry, some legislators are pushing for targeted reinvestment in programs that have shown a strong return on investment, particularly those aimed at empowering women, veterans, and minority entrepreneurs.

The Road Ahead for SBA

For many small businesses, the future is uncertain. The shift in the SBA’s priorities and the associated cuts require business owners to seek alternative support systems. Community organizations, local chambers of commerce, and state-level small business agencies may need to fill the gap left by the federal government.

Entrepreneurs will also need to become more self-reliant, utilizing digital tools and private networks to find mentorship, financing, and business development resources. However, these options are not equally accessible to all, and the risk is that the gap between well-connected entrepreneurs and those in marginalized communities will continue to widen.

At the same time, small business advocacy groups are mobilizing to push for policy reversals and increased investment. They argue that empowering small businesses is not just a matter of economic development but of social equity and national resilience.

SBA Impact Summary

The SBA has long served as a foundation of support for the entrepreneurial spirit that drives the U.S. economy. However, the agency’s recent restructuring and funding cuts are creating ripple effects that threaten to destabilize small businesses, particularly those that are most vulnerable.

Whether these changes result in long-term improvements in efficiency or lasting damage to the small business ecosystem will depend largely on how the government, private sector, and local communities respond. What is clear, though, is that small businesses are facing a new reality—one that will require adaptability, advocacy, and innovation to navigate successfully.

Is your client experiencing a working capital shortfall, unable to meet immediate funding needs for essential expenditures. With Spot Factoring, they can quickly obtain funding against a single invoice, providing vital liquidity without ongoing factoring obligations.

Contains information related to marketing campaigns of the user. These are shared with Google AdWords / Google Ads when the Google Ads and Google Analytics accounts are linked together.

90 days

__utma

ID used to identify users and sessions

2 years after last activity

__utmt

Used to monitor number of Google Analytics server requests

10 minutes

__utmb

Used to distinguish new sessions and visits. This cookie is set when the GA.js javascript library is loaded and there is no existing __utmb cookie. The cookie is updated every time data is sent to the Google Analytics server.

30 minutes after last activity

__utmc

Used only with old Urchin versions of Google Analytics and not with GA.js. Was used to distinguish between new sessions and visits at the end of a session.

End of session (browser)

__utmz

Contains information about the traffic source or campaign that directed user to the website. The cookie is set when the GA.js javascript is loaded and updated when data is sent to the Google Anaytics server

6 months after last activity

__utmv

Contains custom information set by the web developer via the _setCustomVar method in Google Analytics. This cookie is updated every time new data is sent to the Google Analytics server.

2 years after last activity

__utmx

Used to determine whether a user is included in an A / B or Multivariate test.

18 months

_ga

ID used to identify users

2 years

_gali

Used by Google Analytics to determine which links on a page are being clicked

30 seconds

_ga_

ID used to identify users

2 years

_gid

ID used to identify users for 24 hours after last activity

24 hours

_gat

Used to monitor number of Google Analytics server requests when using Google Tag Manager