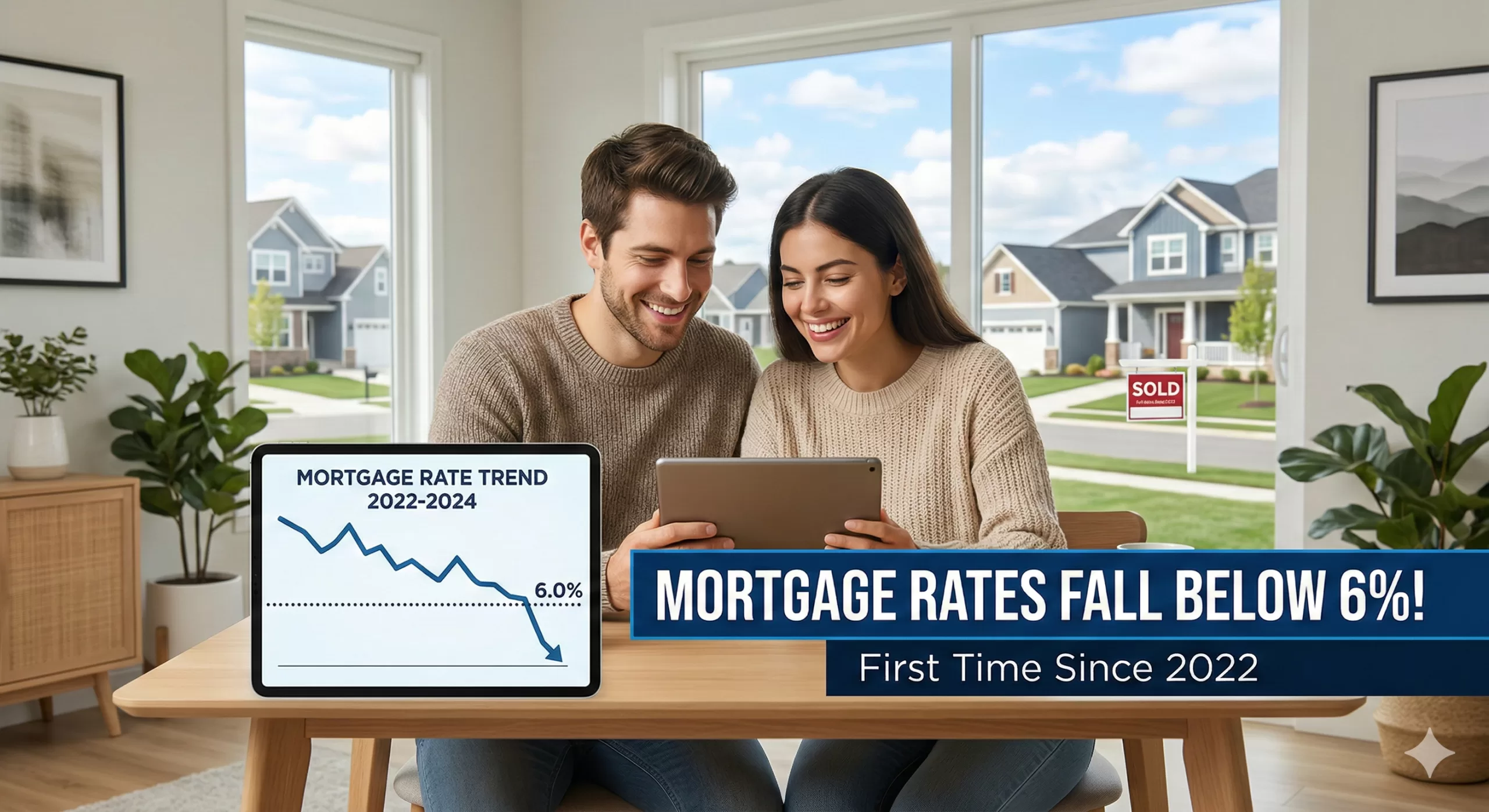

Mortgage Rates – The housing market has seen a welcome shift! Mortgage rates have fallen below 6% for the first time since 2022, offering a significant improvement for potential homebuyers. This news comes as a breath of fresh air after a period of steadily climbing rates that have put a strain on many budgets.

What Does This Mean for Potential Homebuyers?

The drop in mortgage rates translates directly into increased affordability for those looking to purchase a home. This can be beneficial in several ways:

Lower Monthly Payments: A lower interest rate means a smaller portion of your monthly payment goes towards interest, reducing your overall housing cost.

Increased Buying Power: With lower monthly payments, you may be able to qualify for a larger loan amount, potentially allowing you to purchase a more expensive home.

Refinancing Opportunities: Existing homeowners who currently have a higher mortgage rate may be able to refinance their loan and save money on their monthly payments.

Why Are Mortgage Rates Falling?

While the exact reasons behind the rate drop are complex, several factors may be contributing to the trend:

Lower Inflation: Inflation has shown signs of cooling down, which can influence interest rates.

Economic Growth: While economic growth has been moderate, some signs suggest it may be slowing, which can also affect mortgage rates.

Changes in the Bond Market: Bond yields, which are closely tied to mortgage rates, have also seen a decline.

What Should You Do Now?

If you’ve been on the fence about buying a home, this could be an excellent time to re-evaluate your options. Here are some steps to consider:

Get Pre-Approved for a Mortgage: This will give you a clear idea of how much you can borrow and help you understand your monthly payment.

Shop Around for Rates: Different lenders offer varying rates, so it’s essential to compare offers from multiple institutions.

Consider Your Long-Term Goals: While the lower rates are attractive, it’s crucial to ensure that buying a home is the right decision for your long-term financial goals.

Important Note: It’s important to remember that mortgage rates are subject to change based on economic conditions and other factors. While the current trend is encouraging, it’s essential to stay informed about any potential shifts in the market.

Conclusion:

The drop in mortgage rates below 6% is a significant development for the housing market, offering some much-needed relief to potential homebuyers and homeowners alike. If you’ve been considering buying a home, this could be the right time to take action. With lower monthly payments and increased buying power, you may be closer to achieving your homeownership goals than you thought. However, it’s crucial to act carefully and seek professional advice to make the best decision for your individual situation.

Primary Data Sources

Freddie Mac (Primary Mortgage Market Survey): The ultimate source for the 5.98% figure. Freddie Mac released its weekly report on February 26, 2026, confirming that the 30-year fixed-rate mortgage dipped below 6% for the first time in approximately 3.5 years.

The Federal Reserve (FRED): Used to verify historical trends, specifically confirming that the last time rates were at this level was September 8, 2022 (when they were 5.89%).

CBS News: Provided context on the White House’s initiatives (such as the $200 billion mortgage bond purchase plan) and expert commentary on the “spring home-buying season.”

Associated Press (AP): Detailed the influence of the 10-year Treasury yield on mortgage pricing and quoted housing economists regarding market entry for buyers and sellers.

Mortgage rates in 2026 forecast This video provides expert analysis on how these sub-6% rates impact monthly affordability and what to expect for the rest of the 2026 housing market

Remember that brief sigh of relief? The one where it felt like maybe, just maybe, the relentless march of price increases was slowing down? Well, if you’ve been to the grocery store, filled up your gas tank, or even just browsed online recently, you’ve probably noticed it: the break is over. Companies are jacking up prices again, and consumers are once again feeling the pinch.

For a while, many economists and analysts pointed to easing supply chain issues, stabilizing energy costs, and even a slight dip in consumer demand as potential signals that inflation was cooling. Some businesses even held the line on prices, perhaps hoping to retain market share or out of a genuine desire to give their customers a break.

But those days seem to be largely behind us. We’re seeing a resurgence in price hikes across a wide array of sectors. From everyday necessities to discretionary items, the numbers on the tags are climbing.

What’s Driving This Latest Surge?

Several factors are likely contributing to this renewed upward trend:

Persistent Input Costs: While some raw material costs have stabilized, others continue to be elevated. Labor costs are also a significant factor, with many businesses facing pressure to offer higher wages to attract and retain employees. These increased operational expenses often get passed on to the consumer.

Strong Consumer Demand (Still): Despite earlier predictions of a significant slowdown, consumer demand has proven remarkably resilient in many areas. When demand remains high, businesses have less incentive to lower prices and more leeway to raise them.

“Catch-Up” Pricing: Some companies might feel they absorbed increased costs for a period and are now playing catch-up, adjusting prices to reflect their sustained operational expenses.

Geopolitical Factors: Global events continue to create volatility in commodity markets, particularly for energy and certain raw materials, which inevitably impacts production and transportation costs.

Profit Margins: Let’s be honest, businesses are in the business of making a profit. If they perceive an opportunity to increase their margins without significantly impacting sales volume, many will take it.

What Does This Mean for You?

For the average household, this renewed wave of price increases means a continued squeeze on budgets. Discretionary spending may need to be curtailed further, and even essential purchases will require more careful planning. Savings might deplete faster, and the goal of financial stability could feel increasingly distant.

How Can Consumers Cope?

While we can’t control the broader economic forces at play, there are strategies consumers can employ to mitigate the impact:

Become a Savvy Shopper: Compare prices diligently, look for sales and discounts, and consider generic or store-brand alternatives.

Budgeting is Key: Revisit your budget and identify areas where you can cut back. Track your spending to understand exactly where your money is going.

Prioritize Needs vs. Wants: Distinguish between essential purchases and items that can be deferred or eliminated.

Support Local (Where Affordable): Sometimes local businesses, with lower overheads, can offer competitive pricing, or at least you’re supporting your community.

Advocate for Yourself: When possible, negotiate prices for services, or look for loyalty programs that offer discounts.

The “break” from rising prices was indeed short-lived. As companies continue to adjust their pricing strategies, it’s more important than ever for consumers to be vigilant, adapt their spending habits, and advocate for their financial well-being.

In a surprising turn of events, German factory orders in have shown an unexpected and robust surge, signaling a potentially stronger-than-anticipated rebound in the nation’s industrial sector. This latest data has instilled a renewed sense of optimism among economists and policymakers, suggesting that Europe’s largest economy might be on a more solid recovery path than previously estimated.

The Federal Statistical Office announced this morning that new factory orders jumped by a significant margin in the past month, far exceeding analyst expectations. This remarkable uptick follows a period of cautious growth and even some contractions, making the current surge all the more impactful. The increase was broad-based, with both domestic and international orders contributing substantially to the overall rise.

A Deeper Dive into the Numbers

The reported increase in orders was particularly driven by strong demand for capital goods, indicating that businesses are investing more in machinery and equipment – a key indicator of future production capacity and confidence. Intermediate goods also saw a healthy boost, suggesting renewed activity across various supply chains.

Economists are pointing to several factors contributing to this positive development. A resilient global demand, particularly from key trading partners, appears to be playing a significant role. Furthermore, a gradual easing of supply chain bottlenecks, which have plagued manufacturers for months, is allowing companies to fulfill orders more efficiently and take on new business.

Impact on the Broader Economy

This unexpected surge in factory orders is a shot in the arm for the German economy, which has been grappling with persistent inflation and the lingering effects of global uncertainties. A strong industrial sector is crucial for Germany’s economic health, as it is a major employer and a significant contributor to GDP. The improved outlook could lead to increased hiring, higher wages, and ultimately, stronger consumer spending.

The latest economic data brings a sigh of relief for consumers and policymakers alike, as U.S. inflation has shown a more significant easing than anticipated at the beginning of the year. This positive development suggests that efforts to tame rising prices may be gaining traction, offering a glimmer of hope for greater economic stability in the months to come.

For much of the past year, inflation has been a persistent headwind, impacting everything from grocery bills to housing costs. The robust labor market, while a sign of economic strength, also contributed to upward price pressures. However, recent reports indicate a potential shift in this trend.

Several factors appear to be contributing to this welcome slowdown. Supply chain disruptions, which were a major catalyst for price increases, have largely improved. This has allowed for a more consistent flow of goods, reducing bottlenecks and associated costs. Additionally, the Federal Reserve’s aggressive monetary policy, including multiple interest rate hikes, seems to be having its intended effect of cooling demand and reining in inflationary expectations.

While the easing of inflation is certainly good news, it’s important to maintain a balanced perspective. The economy is a complex system, and various forces are constantly at play. Energy prices, geopolitical events, and shifts in consumer spending habits can all influence the trajectory of inflation. Therefore, continuous monitoring and adaptive policymaking will remain crucial.

What does this mean for the average American? For starters, it could translate into less pressure on household budgets over time. If the trend continues, we might see more stable prices for everyday goods and services, allowing purchasing power to stretch further. It also provides the Federal Reserve with more flexibility in its future policy decisions, potentially reducing the need for further aggressive rate hikes.

The journey to sustained price stability is an ongoing one, but the early signs from this year are undoubtedly encouraging. It’s a testament to the resilience of the U.S. economy and the effectiveness of concerted efforts to address inflationary pressures. As we move further into the year, economists and consumers alike will be watching closely to see if this promising trend continues, paving the way for a more predictable and stable economic environment.

Home Sales Take a January Dip: What Does It Mean for the Market?

The housing market, often a dynamic and unpredictable beast, just delivered a notable headline: home sales in January experienced their most significant monthly decline in nearly four years. This news might spark a bit of anxiety for some, and perhaps a glimmer of hope for others. But what’s truly behind this downturn, and what could it signal for the months ahead?

According to recent reports, the seasonally adjusted annual rate of existing home sales saw a substantial drop last month. This marks a notable shift after a period where the market showed some signs of stabilizing, or even modest recovery, in late 2023.

What’s Driving the Decline?

Several factors are likely at play in this January slump:

Mortgage Rate Volatility: While rates have come down from their peaks, they’ve also experienced some upward swings, creating uncertainty for prospective buyers. Higher rates directly impact affordability, pushing some buyers to the sidelines.

Persistent Inventory Shortages: Despite the dip in sales, the fundamental issue of low housing inventory remains a significant challenge in many areas. Fewer homes on the market mean less choice for buyers, and can still keep prices elevated, even with softening demand.

Seasonal Slowdown (Exacerbated): January is typically a slower month for real estate activity due to holidays and winter weather. However, the magnitude of this decline suggests more than just a typical seasonal lull. It could indicate that underlying market pressures are intensifying.

Affordability Challenges: The combination of elevated home prices and higher interest rates continues to stretch buyer budgets thin. For many, especially first-time homebuyers, the dream of homeownership remains a distant one.

Economic Uncertainty: Broader economic concerns, even if subtle, can influence consumer confidence. Worries about inflation, job security, or a potential recession can lead people to postpone major financial decisions like buying a home.

Is This the Start of a Larger Trend?

It’s crucial not to jump to conclusions based on a single month’s data. Real estate markets are complex and influenced by numerous variables. However, a decline of this magnitude certainly warrants close attention.

Potential for Price Adjustments: A sustained drop in demand, particularly if inventory levels begin to rise, could eventually lead to more significant price corrections in some markets. Buyers who have been waiting for prices to come down might see this as a positive sign.

Opportunity for Buyers? For those who are financially secure and ready to buy, a less competitive market could present opportunities. Fewer bidding wars and potentially more negotiating power could be on the horizon if the trend continues.

Impact on Sellers: Sellers might need to adjust their expectations. Pricing strategically and ensuring homes are in top condition will become even more critical in a market where buyers have more leverage.

Looking Ahead

The coming months will be telling. We’ll need to watch several key indicators:

Mortgage Rate Movements: Any significant and sustained drop in interest rates would likely bring buyers back into the market.

Inventory Levels: A notable increase in homes for sale would help alleviate pressure and potentially lead to more balanced market conditions.

Economic Data: Broader economic health, including inflation and employment figures, will continue to play a role in consumer confidence and housing demand.

While January’s numbers present a cautious start to the year for the housing market, they also highlight the ongoing adjustments and recalibrations happening. Whether this dip is a temporary blip or a harbinger of more significant changes remains to be seen, but it’s a clear reminder that the real estate landscape is always evolving.

The results of recent surveys, most notably the Capital One Middle Market Strategic Investments report, have sent a ripple of confidence through the business community: 89% of middle-market companies are optimistic about their growth in 2026.

For those who track the “engine room” of the U.S. economy, this isn’t just a number—it’s a signal of a major strategic pivot. After years of playing defense against inflation and supply chain “whack-a-mole,” the middle market is moving back to offense.

Here is my take on why the “Mighty Middle” is feeling so bullish and what this means for the year ahead.

1. The “Big Beautiful Bill” Effect

A significant driver of this 89% figure is the One Big Beautiful Bill Act (OBBBA) passed in late 2025. Middle-market leaders aren’t just aware of the policy; they are already building it into their spreadsheets.

Tax Certainty: By codifying full expensing of capital expenditures and maintaining the 21% corporate tax rate, the bill has removed the “wait and see” hurdle that often stalls big investments.

Cash Flow: 59% of companies expect improved cash flow through these incentives, giving them the “dry powder” needed to expand.

2. AI: From “Hype” to “Help”

In 2024 and 2025, AI was a buzzword. In 2026, it’s a budget line item.

Operational Efficiency: 66% of middle-market businesses are prioritizing AI investment, not to replace humans, but to solve the persistent labor crunch.

ROI Focus: Unlike the “growth at all costs” tech era, middle-market firms are looking for AI to deliver specific returns—29% expect AI to be their highest-yielding investment this year.

3. Resilience Through “Alternate” Means

What I find most fascinating is the evolution of middle-market financing. With traditional bank lending remaining tight, 50% of these companies are now pursuing alternate financing, specifically private credit.

The Takeaway: Middle-market companies are no longer at the mercy of traditional interest rate cycles. They have diversified their “oxygen supply” (capital), allowing them to stay optimistic even when the Fed is being cautious.

4. The M&A “Spring”

After a multi-year slumber, deal-making is waking up. Nearly 44% of middle-market firms intend to pursue acquisitions in 2026. This suggests that the optimism isn’t just about internal growth; it’s about consolidation and picking up smaller players who may not have the scale to handle 2026’s regulatory and technological demands.

The Bottom Line: Execution is the New Strategy

The 89% optimism rate doesn’t mean the road is easy. Leaders are still citing inflation (97%) and tariffs as major headaches. However, the difference in 2026 is preparedness.

Middle-market companies have spent the last two years “stress-testing” their models. They are leaner, more tech-forward, and more agile than they were pre-2020. If 89% of them believe they can win this year, the rest of the market should probably pay attention.

The “Mighty Middle” is playing offense in 2026. 🚀

The numbers are in, and they are striking: 89% of middle-market companies are officially optimistic about their growth this year.

After years of navigating the “whack-a-mole” challenges of inflation and supply chain disruptions, we are seeing a massive strategic pivot. Middle-market leaders aren’t just surviving; they are scaling.

Why the surge in confidence?

The OBBBA Effect: Tax certainty and full expensing are providing the “dry powder” needed for major capital investments.

AI Integration: We’ve moved past the hype. Companies are now budgeting for AI to solve real-world labor shortages and drive operational efficiency.

Alternative Financing: With traditional bank lending remaining tight, the shift toward private credit and alternative capital sources is keeping growth on track.

M&A Resurgence: Nearly 44% of these firms are looking to acquire, signaling a year of consolidation and expansion.

The bottom line? These companies have “stress-tested” their models for two years. They are leaner, tech-forward, and ready to win.

Is the Middle Market the new economic bellwether for 2026? 📈

The data is hard to ignore: 89% of middle-market firms are entering 2026 with high optimism. This isn’t just “wishful thinking”—it’s a calculated response to a shifting fiscal and technological landscape.

Here are the four pillars driving this confidence:

Fiscal tailwinds: The One Big Beautiful Bill Act (OBBBA) has finally provided the tax certainty and full-expensing incentives required to move “wait-and-see” capital into active deployments.

Maturity in AI adoption: We have moved beyond the “hype cycle.” 66% of mid-cap leaders are now prioritizing AI as a tool for operational leverage, specifically targeting persistent labor bottlenecks.

The Rise of Alternative Credit: As traditional bank lending remains constrained, the pivot toward private credit and specialized liquidity solutions has decoupled middle-market growth from traditional interest rate volatility.

Strategic Consolidation: With 44% of firms pursuing M&A, we are entering a period of significant market “up-tiering.”

The “Mighty Middle” has spent the last 24 months stress-testing their balance sheets. In 2026, they aren’t just defending their position—they are expanding it.

Our Accounts Receivable Factoring program can quickly meet the working capital needs of businesses in the energy industry.

Versant’s underwriting focus is solely on the quality of a company’s accounts receivable, which enables us to rapidly fund businesses which do not qualify for traditional lending.

Let’s explore the potential trends in its Gross Domestic Product (GDP) growth rate throughout 2025. While no one has a crystal ball, we can analyze current trajectories, expert projections, and potential influencing factors to paint a picture of what lies ahead.

The Current Economic Pulse (Briefly looking back at late 2024)

To understand 2025, it’s crucial to acknowledge the economic momentum (or lack thereof) leading into it. We’re likely seeing a continued moderation from the robust growth experienced in the immediate post-pandemic recovery. Inflation, while hopefully tamer, will still be a key variable, influencing consumer spending and investment. Interest rates, dictated by the Federal Reserve, will also play a significant role. Let’s imagine a snapshot of the US economy as we enter 2025.

Q1 2025: A Cautious Start?

As 2025 kicks off, many economists anticipate a period of continued cautious growth. Businesses may still be adjusting to lingering supply chain complexities and a potentially tighter labor market. Consumer spending, the bedrock of the US economy, might see moderate gains, influenced by real wage growth (or lack thereof) and household savings levels. Investment in new projects could be selective, driven by a desire for efficiency and technological advancement. We might see the GDP growth rate hover in the lower to mid-2% range during this initial quarter.

Q2 2025: Finding its Rhythm

Moving into the second quarter, we could witness the economy starting to find a more stable rhythm. Factors such as potentially easing inflationary pressures and a clearer outlook on monetary policy could provide more certainty for businesses and consumers. We might see a slight uptick in manufacturing activity and continued strength in the services sector. Technological innovation, particularly in areas like AI and green energy, could begin to show more tangible contributions to productivity.

Q3 2025: Potential for Acceleration

The third quarter often provides a good indicator of annual performance, and 2025 could see some positive momentum building. If global economic conditions stabilize and major geopolitical tensions remain subdued, US exports could see a boost. Domestically, renewed consumer confidence, perhaps fueled by a strong job market and stable prices, could lead to increased discretionary spending. Business investment might also pick up as companies look to capitalize on growth opportunities. This could be a quarter where GDP growth nudges closer to the mid-2% to even 3% range. Imagine the vibrancy of a thriving economy in full swing.

Q4 2025: A Strong Finish or Continued Moderation?

The final quarter of 2025 will be crucial in determining the overall annual growth rate. Much will depend on the preceding quarters’ performance and any new unforeseen global or domestic events. A strong holiday shopping season, robust corporate earnings, and continued investment in key sectors could lead to a solid finish. However, potential headwinds like persistent inflation or unexpected global economic slowdowns could temper growth. The Federal Reserve’s stance on interest rates will also be keenly watched. The year could conclude with growth stabilizing, setting the stage for 2026.

Key Influencing Factors for 2025:

Inflation and Interest Rates: The Fed’s ability to manage inflation without stifling growth will be paramount.

Consumer Spending: The health of the consumer, driven by wages, employment, and savings, is always a critical determinant.

Business Investment: Companies’ willingness to invest in expansion, R&D, and technology will fuel future growth.

Global Economic Health: International trade and geopolitical stability will have a ripple effect on the US economy.

Technological Advancement: Innovations in AI, automation, and green technologies could boost productivity.

In conclusion, 2025 is shaping up to be a year of continued adaptation and potential growth for the US economy. While we can anticipate some fluctuations, a path of cautious yet steady expansion seems to be the prevailing view among many analysts. The resilience and dynamism of the American economy will undoubtedly be tested, but its capacity for innovation and recovery remains a powerful force.

As the Federal Open Market Committee (FOMC) wraps up its final meeting of 2025 today, all eyes are on the 2:00 PM EST announcement. With the U.S. economy cooling and the labor market showing signs of strain, speculation is high that a Fed Cut in rates is imminent.

Here is a breakdown of the current predictions, the economic data driving the decision, and what odds makers are betting on.

The Consensus: A “December Cut” is Highly Likely

Market watchers are overwhelmingly pricing in a 25-basis-point (0.25%) rate cut.

According to the CME FedWatch Tool, which tracks trading in federal funds futures, there is currently an 87% probability that the Fed will lower the target range to 3.50%–3.75%. This would mark the third consecutive rate reduction, following cuts in September and October, signaling a definitive shift from fighting inflation to supporting the labor market.

Key Factors the Fed is Weighing

The Fed’s “dual mandate” requires it to balance stable prices with maximum employment. For the first time in years, the risks have shifted from overheating inflation to a cooling jobs market.

1. The Cooling Labor Market (The Primary Driver) The unemployment rate has ticked up to 4.4%, a figure that has caught the attention of Fed Chair Jerome Powell. While historically low, the steady rise suggests that high interest rates are finally biting into corporate hiring. Job growth has slowed, and layoffs in sensitive sectors have increased. The Fed is keen to avoid a “hard landing” where unemployment spikes uncontrollably.

2. Sticky but Manageable Inflation Inflation hasn’t disappeared, but it is no longer the five-alarm fire it was two years ago. The latest PCE (Personal Consumption Expenditures) data places headline inflation around 2.7%–2.9%, with core inflation hovering near 2.8%. While this is still above the Fed’s 2% target, it is trending in the right direction, giving the central bank “air cover” to cut rates to support jobs without immediately reigniting price hikes.

3. Economic Growth (GDP) GDP growth has moderated to an annualized rate of roughly 1.8%–2.0%. This suggests the economy is slowing down but not crashing—the definition of the elusive “soft landing.” A rate cut now is viewed as insurance to keep this momentum from stalling out completely in early 2026.

The “Wild Card”: A Divided Committee

Despite the high odds of a cut, this meeting is not without tension. Reports suggest the FOMC is sharply divided.

** The Doves (Cut Now):** Worried that waiting too long will cause a recession. They argue that with inflation falling, real interest rates are effectively rising, tightening financial conditions more than intended.

The Hawks (Pause/Hold): Concerned that cutting rates too quickly could cause inflation to flare up again, especially given that the economy is still growing.

Because of this division, the language in today’s statement will be just as important as the rate decision itself. Investors should look for clues about a “pause” in January. Many analysts believe the Fed may cut today but signal a skip in the next meeting to assess the impact of recent cuts.

What to Watch For

2:00 PM EST: The official statement and decision. Look for the “dot plot” (Summary of Economic Projections) to see where officials expect rates to be at the end of 2026.

2:30 PM EST: Chair Jerome Powell’s press conference. His tone regarding the “balance of risks” will move markets. If he sounds more worried about jobs than inflation, it will confirm that the easing cycle has further to go.

Bottom Line

While nothing is guaranteed until the gavel falls, the smart money is on a 0.25% cut today. The Fed likely views the rising unemployment rate as a warning light it cannot ignore, making a rate reduction the prudent move to secure a soft landing for 2026.

Category

Case for a Rate Cut (The “Doves”)

Case for Holding Steady (The “Hawks”)

Labor Market

Rising Risks: Unemployment has climbed to 4.4%. Doves argue that high rates are now doing unnecessary damage to hiring.

Hidden Strength: Some argue the job market is “normalizing” after the post-pandemic surge rather than collapsing.

Inflation

Progress Made: While at 2.8%, inflation is down significantly from its peak. High “real” rates (inflation vs. interest) are overly restrictive.

Sticky Prices: Inflation remains above the 2% target. Rate cuts could embolden businesses to keep prices high or raise them.

Economic Growth

Growth is Slowing: GDP growth has dipped toward 1.8%. A cut acts as “insurance” to prevent a recession in 2026.

Consumer Resilience: High durable goods spending suggests the economy is not yet in need of a stimulus.

Market Impact

Easing the Burden: Lower rates would provide immediate relief for credit card holders and small businesses facing high debt costs.

Asset Bubbles: Cutting too soon could overheat the stock and housing markets, leading to a boom-bust cycle.

The Federal Reserve has decided to cut the benchmark interest rate by 25 basis points (0.25%).

This move lowers the target range for the federal funds rate to 3.50% to 3.75%. This is the third consecutive rate cut this year and was made in light of elevated inflation and a weakening labor market.

Here are the key takeaways from the announcement and Chair Jerome Powell’s press conference:

✂️ Key Interest Rate Decision

The Cut: The Federal Open Market Committee (FOMC) voted to lower the target range for the federal funds rate by 25 basis points to 3.50%–3.75%.

The Vote: The decision was not unanimous, recording a 9:3 ratio of votes.

One member (Stephen I. Miran) preferred a larger, 50-basis-point cut.

Two members (Austan D. Goolsbee and Jeffrey R. Schmid) preferred no change, keeping the rate steady.

🎙️ Key Quotes and Context from Chair Powell

Powell’s remarks focused on the shifting balance of risks and the current policy stance:

Rationale for the Cut:“With today’s decision, we have lowered our policy rate three-quarters of a percentage point over our last three meetings. This further normalization of our policy stance should help stabilize the labor market while allowing inflation to resume its downward trend toward 2% once the effects of tariffs have passed through.”

The Dual Mandate Challenge: Powell acknowledged the difficulty of balancing the Fed’s two goals (maximum employment and price stability):”In the near term, risks to inflation are tilted to the upside and risks to employment to the downside—a challenging situation… We have one tool. It can’t do both of those—you can’t address both of those at once.”

Forward Guidance (What’s Next): The Fed indicated a cautious, data-dependent approach moving forward:”In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks.” When asked about a pause, Powell suggested the policy rate is now close to the “neutral” level: He indicated that the Fed’s benchmark rate is now likely somewhere close to the “neutral” level… which certainly indicates that he won’t be in a hurry to extend the string of cuts the Fed has made in recent months.

Economic Outlook and Projections (“Dot Plot”): The latest projections indicated a divided committee on future cuts.

The median Fed official is penciling in one rate cut for next year (2026), which is a more cautious outlook than some market expectations.

The Fed projects inflation (based on its preferred gauge) to ease to 2.4% by the end of 2026.

Based on the immediate market data and analyst reactions following the 2:00 PM announcement, here is how the decision is impacting mortgage rates and the stock market.

🏠 Impact on Mortgage Rates

The Verdict: Rates may hold steady or even tick up slightly, despite the Fed cutting rates.

Counter-Intuitive Movement: It often surprises borrowers, but mortgage rates do not move 1-for-1 with the Fed’s rate. Mortgage rates track the 10-year Treasury yield, which actually rose today (hitting roughly 4.21%).

Why? The market had already “priced in” this cut weeks ago. Investors are now looking ahead to 2026. Because the Fed signaled a slower pace for future cuts (a “hawkish cut”), bond markets reacted by pushing long-term yields higher.

Forecast: Experts expect 30-year fixed mortgage rates to hover in the low-to-mid 6% range for now. A significant drop below 6% is unlikely until investors see clearer signs that inflation is permanently defeated.

📈 Impact on the Stock Market

The Verdict: A “Santa Claus Rally” is likely, but 2026 looks choppier.

Immediate Reaction: The S&P 500 and Dow Jones both rose following the news, pushing close to all-time highs. The market “got what it wanted”—a cut to support the economy without panic.

Sector Watch:

Small Caps (Russell 2000): Often benefit most from rate cuts as they rely more on floating-rate debt.

Tech & Growth: Continued to show strength, though valuations remain high.

2026 Outlook: The Fed’s “dot plot” shows they plan to slow down, potentially cutting rates only once in 2026. This is fewer cuts than Wall Street hoped for, which suggests the “easy money” rally might face headwinds early next year as recession risks are still on the table (J.P. Morgan analysts cite a 35% recession probability for 2026).

Area

Short-Term Forecast (Dec ’25)

Why?

Mortgage Rates

Steady / Slight Rise

The cut was already priced in; long-term bond yields are rising.

Stocks

Bullish (Rally)

The “soft landing” narrative is intact; investors are relieved.

Savings Accounts

Slight Drop

High-yield savings rates will drop almost immediately by ~0.25%.

Federal Reserve Monetary Policy and Leadership Outlook

Executive Summary

The Federal Reserve has implemented its second consecutive monthly interest rate cut, lowering the target range by a quarter-point to 3.75%-4.0%. The 10-2 vote by the Federal Open Market Committee (FOMC) highlights internal division among policymakers regarding the path of monetary policy, a decision made amidst sustained pressure from President Donald Trump for more aggressive easing. The outlook for future cuts remains uncertain, complicated by an ongoing federal government shutdown that has postponed the release of critical economic data on inflation and unemployment. Despite this data blackout, investor sentiment currently favors another quarter-point reduction in December, supported by recent private-sector reports indicating a “softening” labor market. Concurrently, the administration is actively considering a successor for Fed Chair Jerome Powell, whose term expires in May 2026, with a list of five candidates being prepared for the President’s review.

——————————————————————————–

I. October 2025 Interest Rate Decision

The Federal Open Market Committee (FOMC) voted on Wednesday, October 29, 2025, to lower its benchmark interest rate, marking the second straight month of monetary easing.

Rate Adjustment: The committee approved a quarter-point reduction.

New Target Range: The interest rate is now set to a range between 3.75% and 4.0%.

Previous Target Range: This is down from the 4.0% to 4.25% range established at the previous month’s meeting.

Committee Vote: The decision passed with a 10-2 vote, indicating some dissent among policymakers regarding the move.

II. Influencing Factors and Economic Context

The Fed’s decision-making process is being influenced by a combination of political pressure, economic data limitations, and emerging concerns about the labor market.

A. Political Pressure

The rate cut follows months of public pressure and criticism from President Donald Trump.

The President has been advocating for steeper and more aggressive cuts to monetary policy.

B. Economic Data Blackout

An ongoing federal government shutdown has significantly hampered the Fed’s ability to assess the U.S. economy’s health.

Key economic reports, including those on inflation and unemployment, have been postponed.

Fed Governor Christopher Waller acknowledged the challenge, stating that because policymakers “don’t know which way the data will break on this conflict,” the FOMC must “move with care” when adjusting rates.

In the absence of official data, Waller noted he has spoken with “business contacts” to help form his economic outlook.

C. Labor Market Concerns

Fed Governor Christopher Waller indicated his focus has shifted from inflation to a “softening” labor market, a stance that supported his vote for the recent rate cut.

This view is corroborated by reports from several firms and economists released in recent weeks, which suggest the labor market has continued to deteriorate. This emerging private-sector data could provide the FOMC with a rationale for an additional rate cut.

III. Future Monetary Policy Outlook

Market expectations are leaning towards further easing, though Fed officials have previously expressed division on the matter.

Investor Expectations: According to CME’s FedWatch tool, investors are favoring an additional quarter-point interest rate reduction at the FOMC’s final 2025 meeting in December.

Potential December Rate: Such a cut would lower the target range to between 3.5% and 3.75%.

Official Division: Minutes from the previous month’s meeting showed that Fed officials were divided on whether a third rate cut in the year would be necessary.

IV. Federal Reserve Leadership Transition

The administration is actively planning for the future leadership of the central bank as the end of Chair Jerome Powell’s term approaches.

Chair’s Term: Jerome Powell’s term as Federal Reserve Chair is set to expire in May 2026.

Succession Plan: Treasury Secretary Scott Bessent confirmed on Monday that a list of candidates to succeed Powell would be presented to President Trump shortly after Thanksgiving.

Candidate Shortlist: Bessent identified five individuals currently under consideration for the role:

Four Cracks in the Foundation: What the Fed’s Rate Cut Really Reveals

Introduction: Beyond the Headlines

The Federal Reserve has cut interest rates for the second straight month, a headline that suggests a confident response to evolving economic conditions. But simmering beneath the surface are the persistent calls for even easier monetary policy from the White House, adding a layer of political drama to an already difficult decision.

A closer look reveals that this rate cut is not a confident step forward; it’s a hesitant move by a divided committee flying blind in a political storm. The real story isn’t the cut itself, but the four converging pressures that expose a deeper crisis of confidence inside our nation’s central bank. But what’s really happening behind those closed doors?

This analysis breaks down the four most impactful and surprising takeaways from the Federal Reserve’s latest move, revealing a clearer picture of the profound challenges shaping U.S. economic policy today and the volatility that may lie ahead.

1. The Fed is Divided: This Was Not a Unanimous Decision

The Federal Open Market Committee (FOMC) voted to lower its key interest rate by a quarter-point, setting the new range between 3.75% and 4%, down from the previous 4% to 4.25%. The critical detail, however, was the 10-2 vote. This rare public dissent reveals deep fractures in the FOMC’s consensus about the path forward.

For markets and businesses, a divided Fed is an unpredictable Fed. This lack of consensus makes it significantly harder to forecast future policy, injecting a fresh dose of potential volatility into the economy. This internal disagreement is hardly surprising, given that policymakers are being forced to navigate without their most trusted instruments.

2. Flying Blind: The Fed is Making Decisions Without Key Data

Compounding the internal division is a startling “data blackout.” An ongoing federal government shutdown has postponed the release of official reports on inflation and unemployment—the two most vital metrics the central bank relies on. This data vacuum forces the Fed to make billion-dollar decisions in a veritable fog.

Policymakers are left to rely on alternative, anecdotal evidence. Fed Governor Christopher Waller noted he has been speaking with “business contacts” to form his economic outlook. While necessary, this reliance on informal data is fraught with risk. It lacks statistical rigor, is potentially biased, and dramatically increases the danger of a policy misstep. As Governor Waller himself acknowledged, this precarious situation demands extreme caution.

…because policymakers “don’t know which way the data will break on this conflict,” the FOMC would “need to move with care” when adjusting interest rates.

3. The Focus is Shifting: A “Softening” Labor Market is the New Top Concern

For months, inflation has been the Fed’s primary dragon to slay. Now, a monumental shift is underway. Fed Governor Christopher Waller recently stated his focus has pivoted from inflation to the “softening” labor market.

The significance of this pivot cannot be overstated. It signals that the Fed’s tolerance for inflation may be increasing if the alternative is rising unemployment. This represents a critical change in the central bank’s risk assessment, prioritizing job preservation over absolute price stability for the first time in this cycle. With recent reports from private firms suggesting the labor market has continued to deteriorate, the committee may find the justification it needs for another cut in December.

4. Political Pressure and a Looming Leadership Change

The Fed’s internal challenges are amplified by significant external pressures, most notably from President Donald Trump, who has been publicly demanding “steeper cuts.” This external pressure from the White House further complicates the internal debates, potentially widening the rift between committee members who prioritize preemptive action and those who advocate for patience.

This political context is intensified by an impending leadership transition. Fed Chair Jerome Powell’s term expires in May 2026, and the conversation about his successor has already begun. Treasury Secretary Scott Bessent has confirmed five candidates are under consideration:

Fed Governor Christopher Waller

Fed Governor Michelle Bowman

Former Fed Governor Kevin Warsh

National Economic Council Director Kevin Hassett

BlackRock executive Rick Rieder

Conclusion: Navigating in a Fog

The Federal Reserve’s latest interest rate cut is not a sign of clear sailing but rather a reflection of an institution navigating through a dense fog. Plagued by internal fractures, a critical lack of official economic data, and persistent political pressure, the central bank is operating under an extraordinary degree of uncertainty. This complex reality is far more revealing than the simple headline of another rate cut.

With the economy’s true health obscured by a data blackout, can the divided Fed steer us clear of a downturn, or is more volatility inevitable?

The Fed’s Big Move: What an Interest Rate Cut Means for You and the Economy

Introduction: Demystifying the Fed’s Power

The Federal Reserve is one of the most powerful economic forces in the United States, and its decisions can ripple through the entire country. The purpose of this article is to explain, in plain language, what the Federal Reserve is, why it changes interest rates, and what its most recent decision means for the economy. At the heart of these critical decisions is a small but influential group known as the FOMC.

1. Who Decides? Meet the FOMC

The Federal Open Market Committee (FOMC) is the part of the Federal Reserve that votes on the nation’s monetary policy, including whether to raise or lower interest rates. Their decisions, however, are not always unanimous. The most recent vote, for instance, was 10-2, which shows that there can be differing opinions among the committee members on the best path forward for the economy.

Now that we know who makes the decision, let’s examine the specific action they took.

2. The Main Event: A Quarter-Point Rate Cut

The FOMC recently voted to lower its key interest rate. This marks the second straight month that the central bank has decided to ease its monetary policy.

Here is a clear breakdown of the change:

Previous Rate Range

New Rate Range

4% to 4.25%

3.75% to 4%

This “quarter-point” reduction simply means the rate was lowered by 0.25%. But a small change like this signals a significant shift in the Fed’s thinking, which leads to a crucial question: why did they make this change?

3. The ‘Why’ Behind the Cut: A Softening Economy

The primary reason for the rate cut is that policymakers are concerned about a “softening” labor market.

Fed Governor Christopher Waller highlighted this concern, indicating his focus had shifted to a “softening” labor market instead of inflation. His viewpoint is supported by recent data; reports from various firms and economists suggest that the labor market has “continued to deteriorate,” which could provide the FOMC with the evidence it needs to support an additional cut in the future.

Of course, not everyone agrees on the Fed’s actions or what should happen next.

4. A Contentious Decision: Different Views on the Economy

The Federal Reserve’s decisions are often the subject of intense debate and are made under significant outside pressure. The latest rate cut is no exception, with several competing viewpoints at play.

President Trump’s View: The President has been a vocal critic, applying pressure on the Fed and calling for “steeper cuts” to interest rates.

Internal Division: The 10-2 vote demonstrates a lack of consensus within the FOMC itself. Last month, Fed officials appeared “divided over whether to cut rates for a third time this year,” underscoring this internal disagreement.

A Data Dilemma: The Fed is facing a major challenge due to an “ongoing federal government shutdown,” which has postponed the release of key reports on inflation and unemployment. This data blackout has forced policymakers like Governor Waller to rely on conversations with their “business contacts” to form an outlook on the economy.

These debates and challenges naturally lead to questions about what the Federal Reserve might do in the future.

5. What Happens Next? Reading the Tea Leaves

Based on the current situation, the future path of interest rates remains uncertain, but there are several key things to watch.

Investor Expectations: According to CME’s FedWatch tool, investors are currently “favoring an additional quarter-point reduction” at the FOMC’s next meeting in December.

The Fed’s Caution: Governor Christopher Waller emphasized the need for prudence, stating that because policymakers “don’t know which way the data will break,” the FOMC would “need to move with care” when adjusting interest rates.

Leadership Questions: President Trump is expected to name his pick to succeed Fed Chair Jerome Powell, whose term expires in May 2026. The candidates under consideration include Fed governors Christopher Waller and Michelle Bowman, former Fed governor Kevin Warsh, National Economic Council Director Kevin Hassett, and BlackRock executive Rick Rieder.

These factors will shape the economic landscape in the months to come.

Conclusion: Your Key Takeaways

To wrap up, understanding the Federal Reserve doesn’t have to be complicated. Here are the most important lessons from their recent decision.

The Federal Reserve, through its FOMC, manages the economy by adjusting interest rates to respond to issues like a weakening labor market.

Lowering interest rates is a tool to encourage economic activity, but decisions on when and how much to cut are complex and often debated.

The Fed’s actions are influenced by economic data, political pressure, and differing expert opinions, making their future moves something that everyone, from investors to the general public, watches closely.

Cookie Consent

We use cookies to improve your experience on our site. By using our site, you consent to cookies.

Contains information related to marketing campaigns of the user. These are shared with Google AdWords / Google Ads when the Google Ads and Google Analytics accounts are linked together.

90 days

__utma

ID used to identify users and sessions

2 years after last activity

__utmt

Used to monitor number of Google Analytics server requests

10 minutes

__utmb

Used to distinguish new sessions and visits. This cookie is set when the GA.js javascript library is loaded and there is no existing __utmb cookie. The cookie is updated every time data is sent to the Google Analytics server.

30 minutes after last activity

__utmc

Used only with old Urchin versions of Google Analytics and not with GA.js. Was used to distinguish between new sessions and visits at the end of a session.

End of session (browser)

__utmz

Contains information about the traffic source or campaign that directed user to the website. The cookie is set when the GA.js javascript is loaded and updated when data is sent to the Google Anaytics server

6 months after last activity

__utmv

Contains custom information set by the web developer via the _setCustomVar method in Google Analytics. This cookie is updated every time new data is sent to the Google Analytics server.

2 years after last activity

__utmx

Used to determine whether a user is included in an A / B or Multivariate test.

18 months

_ga

ID used to identify users

2 years

_gali

Used by Google Analytics to determine which links on a page are being clicked

30 seconds

_ga_

ID used to identify users

2 years

_gid

ID used to identify users for 24 hours after last activity

24 hours

_gat

Used to monitor number of Google Analytics server requests when using Google Tag Manager