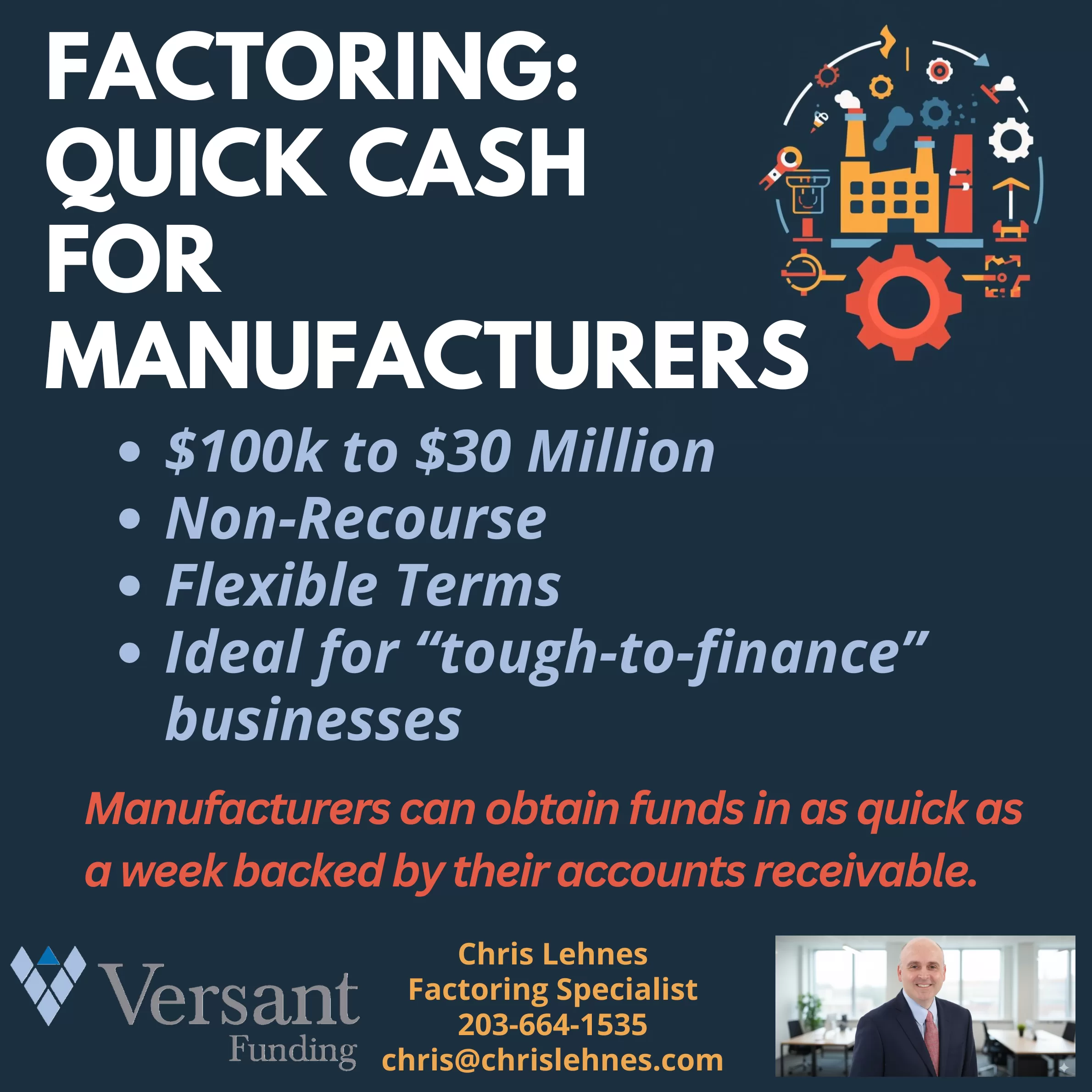

What is Factoring: In the world of distribution, the “growth paradox” is a real headache. You land a massive new retail contract—which is great news—but suddenly you’re shelling out for inventory and shipping costs while your customer sits on a 60- or 90-day payment term.

For many distributors, waiting for those invoices to clear creates a suffocating bottleneck. This is where Accounts Receivable (AR) Factoring comes in. It’s not a loan; it’s a financial tool that turns your unpaid invoices into immediate working capital.

How It Works: The Quick Breakdown

Instead of waiting months for a customer to pay, you sell your outstanding invoices to a “factor” (a specialized financial company).

- The Advance: The factor typically advances you 80% to 90% of the invoice value within 24 hours.

- The Collection: The factor handles the collection from your customer.

- The Rebate: Once the customer pays, the factor sends you the remaining balance, minus a small fee (usually 1–3%).

4 Major Benefits for Distributors

1. Bridge the Inventory Gap

Distributors often have to pay suppliers long before they get paid by their own clients. Factoring provides the liquidity to pay your manufacturers upfront, often allowing you to take advantage of early-payment discounts that can actually offset the cost of the factoring fee itself.

2. Fuel Rapid Scalability

Traditional bank loans are limited by your credit history or collateral. Factoring, however, scales with your sales. The more you sell to reputable customers, the more funding becomes available. It allows you to say “yes” to large orders that you otherwise couldn’t afford to fulfill.

3. Professional Credit Management

Many factoring companies act as an extension of your back office. They perform credit checks on your potential customers, helping you avoid “bad seeds” before you ship a single pallet. This reduces your risk of bad debt and saves your team the awkwardness of making collection calls.

4. No New Debt

Since factoring is the purchase of an asset (your invoice) rather than a loan, it doesn’t show up as debt on your balance sheet. This keeps your debt-to-equity ratio clean, making your business look much healthier to future investors or traditional lenders.

Is It Right For You?

Factoring is particularly powerful if you are:

- A startup with a thin credit history but blue-chip customers.

- Experiencing seasonal spikes that drain your cash reserves.

- Tired of the “waiting game” associated with 30, 60, or 90-day terms.

While there is a cost involved, the ability to reinvest that cash immediately into new inventory or operations often outweighs the fee. In the fast-moving world of distribution, speed is a competitive advantage.

Factoring vs. A Traditional Line of Credit: A Distributor’s Comparison

While both tools solve cash flow problems, they operate very differently. Here is how they stack up for a growing distributor:

| Feature | AR Factoring | Traditional Bank Line of Credit (LOC) |

| Funding Limit Based On… | The creditworthiness of your customers and your accounts receivable balance. | Your business’s credit history, profitability, and your collateral. |

| Speed of Funding | Extremely fast. Setup takes a few days; once active, funding often occurs within 24–48 hours of invoice verification. | Slow. The approval process can take weeks or even months. |

| Debt Type | Not Debt. It is the “asset purchase” of your invoices. | Debt. This is a loan that appears as a liability on your balance sheet. |

| Impact on Credit | Boosts Credit Score. It provides cash to pay your suppliers and operational debts on time. | Lowers “Available” Credit. Utilizing the full LOC can temporarily lower your score until it’s paid down. |

| Administrative Support | The factor often provides credit management and collection services, freeing up your back office. | You retain full responsibility for all collections and monitoring customer credit. |

| Scalability | Unlimited. As your credit-worthy sales grow, your available funding automatically increases. | Capped. Your limit is fixed and requires a re-application process to increase. |

Gemini said

Certainly. Here is a comparison table and a section you can drop directly into your blog post.

Factoring vs. A Traditional Line of Credit: A Distributor’s Comparison

While both tools solve cash flow problems, they operate very differently. Here is how they stack up for a growing distributor:

| Feature | AR Factoring | Traditional Bank Line of Credit (LOC) |

| Funding Limit Based On… | The creditworthiness of your customers and your accounts receivable balance. | Your business’s credit history, profitability, and your collateral. |

| Speed of Funding | Extremely fast. Setup takes a few days; once active, funding often occurs within 24–48 hours of invoice verification. | Slow. The approval process can take weeks or even months. |

| Debt Type | Not Debt. It is the “asset purchase” of your invoices. | Debt. This is a loan that appears as a liability on your balance sheet. |

| Impact on Credit | Boosts Credit Score. It provides cash to pay your suppliers and operational debts on time. | Lowers “Available” Credit. Utilizing the full LOC can temporarily lower your score until it’s paid down. |

| Administrative Support | The factor often provides credit management and collection services, freeing up your back office. | You retain full responsibility for all collections and monitoring customer credit. |

| Scalability | Unlimited. As your credit-worthy sales grow, your available funding automatically increases. | Capped. Your limit is fixed and requires a re-application process to increase. |

Which One Wins for Distributors?

A bank line of credit is almost always the cheapest form of capital if you can get approved for a large enough limit.

However, for distributors in a hyper-growth phase, or those whose balance sheets don’t match their ambition, AR factoring offers unmatched speed and scalability. It allows you to leverage your customers’ financial strength to fund your own growth.

The Final Verdict: When to Choose Factoring

For a distributor, the choice between factoring and other financing boils down to your growth trajectory and customer base.

A traditional bank line of credit is often the lowest-cost option, but it is also the most rigid. If you have years of steady profitability and a “boring” (predictable) growth curve, the bank is your best friend.

However, AR factoring is the superior choice if:

- You are growing faster than your cash flow allows: If a sudden 50% increase in orders would actually break your business because you can’t afford the inventory, you need factoring.

- You have “lumpy” revenue: If you deal with seasonal spikes where you need $500k in October but only $50k in January, the flexibility of factoring is unmatched.

- Your customers are larger than you: If you are a small distributor selling to giants like Walmart or Amazon, a factor will look at their multi-billion-dollar credit rating to fund you, rather than your own limited history.

Ultimately, factoring isn’t just a way to get paid early—it’s a way to weaponize your accounts receivable to outmaneuver competitors who are still stuck waiting for a check in the mail.