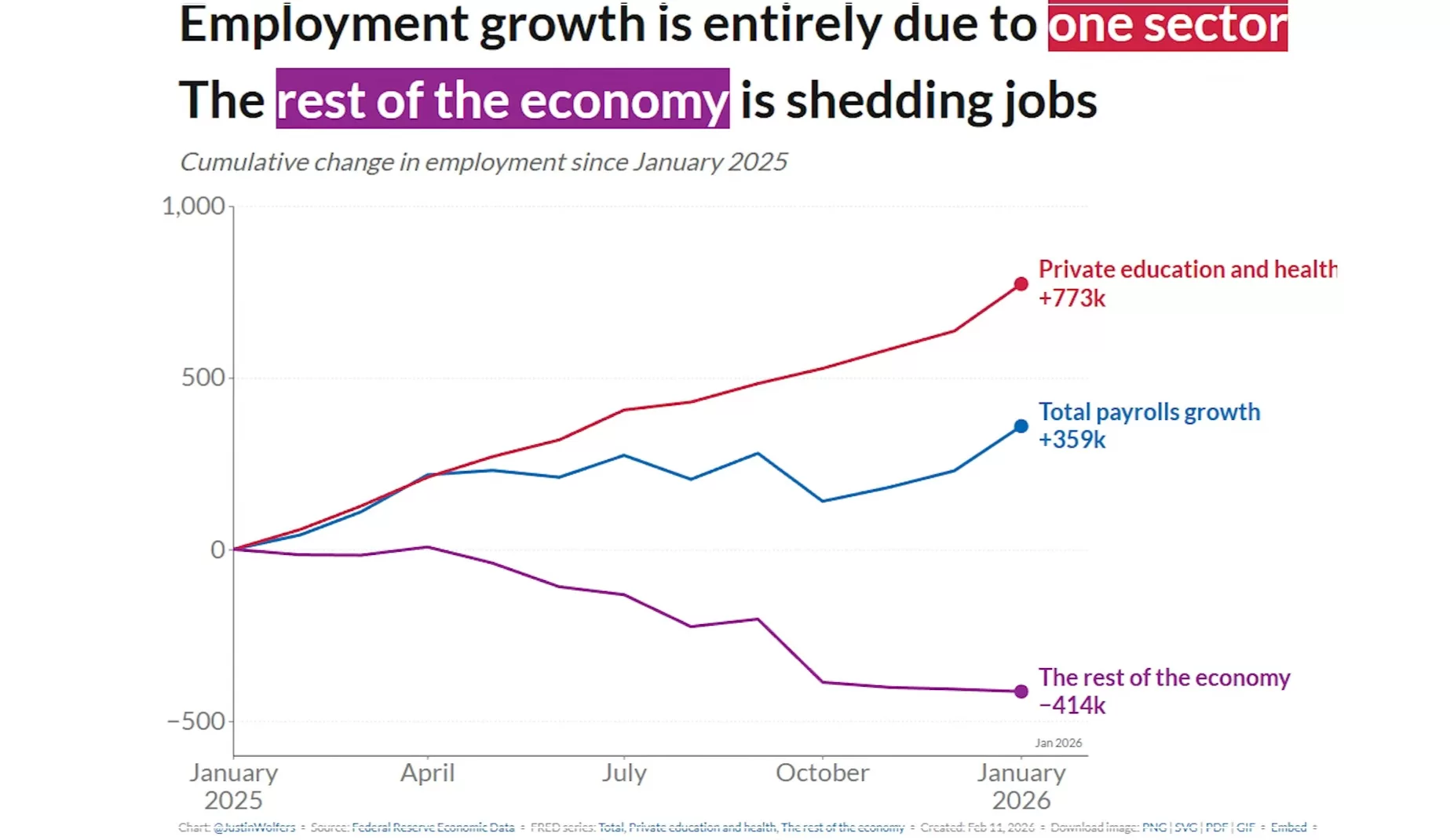

The U.S. labor market began 2026 with a surprising burst of energy, shaking off a sluggish 2025. According to the latest data from the Bureau of Labor Statistics (BLS) released on February 11, 2026, employers added 130,000 jobs in January—easily doubling December’s figures and blowing past economist expectations of roughly 70,000.

While the report was delayed by a week due to a brief federal government shutdown, the results suggest that the “hiring fatigue” seen late last year might be beginning to thaw.

The Numbers at a Glance

The January report offers a mix of resilience and necessary context for the year ahead:

- Total Jobs Added: 130,000 (up from a revised 50,000 in December).

- Unemployment Rate: Ticked down to 4.3% (from 4.4%).

- Average Hourly Earnings: Rose by 0.4% in January, bringing the year-over-year increase to 3.7%.

- Labor Force Participation: Remained steady at 62.5%.

Sector Winners and Losers

The growth wasn’t uniform across the board. In fact, a few key sectors carried the heavy lifting for the entire economy:

- Healthcare & Social Assistance: This sector remains the titan of the U.S. job market, adding 124,000 jobs (82k in healthcare and 42k in social assistance).

- Construction: Added a solid 33,000 jobs, largely driven by nonresidential specialty trade contractors.

- The Tech & White-Collar Slump: Conversely, professional and business services and manufacturing continued to struggle, reflecting ongoing shifts in AI implementation and trade policy impacts.

- Government: Federal employment saw a decline, partly a ripple effect of recent policy shifts and the temporary shutdown.

Why This Matters

After a tumultuous 2025—which was recently revised to show only 181,000 total jobs added for the entire year—this January figure is a massive sigh of relief. It suggests that while the economy isn’t sprinting, it’s found its footing.

“The January gains are a sign that the labor market is stabilizing,” says one economist. “However, the high concentration of growth in healthcare suggests a ‘one-legged stool’ economy that we need to watch closely.”

Looking Ahead

While 130,000 jobs is a “stronger footing,” the market remains complex. Layoffs in high-profile sectors like tech and transportation (notably Amazon and UPS) dominated January headlines, yet the aggregate data shows that other sectors are more than absorbing that displaced talent.

For job seekers, the message is clear: the opportunities are there, but they have shifted. Strategic hiring is the theme of 2026, with a high premium on specialized skills in healthcare, infrastructure, and adaptive technologies.

The January jobs report has effectively shifted the narrative for the Federal Reserve. While the 130,000 jobs added might seem modest by historical standards, it was a significant “beat” compared to expectations, and it has given the Fed a reason to tap the brakes on further interest rate cuts.

Here is how the latest data is influencing the Fed’s next move:

1. From “Easing” to “Holding”

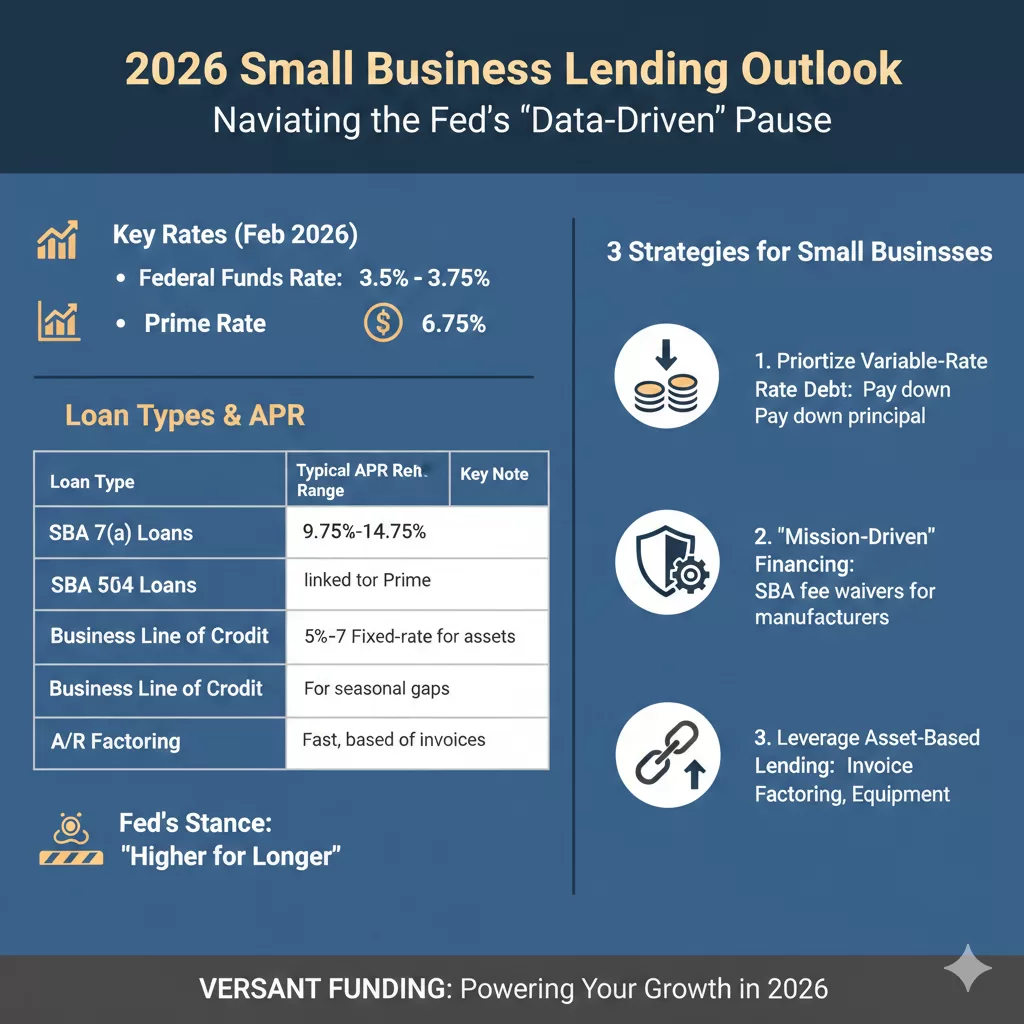

Following three consecutive rate cuts in late 2025, the Federal Reserve held rates steady at its January 28, 2026 meeting, maintaining the federal funds rate at 3.5% to 3.75%. This jobs report reinforces that “pause.”

- The Consensus: With the unemployment rate ticking down to 4.3% and job growth doubling December’s numbers, there is no longer an “emergency” need to stimulate the economy.

- Market Sentiment: Before this report, some traders were betting on a March cut. Now, CME FedWatch tools show those odds have plummeted, with the consensus moving toward a “higher for longer” stance through at least the first half of the year.

2. Emerging Internal Division

The Fed is no longer acting in total unison. The January meeting saw a rare 10-2 vote, with two dissenting members actually pushing for another 25-basis-point cut due to lingering concerns about long-term hiring weakness.

- The Hawks: Officials like Cleveland Fed President Beth Hammack and Dallas Fed President Lorie Logan have signaled that the Fed should “err on the side of patience,” arguing that current rates are “neutral”—neither helping nor hurting the economy.

- The Doves: Those worried about the “one-legged stool” (growth coming only from healthcare) fear that without more cuts, sectors like tech and manufacturing will continue to bleed jobs.

3. The “Neutral Rate” Debate

Chair Jerome Powell recently noted that the economy is on a “firm footing” entering 2026. Analysts now believe the Fed is searching for the neutral rate—the sweet spot where inflation stays at 2% without triggering a recession.

- Because average hourly earnings rose 0.4% in January (3.7% annually), the Fed is wary that cutting rates too soon could reignite inflation, especially with potential new trade tariffs on the horizon.

Key Dates to Watch

| Event | Date | Significance |

| January CPI Report | Feb 13, 2026 | Will confirm if the wage growth in the jobs report is driving up prices. |

| Fed “Beige Book” | Mar 4, 2026 | Regional reports on how small businesses are actually feeling. |

| Next FOMC Meeting | Mar 17-18, 2026 | The next formal window for a rate change decision. |

For a small business owner, the January jobs report isn’t just about hiring statistics—it’s a leading indicator for the cost of your next loan or line of credit.

Following the stronger-than-expected labor data, the Federal Reserve has hit “pause” on interest rate cuts. For businesses at Versant Funding and across the U.S., this means a period of “stabilized high” borrowing costs. Here is what your business needs to know to navigate the financial landscape of early 2026.

2026 Borrowing Outlook: The “Data-Driven” Pause

The Fed began 2026 by holding the federal funds rate steady at 3.5% to 3.75%. While the market had hoped for more aggressive easing, the surge of 130,000 new jobs in January has signaled to policymakers that the economy is not yet in need of more “cheap money.”

Current Lending Rates (As of February 2026)

| Loan Type | Typical APR Range | Key Note |

| SBA 7(a) Loans | 9.75% – 14.75% | Variable rates fluctuate with the Prime Rate (currently 6.75%). |

| SBA 504 Loans | 5% – 7% | Fixed-rate; best for long-term real estate or equipment. |

| Business Lines of Credit | 10% – 28% | Vital for seasonal inventory and payroll gaps. |

| Accounts Receivable Factoring | 24% – 36% | High speed; based on invoice value rather than credit score. |

Three Strategies for Small Businesses

With rates unlikely to drop significantly before the summer, owners should shift from “waiting for better rates” to “optimizing current cash flow.”

- Prioritize Variable-Rate Debt: If you are carrying an SBA 7(a) loan or a variable line of credit, your payments will remain flat for now. Use this stability to pay down principal where possible, as the “higher for longer” stance means interest costs won’t be melting away anytime soon.

- Look for “Mission-Driven” Financing: In 2026, the SBA is waiving guarantee fees for certain small manufacturers (NAICS 31-33). If your business fits this category, you could save thousands in upfront costs regardless of the interest rate.

- Leverage Asset-Based Lending: If traditional bank term loans are too restrictive, consider Invoice Factoring or Equipment Financing. These options often focus more on the value of your assets (your unpaid invoices or machinery) than on the Fed’s baseline rates, providing more predictable access to capital during economic volatility.

The Bottom Line

The “stronger footing” of the U.S. labor market is a double-edged sword: it proves consumer demand is resilient, but it keeps the cost of capital elevated. For 2026, the most successful businesses will be those that prioritize liquidity and debt structure over simply chasing the lowest rate.