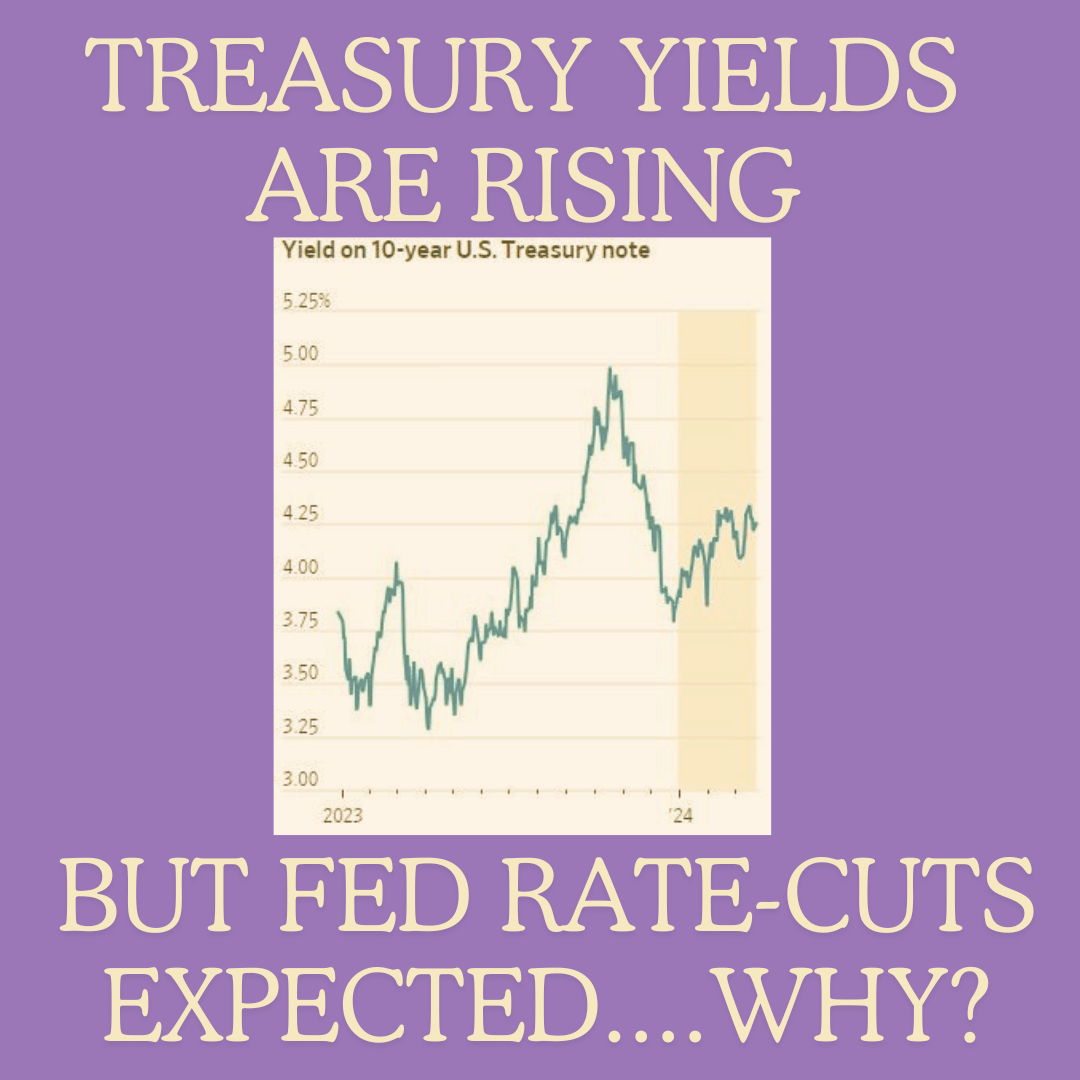

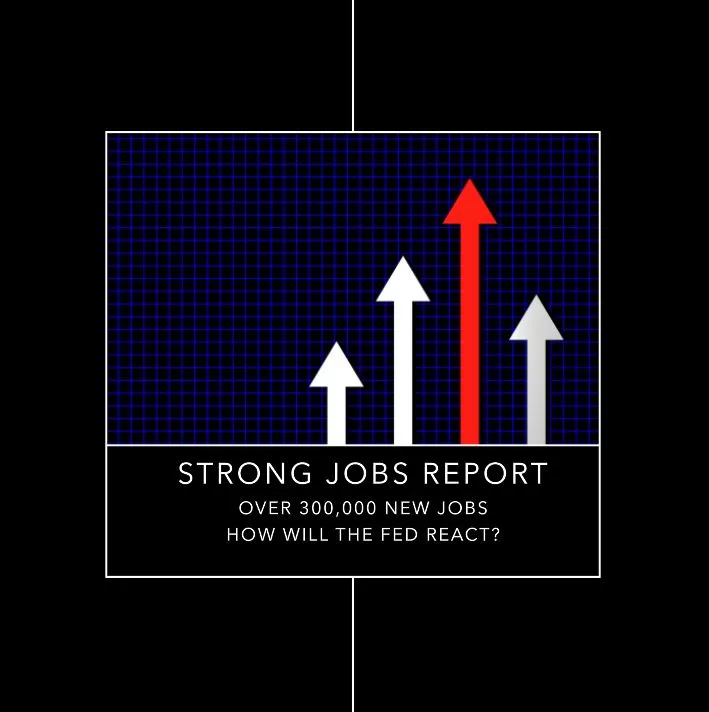

The release of the monthly jobs report by the Bureau of Labor Statistics is a highly anticipated event in financial markets, providing critical insights into the health of the labor market and broader economic conditions. As investors and analysts digest the latest employment figures, attention inevitably turns to the Federal Reserve and its monetary policy decisions. Today’s jobs report is no exception, with market participants eagerly awaiting clues about the Federal Reserve’s stance on interest rates and the path of monetary policy. So, how might today’s jobs report impact the Federal Reserve’s interest rate policy? Strong Jobs Report – Over 300,000 Jobs – How will The Fed React?

Context and Background:

The jobs report serves as a key barometer of economic vitality, offering a snapshot of employment trends, wage growth, and labor force participation. Metrics such as nonfarm payrolls, unemployment rate, and average hourly earnings provide valuable insights into the strength of the labor market and its implications for broader economic growth. Against the backdrop of the post-pandemic recovery and inflationary pressures, today’s jobs report takes on added significance, influencing market expectations for future monetary policy actions by the Federal Reserve. Strong Jobs Report – Over 300,000 Jobs – How will The Fed React?

Employment Data and Monetary Policy:

The Federal Reserve’s monetary policy decisions are guided by its dual mandate of maximum employment and price stability. As such, changes in labor market conditions play a crucial role in shaping the central bank’s interest rate policy. Strong employment growth, declining unemployment, and rising wages may prompt the Federal Reserve to consider tightening monetary policy by raising interest rates to prevent overheating and curb inflationary pressures. Conversely, weak job growth, elevated unemployment, and stagnant wages may lead the Federal Reserve to maintain or even ease its monetary policy stance to support economic recovery and job creation.

Inflationary Pressures:

One factor that the Federal Reserve closely monitors in interpreting the jobs report is its implications for inflationary pressures. A tight labor market characterized by low unemployment and robust wage growth may fuel inflationary pressures as businesses face higher labor costs and pass them on to consumers in the form of higher prices. In response, the Federal Reserve may opt to raise interest rates to cool off the economy and prevent inflation from spiraling out of control. Conversely, sluggish job growth and subdued wage inflation may alleviate concerns about inflation, providing leeway for the Federal Reserve to maintain accommodative monetary policy. Strong Jobs Report – Over 300,000 Jobs – How will The Fed React?

Market Reaction and Forward Guidance:

Market participants closely scrutinize the jobs report for clues about the Federal Reserve’s future policy trajectory, particularly regarding interest rate decisions. Any surprises in the employment data, whether positive or negative, can trigger volatility in financial markets as investors adjust their expectations for interest rates and bond yields. Additionally, investors parse through the accompanying statements and speeches by Federal Reserve officials for insights into their views on the labor market and monetary policy outlook, shaping market sentiment and asset prices in the process.

Conclusion:

Today’s jobs report holds significant implications for the Federal Reserve’s interest rate policy and broader economic conditions. As investors and analysts digest the latest employment figures, they will assess their impact on the Federal Reserve’s dual mandate of maximum employment and price stability. Whether the data signal a tightening or easing of monetary policy, today’s jobs report will undoubtedly shape market expectations and influence investment decisions in the weeks and months ahead.

Learn more about accounts receivable factoring

Connect with Factoring Specialist, Chris Lehnes on LinkedIn