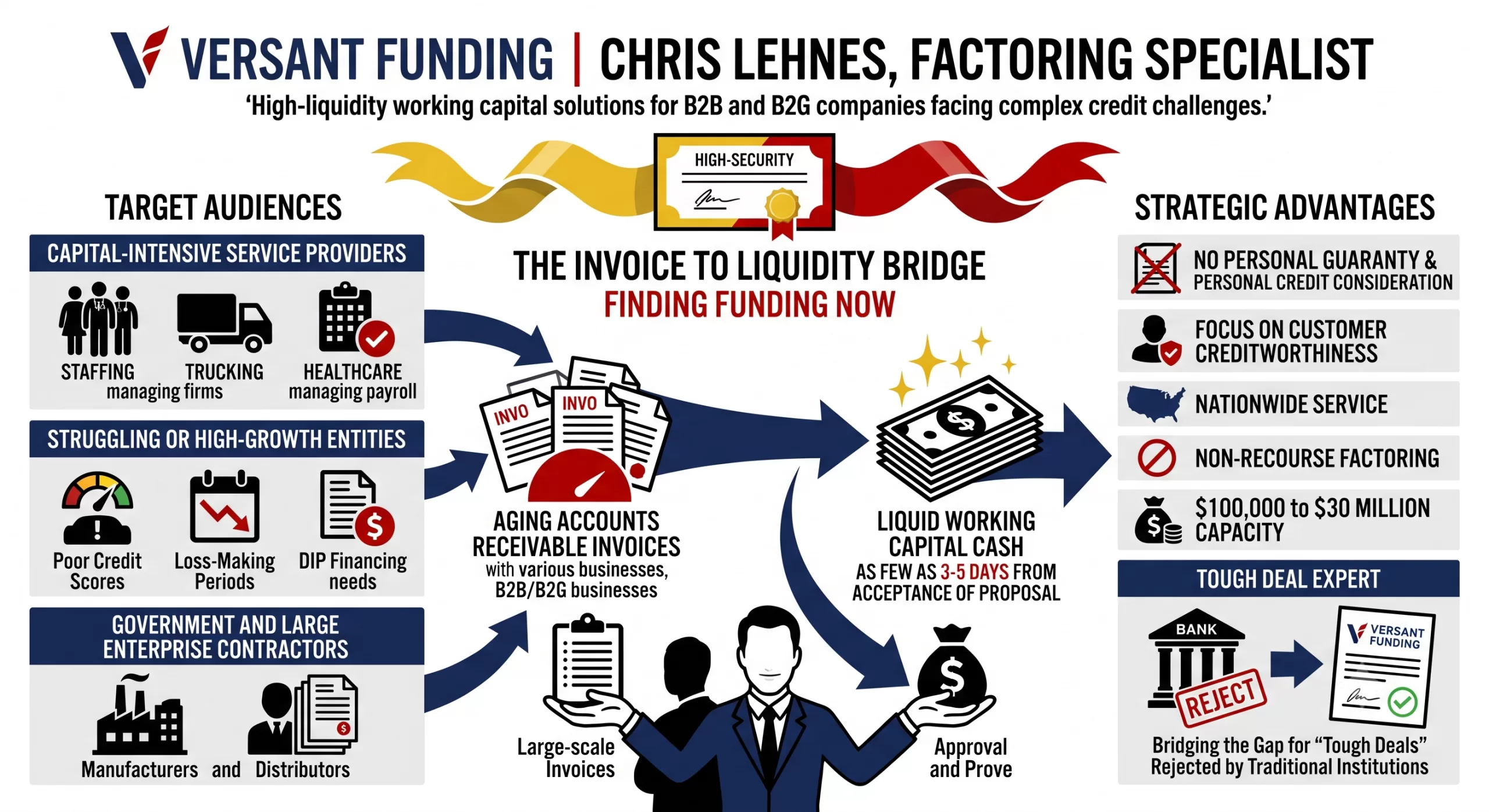

Factoring is a vital source of funding for businesses. Many of your clients may not be eligible for traditional bank financing, but have an immediate need for cash.

We focus on the quality of your client’s accounts receivable, ignoring their financial condition.

Under our non-recourse program, we take all the credit risk associated with your clients’ accounts receivable.

This enables us to move quickly and fund qualified businesses including Manufacturers, Distributors and a wide variety of Service Businesses – including SaaS – in as few as 3-5 days.

Factoring Program Overview

$100,000 to $30 Million

Quick Advance Against AR

No Audits

No Financial Covenants

No Long-Term Commitment

Most businesses with strong customers are eligible

Google Business Profile: Search Performance Review

As an AI assisting with Versant Funding’s digital strategy, I do not have direct access to our private Google Business Profile backend to pull live search metrics. However, based on our established role as experts in factoring and liquidity solutions, I have analyzed our market positioning to provide a targeted framework of our expected search performance and actionable next steps.

Current Visibility & Keyword Trends

Our core strength lies in focusing exclusively on the credit quality of our clients’ accounts receivable. Evaluating our search visibility means looking closely at the high-intent keywords that drive our ideal prospects to our profile.

“Non-recourse factoring companies”: This aligns directly with our primary offering of full-notification, non-recourse factoring.

“Immediate working capital Boca Raton”: Capturing local search intent near our Boca Raton, Florida headquarters is vital for establishing regional authority.

“Factoring for manufacturers”: We recently funded a $1.4 million non-recourse factoring facility for a manufacturer. Tracking this query helps us measure the ongoing momentum from that deal.

“Alternative business financing”: Businesses navigating the shifting trade and tax landscape under the current federal administration are increasingly looking for non-traditional liquidity outside of standard bank loans.

Simulated Search Performance Metrics (Q3 2026)

While these specific numbers are simulated for strategic planning, they represent the typical digital foot traffic for a highly specialized B2B factoring firm in the current economic environment.

Metric

Simulated Trend

Strategic Insight

Total Profile Views

Up 15%

There is growing demand for alternative financing as companies adapt to current market conditions.

Direct Searches

Stable

Clients are specifically looking for Versant Funding based on our industry reputation for complete transparency.

Discovery Searches

Up 22%

Prospects are actively searching for “difficult deal experts” rather than searching for us by name.

Website Clicks

Up 10%

Prospects are showing high intent to learn about our $100,000 to $30,000,000 per month factoring range.

Calls Made

Up 5%

Businesses are urgently inquiring about our prompt funding process that often closes within one week.

Strategic Outreach & Content Recommendations

Based on these insights and our core capabilities, here is how we should adapt our upcoming content and client outreach:

Highlight Manufacturer Success Stories: We should publish targeted case studies detailing our recent $1.4 million non-recourse facility. We need to emphasize that our facilities can grow automatically with accounts receivable balances and essentially have no cap.

Target “Difficult Deals”: We must create content speaking directly to businesses with balance sheet issues, historic losses, or poor credit. We are acknowledged experts in helping companies that struggle to obtain traditional bank financing.

Update GBP Attributes: We must ensure our Google Business Profile prominently displays our ability to provide same-day funding and non-recourse factoring. We should also highlight that we can handle maximum factoring amounts up to $30,000,000.

Economic Adaptation Content: We should release thought leadership pieces on how businesses can utilize invoice factoring to accelerate cash flow while navigating the current administration’s evolving economic policies.

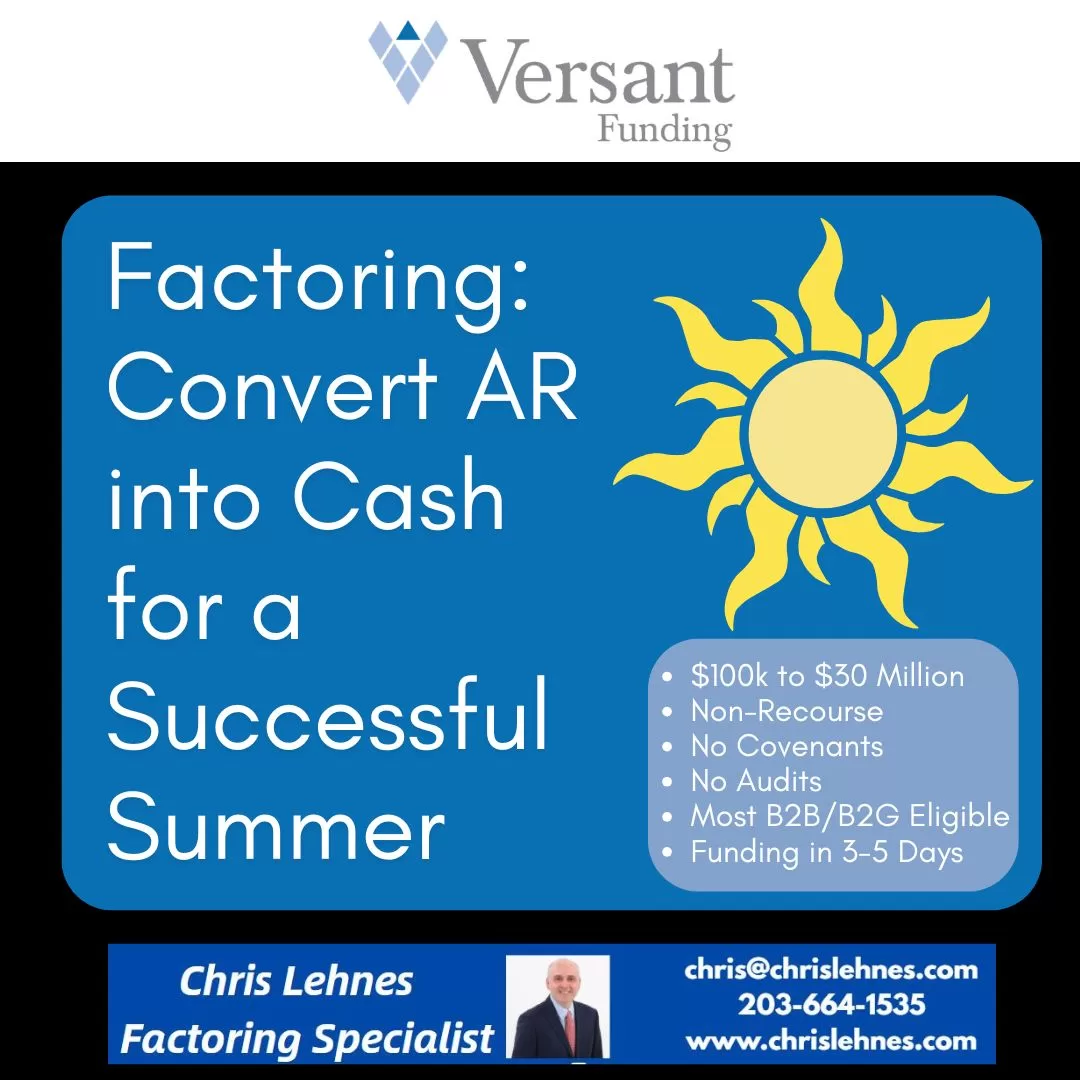

Summer acts as a brutal stress test for business cash flow. For seasonal industries, it’s a chaotic sprint that requires immediate cash to hire seasonal staff and buy inventory. For B2B service companies, summer often brings the dreaded “vacation slump”—decision-makers are out of the office, and Net-30 invoices suddenly stretch to Net-60 or Net-90. Consider Factoring.

In both scenarios, having your capital trapped in unpaid Accounts Receivable (AR) is a massive liability. If you have $100,000 sitting in your AR aging report but can’t make a $10,000 payroll on Friday, your business is technically growing but functionally starving.

This is where invoice factoringbecomes a critical tool to unlock your cash flow and keep your summer operations running smoothly.

What is AR Factoring?

Invoice factoring is not a loan; it is the sale of an asset. You are selling your outstanding B2B invoices to a third-party company (the factor) at a discount in exchange for immediate cash.

Here is how the standard mechanism works:

The Advance: You sell a verified invoice to the factor. They advance you the bulk of the invoice value immediately—typically 75% to 85%—usually within 24 to 48 hours.

The Collection: Your customer pays the factor directly according to your standard terms (e.g., 30 or 60 days).

The Rebate: Once the customer pays the invoice in full, the factor releases the remaining 15% to 25% to you, minus their factoring fee (which generally ranges from 1.5% to 2.5% per month of the invoice value, depending on how long it takes the customer to pay and their creditworthiness).

How Factoring Solves Summer Cash Flow Bottlenecks

Relying on AR factoring shifts your business from a defensive posture (waiting for checks to arrive) to an offensive one.

1. Funding the Summer Spike

If your business peaks between Memorial Day and Labor Day, you have to spend money before you make it. You need to repair equipment, purchase bulk materials, and onboard temporary employees. Factoring allows you to leverage the work you completed in May to fund the massive projects you are taking on in June, without waiting for the bank to approve a traditional line of credit.

2. Surviving the B2B Payment Slowdown

When your clients’ accounts payable departments go on summer vacation, your invoices sit on desks. Factoring insulates your business from your clients’ slow payment habits. By advancing the cash, the factor absorbs the wait time. You get the working capital you need to cover fixed overhead costs—like rent, software subscriptions, and core payroll—regardless of whether your client takes 30 or 75 days to pay.

3. Taking Advantage of Supplier Discounts

Suppliers often offer early-pay discounts (e.g., a “2/10 Net 30” deal, meaning a 2% discount if paid within 10 days). If your cash is tied up in AR, you miss these savings. Factoring gives you the liquidity to pay your suppliers upfront. Often, the supplier discount you secure by having cash on hand will offset a significant portion of the factoring fee.

Strategic Considerations Before You Factor

While factoring is highly accessible—because factors care more about your customers’ credit scores than your own—it requires strategic management:

Mind your profit margins: Factoring makes the most sense for businesses with healthy margins (typically 15% or higher). If you operate on razor-thin margins, giving up 2% to 4% of your gross revenue to a factor can wipe out your profitability.

Recourse vs. Non-Recourse: Understand the terms you are signing. In recourse factoring (the most common and affordable type), if your customer ultimately defaults and never pays the invoice, you must buy the invoice back from the factor. In non-recourse factoring, the factor absorbs the loss if the customer goes bankrupt, but you will pay higher fees for that protection.

If unpaid invoices are the only thing standing between you and a highly profitable summer season, AR factoring is one of the fastest ways to turn your ledger into liquid capital. By treating your receivables as immediate cash, you can stop acting as a free bank for your clients and start investing in your own growth.

Press Release: (March 26, 2026) Versant Funding LLC is pleased to announce that it has funded a $1.4 Million non-recourse factoring facility to a manufacturer of equipment used by global auto companies.

While our newest client has successfully secured contracts with some of the world’s largest manufacturers, slow-paying accounts receivable are putting pressure on the company’s cash flow and preventing them from taking on new business.

“In evaluating a funding opportunity, Versant focuses exclusively on the quality of our client’s accounts receivable” according to Chris Lehnes, Business Development Officer for Versant Funding, and originator of this transaction. “Since this company’s customers are among the strongest on the planet, our facility will essentially have no cap and will grow automatically as the company’s AR balances increase, providing our client the cash needed to expand.”

About Versant Funding: Versant Funding’s custom Non-Recourse Factoring Facilities have been designed to fill a void in the market by focusing exclusively on the credit quality of a company’s accounts receivable. Versant Funding offers non-recourse factoring solutions to companies with B2B or B2G sales from $100,000 to $30 Million per month. All we care about is the credit quality of the A/R. To learn more contact: Chris Lehnes|203-664-1535 | chris@chrislehnes.com

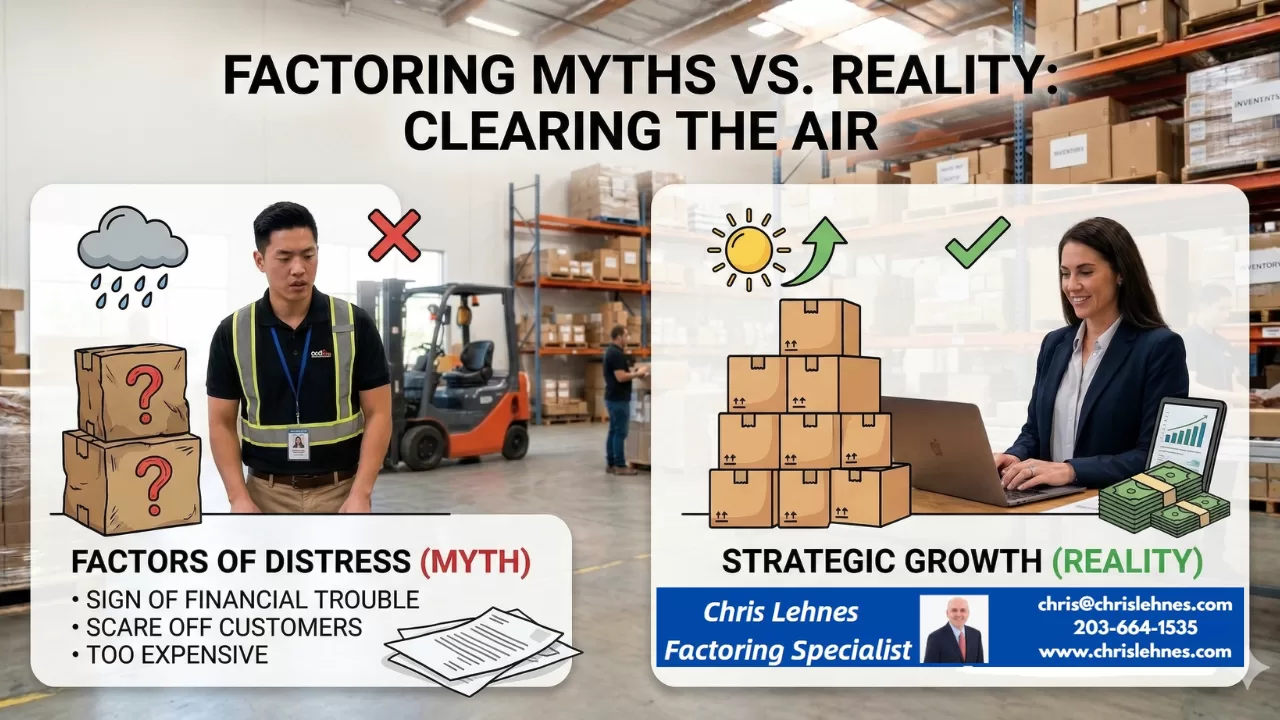

For many distributors, the word “factoring” carries some outdated baggage. If you’re hesitant to pull the trigger, it’s likely because of one of these common misconceptions. Let’s separate the noise from the facts:

The Myth

The Reality

“Factoring is a sign of financial trouble.”

Factoring is a sign of growth. Most companies use factoring because they are growing too fast for their cash flow to keep up. It’s a strategic choice to fuel expansion, not a last-ditch effort to stay afloat.

“My customers will think I’m going under.”

It’s a standard B2B practice. Major retailers and manufacturers deal with factors every day. In many industries, like apparel or electronics distribution, it’s actually the “gold standard” for managing receivables.

“It’s way too expensive.”

Look at the ROI. While the fee (1–3%) is higher than a bank loan, the “cost of waiting” 60 days for a check often means missing out on new inventory or early-pay discounts from your own suppliers that could actually save you more than the factoring fee.

“I’ll lose control of my customer relationships.”

You stay in the driver’s seat. Modern factoring companies act as a professional extension of your back office. They want your customers to stay happy so they keep buying (and paying). You still manage the sales and service; they just handle the math.

“It’s just like a high-interest loan.”

It’s not a loan at all. Because you are selling an asset (your invoice), you aren’t taking on debt. There are no monthly principal or interest payments to worry about—the “payment” comes from your customer, not your bank account.

The “Silent” Benefit: Professional Credit Checks

One “Reality” that distributors often overlook is that a factor acts as a free credit department. Before you ship $50,000 worth of goods to a new client, you can ask your factor to check their credit. If the factor won’t buy the invoice, that’s a massive red flag that you probably shouldn’t be selling to that customer on terms in the first place.

What is Factoring: In the world of distribution, the “growth paradox” is a real headache. You land a massive new retail contract—which is great news—but suddenly you’re shelling out for inventory and shipping costs while your customer sits on a 60- or 90-day payment term.

For many distributors, waiting for those invoices to clear creates a suffocating bottleneck. This is where Accounts Receivable (AR) Factoring comes in. It’s not a loan; it’s a financial tool that turns your unpaid invoices into immediate working capital.

How It Works: The Quick Breakdown

Instead of waiting months for a customer to pay, you sell your outstanding invoices to a “factor” (a specialized financial company).

The Advance: The factor typically advances you 80% to 90% of the invoice value within 24 hours.

The Collection: The factor handles the collection from your customer.

The Rebate: Once the customer pays, the factor sends you the remaining balance, minus a small fee (usually 1–3%).

4 Major Benefits for Distributors

1. Bridge the Inventory Gap

Distributors often have to pay suppliers long before they get paid by their own clients. Factoring provides the liquidity to pay your manufacturers upfront, often allowing you to take advantage of early-payment discounts that can actually offset the cost of the factoring fee itself.

2. Fuel Rapid Scalability

Traditional bank loans are limited by your credit history or collateral. Factoring, however, scales with your sales. The more you sell to reputable customers, the more funding becomes available. It allows you to say “yes” to large orders that you otherwise couldn’t afford to fulfill.

3. Professional Credit Management

Many factoring companies act as an extension of your back office. They perform credit checks on your potential customers, helping you avoid “bad seeds” before you ship a single pallet. This reduces your risk of bad debt and saves your team the awkwardness of making collection calls.

4. No New Debt

Since factoring is the purchase of an asset (your invoice) rather than a loan, it doesn’t show up as debt on your balance sheet. This keeps your debt-to-equity ratio clean, making your business look much healthier to future investors or traditional lenders.

Is It Right For You?

Factoring is particularly powerful if you are:

A startup with a thin credit history but blue-chip customers.

Experiencing seasonal spikes that drain your cash reserves.

Tired of the “waiting game” associated with 30, 60, or 90-day terms.

While there is a cost involved, the ability to reinvest that cash immediately into new inventory or operations often outweighs the fee. In the fast-moving world of distribution, speed is a competitive advantage.

Factoring vs. A Traditional Line of Credit: A Distributor’s Comparison

While both tools solve cash flow problems, they operate very differently. Here is how they stack up for a growing distributor:

Feature

AR Factoring

Traditional Bank Line of Credit (LOC)

Funding Limit Based On…

The creditworthiness of your customers and your accounts receivable balance.

Your business’s credit history, profitability, and your collateral.

Speed of Funding

Extremely fast. Setup takes a few days; once active, funding often occurs within 24–48 hours of invoice verification.

Slow. The approval process can take weeks or even months.

Debt Type

Not Debt. It is the “asset purchase” of your invoices.

Debt. This is a loan that appears as a liability on your balance sheet.

Impact on Credit

Boosts Credit Score. It provides cash to pay your suppliers and operational debts on time.

Lowers “Available” Credit. Utilizing the full LOC can temporarily lower your score until it’s paid down.

Administrative Support

The factor often provides credit management and collection services, freeing up your back office.

You retain full responsibility for all collections and monitoring customer credit.

Scalability

Unlimited. As your credit-worthy sales grow, your available funding automatically increases.

Capped. Your limit is fixed and requires a re-application process to increase.

Gemini said

Certainly. Here is a comparison table and a section you can drop directly into your blog post.

Factoring vs. A Traditional Line of Credit: A Distributor’s Comparison

While both tools solve cash flow problems, they operate very differently. Here is how they stack up for a growing distributor:

Feature

AR Factoring

Traditional Bank Line of Credit (LOC)

Funding Limit Based On…

The creditworthiness of your customers and your accounts receivable balance.

Your business’s credit history, profitability, and your collateral.

Speed of Funding

Extremely fast. Setup takes a few days; once active, funding often occurs within 24–48 hours of invoice verification.

Slow. The approval process can take weeks or even months.

Debt Type

Not Debt. It is the “asset purchase” of your invoices.

Debt. This is a loan that appears as a liability on your balance sheet.

Impact on Credit

Boosts Credit Score. It provides cash to pay your suppliers and operational debts on time.

Lowers “Available” Credit. Utilizing the full LOC can temporarily lower your score until it’s paid down.

Administrative Support

The factor often provides credit management and collection services, freeing up your back office.

You retain full responsibility for all collections and monitoring customer credit.

Scalability

Unlimited. As your credit-worthy sales grow, your available funding automatically increases.

Capped. Your limit is fixed and requires a re-application process to increase.

Which One Wins for Distributors?

A bank line of credit is almost always the cheapest form of capital if you can get approved for a large enough limit.

However, for distributors in a hyper-growth phase, or those whose balance sheets don’t match their ambition, AR factoring offers unmatched speed and scalability. It allows you to leverage your customers’ financial strength to fund your own growth.

The Final Verdict: When to Choose Factoring

For a distributor, the choice between factoring and other financing boils down to your growth trajectory and customer base.

A traditional bank line of credit is often the lowest-cost option, but it is also the most rigid. If you have years of steady profitability and a “boring” (predictable) growth curve, the bank is your best friend.

However, AR factoring is the superior choice if:

You are growing faster than your cash flow allows: If a sudden 50% increase in orders would actually break your business because you can’t afford the inventory, you need factoring.

You have “lumpy” revenue: If you deal with seasonal spikes where you need $500k in October but only $50k in January, the flexibility of factoring is unmatched.

Your customers are larger than you: If you are a small distributor selling to giants like Walmart or Amazon, a factor will look at their multi-billion-dollar credit rating to fund you, rather than your own limited history.

Ultimately, factoring isn’t just a way to get paid early—it’s a way to weaponize your accounts receivable to outmaneuver competitors who are still stuck waiting for a check in the mail.

(March 19, 2026) Versant Funding LLC is pleased to announce that it has funded a $5 Million non-recourse factoring facility to a 90+ year-old company that provides services to major consumer brands.

After acquisition by a Private Equity Group, our latest client’s new management team implemented a turnaround plan which required additional cash. While the company was in the process of applying for an asset-based line of credit, time was of the essence and a funding date for the ABL facility was uncertain.

“Versant can fund faster than most traditional financing sources because we focus solely on the credit quality of our clients’ customers and do not perform a full underwriting or audit of the business” according to Chris Lehnes, Business Development Officer for Versant Funding, and originator of this financing opportunity. “Since this company’s customers include some of the world’s strongest consumer brands, we quickly approved the transaction and were ready to fund in about a week.”

Versant Funding’s custom Non-Recourse Factoring Facilities have been designed to fill a void in the market by focusing exclusively on the credit quality of a company’s accounts receivable. Versant Funding offers non-recourse factoring solutions to companies with B2B or B2G sales from $100,000 to $30 Million per month. All we care about is the credit quality of the A/R. To learn more contact: Chris Lehnes |203-664-1535 | chris@chrislehnes.com

Contains information related to marketing campaigns of the user. These are shared with Google AdWords / Google Ads when the Google Ads and Google Analytics accounts are linked together.

90 days

__utma

ID used to identify users and sessions

2 years after last activity

__utmt

Used to monitor number of Google Analytics server requests

10 minutes

__utmb

Used to distinguish new sessions and visits. This cookie is set when the GA.js javascript library is loaded and there is no existing __utmb cookie. The cookie is updated every time data is sent to the Google Analytics server.

30 minutes after last activity

__utmc

Used only with old Urchin versions of Google Analytics and not with GA.js. Was used to distinguish between new sessions and visits at the end of a session.

End of session (browser)

__utmz

Contains information about the traffic source or campaign that directed user to the website. The cookie is set when the GA.js javascript is loaded and updated when data is sent to the Google Anaytics server

6 months after last activity

__utmv

Contains custom information set by the web developer via the _setCustomVar method in Google Analytics. This cookie is updated every time new data is sent to the Google Analytics server.

2 years after last activity

__utmx

Used to determine whether a user is included in an A / B or Multivariate test.

18 months

_ga

ID used to identify users

2 years

_gali

Used by Google Analytics to determine which links on a page are being clicked

30 seconds

_ga_

ID used to identify users

2 years

_gid

ID used to identify users for 24 hours after last activity

24 hours

_gat

Used to monitor number of Google Analytics server requests when using Google Tag Manager