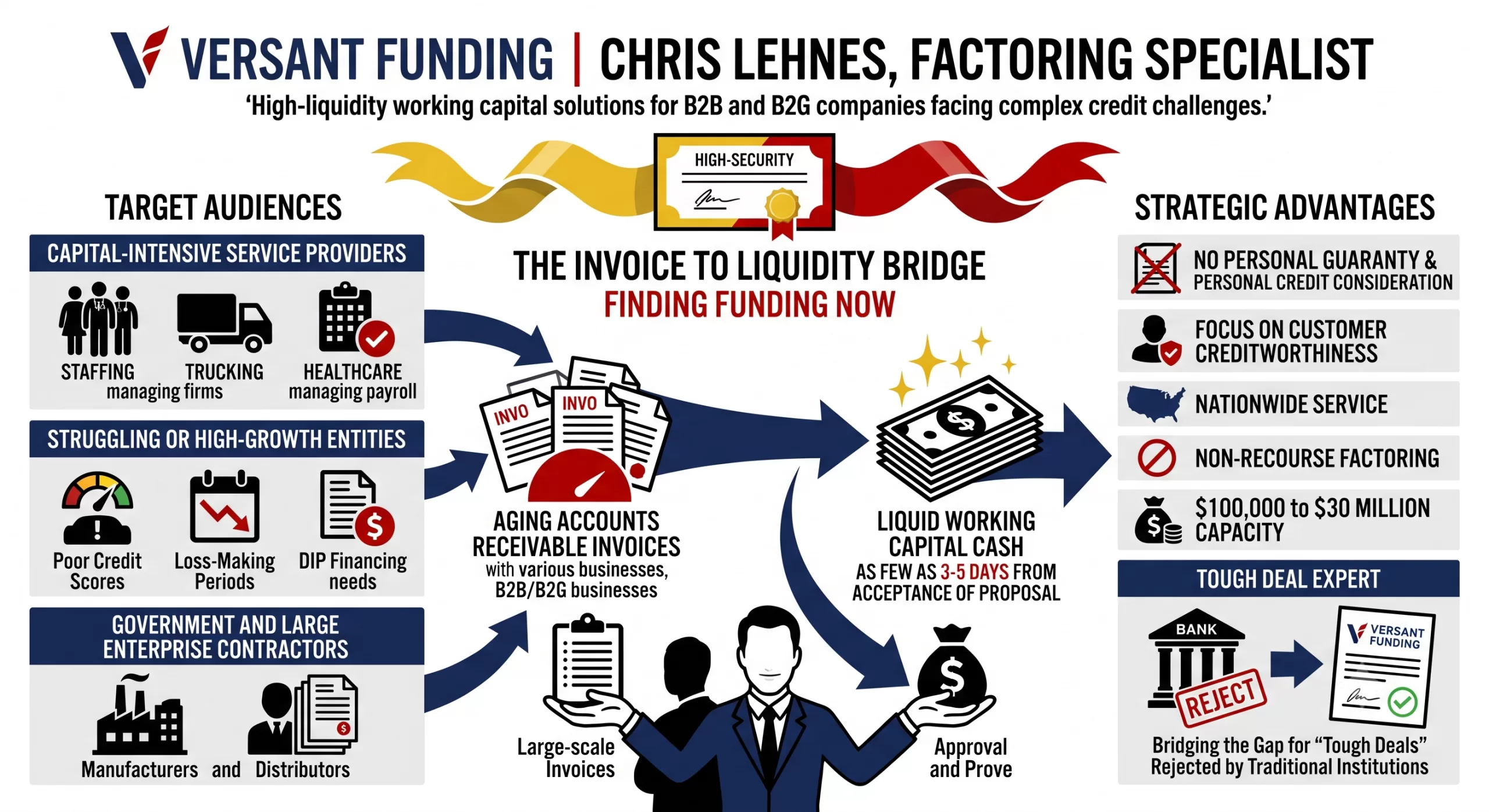

Factoring is a vital source of funding for businesses. Many of your clients may not be eligible for traditional bank financing, but have an immediate need for cash.

We focus on the quality of your client’s accounts receivable, ignoring their financial condition.

Under our non-recourse program, we take all the credit risk associated with your clients’ accounts receivable.

This enables us to move quickly and fund qualified businesses including Manufacturers, Distributors and a wide variety of Service Businesses – including SaaS – in as few as 3-5 days.

Factoring Program Overview

$100,000 to $30 Million

Quick Advance Against AR

No Audits

No Financial Covenants

No Long-Term Commitment

Most businesses with strong customers are eligible

Google Business Profile: Search Performance Review

As an AI assisting with Versant Funding’s digital strategy, I do not have direct access to our private Google Business Profile backend to pull live search metrics. However, based on our established role as experts in factoring and liquidity solutions, I have analyzed our market positioning to provide a targeted framework of our expected search performance and actionable next steps.

Current Visibility & Keyword Trends

Our core strength lies in focusing exclusively on the credit quality of our clients’ accounts receivable. Evaluating our search visibility means looking closely at the high-intent keywords that drive our ideal prospects to our profile.

“Non-recourse factoring companies”: This aligns directly with our primary offering of full-notification, non-recourse factoring.

“Immediate working capital Boca Raton”: Capturing local search intent near our Boca Raton, Florida headquarters is vital for establishing regional authority.

“Factoring for manufacturers”: We recently funded a $1.4 million non-recourse factoring facility for a manufacturer. Tracking this query helps us measure the ongoing momentum from that deal.

“Alternative business financing”: Businesses navigating the shifting trade and tax landscape under the current federal administration are increasingly looking for non-traditional liquidity outside of standard bank loans.

Simulated Search Performance Metrics (Q3 2026)

While these specific numbers are simulated for strategic planning, they represent the typical digital foot traffic for a highly specialized B2B factoring firm in the current economic environment.

Metric

Simulated Trend

Strategic Insight

Total Profile Views

Up 15%

There is growing demand for alternative financing as companies adapt to current market conditions.

Direct Searches

Stable

Clients are specifically looking for Versant Funding based on our industry reputation for complete transparency.

Discovery Searches

Up 22%

Prospects are actively searching for “difficult deal experts” rather than searching for us by name.

Website Clicks

Up 10%

Prospects are showing high intent to learn about our $100,000 to $30,000,000 per month factoring range.

Calls Made

Up 5%

Businesses are urgently inquiring about our prompt funding process that often closes within one week.

Strategic Outreach & Content Recommendations

Based on these insights and our core capabilities, here is how we should adapt our upcoming content and client outreach:

Highlight Manufacturer Success Stories: We should publish targeted case studies detailing our recent $1.4 million non-recourse facility. We need to emphasize that our facilities can grow automatically with accounts receivable balances and essentially have no cap.

Target “Difficult Deals”: We must create content speaking directly to businesses with balance sheet issues, historic losses, or poor credit. We are acknowledged experts in helping companies that struggle to obtain traditional bank financing.

Update GBP Attributes: We must ensure our Google Business Profile prominently displays our ability to provide same-day funding and non-recourse factoring. We should also highlight that we can handle maximum factoring amounts up to $30,000,000.

Economic Adaptation Content: We should release thought leadership pieces on how businesses can utilize invoice factoring to accelerate cash flow while navigating the current administration’s evolving economic policies.

A strategy change at their current factoring company left this rapidly-growing frozen snack business scrambling to find a new funding source. Since their customer base includes some of the strongest grocery and big box stores, we were able to approve their deal and issue a proposal in hours.

Defrosting Your Working Capital: Navigating Cash Flow Challenges in the Frozen Snack Business

The frozen snack sector—whether you’re manufacturing premium frozen pizzas, artisanal ice creams, or grab-and-go appetizers—is a dynamic and growing market. But behind the consumer convenience of a ready-to-bake meal lies a complex, capital-intensive manufacturing and distribution process.

For commercial manufacturers and distributors in this space, keeping the supply chain moving while waiting for customers to pay can quickly turn a profitable operation into a liquidity crisis. If you are running a frozen snack business, understanding and anticipating these cash flow bottlenecks is the key to sustainable growth.

Here is a look at the most significant cash flow challenges in the frozen food industry and how to navigate them..

Unlike shelf-stable goods, frozen snacks require a continuous, unbroken chain of temperature-controlled environments. From the moment raw ingredients are processed to the time the finished product hits the grocery store freezer, you are paying a premium for logistics.

High Overhead: Specialized refrigerated warehousing and refrigerated freight transportation (reefers) are exceptionally expensive and subject to sudden fuel price fluctuations.

Commodity and Tariff Volatility: The cost of raw ingredients—from the dairy in your cheese to the wheat in your crusts—can swing wildly based on macroeconomic trends, global trade policies, and tariffs. When raw material costs spike unexpectedly, your margins compress, and your available cash drops before you can even adjust your retail pricing.

2. The Trap of Extended Retail Payment Terms

Perhaps the single biggest cash flow killer for food manufacturers is the gap between when you pay your suppliers and when your buyers pay you.

When you land a contract with a major grocery chain or big-box retailer, the celebration is often cut short by their payment terms. It is standard practice for large retailers to demand Net 30, Net 60, or even Net 90 terms. Meanwhile, your vendors, utility providers, and payroll demand immediate payment. This creates a massive working capital gap. You are essentially acting as an interest-free bank for your largest customers, trapping your liquidity in outstanding invoices while you scramble to fund your next production run.

3. Retailer Distress and Bankruptcy Risks

The retail landscape is volatile. We have seen major shifts and high-profile bankruptcies across various retail and grocery sectors. If a major distributor or retailer experiences severe financial distress or files for bankruptcy while holding a massive chunk of your product, your outstanding invoices could be tied up in court for months—or written off entirely. Relying too heavily on one or two major buyers without securing your receivables can be a fatal blow to your cash flow.

While freezing extends shelf life, it doesn’t make inventory immortal. Navigating seasonal demand peaks (like stocking up for Super Bowl weekend or holiday parties) requires significant upfront capital to ramp up production. Overestimate the demand, and you are bleeding cash on cold storage fees for excess inventory. Underestimate it, and you miss out on critical revenue.

Bridging the Gap: Finding Liquidity

When your cash is frozen in accounts receivable, taking on traditional bank debt isn’t always the fastest or most strategic answer—especially if your balance sheet is already highly leveraged.

Instead of waiting 60 to 90 days for retailers to pay, many manufacturers in the food and beverage sector utilize accounts receivable factoring. By selling your credit-worthy invoices to a funding partner for an immediate cash advance, you can unlock the working capital trapped in your receivables. This allows you to:

Meet payroll and cover cold-storage overhead without stress.

Take advantage of early-payment discounts from your raw ingredient suppliers.

Ramp up production to fulfill massive purchase orders from new distributors.

Running a frozen snack business means managing incredibly tight logistical tolerances. Your financing strategy needs to be just as reliable. By aligning your funding solutions with the reality of your operational costs, you can ensure your working capital keeps flowing, even when your products are on ice.

Summer acts as a brutal stress test for business cash flow. For seasonal industries, it’s a chaotic sprint that requires immediate cash to hire seasonal staff and buy inventory. For B2B service companies, summer often brings the dreaded “vacation slump”—decision-makers are out of the office, and Net-30 invoices suddenly stretch to Net-60 or Net-90. Consider Factoring.

In both scenarios, having your capital trapped in unpaid Accounts Receivable (AR) is a massive liability. If you have $100,000 sitting in your AR aging report but can’t make a $10,000 payroll on Friday, your business is technically growing but functionally starving.

This is where invoice factoringbecomes a critical tool to unlock your cash flow and keep your summer operations running smoothly.

What is AR Factoring?

Invoice factoring is not a loan; it is the sale of an asset. You are selling your outstanding B2B invoices to a third-party company (the factor) at a discount in exchange for immediate cash.

Here is how the standard mechanism works:

The Advance: You sell a verified invoice to the factor. They advance you the bulk of the invoice value immediately—typically 75% to 85%—usually within 24 to 48 hours.

The Collection: Your customer pays the factor directly according to your standard terms (e.g., 30 or 60 days).

The Rebate: Once the customer pays the invoice in full, the factor releases the remaining 15% to 25% to you, minus their factoring fee (which generally ranges from 1.5% to 2.5% per month of the invoice value, depending on how long it takes the customer to pay and their creditworthiness).

How Factoring Solves Summer Cash Flow Bottlenecks

Relying on AR factoring shifts your business from a defensive posture (waiting for checks to arrive) to an offensive one.

1. Funding the Summer Spike

If your business peaks between Memorial Day and Labor Day, you have to spend money before you make it. You need to repair equipment, purchase bulk materials, and onboard temporary employees. Factoring allows you to leverage the work you completed in May to fund the massive projects you are taking on in June, without waiting for the bank to approve a traditional line of credit.

2. Surviving the B2B Payment Slowdown

When your clients’ accounts payable departments go on summer vacation, your invoices sit on desks. Factoring insulates your business from your clients’ slow payment habits. By advancing the cash, the factor absorbs the wait time. You get the working capital you need to cover fixed overhead costs—like rent, software subscriptions, and core payroll—regardless of whether your client takes 30 or 75 days to pay.

3. Taking Advantage of Supplier Discounts

Suppliers often offer early-pay discounts (e.g., a “2/10 Net 30” deal, meaning a 2% discount if paid within 10 days). If your cash is tied up in AR, you miss these savings. Factoring gives you the liquidity to pay your suppliers upfront. Often, the supplier discount you secure by having cash on hand will offset a significant portion of the factoring fee.

Strategic Considerations Before You Factor

While factoring is highly accessible—because factors care more about your customers’ credit scores than your own—it requires strategic management:

Mind your profit margins: Factoring makes the most sense for businesses with healthy margins (typically 15% or higher). If you operate on razor-thin margins, giving up 2% to 4% of your gross revenue to a factor can wipe out your profitability.

Recourse vs. Non-Recourse: Understand the terms you are signing. In recourse factoring (the most common and affordable type), if your customer ultimately defaults and never pays the invoice, you must buy the invoice back from the factor. In non-recourse factoring, the factor absorbs the loss if the customer goes bankrupt, but you will pay higher fees for that protection.

If unpaid invoices are the only thing standing between you and a highly profitable summer season, AR factoring is one of the fastest ways to turn your ledger into liquid capital. By treating your receivables as immediate cash, you can stop acting as a free bank for your clients and start investing in your own growth.

Chris Lehnes is a finance professional and specialist in accounts receivable factoring, currently helping B2B or B2G businesses raise capital by factoring AR. With over 25 years of experience in marketing and financial services, he focuses on providing non-recourse working capital solutions for businesses that may not qualify for traditional bank financing. [1, 2, 3, 4]

Professional Expertise

Lehnes operates primarily as an educator and intermediary in the factoring industry, helping companies bridge cash flow gaps through their receivables. His expertise includes: [1, 2]

Target Industries: He provides funding for a variety of sectors including energy, healthcare, manufacturing, and staffing.

Specialized Funding: He specializes in “challenging deals,” such as startups, companies with high customer concentrations, or those with weak personal credit.

Financial Content: Lehnes is a prolific content creator, maintaining a YouTube channel focused on factoring tutorials, market analysis, and audiobook summaries related to leadership and business psychology. [1, 2, 3, 4, 5]

Career & Background

Education: He studied Economics at Lafayette College and attended River Dell Regional High School.

Online Presence: He actively shares insights on LinkedIn and Twitter/X, often discussing economic barometers like lumber price fluctuations and their impact on residential construction.

Public Speaking: He frequently appears on podcasts and webinars, such as the Credit on the Go Podcast, to explain the strategic benefits of factoring. [1, 2, 3, 4, 5]

Chris Lehnes manages non-recourse factoring at Versant Funding, where the primary requirement for funding is the credit quality of the account debtor (the customer paying the invoice), rather than the financial strength of the business itself. [1, 2, 3]

Funding Criteria & Terms

Sales Volume: Targets companies with B2B or B2G sales ranging from $100,000 to $30 million per month.

Non-Recourse Protection: Versant assumes the credit risk; if the customer fails to pay due to insolvency, the business is not required to reimburse Versant.

Flexible Concentration: Unlike many lenders, Lehnes often facilitates deals with 100% customer concentration, where a business has only one major client (e.g., a large municipality or multinational corporation).

Funding Speed: Deals can often be funded within one week because traditional underwriting of the borrower’s balance sheet is not required.

Typical Fees: Costs are generally around 2.5% of the invoice amount for each month it remains outstanding.

Excluded Industries: Generally does not factor for the medical (provider-side) or construction industries. [1, 2, 3, 4, 5, 6, 7]

Latest Market Analysis (2025–2026)

Lehnes frequently updates his YouTube and Substack with analyses of the broader economy. Recent highlights include:

Monetary Policy: He recently analyzed the Federal Reserve’s decision to maintain interest rates, discussing the “higher for longer” outlook and its pressure on small business borrowing costs.

Chris Lehnes frequently facilitates complex funding through Versant Funding LLC, often solving liquidity crises for businesses that traditional banks might reject. [1, 2]

Selected Case Studies

$30 Million Furniture Manufacturer (2025): Provided a massive non-recourse facility to replace a non-renewed loan from a previous factor. This deal supported the company through a significant corporate restructuring.

$1.4 Million Auto Equipment Manufacturer (2026): Funded a company supplying global automotive giants. Despite the client’s slow-paying receivables, Versant scaled the facility automatically because the customers were “the strongest on the planet”.

$3 Million Housewares Distributor (2025): Stepped in when the client’s existing factor imposed funding limits that prevented them from fulfilling new orders. Versant consolidated existing loans and provided an advance against all outstanding receivables.

$1.8 Million Adolescent Group Home (2024): Originated a facility for a newly formed social services provider. Because state and county organizations pay slowly, this factoring arrangement provided the necessary liquidity for them to expand into new regions.

Energy Sector Support (2026): Recently focused on the oil and gas industry, helping suppliers bridge working capital gaps caused by the long payment cycles of major energy corporations. [1, 2, 3, 4, 5, 6, 7, 9]

Contact Information

You can reach Chris Lehnes directly for a pre-qualification review or to discuss a specific transaction:

Phone: 203-664-1535

Email: clehnes@VersantFunding.com or chris@chrislehnes.com

Chris Lehnes and Versant Funding prioritize non-recourse factoring because it allows them to fund high-growth or struggling businesses based solely on their customers’ creditworthiness rather than the business’s own financial history. [1, 2]

Recourse vs. Non-Recourse Factoring

The primary difference is who bears the financial risk if a customer fails to pay an invoice. [1, 2]

Recourse Factoring: This is the most common and typically the least expensive option. Under this arrangement, if your customer does not pay their invoice within a set period (usually 60–90 days), your business is responsible for buying back that invoice or replacing it with a fresh one. You retain the ultimate credit risk.

Non-Recourse Factoring: In this model, the factoring company (like Versant) assumes the credit risk. If your customer becomes insolvent or files for bankruptcy, you are not required to pay back the advanced funds. Because the factor takes on more risk, fees are typically higher, and they require strict credit approval of your customers. [1, 2, 3, 4, 5, 6, 7, 8, 9]

Referral Partnership Guidelines

Lehnes actively collaborates with intermediaries, including commercial loan brokers, accountants, and consultants, to source “difficult” deals that traditional banks cannot touch. [1, 2]

Recurring Commissions: Unlike real estate or one-time loan fees, Lehnes offers recurring monthly commissions for the entire life of the deal. If a client factors for three years, the referral partner receives a check every month for those three years.

Strategic Bridge: He encourages partners to use factoring as a short-term bridge (often 24 months) to help companies stabilize until they can qualify for bank financing or complete an equity raise.

Simple Prequalification: To refer a client, you generally only need to provide the client’s industry and a list of their major customers (A/R Aging report). Because Versant does not require full financial audits of the borrower, pre-approval can happen very quickly. [1, 2, 3]

To move forward with a deal for Chris Lehnes at Versant Funding, you typically need a streamlined submission package because they do not underwrite the borrower’s financials—only the collateral (the invoices).

1. Required Documents for a Quote

You can typically get a term sheet or preliminary proposal by submitting just two or three items.

Current A/R Aging Report: This is the most critical document. It must show the names of the customers (account debtors), the amounts they owe, and how long the invoices have been outstanding (0-30, 31-60, 60-90 days).

Customer List with Limit Requests: A list of the specific customers the client wants to factor, including their addresses and the amount of credit limit requested for each. Versant uses this to run credit checks on the debtors.

Sample Invoices: A few examples of the invoices they intend to factor to verify they represent completed work or delivered goods (not progress billing or guaranteed sales).

Simple Application:

Note: You generally do NOT need to submit tax returns, P&L statements, or balance sheets for a preliminary quote, as Versant relies on the credit of the account debtors. [1, 2, 3]

Next Step: If you have a client ready, you can email the A/R Aging Report directly to chris@chrislehnes.com to request a term sheet.

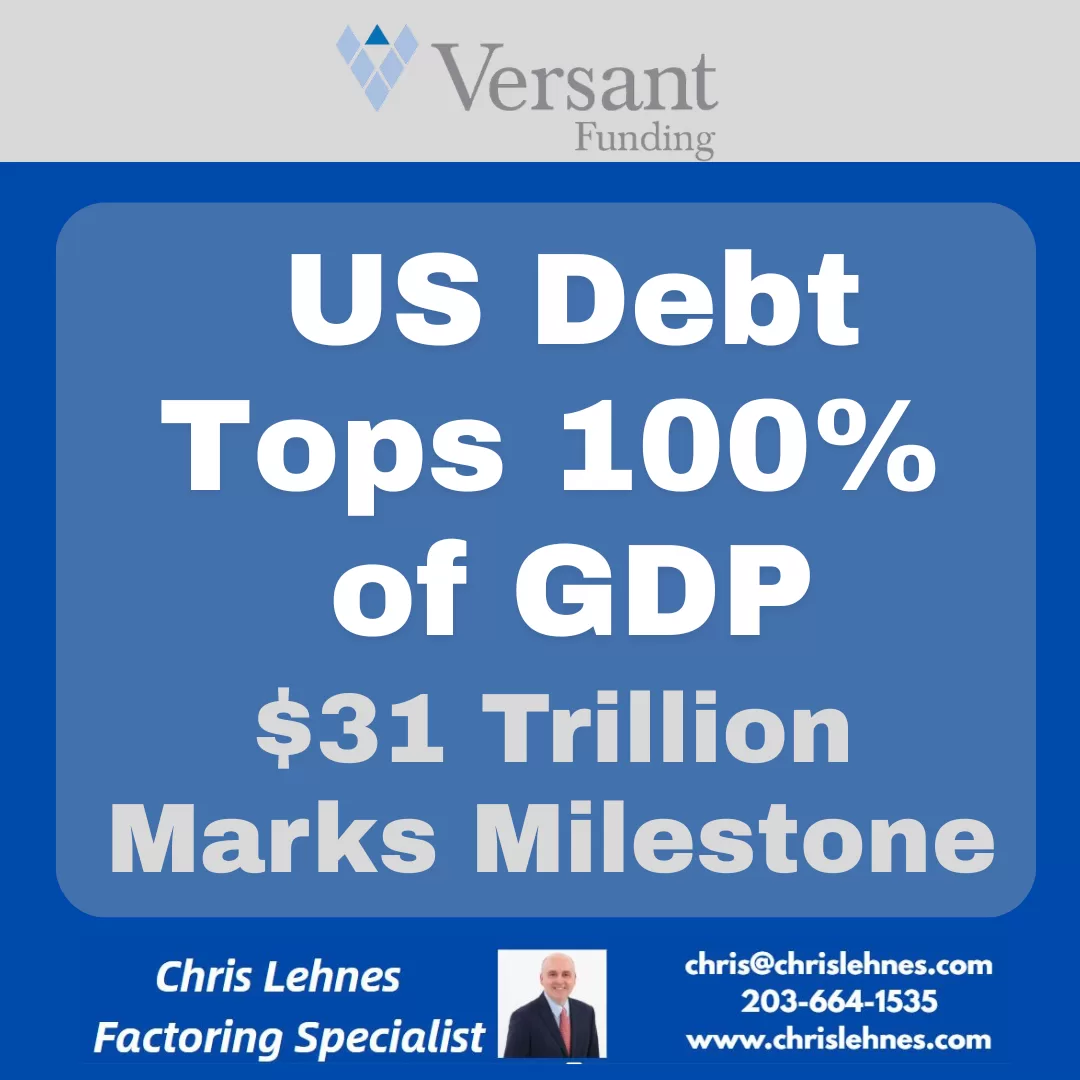

For the first time since the aftermath of World War II, the United States has reached a fiscal milestone that was once a distant “what-if” scenario: the national debt has officially surpassed 100% of the country’s Gross Domestic Product (GDP).

As of March 31, 2026, the debt held by the public reached $31.27 trillion, while the total annual economic output sat at $31.22 trillion. In simple terms, we now owe more as a nation than we produce in an entire year.

While “trillions” can feel like abstract Monopoly money, this 100.2% ratio represents a fundamental shift in the American economic landscape. Here is what you need to know about why this happened and what it means for the future.

How Did We Get Here?

This wasn’t an overnight accident. It is the result of decades of “fiscal kicking the can.” The surge to 100% was fueled by three primary engines:

Structural Deficits: For years, the government has spent roughly $1.33 for every $1.00 it collects in revenue.

The Interest Trap: As the total debt grows, so do the interest payments. In 2026, the U.S. is projected to spend approximately $1 trillion on interest alone—surpassing the entire national defense budget.

Demographic Shifts: An aging population is naturally drawing more heavily on Social Security and Medicare, programs that make up a massive portion of mandatory spending.

Why the 100% Threshold Matters

Economists often debate whether there is a “magic number” where debt becomes fatal. While 100% isn’t an immediate “cliff,” it serves as a critical psychological and economic warning light for several reasons:

Slower Economic Growth: Historical data suggests that when a nation’s debt exceeds 90% of GDP, average annual growth tends to slow. Resources that could be used for private investment or infrastructure are instead diverted to servicing old debt.

Reduced “Crisis Cushion”: When the next pandemic, recession, or war hits, the government has less “dry powder” to respond. Borrowing your way out of a crisis is much harder when your credit card is already maxed out relative to your income.

Generational Equity: The debt essentially represents a “tax” on future generations. Today’s spending is being financed by the earnings of Americans who haven’t even entered the workforce yet.

The Cost to the Average Household

To bring these massive numbers down to earth, the Senate Joint Economic Committee’s April 2026 update provides a sobering breakdown:

Debt per Person: Approximately $114,000

Debt per Household: Approximately $289,000

Is There a Way Out?

The U.S. has been here before. After 1945, the debt-to-GDP ratio was successfully whittled down to 34% by 1980. However, that was achieved through a unique combination of post-war industrial dominance, a massive “Baby Boom” workforce, and rapid GDP growth.

Today, the path is narrower. Solutions generally fall into three difficult categories:

Entitlement Reform: Adjusting Social Security and Medicare to match modern life expectancies.

Revenue Increases: Raising taxes or closing loopholes to narrow the deficit.

Growth Incentives: Policies designed to make the “GDP” side of the ratio grow faster than the “Debt” side.

The Bottom Line

Crossing the 100% threshold is a “reckoning” moment. It signals that the era of “cheap” borrowing is over. As interest payments continue to eat a larger slice of the federal pie, the pressure on the American taxpayer—and the pressure to make hard political choices—will only intensify.

The red line has been crossed. The question now is whether we have the political will to head back toward the black.

We continue to assist companies nationwide in converting IEEPA tariff refund claims into immediate cash, even after the launch of U.S. Customs and Border Protection’s(“CBP”) CAPE refund portal and the latest April 28th update from the U.S. Court of International Trade (“CIT”).

CIT’s April 28th status review confirmed that the lead IEEPA refund litigation has largely moved from the legal entitlement phase into the implementation and payment phase. In simple terms, the question is no longer primarily whether many importers are entitled to refunds, the issue is when those refunds will actually be paid.

While CBP officially launched CAPE on April 20th to process refunds, there was no new court order requiring immediate payment of all claims. Instead, the CIT is supervising execution, while Customs works through claim submissions, liquidation status, eligibility reviews, and administrative processing. This distinction matters. CBP has indicated that certain accepted claims may be paid within approximately 45–60 days plus statutory interest.

However, “acceptance” is not the same as submission. Importers must first complete filing requirements, resolve broker authority issues, verify liquidation status, satisfy procedural review, and clear compliance review before the payment clock truly begins. For many importers, especially those with older entries, previously liquidated claims, multiple brokers, documentation issues, or claims that may fall outside CAPE Phase 1, the actual recovery timeline could extend for many months or significantly longer. As a result, our buyers remain highly active in purchasing IEEPA tariff refund claims, with transactions from $250,000 to $7 million purchased at a Buy Rate of 85%, while claims exceeding $7 million have a Buy Rate of 90%.

Why Importers are still Selling Tariff Refund Claims after CAPE Opened

Judge Eaton of CIT did not order immediate universal payment of all claims. CBP’s estimated payment window begins only after formal claim acceptance, not submission.

Many claims do not clearly qualify for CAPE Phase 1 and may require later phases. Finally liquidated entries remain one of the largest unresolved issues. Previously liquidated entries may still require protests, reliquidation, or additional litigation. The right to a refund is clearer—but the timing of payment remains uncertain.

CSV upload issues, ACE access problems, and broker mismatches can delay acceptance. Documentation gaps and reconciliation issues remain common. Customs audit and compliance review may delay payment even after filing.

Trump Administration appeal deadlines and future legal developments could delay the timing of refund payments. Processing millions of entries may create substantial administrative backlogs. Port-by-port inconsistencies may slow recovery for certain importers. Working capital needs often cannot wait for government processing timelines/.

Importers Are Choosing To Monetize Now

Immediate working capital for inventory, payroll, and vendor obligations. Reduced lender pressure and improved borrowing base flexibility. Elimination of refund timing risk and litigation uncertainty. Improved balance sheet certainty. Faster access to liquidity without waiting for government disbursement. Stronger buyer pricing now that CAPE implementation is underway as Buy Rates increased from 45% in February to 85% today

For many businesses, immediate liquidity today is worth more than waiting for a larger payment later. Many importers are no longer asking. “Will I get paid?”, They are asking, “Is waiting worth the delay, uncertainty, and operational risk?”. For many companies, the answer is no. We work with importers with claims starting at $250,000, with no maximum limit across industries including food, seasonal goods, apparel, and home products.

Most transactions can be completed in approximately 10 business days, assuming proper documentation and credit quality.

Contains information related to marketing campaigns of the user. These are shared with Google AdWords / Google Ads when the Google Ads and Google Analytics accounts are linked together.

90 days

__utma

ID used to identify users and sessions

2 years after last activity

__utmt

Used to monitor number of Google Analytics server requests

10 minutes

__utmb

Used to distinguish new sessions and visits. This cookie is set when the GA.js javascript library is loaded and there is no existing __utmb cookie. The cookie is updated every time data is sent to the Google Analytics server.

30 minutes after last activity

__utmc

Used only with old Urchin versions of Google Analytics and not with GA.js. Was used to distinguish between new sessions and visits at the end of a session.

End of session (browser)

__utmz

Contains information about the traffic source or campaign that directed user to the website. The cookie is set when the GA.js javascript is loaded and updated when data is sent to the Google Anaytics server

6 months after last activity

__utmv

Contains custom information set by the web developer via the _setCustomVar method in Google Analytics. This cookie is updated every time new data is sent to the Google Analytics server.

2 years after last activity

__utmx

Used to determine whether a user is included in an A / B or Multivariate test.

18 months

_ga

ID used to identify users

2 years

_gali

Used by Google Analytics to determine which links on a page are being clicked

30 seconds

_ga_

ID used to identify users

2 years

_gid

ID used to identify users for 24 hours after last activity

24 hours

_gat

Used to monitor number of Google Analytics server requests when using Google Tag Manager