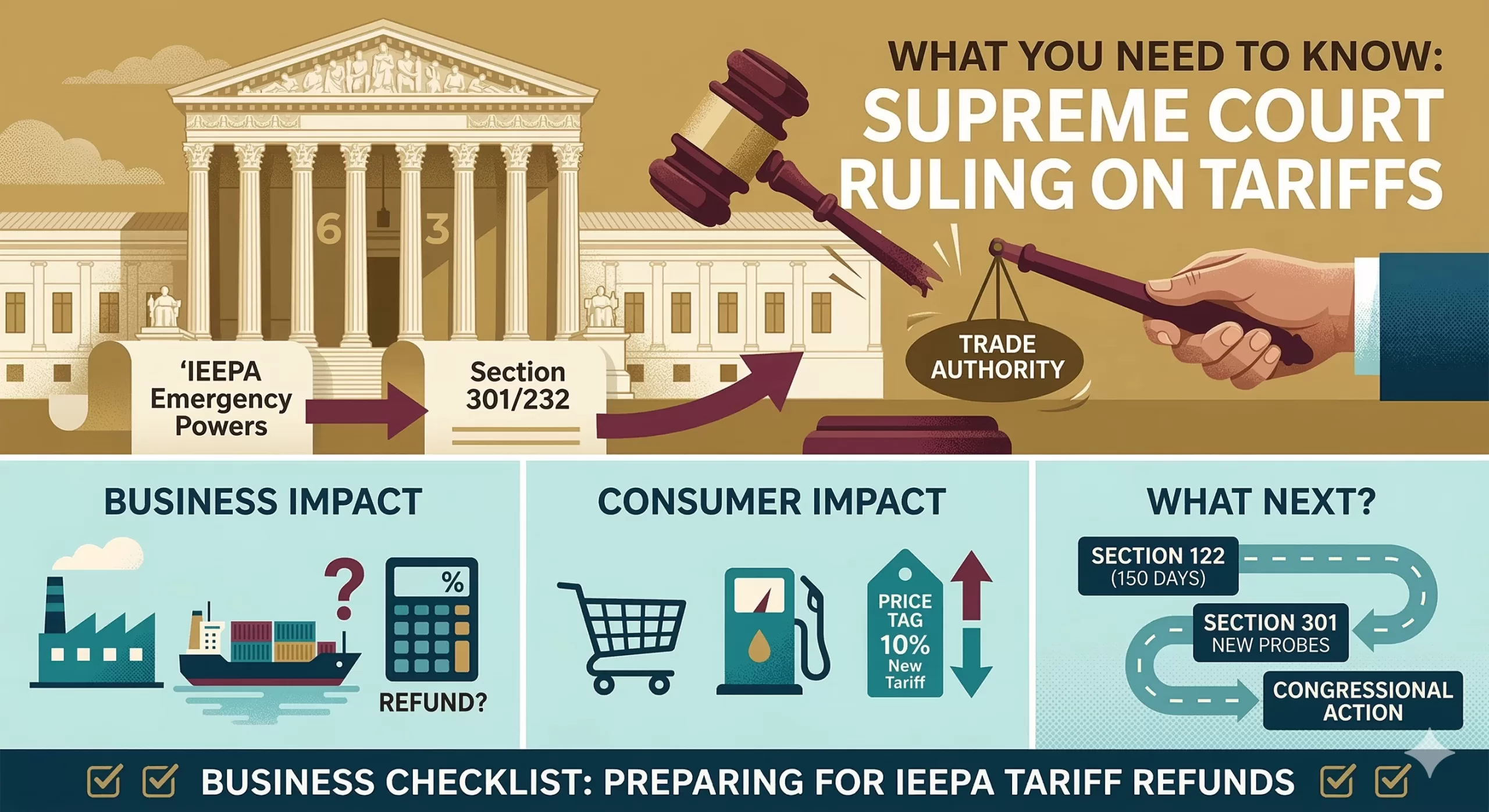

Convert IEEPA Tariff Claims to Cash on an Expedited Basis

I have been actively assisting companies nationwide in converting their IEEPA tariff refund claims into immediate cash.

U.S. Customs and Border Protection is rolling out a centralized system (CAPE) to process refunds, and some trade experts believe that certain importers could begin receiving refunds within the next six months. However, there remains significant uncertainty around timing, and many industry participants believe that a large portion of claims could still take years to fully resolve.

This divergence is driven by several factors, including:

The complexity and scale of processing millions of entries

The possibility that certain categories of claims may be prioritized over others, delaying recovery for more complex or lower-volume importers

The need for new administrative procedures, as IEEPA does not clearly define a refund mechanism

The potential for case-by-case eligibility determinations

Ongoing legal and procedural developments, including possible appeals by the Trump Administration and implementation challenges

Liquidation Status – Whether entries have already been liquidated, which in many cases may require formal protests or litigation to reopen and recover duties

The likelihood of inconsistent treatment across ports (port-by-port) or entry types as CBP implements new processes in phases

Documentation gaps and data reconciliation issues, particularly for older entries or those filed across multiple brokers

The absence of clear guidance on how interest on refunds will be calculated and paid, which could lead to further disputes

Capacity constraints within CBP and the potential for processing backlogs as refund volumes scale

Continued legal challenges around the scope of eligibility, including disputes over classifications, valuation, or origin that could delay specific claims

As a result, while some importers may receive refunds within six months, others, particularly those with more complex or previously liquidated entries, could face a multi-year recovery timeline. To address this uncertainty, financial institutions and hedge funds are actively purchasing IEEPA tariff refund claims at a discount.

Current buy rates are as high as 85% of the expected refund value, depending on claim size, credit quality of the importer and documentation quality as these claims are not directly assignable. AES works with importers with claims starting at $250,000, with no maximum limit. Since entering this market five months ago, AES has facilitated the monetization of approximately $20 million in claims across industries including food, seasonal goods, apparel, and home products.

Market pricing has evolved significantly: Prior to the February 20, 2026, Supreme Court ruling, claims traded at approximately 20–25%

Following the ruling, pricing increased to 40–50%

More recently, improving legal clarity and market participation have driven pricing to current levels of up to 85% of the IEEPA tariff refund amount

While some importers initially adopted a “wait and see” approach in anticipation of near-term refunds, the combination of timing uncertainty and significantly improved pricing has led many to explore monetization as a way to eliminate risk and accelerate liquidity. The Funds AES works with are able to complete transactions in approximately 2–3 weeks, depending on the completeness and quality of documentation.

For more information on this process, contact Factoring Specialist, Chris Lehnes