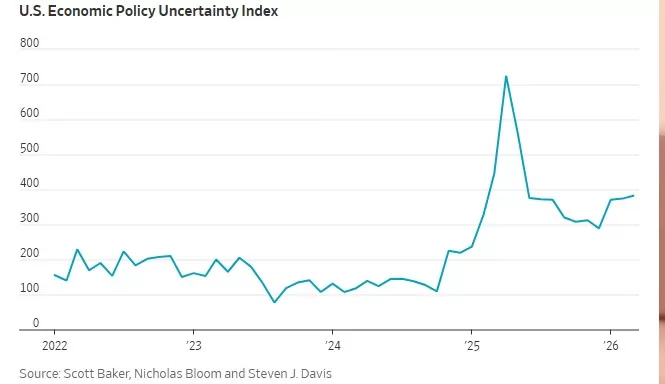

If the global economy feels like a high-wire act lately, you aren’t alone. We are currently navigating a “polycrisis“—a fancy term for when multiple major headaches (inflation, geopolitical tension, and shifting labor markets) all hit the fan at the same time.

We are standing on a narrow ledge. One side leads to a hard landing; the other leads to a stabilized “new normal.” Here is a look at the forces threatening to push us off, and the safety nets that might just pull us back.

The Push: What Could Tip Us Over?

It doesn’t take a wrecking ball to cause a recession; sometimes, it just takes a few well-placed dominos. Here are the primary risks:

The “Higher for Longer” Fatigue: While central banks use interest rates to cool inflation, keeping them elevated for too long puts immense pressure on household debt and corporate margins. If the “lag effect” hits all at once, consumer spending—the engine of the economy—could stall.

Geopolitical Aftershocks: Energy prices are notoriously sensitive to global conflict. Any significant escalation in major trade corridors can reignite supply chain chaos, sending the cost of goods back into the stratosphere.

The Commercial Real Estate Ghost Town: With remote work now a permanent fixture, many office buildings are sitting half-empty. As these property loans come due for refinancing at higher rates, we could see a localized banking tremor.

The Pull: What Could Help Us Pull Through?

It’s not all doom and gloom. There are several structural “muscles” keeping the economy upright:

The Resilient Labor Market: Despite tech layoffs making headlines, overall unemployment remains historically low. As long as people have jobs, they tend to keep spending, which provides a powerful floor for the economy.

The Productivity “AI Bump”: We are at the beginning of a massive technological shift. Early adoption of generative AI is already beginning to streamline workflows and reduce operational costs, which could lead to a non-inflationary growth spurt.

Household Balance Sheets: Unlike the 2008 crash, many consumers and corporations locked in low interest rates years ago. This “debt buffer” has bought the private sector time to adjust to the new economic reality.

The Bottom Line: Balance, Not Freefall

The economy isn’t necessarily “broken,” but it is transitioning. We are moving away from an era of “free money” and into an era where efficiency and strategic investment matter again.

Scenario

Key Driver

Likely Outcome

The Hard Landing

Persistent inflation + high rates

Brief but sharp recession; rising unemployment.

The Soft Landing

Controlled cooling + tech growth

Flat growth for a year, followed by a steady recovery.

The No Landing

Continued high spending

Economy stays hot, but rates stay high indefinitely.

The Takeaway: While the ledge is narrow, the path across is still visible. Navigating the next twelve months will require agility from policymakers and patience from investors. We may be on the edge, but we aren’t over it yet..

Press Release: (March 26, 2026) Versant Funding LLC is pleased to announce that it has funded a $1.4 Million non-recourse factoring facility to a manufacturer of equipment used by global auto companies.

While our newest client has successfully secured contracts with some of the world’s largest manufacturers, slow-paying accounts receivable are putting pressure on the company’s cash flow and preventing them from taking on new business.

“In evaluating a funding opportunity, Versant focuses exclusively on the quality of our client’s accounts receivable” according to Chris Lehnes, Business Development Officer for Versant Funding, and originator of this transaction. “Since this company’s customers are among the strongest on the planet, our facility will essentially have no cap and will grow automatically as the company’s AR balances increase, providing our client the cash needed to expand.”

About Versant Funding: Versant Funding’s custom Non-Recourse Factoring Facilities have been designed to fill a void in the market by focusing exclusively on the credit quality of a company’s accounts receivable. Versant Funding offers non-recourse factoring solutions to companies with B2B or B2G sales from $100,000 to $30 Million per month. All we care about is the credit quality of the A/R. To learn more contact: Chris Lehnes|203-664-1535 | chris@chrislehnes.com

For many distributors, the word “factoring” carries some outdated baggage. If you’re hesitant to pull the trigger, it’s likely because of one of these common misconceptions. Let’s separate the noise from the facts:

The Myth

The Reality

“Factoring is a sign of financial trouble.”

Factoring is a sign of growth. Most companies use factoring because they are growing too fast for their cash flow to keep up. It’s a strategic choice to fuel expansion, not a last-ditch effort to stay afloat.

“My customers will think I’m going under.”

It’s a standard B2B practice. Major retailers and manufacturers deal with factors every day. In many industries, like apparel or electronics distribution, it’s actually the “gold standard” for managing receivables.

“It’s way too expensive.”

Look at the ROI. While the fee (1–3%) is higher than a bank loan, the “cost of waiting” 60 days for a check often means missing out on new inventory or early-pay discounts from your own suppliers that could actually save you more than the factoring fee.

“I’ll lose control of my customer relationships.”

You stay in the driver’s seat. Modern factoring companies act as a professional extension of your back office. They want your customers to stay happy so they keep buying (and paying). You still manage the sales and service; they just handle the math.

“It’s just like a high-interest loan.”

It’s not a loan at all. Because you are selling an asset (your invoice), you aren’t taking on debt. There are no monthly principal or interest payments to worry about—the “payment” comes from your customer, not your bank account.

The “Silent” Benefit: Professional Credit Checks

One “Reality” that distributors often overlook is that a factor acts as a free credit department. Before you ship $50,000 worth of goods to a new client, you can ask your factor to check their credit. If the factor won’t buy the invoice, that’s a massive red flag that you probably shouldn’t be selling to that customer on terms in the first place.

What you should know in selecting a factoring Partner

Choosing a factoring company is like choosing a long-term business partner. The right one will act as your back-office credit department; the wrong one can be an expensive administrative nightmare. Use this checklist to vet potential partners:

1. The Core Logistics

[ ] Industry Expertise: Do they have experience with the specific nuances of distribution (e.g., handling chargebacks, bill-backs, or progressive shipping)?

[ ] Advance Rate: Will they advance at least 80–90% of the invoice value?

[ ] Funding Speed: Can they provide “Same Day” or “Next Day” funding once an invoice is verified?

[ ] Funding Source: Are they a Direct Lender (bank-backed) or an independent factor? (Direct lenders often have lower rates and more stability).

2. Transparency & Fees

[ ] The “All-In” Rate: Ask for a breakdown of all fees. Look out for hidden “junk fees” like application fees, wire fees, or credit check fees.

[ ] Recourse vs. Non-Recourse: * Recourse: You must buy back the invoice if your customer doesn’t pay. (Lower fees).

Non-Recourse: The factor takes the credit risk if the customer goes bankrupt. (Higher fees).

[ ] Volume Requirements: Are there “Monthly Minimums”? If you don’t hit a certain volume, will you be penalized?

3. The “Relationship” Factor

[ ] Dedicated Account Manager: Will you have a single point of contact who knows your business, or a generic 1-800 help desk?

[ ] Customer Interaction Style: How do they contact your customers for verification? You want a partner who is professional and polite, as they represent your brand.

[ ] Technology Integration: Do they sync with your accounting software (QuickBooks, NetSuite, etc.) for easy invoice uploading?

4. Contract Flexibility

[ ] Contract Length: Avoid multi-year lock-ins. Look for month-to-month or one-year terms with clear exit clauses.

[ ] Termination Notice: How much notice is required to leave? (Usually 30–90 days).

[ ] Personal Guarantee: Is a personal guarantee required? (Standard for many small business factors, but worth clarifying).

What is Factoring: In the world of distribution, the “growth paradox” is a real headache. You land a massive new retail contract—which is great news—but suddenly you’re shelling out for inventory and shipping costs while your customer sits on a 60- or 90-day payment term.

For many distributors, waiting for those invoices to clear creates a suffocating bottleneck. This is where Accounts Receivable (AR) Factoring comes in. It’s not a loan; it’s a financial tool that turns your unpaid invoices into immediate working capital.

How It Works: The Quick Breakdown

Instead of waiting months for a customer to pay, you sell your outstanding invoices to a “factor” (a specialized financial company).

The Advance: The factor typically advances you 80% to 90% of the invoice value within 24 hours.

The Collection: The factor handles the collection from your customer.

The Rebate: Once the customer pays, the factor sends you the remaining balance, minus a small fee (usually 1–3%).

4 Major Benefits for Distributors

1. Bridge the Inventory Gap

Distributors often have to pay suppliers long before they get paid by their own clients. Factoring provides the liquidity to pay your manufacturers upfront, often allowing you to take advantage of early-payment discounts that can actually offset the cost of the factoring fee itself.

2. Fuel Rapid Scalability

Traditional bank loans are limited by your credit history or collateral. Factoring, however, scales with your sales. The more you sell to reputable customers, the more funding becomes available. It allows you to say “yes” to large orders that you otherwise couldn’t afford to fulfill.

3. Professional Credit Management

Many factoring companies act as an extension of your back office. They perform credit checks on your potential customers, helping you avoid “bad seeds” before you ship a single pallet. This reduces your risk of bad debt and saves your team the awkwardness of making collection calls.

4. No New Debt

Since factoring is the purchase of an asset (your invoice) rather than a loan, it doesn’t show up as debt on your balance sheet. This keeps your debt-to-equity ratio clean, making your business look much healthier to future investors or traditional lenders.

Is It Right For You?

Factoring is particularly powerful if you are:

A startup with a thin credit history but blue-chip customers.

Experiencing seasonal spikes that drain your cash reserves.

Tired of the “waiting game” associated with 30, 60, or 90-day terms.

While there is a cost involved, the ability to reinvest that cash immediately into new inventory or operations often outweighs the fee. In the fast-moving world of distribution, speed is a competitive advantage.

Factoring vs. A Traditional Line of Credit: A Distributor’s Comparison

While both tools solve cash flow problems, they operate very differently. Here is how they stack up for a growing distributor:

Feature

AR Factoring

Traditional Bank Line of Credit (LOC)

Funding Limit Based On…

The creditworthiness of your customers and your accounts receivable balance.

Your business’s credit history, profitability, and your collateral.

Speed of Funding

Extremely fast. Setup takes a few days; once active, funding often occurs within 24–48 hours of invoice verification.

Slow. The approval process can take weeks or even months.

Debt Type

Not Debt. It is the “asset purchase” of your invoices.

Debt. This is a loan that appears as a liability on your balance sheet.

Impact on Credit

Boosts Credit Score. It provides cash to pay your suppliers and operational debts on time.

Lowers “Available” Credit. Utilizing the full LOC can temporarily lower your score until it’s paid down.

Administrative Support

The factor often provides credit management and collection services, freeing up your back office.

You retain full responsibility for all collections and monitoring customer credit.

Scalability

Unlimited. As your credit-worthy sales grow, your available funding automatically increases.

Capped. Your limit is fixed and requires a re-application process to increase.

Gemini said

Certainly. Here is a comparison table and a section you can drop directly into your blog post.

Factoring vs. A Traditional Line of Credit: A Distributor’s Comparison

While both tools solve cash flow problems, they operate very differently. Here is how they stack up for a growing distributor:

Feature

AR Factoring

Traditional Bank Line of Credit (LOC)

Funding Limit Based On…

The creditworthiness of your customers and your accounts receivable balance.

Your business’s credit history, profitability, and your collateral.

Speed of Funding

Extremely fast. Setup takes a few days; once active, funding often occurs within 24–48 hours of invoice verification.

Slow. The approval process can take weeks or even months.

Debt Type

Not Debt. It is the “asset purchase” of your invoices.

Debt. This is a loan that appears as a liability on your balance sheet.

Impact on Credit

Boosts Credit Score. It provides cash to pay your suppliers and operational debts on time.

Lowers “Available” Credit. Utilizing the full LOC can temporarily lower your score until it’s paid down.

Administrative Support

The factor often provides credit management and collection services, freeing up your back office.

You retain full responsibility for all collections and monitoring customer credit.

Scalability

Unlimited. As your credit-worthy sales grow, your available funding automatically increases.

Capped. Your limit is fixed and requires a re-application process to increase.

Which One Wins for Distributors?

A bank line of credit is almost always the cheapest form of capital if you can get approved for a large enough limit.

However, for distributors in a hyper-growth phase, or those whose balance sheets don’t match their ambition, AR factoring offers unmatched speed and scalability. It allows you to leverage your customers’ financial strength to fund your own growth.

The Final Verdict: When to Choose Factoring

For a distributor, the choice between factoring and other financing boils down to your growth trajectory and customer base.

A traditional bank line of credit is often the lowest-cost option, but it is also the most rigid. If you have years of steady profitability and a “boring” (predictable) growth curve, the bank is your best friend.

However, AR factoring is the superior choice if:

You are growing faster than your cash flow allows: If a sudden 50% increase in orders would actually break your business because you can’t afford the inventory, you need factoring.

You have “lumpy” revenue: If you deal with seasonal spikes where you need $500k in October but only $50k in January, the flexibility of factoring is unmatched.

Your customers are larger than you: If you are a small distributor selling to giants like Walmart or Amazon, a factor will look at their multi-billion-dollar credit rating to fund you, rather than your own limited history.

Ultimately, factoring isn’t just a way to get paid early—it’s a way to weaponize your accounts receivable to outmaneuver competitors who are still stuck waiting for a check in the mail.

The first few warm days of spring mean flowers, baseball, and for many small business owners in March 2026, the annual financial checkup. If you’ve looked at your numbers and realized you need a cash injection for new equipment, that third location, or an aggressive inventory build, you know the drill: It’s time to find the capital. While large national banks are the obvious choice, they are often difficult, impersonal, and slow. By comparison, credit unions have become the unexpected superstars of commercial lending, especially for small and medium-sized enterprises (SMEs).

If you are hunting for a business loan this month, you need to understand why credit unions are dominating and how to find the one that will actually make that critical “yes” happen for your business.

The Not-So-Secret Advantage of the Member-Owner

To understand why credit unions often beat banks on business lending, you have to look at their structure.

Banks answer to shareholders who demand profits and high returns on equity. Every decision, including who gets a loan, is filtered through the lens of maximizing shareholder value.

Credit unions, however, are not-for-profit cooperatives. They do not have public stock. Their members (you, me, and other account holders) are the owners.

This single difference ripples through every interaction. For business lending in 2026, it means:

1. Rates and Fees That Just Make More Sense: Instead of returning profit to Wall Street, credit unions reinvest earnings back into the institution and their members. This often manifests as lower interest rates on commercial loans and significantly lower loan-origination and maintenance fees. In 2026, when inflation has been a recent headache, a difference of 0.5% on a large loan term can mean thousands of dollars saved.

2. Hyper-Local Expertise: When you sit down with a commercial lender at a bank, their rules, algorithms, and models might be set at headquarters 2,000 miles away. They may not understand the specific micro-market in Newtown, Connecticut, where you are operating. But your local credit union officer lives here. They understand why opening a second pizza parlor on the new development is a smart bet, not a risky venture. They lend based on local market knowledge.

3. Relationships Over Risk-Scores: A bank will look at your credit score and financial statements, enter them into a model, and receive a automated “Approve” or “Deny.” Credit unions, especially smaller, focused ones, prioritize relationships. They are more likely to have a real human look at your complete business plan, understand your unique vision, and listen to the story behind your application, not just the numbers on the page.

The “New Reality” of SBA Lending

One of the most important developments in 2026 is that the Small Business Administration (SBA) has made it significantly easier and faster for credit unions to facilitate SBA 7(a) and 504 loans.

For many small businesses, these government-backed loans are the Holy Grail: long terms, lower interest rates, and lower down-payment requirements. Previously, massive banks dominated this space because the paperwork was crushing.

However, the “Streamline and Connect Act” of 2024 (as we projected) drastically simplified the SBA application process and created digital interfaces specifically designed for smaller community financial institutions.

This means that in March 2026, the local credit union you never expected to handle an SBA application is now a Preferred Lender, capable of getting your government-backed loan approved in weeks, not months.

How to Evaluate a Credit Union in March 2026

You can’t just walk into the nearest credit union and expect a perfect loan offer. To find the “best” one for your business right now, you must be strategic:

Step 1: Membership Criteria (The Gateway)

Credit unions can’t just lend to anyone. They operate under a specific “field of membership” (FOM). While some have broadened their charters, many are still strictly limited. To find the “best,” you must find the one you can actually join.

Geographic FOM: Are you eligible because your business is located in Newtown, CT, or the surrounding county? This is the most common path.

Associational or Professional FOM: Are you a veteran? An educator? A first responder? A member of a specific local church or union? There are niche credit unions specialized for these groups, and they often offer highly beneficial industry-specific lending programs.

Step 2: Technology and Speed

While personal relationships are the hallmark of credit unions, it’s 2026. You should not have to wait 30 days for a response to your application. A strong, business-friendly credit union will have a fast, streamlined digital application portal.

They should have digital tools that connect directly to your accounting software (like QuickBooks or Xero), allowing their lenders to instantly verify your cash flow without forcing you to hunt down piles of paper bank statements. If a credit union’s website looks like it hasn’t been updated since 2018, that is a massive red flag.

Step 3: Ask About Specific Business Expertise

The credit union that is excellent for a car loan or a personal mortgage is not necessarily the best choice for a $500,000 commercial line of credit to finance inventory for a manufacturing business.

When you interview a prospective credit union, ask about their experience in your industry. A credit union that specializes in healthcare practice lending will have different perspectives and better loan structures than one that primarily works with general contractors.

The March 2026 Takeaway: Don’t Lead with a Bank

Your default shouldn’t be the massive financial conglomerate that you can only reach via an 800-number. Your first stop in 2026 should be your local, community-focused credit union. They are built to serve owners like you, and they have the tools and local knowledge to help your business take flight this spring.

Factoring Proposal: After recently recovering from the devasting impacts of tariffs, this company requires PO financing to rebuild inventory. Their existing factor is uncooperative and must be replaced by Versant which has the ability to facilitate PO funding though a trusted partner.

In a surprising turn of events, German factory orders in have shown an unexpected and robust surge, signaling a potentially stronger-than-anticipated rebound in the nation’s industrial sector. This latest data has instilled a renewed sense of optimism among economists and policymakers, suggesting that Europe’s largest economy might be on a more solid recovery path than previously estimated.

The Federal Statistical Office announced this morning that new factory orders jumped by a significant margin in the past month, far exceeding analyst expectations. This remarkable uptick follows a period of cautious growth and even some contractions, making the current surge all the more impactful. The increase was broad-based, with both domestic and international orders contributing substantially to the overall rise.

A Deeper Dive into the Numbers

The reported increase in orders was particularly driven by strong demand for capital goods, indicating that businesses are investing more in machinery and equipment – a key indicator of future production capacity and confidence. Intermediate goods also saw a healthy boost, suggesting renewed activity across various supply chains.

Economists are pointing to several factors contributing to this positive development. A resilient global demand, particularly from key trading partners, appears to be playing a significant role. Furthermore, a gradual easing of supply chain bottlenecks, which have plagued manufacturers for months, is allowing companies to fulfill orders more efficiently and take on new business.

Impact on the Broader Economy

This unexpected surge in factory orders is a shot in the arm for the German economy, which has been grappling with persistent inflation and the lingering effects of global uncertainties. A strong industrial sector is crucial for Germany’s economic health, as it is a major employer and a significant contributor to GDP. The improved outlook could lead to increased hiring, higher wages, and ultimately, stronger consumer spending.

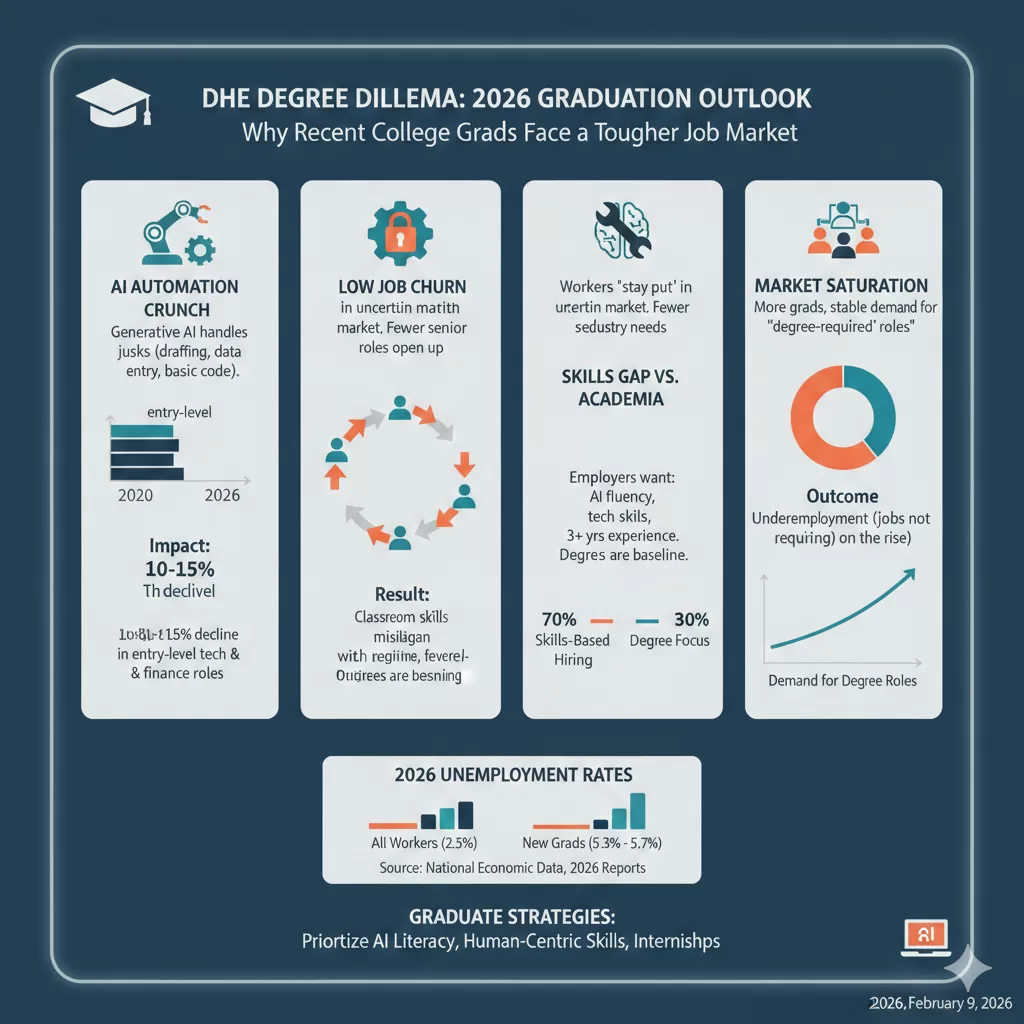

For decades, the path to employment followed a predictable script: graduate high school, earn a four-year degree, and step into a stable career. But for the Class of 2026 and other recent grads, that script has been heavily revised.

While the national unemployment rate remains relatively stable, a closer look reveals a “white-collar friction” that is hitting young graduates particularly hard. Recent data suggests that unemployment for workers aged 22–27 is significantly higher than for the general population, with some reports showing rates as high as 5.3% to 5.7% for new degree holders compared to just 2.5% for their more experienced counterparts.

Why is the “college advantage” seemingly cooling off? Here are the primary factors reshaping the entry-level landscape.

1. The “Bottom Rung” is Being Automated

Perhaps the most significant shift in 2026 is the impact of Generative AI. Historically, junior roles involved “intellectually mundane” tasks: drafting reports, organizing data, or basic coding. These were the “training wheels” of a career.

Today, AI agents handle these tasks with 90% accuracy in seconds.

The Result: Companies are becoming more “top-heavy.” They still need experienced managers to oversee AI, but they need fewer junior employees to do the legwork.

The Crunch: Entry-level hiring has seen double-digit declines in sectors like tech and finance, as firms use AI to boost productivity without expanding their headcount.

2. The Great “Stay Put” (Low Churn)

In a healthy economy, people switch jobs, creating “openings” at the bottom for new talent. In 2026, we are seeing a collapse in voluntary job switching.

“Workers are holding onto their roles because the market feels risky; as a result, the natural ‘churn’ that usually pulls recent grads into the workforce has stalled.”

When mid-level employees don’t move up or out, the entry-level pipeline remains clogged.

3. The Rising “Skills Gap” vs. Academic Focus

There is a growing disconnect between what is taught in the classroom and what is required in a modern office.

The Degree is the Baseline, Not the Finish Line: Employers are shifting toward skills-based hiring. According to NACE, 70% of employers now prioritize specific technical skills and AI fluency over the prestige of the degree itself.

Experience Over Everything: Job postings that once asked for 0–2 years of experience are increasingly demanding 3+ years or specific internships. For a recent grad, this creates the classic paradox: You can’t get the job without experience, but you can’t get experience without the job.

4. Market Saturation

We are currently seeing the result of “education-neutral” growth. The supply of college graduates has increased steadily, but demand for roles that specifically require a degree has leveled off. This has led to a rise in underemployment, where graduates find themselves in roles that don’t actually require their hard-earned credentials.

What Can Grads Do?

The market is tougher, but it isn’t closed. To stand out in the current environment, graduates must:

Prioritize AI Literacy: It’s no longer a “plus”; it’s a requirement. Show how you use AI to work faster and smarter.

Focus on “Human-Centric” Skills: Emphasize critical thinking, complex problem solving, and emotional intelligence—things AI still struggles to replicate.

Treat Internships as Essential: In 2026, an internship is often the only way to bypass the “3 years of experience” requirement.

Our Accounts Receivable Factoring program can quickly meet the working capital needs of businesses in the energy industry.

Versant’s underwriting focus is solely on the quality of a company’s accounts receivable, which enables us to rapidly fund businesses which do not qualify for traditional lending.

Contains information related to marketing campaigns of the user. These are shared with Google AdWords / Google Ads when the Google Ads and Google Analytics accounts are linked together.

90 days

__utma

ID used to identify users and sessions

2 years after last activity

__utmt

Used to monitor number of Google Analytics server requests

10 minutes

__utmb

Used to distinguish new sessions and visits. This cookie is set when the GA.js javascript library is loaded and there is no existing __utmb cookie. The cookie is updated every time data is sent to the Google Analytics server.

30 minutes after last activity

__utmc

Used only with old Urchin versions of Google Analytics and not with GA.js. Was used to distinguish between new sessions and visits at the end of a session.

End of session (browser)

__utmz

Contains information about the traffic source or campaign that directed user to the website. The cookie is set when the GA.js javascript is loaded and updated when data is sent to the Google Anaytics server

6 months after last activity

__utmv

Contains custom information set by the web developer via the _setCustomVar method in Google Analytics. This cookie is updated every time new data is sent to the Google Analytics server.

2 years after last activity

__utmx

Used to determine whether a user is included in an A / B or Multivariate test.

18 months

_ga

ID used to identify users

2 years

_gali

Used by Google Analytics to determine which links on a page are being clicked

30 seconds

_ga_

ID used to identify users

2 years

_gid

ID used to identify users for 24 hours after last activity

24 hours

_gat

Used to monitor number of Google Analytics server requests when using Google Tag Manager