While the macro economy is feeling the “pump shock,” the impact on small business lending and accounts receivable (AR) factoring is more nuanced. For many industries, rising oil prices act as a catalyst for alternative financing, as traditional bank credit tends to tighten just when operational costs spike.

1. Impact on Small Business Lending

Traditional bank lending to small businesses is becoming more restrictive as energy-driven inflation persists.

- The “Double Squeeze”: Small businesses are facing higher input costs (fuel/transport) alongside high interest rates. Banks, wary of compressed profit margins, are increasing their underwriting scrutiny.

- The Approval Gap: As of early 2026, large banks are approving only about 68% of small business loans, compared to 82% at smaller, community-focused institutions.

- Pivot to High-Cost Credit: With traditional loans taking weeks to approve, many businesses are turning to credit cards (averaging 18%–36% interest) to cover immediate fuel and supply chain gaps, significantly increasing their long-term debt burden.

2. The Surge in AR Factoring Demand

In a high-oil-price environment, factoring often shifts from a “last resort” to a strategic cash-flow tool, particularly for energy-intensive sectors.

- Fuel as a Fixed, Immediate Expense: In industries like trucking and oilfield services, fuel must be paid for daily or weekly, while customers (shippers or large operators) often demand 30- to 90-day payment terms. Factoring bridges this “cash gap” without adding traditional debt to the balance sheet.

- Sector-Specific Trends:

- Transportation/Trucking: Factoring companies are seeing record demand. These businesses often enjoy the highest advance rates (90%–97%+) because their invoices are backed by tangible freight delivery.

- Oilfield Services: As drilling activity ramps up in response to higher prices (especially in the Permian Basin), service providers are using factoring to scale quickly—buying new equipment or meeting surge payroll without waiting for 60-day payouts from major oil producers.

- Manufacturing: With raw material costs rising alongside energy, manufacturers are factoring invoices to maintain liquidity reserves to buy inventory before prices hike further.

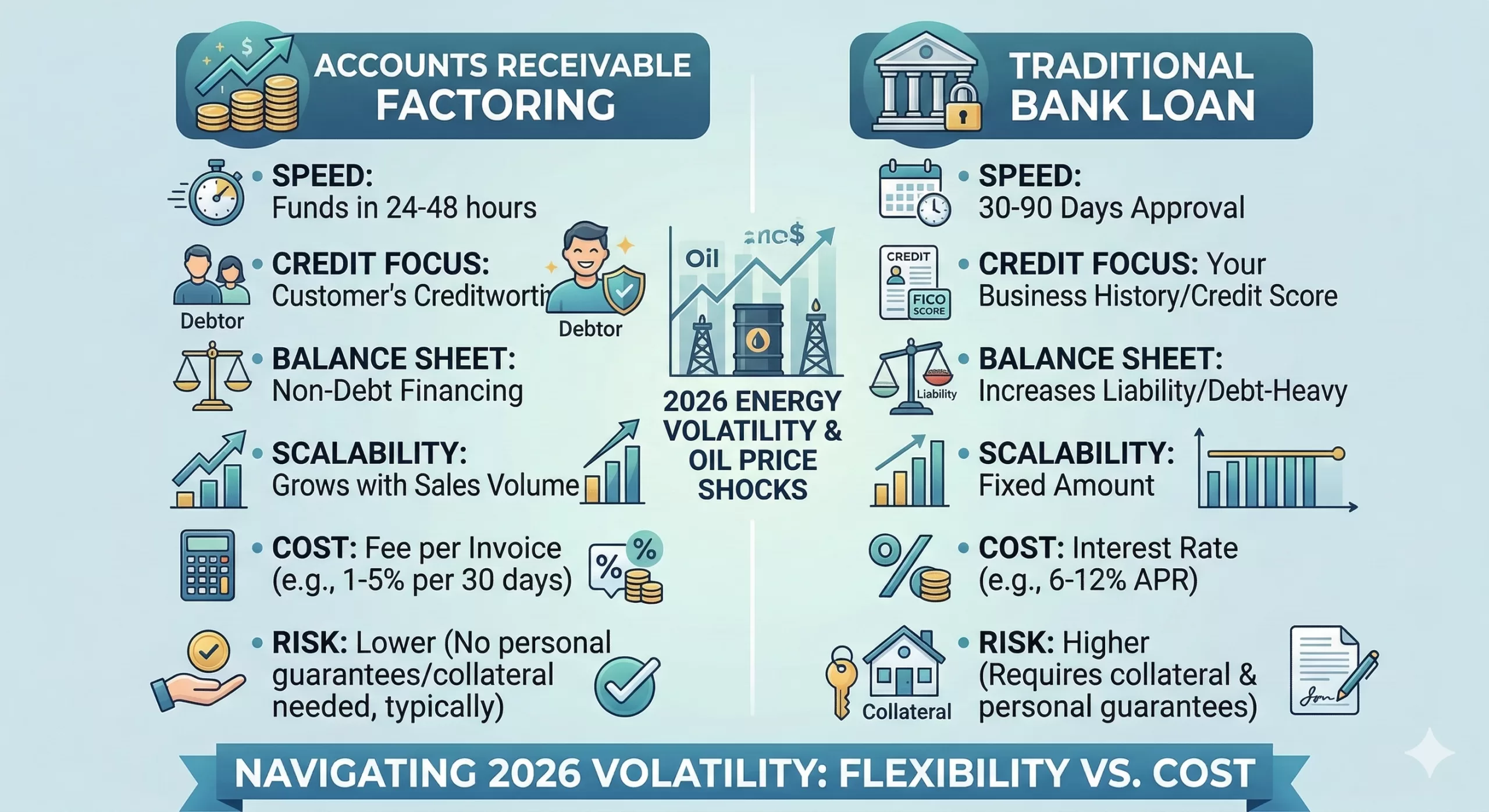

Factoring vs. Traditional Lending in 2026

| Feature | Traditional Bank Loan | AR Factoring |

| Approval Basis | Business credit & history | Customer (Debtor) credit |

| Speed of Funding | 2 – 7 weeks | 24 – 48 hours |

| Debt Load | Increases liability on balance sheet | No new debt (selling an asset) |

| Scalability | Fixed limit | Grows with your sales volume |

| Cost | Lower interest (6%–12%) | Higher fees (1%–5% per 30 days) |

Strategic Outlook

For the remainder of 2026, businesses that rely on “floating” cash flow are likely to prioritize speed over cost. While factoring fees are higher than bank interest, the ability to access cash within 24 hours to pay for $4.00/gallon diesel is often the difference between staying operational and grounding a fleet.

In a volatile economy where oil prices are surging and traditional banks are pulling back, choosing the right financing tool is a high-stakes decision. For B2B businesses—especially those in staffing, digital marketing, and manufacturing—the choice often comes down to the speed of Factoring versus the lower cost of a Bank Loan.

Below is a strategic comparison designed to help you evaluate which path aligns with your current cash flow needs.

Factoring vs. Bank Loans: 2026 Strategic Comparison

| Feature | Accounts Receivable Factoring | Traditional Bank Loan |

| Speed to Cash | Ultra-Fast: Funds usually arrive within 24–48 hours after invoice setup. | Slow: Approval typically takes 30–90 days of underwriting. |

| Credit Focus | The Debtor: Decisions are based on your customer’s credit and payment history. | The Business: Based on your FICO score, tax returns, and years in business. |

| Balance Sheet | Debt-Free: It is the sale of an asset (invoices), not a liability. | Debt-Heavy: Adds a liability that can impact your debt-to-income ratio. |

| Scalability | Unlimited: As your sales grow, your available cash grows automatically. | Fixed: You are capped at a set amount and must re-apply to increase it. |

| Total Cost | Higher Fees: Usually 1%–5% per 30 days (effective APR is higher). | Lower Rates: Typically 6%–12% APR for qualified businesses. |

| Risk | Low: No collateral like your house or equipment is typically required. | High: Often requires a blanket lien on assets or personal guarantees. |

Export to Sheets

The “Why Now?” Factor: Navigating 2026 Volatility

Pros of Factoring in This Market

- Immediate Fuel/Supply Buffer: With diesel prices fluctuating, factoring gives you the cash today to buy inventory or fuel before the next price hike.

- Protects Your Growth: In sectors like digital marketing or staffing, you can’t wait 60 days for a client to pay to meet your weekly payroll. Factoring ensures your team stays paid regardless of when the client cuts the check.

- No “Covenant” Stress: Bank loans often come with strict “covenants” (rules about your profit margins). If high oil prices temporarily squeeze your margins, a bank might call your loan; a factor simply keeps funding your sales.

Cons to Consider

- Margin Impact: If your profit margins are already thin (common in food production or distribution), the 1%–3% factoring fee could eat up a significant portion of your net income.

- Customer Perception: While widely accepted today, some ultra-conservative clients might still prefer to pay you directly rather than a third-party factor.

The Bottom Line

If you have long-term stability and time to wait, a Bank Loan is cheaper. However, if you are growing rapidly or facing unpredictable costs, Factoring acts as a flexible insurance policy for your cash flow.