When we think of the massive oil tankers carving through the turquoise waters of the Persian Gulf, we usually focus on the millions of barrels of crude they carry or the geopolitical weight of the Strait of Hormuz. But behind every voyage is an invisible, multi-layered shield of paper and promise: Maritime Insurance.

In the high-stakes environment of 2026, where regional tensions have sent shockwaves through energy markets, understanding how these vessels are protected is more than just a lesson in finance—it’s a window into how global trade survives in a crisis.

1. The Trinity of Protection

Insuring a $150 million vessel carrying $100 million worth of oil isn’t a “one-and-done” policy. It is built in three primary layers:

Hull and Machinery (H&M)

Think of this as the “comprehensive” insurance for the ship itself. It covers physical damage to the vessel’s structure and engines caused by “perils of the sea”—collisions, groundings, fires, or heavy weather.

- Who provides it? Commercial insurers (often via the Lloyd’s of London market).

Protection and Indemnity (P&I)

This is unique to the shipping world. Instead of a traditional company, shipowners join P&I Clubs—mutual associations where members pool their money to cover third-party liabilities.

- What it covers: Oil spills (pollution), crew injuries, and damage to docks or other ships.

- Why it matters: In the event of a catastrophic leak in the Gulf, the P&I club provides the billions of dollars needed for cleanup.

War Risk Insurance

This is the “hot” layer. Standard H&M policies specifically exclude damage from weapons of war, mines, or terrorism. To sail into the Persian Gulf, owners must purchase a separate War Risk policy.

- The “Listed Areas”: The Joint War Committee (JWC) in London designates high-risk zones. Once a ship enters these waters, its standard coverage is suspended, and a special “voyage premium” kicks in.

2. The “Additional Premium” Spike

In stable times, war risk insurance is a negligible cost. However, in the current 2026 climate—marked by recent escalations—the math has changed drastically.

When the Strait of Hormuz is designated a high-risk zone, insurers charge an Additional War Risk Premium (AWRP).

- Normal rates: Historically around 0.01% to 0.05% of the ship’s value.

- Current 2026 rates: We have seen spikes reaching 1% to 5% (or even 10% for “missile magnet” vessels with specific national ties).

The Reality Check: For a tanker worth $130 million, a 1% premium means the owner must pay $1.3 million just for a single seven-day transit through the Gulf.

3. 2026: The Rise of Government Backstops

The most significant shift this year has been the intervention of national governments. When private insurers find the risk “unpriceable” or “opaque,” they may stop offering coverage entirely, which effectively halts oil flow.

To prevent a global energy collapse, we are seeing:

- U.S. Reinsurance Plans: The U.S. International Development Finance Corp (DFC) recently announced a $20 billion reinsurance program to provide a “safety net” for commercial insurers.

- Sovereign Guarantees: Countries like India or China may provide state-backed insurance for their own flagged vessels to ensure their energy security remains intact when the private market retreats.

4. Why This Matters to You

You might not own a tanker, but you feel the insurance market every time you visit the gas station. When insurance premiums jump from $200,000 to $2,000,000 per trip, that cost is passed down the supply chain. If the “invisible shield” of insurance disappears, the tankers stop moving, and the world’s energy supply enters a chokehold.

Maritime insurance isn’t just a legal requirement; it is the financial lubricant that allows the world’s most dangerous—and essential—trade route to stay open.

When a massive oil spill occurs in the Persian Gulf, the response isn’t just about booms and skimmers—it’s about a highly choreographed financial “waterfall” designed to handle billions of dollars in claims.

In the context of the current 2026 escalations, the International Group of P&I Clubs (IG) and global compensation regimes are facing their most significant test since the 1990s.

1. The P&I “Claims Waterfall” (2026/27 Structure)

If a member vessel spills oil, the money for cleanup and compensation flows through a specific hierarchy. For the 2026 policy year, the limits are structured to handle “mega-spills”:

| Tier | Amount | Source of Funds |

| Individual Club Retention | First $10 million | The specific P&I Club the ship belongs to (e.g., Gard, Skuld). |

| The Pool | $10 million – $100 million | Shared among all 12 P&I Clubs in the International Group. |

| Market Reinsurance (GXL) | $100 million – $1.1 billion | Global reinsurers (lead by AXA XL in 2026). |

| Overspill Layer | Up to ~$9.8 billion | A “catch-all” where all member shipowners globally are taxed to pay the claim. |

Crucial Note for 2026: While general P&I cover can reach nearly $10 billion, oil pollution claims are strictly capped at $1 billion per incident under standard P&I rules. If damages exceed $1 billion, the international “Fund” system takes over.

2. The Three-Tier Compensation Regime

When a spill exceeds what the shipowner’s insurance can pay, international conventions (which most Gulf nations are party to) kick in:

- Tier 1: The Civil Liability Convention (CLC). This is the shipowner’s P&I insurance (up to the $1 billion cap). It is “strict liability,” meaning the owner pays even if the spill wasn’t their “fault,” provided it wasn’t an act of war.

- Tier 2: The 1992 IOPC Fund. If the damage exceeds the shipowner’s limit, this fund (financed by oil importers, not shipowners) pays out additional compensation.

- Tier 3: The Supplementary Fund. Provides a third layer of compensation for major disasters, bringing the total available to approximately $1.15 billion.

3. The 2026 “Act of War” Complication

There is a massive legal “elephant in the room” right now. Under the CLC and P&I rules, shipowners and their insurers are not liable for oil pollution if the spill was caused directly by an “act of war, hostilities, civil war, or insurrection.”

The Current Crisis Scenario:

As of March 2026, several tankers (like the one off the coast of Kuwait last week) have been damaged by explosions.

- If it’s an accident: The P&I “Waterfall” works as described above.

- If it’s a missile/mine (Act of War): The standard P&I Club may deny the claim. This is why the War Risk Insurance you asked about earlier is so critical. It “buys back” that pollution coverage specifically for war events.

The “Blue Card” System

Even in 2026’s volatility, ships must carry a “Blue Card” issued by their P&I Club. This is a certificate of financial responsibility that proves to Gulf coastal states (like Saudi Arabia or the UAE) that there is a billion-dollar guarantee behind that ship, regardless of the geopolitical climate.

4. 2026 Market Update: Coverage Suspensions

As of March 5, 2026, several major P&I clubs (including NorthStandard and the American Club) have issued 72-hour cancellation notices for certain “non-poolable” war risk covers in the Gulf.

- What this means: While the “mutual” (core) insurance remains, the extra “war-time” pollution cover is being moved to a “buy-back” basis, often costing charterers up to $30,000 per week just to maintain the same level of protection they had for $25,000 per year in 2025.

In the wake of the escalations earlier this month, the maritime insurance market effectively seized up. Standard war risk premiums skyrocketed from 0.25% to over 1.5% of a vessel’s value, and many insurers issued 72-hour cancellation notices, essentially “grounding” the global tanker fleet.

To break this deadlock, the U.S. government launched a massive intervention on March 6, 2026. Here is how the new $20 Billion Reinsurance Backstop works and why it’s a radical shift in maritime finance.

1. The “Sovereign Backstop” Mechanics

Normally, the U.S. International Development Finance Corporation (DFC) focuses on infrastructure in developing nations. Under the new directive, it has pivoted to become the world’s largest “reinsurer of last resort” for the Persian Gulf.

- The Waterfall: Private insurers (like Chubb, who was named lead partner yesterday, March 11) issue the primary policies to shipowners. If a tanker is hit, Chubb pays the claim, but the DFC “backstops” the loss, reimbursing the insurance company for the most extreme payouts.

- The Rolling Fund: The DFC is providing $20 billion on a rolling basis. This means as voyages successfully complete and the risk expires, that capacity is “recycled” to cover the next wave of ships.

- Targeted Coverage: The program focuses specifically on Hull & Machinery and Cargo. Notably, early reports suggest it may exclude certain pollution liabilities if a ship is sunk, leaving that risk to the P&I Clubs.

2. Why the Government Stepped In

Private markets like Lloyd’s of London are built on “priceable risk.” When the risk of a missile strike becomes a “near certainty” rather than a “possibility,” private premiums become so expensive they are effectively a “no.”

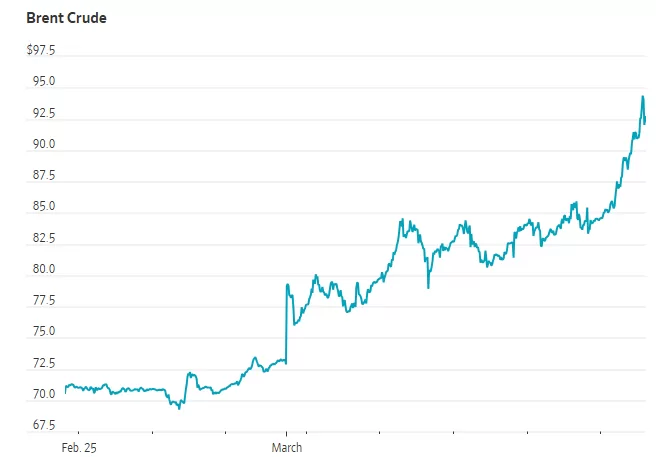

By offering insurance at what the administration calls a “very reasonable price,” the U.S. is effectively subsidizing the cost of the voyage. This prevents a “risk premium” from being tacked onto every barrel of oil, which was threatening to push prices toward $200 a barrel last week.

3. The 2026 “Military-Insurance” Nexus

This isn’t just a financial program; it’s a tactical one. The DFC is coordinating directly with CENTCOM (U.S. Central Command).

- Qualified Vessels: Not every ship gets this coverage. To qualify for the $20 billion pool, vessels must meet strict criteria, likely including adherence to specific “safe corridors” monitored by the U.S. Navy.

- Naval Escorts: President Trump has linked the insurance backstop with the possibility of Navy escorts. The message to shipowners is: “We will insure the ship financially, and we will protect the ship physically.”

4. Current Market Friction

Despite the $20 billion infusion, the “Ghost Fleet” problem remains. Even with a guaranteed payout, many shipowners are hesitant because:

- Crew Safety: Insurance pays for the ship, but it doesn’t protect the lives of the seafarers.

- Force Majeure: Major energy players like QatarEnergy have already declared force majeure on LNG shipments this week, signaling that even with insurance, the physical danger is currently deemed too high for some.

The Big Picture

The center of maritime finance is momentarily shifting from London to Washington. By using the DFC’s balance sheet, the U.S. is attempting to “force” the market back to life. If successful, it could become a blueprint for how global trade is maintained in future “contested” waters.

As of March 12, 2026, the U.S. government’s $20 billion “Sovereign Backstop” has moved from a concept to a live operation. While the program is designed to get oil moving, the “fine print” of who is eligible reveals it is as much a tool of foreign policy as it is a financial product.

Based on the latest updates from the DFC (International Development Finance Corporation) and their lead partner, Chubb, here are the specific eligibility criteria and constraints:

1. The “Preferred Partner” Requirement

To access the government-backed rates, shipowners cannot go to just any broker.

- American Underwriting: Policies must be issued through “Preferred American Insurance Partners.” Chubb was named the lead underwriter on March 11, with other U.S.-listed firms like AIG and Travelers reportedly joining the consortium.

- Direct DFC Application: While Chubb handles the front-end, businesses must register directly with the DFC (via

maritime@dfc.gov) to be vetted for the sovereign guarantee.

2. Vessel & Cargo Constraints

The program is not a “blanket” cover for every ship in the Gulf. It is highly surgical:

- Prioritized Commodities: The backstop is explicitly for “strategic trade.” This includes Crude Oil, LNG, Gasoline, Jet Fuel, and Fertilizer. Ships carrying luxury goods or non-essential consumer electronics are currently pushed to the back of the line.

- Flag Requirements: While “all shipping lines” are technically eligible, priority is being given to U.S.-flagged vessels and those belonging to Allied Nations (specifically citing the UK, Israel, and GCC partners like Saudi Arabia and the UAE).

- The “Shadow Fleet” Exclusion: Any vessel with ties to sanctioned entities or the so-called “Ghost Fleet” (often used to bypass previous price caps) is strictly barred from the program.

3. The “CENTCOM” Compliance Hook

This is the most controversial eligibility rule. To be “qualified,” a vessel must agree to operational oversight by U.S. Central Command (CENTCOM):

- Assigned Corridors: Ships must stay within CENTCOM-designated “Safe Lanes.” Deviating from these coordinates for any reason (other than immediate safety of life at sea) can void the insurance instantly.

- Escort Readiness: Eligibility is often tied to the ship’s ability to integrate with naval escort protocols. If a ship refuses to take on a U.S. security liaison or follow convoy timing, the DFC backstop is retracted.

4. Financial Limits

- Initial Focus: The $20 billion pool currently only covers Hull & Machinery (H&M) and Cargo.

- The P&I Gap: Crucially, the backstop does not yet cover third-party pollution liability (P&I). This means if a ship is hit and causes a massive spill, the owner still relies on their traditional P&I Club. Because those clubs are currently issuing 72-hour cancellation notices for the Gulf, many owners are still refusing to sail despite the U.S. H&M guarantee.

The Current Standoff

Even with this $20 billion “shield,” the Persian Gulf remains at a near-standstill. As of this morning, over 200 ships remain at anchor outside the Strait. The insurance is available, but shipowners are now citing crew safety as the primary barrier—insurers can replace a ship, but they cannot replace a crew.

While the U.S. government’s $20 billion insurance backstop addresses the financial risk of losing a ship, the human element—the crew—has become the ultimate bottleneck. As of March 12, 2026, the “Crew War Risk” landscape has shifted into a high-stakes negotiation between unions and shipowners.

Here is the current breakdown of the incentives and rights for seafarers currently operating in or near the Persian Gulf:

1. The “Warlike Operations Area” (WOA) Designation

On March 5, 2026, the International Bargaining Forum (IBF) officially upgraded the Persian Gulf, the Strait of Hormuz, and the Gulf of Oman from a “High Risk Area” to a Warlike Operations Area (WOA). This is the highest possible danger classification in maritime labor law.

The Financial Incentives (The “Double Pay” Rule)

For seafarers who choose to stay on board during a transit, the pay structure has become extremely lucrative:

- 100% Basic Wage Bonus: Crews receive a bonus equal to their full basic salary for every day the ship is within the WOA.

- 5-Day Minimum: Even if the transit through the Strait takes only 12 hours, the IBF rules mandate a minimum of five days’ worth of bonus pay.

- Death & Disability: Compensation for death or permanent disability resulting from an incident in this zone is doubled (often reaching payouts of $200,000 to $500,000 depending on rank).

The “Combat Pay” Reality: An Able Seaman (AB) who typically earns $2,500/month in the Gulf could effectively earn an extra $400–$500 for a single week’s transit, while a Master (Captain) could see a bonus of several thousand dollars for the same period.

2. The Right to Refuse (Repatriation)

This is the “escape hatch” that is currently causing the massive backlog of 700+ tankers. Under the WOA designation:

- The Refusal Clause: Any seafarer has the legal right to refuse to sail into the Persian Gulf.

- Free Repatriation: If they refuse, the shipping company must fly them home at the company’s expense from the last “safe” port (often Fujairah or Muscat).

- Two-Month Severance: In addition to the flight home, the seafarer is entitled to two months of basic wage as compensation for the loss of their contract.

3. The 2026 “Humanitarian Emergency”

Despite the high pay, we are seeing a mass exodus of crews. As of this week:

- 35,000 Stranded: Over 20,000 commercial seafarers and 15,000 cruise passengers are currently “trapped” in the Gulf.

- Repatriation Gridlock: While crews have the right to leave, regional airspace closures and port lockdowns mean there are effectively no flights available to get them out.

- The “Mental Health” Toll: Unions like the ITF are warning that the combination of missile threats and the inability to go home is creating a psychological crisis on board the “Ghost Fleet” currently anchored off the coast of Oman.

4. The IRGC’s “Permission” System

A new complication emerged yesterday (March 11): The IRGC Navy has declared that all vessels must seek Iranian permission to transit the Strait.

- Crew Risk: Ships that ignore this “permission” (following U.S. orders to stay in “Safe Lanes”) are being specifically targeted.

- The Choice: Crews are now caught between two “Safe Lanes”—the one protected by the U.S. Navy and the one “permitted” by Iran. For many seafarers, no amount of “Double Pay” is worth being the target of a USV (Unmanned Surface Vessel) strike.

Summary of the “Price of Risk”

| Rank | Typical Monthly Base | Estimated Gulf Bonus (7-day Transit) | Total Monthly Potential |

| Master (Captain) | $12,000 | +$2,800 | $14,800 |

| Chief Engineer | $11,000 | +$2,500 | $13,500 |

| Able Seaman (AB) | $2,800 | +$650 | $3,450 |

Contact Factoring Specialist, Chris Lehnes