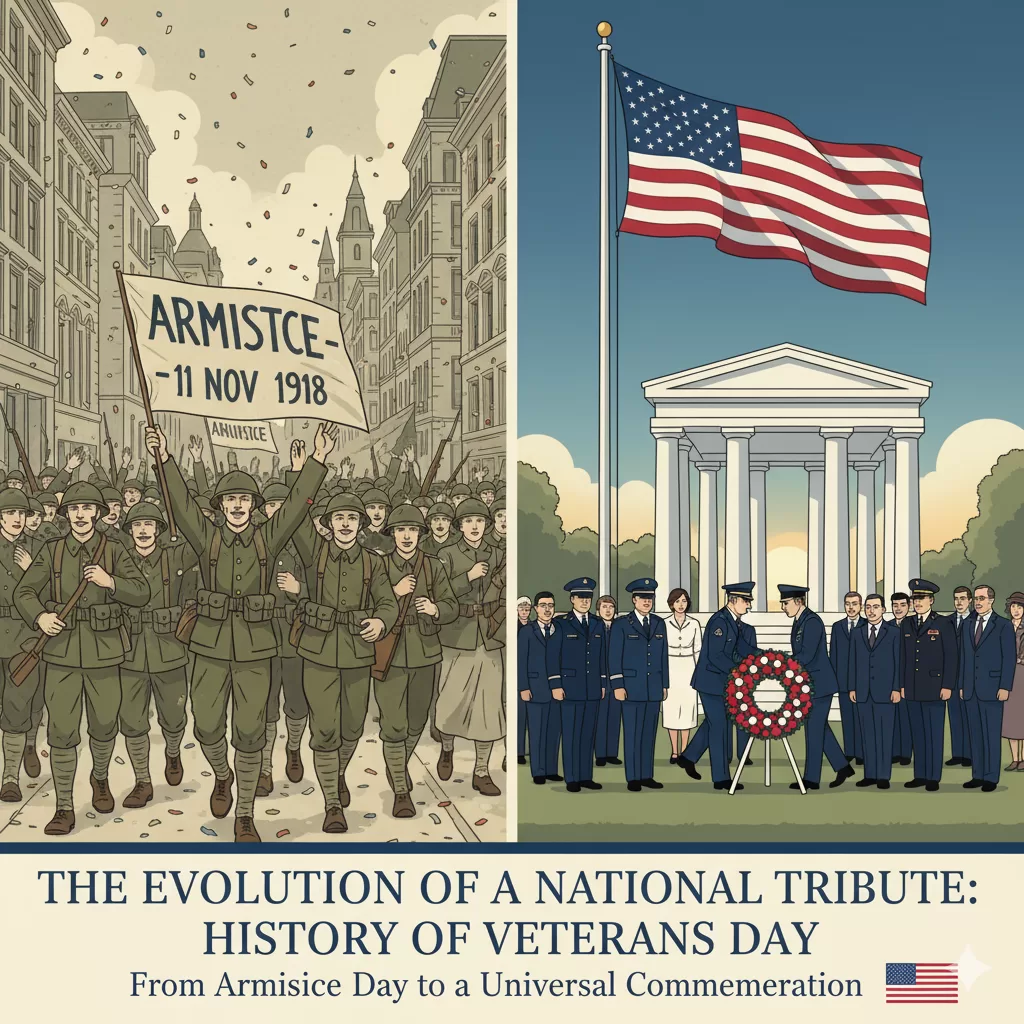

The holiday now known as Veterans Day, celebrated annually on November 11th, stands as a profound testament to the American commitment to its armed forces. It is a day dedicated to honoring all living and deceased military veterans who have served in the United States Armed Forces during wartime or peacetime. The history of this national holiday is not static; it is a narrative of evolution, reflecting the nation’s changing relationship with its military, transforming from a celebration of peace at the end of “the war to end all wars” into a universal commemoration of service.

The journey from Armistice Day to Veterans Day is a chronicle of remembrance, legislative action, and enduring patriotism, rooted in a single, historically significant moment: the cessation of hostilities that ended World War I.

I. Armistice Day: The Birth of a Commemoration – Veterans Day

The foundation of Veterans Day lies in the signing of the armistice that brought an end to the brutal fighting of World War I.

The Eleventh Hour, Eleventh Day, Eleventh Month (1918)

The pivotal date is November 11, 1918. The armistice, a temporary cessation of hostilities between the Allied nations and Germany, went into effect at the “eleventh hour of the eleventh day of the eleventh month.” While the Treaty of Versailles, the official peace treaty, was signed seven months later on June 28, 1919, November 11th was universally accepted as the symbolic end of the Great War.

In the United States and Allied countries, the news sparked spontaneous, joyous celebrations. However, the initial jubilation quickly gave way to a solemn realization of the immense sacrifice. The war had cost the lives of over 116,000 Americans, and millions more worldwide. The impulse to remember, to honor the dead, and to celebrate the hard-won peace became immediate and widespread.

President Wilson’s Proclamation (1919) – Veterans Day

The first official commemoration took place one year later. On November 11, 1919, President Woodrow Wilson proclaimed the first Armistice Day. His words set the initial tone for the observance:

“To us in America, the reflections of Armistice Day will be filled with solemn pride in the heroism of those who died in the country’s service and with gratitude for the victory, both because of the thing from which it has freed us and because of the opportunity it has given America to show her sympathy with peace and justice in the councils of the nations.”

Wilson’s vision for the day included parades, public meetings, and a brief two-minute suspension of all business activities starting at 11:00 a.m. The focus was dual: solemn pride in heroism and dedication to the cause of world peace.

The Tomb of the Unknowns (1921)

A crucial national tradition began in 1921, further cementing November 11th as a day of national reverence. On this date, an unknown American soldier from World War I was interred in the newly created Tomb of the Unknowns at Arlington National Cemetery.

Similar ceremonies had already occurred in France (at the Arc de Triomphe) and the United Kingdom (at Westminster Abbey). The American ceremony, attended by President Warren G. Harding, became the focal point for the nation’s tribute to its war dead, forever linking the sacred site of the Tomb with the Armistice Day commemoration. Congress also declared November 11, 1921, a legal federal holiday for the purpose of honoring all those who participated in the war.

II. Formal Recognition and the Interwar Years (1926-1938)

The observance of Armistice Day continued to grow throughout the 1920s, a decade marked by an idealistic hope for an era of lasting global peace.

Congressional Resolution (1926) – Veterans Day

On June 4, 1926, the U.S. Congress formally recognized the end of World War I and passed a concurrent resolution. This resolution requested that the President of the United States issue annual proclamations calling for the observance of November 11th with appropriate ceremonies. It further stated that the anniversary should be “commemorated with thanksgiving and prayer and exercises designed to perpetuate peace through good will and mutual understanding between nations.”

A Legal Federal Holiday (1938) – Veterans Day

Twelve years later, Armistice Day achieved its highest legislative status up to that point. A Congressional Act approved on May 13, 1938, officially made the 11th of November a legal Federal holiday. The act explicitly stated it was a day to be “dedicated to the cause of world peace and to be thereafter celebrated and known as ‘Armistice Day’.”

At this point, the holiday was explicitly dedicated to honoring the veterans of World War I. The core tradition was established: a moment of silence at 11 a.m., parades, and public orations focused on the themes of peace and the sacrifice of “The Great War” generation.

III. Transformation: From Armistice Day to Veterans Day

The optimistic hope that WWI would be “the war to end all wars” was tragically dashed with the outbreak of World War II in 1939 and the subsequent Korean War (1950–1953). The United States soon had millions of new veterans from multiple conflicts, and the name “Armistice Day” no longer accurately reflected the nation’s veteran population.

The Call for a Broader Holiday (Post-WWII) – Veterans Day

The push to expand the holiday began with a World War II veteran, Raymond Weeks of Birmingham, Alabama. Weeks organized a “National Veterans Day” celebration in 1947, which included a parade and festivities intended to honor all veterans. Weeks continued to lead this celebration annually and is today widely recognized as the “Father of Veterans Day.”

He and other veterans service organizations, such as the American Legion and Veterans of Foreign Wars (VFW), began lobbying Congress to broaden the focus of the federal holiday.

The Official Renaming (1954)

The efforts came to fruition in 1954. The 83rd Congress, recognizing the need to honor veterans from both World War II and the Korean War, amended the Act of 1938. They officially struck out the word “Armistice” and inserted “Veterans.”

President Dwight D. Eisenhower, a veteran and Supreme Commander of Allied Expeditionary Force in World War II, signed the legislation on June 1, 1954, making November 11th a day to honor American veterans of all wars. Later that year, on October 8, 1954, President Eisenhower issued the first Veterans Day Proclamation, encouraging citizens to join in the common purpose of appropriately and universally observing the anniversary.

IV. The Date Controversy and Restoration (1968-1978)

For over a decade, Veterans Day continued to be celebrated on its traditional, historically significant date of November 11th. However, a desire for administrative uniformity and economic stimulation led to a controversial change.

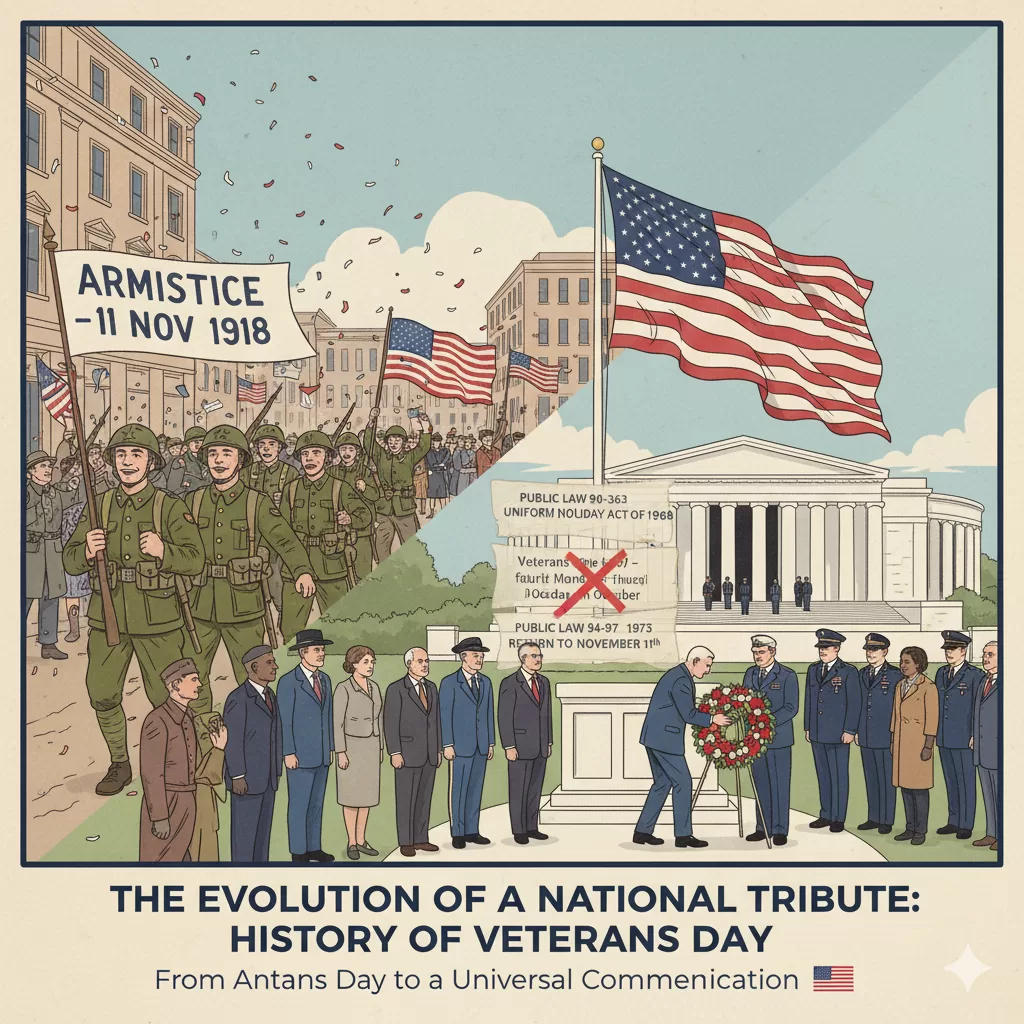

The Uniform Monday Holiday Act (1968)

In 1968, Congress passed the Uniform Monday Holiday Act (Public Law 90-363). The intent of this legislation was to ensure three-day weekends for federal employees by moving four national holidays—Washington’s Birthday, Memorial Day, Columbus Day, and Veterans Day—to be celebrated on a Monday.

Veterans Day was moved to the fourth Monday in October, with the change set to take effect in 1971.

Public Backlash and Reversion (1971-1978)

The first Veterans Day celebrated under the new law, on October 25, 1971, was met with significant confusion and widespread disapproval. It quickly became clear that the historical and patriotic significance of November 11th—the exact “eleventh hour”—was too deeply ingrained in the national memory to be casually changed for convenience.

Many states refused to comply and continued to celebrate the holiday on November 11th. Veterans service organizations, the military community, and the general public overwhelmingly advocated for a return to the original date.

Recognizing the strength of this popular sentiment and the historical importance of the date, President Gerald R. Ford signed Public Law 94-97 on September 20, 1975, which returned the annual observance of Veterans Day to its original date of November 11th, beginning in 1978. Veterans Day has been observed on November 11th ever since, regardless of the day of the week it falls upon.

V. Contemporary Celebrations and Traditions

Today’s observance of Veterans Day carries forward the traditions of Armistice Day while encompassing the scope of a broader, modern tribute.

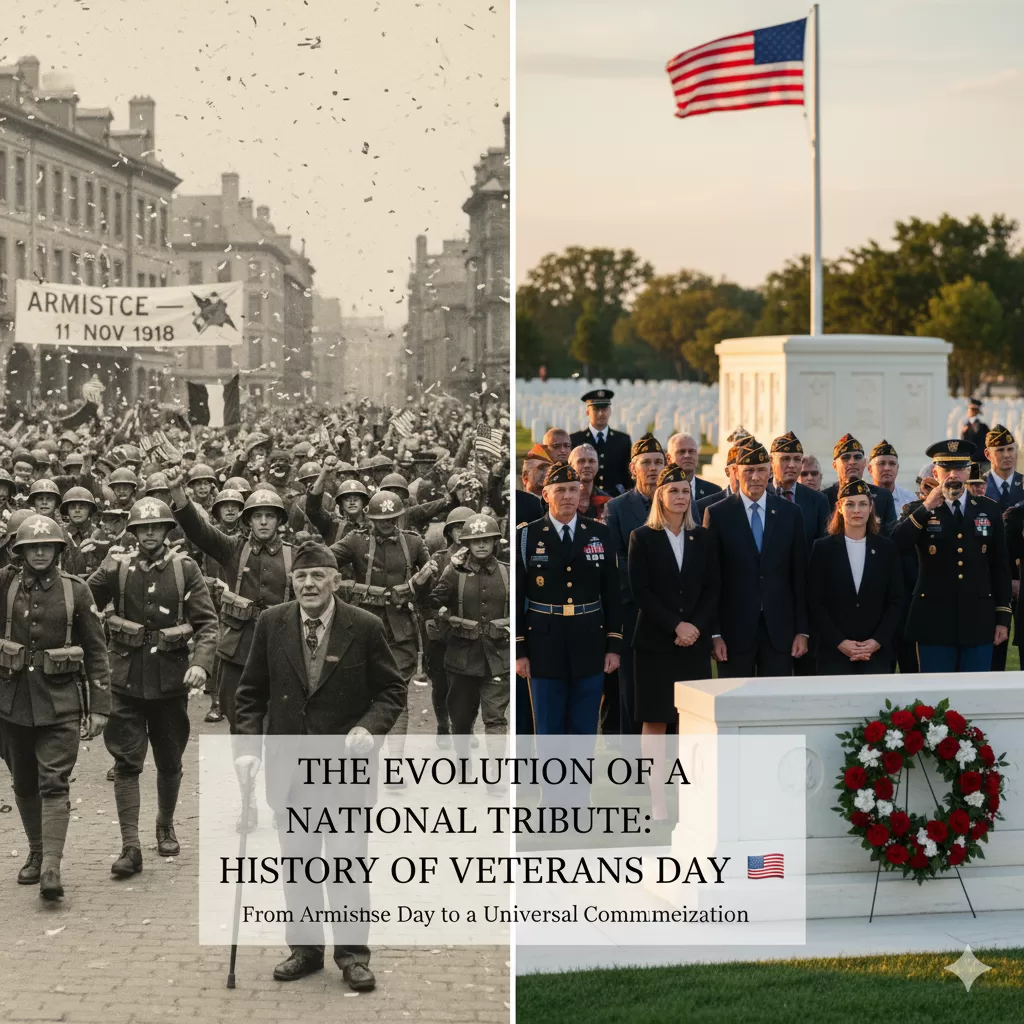

The National Ceremony at Arlington

The focal point for the official, national ceremony remains the Tomb of the Unknowns at Arlington National Cemetery. Every Veterans Day, at 11:00 a.m. EST, a combined color guard representing all military services executes “Present Arms” at the Tomb. A presidential wreath is laid, and the bugler plays Taps, symbolizing the nation’s profound respect and gratitude for its war dead and, by extension, all veterans. The rest of the ceremony takes place in the Memorial Amphitheater, where various military and government officials give addresses.

Parades and Community Events

Across the United States, celebrations include parades, community ceremonies, and memorial services. These local events are a direct link to the original Armistice Day tradition of public meetings and celebratory marches. Many feature marching bands, active duty service members, and, most importantly, veterans of every generation.

Honoring the Living

A crucial distinction between Veterans Day and Memorial Day is their focus. Memorial Day (the last Monday in May) is dedicated to honoring those who died in military service.Veterans Day is a day to honor all American veterans—living and deceased—for their patriotism, love of country, and willingness to serve and sacrifice for the common good.

This distinction shapes contemporary celebrations, which often include:

Gratitude Initiatives: Businesses, schools, and communities offer gestures of thanks, such as discounts, free meals, and card-writing campaigns to express direct gratitude to living veterans.

Educational Outreach: Schools and museums host events to educate the public, especially younger generations, about the history of the U.S. military and the sacrifices made by its service members.

The Two-Minute Silence: While not a universal law, the traditional two-minute silence at 11:00 a.m., commemorating the moment the guns fell silent in 1918, is still observed in many communities as a mark of respect and solemn remembrance.

Conclusion

The history of Veterans Day is a rich and moving narrative, one that begins with a moment of hopeful peace on a battlefield in France and evolves to encompass the service of millions across a century of conflicts. From a day dedicated to the Great War’s “Doughboys” to a universal celebration of all American veterans, the holiday on November 11th remains one of the most significant dates on the national calendar. It stands not only as a day of remembrance for the past but as an active acknowledgment of the commitment and sacrifice of all those who have worn the uniform of the United States Armed Forces.

Julia Austin’s After the Idea is a comprehensive guide to building and scaling a startup with intention. The book argues that long-term success hinges not on the initial idea alone, but on a deliberate, holistic approach to building the business. This is structured around four foundational pillars:

Product, People, Operations, and Working at Scale.

The central thesis is that founders must move beyond a narrow focus on building and fundraising to intentionally design their company’s culture, operational processes, and strategic vision from the outset. Key takeaways include the critical importance of deep “discovery work” to validate a problem before building a solution, treating the selection of a cofounder as a serious “courtship,” and embedding a strong, inclusive culture as the bedrock of the organization. The text provides actionable frameworks for navigating the often-overlooked but vital operational functions of legal, finance, and go-to-market strategy. Finally, it addresses the complex challenges of growth, including the founder’s transition from doer to leader, managing team dynamics at scale, and navigating exits while prioritizing mental health. The author draws extensively from personal experiences at successful startups like Akamai, VMware, and DigitalOcean, as well as from the journeys of her students and coaching clients, to provide a fact-dense, practical roadmap for entrepreneurs.

——————————————————————————–

Part I: The Product Pillar – The Primacy of Discovery of an Idea

The first pillar establishes that while building a product is easier than ever, building the right thing for the right people is the most difficult and critical challenge. A failure to deeply understand the problem and the target customer is a primary reason for startup failure, with 35% of failures attributed to a lack of product-market fit (PMF).

Why Discovery Matters After the Idea

Slow Down to Speed Up: Rushing to build a solution without fully understanding the problem leads to wasted time and money. Proper discovery work can prevent building the wrong product and helps structure the business operations correctly from the start.

Validate, Don’t Assume: Early discovery work validates not only the customer’s pain points but also the operational and business model implications.

Example (Found/Brij): Founders Kait Stephens and Zack Morrison initially aimed to create a B2C product for tracking lost items. Early, low-cost experiments revealed that the operational model (partnering with facilities, managing returns) was complex and unappealing. This discovery process unlocked a pivot to a B2B model (Brij), connecting brands to customers via QR codes—a completely different and more viable business.

Personal and Professional Insight: The discovery process offers crucial personal insights for founders, helping them determine if they are passionate about the market and the type of business they are building.

The Art of Discovery

The book advocates for moving beyond simple interviews and landing pages, which gauge interest rather than intent, to more robust experimentation.

Hypothesis Experiments: This is a four-step process to validate assumptions about personas, problems, and markets.

Brainstorm: Generate specific “I/we believe” statements.

Group: Consolidate similar hypotheses.

Prioritize: Focus on the most critical assumptions to test first.

Design Experiments: Create detailed plans with clear measures for success, moving from a SWAG (“scientific wild-ass guess”) to more concrete metrics over time.

Key Experimentation Techniques:

Ethnographic Research: Observing target customers in their natural environment to uncover subtle pain points and workarounds they may not articulate in interviews.

Example (Halo Braid): Founder Yinka Ogunbiyi spent hours in salons observing stylists to understand nuances like power supply access, storage space, and the desire for a mentally relaxing process, which informed the design of her hair-braiding device.

“Be the Bot”: Manually simulating the product’s function to gain deep, personal understanding before building anything.

Concierge Experiments: The customer is aware of the manual, “white glove” process.

Wizard of Oz (WoZ) Experiments: The customer believes they are interacting with an automated system, but humans are performing the tasks behind the scenes.

Low-Fidelity Experiments: Using paper prototypes, digital mock-ups, or handcrafted samples (like SAYSO cocktails) to test solutions without significant investment.

The Customer Journey and Vision Planning – After the Idea

Journey Mapping: A visual tool to plot a customer’s experience step-by-step, identifying touchpoints, emotional responses, and opportunities for improvement. “As-is” maps document the current process, while “to-be” maps envision the future with the proposed solution.

Storyboarding: A deeper, cartoon-style visualization of the customer’s process that helps build empathy and identify steps that can be eliminated or improved.

Setting a “True North”: Once traction begins, a startup must establish a broad, impact-focused vision or mission statement (e.g., Google’s “To organize the world’s information…”). This statement provides guardrails for future decisions and aligns the team.

Execution with OKRs: The vision is translated into an actionable plan using the Objectives and Key Results (OKR) framework. Goals should be SMART (Specific, Measurable, Achievable, Relevant, Time-bound) and tracked with relevant Key Performance Indicators (KPIs) that are specific to the business’s goals (e.g., OpenTable’s focus on speed of booking vs. Instagram’s focus on time on app).

——————————————————————————–

Part II: The People Pillar – Building a Kick-Ass Organization After the Idea

This pillar argues that the people—from cofounders to the first hires—are a startup’s most important asset. Neglecting the human aspects of the business is a common and fatal error.

The Cofounder Courtship After the Idea

The decision to have a cofounder is one of the most critical a founder will make. The relationship is compared to a marriage, requiring a deliberate and thoughtful “courtship” to ensure alignment.

To Partner or Go Solo?: This decision should be evaluated through three lenses:

Partnership: A self-assessment of one’s ability to collaborate, share risk, and handle conflict.

Expertise: An honest evaluation of skill gaps in technical, operational, or domain-specific areas.

Experience: Assessing real-world experience in operating businesses, particularly startups.

The Courtship Process: A multi-step process for vetting potential cofounders:

Conduct a Listening Tour: Speak with other cofounding teams about their experiences.

Write a Cofounder Job Description: Define the ideal traits, skills, and values.

Test the Relationship: Go beyond coffee chats. Engage in activities (road trips, projects) that reveal how you handle stress and make decisions together.

Have Vulnerable Conversations: Discuss core values, personal histories, and relationships with money.

Have the “Prenup” Conversation: Craft a cofounder agreement that clarifies equity, roles, IP, and exit scenarios before the business is in full flight.

Establishing Culture and Organizational Strategy After the Idea

Envisioning Company Culture: A startup’s core values and culture must be intentionally designed from day one. By the time a team reaches ten people, the culture is difficult to change.

Diversity, Equity, Inclusion & Belonging (DEIB): These practices must be woven into the company’s DNA from the start. A diverse team will not thrive without an inclusive culture where employees feel safe, welcome, celebrated, and championed.

Culture Carriers: These are employees who embody and evangelize the company’s values, fostering community and holding the team to high standards.

The White Box Exercise (WBE): An organizational strategy exercise to plan for future hiring needs.

Imagine the future: Outline business goals for the next 6-12 months.

Sketch the future org chart: Draw a functional chart with “white boxes” for the roles needed to achieve those goals.

Assess the current team: Place current employees into the future boxes, identifying growth potential, lateral moves, or “benchwarmers.”

Create an action plan: Determine who needs investment for growth, which empty boxes need to be filled, and how to handle team members who may not scale.

Hiring and Separation

Hiring Best Practices: Startups must “hold the bar” high for talent. Key practices include writing clear job descriptions that embrace ambiguity, sourcing through networks (“always be recruiting”), considering a “try before you buy” paid project, and focusing on a positive candidate experience.

Separation: Letting people go is inevitable. Before doing so, founders must ask if the person is failing the system, or if the system is failing the person. This involves checking for complicity (e.g., not providing clear expectations or “painting done”). When separation is necessary, it must be handled directly, humanely, and with legal counsel to preserve dignity and protect the company.

——————————————————————————–

Part III: The Operations Pillar – The Foundations of the Business After the Idea

This section covers the “mundane but important” operational activities that are essential for survival and scale. Underestimating their importance is a common mistake that can lead to failure.

Legal and Financial Matters

Lawyering Up: It is critical to engage startup-savvy counsel early. Lawyers unfamiliar with venture financing, equity agreements, and startup norms can be costly and detrimental.

Entity Formation: Choosing the right legal entity (LLC, C Corp, PBC) is a foundational step that impacts liability, taxation, and the ability to raise capital.

Financial Management: Founders must understand their own emotional relationship to money, as it drives nearly every financial decision. Key financial basics include:

Budgeting and Banking: Meticulously tracking cash flow, expenses (including SaaS sprawl), and having contingency plans like a line of credit.

Core Documents: Maintaining a balance sheet, a profit & loss (P&L) statement, and a financial forecast.

Fundraising Strategy After the Idea

Fundraising is framed as a necessary tool (“fuel for the speedboat”), not the ultimate goal.

Venture Backability: Before fundraising, a startup must have evidence of a real problem, proven traction, a clear moat, a strong team, and a defined business model.

Types of Capital and Funding Rounds: The book outlines various capital sources (VC, angel investors, grants, crowdfunding) and the typical progression of funding rounds (pre-seed, seed, priced rounds A/B/C).

The Process: For first-time founders, the process is an arduous journey often requiring over 100 meetings. Key advice includes seeking warm intros, using a “readable” deck to secure meetings and a “narratable” deck for presentations, and thoroughly vetting investors (“marrying someone you cannot divorce”).

Go-to-Market and Internal Alignment

GTM Strategy: This encompasses all activities to bring a product to market. Key elements include:

Branding: Creating the company’s identity, mission, and personality.

Brand Awareness: Ensuring the target market is familiar with the brand.

Key Functions: Public relations, social media, content strategy, and product marketing.

Product-Led Growth (PLG): Using the product itself as the primary driver for acquisition, often through free trials, self-service onboarding, and referrals.

The Two Three-Legged Stools: A framework for ensuring internal alignment:

EPD Stool (Engineering, Product, Design): The team that collaborates to define and build the product.

PSS Stool (Product, Sales, Support): The customer-facing team that creates a crucial feedback loop to ensure the company is building the right solutions and keeping customers happy.

——————————————————————————–

Part IV: The Working at Scale Pillar – Navigating Growth and Exits After the Idea

The final pillar addresses the challenges that arise as a startup moves from a small, nimble team to a larger, more complex organization.

Building to Scale After the Idea

The Boat Metaphor: Illustrates the founder’s evolving role:

Rowboat (Early Stage): Everyone is rowing together, focused on the how.

Motorboat (Growth Stage): The founder begins to toggle between the how and the what, delegating more.

Cruise Ship (Scale Stage): The founder is the captain, focused on the what (destination) and trusting the crew to handle the how.

Organizational Challenges:

Hub-and-Spoke Model: A common bottleneck where the founder acts as the central hub for all communication and decisions. The WE (work efficaciously) framework is presented as a method to move to a more collaborative, empowered model.

Founder Separation Anxiety: Early employees can feel disconnected as the company grows and layers of management are added. This requires intentional communication strategies like open office hours and skip-level meetings.

Product Evolution: To avoid the “build trap” (endlessly adding features to one product) or “peanut buttering” (spreading resources too thinly), a company must foster a culture of innovation to determine “what’s next.”

Balancing Hats and Mental Health

The Hat Conundrum: Founders and early joiners wear many hats. The “Have-to-Do, Want-to-Do, Good-At” (HTD/WTD/GA) assessment is a tool to help leaders prioritize, delegate, or develop skills for their various roles.

Mental Health: The text emphasizes that prioritizing mental health is a necessity, not a luxury. Key strategies include:

Setting firm boundaries between work and personal life.

Practicing self-care (exercise, mindfulness).

Building strong support systems (peer groups, coaches, therapists).

Learning to say “no” to opportunities that don’t align with core priorities.

Exits and Transitions After the Idea

Exits: The most common exit is through M&A. The experience depends heavily on whether the company was bought (a desirable target) versus sold (out of necessity) and the acquirer’s integration experience. Financial outcomes for founders are often significantly less than headline acquisition prices due to dilution.

Transitions: Whether through an exit or a leadership change, transitions are emotionally intense. Founders often struggle with a loss of identity and purpose post-exit. The book advocates for an intentional reflection process to process the experience, identify learnings, and chart a path forward.

Study Guide for After the Idea

Short-Answer Quiz

Describe the “911” incident at Akamai Technologies in 1999. What was the root cause, and what organizational changes did it prompt?

According to the text, what is the “diverge<>converge” process, and in what two scenarios is it recommended for startup teams?

Explain the difference between a “concierge” experiment and a “Wizard of Oz” experiment. Provide an example of one from the source text.

What is a “true north” statement, and how did establishing one benefit DigitalOcean?

The author outlines three lenses for evaluating the need for a cofounder. What are they, and what question does each lens help a founder answer?

What is the “white box exercise” (WBE), and what is its primary purpose for a growing startup?

Explain the concept of Product-Led Growth (PLG) and list three of its core tenets mentioned in the book.

The author describes two “three-legged stools” essential for startup operations. Identify both stools and the functions that make up their respective “legs.”

Describe the “boat metaphor” for a startup’s growth. What are the three phases, and how does a founder’s role typically shift in each phase?

What is the “hub-and-spoke” leadership model, and what two major leadership challenges does it create for a scaling startup?

Essay Questions for After the Idea

Analyze the author’s argument for why deep “discovery work” is critical to a startup’s long-term success, contrasting it with simply building a product quickly. Use the examples of Found/Brij and Halo Braid to support your analysis of different experimentation techniques.

Discuss the concept of “culture carriers” and the importance of establishing an inclusive culture from “day one.” How did the author’s experiences at Akamai and VMware shape the views on hiring, diversity, and creating a sense of belonging?

Examine the relationship between fundraising and a startup’s operational reality as presented in the text. What are the potential “gotchas” for first-time founders, and what is the key difference between being “bought” versus “sold” in an acquisition?

The author states, “people are complicated!” Using examples from Part II (People) and Part IV (Working at Scale), analyze the human challenges of scaling a startup, including the “cofounder courtship,” founder separation anxiety, and balancing different leadership “hats.”

Synthesize the author’s perspective on the interplay between vision, strategy, and execution. How do tools like journey mapping, OKRs, GTM strategies, and crisis management plans form a comprehensive operational foundation for a startup?

Quiz Answer Key for After the Idea

The “911” incident at Akamai was a full network outage in 1999 caused by a bright, early-hire engineer who checked in unapproved code on a Sunday. This rookie mistake, enabled by a lack of process, broke most of the internet at the time. The crisis spurred the leadership team to “grow up,” leading to the implementation of formal engineering and release processes, better monitoring tools, and a structured planning and communication process to prepare the business to scale.

The “diverge<>converge” process is a methodology where team members first consider their thoughts or ideas separately (diverge) and then come together to discuss their perspectives (converge). This technique helps remove bias and influence from dominant personalities. The book recommends using it for discussing the definition of success with cofounders and for brainstorming hypotheses about personas, problems, and markets during the discovery phase.

Both are types of “be the bot” experiments. In a concierge experiment, the participants are fully aware that a human is manually performing the service to learn about the process, such as the students testing meal prep by texting families. In a Wizard of Oz experiment, the audience is unaware that a human is behind the scenes; they believe they are interacting with an automated system, like the Juno founders manually researching loan options for users of their website.

A “true north” statement is a broad, impact-focused vision for the business, similar to a mission statement, that provides direction and guardrails for strategic decisions. At DigitalOcean, the team lacked a clear direction, causing growth to level out. By establishing a true north statement—”To empower developers to build great software”—the leadership team aligned on a strategy that led to shipping seven new products in under 18 months and moving upmarket.

The three lenses are partnership, expertise, and experience. Partnership helps a founder assess their ability to handle collaboration, shared risk, and conflict with a peer. Expertise forces a founder to assess their own technical, domain, or operational skill gaps that a cofounder could fill. Experience helps a founder evaluate their real-world background in operating a business and whether they need a partner with prior startup experience.

The white box exercise (WBE) is a visioning exercise to create an organizational strategy for a scaling company. It involves imagining the business 6-12 months in the future, sketching out a functional organizational chart without names (the “white boxes”), and then assessing the current team to see who fits where, who has growth potential, and what roles need to be hired for. Its purpose is to minimize costly restructurings by planning for future functional needs.

Product-Led Growth (PLG) is a strategy where the product itself is the primary driver of customer acquisition, expansion, and retention. Three of its core tenets are: having an exceptional user experience, offering a self-service model where users can onboard themselves, and providing a “try before you buy” option through free trials or freemium versions.

The first three-legged stool is EPD, representing the product development functions of Engineering, Product, and Design, which must work together to innovate and build solutions. The second is PSS, representing the customer-facing functions of Product, Sales, and Support, which must maintain a solid feedback loop to ensure customer satisfaction and retention.

The boat metaphor describes a startup’s scaling phases. Phase I is the “Rowboat,” where a small team rows together in the fog, focused on the how. Phase II is the “Motorboat” (15-20 people), where the destination is clearer and founders begin toggling between the how and the what. Phase III is the “Cruise Ship,” where founders act as captains focused on the what (direction) and trust their specialized crew to handle the how (execution).

The hub-and-spoke model is when a CEO-founder serves as the central “hub” coordinating all activities between their direct reports (“spokes”) instead of fostering collaboration among them. This creates two challenges: 1) it prevents leaders from developing interdisciplinary teamwork and creates decision-making bottlenecks, and 2) it can create trust issues and a psychologically unsafe environment if the founder discusses one leader’s performance with another.

Glossary of Key Terms in After the Idea

409A valuations The fair market value of the common stock of a private company as valued by a third-party appraiser. Startups need 409A valuations to grant employees stock options on a tax-free basis.

A/B test Testing two versions of a hypothesis to understand which fits better with the intended audience.

Acquihire When a venture is sold to a larger entity for its team and not for its products or services. This occasionally includes its intellectual property as well, although usually just for “parts” and integrated into the purchaser’s products.

Annual recurring revenue (ARR) The amount of revenue a business will garner per year.

Beachhead The starting market from where you are in a good strategic position to capture adjacent markets.

Business-to-business (B2B) A venture that creates products or services that solve problems for other businesses.

Business-to-consumer (B2C) A venture that creates products or services that solve problems for consumers.

Buyer persona Not always the user of the solution, they hold the purse strings. This persona is most common in B2B businesses. For example, the head of HR may buy a candidate-tracking system for their recruiters.

Conversion rate The average number of conversions per ad or other sales interaction, shown as a percentage. Conversion rate is calculated by simply taking the number of conversions and dividing that by the number of interactions that can be tracked to a conversion during the same time period.

Customer acquisition cost (CAC) Measures how much an organization spends to acquire new customers. It is the total cost of sales and marketing efforts, as well as property or equipment, needed to convince a customer to buy a product or service.

Directly responsible individual (DRI) The person who is ultimately responsible for a decision or making sure a project or task is completed.

Direct-to-consumer (DTC) A business that sells its products directly to consumers, typically online through its websites or mobile applications.

Diverge<>converge exercise Breaking down a thinking process into two phases: divergence and convergence. In the divergence phase, generate ideas to broaden possibilities, and in the convergence phase, eliminate or streamline the ideas to converge on the best solution.

Equity dilution A decrease in the percentage of ownership that existing shareholders have in a company. It occurs when a company issues new shares of stock to investors, which increases the total number of outstanding shares. This means that each existing shareholder’s percentage of ownership is reduced.

Fear of missing out (FOMO) A slang term referring to anxiety that an exciting or interesting event may currently be happening elsewhere, often aroused by social media posts.

Hypothesis testing Validating assumptions to make informed decisions about potential solutions.

Ideal customer profile (ICP) Detailed description of the persona that will most benefit from your product.

Initial public offering (IPO) A private company selling shares of its stock to the public for the first time. Also known as “going public.”

Legal redlining A process of reviewing and editing legal documents, such as contracts, by making markings to indicate changes. The term comes from the practice of using a red pen to make annotations, but other colors or annotations can be used in digital documents.

Lifetime value (LTV) A metric that estimates how much revenue a customer will generate for a business over the course of their relationship. Also known as customer lifetime value (CLV or CLTV) or lifetime customer value (LCV).

Minimum viable product (MVP) The most basic solution a business can offer to begin to iterate with its target personas.

Net promoter score (NPS) A metric that measures customer loyalty and satisfaction. It’s calculated by asking customers how likely they are to recommend a company or product to a friend or colleague on a scale of 0 to 10.

Pivot A strategic decision to change a startup’s direction or focus in response to market conditions, experiments, or other external factors. It involves making significant adjustments to the business model, product offering, target market, or overall strategy.

Product-market fit (PMF) When customers are buying, using, and telling others about the company’s product in numbers large enough to sustain that product’s growth and profitability.

Product roadmap An outline of the vision, priorities, and progress of a product over the foreseeable future.

RACI model A managerial tool that helps define roles and responsibilities in a project or process.

Release Making an enhancement/modification of a product available to customers.

Restructuring A strategic company decision that can involve layoffs. A startup may restructure to become more efficient and cut costs or to change or eliminate functions and roles to make room for new hires.

Software as a service (SaaS) A type of software delivery and licensing in which software is accessed online via a subscription, rather than bought and installed on individual computers.

Stock option A form of equity compensation that allows someone to buy a specific number of shares at a preset price.

Strike price The price employees will pay to purchase a share of your startup’s stock when they exercise a stock option.

Target persona A fictional archetype(s) a business builds its solution for.

Total addressable market (TAM) The market segment that will potentially buy a product or service.

Upselling Persuading an existing customer to buy products/services over and above what they are currently purchasing.

User experience (UX) A user’s perception of utility, ease, and efficiency of a product.

Willingness to pay (WTP) The maximum amount a user is ready to pay for an offering.

Word of mouth (WOM) A marketing strategy that encourages consumers to share positive experiences with a product or service with others.

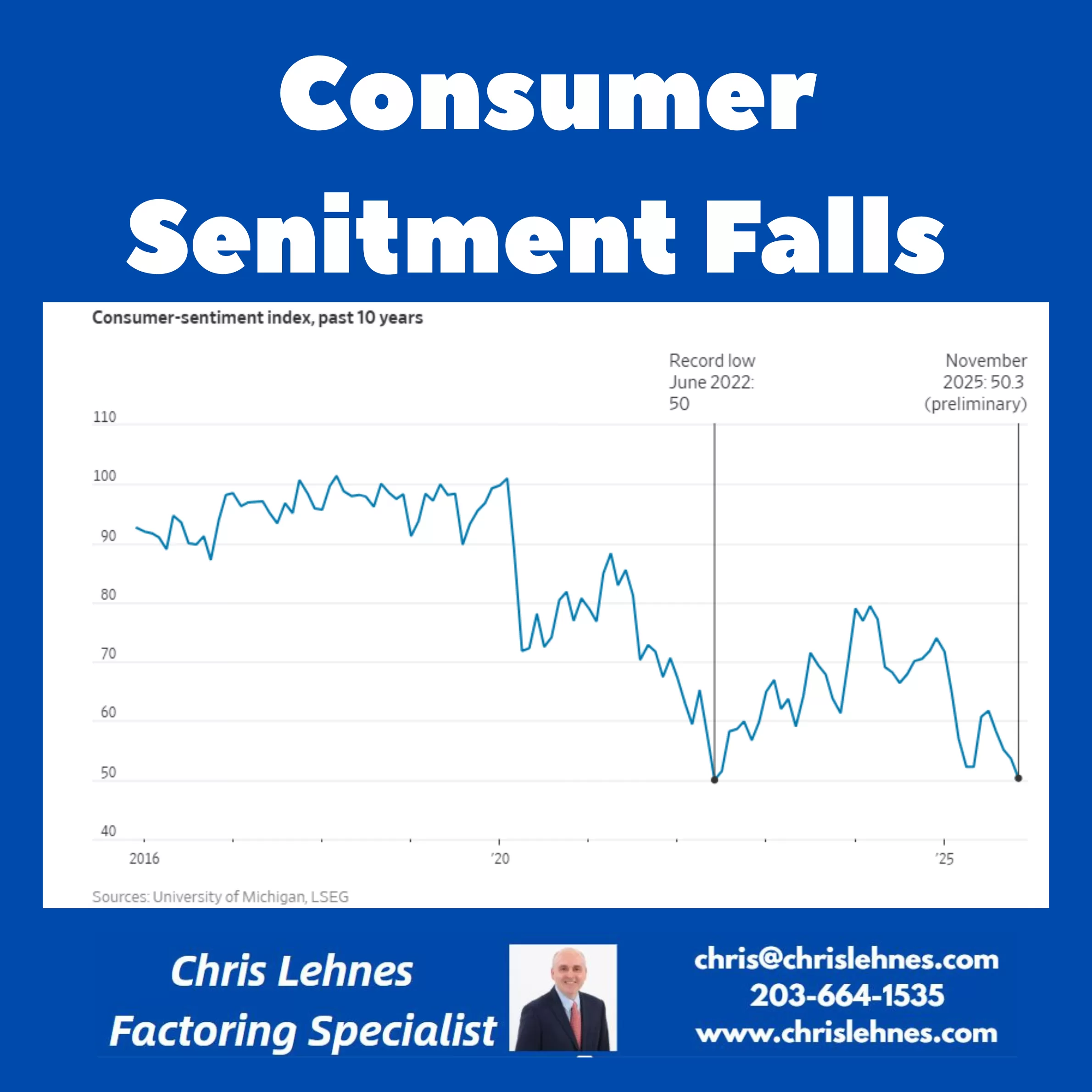

Consumer Sentiment worsened in November, new data showed, as persistent price increases and an extended government stoppage weigh on sentiment.

“With the federal government shutdown dragging on for over a month, consumers are now expressing worries about potential negative consequences for the economy,” said Joanne Hsu, the survey’s director at the University of Michigan.

The survey’s headline index fell to 50.3 in November, from 53.6 last month, based on preliminary responses.

Analysts polled by The Wall Street Journal were expecting a milder decline to 53.

The reading suggests consumer sentiment has dropped below the lows it hit in the spring, after President Trump first rolled out steep new global tariffs.

It is now just slightly above the record trough hit in 2022, amid a historic bout of inflation. Fuller end-of-month data could show a different result, however.

Bad news for the economy: American consumer sentiment took a sharp, unexpected dive in November, driven by lingering concerns over persistent price increases and the drawn-out government shutdown.

“With the federal government shutdown dragging on for over a month, consumers are now expressing worries about potential negative consequences for the economy,” said Joanne Hsu, director of the University of Michigan survey.

This drop wasn’t just a slight dip—it was a significant slide. The survey’s headline index plummeted to 50.3 in November from 53.6 the previous month (based on preliminary responses). This was a much steeper fall than financial analysts expected, who had polled by The Wall Street Journal were bracing for a milder 53.0 reading.

Why this is alarming: The new reading suggests consumer sentiment has now fallen below the spring lows recorded when President Trump first introduced steep new global tariffs. Critically, it is now sitting just above the record low hit in 2022 during the height of historic inflation.

The takeaway? Shoppers are feeling the pain, and uncertainty is at a critical level. While fuller end-of-month data could paint a slightly different picture, this preliminary data is a clear warning sign for economic growth.

Core Principles and Applications of Upstream Thinking

This book synthesizes the core principles of “upstream thinking,” a framework for preventing problems rather than reacting to them. The central thesis is that society is disproportionately focused on downstream responses—addressing crises, emergencies, and failures after they occur. An upstream approach, conversely, involves proactively identifying and dismantling the systems that cause these problems in the first place. This shift is impeded by three primary barriers: Problem Blindness, the failure to see a problem or the belief that it is inevitable; Lack of Ownership, a mindset where those capable of fixing a problem believe it is not their responsibility; and Tunneling, a state of scarcity (of time, money, or bandwidth) that forces short-term, reactive thinking and precludes long-term planning. Successful upstream interventions require leaders to unite diverse teams, identify high-leverage points within complex systems, establish early warning signals, and secure funding for outcomes that are often invisible—the absence of problems. The analysis reveals that effective upstream work is not about finding a single “magic pill” solution but about creating data-rich “scoreboards” that enable continuous learning and systems-level change.

——————————————————————————–

1. The Upstream Philosophy: Prevention Over Reaction

The core concept of upstream thinking is captured in a public health parable: two friends rescuing an endless stream of drowning children from a river, until one goes upstream “to tackle the guy who’s throwing all these kids in the water.” This metaphor distinguishes between downstream actions, which react to problems, and upstream efforts, which aim to prevent them.

Defining Upstream vs. Downstream Action

Downstream Action: Reactive, tangible, and focused on restoration. Examples include a call center representative resolving a customer complaint, a doctor performing bypass surgery, or a police officer making an arrest after a crime. These actions are often demanded by circumstance.

Upstream Action: Proactive, preventative, and focused on systems change. It involves “systems thinking” to systematically reduce the harm caused by problems. Examples include redesigning a website so customers don’t need to call for help, promoting policies that support healthy lifestyles to prevent heart disease, or creating community opportunities that deter crime. These efforts are chosen, not demanded.

The further one moves upstream, the more complex, ambiguous, and slower the solutions become, but the potential for massive and long-lasting good increases significantly. An intervention can exist at many points along a spectrum; for example, swim lessons are further upstream than life preservers in preventing drowning.

The Case of Expedia: A Model for Upstream Intervention

The travel website Expedia provides a clear illustration of a successful upstream intervention.

The Downstream Problem: In 2012, 58 out of every 100 Expedia customers placed a support call after booking. The top reason, accounting for 20 million calls annually at a cost of roughly $100 million, was to request a copy of their itinerary.

The Downstream Mindset: The call center was managed for efficiency—minimizing call time—rather than questioning why the calls were necessary.

The Upstream Shift: A “war room” was created with a mandate to “Save customers from needing to call us.” They analyzed the root causes of the calls.

Upstream Solutions: For the itinerary issue, they implemented simple fixes: adding an automated voice-response option, changing email protocols to avoid spam filters, and creating an online self-service tool.

The Result: The 20 million itinerary-related calls were virtually eliminated. The overall percentage of customers needing to call for support dropped from 58% to approximately 15%. This success was achieved by integrating the work of different teams (product, tech, support) to solve a problem that no single group “owned.”

The Asymmetry of Attention: Why Society Favors Reaction

Despite the clear benefits of prevention, societal efforts are overwhelmingly skewed toward reaction.

Tangibility and Measurement: Downstream work is more tangible and easier to measure. A police officer who writes a stack of tickets has a visible output, while an officer whose presence on a dangerous corner prevents accidents has invisible victims and victories written only in declining data.

Funding and Resources: We spend billions to recover from disasters like hurricanes and earthquakes, while disaster preparedness is “perpetually starved for resources.” The U.S. healthcare system, a $3.5 trillion industry, is designed almost exclusively for reaction, functioning like a giant “Undo button” for ailments rather than a system for creating health.

Heroism: Society celebrates the rescue, the recovery, and the response. Upstream work creates a quieter breed of hero, one “actively fighting for a world in which rescues are no longer required.”

Case Study: Healthcare Spending in the U.S. vs. Norway

The contrast between U.S. and Norwegian healthcare spending illustrates the consequences of a downstream focus. While both nations spend a similar percentage of GDP on total health (combining formal healthcare with “social care” like housing, food, and childcare), their allocation is radically different.

Spending Metric

United States

Norway

Spending Ratio (Upstream:Downstream)

For every 1** spent downstream, the U.S. spends roughly **1 upstream.

For every 1** spent downstream, Norway spends roughly **2.50 upstream.

Focus

World leader in downstream, high-tech treatments (e.g., knee replacements, cancer treatment).

Focus on upstream support systems (e.g., free prenatal/delivery care, 49 weeks of paid parental leave, guaranteed high-quality daycare, free college).

Health Outcomes

34th in infant mortality, 29th in life expectancy, 21st in stress levels.

5th in infant mortality, 5th in life expectancy, 1st in stress levels.

The data suggests the U.S. is not necessarily spending “too much” on health, but that its allocation is radically different from its peers, prioritizing expensive cures over cost-effective prevention.

2. The Three Barriers to Upstream Thinking

Despite the logic of prevention, several powerful forces consistently push individuals and organizations downstream.

A. Problem Blindness: The Invisibility of Solvable Problems

Problem blindness is the belief that negative outcomes are natural, inevitable, or out of one’s control. It is treating a solvable problem like the weather.

Mechanism: It arises from inattentional blindness (intense focus on one task causing one to miss other information, like radiologists missing a gorilla in a CT scan) and habituation (growing accustomed to consistent stimuli until they become normal).

Example: Chicago Public Schools (CPS): In 1998, the 52.4% graduation rate was seen by many as an intractable problem caused by poverty and other societal ills—”that’s just how it is.” The problem was accepted as a regrettable but inevitable condition.

Example: Sexual Harassment: Before the term was coined in 1975 by Lin Farley, the behavior was so normalized that women were often encouraged to tolerate it. Giving the problem a name—”sexual harassment”—was an act of “problematizing the normal,” helping society awaken from problem blindness.

Example: C-Sections in Brazil: An 84% C-section rate in Brazil’s private health system was seen as normal by many doctors, driven by convenience and financial incentives. An activist movement led by mothers who felt pressured into the procedure successfully challenged this norm, reframing it as a public health problem.

B. Lack of Ownership: “Not My Problem to Fix”

This barrier exists when the people or groups best positioned to solve a problem declare, “That’s not mine to fix.” This can result from fragmented responsibilities, self-interest, or a perceived lack of legitimacy.

Fragmented Responsibility: At Expedia, no single team was measured on reducing customer calls, so no one “owned” the problem.

Lack of Psychological Standing: People may feel they lack the legitimacy to act on a problem that doesn’t affect them personally. Research shows that explicitly extending standing (e.g., naming a group “Men and Women Opposed to Proposition 174”) can dramatically increase participation from those without a direct vested interest.

Taking Ownership: Dr. Bob Sanders & Car Seats: Spurred by a 1975 article in Pediatrics that extended psychological standing to pediatricians on auto safety, Dr. Sanders took ownership of the issue. He successfully lobbied for Tennessee to become the first state to mandate child car seats in 1978. This micro-level action catalyzed a macro-level change, with all 50 states passing similar laws by 1985, saving an estimated 11,274 young lives by 2016.

Taking Ownership: Ray Anderson & Interface: The founder of carpet-tile firm Interface took ownership of his company’s environmental impact after reading Paul Hawken’s The Ecology of Commerce. He launched “Mission Zero,” a quest to eliminate the company’s negative environmental footprint by 2020. This was an optional, self-imposed burden that transformed the company’s culture and processes.

C. Tunneling: The Tyranny of Short-Term Crises

When experiencing scarcity of time, money, or mental bandwidth, people adopt “tunnel vision.” They stop long-term planning and focus solely on managing the immediate crisis, which prevents upstream thinking.

The Scarcity Trap: The experience of poverty reduces cognitive capacity more than a full night without sleep. It forces short-sighted decisions (like taking a payday loan) not because people are undisciplined, but because the tunnel of scarcity leaves no room for long-term considerations.

Organizational Tunneling: A study of nurses found they were constantly engaged in creative workarounds for recurring problems (e.g., missing equipment, lack of towels) but never engaged in fixing the underlying processes. Their scarce time and attention kept them in a reactive mode.

Escaping the Tunnel: Escaping requires creating slack—a reserve of time or resources dedicated to problem-solving. This can be structured, as with the “safety huddles” in hospitals or the “Freshman Success Teams” at CPS, which provide a guaranteed forum for emerging from the tunnel to address systems-level issues.

Co-opting the Tunnel: The Ozone Layer: To address the long-term threat of ozone depletion, advocates had to make an upstream problem feel downstream. They co-opted the power of tunneling by creating urgency through public advocacy, the memorable metaphor of an “ozone hole,” and negotiating international agreements like the Montreal Protocol that removed threats for opponents (like DuPont), thus reducing their need to fight the solution.

3. Key Strategies for Upstream Leaders

Successfully navigating the barriers requires addressing a series of fundamental questions.

A. How Will You Unite the Right People?

Upstream work is fundamentally collaborative, requiring leaders to “surround the problem” with all the necessary stakeholders.

Key Insight: Give every stakeholder a role. Progress hinges on voluntary effort, so maintaining a “big tent” is crucial.

Case Study: Iceland’s War on Teen Substance Abuse: In the 1990s, 42% of Icelandic teens reported being drunk in the past month. A coalition of researchers, policymakers, schools, parents, and community groups united to change the culture around teens.

Strategy: They focused on boosting “protective factors” (e.g., participation in formal sports, time spent with parents, “natural highs”) and reducing “risk factors” (unstructured, unsupervised time).

Tactics: They reinforced curfews, gave families “gift cards” for recreational activities, and professionalized coaching in sports clubs.

Result: Over 20 years, the percentage of teens getting drunk in the past 30 days fell from 42% to 5%. Daily smoking dropped from 23% to 3%.

Case Study: Domestic Violence in Newburyport, MA: After a woman was murdered by her estranged husband, the Jeanne Geiger Crisis Center united police, advocates, parole officers, and prosecutors to form a Domestic Violence High Risk Team.

Data-Driven Collaboration: The team meets monthly to review cases of women identified by the “Danger Assessment” tool as being at extreme risk of homicide. They use a by-name list to coordinate actions like police drive-bys and creating emergency plans.

Result: In the 14 years since the team’s formation, not one woman in the communities they serve has been killed in a domestic violence–related homicide, compared to 8 in the 10 years prior.

The Role of Data: In many successful upstream efforts, data is not used for top-down “inspection” but for frontline “learning.” Real-time, granular data (like a by-name list) becomes the centerpiece that unites diverse teams around a concrete and shared goal: “What are we going to do about Michael next week?”

B. How Will You Change the System?

Lasting upstream work must culminate in systems change, altering the “water” we swim in so that better outcomes happen by default.

Systems Determine Probabilities: A well-designed system makes success highly probable (e.g., fluoridated water preventing cavities). A flawed system rigs the game against certain people. As Dr. Anthony Iton discovered, disparities in life expectancy of up to 20 years between nearby ZIP codes are not caused by a few factors, but by entire systems (housing, education, crime, food access) that create “incubators of chronic stress.”

The California Endowment’s BHC Initiative: This $1 billion, 10-year program aims to fix these broken systems not by directly providing health services, but by empowering residents of 14 challenged communities to gain political power and win policy victories that reshape their environments.

The Danger of Enabling Bad Systems: Some well-intentioned downstream efforts can inadvertently prop up the flawed systems that create need. For example, while DonorsChoose provides vital classroom supplies, its success could excuse school districts from their funding obligations. The goal should be to push for a world where such crutches are no longer needed.

C. Where Can You Find a Point of Leverage?

In complex systems, the challenge is finding the right lever. This requires getting “proximate” to the problem.

Case Study: The UChicago Crime Lab & “Becoming a Man” (BAM): To understand youth violence, researchers read 200 consecutive homicide reports. They discovered that many deaths resulted not from strategic gang wars but from impulsive reactions to trivial disputes. This pointed to impulsivity as a leverage point.

The Intervention: They funded and studied “Becoming a Man” (BAM), a program that used small-group sessions and cognitive behavioral therapy (CBT) to help at-risk young men learn to manage anger and slow down their thinking in fraught situations.

The Result: A randomized controlled trial found that BAM participants had 45% fewer violent-crime arrests.

The Power of Proximity: Architects designing for the elderly donned an “age simulation suit” to experience navigation challenges firsthand. This direct experience revealed leverage points like the need for more benches, handrails, and three-step escalators.

D. How Will You Get Early Warning of the Problem?

Early warning signals provide the time and maneuvering room to prevent a problem or blunt its impact.

Predictive Analytics:

LinkedIn: Discovered that a customer’s product usage in the first 30 days could predict their likelihood of churning a year later. They shifted resources to intensive onboarding to ensure early engagement.

Northwell Health EMS: Uses historical data on 911 calls to predict where emergencies will occur (e.g., near nursing homes at mealtimes) and forward-deploys ambulances to reduce response times.

Human Sensors:

Sandy Hook Promise: After the 2012 school shooting, the organization realized that in most mass shootings, the perpetrator tells someone their plans in advance. They created the “Know the Signs” program to train students to spot warning signs and the “Say Something” anonymous tip line to report them. This system has averted multiple credible school shooting threats and led to hundreds of suicide interventions.

The Danger of False Positives: Early warning systems can backfire. An “epidemic” of thyroid cancer in South Korea was revealed to be an epidemic of overdiagnosis. Mass screening found huge numbers of slow-growing, nonlethal cancers (“turtles”), leading to unnecessary and harmful treatments for a problem that didn’t exist.

E. How Will You Measure Success and Avoid “Ghost Victories”?

Success in upstream work is often the absence of a negative event, making it hard to measure. This reliance on proxy measures can lead to “ghost victories”—superficial successes that cloak underlying failure.

Mistaking Macro Trends for Success: In the 1990s, police chiefs across the U.S. claimed credit for falling crime rates, when in fact they were mostly benefiting from a nationwide trend.

Misalignment of Measures and Mission: The City of Boston’s Public Works department measured its sidewalk repair success by spending per zone and 311 cases closed. This led them to fix sidewalks in wealthy neighborhoods (whose residents called 311) while neglecting crumbling sidewalks in poor neighborhoods, undermining their mission of equity and walkability.

Measures Becoming the Mission: This is the most destructive form, where people “game” the metrics. The NYPD’s CompStat system, which held precinct leaders accountable for crime statistics, led to the widespread downgrading of crimes. In a chilling example, a reported rape of a prostitute was nearly reclassified as a “theft of service” to keep the numbers down.

To avoid ghost victories, leaders should use paired measures (balancing quantity with quality, as CPS did with graduation rates and ACT scores) and “pre-game” how measures could be misused.

F. How Will You Avoid Doing Harm?

Upstream interventions tinker with complex systems and can create unintended negative consequences, known as the “cobra effect.”

Case Study: Macquarie Island: A decades-long effort to eradicate invasive species on a subantarctic island created a cascade of problems. Killing rabbits (to stop erosion) led cats to eat rare birds. Killing the cats led to a rabbit population explosion. Killing all pests led to invasive weeds running rampant.

Anticipating Second-Order Effects: Wise interventions require seeing the whole system. The “cobra effect” is when an attempted solution makes the problem worse. Examples include an open-office plan meant to increase face-to-face collaboration actually causing it to plunge by 70%, or a ban on thin plastic bags leading retailers to offer thicker plastic bags.

The Need for Feedback Loops: Because not all consequences can be foreseen, upstream work requires experimentation and fast, reliable feedback loops. A business that creates a feedback loop for its staff meetings (rating each meeting on a 1-5 scale) can continuously improve them, whereas most meetings never get better because there is no mechanism for learning.

G. Who Will Pay for What Does Not Happen?

Funding prevention is notoriously difficult because success is invisible and payment models are designed for reaction.

The “Wrong Pocket Problem”: This occurs when the entity that pays for an intervention is not the one that reaps the financial benefits.

Case Study: The Nurse-Family Partnership (NFP): This program, which provides nurse home visits to first-time, low-income mothers, has been proven by multiple RCTs to produce significant long-term social benefits (e.g., reduced child abuse, preterm births, crime, and welfare payments), yielding a return of over $6 for every $1 invested. However, it struggles to get funding because the benefits are scattered across many “pockets” (Medicaid, criminal justice, social services), while a single entity is asked to bear the upfront cost.

Innovative Funding Models:

Pay for Success: A model being used in South Carolina to fund NFP, where private investors and foundations provide upfront capital. If the program meets pre-agreed success metrics, the government repays the investors. This shifts the financial risk away from the government.

Accountable Care Organizations (ACOs): A model where Medicare shares savings with groups of doctors who succeed in keeping their patients healthier and out of the hospital, creating a direct financial incentive for prevention.

4. Addressing Distant and Improbable Threats (“Far Upstream”)

Upstream thinking can also be applied to one-off, improbable, or unpreventable threats.

The Prophet’s Dilemma: This is a prediction that prevents what it predicts from happening. The massive global effort to fix the Y2K bug is a prime example. When disaster didn’t strike, many claimed it was a hoax, but it is likely the frantic preparations were what prevented the catastrophe.

The Power of Rehearsal: The “Hurricane Pam” simulation, conducted 13 months before Hurricane Katrina, convened 300 stakeholders to game-plan a response to a catastrophic New Orleans hurricane. While the eventual Katrina response was a national failure in many respects, the planning from Pam led to a drastically improved “contraflow” evacuation plan, which is credited with reducing the death toll from a projected 60,000 to approximately 1,700. The lesson is that preparing for disaster requires practice, but organizations in a state of “tunneling” often fail to invest in it.

Existential Risk & The “Black Ball” Hypothesis: Philosopher Nick Bostrom posits that technological invention is like pulling balls from an urn. So far we have pulled white (beneficial) and gray (mixed-blessing) balls. But what if there is a black ball—a technology that is easily accessible and allows a small group to cause mass destruction, thereby destroying civilization? The response to the remote threat of “Moon germs” in the 1960s, which led to the creation of NASA’s Planetary Protection Officer and strict quarantine protocols, provides an early model for how humanity can collectively address improbable but high-stakes risks.

5. Conclusion: You, Upstream

The principles of upstream thinking can be applied by individuals to solve personal and organizational problems.

Personal Application: Identify recurring problems in life—from finding parking to marital friction—and devise systems to prevent them. The creation of “Daddy Dolls” by a military spouse to ease her children’s pain during deployment is a powerful example of an individual creating an upstream solution.

Engaging in Societal Problems: When seeking to contribute to larger issues, one should:

Be impatient for action but patient for outcomes: Upstream work is a long game of chipping away at a problem.

Recognize that macro starts with micro: You cannot help a thousand people until you understand how to help one. Deep, proximate understanding is key.

Favor “Scoreboards” over “Pills”: Prioritize initiatives that use real-time data for continuous learning and adaptation (a scoreboard) over those that seek a single, perfect, scalable solution that cannot be changed (a pill).

The Power of One Person: A single, retiring actuary at the Centers for Medicare & Medicaid Services wrote a “cry of the heart” letter to his boss, successfully arguing that the agency should not count “longer lives” as a cost when evaluating preventive programs. This quiet act of defiance changed a federal rule, unlocking funding for life-saving programs and demonstrating that even within vast bureaucracies, one person can achieve a profound upstream victory.

Upstream Thinking Study Guide

Quiz: Short-Answer Questions

Instructions: Answer the following questions in two to three sentences, drawing exclusively from the information provided in the source context.

Describe the public health parable that opens the text. What is the core lesson it is meant to illustrate?

Explain the problem Ryan O’Neill discovered at Expedia in 2012. What was the upstream solution the company implemented?

What is “problem blindness”? How did this barrier manifest within the Chicago Public Schools (CPS) system regarding its low graduation rate?

Define the barrier of “lack of ownership” and the related concept of “psychological standing.” How did the advocates for child car seat laws in the 1970s overcome this barrier?

What is “tunneling”? How does this phenomenon, as described by Eldar Shafir and Sendhil Mullainathan, act as a barrier to upstream thinking?

Summarize the core philosophy of the “Drug-free Iceland” campaign. What were the “risk factors” and “protective factors” it aimed to influence?

What is a “ghost victory”? Using the example of Boston’s sidewalk repairs, explain how an organization can succeed on its metrics while failing its mission.

How did the University of Chicago Crime Lab identify “impulsivity” as a key leverage point for reducing youth violence? Describe the “Becoming a Man” (BAM) program that addressed this.

Explain the “cobra effect,” using the example of the British administrator’s attempt to reduce the cobra population in Delhi.

What is the “wrong pocket problem”? How does the case of the Nurse-Family Partnership (NFP) illustrate this challenge in funding preventive programs?

Essay Questions

Instructions: The following questions are designed to provoke deeper thought and synthesis of the concepts presented in the text. Formulate a detailed response for each, citing specific examples and arguments from the source material.

The text identifies three primary barriers to upstream thinking: Problem Blindness, Lack of Ownership, and Tunneling. Analyze how these three barriers were present in the Expedia case study and how the company’s leaders ultimately overcame them to implement a successful upstream intervention.

Discuss the role of data in enabling upstream work, contrasting “data for the purpose of learning” with “data for the purpose of inspection.” Use the examples of the Chicago Public Schools’ Freshman On-Track metric, the Newburyport Domestic Violence High Risk Team’s Danger Assessment, and the Rockford homelessness team’s “by-name list” to illustrate your points.

Compare and contrast the challenges of upstream interventions in the public sector versus the private sector, using the stories of Ray Anderson at Interface and Dr. Bob Sanders’s campaign for child car seats in Tennessee. What unique advantages and disadvantages did each leader face in trying to solve a problem they chose to own?

Upstream interventions often create unintended consequences. Using the case studies of the Macquarie Island pest eradication program and the attempts to ban single-use plastic bags, discuss the importance of systems thinking, experimentation, and feedback loops in avoiding harm.

The author argues that our society’s attention is “grossly asymmetrical” and skewed toward downstream reaction rather than upstream prevention. Using the detailed comparison between the United States and Norwegian healthcare systems, analyze the author’s argument. What are the demonstrated benefits and disadvantages of each country’s approach to “buying health”?

Quiz Answer Key

The parable describes two friends rescuing drowning children from a river. While one continues the downstream work of pulling kids from the water, the other goes upstream to “tackle the guy who’s throwing all these kids in the water.” The lesson illustrates the difference between reacting to problems (downstream) and preventing them at their source (upstream).

Ryan O’Neill found that for every 100 Expedia customers, 58 placed a call for help, with the number one reason being a request for their itinerary. The upstream solution was to prevent these calls by adding an automated voice-response option, improving email delivery to avoid spam filters, and creating an online tool for customers to retrieve their own itineraries.

“Problem blindness” is the belief that negative outcomes are natural, inevitable, or out of one’s control. Within CPS, many staff members had come to accept the 50% dropout rate as “just how it is,” believing it was caused by intractable root causes like poverty or lack of student effort, which reinforced a sense of helplessness.

“Lack of ownership” means that the parties capable of addressing a problem believe “that’s not mine to fix.” “Psychological standing” is the sense of legitimacy one feels in protesting or acting on an issue. Annemarie Shelness and Seymour Charles overcame this by publishing an article in Pediatrics, extending psychological standing to pediatricians and framing auto safety as a form of preventive medicine for them to own.

“Tunneling” is a state of mind caused by scarcity of time, money, or bandwidth, where people adopt a narrow, short-term focus on immediate problems. It is a barrier to upstream thinking because it confines people to reactive problem-solving and prevents them from engaging in the long-term planning and systems thinking required to prevent future problems.

The core philosophy was to change the community and cultural environment surrounding teenagers to make substance use feel abnormal. The campaign worked to reduce risk factors, such as unstructured time and friends who drink, while boosting protective factors, like participation in formal sports and spending more time with parents.

A “ghost victory” is a superficial success that cloaks an underlying failure, often occurring when short-term measures do not align with the long-term mission. Boston’s Public Works department succeeded on its measures of closing 311 cases and spending its budget, but this system disproportionately repaired sidewalks in wealthy neighborhoods, failing the ultimate mission of equity and walkability for all citizens.

By studying 200 homicide reports, the Crime Lab found that many deaths resulted not from strategic gang activity but from impulsive reactions to trivial disputes, like arguments over a bike or a basketball game. The “Becoming a Man” (BAM) program used cognitive behavioral therapy (CBT) and group mentoring to teach young men to slow down their thinking and manage anger in fraught situations.

The “cobra effect” occurs when an attempted solution makes the problem worse. In colonial Delhi, a British administrator offered a bounty for dead cobras to reduce their population. In response, citizens began farming cobras to collect the bounty, and when the program was canceled, they released their now-worthless snakes, resulting in more cobras than before.

The “wrong pocket problem” occurs when the entity that pays for a preventive intervention does not receive the primary financial benefit from its success. The Nurse-Family Partnership has been proven to save society money by reducing crime, preterm births, and welfare payments, but it struggles to get funding because these savings are scattered across many different government “pockets” (criminal justice, Medicaid, etc.), none of which want to bear the full upfront cost.

Glossary of Key Terms

Term

Definition

Accountable Care Organization (ACO)

A model where a group of primary care doctors are incentivized by Medicare to keep their patient population healthy and out of the hospital, sharing in the savings generated from prevented hospital visits.

Backward Contamination

The contamination of Earth by a returning spaceship, potentially carrying destructive alien life.

Becoming a Man (BAM)

A program for at-risk youth in Chicago that uses group mentoring and cognitive behavioral therapy (CBT) to help young men learn to manage anger and impulsivity.

By-Name List

A real-time, regularly updated census of a specific population (e.g., all homeless veterans in a city), used by collaborative teams to coordinate services and track progress on an individual basis.

Capitation

A healthcare payment model where providers are paid a flat, risk-adjusted fee per person to take care of all their health needs, incentivizing prevention and cost-effectiveness.

Cobra Effect

An unintended consequence where an attempted solution to a problem makes the problem worse.

Coordinated Entry

A system where a single point of entry is established for people seeking a service (like housing for the homeless), allowing for thoughtful prioritization based on vulnerability rather than a “first-come, first-served” basis.

Data for the Purpose of Learning

A model where real-time data is provided to frontline workers (e.g., teachers, nurses) to help them learn, adapt, and improve their own work, as opposed to “data for the purpose of inspection.”

Data for the Purpose of Inspection

A model where data is used by superiors to hold subordinates accountable for hitting targets, which can create pressure to “game” the metrics.

Downstream Actions

Efforts that react to problems once they have already occurred, such as rescuing a drowning child, answering a customer complaint, or performing emergency surgery.

Forward Contamination

The contamination of another planet with organisms from Earth during space exploration.

Freshman On-Track (FOT)

A metric developed for Chicago Public Schools that predicts a student’s likelihood of graduation based on two factors: completing five full-year course credits and not failing more than one semester of a core course during freshman year.

Functional Zero

A state achieved when the number of people experiencing a problem (e.g., homelessness) is lower than the system’s proven monthly capacity to solve that problem for new cases.

Ghost Victory

A superficial success that cloaks an underlying failure. This can happen when short-term measures are misaligned with the long-term mission, when success is mistakenly attributed to one’s own efforts, or when the measures themselves become the mission in a way that undermines the work.

Housing First

A strategy for addressing homelessness that prioritizes getting people into housing as the first step, providing a stable foundation from which they can then address other issues like substance abuse or unemployment.

Inattentional Blindness

A phenomenon where careful attention to one task leads people to miss important information that is unrelated to that task, such as radiologists missing a gorilla in a CT scan.

Lack of Ownership

A barrier to upstream thinking where the parties who are capable of addressing a problem declare, “That’s not mine to fix.”

Paired Measures

A management principle of balancing a quantity-based metric with a quality-based metric to avoid a situation where improving one undermines the other (e.g., pairing “square feet cleaned” with “quality spot-checks”).

Problem Blindness

A barrier to upstream thinking characterized by the belief that negative outcomes are natural, inevitable, or out of one’s control.

Psychological Standing

The sense of legitimacy people feel they have to protest or take action on a problem, which is often tied to whether they feel personally affected by the issue.

Social Care

A term for upstream spending on health, covering areas that keep people healthy such as housing, pensions, and childcare support.

Tunneling

A third barrier to upstream thinking, caused by scarcity (of time, money, or bandwidth), where people adopt tunnel vision and focus only on short-term, reactive problem-solving, abandoning long-term planning.

Upstream Efforts

Efforts intended to prevent problems before they happen or, alternatively, to systematically reduce the harm caused by those problems. Upstream work is characterized by systems thinking.

Wrong Pocket Problem

A situation that hinders funding for prevention, where the entity that bears the cost of an intervention does not receive the primary financial benefit, which is instead scattered across many other “pockets.”

Contact me to learn if your client qualifies for a quick AR advance.

Accounts Receivable Factoring $100,000 to $30 Million Quick AR Advances No Long-Term Commitment Non-recourse Funding in about a week

We are a great match for businesses with traits such as: Less than 2 years old Negative Net Worth Losses Customer Concentrations Weak Credit Character Issues

Federal Reserve Monetary Policy and Leadership Outlook

Executive Summary