What a Small Business Should Look for in a Web Hosting Service

In today’s digital-first world, a strong online presence is no longer optional—it’s essential for small business success. At the heart of any digital strategy is the web hosting service that powers your website. A reliable web host ensures your site is fast, secure, and always available to customers. But with countless providers and hosting plans available, choosing the right one can feel overwhelming.

For small businesses, the stakes are high. The wrong hosting choice can lead to poor website performance, security vulnerabilities, lost sales, and even damage to your brand. That’s why understanding what to look for in a web hosting service is critical.

This guide explores the most important factors small business owners should consider when selecting a web hosting provider—from uptime and scalability to support and security. Whether you’re launching your first website or thinking of switching hosts, this comprehensive breakdown will help you make an informed, future-proof decision.

Chapter 1: Understanding Web Hosting and Why It Matters

What Is Web Hosting?

Web hosting is a service that stores your website’s files and makes them accessible on the internet. When users type your domain name into a browser, the hosting service delivers the content to their screen. It’s the foundation that supports your online storefront.

Types of Web Hosting

Small business owners should start by understanding the different types of hosting:

Shared Hosting

Affordable and beginner-friendly

Resources are shared with other websites

Suitable for low-traffic websites

VPS (Virtual Private Server) Hosting

Offers dedicated resources on a shared server

More scalable than shared hosting

Ideal for growing businesses

Dedicated Hosting

You rent an entire server

High performance and control

Best for high-traffic sites with custom needs

Cloud Hosting

Uses multiple servers for flexibility and scalability

Pay-as-you-go pricing model

Reliable and resilient to traffic surges

Managed Hosting

The host manages server maintenance, security, and updates

Great for non-technical business owners

Chapter 2: Performance – Speed and Uptime Matter

Website Speed

Website speed impacts both user experience and search engine rankings. According to Google, if a page takes longer than 3 seconds to load, over 50% of users will abandon it.

Look for hosts that offer:

SSD (Solid State Drives)

CDN (Content Delivery Network) integration

Built-in caching mechanisms

Optimized server configurations

Uptime Guarantees

Uptime is the percentage of time your website is online and accessible. Look for providers that offer at least a 99.9% uptime guarantee. Even 0.1% downtime translates into hours of lost availability each year.

What to look for:

Uptime SLAs (Service Level Agreements)

Real-time monitoring

Reputation for reliability

Chapter 3: Security Features for Peace of Mind

Cybersecurity Threats

Small businesses are frequent targets of cyberattacks due to often weaker defenses. A secure host acts as the first line of defense.

Key features to look for:

SSL Certificates: Encrypts data transmission between user and server

Firewalls and DDoS Protection: Blocks unauthorized traffic and attacks

Automatic Backups: Ensures recoverability in case of data loss

Malware Scanning and Removal: Keeps your website clean and functional

If you handle sensitive data (like payments or personal info), you may need to comply with regulations like GDPR or PCI-DSS. Choose a host that helps you stay compliant.

Chapter 4: Customer Support – Help When You Need It

24/7 Availability

Issues can happen at any hour. You need a host with 24/7 customer support—especially if your audience spans multiple time zones.

Support Channels

The best providers offer multiple channels:

Live Chat

Email/Ticketing

Phone Support

Knowledge Base or Help Center

Responsiveness and Expertise

Test support before you commit. Send a few pre-sale questions to evaluate their speed, professionalism, and helpfulness.

Chapter 5: Scalability and Flexibility

Planning for Growth

Your current hosting needs may be small, but they will grow. You need a provider that can grow with you.

Look for:

Easy upgrades from shared to VPS or cloud hosting

Flexible pricing plans

Scalable bandwidth and storage

Support for Custom Tools

If you use CMSs (like WordPress), CRM software, or eCommerce platforms, make sure your host supports them without conflicts.

Chapter 6: Control Panels and Ease of Use

User-Friendly Interfaces

Not every small business has an IT team. You need a hosting platform that’s easy to manage.

Popular control panels:

cPanel: Common and feature-rich

Plesk: Good for Windows hosting

Custom Dashboards: Offered by hosts like WP Engine or Squarespace

Key Features to Check

One-click app installs

File manager

Domain and email management

Access to logs and databases

Chapter 7: Pricing and Value

Understanding Hosting Costs

Pricing varies widely depending on hosting type, features, and billing cycles. But cheapest isn’t always best.

Common pricing structures:

Introductory Offers: Low first-year rates, followed by steep renewals

Monthly vs. Annual Plans: Annual is cheaper long-term

Add-on Costs: Domain registration, email, SSL, backups, etc.

Value Over Price

Evaluate what’s included in the plan:

Free domain?

SSL certificate?

Backups and malware scanning?

Email accounts?

Chapter 8: Domain and Email Services

Integrated Domain Management

Having your domain and hosting in one place simplifies setup and billing. But be cautious—some providers overcharge for renewals.

Business Email Hosting

Branded emails (yourname@yourbusiness.com) are a must for professionalism. Check if the host offers:

Free email accounts

Webmail access

Spam filtering

Integration with Gmail or Outlook

Chapter 9: Reviews, Reputation, and Case Studies

Reading the Right Reviews

Not all reviews are honest. Look for:

Verified customer reviews on third-party platforms (e.g., Trustpilot)

Forums like Reddit or WebHostingTalk

Business use cases or case studies

Red Flags to Watch For

Frequent complaints about downtime

Poor customer support

Sudden price hikes

Security issues or past data breaches

Chapter 10: Specialized Hosting for eCommerce and CMS

eCommerce-Ready Hosting

If you run an online store, your hosting must be optimized for platforms like WooCommerce, Shopify, or Magento.

Look for:

PCI compliance

SSL and secure payment integrations

Fast database performance

CMS-Specific Hosting

Platforms like WordPress require certain configurations. Many hosts offer:

Managed WordPress Hosting

Auto-updates

Built-in caching and staging environments

Chapter 11: Backup and Disaster Recovery

Automated Backups

Manual backups are prone to failure. Ensure your host:

Runs daily or weekly automated backups

Allows one-click restores

Stores backups off-site or in the cloud

Disaster Recovery

Ask about recovery time in case of:

Hardware failure

Cyberattacks

Data corruption

Chapter 12: Environmental Impact and Green Hosting

Eco-Friendly Hosting Options

Environmentally-conscious businesses should consider:

Chapter 13: Legal Considerations and Terms of Service

Understand the Fine Print

Review:

Data ownership: Who owns your data?

Termination clauses

Refund policies

Usage limitations or “fair use” terms

Don’t lock yourself into long-term contracts without exit options.

Chapter 14: Making the Switch

How to Migrate Hosting

If you’re switching from another provider:

Does the host offer free migration assistance?

Will your email, DNS, and databases be preserved?

How long is the expected downtime?

Plan your switch during low-traffic periods and notify customers in advance.

Chapter 15: Top Hosting Providers for Small Businesses in 2025

Recommended Hosting Services

Here are several highly rated providers tailored to small business needs:

Provider

Best For

Features

Bluehost

WordPress & eCommerce

Free domain, SSL, 24/7 support

SiteGround

Reliability & Speed

Top-tier support, daily backups

Hostinger

Budget-Conscious

SSD storage, easy dashboard

WP Engine

Managed WordPress

Fast, secure, staging tools

A2 Hosting

Developers & Speed

Turbo servers, advanced tools

GreenGeeks

Eco-Friendly

300% green energy match

Conclusion

Choosing a web hosting service is one of the most important digital decisions a small business can make. A dependable host serves as the backbone of your online operations—affecting everything from website speed and SEO rankings to customer trust and sales conversion.

By prioritizing speed, security, scalability, support, and overall value, you’ll position your business for digital success. Don’t settle for the cheapest option—invest in a host that will grow with your business and protect your digital footprint.

Remember: the right web hosting service isn’t just a technical choice—it’s a strategic one.

A business owner’s personal credit score isn’t just a number — it’s a powerful financial tool that can affect access to loans, insurance premiums, leasing agreements, and even business partnerships. Whether you’re a startup founder trying to secure funding or an experienced entrepreneur looking to expand, your personal credit can influence the opportunities available to your business. While building business credit is crucial, your personal credit often plays a role in financial decisions — especially for small business owners whose credit profiles may be closely linked with their enterprise.

Improving your personal credit score takes discipline, strategy, and time. But the good news is, with a step-by-step approach, it’s achievable. This article outlines actionable steps business owners can take to boost their personal credit score and ensure it becomes an asset, not a liability.

1. Understanding Your Credit Score

A credit score is a three-digit number that reflects your creditworthiness based on your credit history. Most commonly, credit scores range from 300 to 850, with higher scores indicating better credit. The most widely used scoring models include FICO® Score and VantageScore, both of which evaluate similar criteria:

Payment history (35%)

Amounts owed / credit utilization (30%)

Length of credit history (15%)

Credit mix (10%)

New credit inquiries (10%)

Understanding what contributes to your score helps you focus on the areas where improvement is most needed.

2. Why Personal Credit Score Matters for Business Owners

Even if your business has its own credit profile, lenders and suppliers often review your personal credit to assess your financial responsibility, particularly if your business is new or lacks significant assets.

Here’s how a strong personal credit score can benefit your business:

Easier loan approvals with better terms

Lower interest rates on lines of credit

Reduced need for personal guarantees

Favorable terms with vendors and suppliers

More options for credit cards and banking services

Improving your personal credit can translate directly into enhanced business flexibility and resilience.

3. Step 1: Check Your Credit Score Reports for Accuracy

Start by requesting your free credit reports from the three major bureaus — Equifax, Experian, and TransUnion — through AnnualCreditReport.com. Carefully review each report for:

Incorrect personal information

Duplicate or fraudulent accounts

Incorrect balances

Outdated delinquencies

Payment records errors

Errors are common and can drag down your score unnecessarily. Reviewing your report is the first defense against misinformation.

4. Step 2: Dispute Errors on Your Credit Score

If you find inaccuracies, file a dispute with the credit bureau. Each bureau has an online portal for submitting disputes, or you can send letters via certified mail. Provide documentation that supports your claim, such as payment receipts or statements.

Once submitted, the bureau has 30 to 45 days to investigate and respond. Correcting even one major error (such as a wrongly reported late payment) can significantly raise your score.

5. Step 3: Make On-Time Payments a Priority to Improve Credit Score

Payment history is the most significant factor in your credit score. Even one late payment can hurt your credit for years.

Tips:

Set calendar reminders or autopay for bills

Prioritize at least the minimum payment

Keep a cushion in your checking account to avoid overdrafts

Paying on time consistently will build a solid reputation with creditors and steadily increase your score.

6. Step 4: Reduce Credit Utilization to Improve Credit Score

Credit utilization refers to the ratio of your current revolving credit balances to your total credit limit. Keeping your utilization below 30% is advisable, and below 10% is optimal.

Example: If you have $10,000 in available credit and carry a $3,000 balance, your utilization is 30%.

Strategies:

Pay off balances early in the billing cycle

Ask for higher credit limits (without increasing spending)

Pay multiple times a month if needed

Lower utilization shows you’re not reliant on credit to function — a sign of strong financial health.

7. Step 5: Avoid Opening Too Many New Accounts at Once can Hurt Credit Score

Each time you apply for credit, a hard inquiry appears on your report, which can temporarily lower your score. Multiple inquiries in a short period can raise red flags.

Tip: Space out credit applications and only apply when necessary. If you’re shopping for rates (e.g., mortgage or auto loans), do so within a 14-45 day window so it counts as one inquiry.

8. Step 6: Keep Old Accounts Open

The age of your credit accounts impacts your score. Closing old accounts can shorten your average credit age and reduce your total available credit, both of which hurt your score.

Unless an old account has an annual fee or causes you financial strain, keep it open.

9. Step 7: Diversify Your Credit Mix to Improve Credit Score

Lenders like to see that you can handle different types of credit — such as credit cards, auto loans, mortgages, and installment loans.

You don’t need to open new accounts just for the sake of variety, but having a mix (and managing it responsibly) can help improve your score over time.

10. Step 8: Pay Down Debt Strategically

Use one of these two proven methods:

Snowball Method

Pay off the smallest balance first, while making minimum payments on the rest.

Gain momentum and motivation.

Avalanche Method

Pay off the highest-interest debt first.

Save more on interest in the long run.

Whichever method you choose, the key is consistency and discipline.

11. Step 9: Monitor Your Credit Regularly

Use free credit monitoring tools (like Credit Karma or NerdWallet) or services from your bank to track changes in your score and detect unauthorized activity.

Staying informed allows you to take immediate action if your score drops or if new accounts appear unexpectedly.

12. Step 10: Leverage Business Credit to Separate Risk

One key strategy is to build and use business credit (EIN-based) for your company, so your personal credit isn’t overextended.

Actionable tips:

Apply for an EIN (Employer Identification Number)

Open business bank and credit card accounts

Use vendors that report to business credit bureaus (e.g., Dun & Bradstreet)

This reduces personal liability and protects your score when your business takes on risk.

13. Step 11: Use Personal Credit-Building Tools

There are products and services designed to help rebuild or strengthen credit:

Secured credit cards: Require a cash deposit and are easier to obtain.

Credit builder loans: Help establish credit history without risk.

Authorized user status: Ask a trusted friend or family member to add you to a long-standing account.

These tools can help you build a strong payment history and increase available credit.

14. Step 12: Limit Personal Guarantees Where Possible

Many small business owners use personal guarantees to secure business financing, but these can backfire if the business struggles.

Strategies:

Look for lenders that don’t require a personal guarantee

Negotiate limited guarantees (e.g., a capped amount)

Strengthen your business credit so you can eventually avoid personal tie-ins

Being selective helps you reduce the risk to your personal finances and credit score.

15. Step 13: Establish an Emergency Fund

Having an emergency fund reduces the likelihood that you’ll miss payments or max out credit cards in tough times. Experts recommend saving 3–6 months’ worth of personal expenses.

Automate savings where possible, even if you start small. A healthy cash reserve protects both your credit and peace of mind.

16. Step 14: Work with a Credit Counselor if Needed

If your credit issues are severe or you’re overwhelmed, a reputable nonprofit credit counselor can help. They can assist with:

Budgeting

Debt management plans

Negotiating with creditors

Look for agencies accredited by the NFCC (National Foundation for Credit Counseling) or FCAA (Financial Counseling Association of America).

17. Common Pitfalls to Avoid

Ignoring due dates: Late payments stay on your report for up to 7 years.

Closing credit cards prematurely: Reduces total available credit and credit age.

Applying for too much credit: Leads to multiple hard inquiries.

Using personal credit for business risks: Blurs boundaries and increases personal liability.

Over-reliance on one form of credit: Limits your score potential.

Avoiding these mistakes is just as important as adopting positive habits.

18. How Long Does It Take to See Results?

Immediate (1–2 months): Small improvements from paying down balances or fixing errors

Short term (3–6 months): Noticeable increases from consistent on-time payments and reduced utilization

Long term (6–18 months): Substantial growth as older negatives age off and positive behavior builds history

Improving your credit score is a marathon, not a sprint. Patience and consistency yield the best results.

19. Final Thoughts

As a business owner, your personal credit score is more than a financial statistic — it’s a reflection of your reliability, your planning, and your ability to weather financial storms. In the entrepreneurial world, where credit can unlock opportunities or cause setbacks, having strong personal credit is invaluable.

By following the steps outlined in this guide — from reviewing your credit reports to reducing utilization and separating personal from business finances — you can take control of your credit profile. Not only will you gain access to better financial tools, but you’ll also secure the foundation to grow your business with confidence.

Investing in your personal credit is investing in your business’s future. Start today, stay disciplined, and watch your financial credibility flourish.

This briefing document synthesizes key strategies and facts from “How to Improve Your Personal Credit Score” by Chris Lehnes, a Factoring Specialist. The central theme is that a strong personal credit score is a “powerful financial tool” for business owners, directly impacting access to loans, interest rates, and business opportunities. The document outlines a comprehensive, step-by-step approach to understanding, building, and maintaining excellent personal credit, emphasizing that “improving your credit score is a marathon, not a sprint.” It also highlights the crucial link between personal and business credit, particularly for small business owners.

II. Main Themes and Most Important Ideas/Facts

A. The Critical Importance of Personal Credit for Business Owners

Beyond a Number: A personal credit score is presented as “a powerful financial tool” that influences “access to loans, insurance premiums, leasing agreements, and even business partnerships.”

Direct Business Impact: For business owners, especially startups or those lacking significant assets, personal credit is often reviewed by lenders and suppliers to assess financial responsibility.

Benefits of Strong Personal Credit: A high score translates to “easier loan approvals with better terms,” “lower interest rates,” “reduced need for personal guarantees,” “favorable terms with vendors,” and “more options for credit cards and banking services.” Ultimately, it leads to “enhanced business flexibility and resilience.”

B. Understanding Your Credit Score: The Five Key Factors

Definition: A credit score is a “three-digit number that reflects your creditworthiness based on your credit history,” typically ranging from 300 to 850.

Primary Models: FICO® Score and VantageScore are the most widely used.

Contributing Factors (with weightings):Payment history (35%): The most significant factor.

Amounts owed / credit utilization (30%): Ratio of balances to credit limit.

Length of credit history (15%): Age of accounts.

Credit mix (10%): Variety of credit types.

New credit inquiries (10%): Recent applications.

C. Actionable Steps for Improving Personal Credit

Check Credit Reports for Accuracy (Step 1):

Obtain free reports from Equifax, Experian, and TransUnion via AnnualCreditReport.com.

Scrutinize for “incorrect personal information, duplicate or fraudulent accounts, incorrect balances, outdated delinquencies, [and] payment records errors.”

Errors are common and can “drag down your score unnecessarily.”

Dispute Errors (Step 2):

File disputes online or via certified mail with supporting documentation.

Bureaus have “30 to 45 days” to investigate. “Correcting even one major error… can significantly raise your score.”

Prioritize On-Time Payments (Step 3):

“Payment history is the most significant factor.” “Even one late payment can hurt your credit for years.”

Tips: Set reminders/autopay, prioritize minimum payments, maintain checking account cushion.

Reduce Credit Utilization (Step 4):

Maintain credit utilization (balances vs. total credit limit) “below 30% is advisable, and below 10% is optimal.”

Strategies: Pay off balances early, ask for higher credit limits (without increasing spending), pay multiple times a month. “Lower utilization shows you’re not reliant on credit to function.”

Avoid Too Many New Accounts at Once (Step 5):

Each credit application results in a “hard inquiry,” temporarily lowering the score.

Space out applications; consolidate rate shopping (e.g., mortgages) within a “14-45 day window.”

Keep Old Accounts Open (Step 6):

Closing old accounts shortens average credit age and reduces total available credit, negatively impacting the score.

“Unless an old account has an annual fee or causes you financial strain, keep it open.”

Diversify Credit Mix (Step 7):

Lenders prefer seeing responsible management of various credit types (cards, auto loans, mortgages).

Do not open accounts solely for variety, but manage existing mix responsibly.

Pay Down Debt Strategically (Step 8):

Snowball Method: Pay smallest balance first for motivation.

Avalanche Method: Pay highest-interest debt first to save money.

“Whichever method you choose, the key is consistency and discipline.”

Monitor Credit Regularly (Step 9):

Use free tools (Credit Karma, NerdWallet) or bank services to track changes and detect fraud.

Allows for “immediate action if your score drops or if new accounts appear unexpectedly.”

Leverage Business Credit to Separate Risk (Step 10):

A “key strategy” is to build and use business credit (EIN-based) to avoid overextending personal credit.

Tips: Obtain an EIN, open business bank/credit accounts, use vendors reporting to business bureaus. “This reduces personal liability and protects your score when your business takes on risk.”

Use Personal Credit-Building Tools (Step 11):

Secured credit cards: Require a deposit, easier to obtain.

Credit builder loans: Establish history without risk.

Authorized user status: Benefit from someone else’s good history.

Limit Personal Guarantees (Step 12):

Personal guarantees for business financing can be risky.

Strategies: Seek lenders not requiring guarantees, negotiate limited guarantees, strengthen business credit to avoid them entirely.

Establish an Emergency Fund (Step 13):

Saves credit by preventing missed payments or maxing out cards during hardship.

Recommendation: “3–6 months’ worth of personal expenses.”

Work with a Credit Counselor (Step 14):

For severe issues, nonprofit counselors (NFCC or FCAA accredited) can assist with budgeting, debt management, and creditor negotiation.

D. Common Pitfalls to Avoid

“Ignoring due dates” (late payments on report for up to 7 years).

“Closing credit cards prematurely” (reduces total available credit and credit age).

“Applying for too much credit” (multiple hard inquiries).

“Using personal credit for business risks” (blurs boundaries, increases personal liability).

“Over-reliance on one form of credit” (limits score potential).

E. Timeline for Results

Immediate (1–2 months): Small improvements from paying down balances or fixing errors.

Short Term (3–6 months): “Noticeable increases” from consistent on-time payments and reduced utilization.

Long Term (6–18 months): “Substantial growth” as older negatives age off and positive behavior builds history.

“Improving your credit score is a marathon, not a sprint. Patience and consistency yield the best results.”

III. Conclusion

The document strongly advocates for proactive credit management, asserting that “investing in your personal credit is investing in your business’s future.” By understanding credit score components, diligently following the outlined steps, avoiding common mistakes, and strategically separating personal and business finances, entrepreneurs can ensure their personal credit serves as an “asset, not a liability,” thereby securing a stronger foundation for business growth and financial credibility.

Understanding and Improving Your Personal Credit Score: A Comprehensive Guide

Study Guide

This guide is designed to help you review and solidify your understanding of the provided material on improving personal credit scores, especially for business owners.

I. Core Concepts of Credit Scores

Definition: What is a credit score and what does it represent?

Range: What is the typical range for credit scores, and what do higher scores indicate?

Primary Models: Identify the two most widely used credit scoring models.

Key Factors: List and briefly explain the five primary factors that contribute to a credit score, along with their approximate percentage weights.

II. Importance of Personal Credit for Business Owners

Interlinkage: Why is a business owner’s personal credit often linked to their enterprise, especially for small or new businesses?

Business Benefits: How does a strong personal credit score directly benefit a business (e.g., in terms of loans, interest rates, vendor relationships)?

Risk Separation: What is the ultimate goal in managing personal and business credit?

III. Step-by-Step Credit Improvement Strategies

For each of the following steps, be prepared to explain the action and its impact on your credit score:

Checking Credit Reports:Why is this the first step?

What specific types of errors should you look for?

Where can you get free credit reports?

Disputing Errors:What is the process for disputing errors?

How long do credit bureaus have to investigate?

What is the potential impact of correcting errors?

On-Time Payments:Why is payment history the most significant factor?

What are practical tips for ensuring on-time payments?

Credit Utilization:Define credit utilization.

What are the advisable and optimal utilization percentages?

List strategies to reduce credit utilization.

New Accounts:What is a “hard inquiry” and how does it affect your score?

Why should you avoid opening too many new accounts at once?

What is the exception for rate shopping?

Old Accounts:Why is it generally advisable to keep old accounts open?

What are the exceptions to this rule?

Credit Mix:Why is a diverse credit mix beneficial?

Does the article recommend opening new accounts solely for variety?

Debt Paydown Methods:Describe the Snowball Method.

Describe the Avalanche Method.

What is the key to success for either method?

Regular Monitoring:Why is ongoing credit monitoring important?

What tools can be used for monitoring?

Leveraging Business Credit:What is the purpose of building business credit (EIN-based)?

What actionable tips are provided for building business credit?

Personal Credit-Building Tools:Explain secured credit cards.

Explain credit builder loans.

Explain authorized user status.

Limiting Personal Guarantees:What is a personal guarantee?

Why should business owners try to limit them?

What strategies can help reduce the need for personal guarantees?

Emergency Fund:How does an emergency fund relate to credit health?

What is the recommended size for an emergency fund?

Credit Counseling:When should a business owner consider working with a credit counselor?

What services do they provide?

How can you identify a reputable counselor?

IV. Common Pitfalls and Timeline for Results

Common Pitfalls: Be able to list and explain common mistakes that can negatively impact a credit score.

Timeline for Improvement:What types of improvements can be seen immediately (1-2 months)?

What results can be expected in the short term (3-6 months)?

What defines long-term growth (6-18 months)?

What is the overall philosophy regarding the credit improvement process?

Quiz: Personal Credit Score Improvement

Answer each question in 2-3 sentences.

Explain why a business owner’s personal credit score is considered a “powerful financial tool.”

Name the two most widely used credit scoring models and identify the single most significant factor they evaluate.

What specific types of errors should a person look for when reviewing their credit reports from the three major bureaus?

Define credit utilization and state the optimal percentage recommended in the article.

Why is it generally advised to keep old credit accounts open, even if they are not frequently used?

Briefly describe the difference between the Snowball Method and the Avalanche Method for paying down debt.

How can building business credit (EIN-based) help a business owner protect their personal credit score?

Provide two examples of personal credit-building tools mentioned in the article and explain how they work.

Why is establishing an emergency fund considered a strategy for improving or maintaining a good credit score?

What is the approximate timeframe for seeing “substantial growth” in one’s credit score, and what does this timeframe signify about the process?

Quiz Answer Key

A business owner’s personal credit score is a powerful financial tool because it influences access to various financial resources such as loans, insurance premiums, leasing agreements, and even business partnerships. It directly affects the opportunities available to their business, particularly for small or new enterprises.

The two most widely used credit scoring models are FICO® Score and VantageScore. The single most significant factor they evaluate is payment history, which accounts for 35% of the score.

When reviewing credit reports, a person should carefully look for incorrect personal information, duplicate or fraudulent accounts, incorrect balances, outdated delinquencies, and payment record errors. Identifying and disputing these inaccuracies can prevent unnecessary drops in their score.

Credit utilization refers to the ratio of your current revolving credit balances to your total credit limit. The article advises keeping utilization below 30%, with below 10% being considered optimal for strong financial health.

It is generally advised to keep old credit accounts open because the age of your credit accounts significantly impacts your score. Closing old accounts can shorten your average credit age and reduce your total available credit, both of which negatively affect your score.

The Snowball Method involves paying off the smallest balance first while making minimum payments on other debts, building momentum and motivation. In contrast, the Avalanche Method prioritizes paying off the highest-interest debt first, which saves more money on interest in the long run.

Building business credit (EIN-based) helps a business owner protect their personal credit score by separating business financial risk from personal liability. This strategy ensures that personal credit isn’t overextended when the business takes on debt or risks, reducing the personal impact if the business struggles.

One tool is a secured credit card, which requires a cash deposit as collateral, making it easier to obtain and build payment history. Another is a credit builder loan, where funds are held in an account while the borrower makes regular payments, establishing a positive credit history without immediate financial risk.

Establishing an emergency fund is a strategy for credit health because it reduces the likelihood of missing payments or maxing out credit cards during unexpected financial difficulties. A healthy cash reserve prevents reliance on credit during tough times, protecting one’s credit score.

The approximate timeframe for seeing “substantial growth” in one’s credit score is 6-18 months. This long-term period signifies that improving credit is a “marathon, not a sprint,” emphasizing the need for patience and consistent positive financial behavior to yield the best results.

If your clients are like many small business owners, they have probably faced the frustrating gap between sending an invoice and actually getting paid.

Our Non-Recourse Accounts Receivable Factoring Program offers a smart solution.

Instead of waiting for customers to pay, factoring provides immediate access to the funds tied up in unpaid invoices. That means more money to meet payroll, restock inventory, invest in growth, or simply keep operations running smoothly.

Program Overview

$100,000 to $30 Million

Non-Recourse

No Audits

No Financial Covenants

Most businesses with strong customers eligible

We specialize in difficult deals:

Start-ups

Weak Balance Sheets

Historic Losses

Customer Concentrations

Poor Personal Credit

Character Issues

We focus on the quality of your client’s accounts receivable, ignoring their financial condition.

This enables us to move quickly and fund qualified businesses including Manufacturers, Distributors and a wide variety of Service Businesses in as few as 3-5 days. Contact me today to learn if your client is a fit.

Title: How the China Trade Deal Announced Today Will Impact Small Businesses

Introduction to impact of China Trade Deal

Today, the U.S. and China reached a tentative trade agreement that marks a significant, albeit partial, development in their ongoing economic standoff. This new arrangement preserves existing tariffs—55% on Chinese imports and 10% on U.S. exports—while introducing limited concessions on rare-earth minerals and export controls. The agreement provides minimal relief for most small businesses, which have borne the brunt of the past several years of tariff-induced uncertainty. This article will explore in detail the contents of the deal, assess its implications for various sectors of the small business community, and offer strategic recommendations for adaptation.

Part 1: Understanding the New U.S. – China Trade Deal

The June 11, 2025 deal between the United States and China was framed more as a temporary stabilization than a comprehensive resolution. Here are the key elements:

Tariffs Remain Largely Intact: The U.S. will maintain approximately 55% tariffs on a wide range of Chinese imports. China will reciprocate with 10% tariffs on American goods. The structure formalizes what had become the status quo over the last year.

Rare-Earth Concession: China agreed to issue six-month export licenses for rare-earth materials essential to U.S. electronics, automotive, and defense sectors.

Relaxation of Non-Tariff Measures: Export controls were modestly loosened, and restrictions on student visas for Chinese nationals have been relaxed, which may ease the climate for academic and professional exchange.

While headlines emphasized “agreement,” the reality is that the deal provides only narrow, conditional relief and does little to roll back the broader tariff architecture hurting American small enterprises.

Part 2: Current Landscape for Small Businesses & China

Before assessing the implications of the deal, it is important to understand the pressures already being experienced by small businesses:

Increased Supply Costs: Retailers, manufacturers, and e-commerce sellers reliant on imports have been particularly hard-hit by increased tariffs. The removal of the $800 “de minimis” exemption meant sudden cost spikes for previously low-tariff goods.

Planning Uncertainty: The unpredictability of trade negotiations has left small business owners unable to make informed decisions about inventory, pricing, or expansion.

Disrupted Cash Flow: Delays at ports and sudden changes in pricing structures have left many businesses with overstocked, overpriced inventory they cannot move.

Reduced Competitiveness: Higher input costs mean many small businesses can no longer compete with large corporations that have deeper reserves or more diversified supply chains.

Consumer Backlash: Price increases are alienating customers and diminishing brand loyalty for many small retailers.

Part 3: Sector-by-Sector Analysis – China

Let’s examine how this deal will impact different segments of the small business ecosystem.

Manufacturing

Impact: Moderate Relief.

For small manufacturers reliant on rare-earth materials, the six-month export licenses offer temporary breathing room. Sectors like electronics, defense subcontracting, and advanced manufacturing may see modest improvements in supply chain consistency.

Risks: The time-bound nature of the licenses makes long-term planning difficult. Any lapse in licensing will reintroduce chaos.

E-Commerce

Impact: Minimal to Negative.

Online sellers, particularly those importing fashion, gadgets, or toys, were previously protected by the de minimis exemption. With this gone and no rollback in tariffs, they are squeezed between rising costs and customer expectations for low prices.

Risks: Many sellers may exit the market or shift operations overseas.

Brick-and-Mortar Retail

Impact: Negative.

Stores relying on imported goods—from housewares to ethnic food supplies—will see no cost reduction. Without major economies of scale, small shops must raise prices or reduce product offerings.

Risks: Reduced foot traffic, lower profit margins, and possible closures.

Agriculture & Food Processing

Impact: Negligible.

Most food exports to China still face tariffs. While larger producers may negotiate their way through, small-scale farms and specialty producers face pricing disadvantages.

Risks: Loss of export competitiveness, oversupply in domestic markets.

Professional Services (Consulting, Legal, Educational)

Impact: Potentially Positive.

The easing of visa and academic restrictions may stimulate demand for consulting, education services, and cross-border partnerships.

Risks: Benefits are slow-moving and depend on broader geopolitical stabilization.

Part 4: What the Deal Does Not Address

Despite media attention, the deal sidesteps many of the deeper structural issues affecting small businesses:

No De-escalation Timeline: There is no roadmap for reducing tariffs further or restoring exemptions.

Temporary Nature of Relief: Six-month licenses are not sufficient for meaningful strategic planning.

No Domestic Support Programs: There is no corresponding federal relief for small firms affected by the tariffs.

No Infrastructure for Adaptation: Programs to help small businesses retool supply chains or go digital are still lacking.

No Harmonization of Standards: Differing regulations and standards continue to limit the ability of small businesses to export efficiently.

Part 5: Strategic Recommendations for Small Businesses and China

In light of these dynamics, small businesses must adopt proactive strategies:

1. Supply Chain Diversification

Identify suppliers in countries not subject to high tariffs. Consider nearshoring options such as Mexico, Canada, or domestic production where feasible.

2. Product Portfolio Optimization

Evaluate which products are most impacted by tariffs. Shift focus to less import-dependent or higher-margin offerings.

3. Financial Planning and Resilience

Engage in scenario planning. Consider factoring, SBA loans, or trade finance to stabilize cash flow in periods of uncertainty.

4. Advocacy and Alliances

Join trade associations or local chambers of commerce to advocate for small business interests in ongoing trade negotiations.

5. Customer Communication

Be transparent about price increases or product changes. Position your business as responsive and honest rather than reactive.

6. Digital Adaptation

Invest in e-commerce platforms, CRM tools, and logistics software to increase operational efficiency and customer engagement.

Part 6: The Broader Economic Picture

Small businesses are not isolated from macroeconomic trends. The deal may create the following broader conditions:

Improved Investor Confidence: Markets may respond positively to even temporary stability, which could ease borrowing conditions.

Inflation Management: Stabilizing trade could assist the Federal Reserve in maintaining inflation at the current 2.4% level.

Employment Outlook: Clarity in trade policy may encourage cautious hiring, particularly in sectors such as logistics, warehousing, and small-scale manufacturing.

However, these benefits are conditional and unevenly distributed. Without deeper structural reforms, the new agreement is unlikely to generate a large-scale recovery for the small business sector.

The June 11, 2025 U.S.-China trade agreement is a temporary truce rather than a resolution. While it introduces some modest benefits—particularly for manufacturing reliant on rare-earth minerals—it does little to ease the pain felt by the majority of small businesses still grappling with high tariffs, uncertain supply chains, and squeezed profit margins. Strategic adaptation, political advocacy, and operational resilience will be the keys to survival in this persistently volatile landscape. Until a more comprehensive agreement is reached, small businesses must continue to plan for instability and seize whatever limited advantages the current deal affords.

Briefing Document: Impact of the New U.S.-China Trade Deal on Small Businesses

Date: June 11, 2025 Source: Excerpts from “How the China Trade Deal Will Impact Small Businesses” by Chris Lehnes, Factoring Specialist

This briefing document summarizes the key themes, ideas, and facts presented in Chris Lehnes’ article “How the China Trade Deal Announced Today Will Impact Small Businesses,” published on June 11, 2025. The article assesses the implications of the new U.S.-China trade agreement for various small business sectors and offers strategic recommendations for adaptation.

1. Executive Summary: A “Temporary Stabilization” Not a “Comprehensive Resolution”

The recently announced U.S.-China trade agreement on June 11, 2025, is primarily described as a “temporary stabilization” rather than a significant breakthrough or “comprehensive resolution.” The deal maintains the “status quo” of existing high tariffs (55% on Chinese imports to the U.S. and 10% on U.S. exports to China), offering “minimal relief for most small businesses.” While it introduces limited concessions regarding rare-earth minerals and a relaxation of some non-tariff measures, it largely fails to address the deeper structural issues that have burdened small enterprises.

2. Key Elements of the New Trade Deal

The article highlights the following specific components of the June 11, 2025 agreement:

Tariffs Remain Largely Intact: “The U.S. will maintain approximately 55% tariffs on a wide range of Chinese imports. China will reciprocate with 10% tariffs on American goods.” This formalizes the existing tariff structure.

Rare-Earth Concession: China has agreed to “issue six-month export licenses for rare-earth materials essential to U.S. electronics, automotive, and defense sectors.”

Relaxation of Non-Tariff Measures: There has been a “modest loosening” of export controls and a relaxation of “restrictions on student visas for Chinese nationals,” which may “ease the climate for academic and professional exchange.”

Lehnes emphasizes that despite headlines, the deal offers “only narrow, conditional relief and does little to roll back the broader tariff architecture hurting American small enterprises.”

3. Current Landscape for Small Businesses: Pre-Existing Pressures

Before the deal, small businesses were already facing significant challenges due to the ongoing trade tensions:

Increased Supply Costs: Retailers, manufacturers, and e-commerce sellers dependent on imports “have been particularly hard-hit by increased tariffs.” The removal of the “$800 ‘de minimis’ exemption meant sudden cost spikes for previously low-tariff goods.”

Planning Uncertainty: “The unpredictability of trade negotiations has left small business owners unable to make informed decisions about inventory, pricing, or expansion.”

Disrupted Cash Flow: “Delays at ports and sudden changes in pricing structures have left many businesses with overstocked, overpriced inventory they cannot move.”

Reduced Competitiveness: “Higher input costs mean many small businesses can no longer compete with large corporations that have deeper reserves or more diversified supply chains.”

Consumer Backlash: “Price increases are alienating customers and diminishing brand loyalty for many small retailers.”

4. Sector-by-Sector Impact Analysis

The deal’s impact varies significantly across different small business sectors:

Manufacturing:Moderate Relief. Businesses reliant on rare-earth materials will experience “temporary breathing room” from the six-month export licenses. However, the “time-bound nature of the licenses makes long-term planning difficult.”

E-Commerce:Minimal to Negative. Online sellers previously protected by the “de minimis” exemption are now “squeezed between rising costs and customer expectations for low prices,” with many potentially having to “exit the market or shift operations overseas.”

Brick-and-Mortar Retail:Negative. Stores relying on imported goods “will see no cost reduction” and must “raise prices or reduce product offerings,” leading to “reduced foot traffic, lower profit margins, and possible closures.”

Agriculture & Food Processing:Negligible. Most food exports still face tariffs, making it difficult for “small-scale farms and specialty producers [to] face pricing disadvantages” and risk “loss of export competitiveness, oversupply in domestic markets.”

Professional Services (Consulting, Legal, Educational):Potentially Positive. The easing of visa and academic restrictions “may stimulate demand for consulting, education services, and cross-border partnerships,” though benefits are “slow-moving.”

5. What the Deal Does Not Address

The article identifies several critical omissions in the new agreement:

No De-escalation Timeline: “There is no roadmap for reducing tariffs further or restoring exemptions.”

Temporary Nature of Relief: “Six-month licenses are not sufficient for meaningful strategic planning.”

No Domestic Support Programs: “There is no corresponding federal relief for small firms affected by the tariffs.”

No Infrastructure for Adaptation: “Programs to help small businesses retool supply chains or go digital are still lacking.”

No Harmonization of Standards: “Differing regulations and standards continue to limit the ability of small businesses to export efficiently.”

6. Strategic Recommendations for Small Businesses

Given the persistent volatility, Lehnes advises small businesses to adopt proactive strategies:

Supply Chain Diversification: “Identify suppliers in countries not subject to high tariffs. Consider nearshoring options such as Mexico, Canada, or domestic production where feasible.”

Product Portfolio Optimization: “Evaluate which products are most impacted by tariffs. Shift focus to less import-dependent or higher-margin offerings.”

Financial Planning and Resilience: “Engage in scenario planning. Consider factoring, SBA loans, or trade finance to stabilize cash flow.”

Advocacy and Alliances: “Join trade associations or local chambers of commerce to advocate for small business interests.”

Customer Communication: “Be transparent about price increases or product changes.”

Digital Adaptation: “Invest in e-commerce platforms, CRM tools, and logistics software to increase operational efficiency.”

7. Broader Economic Picture and Conclusion

While the deal may lead to “improved investor confidence” and potentially assist with “inflation management” (currently at 2.4%), these benefits are “conditional and unevenly distributed.” The article concludes that “without deeper structural reforms, the new agreement is unlikely to generate a large-scale recovery for the small business sector.”

In essence, the June 11, 2025 U.S.-China trade agreement is a “temporary truce rather than a resolution.” Small businesses must continue to “plan for instability and seize whatever limited advantages the current deal affords.”

U.S.-China Trade Deal and Small Businesses: A Comprehensive Study Guide

I. Overview of the New U.S.-China Trade Deal (June 11, 2025)

Nature of the Agreement: A tentative, partial development aimed at temporary stabilization rather than a comprehensive resolution of economic tensions.

Tariff Structure:U.S. tariffs on Chinese imports: Approximately 55% (largely maintained).

China tariffs on U.S. exports: 10% (largely reciprocated).

Formalizes the status quo of the past year.

Key Concessions:Rare-Earth Materials: China to issue six-month export licenses for rare-earth materials vital to U.S. electronics, automotive, and defense sectors.

Non-Tariff Measures: Modest loosening of export controls and relaxation of student visa restrictions for Chinese nationals.

Overall Impact: Provides narrow, conditional relief and does little to roll back the broader tariff architecture impacting American small enterprises.

II. Current Landscape for Small Businesses Pre-Deal

Increased Supply Costs: Tariffs have significantly raised costs for retailers, manufacturers, and e-commerce sellers relying on imports. The removal of the $800 “de minimis” exemption exacerbated this.

Planning Uncertainty: Unpredictability of trade negotiations hinders informed decision-making on inventory, pricing, and expansion.

Disrupted Cash Flow: Delays at ports and sudden pricing changes lead to overstocked, overpriced inventory.

Reduced Competitiveness: Higher input costs make it difficult for small businesses to compete with large corporations with deeper reserves or diversified supply chains.

Consumer Backlash: Price increases alienate customers and diminish brand loyalty.

III. Sector-by-Sector Analysis of Deal Impact

Manufacturing:Impact: Moderate Relief. Temporary breathing room from six-month rare-earth export licenses for sectors like electronics, defense subcontracting, and advanced manufacturing.

Risks: Time-bound licenses make long-term planning difficult; potential reintroduction of chaos if licenses lapse.

E-Commerce:Impact: Minimal to Negative. No rollback of tariffs, and the removed de minimis exemption continues to squeeze online sellers.

Risks: Many sellers may exit the market or shift operations overseas.

Brick-and-Mortar Retail:Impact: Negative. No cost reduction for stores reliant on imported goods; must raise prices or reduce offerings without economies of scale.

Agriculture & Food Processing:Impact: Negligible. Most food exports to China still face tariffs; small-scale producers face pricing disadvantages.

Risks: Loss of export competitiveness, oversupply in domestic markets.

Professional Services (Consulting, Legal, Educational):Impact: Potentially Positive. Easing of visa and academic restrictions may stimulate demand for cross-border services and partnerships.

Risks: Benefits are slow-moving and contingent on broader geopolitical stabilization.

IV. What the Deal Does NOT Address

No De-escalation Timeline: Lacks a roadmap for further tariff reduction or exemption restoration.

Temporary Nature of Relief: Six-month licenses are insufficient for meaningful strategic planning.

No Domestic Support Programs: Absence of federal relief for small firms affected by tariffs.

No Infrastructure for Adaptation: Lacks programs to help small businesses retool supply chains or digitalize operations.

No Harmonization of Standards: Differing regulations continue to limit efficient small business exports.

V. Strategic Recommendations for Small Businesses

Supply Chain Diversification: Identify suppliers in low-tariff countries, consider nearshoring (Mexico, Canada), or domestic production.

Product Portfolio Optimization: Shift focus to less import-dependent or higher-margin offerings.

Financial Planning and Resilience: Engage in scenario planning, explore factoring, SBA loans, or trade finance to stabilize cash flow.

Advocacy and Alliances: Join trade associations or chambers of commerce to advocate for small business interests.

Customer Communication: Be transparent about price increases or product changes.

Digital Adaptation: Invest in e-commerce platforms, CRM tools, and logistics software.

Inflation Management: Could assist the Federal Reserve in maintaining inflation at 2.4%.

Employment Outlook: Clarity may encourage cautious hiring in logistics, warehousing, and small-scale manufacturing.

Overall Conclusion: The agreement is a temporary truce. Without deeper structural reforms, it’s unlikely to generate a large-scale recovery for the small business sector. Strategic adaptation and resilience are key to survival.

Quiz: U.S.-China Trade Deal Impact on Small Businesses

Instructions: Answer each question in 2-3 sentences.

What is the primary characteristic of the June 11, 2025, U.S.-China trade agreement, as described in the source?

How do the tariffs on Chinese imports and U.S. exports compare after the new deal?

Which specific material did China agree to issue export licenses for, and which U.S. sectors benefit?

Before the deal, what was a significant financial pressure on small businesses due to trade policies, specifically mentioned as being “gone”?

Why is the impact of the deal on the E-Commerce sector described as “Minimal to Negative”?

What is the primary risk for small manufacturers despite the temporary relief they might experience from the deal?

Beyond tariffs, what crucial aspect related to trade policy did the deal not address, which is vital for small business planning?

Name two specific strategic recommendations provided for small businesses to adapt to the current trade landscape.

How might the new trade deal indirectly impact broader investor confidence, according to the article?

What type of businesses within the “Professional Services” sector are expected to see a potentially positive impact from the deal?

Answer Key

The June 11, 2025, U.S.-China trade agreement is characterized as a tentative, partial development that offers temporary stabilization rather than a comprehensive resolution. It formalizes existing tariffs and provides only narrow, conditional relief.

After the new deal, the U.S. will maintain approximately 55% tariffs on a wide range of Chinese imports, while China will reciprocate with 10% tariffs on American goods. This structure largely formalizes the status quo of the past year.

China agreed to issue six-month export licenses for rare-earth materials. This concession is essential to U.S. electronics, automotive, and defense sectors, offering them temporary breathing room.

Before the deal, the removal of the $800 “de minimis” exemption was a significant financial pressure on small businesses, causing sudden cost spikes for previously low-tariff imported goods. This removal particularly affected retailers and e-commerce sellers.

The impact on the E-Commerce sector is “Minimal to Negative” because the deal did not roll back tariffs, and the prior protection offered by the de minimis exemption is gone. This leaves online sellers squeezed between rising costs and customer expectations for low prices, potentially forcing them to exit the market.

The primary risk for small manufacturers, despite the temporary relief from rare-earth licenses, is the time-bound nature of these licenses. This makes long-term planning difficult, as any lapse in licensing will reintroduce chaos and supply chain instability.

Beyond tariffs, the deal did not address a crucial aspect related to trade policy for small business planning: the lack of a de-escalation timeline. There is no roadmap for further reducing tariffs or restoring exemptions, leaving businesses with continued uncertainty.

Two strategic recommendations for small businesses are Supply Chain Diversification, which involves identifying suppliers in low-tariff countries or considering nearshoring, and Financial Planning and Resilience, which includes engaging in scenario planning and exploring financing options like SBA loans.

The new trade deal might indirectly impact broader investor confidence positively, as markets may respond to even temporary stability. This improved confidence could potentially ease borrowing conditions for businesses.

Businesses within the “Professional Services” sector, such as consulting, legal, and educational services, are expected to see a potentially positive impact. This is due to the easing of visa and academic restrictions, which may stimulate demand for cross-border partnerships and services.

Essay Format Questions

Analyze the primary characteristics of the June 11, 2025, U.S.-China trade agreement. Discuss how its “tentative” and “partial” nature distinguishes it from a comprehensive resolution, and explain the implications of maintaining existing tariff structures.

Evaluate the varying impacts of the new trade deal across different small business sectors (Manufacturing, E-Commerce, Brick-and-Mortar Retail, Agriculture & Food Processing, Professional Services). Why do some sectors experience “moderate relief” while others face “minimal to negative” consequences?

The article highlights several critical issues that the trade deal does not address. Discuss at least three of these unaddressed issues and explain how their omission continues to pose significant challenges for small businesses.

Propose a comprehensive strategic plan for a hypothetical small business (e.g., an e-commerce gadget seller or a small electronics manufacturer) based on the recommendations provided in the source. Justify how each chosen strategy directly addresses the specific challenges this business faces due to the current trade landscape.

Discuss the broader economic picture presented in the article. To what extent does the temporary stability offered by the deal contribute to “improved investor confidence,” “inflation management,” and a positive “employment outlook,” and what are the limitations or conditionalities of these benefits?

Glossary of Key Terms

Tariffs: Taxes imposed by a government on imported or exported goods. In this context, used by the U.S. and China to control trade flows.

Rare-Earth Materials: A group of 17 chemical elements essential for the production of high-tech devices, including electronics, electric vehicles, and defense systems. China is a dominant producer.

Export Controls: Government regulations that restrict or prohibit the export of certain goods, technologies, or services to specific destinations or entities.

De Minimis Exemption ($800): A U.S. Customs and Border Protection regulation that allowed imported goods valued at $800 or less to enter the country duty-free and with minimal formal entry procedures. Its removal significantly increased costs for many small businesses.

Supply Chain Diversification: The strategy of sourcing materials, components, or finished goods from multiple suppliers in different geographic locations to reduce reliance on a single source or region and mitigate risks.

Nearshoring: The practice of relocating business processes or production to a nearby country, often sharing a border or region, to reduce costs while maintaining geographical proximity.

Factoring: A financial transaction where a business sells its accounts receivable (invoices) to a third party (a “factor”) at a discount in exchange for immediate cash. Used to stabilize cash flow.

SBA Loans: Loans guaranteed by the U.S. Small Business Administration, designed to help small businesses access capital for various purposes, often with more favorable terms than traditional bank loans.

Trade Finance: Financial products and services that facilitate international trade and commerce, typically involving banks or financial institutions providing credit, guarantees, or insurance to mitigate risks for importers and exporters.

CRM Tools (Customer Relationship Management): Software systems designed to manage and analyze customer interactions and data throughout the customer lifecycle, with the goal of improving business relationships with customers and assisting in customer retention and sales growth.

Inflation Management: Actions taken by central banks or governments to control the rate at which prices for goods and services are rising, often targeting a specific inflation rate to maintain economic stability.

Leveraging SaaS to Boost Efficiency in Small Businesses

Small Businesses and SaaS

In an increasingly digital world, small businesses face immense pressure to remain competitive, agile, and efficient. Fortunately, Software as a Service (SaaS) has emerged as a transformative solution, offering access to powerful tools and platforms without the need for heavy infrastructure or extensive IT staff. From customer relationship management to accounting and collaboration, SaaS empowers small businesses to streamline operations, reduce costs, and scale effectively. This article explores how small businesses can leverage SaaS to improve efficiency across various facets of their operations.

What is SaaS?

Software as a Service (SaaS) is a cloud-based model that delivers software applications over the internet. Unlike traditional software, which requires installation and maintenance on individual machines, SaaS applications are hosted remotely and accessed via web browsers. This eliminates the need for on-premise infrastructure and provides real-time access to data and tools.

Key Characteristics of SaaS:

Subscription-based pricing

Cloud-hosted and accessible via the internet

Automatic updates and maintenance

Scalability and flexibility

Cross-device compatibility

Popular examples of SaaS include Google Workspace, Salesforce, QuickBooks Online, and Slack. These platforms are designed to help businesses manage workflows, communicate effectively, and enhance customer relationships

Benefits of SaaS for Small Businesses

1. Cost Efficiency

One of the most appealing aspects of SaaS for small businesses is its affordability. Traditional software often requires a significant upfront investment for licenses, hardware, and IT support. SaaS, by contrast, operates on a subscription model, allowing businesses to pay a manageable monthly or annual fee. This model significantly reduces capital expenditures and allows for predictable budgeting.

Moreover, SaaS providers handle updates, maintenance, and security, further reducing the need for an in-house IT team.

2. Scalability and Flexibility

As businesses grow, their software needs evolve. SaaS platforms are inherently scalable, allowing small businesses to upgrade their plans or add users without major disruptions. Whether a company is hiring new employees or expanding into new markets, SaaS solutions can be adjusted to match the pace of growth.

3. Accessibility and Remote Work Enablement

With SaaS, employees can access work-related applications from anywhere with an internet connection. This flexibility supports remote work and enables teams to collaborate across locations. In the wake of the COVID-19 pandemic, the ability to work from home has become essential for business continuity.

4. Integration and Automation

SaaS applications often come with APIs and integration capabilities, allowing them to connect with other tools and platforms. This interoperability reduces manual data entry and streamlines workflows. For example, a CRM tool can be integrated with email marketing software to automate customer outreach based on user behavior.

5. Enhanced Security

Leading SaaS providers invest heavily in security protocols to protect customer data. These measures typically exceed what small businesses could afford on their own. Features such as encryption, multi-factor authentication, and regular backups are standard in many SaaS offerings.

6. Rapid Deployment and Ease of Use

SaaS applications are typically user-friendly and require minimal setup. This means small businesses can implement new tools quickly and start seeing benefits immediately. Many SaaS providers also offer training resources and customer support to assist with onboarding.

Key Areas Where SaaS Enhances Efficiency

1. Customer Relationship Management (CRM)

CRM systems help businesses manage interactions with current and potential customers. SaaS-based CRMs like Salesforce, HubSpot, and Zoho CRM provide a centralized platform to track leads, sales, and customer communications.

Efficiency Gains:

Automated follow-ups and reminders

Real-time sales analytics

Improved customer segmentation and targeting

Enhanced customer service through shared data access

2. Accounting and Finance

SaaS accounting platforms such as QuickBooks Online, Xero, and FreshBooks simplify bookkeeping, invoicing, and financial reporting. These tools reduce the need for manual data entry and help ensure compliance with tax regulations.

Efficiency Gains:

Real-time financial tracking

Automated invoice generation and reminders

Seamless bank integration

Easy collaboration with accountants and financial advisors

3. Project Management and Collaboration

Platforms like Trello, Asana, Monday.com, and ClickUp facilitate task management and team collaboration. These tools allow small businesses to track progress, assign responsibilities, and communicate effectively.

Efficiency Gains:

Centralized task and project tracking

Integrated communication channels

Time tracking and deadline management

Improved accountability and transparency

4. Marketing and Sales Automation

SaaS marketing tools such as Mailchimp, ActiveCampaign, and Hootsuite enable small businesses to execute marketing campaigns with minimal effort. These platforms often include features like email automation, social media scheduling, and customer analytics.

Efficiency Gains:

Automated email workflows

Audience segmentation

Social media management from a single dashboard

Performance analytics and A/B testing

5. Human Resources and Payroll

SaaS solutions for HR, like Gusto, BambooHR, and Zenefits, simplify employee onboarding, time tracking, benefits administration, and payroll processing.

Efficiency Gains:

Automated payroll and tax filing

Self-service portals for employees

Centralized employee records

Compliance tracking and reporting

6. E-commerce and Point of Sale (POS)

Platforms like Shopify, Square, and WooCommerce provide small businesses with end-to-end solutions for online and in-store sales. These systems integrate inventory management, sales reporting, and customer insights.

Efficiency Gains:

Seamless online store setup

Integrated payment processing

Inventory and order tracking

Marketing and SEO tools

7. Document Management and eSignatures

Tools like DocuSign, Adobe Acrobat Sign, and PandaDoc allow businesses to manage contracts and obtain electronic signatures securely.

Efficiency Gains:

Faster document turnaround

Secure and compliant digital signature solutions

Template creation and reuse

Reduced reliance on physical paperwork

Industry-Specific SaaS Solutions

While general-purpose SaaS platforms offer broad utility, industry-specific tools provide tailored functionality to meet niche requirements.

1. Healthcare

Practice management: Kareo, SimplePractice

Telehealth: Doxy.me, Amwell

2. Retail

Inventory management: Vend, Lightspeed

POS systems: Clover, Shopify POS

3. Legal Services

Case management: Clio, MyCase

Billing and time tracking: TimeSolv, Bill4Time

4. Real Estate

CRM and listing management: BoomTown, Follow Up Boss

Document signing and storage: Dotloop, DocuSign

5. Construction

Project management: Procore, Buildertrend

Estimating and bidding: CoConstruct, JobNimbus

Strategies for Successful SaaS Implementation

1. Identify Business Needs

Before selecting a SaaS solution, small businesses should assess their pain points and define clear objectives. This ensures that the chosen software aligns with actual business needs and priorities.

2. Evaluate Vendors

Factors to consider when choosing a SaaS provider include:

Pricing and contract terms

Features and scalability

User reviews and case studies

Customer support and onboarding services

3. Ensure Data Security and Compliance

Businesses must understand how their data is stored, who has access, and what compliance standards the provider follows (e.g., GDPR, HIPAA). A thorough review of the provider’s security policies is essential.

4. Plan for Integration

Choose SaaS tools that integrate with existing systems. This reduces data silos and improves overall efficiency. API availability and third-party integrations should be part of the selection criteria.

5. Train Employees

Even the best software is only as effective as its users. Provide comprehensive training to ensure that staff can utilize the tools efficiently. Many SaaS providers offer tutorials, webinars, and support resources.

6. Monitor Performance

Track key performance indicators (KPIs) to measure the impact of SaaS tools on business operations. Common metrics include productivity, cost savings, customer satisfaction, and revenue growth.

Common Challenges and How to Overcome Them

1. Resistance to Change

Employees may be hesitant to adopt new tools. Overcome this by involving them early in the selection process and highlighting the benefits of the new system.

2. Overwhelming Choice

With thousands of SaaS products on the market, it can be difficult to choose the right one. Focus on specific business needs and prioritize platforms with a proven track record.

3. Subscription Creep

Using too many SaaS tools can lead to higher costs and overlapping functionality. Regularly audit your subscriptions to eliminate redundancy and consolidate where possible.

4. Data Migration Issues

Transitioning from legacy systems to SaaS platforms can involve complex data migration. Work with vendors who offer migration support and test the new system thoroughly before going live.

5. Dependence on Internet Connectivity

SaaS tools require a stable internet connection. Ensure that your business has reliable connectivity and consider offline-access features where necessary.

Case Studies

Case Study 1: Boosting Productivity with a CRM

A small digital marketing agency struggled to manage client communication and track leads. After implementing HubSpot CRM, they automated follow-ups, centralized contact data, and improved client retention by 25%.

Case Study 2: Streamlining Accounting Processes

A family-run retail store adopted QuickBooks Online to replace manual bookkeeping. This move reduced accounting errors by 40% and saved over 10 hours per week in administrative work.

Case Study 3: Enhancing Team Collaboration

A remote design firm used Trello and Slack to coordinate projects across multiple time zones. These tools allowed them to manage deadlines more effectively and reduce project delivery times by 30%.

Case Study 4: Automating Marketing for Growth

An e-commerce startup used Mailchimp to automate their email campaigns. By segmenting their audience and using A/B testing, they increased their email open rates by 20% and sales by 15% in three months.

The Future of SaaS for Small Businesses

The SaaS market is poised for continued growth, with innovations such as artificial intelligence (AI), machine learning (ML), and advanced analytics reshaping how businesses operate. Future SaaS tools will offer even more automation, predictive insights, and personalization.

Emerging Trends:

AI-powered chatbots and customer service

Predictive analytics for sales and marketing

Workflow automation across departments

Industry-specific microservices

As these tools become more accessible, small businesses will be better equipped to compete with larger enterprises.

Conclusion

SaaS offers small businesses an unparalleled opportunity to improve efficiency, reduce costs, and scale operations. From CRM and accounting to marketing and HR, SaaS tools provide the agility and functionality that modern businesses need to thrive. By selecting the right solutions, integrating them effectively, and fostering a culture of continuous improvement, small businesses can harness the full potential of SaaS and position themselves for sustained success.

As technology continues to evolve, staying informed and adaptable will be key. Small businesses that embrace SaaS not only survive in a competitive marketplace but also unlock new avenues for innovation and growth.

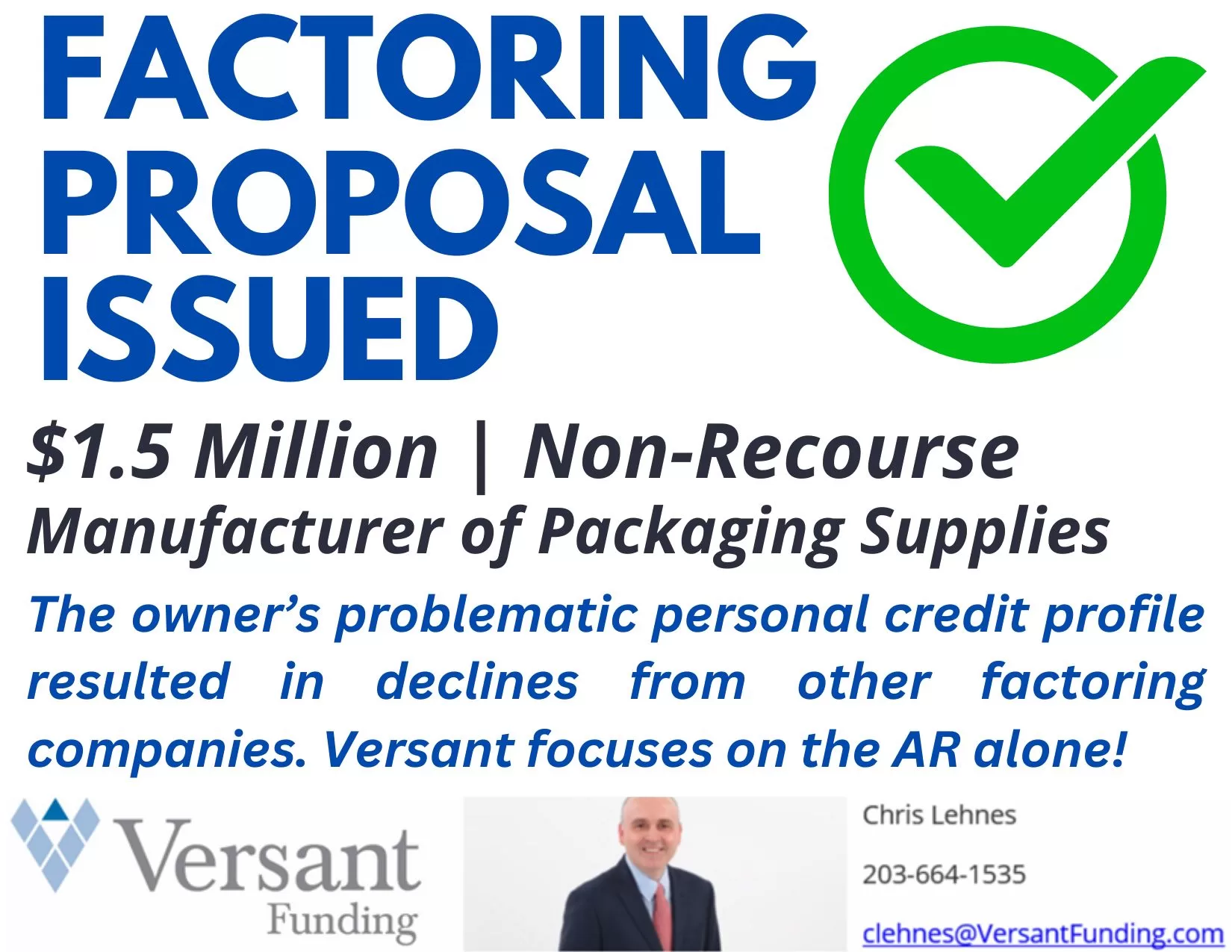

Factoring Proposal Issued: $1.5 Million | Manufacturer: The owner’s problematic personal credit profile resulted in declines from other factoring companies. Versant focuses on the AR alone!

Accounts Receivable Factoring $100,000 to $30 Million Quick AR Advances No Long-Term Commitment Non-recourse Funding in about a week

We are a great match for businesses with traits such as: Less than 2 years old Negative Net Worth Losses Customer Concentrations Weak Credit Character Issues

Chris Lehnes | Factoring Specialist | 203-664-1535 | chris@chrislehnes.com

Title: Our Dollar, Your Problem: A Deep Dive into Kenneth Rogoff’s Insight on the Dollar’s Dominance and Future

Introduction

In his sweeping narrative “Our Dollar, Your Problem: An Insider’s View of Seven Turbulent Decades of Global Finance, and the Road Ahead,” Kenneth Rogoff delivers a rare blend of historical context, insider perspective, and forward-looking analysis. His experience as a former chief economist of the International Monetary Fund and a Harvard economist grants him unique credibility to speak on the global role of the U.S. dollar, its ascent to dominance, its profound influence on the world economy, and the precarious road it now treads. This analysis aims to summarize the core themes of Rogoff’s book, dissect the economic principles that underpin his assertions, and evaluate the implications of his forecast for global finance.

Part I: The Historical Ascent of the Dollar

The story of the U.S. dollar is intrinsically tied to the evolution of the global financial system. Rogoff traces this arc beginning with the end of World War II, where the United States emerged not only militarily dominant but economically unscathed compared to its war-torn European and Asian allies. This set the stage for the Bretton Woods Agreement, a monetary framework wherein the dollar was pegged to gold, and other currencies were pegged to the dollar.