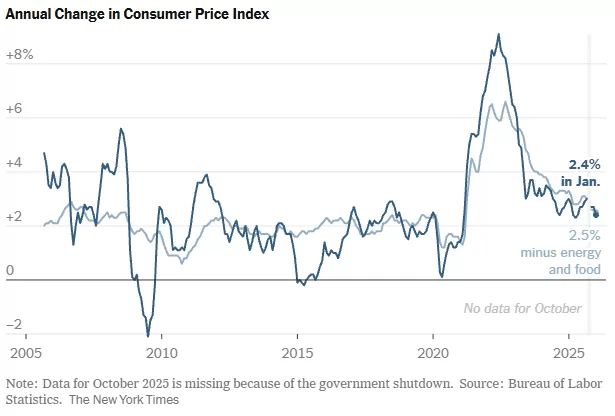

The latest economic data brings a sigh of relief for consumers and policymakers alike, as U.S. inflation has shown a more significant easing than anticipated at the beginning of the year. This positive development suggests that efforts to tame rising prices may be gaining traction, offering a glimmer of hope for greater economic stability in the months to come.

For much of the past year, inflation has been a persistent headwind, impacting everything from grocery bills to housing costs. The robust labor market, while a sign of economic strength, also contributed to upward price pressures. However, recent reports indicate a potential shift in this trend.

Several factors appear to be contributing to this welcome slowdown. Supply chain disruptions, which were a major catalyst for price increases, have largely improved. This has allowed for a more consistent flow of goods, reducing bottlenecks and associated costs. Additionally, the Federal Reserve’s aggressive monetary policy, including multiple interest rate hikes, seems to be having its intended effect of cooling demand and reining in inflationary expectations.

While the easing of inflation is certainly good news, it’s important to maintain a balanced perspective. The economy is a complex system, and various forces are constantly at play. Energy prices, geopolitical events, and shifts in consumer spending habits can all influence the trajectory of inflation. Therefore, continuous monitoring and adaptive policymaking will remain crucial.

What does this mean for the average American? For starters, it could translate into less pressure on household budgets over time. If the trend continues, we might see more stable prices for everyday goods and services, allowing purchasing power to stretch further. It also provides the Federal Reserve with more flexibility in its future policy decisions, potentially reducing the need for further aggressive rate hikes.

The journey to sustained price stability is an ongoing one, but the early signs from this year are undoubtedly encouraging. It’s a testament to the resilience of the U.S. economy and the effectiveness of concerted efforts to address inflationary pressures. As we move further into the year, economists and consumers alike will be watching closely to see if this promising trend continues, paving the way for a more predictable and stable economic environment.

Home Sales Take a January Dip: What Does It Mean for the Market?

The housing market, often a dynamic and unpredictable beast, just delivered a notable headline: home sales in January experienced their most significant monthly decline in nearly four years. This news might spark a bit of anxiety for some, and perhaps a glimmer of hope for others. But what’s truly behind this downturn, and what could it signal for the months ahead?

According to recent reports, the seasonally adjusted annual rate of existing home sales saw a substantial drop last month. This marks a notable shift after a period where the market showed some signs of stabilizing, or even modest recovery, in late 2023.

What’s Driving the Decline?

Several factors are likely at play in this January slump:

Mortgage Rate Volatility: While rates have come down from their peaks, they’ve also experienced some upward swings, creating uncertainty for prospective buyers. Higher rates directly impact affordability, pushing some buyers to the sidelines.

Persistent Inventory Shortages: Despite the dip in sales, the fundamental issue of low housing inventory remains a significant challenge in many areas. Fewer homes on the market mean less choice for buyers, and can still keep prices elevated, even with softening demand.

Seasonal Slowdown (Exacerbated): January is typically a slower month for real estate activity due to holidays and winter weather. However, the magnitude of this decline suggests more than just a typical seasonal lull. It could indicate that underlying market pressures are intensifying.

Affordability Challenges: The combination of elevated home prices and higher interest rates continues to stretch buyer budgets thin. For many, especially first-time homebuyers, the dream of homeownership remains a distant one.

Economic Uncertainty: Broader economic concerns, even if subtle, can influence consumer confidence. Worries about inflation, job security, or a potential recession can lead people to postpone major financial decisions like buying a home.

Is This the Start of a Larger Trend?

It’s crucial not to jump to conclusions based on a single month’s data. Real estate markets are complex and influenced by numerous variables. However, a decline of this magnitude certainly warrants close attention.

Potential for Price Adjustments: A sustained drop in demand, particularly if inventory levels begin to rise, could eventually lead to more significant price corrections in some markets. Buyers who have been waiting for prices to come down might see this as a positive sign.

Opportunity for Buyers? For those who are financially secure and ready to buy, a less competitive market could present opportunities. Fewer bidding wars and potentially more negotiating power could be on the horizon if the trend continues.

Impact on Sellers: Sellers might need to adjust their expectations. Pricing strategically and ensuring homes are in top condition will become even more critical in a market where buyers have more leverage.

Looking Ahead

The coming months will be telling. We’ll need to watch several key indicators:

Mortgage Rate Movements: Any significant and sustained drop in interest rates would likely bring buyers back into the market.

Inventory Levels: A notable increase in homes for sale would help alleviate pressure and potentially lead to more balanced market conditions.

Economic Data: Broader economic health, including inflation and employment figures, will continue to play a role in consumer confidence and housing demand.

While January’s numbers present a cautious start to the year for the housing market, they also highlight the ongoing adjustments and recalibrations happening. Whether this dip is a temporary blip or a harbinger of more significant changes remains to be seen, but it’s a clear reminder that the real estate landscape is always evolving.

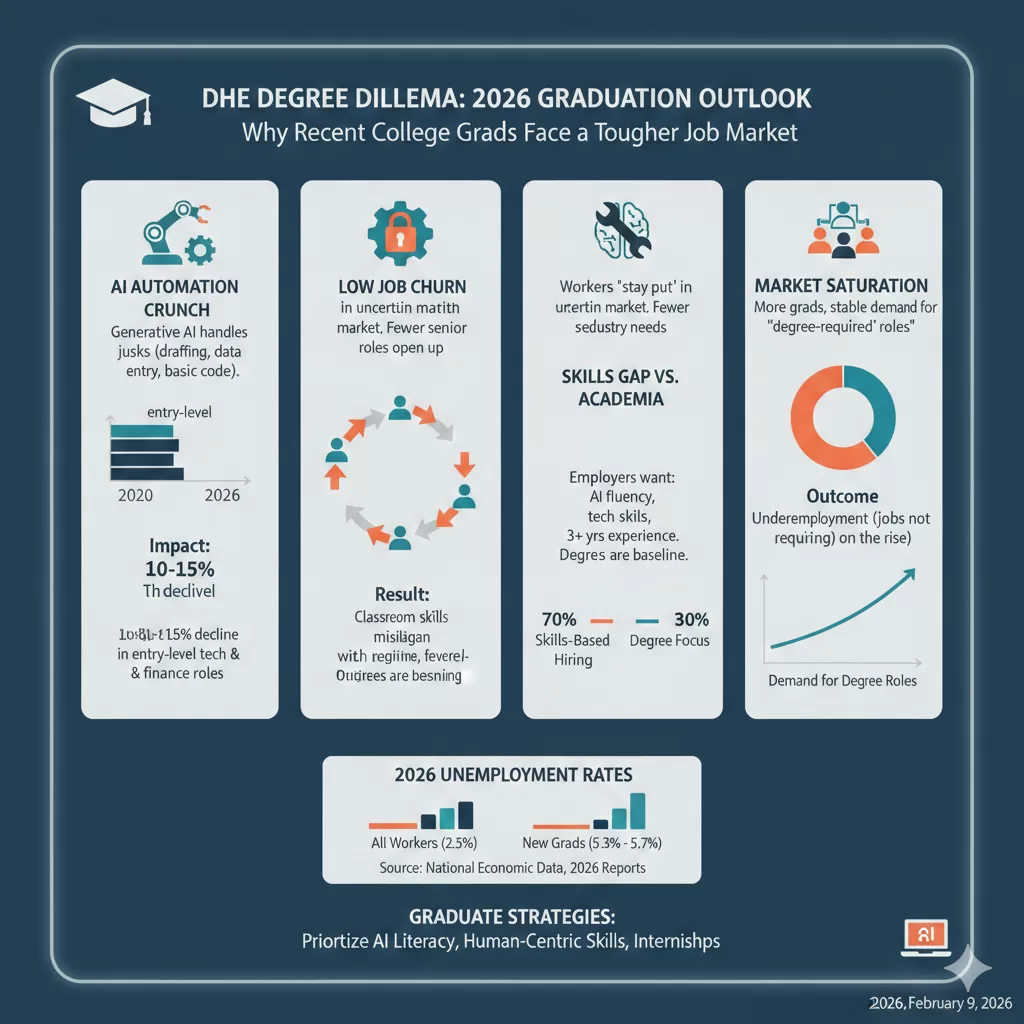

For decades, the path to employment followed a predictable script: graduate high school, earn a four-year degree, and step into a stable career. But for the Class of 2026 and other recent grads, that script has been heavily revised.

While the national unemployment rate remains relatively stable, a closer look reveals a “white-collar friction” that is hitting young graduates particularly hard. Recent data suggests that unemployment for workers aged 22–27 is significantly higher than for the general population, with some reports showing rates as high as 5.3% to 5.7% for new degree holders compared to just 2.5% for their more experienced counterparts.

Why is the “college advantage” seemingly cooling off? Here are the primary factors reshaping the entry-level landscape.

1. The “Bottom Rung” is Being Automated

Perhaps the most significant shift in 2026 is the impact of Generative AI. Historically, junior roles involved “intellectually mundane” tasks: drafting reports, organizing data, or basic coding. These were the “training wheels” of a career.

Today, AI agents handle these tasks with 90% accuracy in seconds.

The Result: Companies are becoming more “top-heavy.” They still need experienced managers to oversee AI, but they need fewer junior employees to do the legwork.

The Crunch: Entry-level hiring has seen double-digit declines in sectors like tech and finance, as firms use AI to boost productivity without expanding their headcount.

2. The Great “Stay Put” (Low Churn)

In a healthy economy, people switch jobs, creating “openings” at the bottom for new talent. In 2026, we are seeing a collapse in voluntary job switching.

“Workers are holding onto their roles because the market feels risky; as a result, the natural ‘churn’ that usually pulls recent grads into the workforce has stalled.”

When mid-level employees don’t move up or out, the entry-level pipeline remains clogged.

3. The Rising “Skills Gap” vs. Academic Focus

There is a growing disconnect between what is taught in the classroom and what is required in a modern office.

The Degree is the Baseline, Not the Finish Line: Employers are shifting toward skills-based hiring. According to NACE, 70% of employers now prioritize specific technical skills and AI fluency over the prestige of the degree itself.

Experience Over Everything: Job postings that once asked for 0–2 years of experience are increasingly demanding 3+ years or specific internships. For a recent grad, this creates the classic paradox: You can’t get the job without experience, but you can’t get experience without the job.

4. Market Saturation

We are currently seeing the result of “education-neutral” growth. The supply of college graduates has increased steadily, but demand for roles that specifically require a degree has leveled off. This has led to a rise in underemployment, where graduates find themselves in roles that don’t actually require their hard-earned credentials.

What Can Grads Do?

The market is tougher, but it isn’t closed. To stand out in the current environment, graduates must:

Prioritize AI Literacy: It’s no longer a “plus”; it’s a requirement. Show how you use AI to work faster and smarter.

Focus on “Human-Centric” Skills: Emphasize critical thinking, complex problem solving, and emotional intelligence—things AI still struggles to replicate.

Treat Internships as Essential: In 2026, an internship is often the only way to bypass the “3 years of experience” requirement.

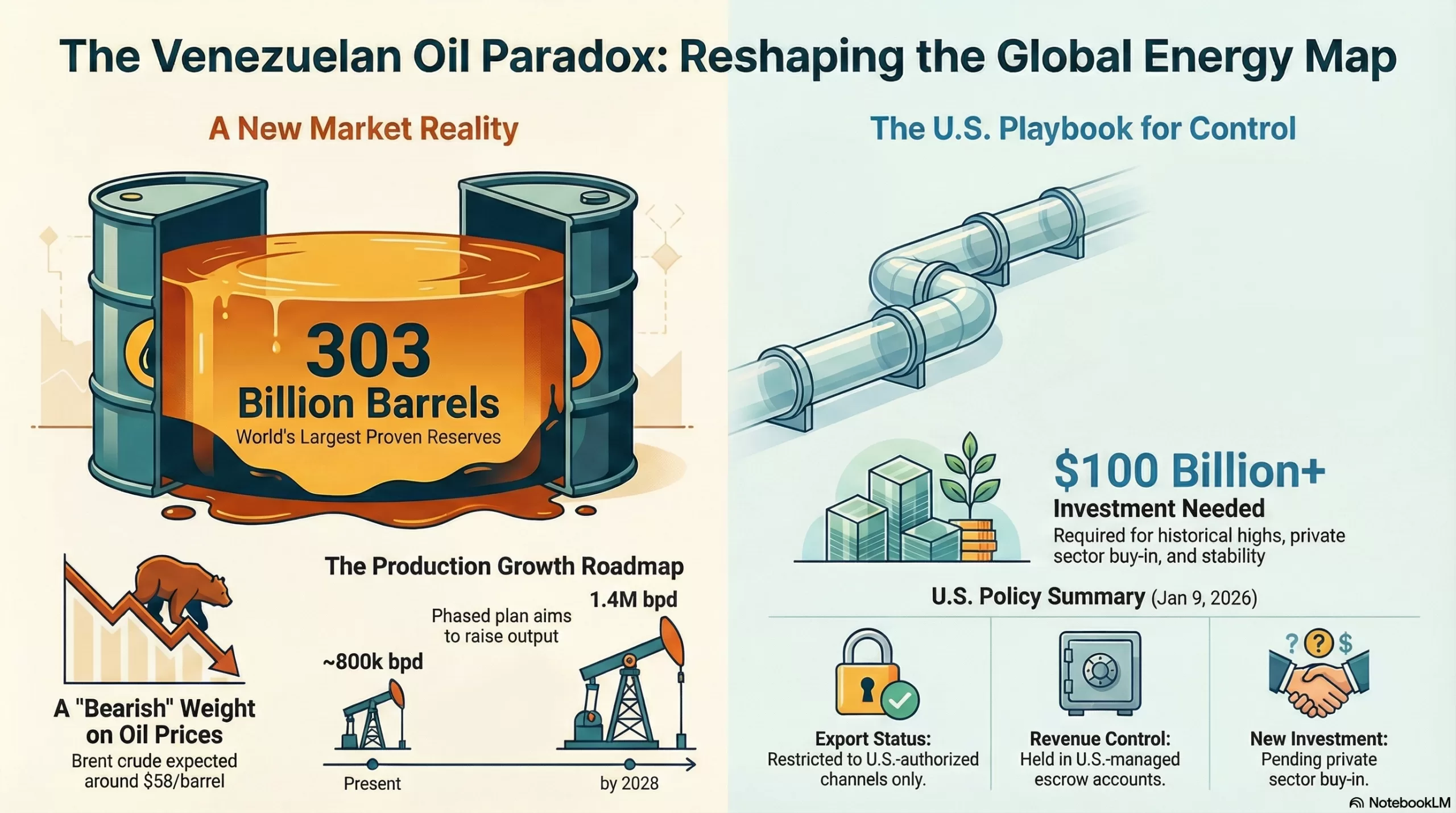

The start of 2026 has brought one of the most significant shifts in the energy sector in decades. With the recent capture of Nicolás Maduro on January 3, 2026, and the subsequent move by the U.S. administration to overhaul Venezuela’s energy infrastructure, the global oil market is facing a new “Venezuelan Paradox.”

While Venezuela holds the world’s largest proven oil reserves—estimated at over 303 billion barrels—its actual impact on the global market is currently a tug-of-war between massive long-term potential and a short-term supply glut.

1. The Immediate Shock: Volatility vs. the “Glut”

In the days following the January 3rd intervention, oil prices saw a brief “short squeeze” as traders priced in geopolitical risk, with prices nudging toward $60/barrel. However, the broader market remains in a state of oversupply.

Experts from J.P. Morgan and the IEA highlight that the market is currently facing a significant supply glut. Brent crude is forecasted to average around $58/barrel for the remainder of 2026. Because the world is already well-supplied by U.S. shale and Guyana, the return of Venezuelan barrels acts as a “bearish” weight on prices rather than a catalyst for a spike.

2. The Production Road Map: From 800k to 1.4M

As of early 2026, Venezuela’s production sits between 750,000 and 960,000 barrels per day (bpd). While the U.S. Department of Energy (DOE) is already moving to release millions of barrels of “sanctioned oil” held in floating storage, actual production growth will take time.

Short-term (End of 2026): Production could realistically ramp up to 1.1–1.2 million bpd if sanctions are selectively rolled back to allow for infrastructure repairs.

Medium-term (2027-2028): With sustained investment from firms like Chevron and others, output could hit 1.4 million bpd.

The Long Game: Reaching the historical highs of 3 million bpd is estimated to require over $100 billion in investment and at least a decade of stable governance.

3. Geopolitical Pivot: China’s Loss, the U.S. Gulf’s Gain

For years, Venezuela’s oil was the lifeblood of China’s “teapot” (independent) refineries, often sold at steep discounts to circumvent sanctions. That era is ending.

The U.S. administration has signaled that Venezuelan oil will now flow through “authorized channels,” prioritizing U.S. and Western markets. This creates a massive shift in trade flows:

U.S. Gulf Coast Refiners: These facilities were originally built to process the heavy, sour crude that Venezuela produces. They are expected to reclaim these volumes, reducing their reliance on more expensive alternatives.

China’s Response: Chinese refineries are likely to pivot toward Russian Urals or Iranian Heavy, potentially intensifying competition for those sanctioned grades.

4. The OPEC+ Balancing Act

Venezuela is a founding member of OPEC, but its production has been so low for so long that it has mostly been a “silent partner.” In response to the 2026 developments, OPEC+ has paused its planned output hikes for Q1 2026.

The group, led by Saudi Arabia and Russia, is wary of a “perfect storm”: a global slowdown combined with a sudden surge in Venezuelan exports. If Venezuela successfully rehabilitates its sector, OPEC+ may have to maintain deeper cuts for longer to prevent prices from sliding into the $40s.

The Bottom Line

The “Venezuelan effect” in 2026 is less about a sudden flood of oil and more about a reordering of the global energy map. For the first time in a generation, the “Western Hemisphere energy powerhouse” (U.S., Canada, Guyana, and Venezuela) looks like a unified block that could significantly challenge the pricing power of Middle Eastern and Russian suppliers.

For small businesses and consumers, this is generally good news. The presence of Venezuelan “upside risk” to supply acts as a ceiling for oil prices, likely keeping fuel and energy costs stable throughout the year.

The landscape for Venezuelan oil shifted dramatically following the capture of Nicolás Maduro on January 3, 2026.1 The U.S. administration has moved quickly to assert control over the sector, balancing long-term infrastructure goals with immediate market pressure.2

Here is a summary of the current U.S. policy changes and strategic directives as of January 9, 2026:

1. The “Approved Channels” Only Policy3

The U.S. has established a strict “quarantine” on all oil movements.

Controlled Sales: The Energy Department has mandated that the only oil allowed to leave Venezuela must flow through U.S.-approved channels.4

Vessel Seizures: The U.S. Coast Guard and DOJ have already begun seizing “dark fleet” tankers in the North Atlantic and Caribbean that were attempting to move sanctioned oil outside of these new channels.5

The 50M Barrel Release: Interim authorities have agreed to turn over 30 to 50 million barrels of existing storage to the U.S. for sale at market prices.6

2. Financial & Revenue Control

A central pillar of the new policy is the “purse strings” strategy:7

Escrow Accounts: Revenue from Venezuelan oil sales is being deposited into U.S.-controlled accounts at globally recognized banks.8

Disbursement: Funds are intended to be disbursed at the discretion of the U.S. government to support the “American and Venezuelan populations,” rather than the previous regime’s lieutenants.9

Conditionality: Further sanctions relief is tied to Venezuela severing all economic ties with China, Russia, Iran, and Cuba.10

3. “Selective” Sanctions Rollbacks

Instead of a broad lifting of all sanctions, the Treasury’s Office of Foreign Assets Control (OFAC) is issuing private waivers and specific licenses:11

Infrastructure Priority: Licenses are being granted specifically for the import of oil field equipment, parts, and services.12 This is designed to reverse decades of decay in the Orinoco Belt.

Diluent Imports: The U.S. is authorizing the shipment of diluents (thinners) to Venezuela, which are required to make their heavy crude liquid enough to pump through pipelines and onto tankers.13

Direct Waivers: Private trading firms are being granted specific waivers to resume purchases, provided the oil is sold to U.S.-based buyers.14

4. The “Private Sector Pivot”

President Trump is meeting with executives from ExxonMobil, Chevron, and others (as of Friday, Jan 9) to pitch a massive redevelopment plan:15

The Investment Goal: The administration is pushing for private companies to lead a $60B–$100B overhaul of the industry.

The Conflict: There is a stated policy goal of driving global oil prices down to $50/barrel.16 This creates a “profitability gap” for oil majors, who argue that the cost of extracting heavy Venezuelan crude may not be viable if prices fall that low.

Key Policy Benchmarks for 2026

Policy Area

Current Status (Jan 9, 2026)

Export Status

Restricted to U.S.-authorized channels only.

Revenue Control

Held in U.S.-managed accounts.

New Investment

Pending private sector “buy-in” and stability guarantees.

OPEC Status

Effectively suspended from quota participation during transition.

Briefing: The 2026 Venezuelan Oil Sector Transformation

Executive Summary

The capture of Nicolás Maduro on January 3, 2026, has triggered a fundamental and rapid transformation of Venezuela’s oil sector, creating what is termed the “Venezuelan Paradox.” While the nation possesses the world’s largest proven oil reserves at over 303 billion barrels, its immediate market impact is a bearish pressure on prices due to a global supply glut, rather than a price spike. The U.S. administration has swiftly implemented a strategy of direct control over Venezuela’s oil exports and revenue, mandating that all sales flow through “approved channels” and placing proceeds into U.S.-managed escrow accounts.

This strategic pivot is causing a significant reordering of the global energy map. U.S. Gulf Coast refiners, designed for Venezuelan heavy crude, are positioned to benefit, while China’s independent refineries lose a primary source of discounted oil. In response to the potential for increased Venezuelan supply, OPEC+ has paused planned output hikes, wary of a price collapse. The overarching outcome is the potential formation of a powerful, unified Western Hemisphere energy bloc (U.S., Canada, Guyana, and Venezuela) capable of challenging the pricing power of Middle Eastern and Russian suppliers. For consumers, this development is expected to act as a ceiling on oil prices, promoting stable energy costs through 2026.

1. The Venezuelan Paradox: Market Dynamics and Production Outlook

The events of early January 2026 have introduced a complex dynamic into the global oil market, defined by the conflict between Venezuela’s immense long-term potential and the immediate realities of its dilapidated infrastructure and a well-supplied global market.

Immediate Market Impact: Volatility vs. Glut

Initial Volatility: In the immediate aftermath of the January 3 intervention, oil prices experienced a brief “short squeeze” driven by geopolitical risk, temporarily pushing prices toward $60 per barrel.

Prevailing Glut: This volatility was short-lived, as the broader market remains in a state of oversupply. Analysis from J.P. Morgan and the IEA indicates a significant supply glut, reinforced by ample production from U.S. shale and Guyana.

Price Forecast: The re-entry of Venezuelan barrels is viewed as a “bearish” weight on the market. Brent crude is forecasted to average approximately $58 per barrel for the remainder of 2026.

Phased Production Roadmap

Venezuela’s current oil production stands between 750,000 and 960,000 barrels per day (bpd). A multi-stage recovery is anticipated, contingent on investment and stability.

Short-Term (End of 2026): Production could ramp up to 1.1–1.2 million bpd with selective rollbacks on sanctions to permit essential infrastructure repairs.

Medium-Term (2027-2028): Sustained investment from major firms like Chevron could elevate output to 1.4 million bpd.

Long-Term Goal: Reaching the historical peak production of 3 million bpd is a formidable challenge, estimated to require over $100 billion in capital investment and at least a decade of stable governance.

2. U.S. Strategic Control and Policy Directives

The U.S. administration has enacted a comprehensive policy framework to manage Venezuela’s oil sector, focusing on controlling exports, revenue, and the pace of redevelopment.

“Approved Channels” and Asset Control

Export Quarantine: The U.S. has instituted a strict policy mandating that the only oil permitted to leave Venezuela must move through U.S.-approved channels.

Enforcement Actions: The U.S. Coast Guard and Department of Justice have begun seizing “dark fleet” tankers in the North Atlantic and Caribbean attempting to transport sanctioned oil outside these new regulations.

Release of Stored Oil: Interim Venezuelan authorities have agreed to transfer 30 to 50 million barrels of oil from floating storage to U.S. control for sale at market prices.

Financial Controls and Sanctions Policy

A “purse strings” strategy is central to the U.S. approach, ensuring financial oversight and leveraging sanctions for policy goals.

Escrow Accounts: All revenue from authorized Venezuelan oil sales is being deposited into U.S.-controlled escrow accounts at major international banks. Funds are intended for the “American and Venezuelan populations.”

Conditional Relief: Further sanctions relief is explicitly tied to Venezuela severing all economic ties with China, Russia, Iran, and Cuba.

Selective Waivers: The Treasury’s Office of Foreign Assets Control (OFAC) is issuing private waivers and specific licenses rather than a blanket lifting of sanctions. These licenses prioritize:

Import of oil field equipment, parts, and services to repair the Orinoco Belt.

Shipment of diluents required to make Venezuela’s heavy crude transportable.

Waivers for private trading firms to purchase oil, provided it is sold to U.S.-based buyers.

The Private Sector Pivot and Investment Strategy

The U.S. is encouraging private investment to lead the sector’s revitalization, though a potential conflict exists between policy goals and corporate profitability.

Investment Goal: President Trump is actively meeting with executives from ExxonMobil, Chevron, and other firms to promote a massive redevelopment plan estimated to cost between $60 billion and $100 billion.

The Profitability Conflict: A stated administration policy goal is to drive global oil prices down to $50 per barrel. Oil majors have expressed concern that this price point may render the extraction of heavy Venezuelan crude unprofitable, creating a “profitability gap” that could hinder investment.

Key Policy Benchmarks (as of Jan 9, 2026)

Policy Area

Current Status

Export Status

Restricted to U.S.-authorized channels only.

Revenue Control

Held in U.S.-managed accounts.

New Investment

Pending private sector “buy-in” and stability guarantees.

OPEC Status

Effectively suspended from quota participation during transition.

3. Geopolitical Realignment and Global Impact

The shift in Venezuela’s oil policy is causing a significant reordering of global energy trade flows and prompting strategic recalculations by major market players.

Shifting Trade Flows: U.S. Gulf vs. China

U.S. Gulf Coast Gains: Refineries along the U.S. Gulf Coast, which were originally engineered to process Venezuela’s specific grade of heavy, sour crude, are expected to be the primary beneficiaries. They can now reclaim these volumes, reducing their dependence on more expensive alternatives.

China’s Loss: The era of China’s “teapot” (independent) refineries sourcing heavily discounted Venezuelan crude is ending. Chinese refiners are now expected to pivot toward other sanctioned grades, such as Russian Urals or Iranian Heavy, potentially increasing competition for these barrels.

OPEC+ Response and Price Stabilization

As a founding member of OPEC, Venezuela’s potential return to significant production levels presents a challenge to the cartel’s market management strategy.

Preemptive Action: In response to the developments, OPEC+ (led by Saudi Arabia and Russia) has paused its planned output hikes for Q1 2026.

Managing the “Perfect Storm”: The group is concerned about a “perfect storm” scenario where a global economic slowdown coincides with a surge in Venezuelan exports.

Future Cuts: If Venezuela successfully rehabilitates its oil sector, OPEC+ may be forced to maintain deeper and longer production cuts to prevent crude prices from sliding into the $40s per barrel range.

4. Conclusion: A New Energy Landscape

The “Venezuelan effect” in 2026 is less about an immediate flood of new oil and more about a fundamental reordering of the global energy map. For the first time in a generation, a unified “Western Hemisphere energy powerhouse”—comprising the United States, Canada, Guyana, and a revitalized Venezuela—appears poised to emerge. This bloc could significantly challenge the long-held pricing power of suppliers in the Middle East and Russia. For consumers and businesses, this shift introduces substantial “upside risk” to global supply, creating a natural ceiling for oil prices and likely contributing to stable fuel and energy costs throughout the year.

Let’s explore the potential trends in its Gross Domestic Product (GDP) growth rate throughout 2025. While no one has a crystal ball, we can analyze current trajectories, expert projections, and potential influencing factors to paint a picture of what lies ahead.

The Current Economic Pulse (Briefly looking back at late 2024)

To understand 2025, it’s crucial to acknowledge the economic momentum (or lack thereof) leading into it. We’re likely seeing a continued moderation from the robust growth experienced in the immediate post-pandemic recovery. Inflation, while hopefully tamer, will still be a key variable, influencing consumer spending and investment. Interest rates, dictated by the Federal Reserve, will also play a significant role. Let’s imagine a snapshot of the US economy as we enter 2025.

Q1 2025: A Cautious Start?

As 2025 kicks off, many economists anticipate a period of continued cautious growth. Businesses may still be adjusting to lingering supply chain complexities and a potentially tighter labor market. Consumer spending, the bedrock of the US economy, might see moderate gains, influenced by real wage growth (or lack thereof) and household savings levels. Investment in new projects could be selective, driven by a desire for efficiency and technological advancement. We might see the GDP growth rate hover in the lower to mid-2% range during this initial quarter.

Q2 2025: Finding its Rhythm

Moving into the second quarter, we could witness the economy starting to find a more stable rhythm. Factors such as potentially easing inflationary pressures and a clearer outlook on monetary policy could provide more certainty for businesses and consumers. We might see a slight uptick in manufacturing activity and continued strength in the services sector. Technological innovation, particularly in areas like AI and green energy, could begin to show more tangible contributions to productivity.

Q3 2025: Potential for Acceleration

The third quarter often provides a good indicator of annual performance, and 2025 could see some positive momentum building. If global economic conditions stabilize and major geopolitical tensions remain subdued, US exports could see a boost. Domestically, renewed consumer confidence, perhaps fueled by a strong job market and stable prices, could lead to increased discretionary spending. Business investment might also pick up as companies look to capitalize on growth opportunities. This could be a quarter where GDP growth nudges closer to the mid-2% to even 3% range. Imagine the vibrancy of a thriving economy in full swing.

Q4 2025: A Strong Finish or Continued Moderation?

The final quarter of 2025 will be crucial in determining the overall annual growth rate. Much will depend on the preceding quarters’ performance and any new unforeseen global or domestic events. A strong holiday shopping season, robust corporate earnings, and continued investment in key sectors could lead to a solid finish. However, potential headwinds like persistent inflation or unexpected global economic slowdowns could temper growth. The Federal Reserve’s stance on interest rates will also be keenly watched. The year could conclude with growth stabilizing, setting the stage for 2026.

Key Influencing Factors for 2025:

Inflation and Interest Rates: The Fed’s ability to manage inflation without stifling growth will be paramount.

Consumer Spending: The health of the consumer, driven by wages, employment, and savings, is always a critical determinant.

Business Investment: Companies’ willingness to invest in expansion, R&D, and technology will fuel future growth.

Global Economic Health: International trade and geopolitical stability will have a ripple effect on the US economy.

Technological Advancement: Innovations in AI, automation, and green technologies could boost productivity.

In conclusion, 2025 is shaping up to be a year of continued adaptation and potential growth for the US economy. While we can anticipate some fluctuations, a path of cautious yet steady expansion seems to be the prevailing view among many analysts. The resilience and dynamism of the American economy will undoubtedly be tested, but its capacity for innovation and recovery remains a powerful force.

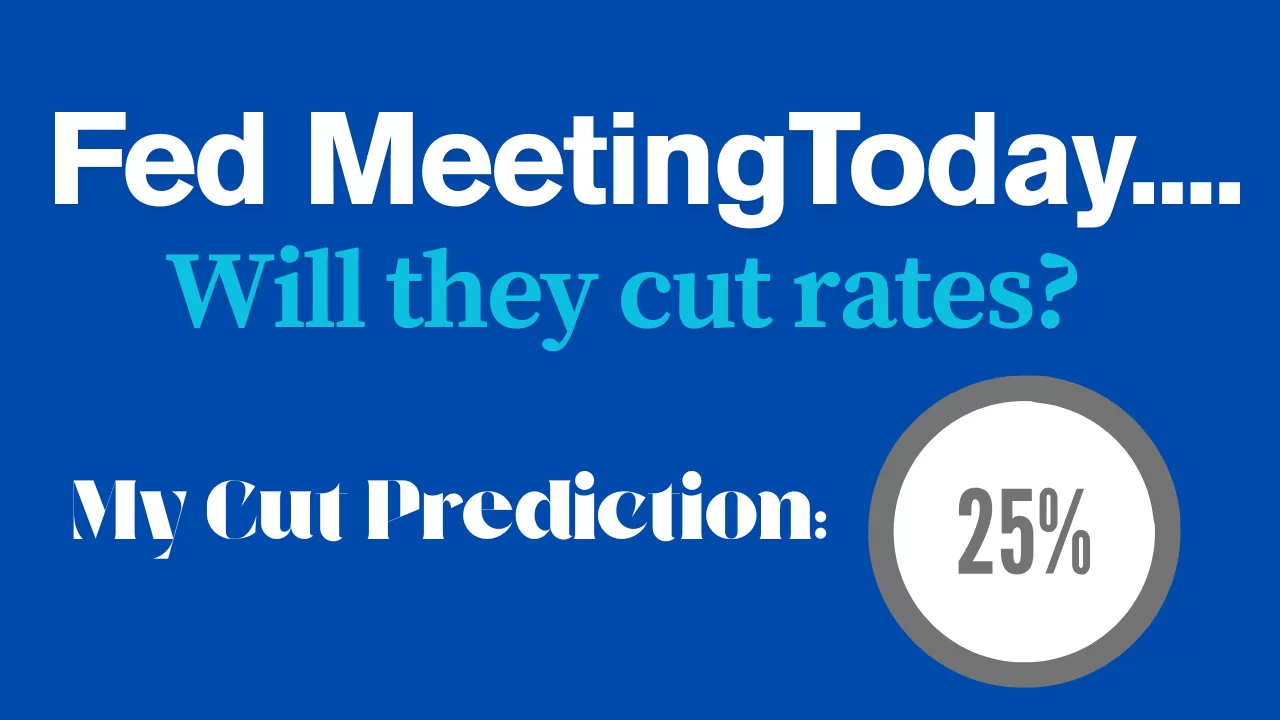

As the Federal Open Market Committee (FOMC) wraps up its final meeting of 2025 today, all eyes are on the 2:00 PM EST announcement. With the U.S. economy cooling and the labor market showing signs of strain, speculation is high that a Fed Cut in rates is imminent.

Here is a breakdown of the current predictions, the economic data driving the decision, and what odds makers are betting on.

The Consensus: A “December Cut” is Highly Likely

Market watchers are overwhelmingly pricing in a 25-basis-point (0.25%) rate cut.

According to the CME FedWatch Tool, which tracks trading in federal funds futures, there is currently an 87% probability that the Fed will lower the target range to 3.50%–3.75%. This would mark the third consecutive rate reduction, following cuts in September and October, signaling a definitive shift from fighting inflation to supporting the labor market.

Key Factors the Fed is Weighing

The Fed’s “dual mandate” requires it to balance stable prices with maximum employment. For the first time in years, the risks have shifted from overheating inflation to a cooling jobs market.

1. The Cooling Labor Market (The Primary Driver) The unemployment rate has ticked up to 4.4%, a figure that has caught the attention of Fed Chair Jerome Powell. While historically low, the steady rise suggests that high interest rates are finally biting into corporate hiring. Job growth has slowed, and layoffs in sensitive sectors have increased. The Fed is keen to avoid a “hard landing” where unemployment spikes uncontrollably.

2. Sticky but Manageable Inflation Inflation hasn’t disappeared, but it is no longer the five-alarm fire it was two years ago. The latest PCE (Personal Consumption Expenditures) data places headline inflation around 2.7%–2.9%, with core inflation hovering near 2.8%. While this is still above the Fed’s 2% target, it is trending in the right direction, giving the central bank “air cover” to cut rates to support jobs without immediately reigniting price hikes.

3. Economic Growth (GDP) GDP growth has moderated to an annualized rate of roughly 1.8%–2.0%. This suggests the economy is slowing down but not crashing—the definition of the elusive “soft landing.” A rate cut now is viewed as insurance to keep this momentum from stalling out completely in early 2026.

The “Wild Card”: A Divided Committee

Despite the high odds of a cut, this meeting is not without tension. Reports suggest the FOMC is sharply divided.

** The Doves (Cut Now):** Worried that waiting too long will cause a recession. They argue that with inflation falling, real interest rates are effectively rising, tightening financial conditions more than intended.

The Hawks (Pause/Hold): Concerned that cutting rates too quickly could cause inflation to flare up again, especially given that the economy is still growing.

Because of this division, the language in today’s statement will be just as important as the rate decision itself. Investors should look for clues about a “pause” in January. Many analysts believe the Fed may cut today but signal a skip in the next meeting to assess the impact of recent cuts.

What to Watch For

2:00 PM EST: The official statement and decision. Look for the “dot plot” (Summary of Economic Projections) to see where officials expect rates to be at the end of 2026.

2:30 PM EST: Chair Jerome Powell’s press conference. His tone regarding the “balance of risks” will move markets. If he sounds more worried about jobs than inflation, it will confirm that the easing cycle has further to go.

Bottom Line

While nothing is guaranteed until the gavel falls, the smart money is on a 0.25% cut today. The Fed likely views the rising unemployment rate as a warning light it cannot ignore, making a rate reduction the prudent move to secure a soft landing for 2026.

Category

Case for a Rate Cut (The “Doves”)

Case for Holding Steady (The “Hawks”)

Labor Market

Rising Risks: Unemployment has climbed to 4.4%. Doves argue that high rates are now doing unnecessary damage to hiring.

Hidden Strength: Some argue the job market is “normalizing” after the post-pandemic surge rather than collapsing.

Inflation

Progress Made: While at 2.8%, inflation is down significantly from its peak. High “real” rates (inflation vs. interest) are overly restrictive.

Sticky Prices: Inflation remains above the 2% target. Rate cuts could embolden businesses to keep prices high or raise them.

Economic Growth

Growth is Slowing: GDP growth has dipped toward 1.8%. A cut acts as “insurance” to prevent a recession in 2026.

Consumer Resilience: High durable goods spending suggests the economy is not yet in need of a stimulus.

Market Impact

Easing the Burden: Lower rates would provide immediate relief for credit card holders and small businesses facing high debt costs.

Asset Bubbles: Cutting too soon could overheat the stock and housing markets, leading to a boom-bust cycle.

The Federal Reserve has decided to cut the benchmark interest rate by 25 basis points (0.25%).

This move lowers the target range for the federal funds rate to 3.50% to 3.75%. This is the third consecutive rate cut this year and was made in light of elevated inflation and a weakening labor market.

Here are the key takeaways from the announcement and Chair Jerome Powell’s press conference:

✂️ Key Interest Rate Decision

The Cut: The Federal Open Market Committee (FOMC) voted to lower the target range for the federal funds rate by 25 basis points to 3.50%–3.75%.

The Vote: The decision was not unanimous, recording a 9:3 ratio of votes.

One member (Stephen I. Miran) preferred a larger, 50-basis-point cut.

Two members (Austan D. Goolsbee and Jeffrey R. Schmid) preferred no change, keeping the rate steady.

🎙️ Key Quotes and Context from Chair Powell

Powell’s remarks focused on the shifting balance of risks and the current policy stance:

Rationale for the Cut:“With today’s decision, we have lowered our policy rate three-quarters of a percentage point over our last three meetings. This further normalization of our policy stance should help stabilize the labor market while allowing inflation to resume its downward trend toward 2% once the effects of tariffs have passed through.”

The Dual Mandate Challenge: Powell acknowledged the difficulty of balancing the Fed’s two goals (maximum employment and price stability):”In the near term, risks to inflation are tilted to the upside and risks to employment to the downside—a challenging situation… We have one tool. It can’t do both of those—you can’t address both of those at once.”

Forward Guidance (What’s Next): The Fed indicated a cautious, data-dependent approach moving forward:”In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks.” When asked about a pause, Powell suggested the policy rate is now close to the “neutral” level: He indicated that the Fed’s benchmark rate is now likely somewhere close to the “neutral” level… which certainly indicates that he won’t be in a hurry to extend the string of cuts the Fed has made in recent months.

Economic Outlook and Projections (“Dot Plot”): The latest projections indicated a divided committee on future cuts.

The median Fed official is penciling in one rate cut for next year (2026), which is a more cautious outlook than some market expectations.

The Fed projects inflation (based on its preferred gauge) to ease to 2.4% by the end of 2026.

Based on the immediate market data and analyst reactions following the 2:00 PM announcement, here is how the decision is impacting mortgage rates and the stock market.

🏠 Impact on Mortgage Rates

The Verdict: Rates may hold steady or even tick up slightly, despite the Fed cutting rates.

Counter-Intuitive Movement: It often surprises borrowers, but mortgage rates do not move 1-for-1 with the Fed’s rate. Mortgage rates track the 10-year Treasury yield, which actually rose today (hitting roughly 4.21%).

Why? The market had already “priced in” this cut weeks ago. Investors are now looking ahead to 2026. Because the Fed signaled a slower pace for future cuts (a “hawkish cut”), bond markets reacted by pushing long-term yields higher.

Forecast: Experts expect 30-year fixed mortgage rates to hover in the low-to-mid 6% range for now. A significant drop below 6% is unlikely until investors see clearer signs that inflation is permanently defeated.

📈 Impact on the Stock Market

The Verdict: A “Santa Claus Rally” is likely, but 2026 looks choppier.

Immediate Reaction: The S&P 500 and Dow Jones both rose following the news, pushing close to all-time highs. The market “got what it wanted”—a cut to support the economy without panic.

Sector Watch:

Small Caps (Russell 2000): Often benefit most from rate cuts as they rely more on floating-rate debt.

Tech & Growth: Continued to show strength, though valuations remain high.

2026 Outlook: The Fed’s “dot plot” shows they plan to slow down, potentially cutting rates only once in 2026. This is fewer cuts than Wall Street hoped for, which suggests the “easy money” rally might face headwinds early next year as recession risks are still on the table (J.P. Morgan analysts cite a 35% recession probability for 2026).

Area

Short-Term Forecast (Dec ’25)

Why?

Mortgage Rates

Steady / Slight Rise

The cut was already priced in; long-term bond yields are rising.

Stocks

Bullish (Rally)

The “soft landing” narrative is intact; investors are relieved.

Savings Accounts

Slight Drop

High-yield savings rates will drop almost immediately by ~0.25%.

A government shutdown, defined as a lapse in federal appropriations, is frequently framed as a political skirmish in Washington D.C. Yet, its financial reverberations are immediately and intensely felt across the nation, striking at the heart of the U.S. economy: its small businesses. Comprising over 33 million firms and responsible for generating two-thirds of net new jobs, the small business ecosystem is the engine of American enterprise.

However, this vital sector is uniquely fragile when faced with political paralysis. A shutdown creates immediate, cascading, and disproportionate negative effects on small businesses, necessitating proactive recovery strategies from both the private and public sectors. This analysis details the mechanics of this damage—from frozen payments and suspended loans to depressed consumer spending—and outlines the essential steps small businesses must take to recover, mitigate future risk, and advocate for systemic protection.

🛑 II. Immediate and Direct Impacts of Shutdown

The moment a shutdown is triggered, the consequences for small businesses that interact directly with the federal apparatus are sudden, severe, and measurable.

The Freeze on Federal Contracts 📜

For the large segment of small businesses that operate as federal contractors, the shutdown delivers a direct financial shock:

Delayed Payments: The most critical blow is the cessation of payments, converting reliable accounts receivable into financial dead weight. Small contractors, operating on thin margins, are instantly thrust into a cash flow crisis. During the 2018-2019 shutdown, it was estimated that over 90% of federal contractor invoices went unpaid for the duration, causing thousands of small contractors to miss payroll.

Work Stoppage (Stop-Work Orders): For ongoing contracts, agencies issue stop-work orders. The business stops billing, losing revenue entirely, and must decide whether to retain specialized staff without pay or risk the loss of highly skilled talent.

Contracting Uncertainty: The entire procurement pipeline freezes. The Department of Defense (DOD) and NASA, major sources of small business contracting, halted the award of all non-essential contracts, stalling critical high-tech and defense projects.

Suspension of Critical Loans and Financial Support 💰

Small businesses rely heavily on the federal government for capital access, a lifeline that is severed during a shutdown.

SBA Loan Program Stoppage: The suspension of the SBA’s flagship loan programs—primarily the SBA 7(a) and 504 loan guarantee programs—halts guarantees. During the 2018-2019 event, the SBA stopped processing all new loan applications, estimated to have frozen approximately $2 billion in small business financing per week, crippling expansion plans nationwide.

Disaster Loan Delays: Businesses recovering from recent natural disasters also face an immediate freeze in the processing of Economic Injury Disaster Loan (EIDL) applications.

Regulatory and Licensing Paralysis 📝

For firms in regulated industries, the shutdown acts as an involuntary stop sign.

Permit and License Delays: A small craft brewery waiting for a TTB permit to launch a new product cannot proceed. The TTB’s closure in 2018-2019 created a significant backlog, delaying the opening of new breweries, wineries, and distilleries, as they could not legally bottle and sell their products.

Customs and Trade Complications: Small businesses involved in international trade can face delays in clearances and inspections required from furloughed personnel at various agencies, leading to supply chain snags.

📉 III. Indirect and Secondary Economic Impacts – Shutdown

The government shutdown rapidly produces a secondary layer of damage through channels far removed from D.C., primarily through reduced consumer spending and heightened market uncertainty.

The “Furlough Effect” on Consumer Demand 🛍️

The largest secondary impact stems from the sudden loss of income for hundreds of thousands of federal employees and non-essential contractors.

Loss of Federal Employee Income: Furloughed federal workers are placed on mandatory, unpaid leave, forcing them to drastically cut back on discretionary spending. The 35-day shutdown resulted in approximately 800,000 federal workers missing two full paychecks, translating into billions of dollars in lost spending power.

Impact on Local Economies: Businesses relying on the patronage of federal workers suffer immediately. Small restaurants and shops near federal hubs in the D.C. area, as well as businesses dependent on National Park Service tourists, reported revenue declines of 50% or more, with many having to temporarily close their doors. The lack of guaranteed back pay for contractors deepened the slump.

Financial Market and Investor Uncertainty 🏦

A shutdown injects volatility into financial and capital markets, altering the risk assessment for small businesses.

Lender Hesitation: Banks become more hesitant to underwrite new commercial loans, fearing a prolonged economic downturn. Anecdotal evidence from 2019 suggested that many community banks placed a temporary moratorium on all new small business lending until the appropriations process was resolved.

SEC Delays: Small, high-growth companies attempting to raise capital through public filings or private offerings find their efforts stalled. During the shutdown, the SEC could not process many filings, delaying the capital raises of emerging technology and biotech firms.

Data and Resource Loss 📊

Small businesses rely on accurate, timely federal data to make strategic decisions. A shutdown halts the release of critical economic intelligence.

Statistical Freeze: The cessation of data from agencies like the Bureau of Labor Statistics (BLS) and the Census Bureau leaves businesses flying blind. Key economic indicators, including reports on housing starts, retail sales, and GDP components, were delayed, forcing small business owners to make crucial expansion decisions without reliable, up-to-date data.

Loss of Free Technical Assistance: Key support networks like Small Business Development Centers (SBDCs) and the volunteer-based SCORE mentorship program often lose funding or access, cutting off cost-free assistance vital for struggling firms.

🧠 IV. Psychological and Operational Strain

The non-financial impacts inflict deep stress on owners and staff, often determining the long-term viability of the business.

Talent Exodus: Faced with prolonged unpaid leave or layoff risk, highly skilled employees often leave for stable work in the private sector, resulting in costly brain drain.

Cash Flow Crisis Management: Owners are forced into high-risk personal finance decisions. In 2019, many small business owners dependent on federal contracts revealed they had liquidated personal retirement accounts or taken out expensive home equity loans to cover their company’s payroll.

Damage to Business Reputation: The inability to fulfill contracts or meet delivery deadlines due to stop-work orders risks lost goodwill and potential exclusion from future partnership opportunities.

🛠️ V. Strategies for Small Business Recovery and Mitigation – Shutdown

The recovery phase demands proactive management, aggressive financial triage, and a fundamental reassessment of business risk.

5.1 Immediate Financial Triage: Stabilizing the Vessel

The 90-Day Cash Flow Plan (The Survival Budget): Create a hyper-detailed projection, categorizing expenses as Mission-Critical, Negotiable, or Eliminatable.

Aggressive Negotiation with Creditors: Proactively contact commercial lenders to request interest-only payments or short-term principal forbearance. In 2019, many banks, anticipating the back pay to federal workers, were quick to offer forbearance options, but contractors needed to be aggressive in requesting similar terms.

Accessing Local Capital: Immediately explore bridge loan options from local Credit Unions and CDFIs.

5.2 Re-Engaging Federal Systems and Documentation

Upon reopening, businesses must move swiftly and meticulously:

Prioritizing Re-activation: Immediately contact the Contracting Officer (CO) for a Written Resumption Order before restarting work. Be prepared to immediately re-file or re-activate stalled SBA loan applications.

Detailed Documentation: Meticulously document all incurred costs related to the shutdown. This documentation is crucial for negotiating future claims for Termination for Convenience costs.

5.3 Diversification and Risk Management: The Long-Term Shield

The most effective strategy is to ensure the business is never again so vulnerable to political instability.

Client Base Diversification: Actively work to cap federal revenue reliance (e.g., at 60-70% of total revenue) and pursue contracts with state and local governments or the private sector.

Building a Shutdown-Proof Emergency Fund: Adopt the financial discipline to build a dedicated cash reserve equal to 3 to 6 months of operational expenses. This reserve is strictly for maintaining payroll and core utilities during a non-economic disruption.

Operational Agility: Implement cross-training programs to utilize staff for internal projects if a stop-work order is issued, retaining skilled talent while maintaining some level of productivity.

5.4 Advocacy and Systemic Change

Small business owners must leverage their collective voice to push for legislative reform.

The “Wall Off” Principle: Advocate for legislation that grants Excepted Status to critical, non-political economic functions, most importantly the SBA Loan Guarantee Processing and the Payment of Existing, Obligated Federal Contractors. Shielding these functions from the appropriations fight is essential to maintaining the stability of the small business economy.

VI. Conclusion

The resilience of the small business sector is severely tested by government shutdowns. These events are not merely political theatre; they are systemic economic disruptions that destroy cash flow, erode consumer confidence, and inflict severe psychological stress on owners and employees. The 35-day shutdown of 2018-2019 provided undeniable proof that the small business community bears a disproportionate burden of political gridlock.

While recovery demands aggressive financial triage and meticulous documentation, the long-term solution lies in diversification and structural preparedness. Policymakers must recognize that failure to fund critical economic functions, even temporarily, causes an outsized and destructive ripple effect. Ensuring the continuity of SBA lending and contractor payments must be treated as a matter of essential economic stability, insulating the national engine of job creation from political gridlock.

More Than a Headline: 5 Ways a Government Shutdown Silently Cripples Main Street America

1.0 Introduction: Beyond the Beltway Drama

When the federal government shuts down, the news cycle often frames it as a distant political battle confined to Washington D.C. Yet, its financial reverberations are immediately and intensely felt across the nation, striking directly at the heart of the U.S. economy: its small businesses, the very engine of American enterprise responsible for creating two-thirds of all net new jobs.

This vital sector is uniquely and disproportionately vulnerable to the consequences of political paralysis. A shutdown creates an immediate cascade of damage that extends far beyond federal employees, impacting entrepreneurs and local economies nationwide. Here are the five most significant and surprising ways this political gridlock cripples small businesses, proving the damage is far more widespread than a headline can capture.

2.0 The Shutdown’s Ripple Effect: 5 Surprising Impacts on Small Business

2.1 Takeaway 1: The Instant Cash Flow Apocalypse

For the thousands of small businesses operating as federal contractors, a government shutdown triggers an immediate financial shock. During the 35-day shutdown of 2018-2019, an estimated 90% of federal contractor invoices went unpaid. This instantly converts reliable accounts receivable into dead weight, thrusting companies with thin margins into a severe cash flow crisis. Revenue doesn’t just get delayed—it stops entirely, as agencies issue formal “stop-work orders.” Major sources of small business contracting, like the Department of Defense (DOD) and NASA, halt the award of new projects, freezing the entire procurement pipeline and forcing owners into devastating choices, such as whether to miss payroll or attempt to retain highly skilled talent without any pay.

2.2 Takeaway 2: The $2 Billion Weekly Freeze on Ambition

A shutdown severs a critical lifeline for small businesses seeking to grow: access to capital. The Small Business Administration (SBA) is forced to suspend its flagship 7(a) and 504 loan guarantee programs. During the 2018-2019 shutdown, this stoppage was estimated to have frozen approximately $2 billion in small business financing per week. This freeze also extends to Economic Injury Disaster Loan (EIDL) applications, harming businesses already reeling from natural disasters and compounding their crisis. This number represents more than just money on hold; it signifies crippled expansion plans, delayed hiring, and stalled innovation for entrepreneurs across the country who suddenly find their ambitions on indefinite hold.

2.3 Takeaway 3: The Economic Paralysis Spreads Far From D.C.

The financial damage quickly spreads through the “Furlough Effect.” When approximately 800,000 federal workers missed two full paychecks during the extended shutdown, they were forced to drastically cut back on consumer spending. The impact on local economies was immediate and severe. Small restaurants and shops near federal hubs and businesses dependent on National Park Service tourists reported revenue declines of 50% or more. This secondary impact demonstrates how deeply intertwined Main Street is with government operations, even for businesses with no direct federal contracts.

2.4 Takeaway 4: It Puts New Ventures on Indefinite Hold

The impact extends beyond money, creating a regulatory and licensing paralysis that acts as an involuntary stop sign for new ventures. Consider a small craft brewery that has developed a new product but is waiting on a permit from the Alcohol and Tobacco Tax and Trade Bureau (TTB). When the government shuts down, the TTB closes. The brewery cannot legally bottle and sell its new product, killing entrepreneurial momentum. This specific example shows how a shutdown can delay the opening of new breweries, wineries, and distilleries entirely unrelated to government contracting, freezing the very spirit of enterprise.

2.5 Takeaway 5: The Hidden Human Cost for Owners and Employees

Beyond the financial statements, a shutdown inflicts deep psychological and operational strains. The uncertainty can trigger a “talent exodus,” as highly skilled employees leave for more stable private-sector work rather than risk prolonged layoffs. At the same time, owners are forced to take extreme personal risks to keep their businesses afloat. During the 2019 shutdown, many small business owners dependent on federal contracts revealed they had liquidated personal retirement accounts or taken out home equity loans simply to cover their company’s payroll. Finally, the inability to fulfill contracts due to stop-work orders causes lasting damage to a business’s reputation, risking lost goodwill and exclusion from future opportunities.

3.0 Conclusion: From Crisis to Resilience

Government shutdowns are not political theatre; they are systemic economic disruptions that inflict deep, lasting, and disproportionate damage on the nation’s primary job creators. While the immediate aftermath requires financial triage, the long-term solution for businesses lies in strategic preparation, including diversifying their client base and building robust emergency funds.

The 35-day shutdown of 2018-2019 provided undeniable proof that the small business community bears a disproportionate burden of political gridlock.

This repeated cycle of crisis demands a systemic solution, forcing policymakers to answer a fundamental question. It underscores the urgent need to protect the bedrock of the American economy from political instability. How can we insulate essential economic functions, like SBA lending and contractor payments, from future political gridlock to protect the engine of our economy?

The Economic Impact of Government Shutdowns on U.S. Small Businesses

Executive Summary

A government shutdown, or a lapse in federal appropriations, inflicts immediate, severe, and disproportionate harm on the U.S. small business sector—an ecosystem of over 33 million firms responsible for generating two-thirds of net new jobs. The financial repercussions extend far beyond political centers, creating a cascade of negative effects that destabilize this vital engine of the American economy.

The 35-day shutdown of 2018-2019 serves as definitive proof of this vulnerability, where an estimated $2 billion in small business financing was frozen per week due to the suspension of Small Business Administration (SBA) loan processing. During this period, over 90% of federal contractor invoices went unpaid, thrusting thousands of firms into a cash flow crisis. The shutdown’s impact is multifaceted, manifesting as direct financial shocks, indirect economic downturns, and severe operational strains.

Key Impacts Include:

Direct Financial Disruption: Federal contractors face an immediate freeze on payments and stop-work orders. Access to critical capital through SBA loan programs (7(a), 504) is severed, and regulatory processes, such as TTB permits for breweries and wineries, are halted.

Secondary Economic Damage: The furloughing of federal workers—approximately 800,000 during the 2018-2019 event—triggers a sharp decline in consumer spending, with local businesses reporting revenue drops of 50% or more. Market uncertainty causes banks to hesitate on lending and stalls capital-raising efforts at the SEC.

Operational and Psychological Strain: The crisis forces owners into high-risk personal financial decisions, such as liquidating retirement accounts to make payroll. It also triggers an exodus of skilled talent and damages business reputations.

Recovery requires immediate financial triage, proactive creditor negotiation, and meticulous documentation for future claims. However, long-term survival hinges on strategic diversification to reduce reliance on federal revenue (capping it at 60-70%) and building a robust emergency cash reserve of 3-6 months. Ultimately, the analysis advocates for systemic reform through legislation that would “wall off” critical economic functions, such as SBA loan processing and contractor payments, from political appropriations battles to ensure national economic stability.

——————————————————————————–

1. The Anatomy of a Shutdown’s Impact

Government shutdowns are systemic economic disruptions that deliver measurable damage through direct, indirect, and operational channels. The small business sector is uniquely fragile and bears a disproportionate burden of the consequences of political gridlock.

1.1. Direct Financial and Operational Shocks

The most immediate consequences are felt by businesses that interact directly with the federal government for contracts, financing, or regulatory approval.

Impact Area

Mechanism of Harm

2018-2019 Shutdown Case Data

Freeze on Federal Contracts

Delayed Payments: Reliable accounts receivable become financial dead weight, creating an instant cash flow crisis for contractors operating on thin margins. <br> Stop-Work Orders: Agencies halt ongoing contract work, stopping all revenue streams and forcing difficult staffing decisions.

Over 90% of federal contractor invoices went unpaid, causing thousands of small contractors to miss payroll. The DOD and NASA halted all non-essential contract awards.

Suspension of Financial Support

SBA Loan Stoppage: The suspension of the SBA’s 7(a) and 504 loan guarantee programs cuts off a critical lifeline for capital access. <br> Disaster Loan Delays: The processing of Economic Injury Disaster Loan (EIDL) applications is frozen.

The SBA stopped all new loan processing, freezing an estimated $2 billion in small business financing per week, crippling nationwide expansion plans.

Regulatory Paralysis

Permit and License Delays: Businesses in regulated industries cannot proceed with new products or operations. <br> Trade Complications: Furloughed personnel cause delays in customs clearances and inspections, creating supply chain disruptions.

The closure of the Alcohol and Tobacco Tax and Trade Bureau (TTB) created a significant backlog, delaying the opening of new breweries, wineries, and distilleries.

1.2. Indirect Economic Reverberations

The shutdown’s impact quickly radiates outward, depressing the broader economy through reduced spending, market volatility, and a loss of critical data.

The “Furlough Effect” on Consumer Demand: The furloughing of federal workers and non-essential contractors removes billions of dollars from the economy.

During the 35-day shutdown, approximately 800,000 federal workers missed two full paychecks.

This led to a drastic cutback in discretionary spending, causing small businesses near federal hubs and National Parks to report revenue declines of 50% or more.

Financial Market and Investor Uncertainty: Political paralysis creates economic volatility, making lenders more risk-averse.

Anecdotal evidence from 2019 suggests many community banks placed a temporary moratorium on new small business lending.

The Securities and Exchange Commission (SEC) could not process many filings, delaying capital raises for emerging technology and biotech firms.

Loss of Data and Resources: The halt in the release of federal data forces businesses to make strategic decisions without critical intelligence.

Agencies like the Bureau of Labor Statistics (BLS) and the Census Bureau delayed key economic indicators on retail sales, housing starts, and GDP components.

Federally funded support networks like Small Business Development Centers (SBDCs) and the SCORE mentorship program lost access or funding, cutting off free assistance.

1.3. Psychological and Operational Strain

Beyond the financial metrics, a shutdown imposes severe non-financial burdens that can determine a business’s long-term viability.

Talent Exodus: Highly skilled employees, facing layoff risks or unpaid leave, often seek more stable employment in the private sector, resulting in a costly “brain drain.”

Cash Flow Crisis Management: Owners are forced into high-risk personal financial decisions. During the 2019 shutdown, many small business owners reported liquidating personal retirement accounts or taking out expensive home equity loans to cover company payroll.

Damage to Business Reputation: Inability to fulfill contracts due to stop-work orders can damage goodwill with partners and risk exclusion from future opportunities.

2. A Framework for Recovery and Resilience

Recovery from a government shutdown requires a combination of immediate financial triage and long-term strategic adjustments to mitigate future risk.

2.1. Immediate Recovery Actions

Once government operations resume, small businesses must act swiftly and methodically to stabilize their finances and restart operations.

Financial Triage:

The 90-Day Cash Flow Plan: Develop a detailed “survival budget” that categorizes all expenses as Mission-Critical, Negotiable, or Eliminatable.

Aggressive Creditor Negotiation: Proactively contact lenders to request short-term forbearance or interest-only payments.

Access Local Capital: Explore bridge loan options from local Credit Unions and Community Development Financial Institutions (CDFIs).

Re-Engaging Federal Systems:

Prioritize Re-activation: Immediately contact the relevant Contracting Officer (CO) to obtain a Written Resumption Order before restarting any work.

Document Everything: Meticulously document all shutdown-related costs. This is crucial for negotiating any future claims for “Termination for Convenience” costs.

2.2. Long-Term Mitigation and Risk Management

The most effective strategy is to build a business model that is fundamentally less vulnerable to political instability.

Client Base Diversification: Actively work to reduce reliance on federal contracts by pursuing clients in the private sector or at the state and local government levels. The recommended target is to cap federal revenue reliance at 60-70% of total revenue.

Shutdown-Proof Emergency Fund: Build and maintain a dedicated cash reserve equivalent to 3 to 6 months of essential operational expenses (payroll, core utilities). This fund should be reserved strictly for non-economic disruptions.

Enhance Operational Agility: Implement staff cross-training programs. This allows employees to be repurposed for internal projects during a stop-work order, retaining skilled talent while maintaining productivity.

3. Proposed Systemic Reforms: The “Wall Off” Principle

To prevent future economic damage, small business owners are encouraged to advocate for legislative reforms that insulate core economic functions from political gridlock. The central proposal is the “Wall Off” principle, which calls for legislation that grants “Excepted Status” to critical, non-political economic functions. This would ensure their continuity during a lapse in appropriations.

The two most critical functions to be shielded are:

SBA Loan Guarantee Processing: To maintain the flow of capital to small businesses.

Payment of Existing, Obligated Federal Contractors: To prevent immediate cash flow crises for firms that have already performed work.

Treating the continuity of these functions as a matter of essential economic stability is paramount to protecting the national engine of job creation.

Federal Reserve Monetary Policy and Leadership Outlook

Executive Summary

The Federal Reserve has implemented its second consecutive monthly interest rate cut, lowering the target range by a quarter-point to 3.75%-4.0%. The 10-2 vote by the Federal Open Market Committee (FOMC) highlights internal division among policymakers regarding the path of monetary policy, a decision made amidst sustained pressure from President Donald Trump for more aggressive easing. The outlook for future cuts remains uncertain, complicated by an ongoing federal government shutdown that has postponed the release of critical economic data on inflation and unemployment. Despite this data blackout, investor sentiment currently favors another quarter-point reduction in December, supported by recent private-sector reports indicating a “softening” labor market. Concurrently, the administration is actively considering a successor for Fed Chair Jerome Powell, whose term expires in May 2026, with a list of five candidates being prepared for the President’s review.

——————————————————————————–

I. October 2025 Interest Rate Decision

The Federal Open Market Committee (FOMC) voted on Wednesday, October 29, 2025, to lower its benchmark interest rate, marking the second straight month of monetary easing.

Rate Adjustment: The committee approved a quarter-point reduction.

New Target Range: The interest rate is now set to a range between 3.75% and 4.0%.

Previous Target Range: This is down from the 4.0% to 4.25% range established at the previous month’s meeting.

Committee Vote: The decision passed with a 10-2 vote, indicating some dissent among policymakers regarding the move.

II. Influencing Factors and Economic Context

The Fed’s decision-making process is being influenced by a combination of political pressure, economic data limitations, and emerging concerns about the labor market.

A. Political Pressure

The rate cut follows months of public pressure and criticism from President Donald Trump.

The President has been advocating for steeper and more aggressive cuts to monetary policy.

B. Economic Data Blackout

An ongoing federal government shutdown has significantly hampered the Fed’s ability to assess the U.S. economy’s health.

Key economic reports, including those on inflation and unemployment, have been postponed.

Fed Governor Christopher Waller acknowledged the challenge, stating that because policymakers “don’t know which way the data will break on this conflict,” the FOMC must “move with care” when adjusting rates.

In the absence of official data, Waller noted he has spoken with “business contacts” to help form his economic outlook.

C. Labor Market Concerns

Fed Governor Christopher Waller indicated his focus has shifted from inflation to a “softening” labor market, a stance that supported his vote for the recent rate cut.

This view is corroborated by reports from several firms and economists released in recent weeks, which suggest the labor market has continued to deteriorate. This emerging private-sector data could provide the FOMC with a rationale for an additional rate cut.

III. Future Monetary Policy Outlook

Market expectations are leaning towards further easing, though Fed officials have previously expressed division on the matter.

Investor Expectations: According to CME’s FedWatch tool, investors are favoring an additional quarter-point interest rate reduction at the FOMC’s final 2025 meeting in December.

Potential December Rate: Such a cut would lower the target range to between 3.5% and 3.75%.

Official Division: Minutes from the previous month’s meeting showed that Fed officials were divided on whether a third rate cut in the year would be necessary.

IV. Federal Reserve Leadership Transition

The administration is actively planning for the future leadership of the central bank as the end of Chair Jerome Powell’s term approaches.

Chair’s Term: Jerome Powell’s term as Federal Reserve Chair is set to expire in May 2026.

Succession Plan: Treasury Secretary Scott Bessent confirmed on Monday that a list of candidates to succeed Powell would be presented to President Trump shortly after Thanksgiving.

Candidate Shortlist: Bessent identified five individuals currently under consideration for the role:

Four Cracks in the Foundation: What the Fed’s Rate Cut Really Reveals

Introduction: Beyond the Headlines

The Federal Reserve has cut interest rates for the second straight month, a headline that suggests a confident response to evolving economic conditions. But simmering beneath the surface are the persistent calls for even easier monetary policy from the White House, adding a layer of political drama to an already difficult decision.

A closer look reveals that this rate cut is not a confident step forward; it’s a hesitant move by a divided committee flying blind in a political storm. The real story isn’t the cut itself, but the four converging pressures that expose a deeper crisis of confidence inside our nation’s central bank. But what’s really happening behind those closed doors?

This analysis breaks down the four most impactful and surprising takeaways from the Federal Reserve’s latest move, revealing a clearer picture of the profound challenges shaping U.S. economic policy today and the volatility that may lie ahead.

1. The Fed is Divided: This Was Not a Unanimous Decision

The Federal Open Market Committee (FOMC) voted to lower its key interest rate by a quarter-point, setting the new range between 3.75% and 4%, down from the previous 4% to 4.25%. The critical detail, however, was the 10-2 vote. This rare public dissent reveals deep fractures in the FOMC’s consensus about the path forward.

For markets and businesses, a divided Fed is an unpredictable Fed. This lack of consensus makes it significantly harder to forecast future policy, injecting a fresh dose of potential volatility into the economy. This internal disagreement is hardly surprising, given that policymakers are being forced to navigate without their most trusted instruments.

2. Flying Blind: The Fed is Making Decisions Without Key Data

Compounding the internal division is a startling “data blackout.” An ongoing federal government shutdown has postponed the release of official reports on inflation and unemployment—the two most vital metrics the central bank relies on. This data vacuum forces the Fed to make billion-dollar decisions in a veritable fog.

Policymakers are left to rely on alternative, anecdotal evidence. Fed Governor Christopher Waller noted he has been speaking with “business contacts” to form his economic outlook. While necessary, this reliance on informal data is fraught with risk. It lacks statistical rigor, is potentially biased, and dramatically increases the danger of a policy misstep. As Governor Waller himself acknowledged, this precarious situation demands extreme caution.

…because policymakers “don’t know which way the data will break on this conflict,” the FOMC would “need to move with care” when adjusting interest rates.

3. The Focus is Shifting: A “Softening” Labor Market is the New Top Concern

For months, inflation has been the Fed’s primary dragon to slay. Now, a monumental shift is underway. Fed Governor Christopher Waller recently stated his focus has pivoted from inflation to the “softening” labor market.

The significance of this pivot cannot be overstated. It signals that the Fed’s tolerance for inflation may be increasing if the alternative is rising unemployment. This represents a critical change in the central bank’s risk assessment, prioritizing job preservation over absolute price stability for the first time in this cycle. With recent reports from private firms suggesting the labor market has continued to deteriorate, the committee may find the justification it needs for another cut in December.

4. Political Pressure and a Looming Leadership Change

The Fed’s internal challenges are amplified by significant external pressures, most notably from President Donald Trump, who has been publicly demanding “steeper cuts.” This external pressure from the White House further complicates the internal debates, potentially widening the rift between committee members who prioritize preemptive action and those who advocate for patience.

This political context is intensified by an impending leadership transition. Fed Chair Jerome Powell’s term expires in May 2026, and the conversation about his successor has already begun. Treasury Secretary Scott Bessent has confirmed five candidates are under consideration:

Fed Governor Christopher Waller

Fed Governor Michelle Bowman

Former Fed Governor Kevin Warsh

National Economic Council Director Kevin Hassett

BlackRock executive Rick Rieder

Conclusion: Navigating in a Fog

The Federal Reserve’s latest interest rate cut is not a sign of clear sailing but rather a reflection of an institution navigating through a dense fog. Plagued by internal fractures, a critical lack of official economic data, and persistent political pressure, the central bank is operating under an extraordinary degree of uncertainty. This complex reality is far more revealing than the simple headline of another rate cut.

With the economy’s true health obscured by a data blackout, can the divided Fed steer us clear of a downturn, or is more volatility inevitable?

The Fed’s Big Move: What an Interest Rate Cut Means for You and the Economy

Introduction: Demystifying the Fed’s Power

The Federal Reserve is one of the most powerful economic forces in the United States, and its decisions can ripple through the entire country. The purpose of this article is to explain, in plain language, what the Federal Reserve is, why it changes interest rates, and what its most recent decision means for the economy. At the heart of these critical decisions is a small but influential group known as the FOMC.

1. Who Decides? Meet the FOMC

The Federal Open Market Committee (FOMC) is the part of the Federal Reserve that votes on the nation’s monetary policy, including whether to raise or lower interest rates. Their decisions, however, are not always unanimous. The most recent vote, for instance, was 10-2, which shows that there can be differing opinions among the committee members on the best path forward for the economy.

Now that we know who makes the decision, let’s examine the specific action they took.

2. The Main Event: A Quarter-Point Rate Cut

The FOMC recently voted to lower its key interest rate. This marks the second straight month that the central bank has decided to ease its monetary policy.

Here is a clear breakdown of the change:

Previous Rate Range

New Rate Range

4% to 4.25%

3.75% to 4%

This “quarter-point” reduction simply means the rate was lowered by 0.25%. But a small change like this signals a significant shift in the Fed’s thinking, which leads to a crucial question: why did they make this change?

3. The ‘Why’ Behind the Cut: A Softening Economy

The primary reason for the rate cut is that policymakers are concerned about a “softening” labor market.

Fed Governor Christopher Waller highlighted this concern, indicating his focus had shifted to a “softening” labor market instead of inflation. His viewpoint is supported by recent data; reports from various firms and economists suggest that the labor market has “continued to deteriorate,” which could provide the FOMC with the evidence it needs to support an additional cut in the future.

Of course, not everyone agrees on the Fed’s actions or what should happen next.

4. A Contentious Decision: Different Views on the Economy

The Federal Reserve’s decisions are often the subject of intense debate and are made under significant outside pressure. The latest rate cut is no exception, with several competing viewpoints at play.

President Trump’s View: The President has been a vocal critic, applying pressure on the Fed and calling for “steeper cuts” to interest rates.

Internal Division: The 10-2 vote demonstrates a lack of consensus within the FOMC itself. Last month, Fed officials appeared “divided over whether to cut rates for a third time this year,” underscoring this internal disagreement.

A Data Dilemma: The Fed is facing a major challenge due to an “ongoing federal government shutdown,” which has postponed the release of key reports on inflation and unemployment. This data blackout has forced policymakers like Governor Waller to rely on conversations with their “business contacts” to form an outlook on the economy.

These debates and challenges naturally lead to questions about what the Federal Reserve might do in the future.

5. What Happens Next? Reading the Tea Leaves