If the global economy feels like a high-wire act lately, you aren’t alone. We are currently navigating a “polycrisis“—a fancy term for when multiple major headaches (inflation, geopolitical tension, and shifting labor markets) all hit the fan at the same time.

We are standing on a narrow ledge. One side leads to a hard landing; the other leads to a stabilized “new normal.” Here is a look at the forces threatening to push us off, and the safety nets that might just pull us back.

The Push: What Could Tip Us Over?

It doesn’t take a wrecking ball to cause a recession; sometimes, it just takes a few well-placed dominos. Here are the primary risks:

The “Higher for Longer” Fatigue: While central banks use interest rates to cool inflation, keeping them elevated for too long puts immense pressure on household debt and corporate margins. If the “lag effect” hits all at once, consumer spending—the engine of the economy—could stall.

Geopolitical Aftershocks: Energy prices are notoriously sensitive to global conflict. Any significant escalation in major trade corridors can reignite supply chain chaos, sending the cost of goods back into the stratosphere.

The Commercial Real Estate Ghost Town: With remote work now a permanent fixture, many office buildings are sitting half-empty. As these property loans come due for refinancing at higher rates, we could see a localized banking tremor.

The Pull: What Could Help Us Pull Through?

It’s not all doom and gloom. There are several structural “muscles” keeping the economy upright:

The Resilient Labor Market: Despite tech layoffs making headlines, overall unemployment remains historically low. As long as people have jobs, they tend to keep spending, which provides a powerful floor for the economy.

The Productivity “AI Bump”: We are at the beginning of a massive technological shift. Early adoption of generative AI is already beginning to streamline workflows and reduce operational costs, which could lead to a non-inflationary growth spurt.

Household Balance Sheets: Unlike the 2008 crash, many consumers and corporations locked in low interest rates years ago. This “debt buffer” has bought the private sector time to adjust to the new economic reality.

The Bottom Line: Balance, Not Freefall

The economy isn’t necessarily “broken,” but it is transitioning. We are moving away from an era of “free money” and into an era where efficiency and strategic investment matter again.

Scenario

Key Driver

Likely Outcome

The Hard Landing

Persistent inflation + high rates

Brief but sharp recession; rising unemployment.

The Soft Landing

Controlled cooling + tech growth

Flat growth for a year, followed by a steady recovery.

The No Landing

Continued high spending

Economy stays hot, but rates stay high indefinitely.

The Takeaway: While the ledge is narrow, the path across is still visible. Navigating the next twelve months will require agility from policymakers and patience from investors. We may be on the edge, but we aren’t over it yet..

(March 19, 2026) Versant Funding LLC is pleased to announce that it has funded a $5 Million non-recourse factoring facility to a 90+ year-old company that provides services to major consumer brands.

After acquisition by a Private Equity Group, our latest client’s new management team implemented a turnaround plan which required additional cash. While the company was in the process of applying for an asset-based line of credit, time was of the essence and a funding date for the ABL facility was uncertain.

“Versant can fund faster than most traditional financing sources because we focus solely on the credit quality of our clients’ customers and do not perform a full underwriting or audit of the business” according to Chris Lehnes, Business Development Officer for Versant Funding, and originator of this financing opportunity. “Since this company’s customers include some of the world’s strongest consumer brands, we quickly approved the transaction and were ready to fund in about a week.”

Versant Funding’s custom Non-Recourse Factoring Facilities have been designed to fill a void in the market by focusing exclusively on the credit quality of a company’s accounts receivable. Versant Funding offers non-recourse factoring solutions to companies with B2B or B2G sales from $100,000 to $30 Million per month. All we care about is the credit quality of the A/R. To learn more contact: Chris Lehnes |203-664-1535 | chris@chrislehnes.com

The first few warm days of spring mean flowers, baseball, and for many small business owners in March 2026, the annual financial checkup. If you’ve looked at your numbers and realized you need a cash injection for new equipment, that third location, or an aggressive inventory build, you know the drill: It’s time to find the capital. While large national banks are the obvious choice, they are often difficult, impersonal, and slow. By comparison, credit unions have become the unexpected superstars of commercial lending, especially for small and medium-sized enterprises (SMEs).

If you are hunting for a business loan this month, you need to understand why credit unions are dominating and how to find the one that will actually make that critical “yes” happen for your business.

The Not-So-Secret Advantage of the Member-Owner

To understand why credit unions often beat banks on business lending, you have to look at their structure.

Banks answer to shareholders who demand profits and high returns on equity. Every decision, including who gets a loan, is filtered through the lens of maximizing shareholder value.

Credit unions, however, are not-for-profit cooperatives. They do not have public stock. Their members (you, me, and other account holders) are the owners.

This single difference ripples through every interaction. For business lending in 2026, it means:

1. Rates and Fees That Just Make More Sense: Instead of returning profit to Wall Street, credit unions reinvest earnings back into the institution and their members. This often manifests as lower interest rates on commercial loans and significantly lower loan-origination and maintenance fees. In 2026, when inflation has been a recent headache, a difference of 0.5% on a large loan term can mean thousands of dollars saved.

2. Hyper-Local Expertise: When you sit down with a commercial lender at a bank, their rules, algorithms, and models might be set at headquarters 2,000 miles away. They may not understand the specific micro-market in Newtown, Connecticut, where you are operating. But your local credit union officer lives here. They understand why opening a second pizza parlor on the new development is a smart bet, not a risky venture. They lend based on local market knowledge.

3. Relationships Over Risk-Scores: A bank will look at your credit score and financial statements, enter them into a model, and receive a automated “Approve” or “Deny.” Credit unions, especially smaller, focused ones, prioritize relationships. They are more likely to have a real human look at your complete business plan, understand your unique vision, and listen to the story behind your application, not just the numbers on the page.

The “New Reality” of SBA Lending

One of the most important developments in 2026 is that the Small Business Administration (SBA) has made it significantly easier and faster for credit unions to facilitate SBA 7(a) and 504 loans.

For many small businesses, these government-backed loans are the Holy Grail: long terms, lower interest rates, and lower down-payment requirements. Previously, massive banks dominated this space because the paperwork was crushing.

However, the “Streamline and Connect Act” of 2024 (as we projected) drastically simplified the SBA application process and created digital interfaces specifically designed for smaller community financial institutions.

This means that in March 2026, the local credit union you never expected to handle an SBA application is now a Preferred Lender, capable of getting your government-backed loan approved in weeks, not months.

How to Evaluate a Credit Union in March 2026

You can’t just walk into the nearest credit union and expect a perfect loan offer. To find the “best” one for your business right now, you must be strategic:

Step 1: Membership Criteria (The Gateway)

Credit unions can’t just lend to anyone. They operate under a specific “field of membership” (FOM). While some have broadened their charters, many are still strictly limited. To find the “best,” you must find the one you can actually join.

Geographic FOM: Are you eligible because your business is located in Newtown, CT, or the surrounding county? This is the most common path.

Associational or Professional FOM: Are you a veteran? An educator? A first responder? A member of a specific local church or union? There are niche credit unions specialized for these groups, and they often offer highly beneficial industry-specific lending programs.

Step 2: Technology and Speed

While personal relationships are the hallmark of credit unions, it’s 2026. You should not have to wait 30 days for a response to your application. A strong, business-friendly credit union will have a fast, streamlined digital application portal.

They should have digital tools that connect directly to your accounting software (like QuickBooks or Xero), allowing their lenders to instantly verify your cash flow without forcing you to hunt down piles of paper bank statements. If a credit union’s website looks like it hasn’t been updated since 2018, that is a massive red flag.

Step 3: Ask About Specific Business Expertise

The credit union that is excellent for a car loan or a personal mortgage is not necessarily the best choice for a $500,000 commercial line of credit to finance inventory for a manufacturing business.

When you interview a prospective credit union, ask about their experience in your industry. A credit union that specializes in healthcare practice lending will have different perspectives and better loan structures than one that primarily works with general contractors.

The March 2026 Takeaway: Don’t Lead with a Bank

Your default shouldn’t be the massive financial conglomerate that you can only reach via an 800-number. Your first stop in 2026 should be your local, community-focused credit union. They are built to serve owners like you, and they have the tools and local knowledge to help your business take flight this spring.

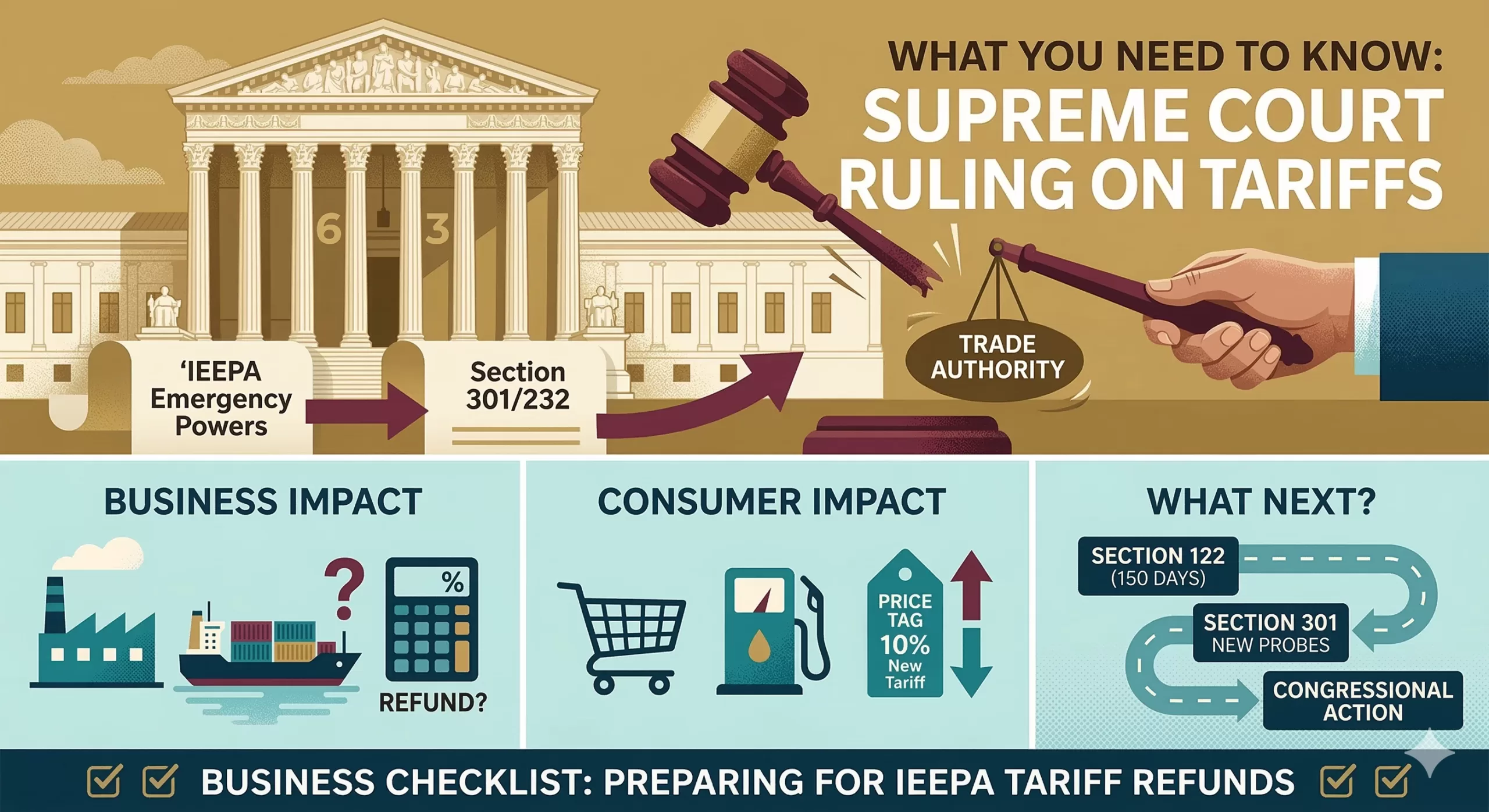

In a landmark decision that has reshaped the landscape of IEEPA Tariffs and American trade policy, the Supreme Court recently issued a ruling in Learning Resources, Inc. v. Trump. The 6-3 decision struck down a series of sweeping tariffs, delivering a significant blow to the administration’s use of emergency powers to regulate the economy.

If you’re a business owner, importer, or simply a consumer wondering why prices are shifting again, here is everything you need to know about this historic ruling about IEEPA Tariffs and what comes next.

The Heart of the Case: IEEPA Tariffs vs. The Taxing Power

The central question before the Court was whether the International Emergency Economic Powers Act (IEEPA) of 1977 gives the President the authority to impose tariffs.

The administration had used IEEPA to levy “reciprocal tariffs” and “trafficking tariffs” on products from China, Canada, and Mexico, arguing that trade imbalances and border security issues constituted a national emergency. However, the Supreme Court ruled that:

Tariffs are Taxes: Chief Justice John Roberts, writing for the majority, emphasized that the power to tax—which includes tariffs—belongs exclusively to Congress under Article I of the Constitution.

“Regulate” is not “Tax”: The Court held that IEEPA’s authority to “regulate importation” does not mean the President can unilaterally set tax rates

The Major Questions Doctrine: The Court applied this principle, stating that if Congress intended to delegate such massive economic power to the Executive Branch, it would have said so clearly and explicitly.

“The Framers did not vest any part of the taxing power in the Executive Branch,” wrote Chief Justice Roberts.

What Happens to the Money? The Refund “Mess”

One of the most pressing questions for businesses is the status of the billions of dollars already collected. Since 2025, the government has gathered an estimated $133 billion to $200 billion in IEEPA-based tariffs.

Court of International Trade (CIT) Action: Following the Supreme Court ruling, the CIT has ordered U.S. Customs and Border Protection (CBP) to begin preparing for a massive refund process.

The “Mess” Factor: Justice Brett Kavanaugh noted in his dissent that issuing these refunds will be a “mess.” It remains unclear exactly how and when businesses will see that money returned, as the Supreme Court did not provide a specific roadmap for the refund process

The Administration’s Pivot: Section 122 and 301

If you thought this ruling meant the end of tariffs, think again. Within hours of the decision, the administration began moving to alternative legal authorities:

Section 122 (Trade Act of 1974): The President implemented a temporary 10% global baseline tariff under this law. However, this power is limited to 150 days and a maximum rate of 15% unless Congress intervenes.

Section 301 Investigations: The U.S. Trade Representative (USTR) has launched new investigations into “structural excess capacity” and “forced labor” in countries like China and Mexico. These could lead to new, more legally “durable” tariffs in the coming months.

Section 232 Still Stands: Tariffs on steel and aluminum, which rely on a different national security statute, were not affected by this specific ruling and remain in place.

What This Means for You

For Businesses and Importers

The immediate relief from IEEPA tariffs is a win, but it is replaced by a new 10% surcharge under Section 122. You should:

Audit your entries: Identify which tariffs you paid were based on IEEPA to prepare for potential refund claims.

Stay Flexible: The trade environment remains volatile as the administration shifts its legal strategy to avoid future Court losses.

For Consumers

While the invalidation of billions in tariffs sounds like a price drop is coming, the introduction of the new 10% global tariff may offset those savings. Economists expect “trade-weighted” average tariff rates to remain higher than historical norms through 2026.

Summary of Key Impacts

Feature

IEEPA Tariffs (Struck Down)

Section 122 Tariffs (New)

Legal Status

Unconstitutional/Invalid

Currently Active

Current Rate

0% (Effective Feb 20, 2026)

10% (Effective Feb 24, 2026)

Duration

N/A

150 Days (Expires July 24, 2026)

Refunds

Likely, but process is TBD

No

The Supreme Court has drawn a firm line in the sand regarding the separation of powers. While the President still has significant tools to influence trade, the era of “unbounded” emergency tariffs appears to be over.

The final numbers for 2025 are in, and there has been a GDP Downward Revision… they’ve arrived with a bit of a chill. On March 13, 2026, the Bureau of Economic Analysis (BEA) released its second estimate for the fourth quarter of 2025, significantly revising real GDP growth downward to an annualized rate of 0.7%.

This is a sharp departure from the initial “advance” estimate of 1.4% and a massive deceleration from the robust 4.4% growth seen in the third quarter. For the full year, the U.S. economy grew by 2.1%, a slight dip from previous projections.

So, what happened at the end of the year to take the wind out of the economy’s sails?

The Culprits: Shutdowns, Slumps, and Spending

Several factors converged in late 2025 to create this “soft landing” that felt a little more like a bump.

The 43-Day Government Shutdown: The most visible drag was the historic federal government shutdown that spanned October and November. While essential services remained, the lack of federal paychecks and halted government contracts took a measurable bite out of domestic demand.

A “Low-Hire” Labor Market: While mass layoffs weren’t the headline, a “low-hire, low-fire” environment took hold. Monthly job gains slowed to a crawl, and the unemployment rate ticked up to 4.6% by November, making consumers more cautious with their wallets.

The Trade Drag: Exports were revised downward as global demand softened, and a “front-loading” effect—where companies rushed to import goods earlier in the year to avoid new tariffs—faded out, leaving a gap in activity for the final months.

Sticky Inflation: Despite the slower growth, the PCE price index (the Fed’s favorite inflation gauge) remained at 2.9%. This combination of stagnant growth and persistent inflation has put the Federal Reserve in a difficult “wait-and-see” position.

Silver Linings in the Data

It’s not all doom and gloom. Even with the downward revision, there are signs of underlying resilience:

Investment is Picking Up: While consumer spending moderated, business investment—particularly in AI infrastructure—actually accelerated in Q4, acting as a critical floor for the economy.

Market Resilience: Interestingly, Wall Street took the news in stride. Markets actually rallied following the release, as investors bet that the soft GDP data would finally force the Federal Reserve to consider more aggressive rate cuts later in 2026.

Recouping the Loss: Economists expect much of the “lost” output from the government shutdown to be recovered in the first half of 2026 as backlogged projects and federal spending finally hit the books.

What’s Next for 2026?

The downward revision confirms that the “Goldilocks” era of high growth and falling inflation has hit a snag. Most forecasters, including the IMF and S&P Global, now project a steady but modest growth rate of around 1.8% to 2.0% for 2026.

The big question remains the Federal Reserve. With growth at 0.7% but inflation still above their 2% target, the path to interest rate cuts remains narrow. For now, the “wait-and-see” approach is the only game in town.

1. The Tech Sector: From Growth to Efficiency

While the broader economy slowed, Tech remained a relative fortress, but the “flavor” of investment is changing.

AI Infrastructure as a Life Raft: Business investment in “Intellectual Property Products” (tech speak for software and AI R&D) was one of the few areas that actually accelerated in Q4 2025. Companies are doubling down on AI to find the efficiencies they need to survive a low-growth environment.

The “Low-Hire” Reality: Expect the “low-hire” trend to persist in Silicon Valley. With GDP growth revised downward, tech giants are focusing on “AI-driven productivity” rather than aggressive headcount expansion.

Valuation Pressure: While the stock market has been resilient, persistent 2.9% inflation means the Federal Reserve isn’t in a rush to slash rates. High-growth tech stocks are sensitive to interest rates; if those rates stay “higher for longer,” we may see more volatility in tech valuations throughout 2026.

2. The Real Estate Market: A Tale of Two Interests

The GDP Downward Revision has created a paradoxical situation for housing.

Mortgage Rate Relief? Traditionally, weak GDP data pushes bond yields down, which can lower mortgage rates. Many analysts now expect the 30-year fixed rate to drift toward 6.0%–6.2% in 2026. This could finally “unlock” homeowners who have been trapped by high rates.

The “Sentiment” Gap: The revision highlights a cooling labor market (unemployment at 4.6%). Even if mortgage rates drop, buyer “jitters” may keep the market from exploding. J.P. Morgan research suggests national home prices may stall at 0% growth in 2026 as demand and supply reach a fragile equilibrium.

Commercial Real Estate (CRE) Stress: The 0.7% GDP print is toughest on office and retail CRE. Slower economic activity means less demand for physical space, likely leading to more “strategic defaults” or building repurposing projects in 2026.

The Federal Reserve’s “Tightrope”

The GDP Downward Revision puts the Fed in a bind. Usually, 0.7% growth would trigger an immediate rate cut to “save” the economy. However, with inflation still at 2.9%, they risk reigniting price hikes if they move too fast.

The Bottom Line: 2026 will be the year of the “Efficiency Play.” Whether you are a tech firm or a homebuyer, the goal is no longer “growth at any cost,” but rather finding value in a slower, more deliberate economic landscape.

Headline: 📉 GDP Revised to 0.7%: What it means for Tech & Real Estate in 2026.

The “Second Estimate” for Q4 2025 is out, and the numbers confirm a significant cooling of the U.S. economy. Real GDP growth was revised down to an annualized 0.7%—a sharp drop from the earlier 1.4% estimate.

While the 43-day government shutdown in late 2025 played a major role, the ripple effects for 2026 are already taking shape:

💻 TECH: The era of “growth at any cost” is officially over. We’re seeing a pivot toward Efficiency Tech. While broader spending is cooling, investment in AI infrastructure is accelerating as companies scramble to automate their way out of a low-growth environment.

🏠 REAL ESTATE: It’s a paradox. Slower growth usually means lower mortgage rates, and we’re already seeing 30-year fixed rates dip toward 6.0%. However, with unemployment ticking up to 4.6%, buyer “jitters” are real. J.P. Morgan predicts a 0% national price growth for 2026—a true flatline.

⚖️ THE FED: Chair Jerome Powell and the FOMC are walking a tightrope. With inflation still “sticky” at 2.4%–2.9%, they can’t rush to cut rates despite the sub-1% growth.

The Bottom Line: 2026 will reward the “Lean and Leaner.” Whether you’re managing a portfolio or a product roadmap, efficiency is the new growth.

1/ 🚨 BREAKING: U.S. Q4 2025 GDP revised DOWN to 0.7% (from 1.4%). The 2025 “Cold Snap” is official. Here’s the 30-second breakdown of what this means for your wallet in 2026. 🧵👇

2/ Why the drop? The 43-day government shutdown was a massive anchor, but we also saw a deceleration in consumer spending and exports. The economy didn’t crash, but it definitely pulled the emergency brake. 🛑

3/ 💻 TECH IMPACT: Silicon Valley is staying “Low-Hire.” With 0.7% growth, companies are prioritizing AI-driven productivity over expansion. If it doesn’t automate a process or save a dollar, it’s not getting funded this year.

4/ 🏠 HOUSING IMPACT: Good news? Mortgage rates are sliding toward 5.8%–6.0%. Bad news? A weaker labor market means fewer people are ready to jump. Expect a “sideways” year for home prices. 📉➡️

5/ 🏦 FED WATCH: All eyes on the March 18 FOMC meeting. The market was hoping for cuts, but with inflation at 2.4%, the Fed might stay “Higher for Longer” to ensure the fire is out.

6/Summary: 2026 is the year of the “Efficiency Play.” Growth is slow, money is still relatively expensive, and AI is the only engine still revving. Stay nimble. #GDP #Economy #Inflation

📸 Instagram/Threads: The Visual Summary

Caption:

The numbers are in: The U.S. economy hit a “speed bump” at the end of 2025. 📉 GDP growth was just revised down to 0.7%.

What this means for you: ✅ Mortgage Rates: Might actually get a bit friendlier (seeing 5.8% – 6% averages). ✅ Tech: More AI tools, fewer new job postings. Efficiency is 👑. ✅ Inflation: Still hanging around 2.4%, keeping the Fed on high alert.

It’s not a recession—it’s a recalibration. 2026 is about playing the long game. ♟️

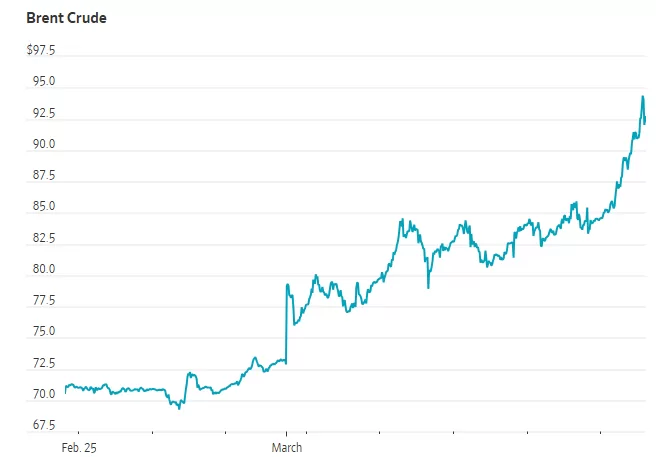

Tank Top Crisis Looms: In the world of global energy, we often focus on the flow of oil—the pipelines, the tankers, and the daily production quotas. But today, the headlines are focusing on something much more static and far more dangerous: storage.

As highlighted in a recent Wall Street Journal report, Kuwait has officially begun cutting its oil production. The reason isn’t a lack of demand or a diplomatic shift in OPEC+ policy. It is a physical reality known in the industry as reaching “tank tops.” Quite simply, Kuwait has run out of places to put its oil.

The Chokepoint Catalyst

The crisis stems from the effective closure of the Strait of Hormuz, a vital maritime artery through which roughly one-fifth of the world’s oil supply passes. Following a series of geopolitical escalations and strikes on energy assets in the Gulf, shipping traffic has ground to a near-halt.

For a nation like Kuwait, which relies heavily on this single export route, a blocked strait creates an immediate and literal backlog. When the tankers can’t leave, the oil has nowhere to go but into storage tanks. Once those tanks are full, the only remaining option is to stop the pumps.

A High-Stakes Domino Effect

Kuwait isn’t the first to hit this wall, and it likely won’t be the last.

Iraq has already slashed its production by more than half, losing roughly 1.5 million barrels per day.

The UAE is estimated to be only days away from its own storage limits.

Saudi Arabia, while possessing much larger storage capacity and alternative pipeline routes to the Red Sea, is also feeling the pressure as the backlog grows.

This “domino effect” of production shutdowns is what keeps energy analysts awake at night. Shutting down an oil well isn’t as simple as flipping a light switch. It is a technically complex and expensive process that can cause long-term damage to reservoir pressure. Restarting these wells once the crisis ends can take weeks, meaning the supply shock will linger long after the shipping lanes reopen.

The Global Fallout: $100 Oil?

The markets have reacted with predictable volatility. Brent crude has already surged past $90 a barrel, a 25% increase since the conflict began. Analysts warn that if the storage crisis forces more Gulf producers to “shut in” their wells, we could see prices easily breach the $100 mark, or even climb toward $150 according to some regional ministers.

Beyond the pump, this crisis threatens to reignite global inflation just as central banks were beginning to find their footing. It serves as a stark reminder of how fragile the global energy infrastructure remains and how a single geographic chokepoint can hold the world’s economy hostage.

The Bottom Line

The situation in Kuwait is a canary in the coal mine. It proves that in a modern energy crisis, the bottleneck isn’t just about who has the oil—it’s about who has the room to hold it when the world stops moving. As storage tanks across the Gulf reach their limits, the pressure isn’t just building in the pipes; it’s building on the global economy.

While the macro economy is feeling the “pump shock,” the impact on small business lending and accounts receivable (AR) factoring is more nuanced. For many industries, rising oil prices act as a catalyst for alternative financing, as traditional bank credit tends to tighten just when operational costs spike.

1. Impact on Small Business Lending

Traditional bank lending to small businesses is becoming more restrictive as energy-driven inflation persists.

The “Double Squeeze”: Small businesses are facing higher input costs (fuel/transport) alongside high interest rates. Banks, wary of compressed profit margins, are increasing their underwriting scrutiny.

The Approval Gap: As of early 2026, large banks are approving only about 68% of small business loans, compared to 82% at smaller, community-focused institutions.

Pivot to High-Cost Credit: With traditional loans taking weeks to approve, many businesses are turning to credit cards (averaging 18%–36% interest) to cover immediate fuel and supply chain gaps, significantly increasing their long-term debt burden.

2. The Surge in AR Factoring Demand

In a high-oil-price environment, factoring often shifts from a “last resort” to a strategic cash-flow tool, particularly for energy-intensive sectors.

Fuel as a Fixed, Immediate Expense: In industries like trucking and oilfield services, fuel must be paid for daily or weekly, while customers (shippers or large operators) often demand 30- to 90-day payment terms. Factoring bridges this “cash gap” without adding traditional debt to the balance sheet.

Sector-Specific Trends:

Transportation/Trucking: Factoring companies are seeing record demand. These businesses often enjoy the highest advance rates (90%–97%+) because their invoices are backed by tangible freight delivery.

Oilfield Services: As drilling activity ramps up in response to higher prices (especially in the Permian Basin), service providers are using factoring to scale quickly—buying new equipment or meeting surge payroll without waiting for 60-day payouts from major oil producers.

Manufacturing: With raw material costs rising alongside energy, manufacturers are factoring invoices to maintain liquidity reserves to buy inventory before prices hike further.

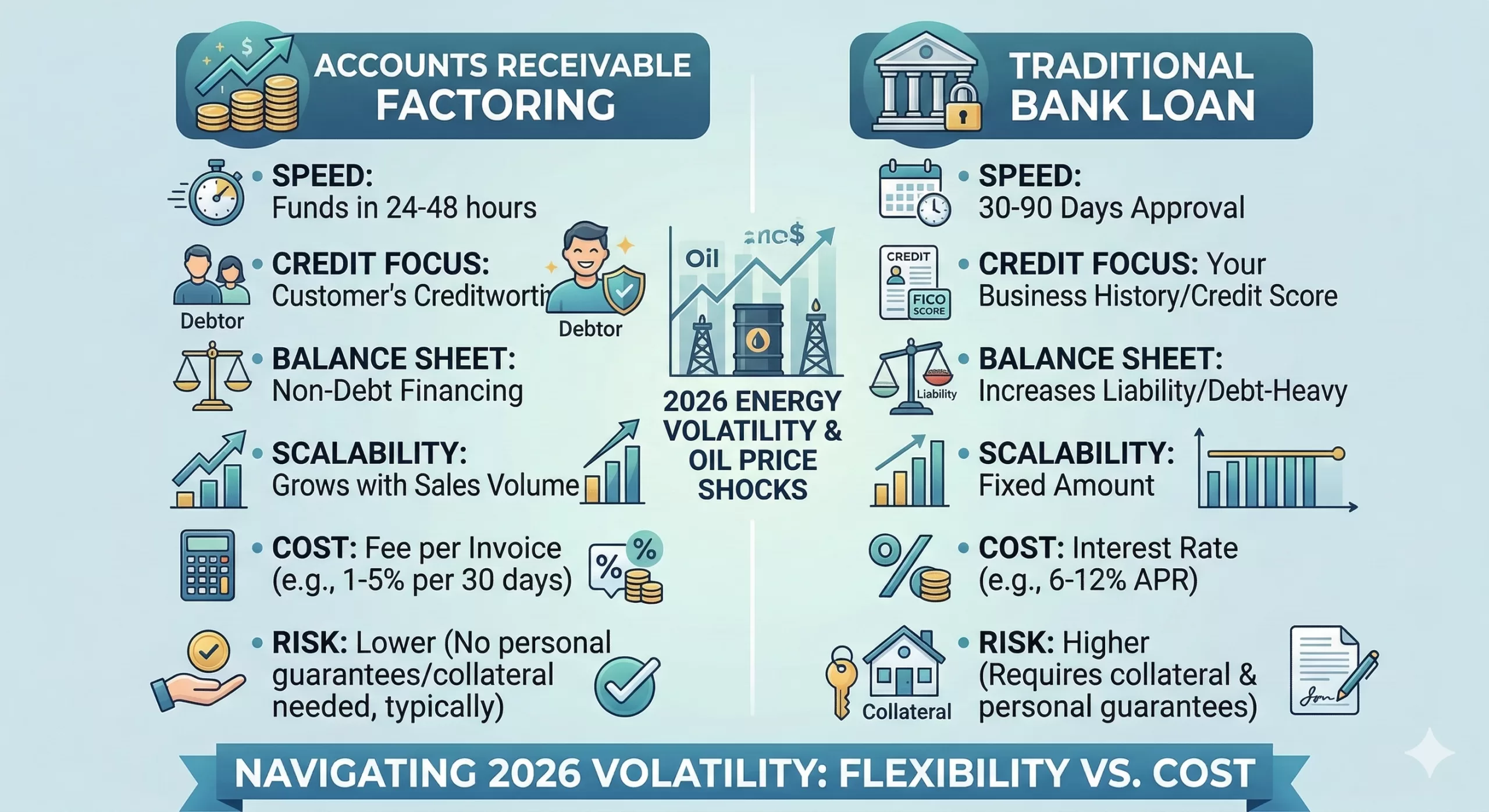

Factoring vs. Traditional Lending in 2026

Feature

Traditional Bank Loan

AR Factoring

Approval Basis

Business credit & history

Customer (Debtor) credit

Speed of Funding

2 – 7 weeks

24 – 48 hours

Debt Load

Increases liability on balance sheet

No new debt (selling an asset)

Scalability

Fixed limit

Grows with your sales volume

Cost

Lower interest (6%–12%)

Higher fees (1%–5% per 30 days)

Strategic Outlook

For the remainder of 2026, businesses that rely on “floating” cash flow are likely to prioritize speed over cost. While factoring fees are higher than bank interest, the ability to access cash within 24 hours to pay for $4.00/gallon diesel is often the difference between staying operational and grounding a fleet.

In a volatile economy where oil prices are surging and traditional banks are pulling back, choosing the right financing tool is a high-stakes decision. For B2B businesses—especially those in staffing, digital marketing, and manufacturing—the choice often comes down to the speed of Factoring versus the lower cost of a Bank Loan.

Below is a strategic comparison designed to help you evaluate which path aligns with your current cash flow needs.

Factoring vs. Bank Loans: 2026 Strategic Comparison

Feature

Accounts Receivable Factoring

Traditional Bank Loan

Speed to Cash

Ultra-Fast: Funds usually arrive within 24–48 hours after invoice setup.

Slow: Approval typically takes 30–90 days of underwriting.

Credit Focus

The Debtor: Decisions are based on your customer’s credit and payment history.

The Business: Based on your FICO score, tax returns, and years in business.

Balance Sheet

Debt-Free: It is the sale of an asset (invoices), not a liability.

Debt-Heavy: Adds a liability that can impact your debt-to-income ratio.

Scalability

Unlimited: As your sales grow, your available cash grows automatically.

Fixed: You are capped at a set amount and must re-apply to increase it.

Total Cost

Higher Fees: Usually 1%–5% per 30 days (effective APR is higher).

Lower Rates: Typically 6%–12% APR for qualified businesses.

Risk

Low: No collateral like your house or equipment is typically required.

High: Often requires a blanket lien on assets or personal guarantees.

Export to Sheets

The “Why Now?” Factor: Navigating 2026 Volatility

Pros of Factoring in This Market

Immediate Fuel/Supply Buffer: With diesel prices fluctuating, factoring gives you the cash today to buy inventory or fuel before the next price hike.

Protects Your Growth: In sectors like digital marketing or staffing, you can’t wait 60 days for a client to pay to meet your weekly payroll. Factoring ensures your team stays paid regardless of when the client cuts the check.

No “Covenant” Stress: Bank loans often come with strict “covenants” (rules about your profit margins). If high oil prices temporarily squeeze your margins, a bank might call your loan; a factor simply keeps funding your sales.

Cons to Consider

Margin Impact: If your profit margins are already thin (common in food production or distribution), the 1%–3% factoring fee could eat up a significant portion of your net income.

Customer Perception: While widely accepted today, some ultra-conservative clients might still prefer to pay you directly rather than a third-party factor.

The Bottom Line

If you have long-term stability and time to wait, a Bank Loan is cheaper. However, if you are growing rapidly or facing unpredictable costs, Factoring acts as a flexible insurance policy for your cash flow.

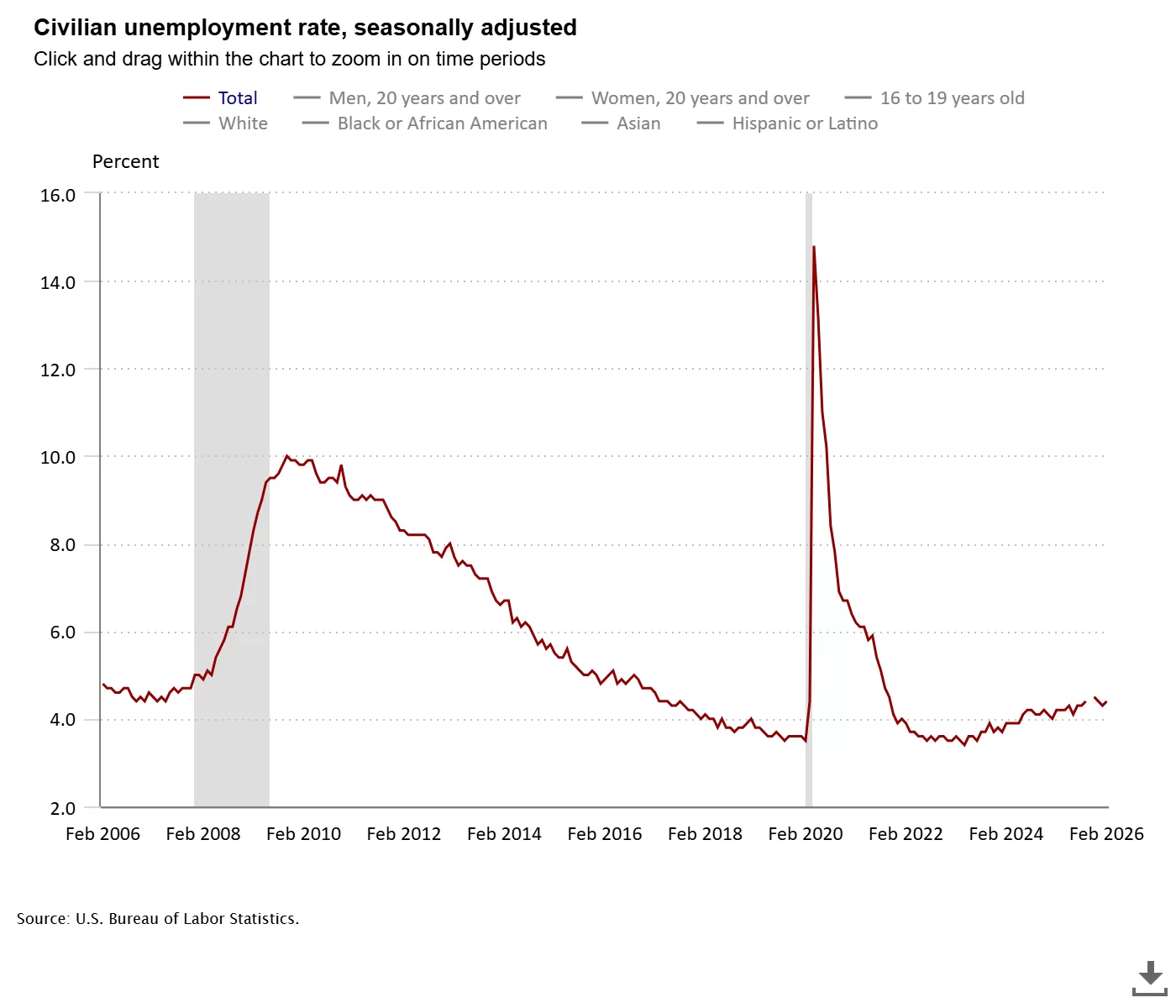

Economy Sheds 92,000 Jobs. The American labor market hit a significant speed bump last month, as the Bureau of Labor Statistics (BLS) reported a loss of 92,000 jobs for February 2026. This unexpected contraction caught economists off guard, as many had projected a modest gain of roughly 60,000 positions.

Coupled with the job losses, the national unemployment rate ticked up to 4.4%, rising from 4.3% in January. While the figure remains low by historical standards, the sudden reversal in momentum has reignited concerns about the underlying health of the economy amidst ongoing geopolitical tensions and domestic labor disputes.

The Numbers at a Glance

The February report was a stark contrast to the start of the year, which initially saw a healthy gain in January. However, even those numbers were revised downward, painting a picture of a job market that is struggling to maintain its footing.

Metric

February 2026 Data

Comparison

Nonfarm Payrolls

-92,000

Down from +126,000 (revised) in Jan

Unemployment Rate

4.4%

Up from 4.3%

December Revision

-17,000

Revised down from +48,000

Labor Force Participation

62.0%

Lowest level since December 2021

Key Drivers of the Decline

Several factors converged to create the “perfect storm” that led to February’s disappointing figures:

Labor Disputes: The healthcare sector, usually a reliable engine of growth, shed 28,000 jobs. Much of this was attributed to a major strike involving over 30,000 workers at Kaiser Permanente in California and Hawaii.

Harsh Winter Weather: Severe storms across the country likely hampered hiring in the construction sector, which saw a decline of 11,000 jobs.

Sector-Specific Weakness: The Information and Transportation/Warehousing sectors both lost 11,000 jobs, while the Federal Government continued its downward trend, losing 10,000 positions.

Geopolitical Uncertainty: The escalation of the conflict in the Middle East has driven up crude oil prices, injecting a new layer of caution into business spending and hiring plans.

“Just when it looked like the labor market was stabilizing, this report delivers a knock-down blow to that view. It’s bad news whichever way you look at it.”

— Olu Sonola, Head of U.S. Economics at Fitch Ratings.

Silver Linings and the Path Forward

Despite the gloomy headline, there were a few areas of resilience. Average hourly earnings rose by 0.4% for the month, representing a 3.8% increase year-over-year. This suggests that while hiring has slowed, those currently employed are still seeing wage growth that is largely keeping pace with inflation.

The Federal Reserve now faces a delicate balancing act. While the job losses might typically signal a need for interest rate cuts to stimulate the economy, the surge in energy prices due to the war in Iran keeps the threat of inflation high.

Economists will be looking toward the March report (scheduled for release on April 3rd) to determine if February was a temporary blip caused by weather and strikes, or the start of a more concerning long-term trend.

Mortgage Rates – The housing market has seen a welcome shift! Mortgage rates have fallen below 6% for the first time since 2022, offering a significant improvement for potential homebuyers. This news comes as a breath of fresh air after a period of steadily climbing rates that have put a strain on many budgets.

What Does This Mean for Potential Homebuyers?

The drop in mortgage rates translates directly into increased affordability for those looking to purchase a home. This can be beneficial in several ways:

Lower Monthly Payments: A lower interest rate means a smaller portion of your monthly payment goes towards interest, reducing your overall housing cost.

Increased Buying Power: With lower monthly payments, you may be able to qualify for a larger loan amount, potentially allowing you to purchase a more expensive home.

Refinancing Opportunities: Existing homeowners who currently have a higher mortgage rate may be able to refinance their loan and save money on their monthly payments.

Why Are Mortgage Rates Falling?

While the exact reasons behind the rate drop are complex, several factors may be contributing to the trend:

Lower Inflation: Inflation has shown signs of cooling down, which can influence interest rates.

Economic Growth: While economic growth has been moderate, some signs suggest it may be slowing, which can also affect mortgage rates.

Changes in the Bond Market: Bond yields, which are closely tied to mortgage rates, have also seen a decline.

What Should You Do Now?

If you’ve been on the fence about buying a home, this could be an excellent time to re-evaluate your options. Here are some steps to consider:

Get Pre-Approved for a Mortgage: This will give you a clear idea of how much you can borrow and help you understand your monthly payment.

Shop Around for Rates: Different lenders offer varying rates, so it’s essential to compare offers from multiple institutions.

Consider Your Long-Term Goals: While the lower rates are attractive, it’s crucial to ensure that buying a home is the right decision for your long-term financial goals.

Important Note: It’s important to remember that mortgage rates are subject to change based on economic conditions and other factors. While the current trend is encouraging, it’s essential to stay informed about any potential shifts in the market.

Conclusion:

The drop in mortgage rates below 6% is a significant development for the housing market, offering some much-needed relief to potential homebuyers and homeowners alike. If you’ve been considering buying a home, this could be the right time to take action. With lower monthly payments and increased buying power, you may be closer to achieving your homeownership goals than you thought. However, it’s crucial to act carefully and seek professional advice to make the best decision for your individual situation.

Primary Data Sources

Freddie Mac (Primary Mortgage Market Survey): The ultimate source for the 5.98% figure. Freddie Mac released its weekly report on February 26, 2026, confirming that the 30-year fixed-rate mortgage dipped below 6% for the first time in approximately 3.5 years.

The Federal Reserve (FRED): Used to verify historical trends, specifically confirming that the last time rates were at this level was September 8, 2022 (when they were 5.89%).

CBS News: Provided context on the White House’s initiatives (such as the $200 billion mortgage bond purchase plan) and expert commentary on the “spring home-buying season.”

Associated Press (AP): Detailed the influence of the 10-year Treasury yield on mortgage pricing and quoted housing economists regarding market entry for buyers and sellers.

Mortgage rates in 2026 forecast This video provides expert analysis on how these sub-6% rates impact monthly affordability and what to expect for the rest of the 2026 housing market

In a surprising turn of events, German factory orders in have shown an unexpected and robust surge, signaling a potentially stronger-than-anticipated rebound in the nation’s industrial sector. This latest data has instilled a renewed sense of optimism among economists and policymakers, suggesting that Europe’s largest economy might be on a more solid recovery path than previously estimated.

The Federal Statistical Office announced this morning that new factory orders jumped by a significant margin in the past month, far exceeding analyst expectations. This remarkable uptick follows a period of cautious growth and even some contractions, making the current surge all the more impactful. The increase was broad-based, with both domestic and international orders contributing substantially to the overall rise.

A Deeper Dive into the Numbers

The reported increase in orders was particularly driven by strong demand for capital goods, indicating that businesses are investing more in machinery and equipment – a key indicator of future production capacity and confidence. Intermediate goods also saw a healthy boost, suggesting renewed activity across various supply chains.

Economists are pointing to several factors contributing to this positive development. A resilient global demand, particularly from key trading partners, appears to be playing a significant role. Furthermore, a gradual easing of supply chain bottlenecks, which have plagued manufacturers for months, is allowing companies to fulfill orders more efficiently and take on new business.

Impact on the Broader Economy

This unexpected surge in factory orders is a shot in the arm for the German economy, which has been grappling with persistent inflation and the lingering effects of global uncertainties. A strong industrial sector is crucial for Germany’s economic health, as it is a major employer and a significant contributor to GDP. The improved outlook could lead to increased hiring, higher wages, and ultimately, stronger consumer spending.