Factoring Proposal: After recently recovering from the devasting impacts of tariffs, this company requires PO financing to rebuild inventory. Their existing factor is uncooperative and must be replaced by Versant which has the ability to facilitate PO funding though a trusted partner.

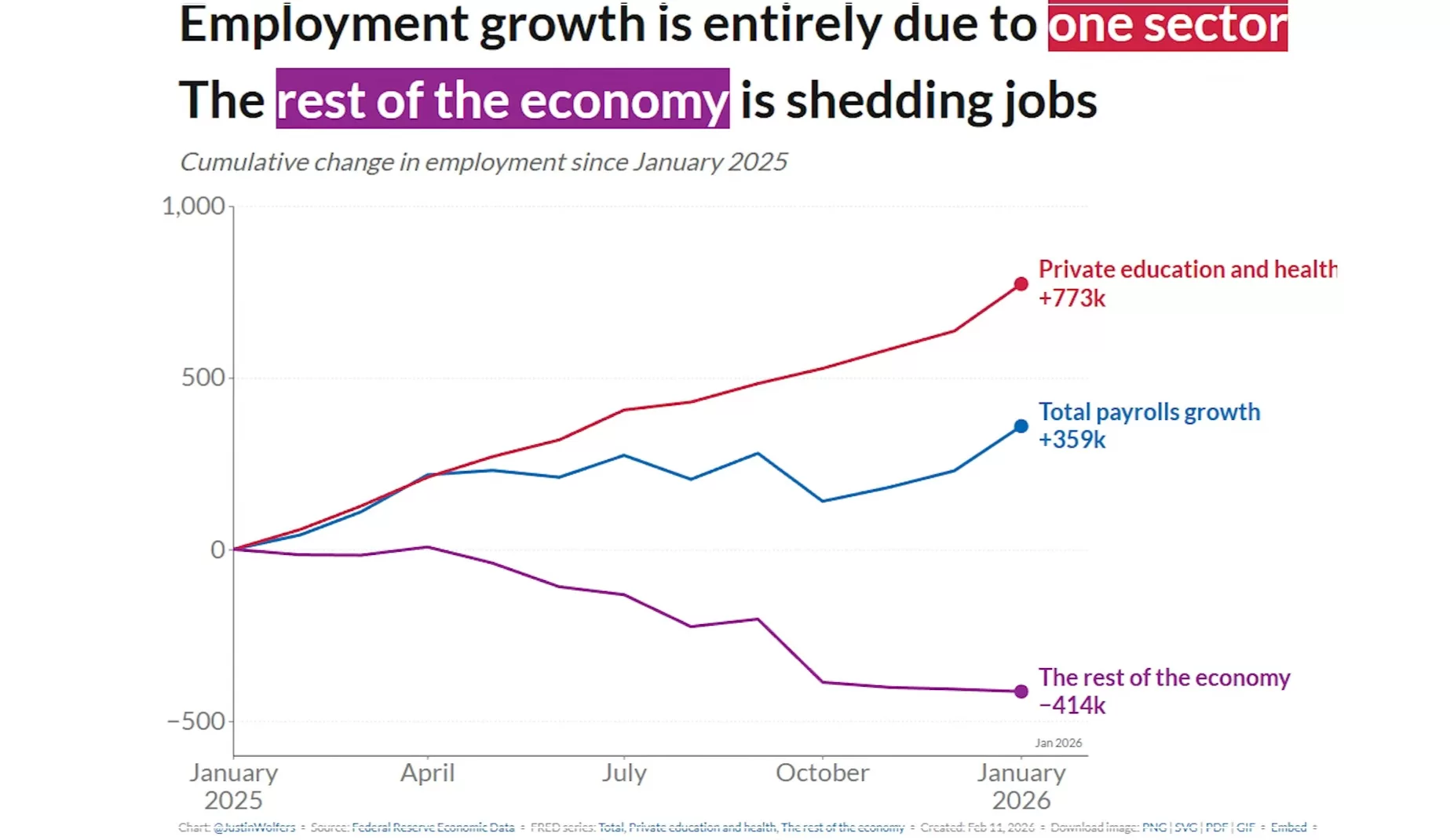

The U.S. labor market began 2026 with a surprising burst of energy, shaking off a sluggish 2025. According to the latest data from the Bureau of Labor Statistics (BLS) released on February 11, 2026, employers added 130,000 jobs in January—easily doubling December’s figures and blowing past economist expectations of roughly 70,000.

While the report was delayed by a week due to a brief federal government shutdown, the results suggest that the “hiring fatigue” seen late last year might be beginning to thaw.

The Numbers at a Glance

The January report offers a mix of resilience and necessary context for the year ahead:

Total Jobs Added: 130,000 (up from a revised 50,000 in December).

Unemployment Rate: Ticked down to 4.3% (from 4.4%).

Average Hourly Earnings: Rose by 0.4% in January, bringing the year-over-year increase to 3.7%.

Labor Force Participation: Remained steady at 62.5%.

Sector Winners and Losers

The growth wasn’t uniform across the board. In fact, a few key sectors carried the heavy lifting for the entire economy:

Healthcare & Social Assistance: This sector remains the titan of the U.S. job market, adding 124,000 jobs (82k in healthcare and 42k in social assistance).

Construction: Added a solid 33,000 jobs, largely driven by nonresidential specialty trade contractors.

The Tech & White-Collar Slump: Conversely, professional and business services and manufacturing continued to struggle, reflecting ongoing shifts in AI implementation and trade policy impacts.

Government: Federal employment saw a decline, partly a ripple effect of recent policy shifts and the temporary shutdown.

Why This Matters

After a tumultuous 2025—which was recently revised to show only 181,000 total jobs added for the entire year—this January figure is a massive sigh of relief. It suggests that while the economy isn’t sprinting, it’s found its footing.

“The January gains are a sign that the labor market is stabilizing,” says one economist. “However, the high concentration of growth in healthcare suggests a ‘one-legged stool’ economy that we need to watch closely.”

Looking Ahead

While 130,000 jobs is a “stronger footing,” the market remains complex. Layoffs in high-profile sectors like tech and transportation (notably Amazon and UPS) dominated January headlines, yet the aggregate data shows that other sectors are more than absorbing that displaced talent.

For job seekers, the message is clear: the opportunities are there, but they have shifted. Strategic hiring is the theme of 2026, with a high premium on specialized skills in healthcare, infrastructure, and adaptive technologies.

The January jobs report has effectively shifted the narrative for the Federal Reserve. While the 130,000 jobs added might seem modest by historical standards, it was a significant “beat” compared to expectations, and it has given the Fed a reason to tap the brakes on further interest rate cuts.

Here is how the latest data is influencing the Fed’s next move:

1. From “Easing” to “Holding”

Following three consecutive rate cuts in late 2025, the Federal Reserve held rates steady at its January 28, 2026 meeting, maintaining the federal funds rate at 3.5% to 3.75%. This jobs report reinforces that “pause.”

The Consensus: With the unemployment rate ticking down to 4.3% and job growth doubling December’s numbers, there is no longer an “emergency” need to stimulate the economy.

Market Sentiment: Before this report, some traders were betting on a March cut. Now, CME FedWatch tools show those odds have plummeted, with the consensus moving toward a “higher for longer” stance through at least the first half of the year.

2. Emerging Internal Division

The Fed is no longer acting in total unison. The January meeting saw a rare 10-2 vote, with two dissenting members actually pushing for another 25-basis-point cut due to lingering concerns about long-term hiring weakness.

The Hawks: Officials like Cleveland Fed President Beth Hammack and Dallas Fed President Lorie Logan have signaled that the Fed should “err on the side of patience,” arguing that current rates are “neutral”—neither helping nor hurting the economy.

The Doves: Those worried about the “one-legged stool” (growth coming only from healthcare) fear that without more cuts, sectors like tech and manufacturing will continue to bleed jobs.

3. The “Neutral Rate” Debate

Chair Jerome Powell recently noted that the economy is on a “firm footing” entering 2026. Analysts now believe the Fed is searching for the neutral rate—the sweet spot where inflation stays at 2% without triggering a recession.

Because average hourly earnings rose 0.4% in January (3.7% annually), the Fed is wary that cutting rates too soon could reignite inflation, especially with potential new trade tariffs on the horizon.

Key Dates to Watch

Event

Date

Significance

January CPI Report

Feb 13, 2026

Will confirm if the wage growth in the jobs report is driving up prices.

Fed “Beige Book”

Mar 4, 2026

Regional reports on how small businesses are actually feeling.

Next FOMC Meeting

Mar 17-18, 2026

The next formal window for a rate change decision.

For a small business owner, the January jobs report isn’t just about hiring statistics—it’s a leading indicator for the cost of your next loan or line of credit.

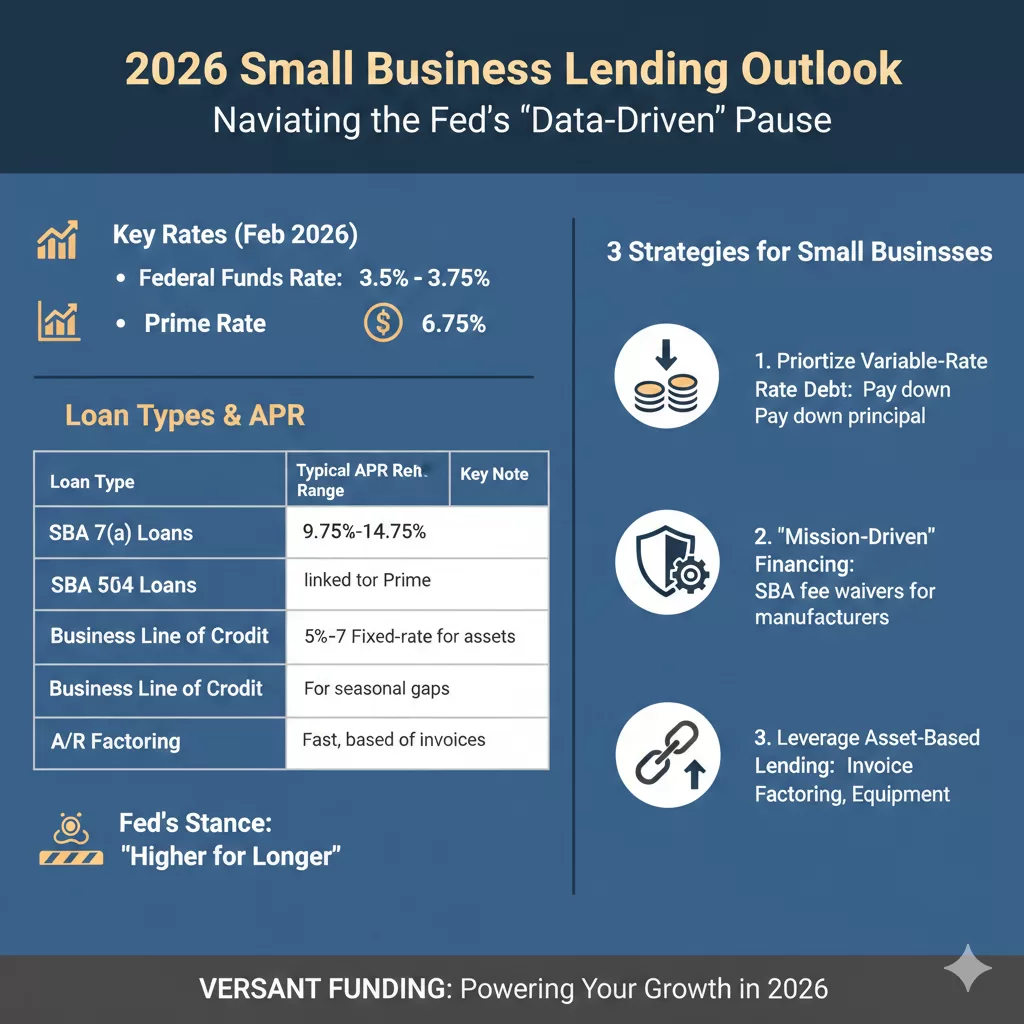

Following the stronger-than-expected labor data, the Federal Reserve has hit “pause” on interest rate cuts. For businesses at Versant Funding and across the U.S., this means a period of “stabilized high” borrowing costs. Here is what your business needs to know to navigate the financial landscape of early 2026.

2026 Borrowing Outlook: The “Data-Driven” Pause

The Fed began 2026 by holding the federal funds rate steady at 3.5% to 3.75%. While the market had hoped for more aggressive easing, the surge of 130,000 new jobs in January has signaled to policymakers that the economy is not yet in need of more “cheap money.”

Current Lending Rates (As of February 2026)

Loan Type

Typical APR Range

Key Note

SBA 7(a) Loans

9.75% – 14.75%

Variable rates fluctuate with the Prime Rate (currently 6.75%).

SBA 504 Loans

5% – 7%

Fixed-rate; best for long-term real estate or equipment.

Business Lines of Credit

10% – 28%

Vital for seasonal inventory and payroll gaps.

Accounts Receivable Factoring

24% – 36%

High speed; based on invoice value rather than credit score.

Three Strategies for Small Businesses

With rates unlikely to drop significantly before the summer, owners should shift from “waiting for better rates” to “optimizing current cash flow.”

Prioritize Variable-Rate Debt: If you are carrying an SBA 7(a) loan or a variable line of credit, your payments will remain flat for now. Use this stability to pay down principal where possible, as the “higher for longer” stance means interest costs won’t be melting away anytime soon.

Look for “Mission-Driven” Financing: In 2026, the SBA is waiving guarantee fees for certain small manufacturers (NAICS 31-33). If your business fits this category, you could save thousands in upfront costs regardless of the interest rate.

Leverage Asset-Based Lending: If traditional bank term loans are too restrictive, consider Invoice Factoring or Equipment Financing. These options often focus more on the value of your assets (your unpaid invoices or machinery) than on the Fed’s baseline rates, providing more predictable access to capital during economic volatility.

The Bottom Line

The “stronger footing” of the U.S. labor market is a double-edged sword: it proves consumer demand is resilient, but it keeps the cost of capital elevated. For 2026, the most successful businesses will be those that prioritize liquidity and debt structure over simply chasing the lowest rate.

The results of recent surveys, most notably the Capital One Middle Market Strategic Investments report, have sent a ripple of confidence through the business community: 89% of middle-market companies are optimistic about their growth in 2026.

For those who track the “engine room” of the U.S. economy, this isn’t just a number—it’s a signal of a major strategic pivot. After years of playing defense against inflation and supply chain “whack-a-mole,” the middle market is moving back to offense.

Here is my take on why the “Mighty Middle” is feeling so bullish and what this means for the year ahead.

1. The “Big Beautiful Bill” Effect

A significant driver of this 89% figure is the One Big Beautiful Bill Act (OBBBA) passed in late 2025. Middle-market leaders aren’t just aware of the policy; they are already building it into their spreadsheets.

Tax Certainty: By codifying full expensing of capital expenditures and maintaining the 21% corporate tax rate, the bill has removed the “wait and see” hurdle that often stalls big investments.

Cash Flow: 59% of companies expect improved cash flow through these incentives, giving them the “dry powder” needed to expand.

2. AI: From “Hype” to “Help”

In 2024 and 2025, AI was a buzzword. In 2026, it’s a budget line item.

Operational Efficiency: 66% of middle-market businesses are prioritizing AI investment, not to replace humans, but to solve the persistent labor crunch.

ROI Focus: Unlike the “growth at all costs” tech era, middle-market firms are looking for AI to deliver specific returns—29% expect AI to be their highest-yielding investment this year.

3. Resilience Through “Alternate” Means

What I find most fascinating is the evolution of middle-market financing. With traditional bank lending remaining tight, 50% of these companies are now pursuing alternate financing, specifically private credit.

The Takeaway: Middle-market companies are no longer at the mercy of traditional interest rate cycles. They have diversified their “oxygen supply” (capital), allowing them to stay optimistic even when the Fed is being cautious.

4. The M&A “Spring”

After a multi-year slumber, deal-making is waking up. Nearly 44% of middle-market firms intend to pursue acquisitions in 2026. This suggests that the optimism isn’t just about internal growth; it’s about consolidation and picking up smaller players who may not have the scale to handle 2026’s regulatory and technological demands.

The Bottom Line: Execution is the New Strategy

The 89% optimism rate doesn’t mean the road is easy. Leaders are still citing inflation (97%) and tariffs as major headaches. However, the difference in 2026 is preparedness.

Middle-market companies have spent the last two years “stress-testing” their models. They are leaner, more tech-forward, and more agile than they were pre-2020. If 89% of them believe they can win this year, the rest of the market should probably pay attention.

The “Mighty Middle” is playing offense in 2026. 🚀

The numbers are in, and they are striking: 89% of middle-market companies are officially optimistic about their growth this year.

After years of navigating the “whack-a-mole” challenges of inflation and supply chain disruptions, we are seeing a massive strategic pivot. Middle-market leaders aren’t just surviving; they are scaling.

Why the surge in confidence?

The OBBBA Effect: Tax certainty and full expensing are providing the “dry powder” needed for major capital investments.

AI Integration: We’ve moved past the hype. Companies are now budgeting for AI to solve real-world labor shortages and drive operational efficiency.

Alternative Financing: With traditional bank lending remaining tight, the shift toward private credit and alternative capital sources is keeping growth on track.

M&A Resurgence: Nearly 44% of these firms are looking to acquire, signaling a year of consolidation and expansion.

The bottom line? These companies have “stress-tested” their models for two years. They are leaner, tech-forward, and ready to win.

Is the Middle Market the new economic bellwether for 2026? 📈

The data is hard to ignore: 89% of middle-market firms are entering 2026 with high optimism. This isn’t just “wishful thinking”—it’s a calculated response to a shifting fiscal and technological landscape.

Here are the four pillars driving this confidence:

Fiscal tailwinds: The One Big Beautiful Bill Act (OBBBA) has finally provided the tax certainty and full-expensing incentives required to move “wait-and-see” capital into active deployments.

Maturity in AI adoption: We have moved beyond the “hype cycle.” 66% of mid-cap leaders are now prioritizing AI as a tool for operational leverage, specifically targeting persistent labor bottlenecks.

The Rise of Alternative Credit: As traditional bank lending remains constrained, the pivot toward private credit and specialized liquidity solutions has decoupled middle-market growth from traditional interest rate volatility.

Strategic Consolidation: With 44% of firms pursuing M&A, we are entering a period of significant market “up-tiering.”

The “Mighty Middle” has spent the last 24 months stress-testing their balance sheets. In 2026, they aren’t just defending their position—they are expanding it.

Factoring Proposal: With only a single major distributor as customer, this business was unable to find a lender willing to fund them. Our underwriting focuses solely on the quality of our client’s customer so time in business and customer concentration are irrelevant.

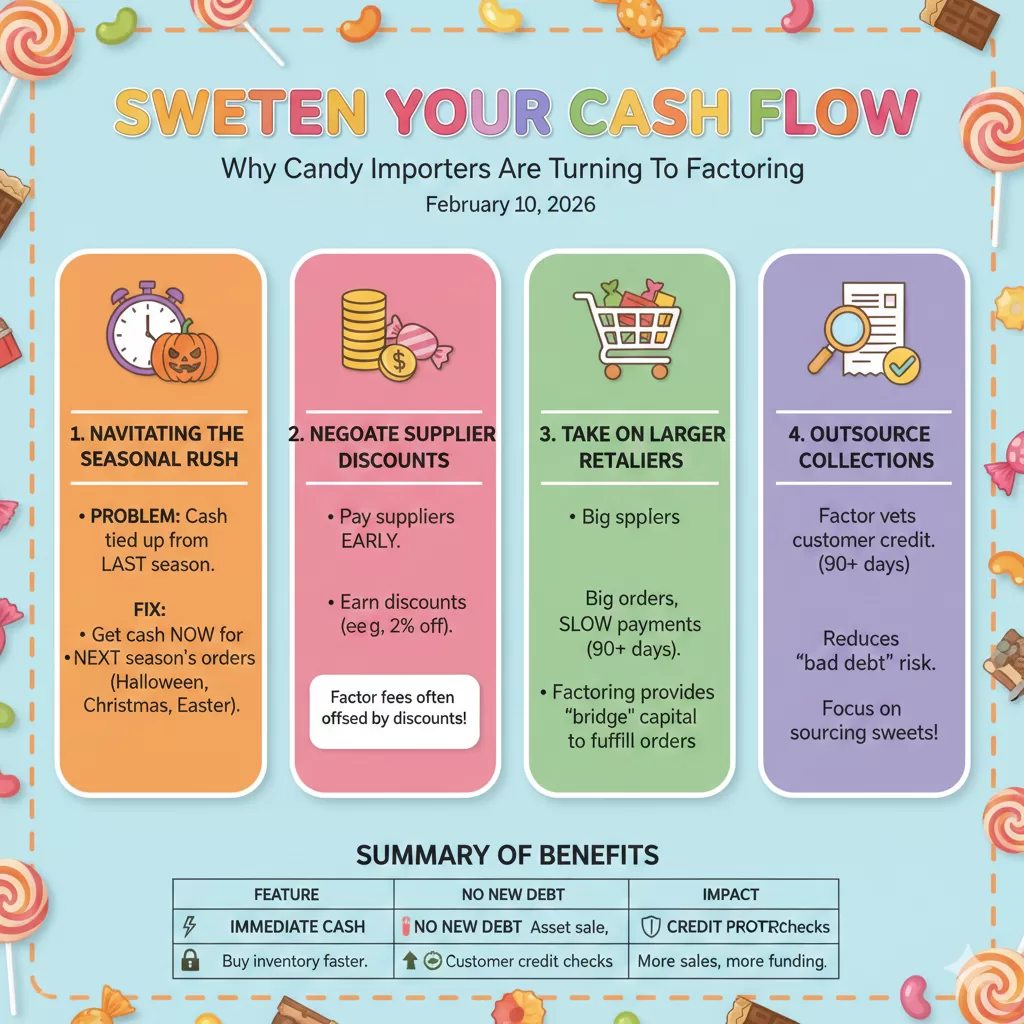

In the world of candy importing, timing is everything. You have to navigate seasonal peaks (think Halloween and Valentine’s Day), manage international shipping lead times, and juggle the demands of large retailers.

However, there is often a massive gap between the moment your colorful shipments clear customs and the moment your retail partners actually pay their invoices. If your capital is trapped in Accounts Receivable (AR), you might find yourself unable to jump on the next big inventory opportunity.

This is where Accounts Receivable Factoring—also known as invoice factoring—becomes a game-changer.

What Exactly is Factoring?

Factoring isn’t a loan; it’s the sale of your assets. You sell your outstanding invoices to a “factor” (a specialized financial company) at a slight discount. In return, you get immediate access to the cash that was previously tied up for 30, 60, or even 90 days.

1. Navigating the Seasonal Rush

Candy is a highly seasonal business. To prepare for the “Big Three”—Halloween, Christmas, and Easter—importers must place massive orders months in advance.

The Problem: Your cash is tied up in invoices from the previous season while you need to pay suppliers for the next one.

The Factoring Fix: By factoring current invoices, you get an immediate cash injection to cover manufacturing and shipping costs for upcoming peak periods, ensuring you never miss a shelf-stocking deadline.

2. Negotiating Supplier Discounts

When you have “cash in hand” thanks to factoring, you move to the front of the line with global suppliers. Many international manufacturers offer early payment discounts (e.g., a 2% discount if paid within 10 days).

The small fee you pay for factoring is often completely offset by the discounts you earn from your suppliers by paying them early.

3. Taking on Larger Retailers

Big-box retailers are great for volume, but they are notorious for long payment terms. If a major chain wants to place a massive order but won’t pay for 90 days, a small-to-medium importer might have to say “no” simply because they can’t afford to wait that long for the payout.

Factoring provides the “bridge” capital. You can fulfill the order, factor the invoice the day the candy ships, and have the funds to keep the rest of your business running smoothly.

4. Outsourcing the “Headache” of Collections

Many factoring companies handle the back-end credit checking and collections process. For a lean importing team, this is a massive relief.

The factor vets the creditworthiness of your customers before you even ship, reducing your risk of “bad debt” and allowing you to focus on sourcing the best sweets rather than chasing down checks.

Summary of Benefits

Feature

Impact on Your Candy Business

Immediate Cash

Buy inventory for the next holiday season without waiting.

No New Debt

Factoring is an asset sale, not a bank loan with monthly interest.

Credit Protection

Many factors provide credit snapshots of your retail partners.

Scalability

The more you sell, the more funding becomes available.

Is Factoring Right for You?

If your candy importing business is growing faster than your bank account can keep up with, factoring provides the liquidity to keep your momentum. It turns your “sold” inventory back into “buying” power instantly.

The Sluggish Job Growth of the U.S. labor market is currently sending mixed signals that lean toward the “rough” side. After months of subtle hiring freezes and quiet cutbacks, the dam has seemingly broken, leading to a wave of high-profile layoff announcements that have left both job seekers and investors on edge.

From “Quiet Quitting” to “Quiet Hiring”… to Just “Quiet”

Last year, the narrative was dominated by “labor hoarding”—companies holding onto staff despite economic uncertainty. That trend has officially cooled. What we are seeing now is a three-phase retraction:

The Big Freeze: Before the layoffs began, many firms implemented unannounced hiring freezes. If you noticed your applications disappearing into a “black hole” in Q4, you weren’t imagining it.

The Strategic Cut: We’ve moved past the “growth at all costs” mindset of the early 2020s. Companies are now optimizing for efficiency, which often means trimming middle management and non-core departments.

Market Rattling: These moves aren’t just affecting workers; they’re making Wall Street twitchy. While layoffs sometimes boost stock prices in the short term by promising better margins, a systemic pullback in hiring signals a lack of confidence in broader consumer spending.

Why is this happening now?

It’s a perfect storm of economic factors. Interest rates remain a point of contention, and the “higher for longer” reality has finally forced CFOs to tighten the belt. Additionally, the rapid integration of AI and automation is no longer a futuristic concept—it’s actively reshaping how companies budget for human capital.

Key Takeaway: The power dynamic has shifted. We are no longer in the “Great Resignation” era where candidates held all the cards. We are in an “Employer’s Market” characterized by high competition and rigorous vetting.

Survival Tips for the 2026 Job Seeker

If you’re currently in the trenches or worried about your role, “rough” doesn’t have to mean “impossible.” Here is how to adapt:

Focus on ‘Recession-Proof’ Skills: Lean into roles that directly impact revenue or operational efficiency.

Networking is the New Resume: With hiring portals frozen or flooded, a warm introduction is often the only way to bypass the digital gatekeepers.

Audit Your Tech Literacy: Companies are hiring for roles that can leverage new tools to do more with less. Show that you are that person.

The January chill in the job market is a sobering reminder that economic cycles are inevitable. While the headlines look daunting, history shows that these periods of contraction often lead to leaner, more resilient industries. The goal for now? Stay agile, stay informed, and keep your pulse on the shifting landscape.

Every year, we’re told that January is the season for “new beginnings.” But for many of my colleagues and friends, 2026 started with a calendar invite that no one wants to see.

With over 100,000 layoffs announced just last month, it’s easy to feel like the ground is shifting beneath us. It’s frustrating to see companies freeze hiring right when talented people are looking for their next chapter.

What I’ve learned during market shifts like this:

Your job is what you do, not who you are. Resilience starts with separating your self-worth from a corporate headcount.

The “Hidden Market” is real. When the portals freeze, the human network thaws. Most of the hiring right now is happening through referrals and back-channel conversations.

Skill-stacking is the best defense. The folks I see landing roles right now are the ones who didn’t just wait—they spent the “freeze” learning how to leverage AI to make themselves a “team of one.”

If you were part of the January cuts, take a breath. The market is rough, but you are capable.

If I can help you with a referral, a resume check, or just a word of encouragement, please reach out. Let’s help each other get through the “January Chill.” ☕️👇

January just delivered a wake-up call to the U.S. workforce. Here’s the “lowdown” on the slowdown:

108k+: Layoffs announced in the last 31 days (the highest since ’09).

Record Lows: Hiring plans have hit a historic slump for Q1.

The Shift: Efficiency and AI-proficiency are officially the new “must-haves.”

The bottom line? The “Great Resignation” is a memory. We are now in the “Great Recalibration.”

If you’re hiring, post your roles in the comments. If you’re looking, tell us one “efficiency win” you’ve had recently. Let’s turn this feed into a resource.

Our Accounts Receivable Factoring program can quickly meet the working capital needs of businesses in the energy industry.

Versant’s underwriting focus is solely on the quality of a company’s accounts receivable, which enables us to rapidly fund businesses which do not qualify for traditional lending.

Factoring Press Release : Versant Funds $5 Million Non-Recourse Factoring Facility to Manufacturer

(January 27, 2026) Versant Funding LLC is pleased to announce that it has funded a $5 Million non-recourse factoring facility to a company that manufactures products for a large customer base which includes one of America’s largest municipalities.

After a transition to Private Equity ownership and management restructuring, our newest client required an infusion of working capital to meet an urgent cash need. While the company has hundreds of customers with AR outstanding, the most efficient way to fund was to factor only the AR of their largest customer, but most factoring companies would not permit 100% customer concentration.

“Versant focuses solely on the credit quality of our clients’ customers,” according to Chris Lehnes, Business Development Officer for Versant Funding, and originator of this financing opportunity. “Since the company’s largest account is a large US city, we were willing to allow 100% customer concentration and meet the client’s short-term funding need.”

About Versant Funding

Versant Funding’s custom Non-Recourse Factoring Facilities have been designed to fill a void in the market by focusing exclusively on the credit quality of a company’s accounts receivable. Versant Funding offers non-recourse factoring solutions to companies with B2B or B2G sales from $100,000 to $30 Million per month. All we care about is the credit quality of the A/R. To learn more contact: Chris Lehnes | 203-664-1535 | chis@chrislehnes.com

Immediate Cash Flow: The manufacturer gains immediate access to working capital by selling its invoices to Versant Funding, significantly improving liquidity.

Mitigation of Customer Concentration Risk: By utilizing non-recourse factoring, Versant Funding assumes the credit risk associated with the manufacturer’s customer, protecting the manufacturer from potential bad debt.

Support for Growth: The increased cash flow will enable the manufacturer to invest in new equipment, expand production, take on larger orders, and capitalize on new market opportunities.

Operational Efficiency: The manufacturer can focus on its core business operations and production, knowing its cash flow is stable and predictable.

Flexible and Scalable: The factoring facility is designed to grow with the manufacturer’s sales, providing ongoing access to capital as their business expands.

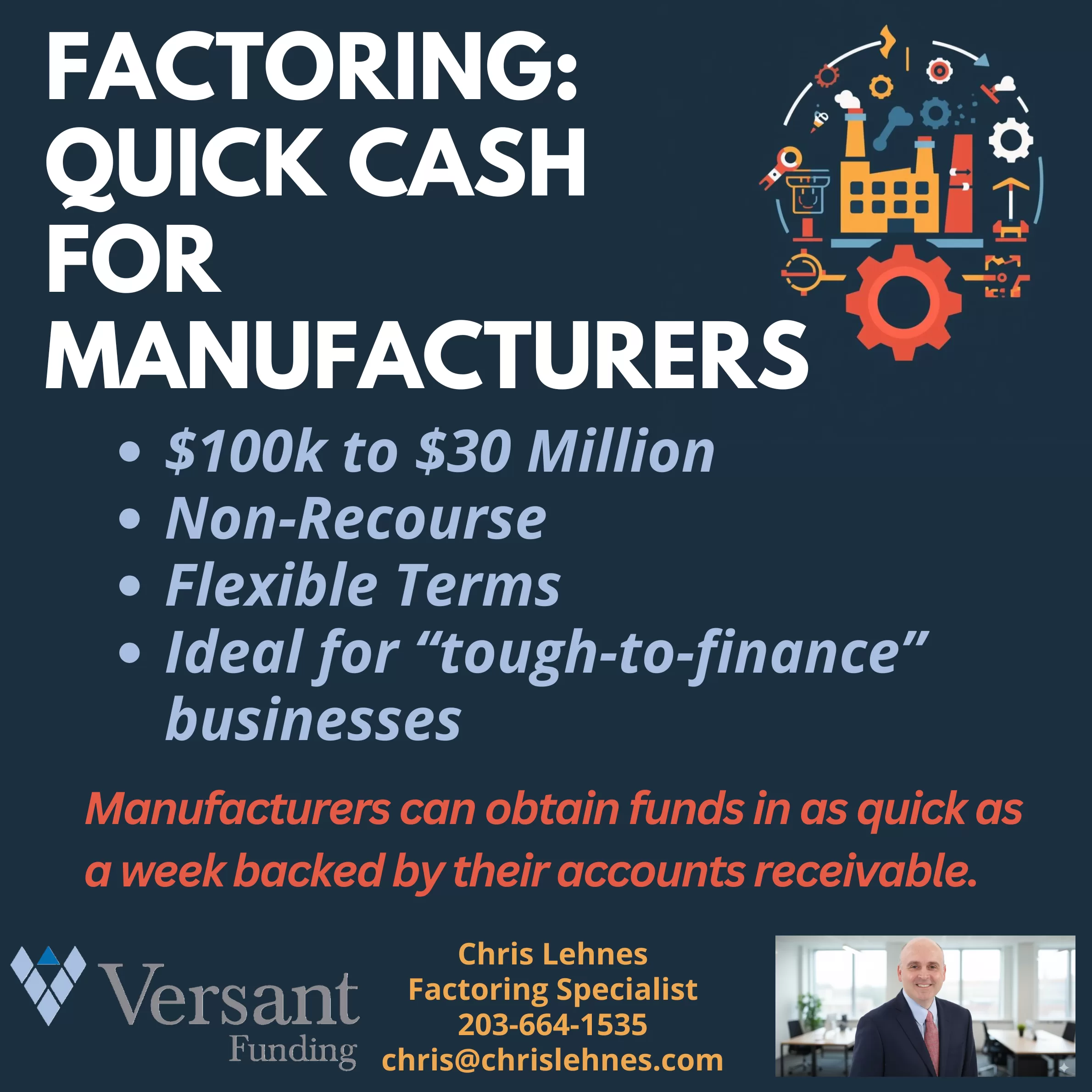

Factoring: The Quick Cash Solution Manufacturers Need Now

In today’s dynamic market, manufacturers face a unique set of challenges. From managing inventory and production schedules to navigating supply chain disruptions and fluctuating demand, the need for reliable, accessible capital is constant. That’s where factoring comes in, offering a powerful and often overlooked solution for quick cash.

At Versant Funding, we understand the specific financial pressures manufacturers endure. That’s why we specialize in providing tailored factoring services designed to get you the capital you need, when you need it. Our latest video, which you can watch above, highlights how factoring can be a game-changer for your business.

What is Factoring, and Why is it Perfect for Manufacturers?

Simply put, factoring allows you to sell your accounts receivable (invoices) to a third party (the factor) at a small discount in exchange for immediate cash. Instead of waiting 30, 60, or even 90 days for your customers to pay, you get the funds right away.

For manufacturers, this means:

Quick Cash Flow: No more cash flow gaps hindering your production or growth initiatives. Get funds in as quick as a week!

Significant Funding: We offer funding from $100,000 to $30 Million, providing substantial support whether you’re a growing mid-sized company or a large enterprise.

Non-Recourse Factoring: This is a crucial benefit for manufacturers. With non-recourse factoring, if your customer fails to pay due to bankruptcy or insolvency, you’re typically not responsible for repaying the advance. This transfers the credit risk away from your balance sheet.

Flexible Terms: We work with you to create terms that fit your unique business model and cash flow requirements.

Ideal for “Tough-to-Finance” Businesses: Traditional bank loans can be hard to secure, especially for newer companies, those with limited collateral, or those experiencing rapid growth. Factoring focuses on the quality of your accounts receivable, making it an accessible option when other avenues are closed.

How Manufacturers Benefit from Factoring:

Imagine being able to:

Purchase Raw Materials: Take advantage of bulk discounts or secure critical components without delay.

Meet Payroll: Ensure your skilled workforce is paid on time, every time.

Invest in New Equipment: Upgrade machinery or expand your production lines to increase efficiency and capacity.

Handle Large Orders: Don’t turn away big opportunities because of insufficient working capital.

Improve Credit Standing: Use the immediate cash to pay suppliers promptly, potentially earning early payment discounts and strengthening your vendor relationships.

Why?

We pride ourselves on being more than just a capital provider. We are your partner in growth. I am dedicated to understanding the intricacies of the manufacturing sector and crafting financial solutions that truly work.

Ready to unlock the potential of your accounts receivable?

To see how factoring can transform your manufacturing business reach out to Chris Lehnes today for a no-obligation consultation.

The 2026 Growth Gap: How Accounts Receivable Factoring Fuels Small Business Success

Factoring: Quick Cash to Kick Off the Year: As we move through 2026, the economic landscape for small businesses is defined by a paradox: opportunity is everywhere, but cash is moving slower than ever. While sectors like high-tech manufacturing and professional services are seeing a resurgence, many entrepreneurs find themselves “asset rich but cash poor.”

You’ve landed the big contract, your team is working overtime, and your sales are climbing. Yet, your bank account doesn’t reflect that success because your capital is trapped in Accounts Receivable (AR). If you’re waiting 30, 60, or even 90 days for clients to pay their invoices, you aren’t just waiting for money—you’re waiting to grow.

This is where Accounts Receivable Factoring becomes a strategic engine for your business.

What is AR Factoring in 2026?

Accounts receivable factoring (or invoice factoring) is not a loan. It is the sale of your outstanding invoices to a third party (a “factor”) at a slight discount in exchange for immediate liquidity.

In 2026, the process has been revolutionized by fintech integrations. Most modern factoring platforms now sync directly with your accounting software (like QuickBooks or Xero), allowing for “one-click” funding that can land in your account within 24 hours.

Why Factoring is the “Secret Weapon” for 2026

While traditional bank loans focus on your credit score and years of profitability, factoring focuses on the creditworthiness of your customers. This makes it an ideal solution for:

Rapidly Growing Startups: When sales outpace your cash reserves.

Seasonal Businesses: Managing the “lumpy” cash flow of peak seasons.

Service Providers: Staffing agencies or consultants who must pay employees weekly but get paid by clients monthly.

3 Ways Factoring Helps You Thrive This Year

1. Turn “Net-90” into “Right Now”

The most significant barrier to growth in 2026 is the “Cash Gap.” If you have $100,000 in open invoices, that’s $100,000 you can’t use to buy inventory, hire talent, or pay for digital marketing. Factoring unlocks up to 90-95% of that value immediately, giving you the agility to say “yes” to new opportunities without checking your balance first.

2. Fuel Expansion Without Adding Debt

In an era of “snagflation”—where mild inflation persists alongside a shifting labor market—loading your balance sheet with high-interest debt can be risky. Because factoring is a purchase of assets, it doesn’t show up as a loan. You are simply accelerating the arrival of money you’ve already earned.

3. Outsourced Credit & Collections

Modern factoring companies do more than just provide cash. They often act as your back-office credit department. In 2026, where business bankruptcies are slightly on the rise, having a partner who vets the credit risk of your potential clients is a massive competitive advantage. They handle the collections, freeing you up to focus on your product.

Is it Right for You?

To help you decide, here is a quick comparison of how factoring stacks up against traditional financing in today’s market:

Feature

AR Factoring

Traditional Bank Loan

Speed

24–48 Hours

3–6 Weeks

Approval Basis

Customer’s Credit

Your Credit & Collateral

Debt

None (Asset Sale)

Increases Liabilities

Flexibility

Scales with Sales

Fixed Credit Limit

Cost

1%–5% Service Fee

Interest Rate + Fees

Final Thoughts: Don’t Let Your Invoices Hold You Back

In 2026, the winners won’t necessarily be the companies with the biggest ideas, but those with the highest liquidity. AR factoring provides a bridge over the cash flow gaps that sink 82% of small businesses. It turns your hard work into immediate fuel.

In“Stolen Focus”, author Johann Hari investigates the modern erosion of human attention through personal anecdotes and scientific research. He argues that our inability to focus is not a personal failure of willpower but a result of systemic environmental factors, including the rise of surveillance capitalism and addictive technology. The text highlights how digital platforms use algorithms to maximize screen time, which disrupts our flow states and capacity for deep thought. Hari describes his own digital detox in Provincetown to illustrate that individual isolation is an insufficient long-term solution to a global crisis. Ultimately, the book calls for an “Attention Rebellion” to reclaim our minds from corporate and structural forces that prioritize speed over depth. Through interviews with experts, he explores how better sleep, nutrition, and play are essential to restoring our collective focus.

Briefing Document: The Crisis of Stolen Focus

Executive Summary

This document synthesizes key findings on the contemporary crisis of attention, arguing that the pervasive decline in our ability to focus is not an individual failing but a systemic problem driven by powerful technological, social, and economic forces. Decades of research and expert testimony indicate that our environment is being systematically engineered to degrade focus for profit and productivity, a reality that necessitates a collective, structural response rather than isolated individual efforts.

Key Takeaways:

Systemic, Not Personal, Failure: The collapsing ability to pay attention is not primarily due to personal laziness or a lack of willpower. It is a societal issue caused by powerful forces—from Big Tech to broader economic pressures—that are actively “pouring acid on your attention every day.”

The Architecture of Distraction: The dominant business model of major technology platforms, “surveillance capitalism,” is fundamentally designed to capture and sell human attention. This model incentivizes the creation of features like infinite scroll and outrage-fueling algorithms that maximize screen time by hijacking psychological vulnerabilities, leading to a state of constant distraction and heightened societal anger.

Erosion of Deep Thinking: The crisis extends beyond simple distraction. Foundational states for deep thought are being systematically crippled. These include “flow states” (deep, effortless immersion), the cognitive patience fostered by deep reading, and the creative consolidation that occurs during mind-wandering—all of which are suppressed by an environment of constant switching and stimulation.

The Fallacy of “Cruel Optimism”: Solutions that focus exclusively on individual willpower—such as digital detoxes or self-help techniques—are a form of “cruel optimism.” They offer inadequate, small-scale answers to vast, systemic problems, effectively blaming the victim. This is analogous to responding to the obesity crisis with diet books alone while ignoring the toxic food environment that drives it.

A Call for an “Attention Rebellion”: Addressing the crisis requires a collective social and political movement. The path forward involves systemic changes, including the regulation of technology companies to ban surveillance capitalism, a widespread shift to a four-day work week to combat exhaustion, and a fundamental rethinking of a culture predicated on ever-increasing speed and growth.

I. The Nature of the Attention Crisis

The degradation of focus is a tangible, measurable phenomenon impacting individuals and societies. It manifests in the struggle to be present in one’s own life, as illustrated by a trip to Graceland where visitors, including the author’s godson, experienced the iconic location primarily through the mediated reality of iPads and smartphones rather than direct observation. This personal experience is a microcosm of a larger, scientifically documented trend.

A. Scientific Evidence of Shrinking Attention

A landmark study led by scientist Sune Lehmann at the Technical University of Denmark analyzed data from the 1880s to the present, including Google Books, Twitter, and movie ticket sales.

Key Finding: The research provides the first major scientific proof that collective attention spans have been shrinking for over 130 years. Topics now rise to peak popularity and fade from public discussion at an ever-accelerating rate.

Primary Cause: While the internet has dramatically accelerated this trend, the root cause is a continuous increase in the volume and speed of information. As Lehmann’s model demonstrates, “The more information you pump in, the less time people can focus on any individual piece of it.”

Consequence: The sacrifice for this speed is depth. As Sune Lehmann states, “Depth takes time. And depth takes reflection… All of these things that require depth are suffering. It’s pulling us more and more up onto the surface.”

B. A Systemic Problem, Not an Individual Failing

The prevailing narrative of self-blame—attributing distraction to laziness or lack of discipline—is a profound misunderstanding of the issue. The source context argues that this is a systemic problem being actively perpetrated.

An “Attentional Pathogenic Culture”: Experts believe society is creating an environment where sustained focus is exceptionally difficult, forcing individuals to “swim upstream to achieve it.”

An expert, when asked how one might design a society to ruin people’s attention, replied, “Probably about what our society is doing.”

The Core Argument: The document posits that there are twelve deep forces damaging attention, driven by powerful entities including, but not limited to, Big Tech. The central thesis is that “you are living in a system that is pouring acid on your attention every day, and then you are being told to blame yourself and to fiddle with your own habits while the world’s attention burns.”

II. Key Drivers of Attention Degradation

The crisis is multifaceted, stemming from a confluence of technological, physiological, and environmental factors that have fundamentally altered how we live, work, and think.

A. The Architecture of Distraction: Technology’s Business Model

The design of modern digital technology is a primary cause of attention degradation, driven by a business model known as surveillance capitalism. Former Silicon Valley insiders like Tristan Harris (ex-Google) and Aza Raskin (inventor of infinite scroll) provide a detailed critique.

The Business Model: Social media companies profit not just from showing advertisements, but from collecting vast amounts of user data to create predictive models. These models are then sold to advertisers who wish to influence behavior. This economic model has a single imperative: maximize user screen time to gather more data.

Designed for Addiction: To achieve maximum screen time, platforms are built using principles from B.F. Skinner’s behavioral psychology, creating “a craving” in users. Techniques include:

Infinite Scroll: Designed by Aza Raskin, this feature removes natural stopping points, encouraging continuous, mindless consumption. Raskin estimates it makes users spend 50% more time on sites.

Variable Reinforcements: The unpredictable delivery of “likes” and notifications operates like a slot machine, creating a compulsive need to check for rewards.

Task Switching: Notifications are designed to constantly pull users away from other tasks, incurring a “switch cost effect” that slows thinking, increases errors, reduces creativity, and impairs memory.

Algorithms of Outrage: To keep users engaged, algorithms on platforms like YouTube and Facebook have learned that shocking, anger-inducing, and extreme content is most effective.

The YouTube Effect: Former YouTube engineer Guillaume Chaslot revealed that the algorithm systematically recommends increasingly extreme content. Watching a factual video about the Holocaust could lead to Holocaust-denial content within five videos.

Political Consequences: This dynamic has profound real-world impacts, contributing to political polarization and radicalization. In Brazil, Jair Bolsonaro’s rise was fueled by social media algorithms promoting his outrageous content, leading his supporters to chant “Facebook! Facebook!” upon his victory.

B. The Erosion of Foundational States for Focus

Beyond active distraction, the modern environment systematically undermines the mental states essential for deep thinking and well-being.

Flow States: Researched by psychologist Mihaly Csikszentmihalyi, “flow” is the deepest form of human focus, achieved when one is fully absorbed in a single, meaningful task at the edge of one’s abilities. Multitasking and constant interruption are antithetical to flow. Starved of flow, we become “stumps of ourselves, sensing somewhere what we might have been.”

Deep Reading: The decline in sustained reading of physical books represents a major loss of a common flow state.

Comprehension: Studies show that reading on screens leads to lower comprehension compared to reading on paper. The gap for elementary school children is equivalent to two-thirds of a year’s growth.

Empathy: Research by Professor Raymond Mar shows that reading fiction functions as an “empathy gym.” By simulating the inner lives of others, it measurably improves a reader’s ability to understand real-world emotions. This effect is not found with non-fiction or the fragmented narratives of social media.

Mind-Wandering: Far from being a waste of time, mind-wandering is an essential brain state (the “default mode network”) critical for consolidating memories, making new connections, and long-term planning. Constant digital stimulation suppresses this state, degrading the quality of our thinking.

C. Physiological and Environmental Assaults on Attention

Our ability to focus is also under direct physiological attack from changes in our lifestyles and physical environment.

Factor

Description of Impact

Sleep Deprivation

Chronic sleep loss has severe cognitive effects. Staying awake for 18 hours impairs reaction time to a level equivalent to 0.05% blood alcohol. The prefrontal cortex, crucial for judgment, is particularly sensitive. This is exacerbated by evening exposure to blue light from screens, which disrupts sleep-regulating hormones.

Stress & Hypervigilance

As demonstrated by Dr. Nadine Burke Harris, Surgeon General of California, stress and trauma (especially in childhood) trigger a state of hypervigilance. The brain becomes wired to constantly scan for threats, making deep, calm focus impossible. This is often misdiagnosed as ADHD.

Overwork & Exhaustion

Working hours have steadily increased, leading to widespread exhaustion. An experiment at Perpetual Guardian in New Zealand, led by CEO Andrew Barnes, proved that a four-day work week (for the same pay) led to a 35% decrease in off-task social media use, a 15% drop in stress, and an overall increase in productivity.

Diet & Pollution

A growing body of evidence suggests that modern diets high in processed foods and exposure to environmental pollutants (such as lead, BPA, and other industrial chemicals) directly harm brain function and focus. Professor Barbara Demeneix states, “there is no way we can have a normal brain today” due to this constant chemical exposure.

D. The Transformation of Childhood and the Rise of ADHD

Children’s attention problems are escalating dramatically, a trend that cannot be explained by biology alone. The very nature of childhood has been radically altered in ways that undermine the development of focus.

The Collapse of Free Play: Unsupervised, unstructured play has been nearly eliminated from children’s lives, replaced by homework (up 145% between 1981-1997), screens, and adult-supervised activities.

The Importance of Play: Free play is “the primary technology for learning.” It is where children learn negotiation, problem-solving, emotional regulation, and how to pursue their own intrinsic motivations—the internal drive to do things for their own sake, which is the foundation of sustained attention.

An Environmental Mismatch: Drawing an analogy from veterinary science, the text suggests children are like zoo animals. When a horse is confined to a stall, it develops compulsive behaviors because its “frustrated biological objectives” (the need to run and graze) are denied. Similarly, children are being raised in environments that thwart their innate needs for play and autonomy, leading to behaviors labeled as ADHD.

III. The Fallacy of Individual Solutions and “Cruel Optimism”

The dominant cultural response to the attention crisis is to advocate for individual self-discipline. This approach, while well-intentioned, is fundamentally flawed and represents a form of “cruel optimism.”

The Provincetown Experiment: The author’s three-month digital detox in Provincetown demonstrated the profound benefits of disconnecting—a recovery of flow, deep reading, and calm. However, it also highlighted the limitations of this approach: it is a privilege few can afford, and the return to the normal environment quickly eroded the gains.

The “Indistractible” Argument: This viewpoint, championed by tech designer Nir Eyal (author of Hooked), posits that distraction is caused by “internal triggers” and can be managed through personal life-hacks.

The Obesity Analogy: This individual-centric view is compared to the failed response to the obesity crisis. For decades, the culture blamed individuals for being overweight and sold them diet books. This failed because the root problem was a systemic change in the food environment. Similarly, digital diet books will not solve the attention crisis.

Authentic Optimism: The alternative is to collectively address the underlying causes of the problem. Instead of shaming individuals, the focus must shift to changing the toxic environment that is degrading everyone’s attention.

IV. A Path Forward: Systemic Change and the “Attention Rebellion”

Reclaiming focus requires a collective fight to change the systems that are stealing it. This involves a multi-pronged strategy aimed at reforming technology, work culture, and ultimately, our societal values.

A. Reforming Technology

The business model of surveillance capitalism must be dismantled.

Ban the Current Model: Regulation is needed to make the current “track and manipulate” business model illegal.

Shift to New Models: Alternatives include subscription-based services (where the user is the customer, not the product) or treating major platforms as public utilities.

Redesign for Human Values: Once financial incentives are realigned, technology can be redesigned to serve human intentions, not to capture attention. Simple changes could include:

Batching notifications into a single daily update.

Designing platforms to facilitate real-world meetups.

B. Reclaiming Time and Rest

Structural changes are necessary to combat the culture of exhaustion.

The Four-Day Work Week: Widespread adoption of a shorter work week has been proven to increase focus, reduce stress, and maintain or even boost productivity.

The Fight for Time: Historically, gains like the weekend were not given freely by employers; they were won through decades of organized labor campaigns. A similar fight will be required to reclaim more time for rest and reflection.

C. Building a Movement: The Attention Rebellion

Individual action is insufficient; a broad-based social movement is required to force systemic change.

Historical Precedent: The women’s rights movement and the successful campaign to ban leaded gasoline demonstrate that organized citizens can defeat powerful interests.

“Site Battles”: Activist Ben Stewart suggests the movement can gain momentum through “site battles”—dramatic, nonviolent confrontations at symbolic locations (e.g., Facebook HQ) to raise public consciousness about the crisis.

The Goal: The movement’s aim is “personal liberation—liberating ourselves from people who are controlling our minds without our consent.”

The Ultimate Challenge: In the long term, a sustainable solution will require challenging the core logic of an economy built on perpetual growth, which fuels the relentless demand for more speed, more consumption, and ultimately, less attention. As Dr. Charles Czeisler notes, “our economic system has become dependent on sleep-depriving people. The attentional failures are just roadkill. That’s just the cost of doing business.”