2025 GDP Downward Revision

The final numbers for 2025 are in, and there has been a GDP Downward Revision… they’ve arrived with a bit of a chill. On March 13, 2026, the Bureau of Economic Analysis (BEA) released its second estimate for the fourth quarter of 2025, significantly revising real GDP growth downward to an annualized rate of 0.7%.

This is a sharp departure from the initial “advance” estimate of 1.4% and a massive deceleration from the robust 4.4% growth seen in the third quarter. For the full year, the U.S. economy grew by 2.1%, a slight dip from previous projections.

So, what happened at the end of the year to take the wind out of the economy’s sails?

The Culprits: Shutdowns, Slumps, and Spending

Several factors converged in late 2025 to create this “soft landing” that felt a little more like a bump.

- The 43-Day Government Shutdown: The most visible drag was the historic federal government shutdown that spanned October and November. While essential services remained, the lack of federal paychecks and halted government contracts took a measurable bite out of domestic demand.

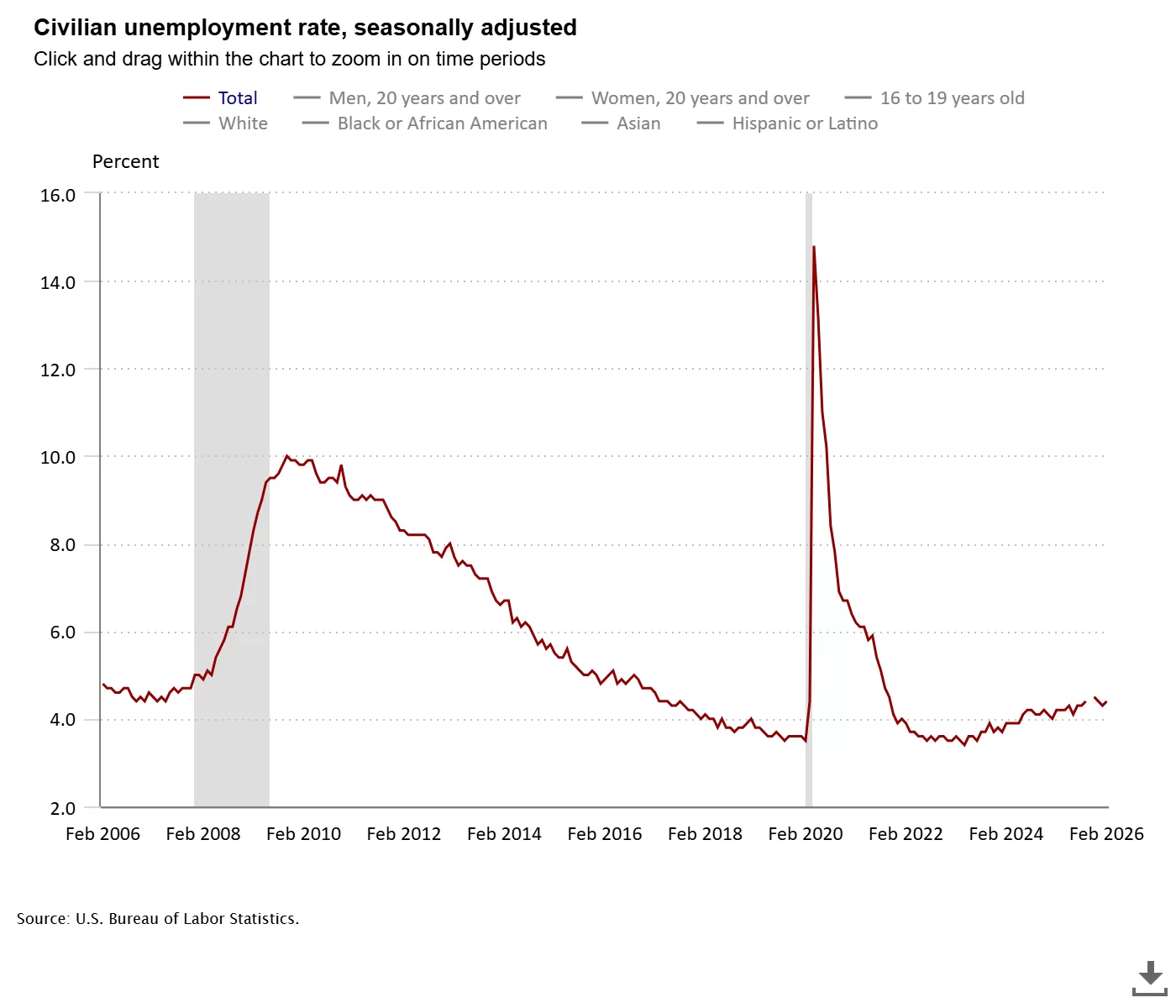

- A “Low-Hire” Labor Market: While mass layoffs weren’t the headline, a “low-hire, low-fire” environment took hold. Monthly job gains slowed to a crawl, and the unemployment rate ticked up to 4.6% by November, making consumers more cautious with their wallets.

- The Trade Drag: Exports were revised downward as global demand softened, and a “front-loading” effect—where companies rushed to import goods earlier in the year to avoid new tariffs—faded out, leaving a gap in activity for the final months.

- Sticky Inflation: Despite the slower growth, the PCE price index (the Fed’s favorite inflation gauge) remained at 2.9%. This combination of stagnant growth and persistent inflation has put the Federal Reserve in a difficult “wait-and-see” position.

Silver Linings in the Data

It’s not all doom and gloom. Even with the downward revision, there are signs of underlying resilience:

- Investment is Picking Up: While consumer spending moderated, business investment—particularly in AI infrastructure—actually accelerated in Q4, acting as a critical floor for the economy.

- Market Resilience: Interestingly, Wall Street took the news in stride. Markets actually rallied following the release, as investors bet that the soft GDP data would finally force the Federal Reserve to consider more aggressive rate cuts later in 2026.

- Recouping the Loss: Economists expect much of the “lost” output from the government shutdown to be recovered in the first half of 2026 as backlogged projects and federal spending finally hit the books.

What’s Next for 2026?

The downward revision confirms that the “Goldilocks” era of high growth and falling inflation has hit a snag. Most forecasters, including the IMF and S&P Global, now project a steady but modest growth rate of around 1.8% to 2.0% for 2026.

The big question remains the Federal Reserve. With growth at 0.7% but inflation still above their 2% target, the path to interest rate cuts remains narrow. For now, the “wait-and-see” approach is the only game in town.

1. The Tech Sector: From Growth to Efficiency

While the broader economy slowed, Tech remained a relative fortress, but the “flavor” of investment is changing.

- AI Infrastructure as a Life Raft: Business investment in “Intellectual Property Products” (tech speak for software and AI R&D) was one of the few areas that actually accelerated in Q4 2025. Companies are doubling down on AI to find the efficiencies they need to survive a low-growth environment.

- The “Low-Hire” Reality: Expect the “low-hire” trend to persist in Silicon Valley. With GDP growth revised downward, tech giants are focusing on “AI-driven productivity” rather than aggressive headcount expansion.

- Valuation Pressure: While the stock market has been resilient, persistent 2.9% inflation means the Federal Reserve isn’t in a rush to slash rates. High-growth tech stocks are sensitive to interest rates; if those rates stay “higher for longer,” we may see more volatility in tech valuations throughout 2026.

2. The Real Estate Market: A Tale of Two Interests

The GDP Downward Revision has created a paradoxical situation for housing.

- Mortgage Rate Relief? Traditionally, weak GDP data pushes bond yields down, which can lower mortgage rates. Many analysts now expect the 30-year fixed rate to drift toward 6.0%–6.2% in 2026. This could finally “unlock” homeowners who have been trapped by high rates.

- The “Sentiment” Gap: The revision highlights a cooling labor market (unemployment at 4.6%). Even if mortgage rates drop, buyer “jitters” may keep the market from exploding. J.P. Morgan research suggests national home prices may stall at 0% growth in 2026 as demand and supply reach a fragile equilibrium.

- Commercial Real Estate (CRE) Stress: The 0.7% GDP print is toughest on office and retail CRE. Slower economic activity means less demand for physical space, likely leading to more “strategic defaults” or building repurposing projects in 2026.

The Federal Reserve’s “Tightrope”

The GDP Downward Revision puts the Fed in a bind. Usually, 0.7% growth would trigger an immediate rate cut to “save” the economy. However, with inflation still at 2.9%, they risk reigniting price hikes if they move too fast.

The Bottom Line: 2026 will be the year of the “Efficiency Play.” Whether you are a tech firm or a homebuyer, the goal is no longer “growth at any cost,” but rather finding value in a slower, more deliberate economic landscape.

Contact Factoring Specialist Chris Lehnes

Headline: 📉 GDP Revised to 0.7%: What it means for Tech & Real Estate in 2026.

The “Second Estimate” for Q4 2025 is out, and the numbers confirm a significant cooling of the U.S. economy. Real GDP growth was revised down to an annualized 0.7%—a sharp drop from the earlier 1.4% estimate.

While the 43-day government shutdown in late 2025 played a major role, the ripple effects for 2026 are already taking shape:

💻 TECH: The era of “growth at any cost” is officially over. We’re seeing a pivot toward Efficiency Tech. While broader spending is cooling, investment in AI infrastructure is accelerating as companies scramble to automate their way out of a low-growth environment.

🏠 REAL ESTATE: It’s a paradox. Slower growth usually means lower mortgage rates, and we’re already seeing 30-year fixed rates dip toward 6.0%. However, with unemployment ticking up to 4.6%, buyer “jitters” are real. J.P. Morgan predicts a 0% national price growth for 2026—a true flatline.

⚖️ THE FED: Chair Jerome Powell and the FOMC are walking a tightrope. With inflation still “sticky” at 2.4%–2.9%, they can’t rush to cut rates despite the sub-1% growth.

The Bottom Line: 2026 will reward the “Lean and Leaner.” Whether you’re managing a portfolio or a product roadmap, efficiency is the new growth.

#Economy2026 #GDP #TechTrends #RealEstate #FederalReserve #Investing

🧵 X (Twitter): The Fast-Action Thread

Target Audience: Market Watchers and News Junkies

1/ 🚨 BREAKING: U.S. Q4 2025 GDP revised DOWN to 0.7% (from 1.4%). The 2025 “Cold Snap” is official. Here’s the 30-second breakdown of what this means for your wallet in 2026. 🧵👇

2/ Why the drop? The 43-day government shutdown was a massive anchor, but we also saw a deceleration in consumer spending and exports. The economy didn’t crash, but it definitely pulled the emergency brake. 🛑

3/ 💻 TECH IMPACT: Silicon Valley is staying “Low-Hire.” With 0.7% growth, companies are prioritizing AI-driven productivity over expansion. If it doesn’t automate a process or save a dollar, it’s not getting funded this year.

4/ 🏠 HOUSING IMPACT: Good news? Mortgage rates are sliding toward 5.8%–6.0%. Bad news? A weaker labor market means fewer people are ready to jump. Expect a “sideways” year for home prices. 📉➡️

5/ 🏦 FED WATCH: All eyes on the March 18 FOMC meeting. The market was hoping for cuts, but with inflation at 2.4%, the Fed might stay “Higher for Longer” to ensure the fire is out.

6/ Summary: 2026 is the year of the “Efficiency Play.” Growth is slow, money is still relatively expensive, and AI is the only engine still revving. Stay nimble. #GDP #Economy #Inflation

📸 Instagram/Threads: The Visual Summary

Caption:

The numbers are in: The U.S. economy hit a “speed bump” at the end of 2025. 📉 GDP growth was just revised down to 0.7%.

What this means for you: ✅ Mortgage Rates: Might actually get a bit friendlier (seeing 5.8% – 6% averages). ✅ Tech: More AI tools, fewer new job postings. Efficiency is 👑. ✅ Inflation: Still hanging around 2.4%, keeping the Fed on high alert.

It’s not a recession—it’s a recalibration. 2026 is about playing the long game. ♟️

#MoneyMatters #EconomyNews #2026Forecast #RealEstateTips #TechNews